Pediatric Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

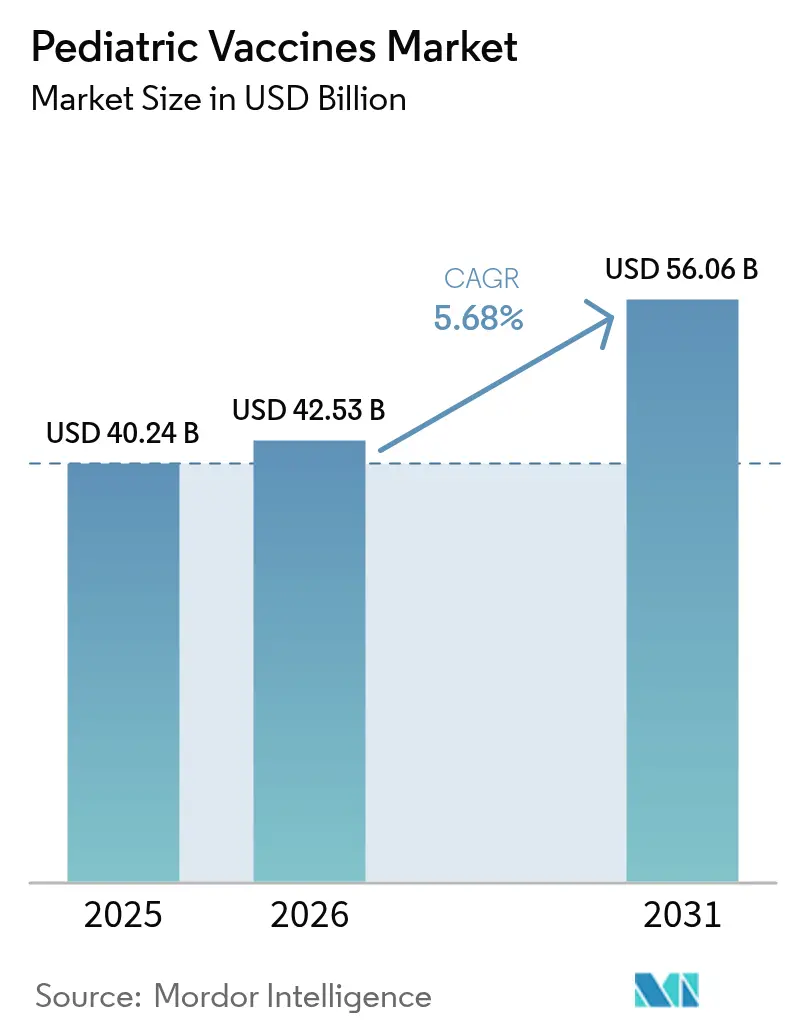

| Market Size (2026) | USD 42.53 Billion |

| Market Size (2031) | USD 56.06 Billion |

| Growth Rate (2026 - 2031) | 5.68% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Pediatric Vaccines Market Analysis by Mordor Intelligence

The pediatric vaccines market size was valued at USD 40.24 billion in 2025 and estimated to grow from USD 42.53 billion in 2026 to reach USD 56.06 billion by 2031, at a CAGR of 5.68% during the forecast period (2026-2031). Strong governmental funding, a growing preference for multivalent formulations and the rapid scale-up of mRNA and other next-generation platforms are sustaining this growth momentum. Expanded public immunization budgets, exemplified by the United States Vaccines for Children Program and the USD 5 billion Project NextGen investment in advanced COVID-19 prophylaxis, continue to underpin volumes and spur innovation. At the same time, digital supply-chain automation and blockchain-based traceability solutions aim to curb the one-in-three wastage rate that still affects global vaccine distribution, thereby protecting up to USD 30 billion in value annually. Market opportunities are also widening as maternal RSV immunization enters routine use, and as manufacturers bring higher-valent conjugates and recombinant candidates to commercial scale.

Key Report Takeaways

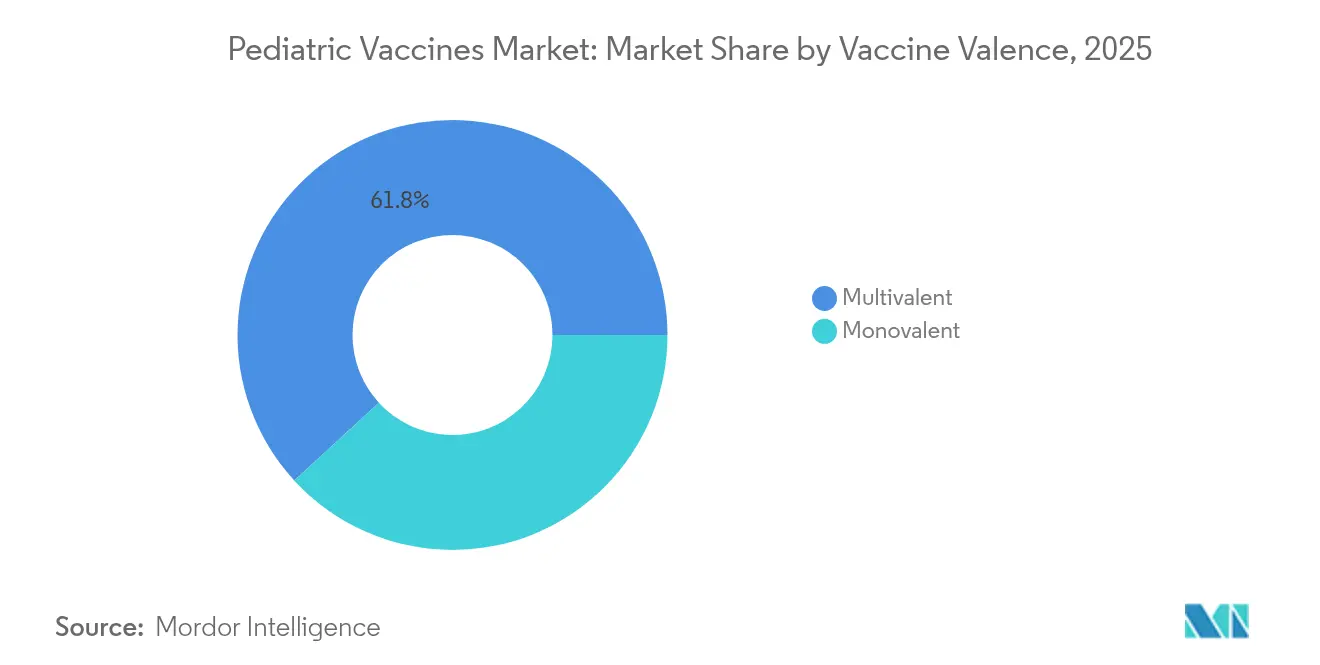

- By vaccine valence, multivalent products led with 61.83% revenue share in 2025, while monovalent vaccines are projected to post the fastest 6.35% CAGR to 2031.

- By technology platform, conjugate vaccines held 35.82% of 2025 revenue; the recombinant segment is set to expand at a 6.31% CAGR through 2031.

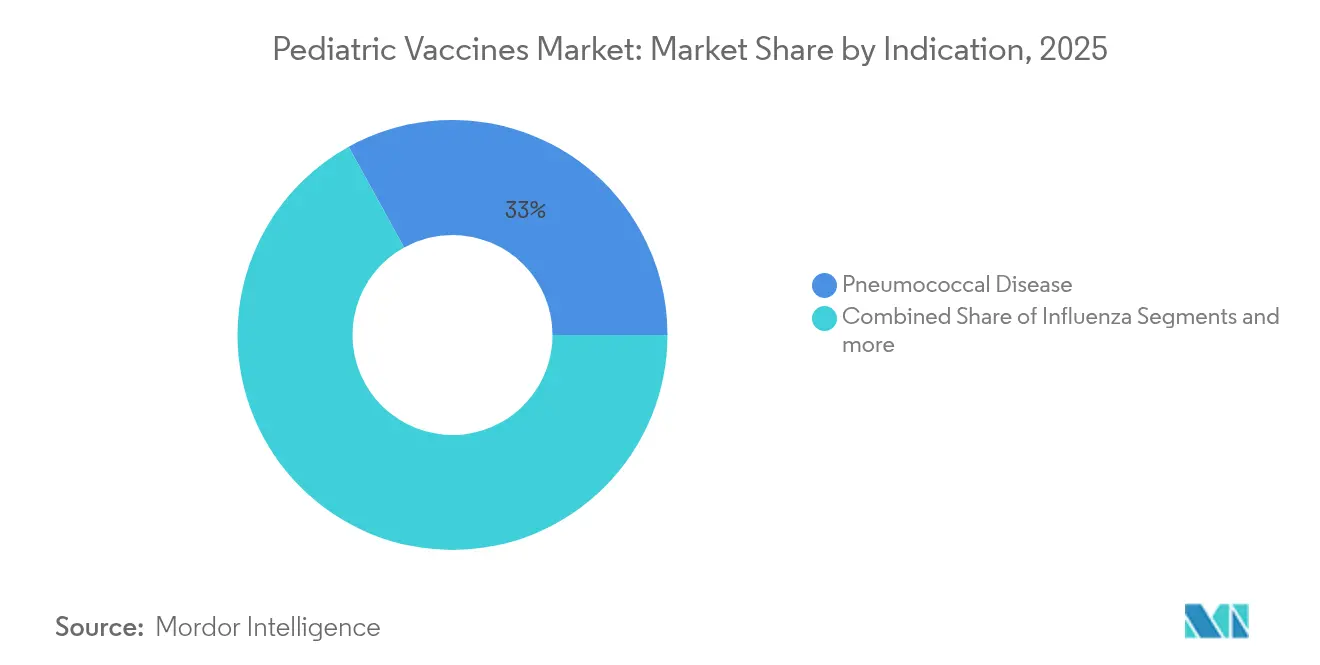

- By indication, pneumococcal formulations accounted for 33.02% revenue in 2025, whereas influenza vaccines exhibit the highest 6.23% CAGR outlook to 2031.

- By distribution channel, the public sector commanded 66.12% of global sales in 2025; the private channel is forecast to grow at 6.19% CAGR as coverage broadens.

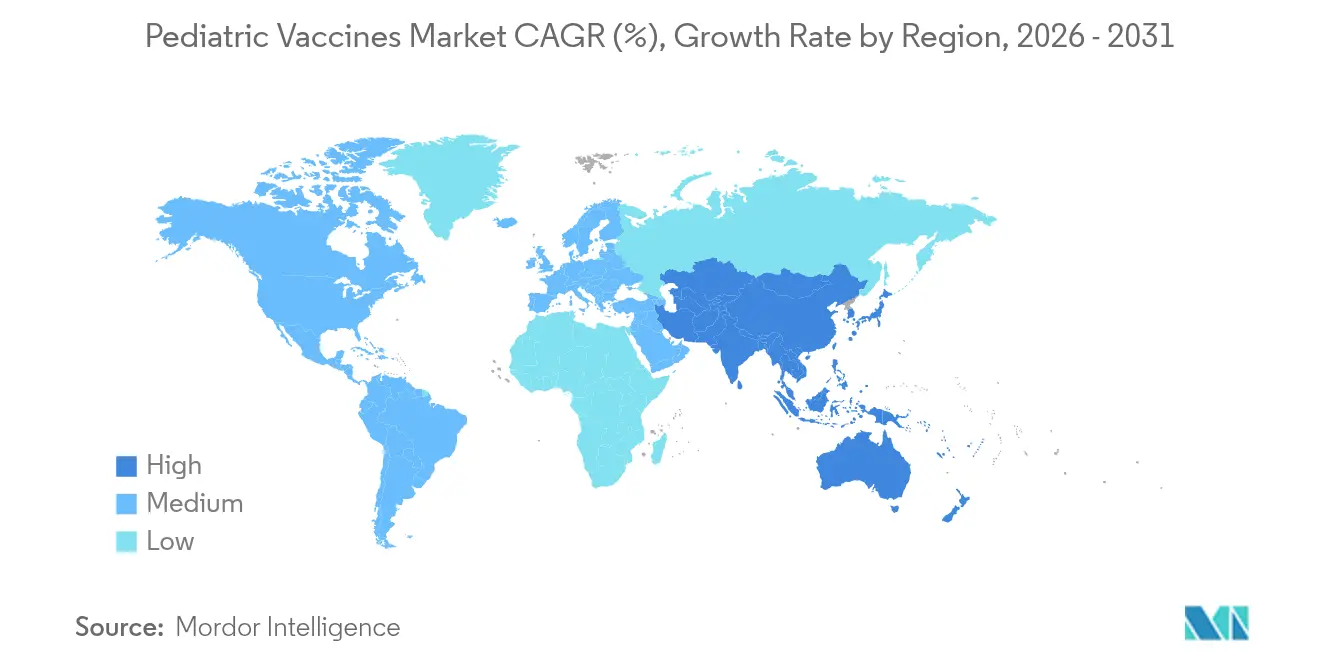

- By geography, North America captured 38.72% of 2025 revenue, while Asia-Pacific is on track for the leading 6.46% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Pediatric Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising burden of vaccine-preventable diseases & growing immunization awareness | +1.2% | Global, high in Asia-Pacific & Sub-Saharan Africa | Medium term (2-4 years) |

| Escalating government & NGO funding for pediatric vaccine R&D and procurement | +1.0% | North America & Europe for R&D; LMICs for procurement | Long term (≥ 4 years) |

| Rapid adoption of higher-valent/combination vaccines to reduce needle burden | +0.8% | North America & EU leading; Asia-Pacific following | Short term (≤ 2 years) |

| Expansion of next-gen platforms (mRNA, VLP, viral-vector) into pediatric profiles | +0.9% | North America & EU core; developed APAC spill-over | Long term (≥ 4 years) |

| Emergence of maternal & neonatal RSV immunization as new blockbuster segment | +0.7% | Early adoption in high-income markets | Medium term (2-4 years) |

| Clinic-level digital supply-chain automation improving pediatric vaccine uptake | +0.4% | Digitally mature markets worldwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising burden of vaccine-preventable diseases & growing immunization awareness

Measles outbreaks underscore widening immunity gaps, with Vietnam recording 81,691 suspected cases in 2025, the highest since 2020 [1]World Health Organization, “Measles – Global Situation Update,” who.int . Similar spikes in pertussis and varicella across parts of Sub-Saharan Africa are prompting emergency catch-up campaigns, driving short-term procurement surges and longer-run commitments to reinforce routine schedules. Influenza mortality among children likewise remains a policy flashpoint, leading national agencies to intensify seasonal vaccination messaging and pivot toward highly immunogenic adjuvanted or cell-based formulations. These epidemiological pressures are stimulating investment in cold-chain upgrades as well as point-of-care digital registries that track individual dose completion and flag drop-outs in real time. Collectively, such measures expand demand for convenience-oriented combination products and encourage accelerated approvals for novel antigens.

Escalating government & NGO funding for pediatric vaccine R&D and procurement

Project NextGen channels USD 5 billion into mucosal and pan-coronavirus candidates poised for pediatric evaluation, signalling long-term federal commitment to transformative prophylaxis. In parallel, Gavi’s 2026-2030 strategy seeks at least USD 9 billion in new donor pledges and allocates USD 1.2 billion to the African Vaccine Manufacturing Accelerator to localize production. At the access end, the United States Vaccines for Children Program reliably removes out-of-pocket costs, stabilizing baseline volumes and insulating manufacturers from demand shocks. Such multi-tiered funding frameworks de-risk innovation, shorten payback horizons and help sustain a diversified late-stage pipeline targeting unmet pediatric needs.

Rapid adoption of higher-valent/combination vaccines to reduce needle burden

Public schedules now prioritize hexavalent and pentavalent injections such as Vaxelis, Pediarix and Pentacel, cutting the total shot count without compromising coverage [2]Centers for Disease Control and Prevention, “Child and Adolescent Immunization Schedule 2025,” cdc.gov . In China, DTaP-IPV/Hib uptake climbed from 11.25% in 2019 to 18.74% in 2021 despite persistent urban–rural disparities. Technology advances are reinforcing this trend: Massachusetts Institute of Technology researchers have created polymer microparticles that release sequential doses, theoretically converting multi-visit courses into a single administration. Combination logic is moving beyond classical DTP-polio-Hib groupings toward respiratory bundles; Moderna and Sanofi are each advancing COVID-19/influenza dual candidates that could streamline seasonal paediatric campaigns.

Expansion of next-gen platforms (mRNA, VLP, viral-vector) into pediatric profiles

Moderna’s mRNA-1345 earned first-in-class approval for RSV, validating mRNA versatility beyond COVID-19. Early-stage multivalent mRNA-DTP constructs elicit Th1-biased responses comparable to whole-cell pertussis, potentially solving the durability issues seen with acellular formulations [3]M. Allison Wolf, "Multivalent mRNA-DTP vaccines are immunogenic and provide protection from Bordetella pertussis challenge in mice," nature.com. Virus-like particle technology likewise broke ground when Bavarian Nordic’s Vimkunya chikungunya vaccine achieved a 97.8% seroresponse within 21 days. Such breakthroughs compress development timelines, enable modular antigen swapping and support smaller, flexible manufacturing footprints attractive to regional producers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of full immunization schedules per child | -0.8% | Global, acute in LMIC and uninsured cohorts | Short term (≤ 2 years) |

| Limited healthcare coverage & infrastructure in low- and middle-income countries | -1.1% | Sub-Saharan Africa, South Asia, rural Latin America | Long term (≥ 4 years) |

| Growing vaccine hesitancy and misinformation on pediatric shots | -0.9% | North America & Europe | Medium term (2-4 years) |

| Ultra-cold-chain & last-mile logistics gaps for novel modalities | -0.6% | Tropical and remote regions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High cost of full immunization schedules per child

The CDC now recommends 36 doses before age 2 and more than 70 by age 18, translating into public-sector costs of roughly USD 1,452 and private-sector outlays of USD 2,012 per child according to peer-reviewed analyses. Middle-income economies that recently transitioned out of Gavi support feel the squeeze most acutely, as list prices outpace national purchasing power yet donor assistance winds down. Combination vaccines mitigate some expenditure, but newer platforms such as mRNA still carry premium price tags owing to sophisticated bioprocessing and distribution overheads. Consequently, procurement agencies are piloting outcome-based contracts and pooled advance purchase agreements to preserve coverage levels without breaching budget ceilings.

Limited healthcare coverage & infrastructure in low- and middle-income countries

WHO estimates that routine immunization averted 4.2 million deaths in 2023—below the 4.6 million target—underscoring capacity gaps in several regions. Studies from Nepal show that freeze-preventive cold boxes can protect inventory worth USD 1,704 per shipment, yet scale-up remains slow because of capital constraints. Blockchain pilots such as VaccineLedger aim to improve end-to-end visibility and reduce the current one-in-three wastage level. Nevertheless, shortages of trained vaccinators and patchy electronic health-record systems limit the speed at which these technological fixes translate into higher coverage percentages.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vaccine Valence: Multivalent Dominance Drives Compliance

Multivalent formulations captured 61.83% of pediatric vaccines market revenue in 2025, illustrating the clear efficiency gains health systems achieve when several antigens are delivered in one injection. The segment benefits from simplified logistics, reduced clinic visits and improved caregiver acceptance, all of which lower missed-dose rates and contribute to sustained herd immunity.

Demand for monovalent products remains resilient, growing at a 6.35% CAGR through 2031 as niche applications emerge for single-antigen boosters, rapid outbreak control and immunisation of immunocompromised children. Innovations such as MIT’s time-release microparticle technology promise to blur the line between single and multi-antigen approaches by packaging separate doses into one shot. As national schedules widen to include maternal RSV and expanded meningococcal protection, the pediatric vaccines market will continue to balance convenience-driven multivalent uptake against targeted monovalent interventions that address specific epidemiological gaps.

By Technology Platform: Conjugate Leadership Amid Recombinant Acceleration

Conjugate vaccines maintained a 35.82% revenue lead in 2025, buoyed by two decades of clinical performance against encapsulated bacteria and their inclusion in nearly all first-year schedules. This dominance is unlikely to diminish soon; nevertheless, recombinant technologies are advancing the fastest at 6.31% CAGR as manufacturers exploit high-yield expression systems and scalable bioreactors to meet surging global demand.

The pediatric vaccines market size for recombinant candidates is forecast to expand materially once higher-valent constructs like Sanofi’s PCV21 move beyond Phase 3 and enter tender cycles. Concurrently, multivalent mRNA-DTP prototypes illustrate how recombinant and nucleic-acid platforms can cooperate to address waning pertussis immunity. This convergence accelerates portfolio refresh rates and provides mid-tier manufacturers with a cost-effective route into complex antigen markets traditionally controlled by a handful of incumbents.

By Indication: Pneumococcal Dominance Contrasts Influenza Urgency

Pneumococcal products accounted for 33.02% of 2025 revenue, validating the persistent burden of invasive disease despite longstanding infant programs. Vaxcyte’s 31-valent conjugate VAX-31, now in adult Phase 3 with pediatric trials slated for 2025, exemplifies the arms race to broaden serotype coverage beyond the current 15- and 20-valent benchmarks.

Influenza vaccines are projected to achieve the highest 6.23% CAGR through 2031, reflecting policy shifts toward annual paediatric dosing and the looming prospect of universal flu antigens that could slash breakthrough infections. The pediatric vaccines market share for trivalent products may rise temporarily after the CDC removed B/Yamagata lineage from recommendations in 2025. However, dual COVID-19/flu options under development could eventually re-shape this indication by bundling respiratory protection into a single seasonal shot, improving adherence and trimming clinic workload.

By Distribution Channel: Public Sector Strength Enables Private Growth

Public procurement sustained 66.12% of global 2025 revenue, anchored by long-running programs such as Vaccines for Children in the United States and bulk tenders in the European Union. These channels guarantee baseline volumes and foster price stability, allowing producers to amortize capital expenditure across large, predictable orders.

Private distribution is projected to rise at a 6.19% CAGR as insurers expand coverage and parents increasingly seek convenience services like same-day vaccination or bundled wellness checks. Market entrants are responding with cloud-based inventory apps and blockchain-authenticated dose tracking; UNICEF-supported VaccineLedger pilots demonstrate how the same platform can serve both public clinics and private paediatricians. Investment flows into software providers such as Canid underscore investor confidence that streamlined workflow tools will further widen access in the pediatric vaccines market.

Geography Analysis

North America controlled 38.72% of global revenue in 2025, buoyed by robust reimbursement systems, stringent school-entry mandates and a continuous stream of FDA approvals such as GSK’s 5-in-1 meningococcal shot and Merck’s VAXNEUVANCE pediatric indication. The region nonetheless grapples with pockets of hesitancy that threaten coverage thresholds, prompting new digital reminder campaigns and pharmacist-administered programs to keep uptake high. The pediatric vaccines market size in North America is further sustained by Project NextGen funding that lowers technological risk for domestic manufacturers developing multi-pathogen candidates.

Asia-Pacific is forecast to post the highest 6.46% CAGR through 2031. Drivers include large birth cohorts, rising disposable incomes and national rollouts such as India’s successful pneumococcal conjugate expansion, which reached 83% booster coverage by 2023. Yet infrastructure gaps and disease resurgence remain pressing challenges; measles surges in Vietnam and neighbouring nations have spurred emergency vaccine stockpiles and fast-track tendering. Regional bodies like APEC have adopted a decade-long plan aiming to vaccinate 23 million children who missed doses during COVID-19 disruptions, signalling persistent momentum for the pediatric vaccines market in fast-growing economies.

Europe retains a sizable share, underpinned by the European Commission’s centralised marketing authorisation process that speeds harmonised access. Recent approval of Pfizer’s PREVENAR 20 offers the broadest pneumococcal serotype coverage yet for infants and adolescents, cementing conjugate uptake across member states. However, budget ceilings in several economies sharpen the focus on value-based procurement, and reimbursement deliberations are increasingly linked to real-world effectiveness data.

The Middle East & Africa and South America present mixed pictures. Several African Union members leverage Gavi co-financing to build indigenous manufacturing under the African Vaccine Manufacturing Accelerator, while Peru and neighbouring markets work to restore routine childhood coverage lost during the pandemic. Overall, heterogeneous funding and infrastructure will keep growth below the global average, yet targeted donor initiatives, technology transfer agreements and cold-chain modernisation point to gradual improvements in the pediatric vaccines market across these regions.

Competitive Landscape

Global supply remains moderately concentrated around GSK, Pfizer, Sanofi and Merck, whose broad portfolios and tendering expertise protect incumbency in high-volume paediatric indications. Patent disputes are intensifying, evidenced by Pfizer’s challenge to three GSK RSV patents, signalling that intellectual-property fences are a pivotal defence as platform convergence blurs product differentiation. Still, the pediatric vaccines market welcomes emerging innovators leveraging cell-free synthesis, self-amplifying RNA and nanoparticle design to outflank serotype coverage limits and cut manufacturing costs.

Technology-led partnerships multiply as established players seek digital and bio-analytic upgrades. Merck’s collaboration with Benchling integrates cloud LIMS into vaccine quality workflows to slash lead times during scale-up, while UNICEF and multiple sovereign funds back blockchain traceability pilots to raise supply-chain transparency. Such alliances lower barriers for region-specific entrants that possess distribution know-how but lack large-molecule R&D capacity.

Regional manufacturers are exploiting compulsory-licence mechanisms and technology-transfer windows to gain share. Bharat Biotech’s rotavirus successes and Serum Institute’s growing conjugate pipeline exemplify how volume-driven pricing power can be achieved