Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 96.24 Billion |

| Market Size (2031) | USD 134.85 Billion |

| Growth Rate (2026 - 2031) | 6.98% CAGR |

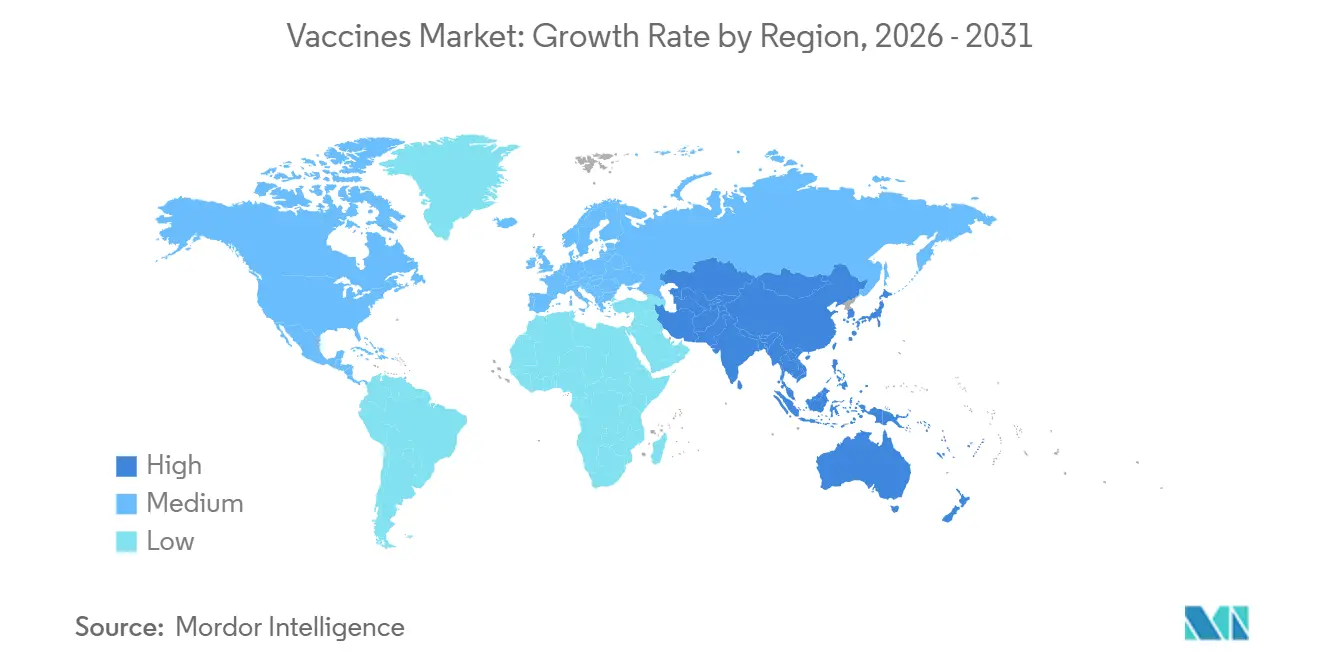

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

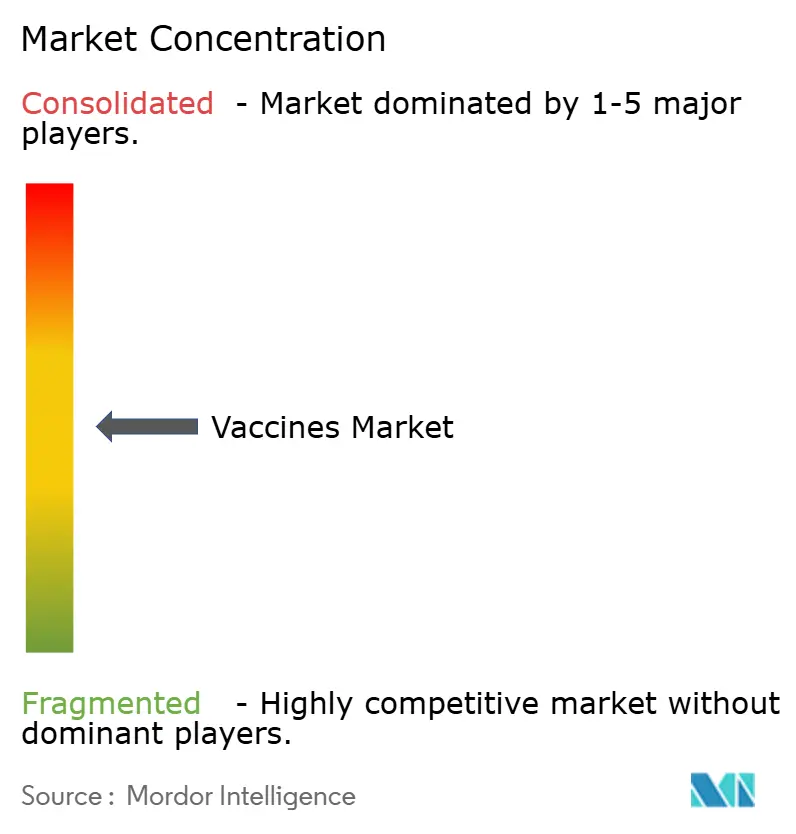

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Vaccines Market Analysis by Mordor Intelligence

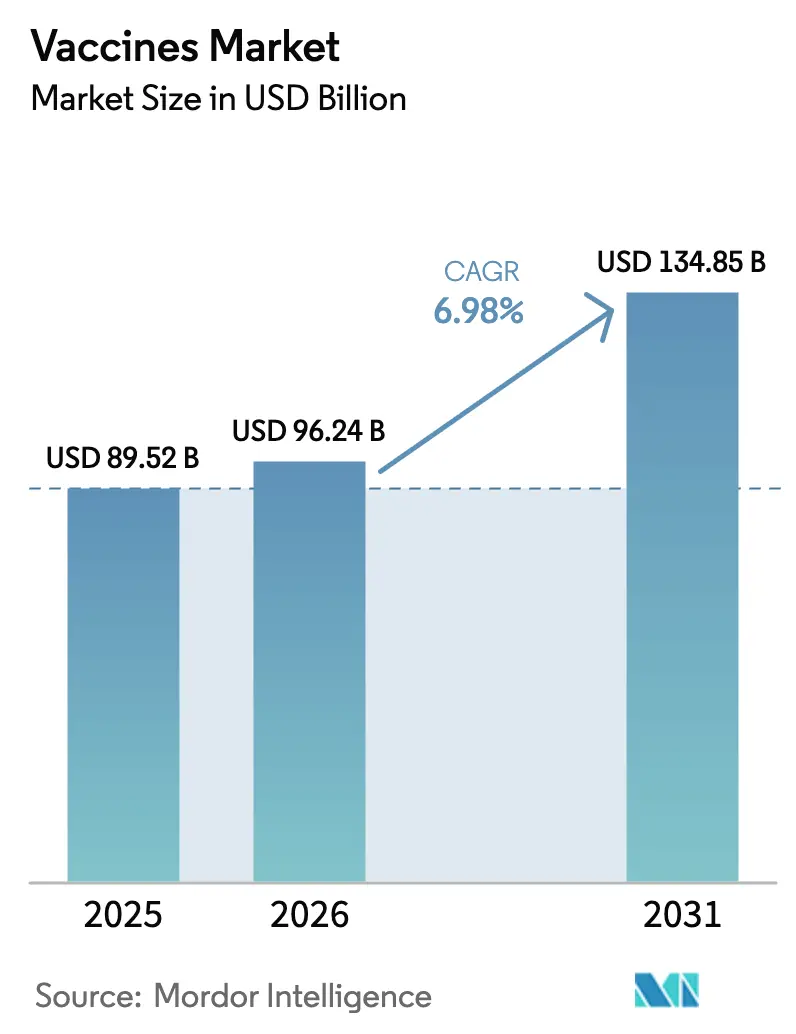

The Vaccines Market size is expected to grow from USD 89.52 billion in 2025 to USD 96.24 billion in 2026 and is forecast to reach USD 134.85 billion by 2031 at 6.98% CAGR over 2026-2031.

Elevated demand for adult and geriatric immunization, accelerated platform repurposing of mRNA facilities, and catch-up drives in low- and middle-income countries (LMICs) underpin this growth trajectory. RSV and shingles launches are expanding the revenue base beyond pediatric schedules, while Gavi’s refreshed funding pool guarantees multi-year procurement visibility across 57 LMICs. Supply-side momentum is equally strong: Indian and Chinese manufacturers brought 800 million incremental doses online in 2024, and CDMO consolidation is tightening fill-finish availability, nudging large sponsors toward vertical integration. Cold-chain gaps and vaccine hesitancy remain structural constraints; however, advances in technology, such as micro-array patches, AI-guided antigen design, and self-amplifying RNA, offer cost and speed advantages that offset those headwinds.

Key Report Takeaways

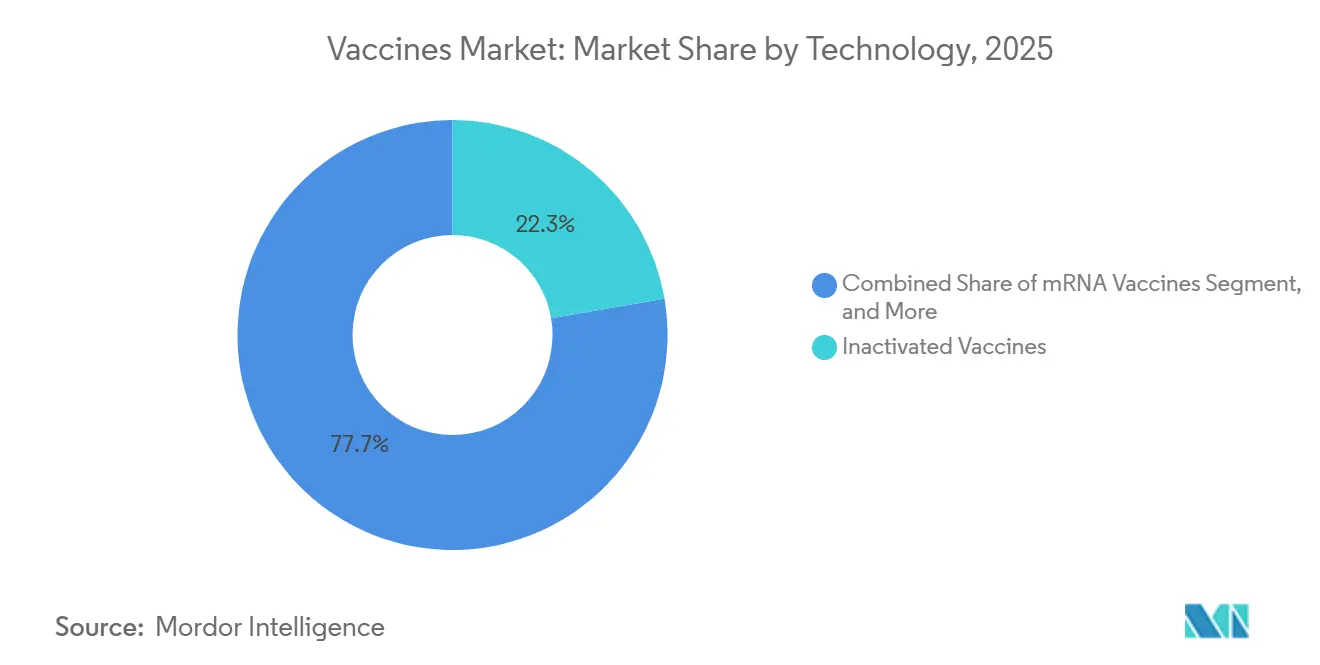

- By technology, inactivated vaccines captured 22.31% of the vaccine market share in 2025; mRNA platforms are projected to grow at a 9.87% CAGR through 2031.

- By vaccine type, multivalent formulations accounted for 66.73% of the vaccine market share in 2025 and are expected to advance at a 10.51% CAGR through 2031.

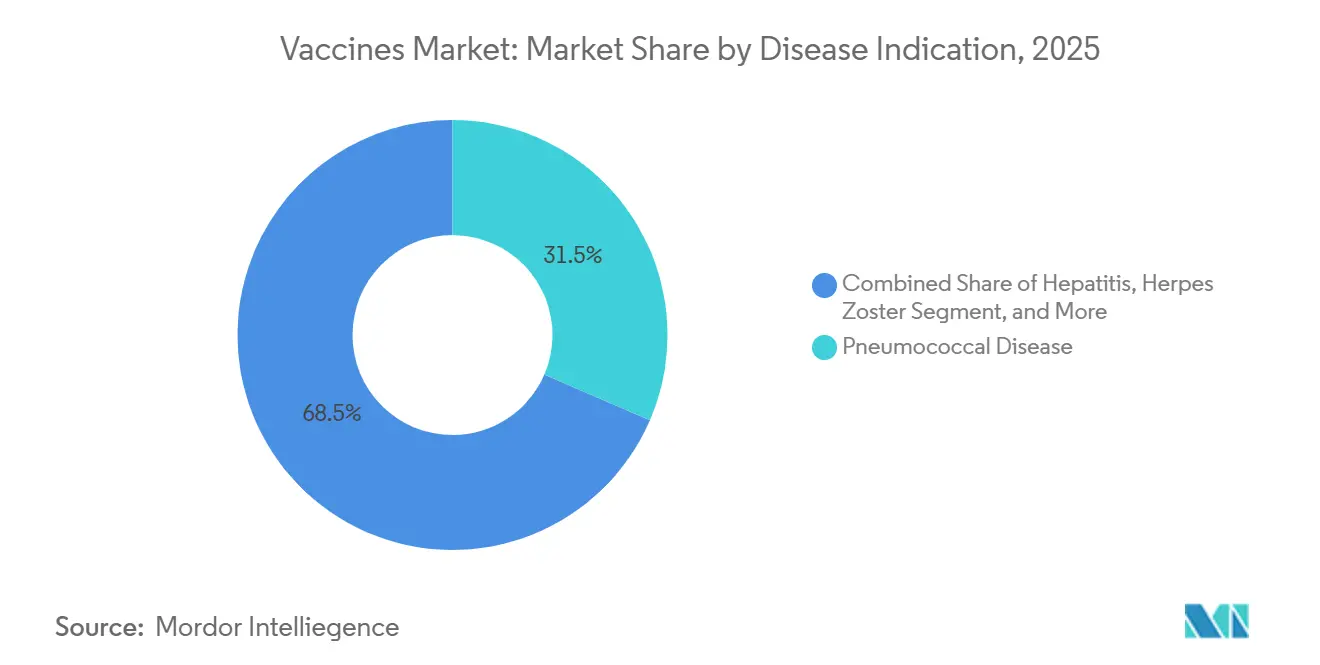

- By disease indication, pneumococcal vaccines led the vaccine market share with 31.48% in 2025, while RSV vaccines are expected to expand at an 8.63% CAGR through 2031.

- By route of administration, parenteral administration retained a 44.46% share of overall delivery routes in 2025 and represents the fastest-expanding method, with a 12.45% CAGR to 2031.

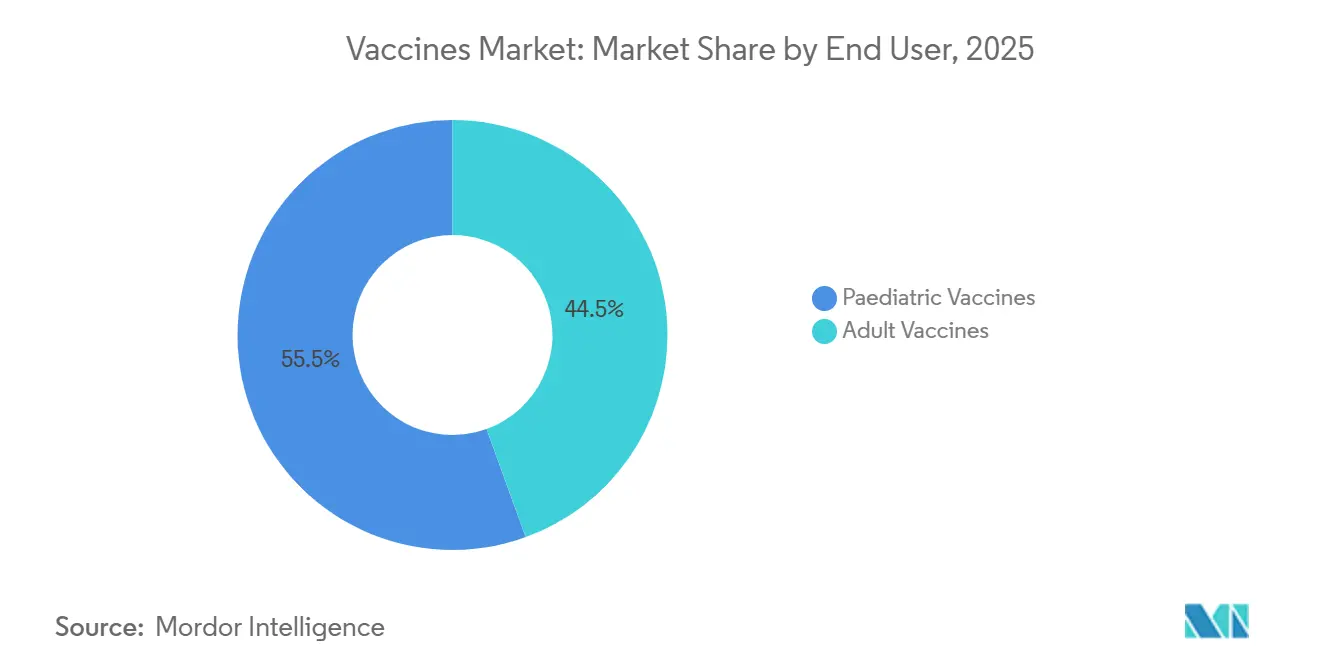

- By end user, the pediatric cohort accounted for 55.54% of the vaccine market share in 2025, whereas adult immunization is projected to grow at an 11.31% CAGR through 2031.

- By geography, North America accounted for the largest regional contribution, representing 39.26% of the vaccine market size in 2025; the Asia-Pacific region is poised for an 8.96% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| COVID-19 Platform Acceleration | +1.2% | Global, with highest impact in North America, Europe, and advanced APAC markets | Short term (≤ 2 years) |

| Routine Immunisation Catch-Up Programmes Post-Pandemic | +0.9% | Global, concentrated in Sub-Saharan Africa, South Asia, and Latin America | Short term (≤ 2 years) |

| Growing Adult & Geriatric Vaccination Mandates | +2.1% | North America, Europe, Japan, South Korea, Australia | Medium term (2-4 years) |

| Government-Funded National Immunisation Plans in LMICs | +1.5% | LMIC regions, APAC core, Sub-Saharan Africa, spill-over to Latin America | Long term (≥ 4 years) |

| Needle-Free Micro-Array Patches Entering Phase III | +0.7% | Global, early adoption in Australia, Singapore, tropical LMIC markets | Long term (≥ 4 years) |

| AI-Optimised Antigen Design Reducing Time-To-Market | +0.5% | Global, led by North America and Europe with technology transfer to APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

COVID-19 Platform Acceleration and Routine Immunization Catch-Up

The mRNA infrastructure built during the pandemic now halves the development cycles for new antigens; Moderna’s mRNA-1345 RSV candidate reached FDA authorization just 18 months after the initiation of its pivotal trial. BioNTech’s Phase II trivalent flu-COVID-RSV booster aims to replace three separate shots for adults over 50, reflecting cost-containment and compliance benefits. Concurrently, 67 million children missed at least one basic dose between 2020 and 2023, prompting governments to deploy supplementary outreach efforts. India’s Mission Indradhanush 5.0 mobilized 120,000 GPS-tracked vans to vaccinate 9.8 million under-immunized children in 2025.[1]Ministry of Health and Family Welfare, India, “Mission Indradhanush 5.0,” mohfw.gov.in The Serum Institute responded by scaling up its pentavalent output, reporting a 34% year-on-year volume increase that same year.

Growing Adult and Geriatric Vaccination Mandates

Japan’s revised Preventive Vaccination Act requires pneumococcal and shingles coverage for citizens aged 65 and above, adding 15 million annual doses and subsidizing 70% of the end-user cost. The U.S. CDC endorsed RSV vaccination for adults over 60 in June 2024, and Pfizer forecasts USD 2 billion in domestic RSV revenue by 2027. South Korea mirrors the model, covering 80% of senior vaccine costs through its National Health Insurance Service. Economic data support the policy: preventing a single RSV hospitalization in seniors yields approximately USD 12,000 in direct health-system savings, according to a 2024 Lancet study.

Government-Funded National Immunization Plans in LMICs

Gavi’s 2025 replenishment unlocked USD 9 billion, earmarked for 1.2 billion doses across 57 countries, with a heavy skew toward PCV and rotavirus procurement. Nigeria and Bangladesh introduced PCV13 and rotavirus vaccines in early 2025, respectively, following delays attributed to pandemic-related supply shortages.[2]UNICEF, “Cold-Chain Capacity Assessment 2024,” unicef.org Tiered pricing remains acute: The Serum Institute supplies PCV to Gavi at USD 2.15 per dose, versus USD 150 in the United States, underscoring a sharply bifurcated economics.[3]Serum Institute of India, “Pentavalent Vaccine Supply to Gavi,” seruminstitute.com China’s Belt and Road Initiative has added a USD 200 million fill-finish plant in Nairobi, capable of producing 50 million inactivated polio and hepatitis B doses annually. Yet donor reliance persists: 18 of 42 LMIC immunization budgets remain more than 60% dependent on external funding, according to a 2025 Global Fund audit.

Needle-Free Micro-Array Patches and AI-Optimized Antigen Design

Vaxxas advanced its high-density micro-array patch to Phase III in August 2025; the technology delivers antigens through 5,000 dissolving projections, eliminating both cold-chain and skilled-personnel barriers. If regulatory clearance follows, trial data suggest a 40% lower last-mile cost in tropical climates. Separately, Moderna’s February 2025 partnership with OpenAI utilizes large language models for epitope prediction, reducing pre-clinical work from 18 months to 6 months. A Nipah vaccine entered Phase I trials nine months after the WHO flagged an outbreak, exemplifying AI-accelerated responsiveness. GSK’s AI-curated TLR7/8 adjuvant boosted antibody titers in elderly volunteers by 60% compared with alum, as published in Nature Immunology in March 2025.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cold-Chain Bottlenecks in Remote Regions | -0.9% | Sub-Saharan Africa, South Asia, Latin America rural areas | Medium term (2-4 years) |

| Volatile Bulk Antigen Supply Pricing | -0.7% | Global, with acute impact on LMIC procurement | Short term (≤ 2 years) |

| Vaccine Hesitancy Driven by Social Media Disinformation | -1.1% | Europe, North America, pockets of APAC | Short term (≤ 2 years) |

| Concentration of Fill-Finish Capacity in CDMOs | -0.6% | Global, supply-chain chokepoint | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cold-Chain Bottlenecks and Volatile Bulk Antigen Supply Pricing

Only 22% of health facilities in sub-Saharan Africa are equipped with WHO-certified refrigeration, and outages lasting more than 8 hours occur monthly in 45% of rural clinics. India discarded 12% of the procured vaccine doses in 2024 due to temperature excursions, resulting in a loss of USD 87 million. Solar-powered units reduce waste by 30% but cost USD 5,000 each, which limits scalability. Antigen supply swings compound the issue: a fire at Bilthoven Biologicals erased 18% of the global inactivated poliovirus capacity, driving prices 42% higher between January 2024 and June 2025.

Vaccine Hesitancy and Concentration of Fill-Finish Capacity in CDMOs

Measles cases tripled in Europe between 2023 and 2025 after MMR uptake fell below the 95% herd-immunity threshold; 28% of surveyed parents cited online misinformation as a decisive factor. France now mandates MMR proof for preschool entry, pushing coverage from 89% to 94% within six months. Supply fragility also stems from CDMO concentration: Emergent BioSolutions and Catalent control ~40% of global aseptic lines. A 2024 FDA citation at Catalent’s Baltimore plant delayed Novavax deliveries by nine months, resulting in USD 300 million in lost revenue. Pfizer pre-empted similar risks by adding 200 million doses of annual mRNA fill-finish at its Kalamazoo site in October 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: mRNA Platforms Gain Share Despite Inactivated Vaccine Incumbency

Inactivated vaccines retained 22.31% of vaccines market share in 2025 due to established low-cost capacity in China and large-volume LMIC contracts. Yet, mRNA pipelines exhibit the highest velocity, with a 9.87% CAGR projected to 2031, as Moderna and BioNTech redeploy their COVID-19 infrastructure to seasonal boosters. The vaccine market size tied to conjugate technologies remains substantial, anchored by Pfizer’s Prevnar 20, which commands 60% of pneumococcal revenues. Live attenuated and recombinant vaccines face commoditization pressure from Indian biosimilars, which are priced 30% lower in Asia. Viral-vector platforms are relegated to adult segments after rare thrombotic events pushed European regulators to age-restricted labels. Hybrid-immunity data from a 2025 NEJM study showed four-fold antibody persistence when two inactivated doses were followed by an mRNA booster, prompting China to authorize heterologous regimens for 300 million eligible adults.

The medium-term outlook suggests that value, rather than volume, will dictate technology competition. SA RNA research, filed in nine Moderna patents between 2024 and 2025, promises a ten-fold dose reduction and a 60% manufacturing cost saving if trials validate current projections. Developers in LMICs are exploring enzyme-free RNA replication to bypass cold-chain constraints, illustrating how technology gaps and cost sensitivities continue to shape platform choices across buyer segments.

By Vaccine Type: Multivalent Formulations Dominate Pediatric Schedules

Multivalent products accounted for 66.73% of the global vaccines market in 2025 and are projected to grow at a rate of 10.51% per year through 2031, as health systems consolidate clinic touchpoints. Serum Institute’s pentavalent shot, priced at USD 1.85 for Gavi programs, displaced higher-priced European alternatives and captured 42% of LMIC orders in 2025. Quadrivalent flu formulations added 180 million doses in 2025 after the WHO downgraded trivalent formats that had missed B/Yamagata coverage for two consecutive seasons.

Monovalent adults launch a chip into pediatric dominance. Shingrix and Abrysvo command USD 280–295 per dose in the United States, funneling margin to the adult book despite lower unit volumes. Needle-free platforms may eventually favor multivalent patches, but regulatory clarity will be crucial; the FDA’s December 2025 draft left efficacy endpoints vague for non-injectable, multivalent delivery.

By Disease Indication: RSV Vaccines Emerge as Fastest-Growing Segment

Pneumococcal vaccines delivered 31.48% of 2025 revenue, but RSV is rising at an 8.63% CAGR as newly approved adult and maternal formulations unlock previously untapped demand. Medicare alone faces approximately USD 3 billion in annual RSV hospitalization costs, validating the payer's appetite for prevention. Bavarian Nordic’s European clearance for mResvia in March 2025 further intensifies competition. Meanwhile, HPV uptake surged after China added Gardasil 9 to its subsidized list in January 2025, leading to the immediate production of 30 million additional doses. Rotavirus programs experienced a setback when a 2024 contamination event at GSK’s Belgian site reduced supply by 25%, delaying African schedules, but resumed in mid-2025.

Emerging pathogens such as chikungunya and Nipah underscore the existence of niche opportunity pools. Valneva’s FDA approval for chikungunya in November 2024 secured a USD 80 million Brazilian contract within four months. Moderna’s Nipah candidate entered first-in-human dosing just nine months post-outbreak, signaling platform agility that could redefine how the vaccines market responds to localized epidemics.

By Route of Administration: Parenteral Dominance Faces Needle-Free Disruption

Parenteral delivery accounted for 44.46% of volumes in 2025 and is forecast to expand at a 12.45% CAGR, boosted by high-value adult RSV, pneumococcal, and shingles products. Auto-injectors and pre-filled syringes reduce staffing constraints; Pfizer’s one-step Prevnar 20 device cut administration time by 35% in South African pilot clinics. Oral routes remain pediatrics-focused and are capped at a 4.1% CAGR, as IPV global policy crowds out OPV beyond 2026.

Alternative routes such as Vaxxas’ micro-array patch demonstrated 92% seroconversion without refrigeration, positioning the approach as a cold-chain workaround for tropical LMICs. Intranasal candidates, such as Bharat Biotech’s iNCOVACC, offer potential for mucosal immunity but face uncertain regulatory pathways; no intranasal vaccine has cleared FDA review since 2003.

By End-User: Adult Vaccines Outpace Pediatric Growth

The pediatric vaccine segment held 55.54% of the vaccine market share in 2025, whereas the adult segment is the fastest-growing end-user, with an 11.31% CAGR, while pediatric uptake is static, driven by births. Japan’s and South Korea’s senior mandates drive demand for shingles and pneumococcal boosters, while RSV approvals add a second adult blockbuster category. The average revenue per adult dose reached USD 87 in 2025, seven times that of pediatric equivalents, underscoring a pivot toward margin-rich portfolios.

Retail pharmacies administered 48% of U.S. flu shots in 2025, disintermediating physician offices and broadening after-hours access. Pediatric schedules still post high volumes but face a margin squeeze from aggressive Indian biosimilar pricing and declining birth cohorts in East Asia; Japanese births fell to 730,000 in 2025, a 6% year-over-year decline.

Geography Analysis

North America accounted for a 39.26% contribution to the vaccine market size in 2025, driven by the launch of premium-priced adult vaccines. RSV vaccines generated USD 1.8 billion in their first year in the U.S., and shingles revenues reached USD 2.4 billion. Canada added RSV to its publicly funded list in April 2025, resulting in a CAD 120 million (USD 88 million) increase in provincial budgets. Vaccine hesitancy remains a drag; U.S. measles incidence rose 28% in 2025, catalyzing a USD 50 million CDC awareness drive.

The Asia-Pacific region, expanding at an 8.96% CAGR, benefits from manufacturing economies of scale, as the Serum Institute and Bharat Biotech now supply 62% of Gavi's demand. China approved 12 home-grown vaccines in 2025, including those for RSV and HPV, thereby reducing its dependency on imports. Japan’s aging demographics drive up adult booster volumes, while Australia fast-tracks Moderna’s RSV vaccine, underscoring regulator alignment on unmet need criteria. Cold-chain fragility persists in rural India and Indonesia, where spoilage rates for temperature-sensitive antigens approach 12%.

Europe’s regulatory rigor and fragmented procurement influence launch pacing; Bavarian Nordic’s mResvia became the region’s third RSV option within twelve months, intensifying price competition. France’s preschool MMR requirement lifted coverage five percentage points in six months, a policy Germany and Italy are studying. Africa’s meningitis belt launched an 18 million-dose emergency campaign in Nigeria, but one-third of the shipments arrived after the peak due to logistics snags. South America’s momentum centers on Brazil’s inclusion of HPV for boys and Argentina’s USD 60 million IDB-funded cold-chain upgrade, though Argentine macro-instability delayed rotavirus tenders by five months.

Competitive Landscape

The top five players, Pfizer, GSK, Sanofi, Merck, and Moderna, captured a significant portion of 2025 revenue, indicating moderate consolidation. Platform leverage is the key differentiator: Moderna’s ability to recycle its lipid nanoparticle chassis enabled an 18-month turnaround for RSV approval, influencing BioNTech’s strategy for a trivalent booster. Valneva’s clearance of chikungunya demonstrates the viability of its niche playbook, especially when paired with sovereign procurement contracts. Indian and Chinese suppliers continue to offer disruptive pricing; together, they supplied 62% of Gavi volumes in 2025, capturing market share from multinationals in LMIC tenders.

Vertical integration mitigates CDMO bottlenecks. Pfizer’s USD 450 million Kalamazoo upgrade added 200 million annual mRNA doses, de-risking supply after Novavax’s Catalent-linked delay. Patent landscapes signal strategic bets: GSK filed 14 elder-focused adjuvant patents in 2024-25, while Moderna logged nine for saRNA’s lower-dose potential. Regulatory convergence via ICH’s 2025 guideline trimmed average multi-jurisdiction lot-release timelines by three months, though 42 of 54 African regulators still demand standalone approvals, prolonging LMIC launch cycles.

Vaccines Industry Leaders

Merck & Co. Inc.

Moderna, Inc

Pfizer, Inc

Sanofi SA

Serum Institute of India Pvt Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Dr. Reddy’s Laboratories has made a significant stride in India’s immunisation landscape with the launch of Hevaxin, the country’s first and only hepatitis E vaccine approved by the Drug Controller General of India (DCGI). Designed for active immunisation against HEV infection, Hevaxin fills a critical gap in the prevention of hepatitis E, a disease that poses serious public health challenges in regions with limited sanitation infrastructure. This development highlights Dr. Reddy’s role in expanding India’s vaccine portfolio and addressing unmet medical needs.

- January 2026: CD Bioparticles has announced the introduction of an advanced animal mRNA vaccine platform, marking a significant innovation in veterinary medicine. The platform offers comprehensive solutions, including sequence optimisation, mRNA production, lipid nanoparticle (LNP) formulation, and preclinical testing.

- April 2024: Bavarian Nordic made its FDA-approved Mpox vaccine JYNNEOS commercially available in the United States, expanding access through additional procurement, reimbursement, and distribution pathways.

- January 2026: In Africa, the Lagos State Government has launched a large-scale measles-rubella vaccination campaign targeting 10.5 million children. This initiative is designed to close immunity gaps, protect vulnerable populations, and reduce the risks of preventable diseases across the state.

- September 2025: The University of Oxford, in collaboration with the Ellison Institute of Technology (EIT), has embarked on a groundbreaking initiative to advance vaccine research. Backed by GBP 118 million in funding, this ambitious programme will harness artificial intelligence to accelerate the discovery and development of next-generation vaccines. The partnership underscores Oxford’s commitment to global health and medical sciences, aiming to strengthen preparedness against emerging infectious diseases and improve vaccine accessibility worldwide.

Global Vaccines Market Report Scope

As per the report's scope, vaccines are biological preparations designed to provide immunity against specific diseases. They stimulate the body's immune system to recognize and combat pathogens, such as viruses or bacteria. Vaccines are crucial in preventing infectious diseases, reducing mortality rates, and promoting public health globally. They are administered through various methods, including injections and oral doses.

The vaccine market is segmented by technology, type, disease indication, route of administration, end-user, and geography. On the basis of technology, the market is segmented into conjugate vaccines, inactivated vaccines, live attenuated vaccines, mRNA vaccines, recombinant vaccines, toxoid vaccines, and viral vector vaccines. Based on type, the market is segmented into monovalent vaccines and multivalent vaccines. By disease indication, the market is segmented into DTP, hepatitis, herpes zoster, HPV, influenza, meningococcal disease, MMR, pneumococcal disease, polio, rotavirus, RSV, and other disease indications. On the basis of the route of administration, the market is segmented into oral administration, parenteral administration, and other routes of administration. By end-user, the market is bifurcated into adult vaccines and pediatric vaccines. On the basis of geography, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report offers the value (in USD) for the above-mentioned segments.

| Conjugate Vaccines |

| Inactivated Vaccines |

| Live Attenuated Vaccines |

| mRNA Vaccines |

| Recombinant Vaccines |

| Toxoid Vaccines |

| Viral-Vector Vaccines |

| Monovalent Vaccines |

| Multivalent Vaccines |

| DTP |

| Hepatitis |

| Herpes Zoster |

| HPV |

| Influenza |

| Meningococcal Disease |

| MMR |

| Pneumococcal Disease |

| Polio |

| Rotavirus |

| RSV |

| Other Indications |

| Oral |

| Parenteral |

| Other Route of Administration |

| Adult Vaccines |

| Paediatric Vaccines |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Technology | Conjugate Vaccines | |

| Inactivated Vaccines | ||

| Live Attenuated Vaccines | ||

| mRNA Vaccines | ||

| Recombinant Vaccines | ||

| Toxoid Vaccines | ||

| Viral-Vector Vaccines | ||

| By Vaccine Type | Monovalent Vaccines | |

| Multivalent Vaccines | ||

| By Disease Indication | DTP | |

| Hepatitis | ||

| Herpes Zoster | ||

| HPV | ||

| Influenza | ||

| Meningococcal Disease | ||

| MMR | ||

| Pneumococcal Disease | ||

| Polio | ||

| Rotavirus | ||

| RSV | ||

| Other Indications | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Other Route of Administration | ||

| By End-User | Adult Vaccines | |

| Paediatric Vaccines | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current global value of the vaccines market?

The vaccines market size stands at USD 96.24 billion in 2026 and is projected to reach USD 134.85 billion by 2031.

Which segment is expanding fastest within vaccines?

Adult immunization is advancing at an 11.31% CAGR, driven by RSV, shingles, and pneumococcal boosters.

How are mRNA technologies reshaping vaccine economics?

Repurposed mRNA facilities now compress development timelines to under three years and support high-margin adult launches such as RSV boosters.

Why do multivalent vaccines dominate pediatric schedules?

By combining up to six antigens per shot, multivalent formulations cut clinic visits, improve compliance, and currently account for two-thirds of pediatric doses.

Which regions show the highest growth potential?

Asia-Pacific leads with an 8.96% CAGR, propelled by large-scale manufacturing in India and China and expanding adult mandates in Japan, Australia, and South Korea.

Page last updated on: