Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.18 Billion |

| Market Size (2026) | USD 2.42 Billion |

| Market Size (2031) | USD 4.08 Billion |

| Growth Rate (2026 - 2031) | 11.02% CAGR |

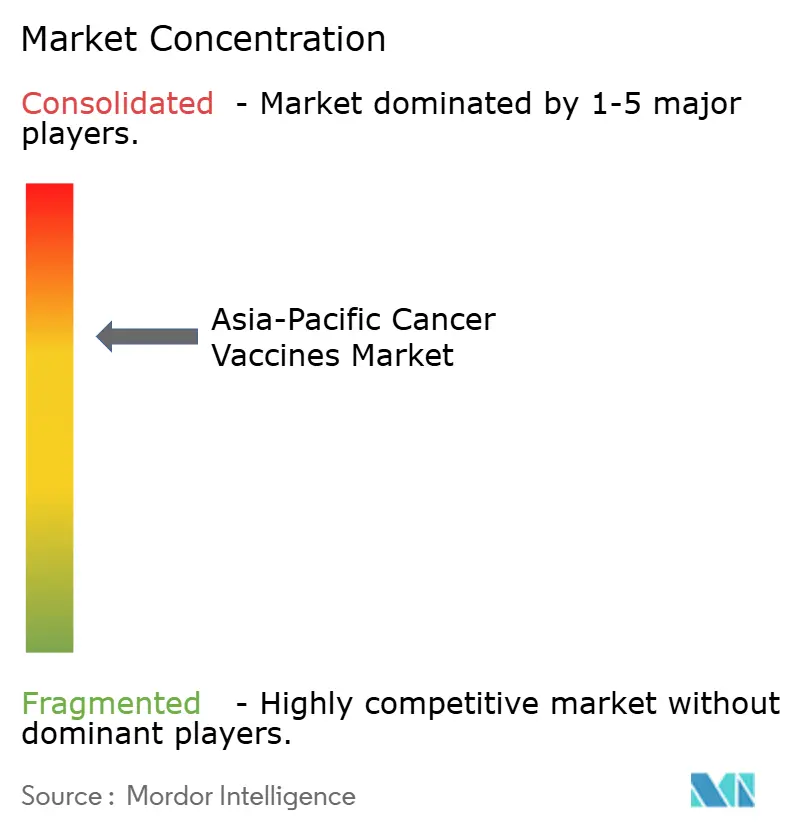

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Asia-Pacific Cancer Vaccines Market Analysis by Mordor Intelligence

The Asia-Pacific cancer vaccines market size is expected to grow from USD 2.18 billion in 2025 to USD 2.42 billion in 2026 and is forecast to reach USD 4.08 billion by 2031 at 11.02% CAGR over 2026-2031. Sustained growth rests on the region’s escalating cancer burden, policy-backed HPV immunisation roll-outs, and rapid breakthroughs in personalised mRNA–neoantigen platforms. Governments prioritise cervical-cancer prevention, while investors funnel capital into biotech clusters that shorten clinical timelines for new therapeutic vaccines. Contract development and manufacturing organisations (CDMOs) in China, India, and South Korea add capacity for viral-vector and mRNA production, flattening supply-chain risk and lowering unit costs. Intensifying competition from immune checkpoint inhibitors, CAR-T therapies, and emerging combination regimens tempers the speed of therapeutic uptake, yet economic analyses still favour vaccination over treatment for many tumour types. Together, these factors underpin double-digit annual expansion of the Asia-Pacific cancer vaccines market.

Key Report Takeaways

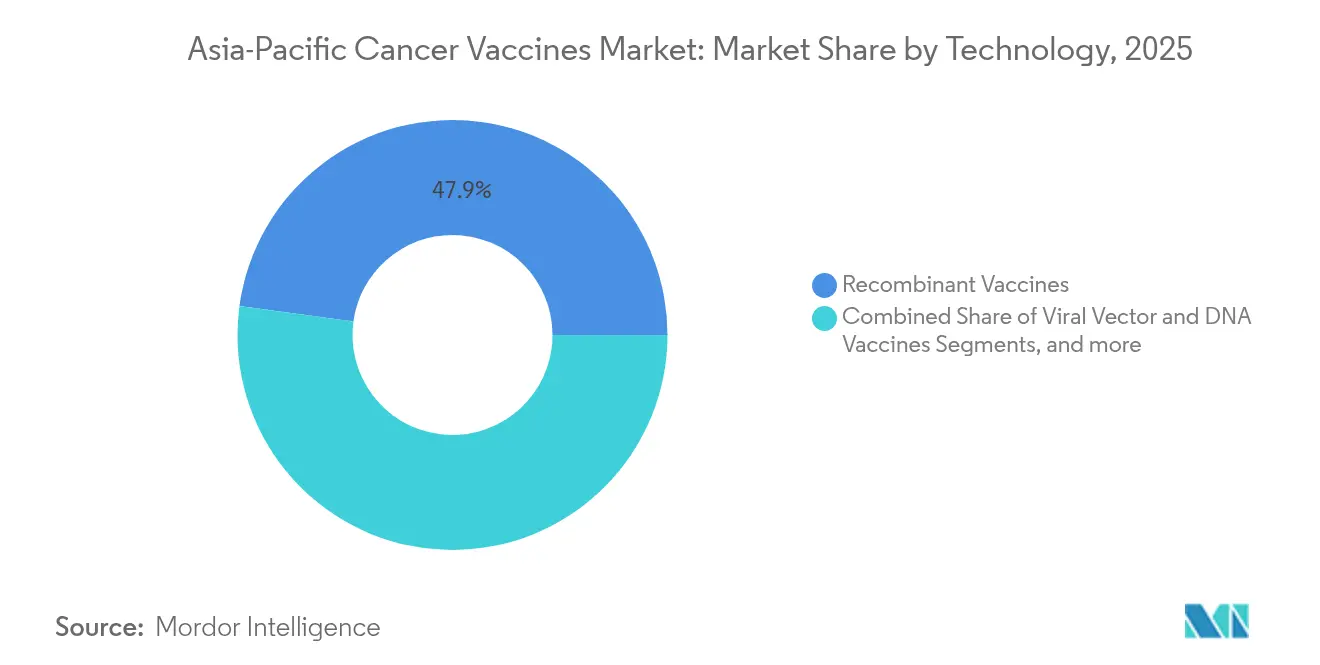

- By technology, recombinant vaccines led with 47.85% revenue share in 2025; mRNA/neoantigen platforms are projected to grow at a 11.92% CAGR to 2031.

- By treatment method, preventive products dominated with 90.75% of the Asia-Pacific cancer vaccines market share in 2025, while therapeutic formulations are forecast to expand at a 12.05% CAGR through 2031.

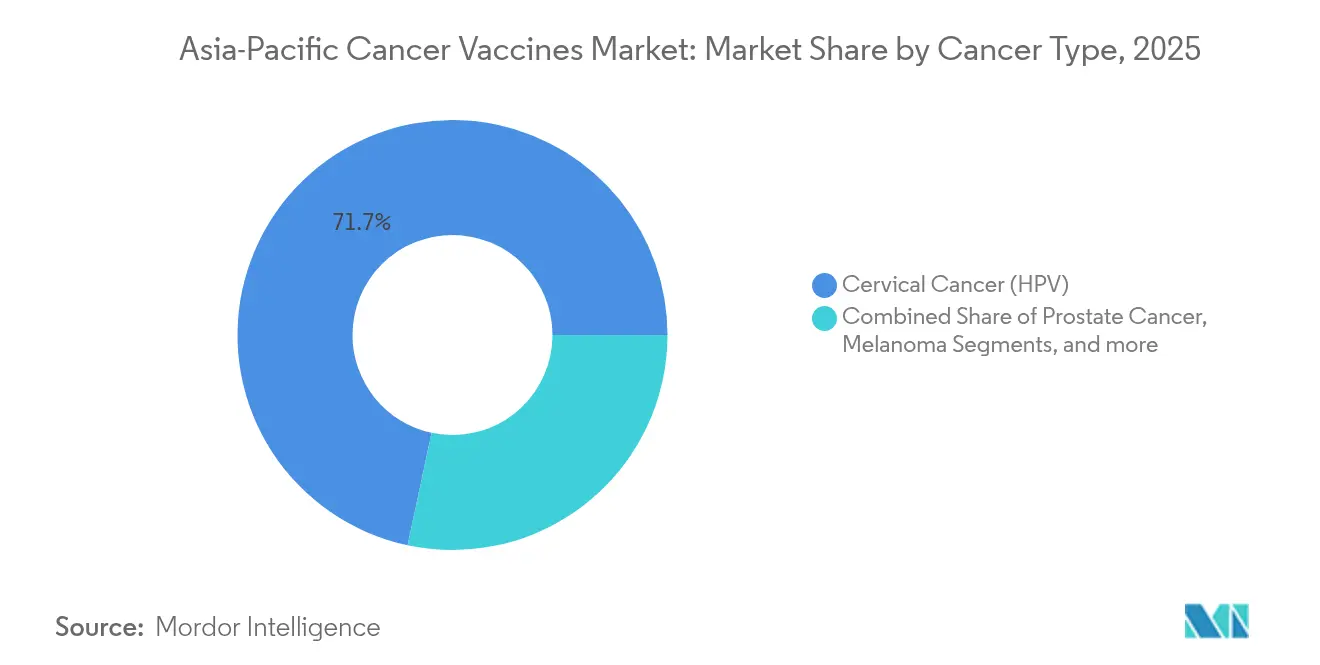

- By cancer type, cervical-cancer-focused HPV vaccines accounted for 71.65% of 2025 revenue; melanoma vaccines are the fastest-growing segment, advancing at a 12.11% CAGR to 2031.

- By delivery route, the intramuscular segment captured 65.60% of sales in 2025; intravenous administration is poised for 12.20% CAGR expansion to 2031.

- By geography, China commanded 29.10% of the Asia-Pacific cancer vaccines market size in 2025, whereas India is projected to post the highest regional CAGR of 12.24% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Asia-Pacific Cancer Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing burden of cancer across APAC | +2.8% | China, India, regional urban hubs | Long term (≥ 4 years) |

| HPV-vaccination national roll-outs | +2.1% | China, Japan, India, Australia | Medium term (2-4 years) |

| Shift toward personalised neo-antigen vaccine platforms | +1.9% | China, Japan, Singapore | Medium term (2-4 years) |

| Rapid scale-up of regional CDMO capacity for mRNA/viral-vector vaccines | +1.6% | China, India, South Korea | Short term (≤ 2 years) |

| Government price support for locally made HPV vaccines | +1.4% | China, India, Indonesia | Medium term (2-4 years) |

| Oncology-focused venture funding surge into biotech clusters | +1.2% | Singapore, China, Japan | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Growing Burden of Cancer Across APAC Drives Market Expansion

Asia-Pacific now shoulders 60% of global cancer cases, a figure driven by urbanisation, dietary shifts, and rapid population ageing. China reports 4.57 million new diagnoses annually, while cervical cancer incidence in India exceeds 23 per 100,000 women in several states. Region-specific malignancies—nasopharyngeal, hepatocellular, and gastric cancers—raise unique prevention needs. Economic modelling shows that vaccination can cut cervical cancer incidence by 20-76% across Vietnam, Thailand, and Indonesia, making prophylaxis more cost-effective than treatment. These dynamics sustain long-term demand for both preventive and therapeutic cancer vaccines.

HPV-Vaccination National Roll-Outs Accelerate Market Penetration

China’s Healthy China 2030 agenda places HPV immunisation at the centre of women’s-health policy, even though coverage among girls aged 9-14 stands at just 2.24% [1]Huijiao Yan, "Cervical cancer prevention in China: where are we now, and what’s next?," Cancer Biology and Medicine, cancerbiomed.org. Japan reversed its decade-long suspension of proactive HPV recommendations, Australia already tops 90% coverage, and Indonesia’s campaigns show 54-82% declines in HPV-related disease. Incremental cost-effectiveness ratios range from USD 166 to USD 450 per QALY in Mongolia, Indonesia, and Thailand, giving finance ministries confidence to fund large-scale procurement. Predictable demand volumes allow suppliers to negotiate long-term contracts and ramp regional output.

Shift Toward Personalised Neo-Antigen Vaccine Platforms

Chinese innovators have propelled the transition from broad-spectrum to patient-specific vaccines. Likang Life Sciences’ LK-101 and Everest Medicines’ EVM16 harness AI algorithms to select tumour-exclusive epitopes and encode them into mRNA constructs [2]Everest Medicines, "Everest Medicines Announces First Patient Dosed with EVM16, Its First Internally Developed Personalized mRNA Cancer Vaccine," everestmedicines.com. Projected six-dose regimens cost below CNY 100,000 (USD 13,800), undercutting comparable Western therapies by 99% without sacrificing response rates. Personalisation also aligns with HLA-A 11:01 prevalence in up to 60% of Asian populations, supporting robust immunogenicity [3]Xinjing Wang, "Combination therapy of KRAS G12V mRNA vaccine and pembrolizumab: clinical benefit in patients with advanced solid tumors," Cell Research, nature.com. Rapid design-to-manufacture cycles shorten development timelines from months to weeks, reinforcing Asia-Pacific leadership in precision oncology.

Rapid Scale-Up of Regional CDMO Capacity for mRNA/Viral-Vector Vaccines

Takara Bio and Thermo Fisher’s new facility utilises DynaDrive single-use bioreactors to deliver clinical and commercial runs of viral vectors under GMP. Overall biologics capacity in China reached 4.7 million L in 2025, with India contributing 941,000 L across vaccine platforms. StemiRNA Therapeutics now operates lines capable of 100 million doses annually, funded by nearly USD 200 million in equity rounds. Singapore and South Korea invest in full-stack mRNA ecosystems, lowering import reliance and creating alternative supply corridors for ultra-cold-chain products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Competition from immune-checkpoint inhibitors & CAR-T therapies | -1.8% | Japan, Australia, urban China | Medium term (2-4 years) |

| Low adult-immunisation acceptance in Southeast Asia | -1.5% | Indonesia, Thailand, Philippines, Vietnam | Long term (≥ 4 years) |

| Supply-chain fragility for ultra-cold-chain mRNA vaccines | -1.2% | Infrastructure-limited areas | Short term (≤ 2 years) |

| Heightened regulatory scrutiny after safety-signal incidents | -0.9% | Japan, South Korea, Singapore | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Competition from Immune-Checkpoint Inhibitors & CAR-T Therapies

PD-1/PD-L1 inhibitors could generate USD 4 billion in China by 2025, with domestic firms moving beyond lung and liver cancer into broader solid-tumour pipelines. Claudin18.2 CAR-T protocols report 38.8% objective response and 91.8% disease-control rates in early-phase gastrointestinal trials. Acceptable safety profiles—96.1% of adverse events graded mild or moderate—bolster clinician confidence and may divert patients from vaccine based therapeutics. Combination regimens such as efti plus pembrolizumab post 32.8% response versus 26.7% for monotherapy, further crowding the immuno-oncology landscape.

Low Adult-Immunisation Acceptance in Several Southeast-Asian Nations

Cultural conservatism, religious beliefs, and misinformation lower vaccine intent among adults. Surveys show high uptake when HPV shots are free, but willingness falls once co-payment is introduced. Community-led communication, home-visit outreach, and faith-based advocacy have improved completion rates, yet hesitancy persists among older cohorts. ASEAN nations confront an added hurdle: an ageing population expected to reach 1.3 billion over 65 by 2050. Without targeted public-health campaigns, low adult uptake could slow therapeutic vaccine roll-outs despite clear cost-effectiveness.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: mRNA Platforms Challenge Recombinant Vaccine Dominance

Recombinant products held 47.85% of 2025 revenue, anchoring the Asia-Pacific cancer vaccines market with proven safety records and well-established GMP lines. The mRNA/neoantigen class is set to rise at 11.92% CAGR, reshaping the competitive grid as cost-efficient Chinese playersrapidly commercialise personalised candidates. Viral-vector and DNA modalities post stable mid-single-digit trajectories, serving as bridges between legacy constructs and next-generation therapies. Whole-cell and dendritic-cell vaccines remain niche, yet they retain clinical relevance for advanced solid tumours that require multi-antigen responses.

The mRNA upswing is powered by AI-driven target discovery and flexible production cycles that compress sequence-to-clinic timelines. Likang Life Sciences’ LK-101 and StemiRNA’s lipid-polyplex system illustrate cost-engineering advantages, enabling six-dose regimens at one-hundredth of prevailing Western prices. Regional CDMO build-outs further widen the gap by eliminating transcontinental freight and customs delays. As a result, mRNA lines are forecast to absorb a sizeable share of future approvals, particularly in cancers with high mutational loads such as melanoma and lung adenocarcinoma.

By Treatment Method: Therapeutic Vaccines Gain Momentum Despite Preventive Dominance

Preventive formulations controlled 90.75% of 2025 revenue, reflecting government-funded HPV programmes and broad public-health messaging. Therapeutic candidates, however, are tracking a 12.05% CAGR on rising demand for patient-specific regimens that augment checkpoint inhibitors. The Asia-Pacific cancer vaccines market size for therapeutic injections is projected to expand from USD 221.6 million in 2026 to roughly USD 391.4 million by 2031, underscoring the shift toward integrated care pathways.

Economic models continue to favour prophylaxis, with HPV programmes costing below USD 450 per QALY in multiple low- and middle-income settings. Yet second-line data for agents like BVAC-C, which delivered 19.2% objective response and 53.8% disease control in refractory cervical cancer, validate therapeutic relevance. As neoantigen selection tools mature, therapeutic cycles are expected to integrate seamlessly with standard chemoradiation, redefining downstream revenue pools.

By Cancer Type: Melanoma Vaccines Accelerate Beyond HPV Applications

HPV-driven cervical-cancer prevention generated 71.65% of 2025 volume, due to widescale adolescent immunisation in China, Australia, and Japan. Melanoma candidates, boosted by combination trials pairing mRNA vaccines with pembrolizumab, are slated for a 12.11% CAGR through 2031. The Asia-Pacific cancer vaccines market share for melanoma solutions is forecast to double by 2031 as KRAS- and NRAS-targeted regimens move into pivotal studies.

Japan’s modelled adoption of 9-valent HPV immunisers could avert over 43,000 deaths across a century, illustrating the lasting footprint of prophylaxis. Meanwhile, KRAS G12V mRNA constructs have shown clinical benefit in heavily pretreated patients, positioning melanoma as the template for personalised approaches in other solid tumours. Prostate and hepatocellular indications follow closely, drawing on peptide-based candidates such as GPC3 that cut one-year recurrence by 15% in early investigators’ analyses.

By Delivery Route: Intravenous Administration Emerges for Therapeutic Applications

Intramuscular shots captured 65.60% of 2025 demand thanks to legacy HPV programme logistics and healthcare-worker familiarity. Intravenous infusions will rise fastest at 12.20% CAGR, expanding the Asia-Pacific cancer vaccines market size for systemic delivery significantly. Intradermal and subcutaneous modes find limited yet strategic footholds where dose-sparing or home-based care is essential.

Intravenous administration offers direct biodistribution for complex therapeutics that require rapid lymphatic engagement. Early-phase melanoma trials demonstrate potent CD8+ T-cell expansion with IV mRNA dosing, reinforcing adoption for personalised vaccines. Intramuscular formulations remain standard for prophylaxis; indeed, L2-based multivalent HPV constructs delivered via lipid-nanoparticle IM injection outperformed traditional adjuvanted comparators on neutralising-antibody breadth.

Geography Analysis

China accounted for 29.10% of the Asia-Pacific cancer vaccines market in 2025, translating to roughly USD 634 million in annual revenue. Scale stems from 89 registered vaccine trials, six approved oncology immunisers, and a deep CDMO base that buffers global supply shocks. National procurement frameworks and provincial subsidy schemes keep recombinant-HPV prices below USD 110 per course, maintaining high adolescent uptake despite urban-rural disparities.

India is the fastest-growing market, pacing a 12.24% CAGR to 2031 on the back of universal cervical-cancer immunisation readiness. The Serum Institute’s indigenous HPV shot widens access through sub-USD 5 ex-factory pricing that meets government tender requirements. Clinical-trial incentives, a large treatment-naïve cohort, and English-speaking investigators attract multinationals seeking operational cost savings up to 30% versus Western counterparts.

Japan commands mid-teens share with stringent regulatory oversight and renewed HPV programme endorsement. Government subsidies now back full-course vaccination for girls aged 12-16, reversing a years-long coverage slump. South Korea leverages innovation clusters outside Seoul to trial mRNA constructs, while Australia enjoys the region’s highest prophylactic coverage above 90%, reflecting decades of school-based delivery success.

Across emerging ASEAN economies, variable adult-immunisation acceptance creates a patchwork of demand patterns. Malaysia’s pilot HPV programme posts 85% completion among schoolgirls, yet adult catch-up remains below 20%. Vietnam and Thailand see marked incidence reductions where sub-national pilots integrate electronic-health-record tracking. Infrastructure limitations—for example, unreliable ultra-cold storage in rural archipelagos—pose a near-term headwind to mRNA penetration but also justify investment in thermostable formulations.

Competitive Landscape

The market exhibits moderately consolidated concentration, with multinational incumbents holding entrenched HPV franchises while regional specialists race ahead in personalised therapeutics. Merck’s Gardasil and GSK’s Cervarix dominate prophylaxis tenders, supported by extensive safety data and supply continuity. Pfizer advances BNT122 in colorectal cancer under its BioNTech alliance, signalling a shift toward therapeutic expansion.

Chinese firms leverage cost and speed advantages. Likang Life Sciences targets first-to-market status for LK-101, the nation’s inaugural personalised neoantigen vaccine, while Everest Medicines’ EVM16 integrates AI epitope prediction for solid tumours. StemiRNA’s 100-million-dose annual capacity underpins strategic partnerships with domestic hospitals to embed vaccine manufacturing within provincial oncology centres.

Japanese innovators such as NEC adopt bioinformatics suites for epitope selection, pairing with Takara Bio’s viral-vector line to cut tech-transfer timelines. South Korean CDMOs focus on GMP-grade lipid-nanoparticle production, closing a critical raw-material gap. Competitive tactics increasingly blend joint ventures, AI collaborations, and government co-funding, signalling that scale and informatics prowess will decide long-term winners in the Asia-Pacific cancer vaccines market.

Asia-Pacific Cancer Vaccines Industry Leaders

-

Glaxosmithkline Plc

-

Bristol-Myers Squibb

-

Sanofi

-

Eli Lilly

-

AstraZeneca Plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Everest Medicines dosed the first patient with EVM16, a personalised mRNA cancer vaccine, at Peking University Cancer Hospital, utilising AI-driven neoantigen prediction for advanced solid tumours.

- November 2024: CSPC Pharmaceutical Group received NMPA clearance to begin clinical trials of SYS-6026, an HPV mRNA vaccine targeting high-grade squamous intraepithelial lesions linked to HPV16 and HPV18.

- August 2024: WestGene Biopharma’s WGc-043 mRNA therapeutic cancer vaccine secured dual IND approvals from China’s NMPA and the US FDA, enabling parallel Phase 1 programmes.

- March 2024: Serum Institute of India announced plans to expand supply of its indigenous HPV vaccine for a national immunisation campaign targeting girls aged 9-14.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the Asia-Pacific cancer vaccines market as the value generated by prophylactic and therapeutic immunogenic preparations that prime the immune system to prevent or treat malignant tumors across China, Japan, India, South Korea, Australia, and the remaining regional economies. These formulations span recombinant, viral-vector, DNA, mRNA/neoantigen, whole-cell, and dendritic-cell technologies delivered through intramuscular, intradermal, sub-cutaneous, or intravenous routes.

Scope exclusion: Cell-based adoptive immunotherapies such as CAR-T or TCR-T, as well as non-oncology vaccine sales, are omitted.

Segmentation Overview

-

By Technology

- Recombinant Vaccines

- Viral Vector & DNA Vaccines

- mRNA/Neoantigen Personalised Vaccines

- Whole-cell & Dendritic Cell Vaccines

- Other Technologies

-

By Treatment Method

- Preventive Vaccines

- Therapeutic Vaccines

-

By Cancer Type

- Cervical Cancer (HPV)

- Prostate Cancer

- Melanoma

- Other Cancers

-

By Delivery Route

- Intramuscular

- Intradermal / Sub-cutaneous

- Intravenous

-

By Geography

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interview medical oncologists, immunization program officers, CDMO executives, and payor advisors across core economies. These discussions validate penetration assumptions, real-world dose pricing, and pipeline launch timing, enabling us to close information gaps left by desk work and to challenge early model outputs.

Desk Research

We begin by mining tier-1 open datasets such as WHO GLOBOCAN incidence files, China NHC immunization bulletins, India's National Cancer Registry, Japan PMDA trial logs, and peer-reviewed articles in Lancet Oncology. Supplementary intelligence flows from customs shipment dashboards, association portals like the Asia Pacific Cancer Society, and company 10-Ks captured via D&B Hoovers and Dow Jones Factiva. National reimbursement schedules and tender listings offer real-world price corridors. The sources listed illustrate our approach; numerous additional references were employed for corroboration and clarification.

Market-Sizing & Forecasting

A top-down incidence-to-uptake construct estimates eligible patient pools, which are then aligned with government procurement budgets and private-sector demand. Results are cross-checked through sampled bottom-up roll-ups of leading supplier revenues and channel checks. Key variables include HPV vaccination coverage among adolescent girls, clinical trial success rates for mRNA/neoantigen candidates, average selling price shifts following national tender rounds, cervical-cancer prevalence trends, and public immunization funding growth. Multivariate regression, augmented by scenario analysis for pipeline attrition, projects each driver through 2030. Where supplier roll-ups under-represent fragmented local production, gap factors derived from import data are applied.

Data Validation & Update Cycle

Outputs undergo variance tests against historical spending, peer ratios, and emerging regulatory signals. A two-step analyst review precedes sign-off, and the dataset is refreshed annually, with ad-hoc updates triggered by major approvals, reimbursement changes, or macro disruptions.

Why Mordor's Asia-Pacific Cancer Vaccines Baseline Commands Trust

Published estimates often diverge because firms draw boundaries differently, prefer alternate pricing references, or refresh on uneven calendars.

Key gap drivers stem from scope breadth, input transparency, and refresh cadence. Mordor Intelligence grounds its baseline in cancer-specific incidence and vaccination uptake rather than pooled biologic sales, applies country-level prices obtained from tenders, and revisits every assumption each year, which curbs over or under shooting.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.18 B (2025) | Mordor Intelligence | |

| USD 1.30 B (2024) | Regional Consultancy A | Excludes mRNA/neoantigen products and relies on shipment volumes without physician-level uptake checks |

| USD 1.99 B (2023) | Trade Journal B | Applies 2023 vaccine revenue then inflates with generic growth rates; lacks country incidence adjustment and deep primary validation |

| USD 4.12 B (2025) | Global Consultancy A | Bundles HPV sales with broader biologic therapies and uses aggressive 17 % CAGR; includes private-clinic spend across Southeast Asia |

These contrasts show that when scope, inputs, and cadence are aligned with clinical reality, Mordor's balanced baseline emerges as the dependable reference for planning, investment, and policy decisions.

Key Questions Answered in the Report

What is the current size of the Asia-Pacific cancer vaccines market?

The market stands at USD 2.42 billion in 2026 and is projected to hit USD 4.08 billion by 2031, reflecting an 11.02% CAGR.

Which technology segment is expanding fastest?

MRNA/neoantigen platforms are the most rapidly growing, with a 11.92% CAGR forecast through 2031.

Why does India show the highest growth rate?

India benefits from national HPV immunisation readiness, low-cost domestic manufacturing, and a rising oncology clinical-trial ecosystem, driving a 12.24% CAGR.

How dominant are preventive vaccines today?

Preventive formulations, led by HPV shots, accounted for 90.75% of market revenue in 2025.

What restrains wider adult immunisation uptake in Southeast Asia?

Cultural conservatism, limited awareness, and infrastructural hurdles continue to curb adult vaccination rates, particularly for therapeutic cancer vaccines.

Page last updated on: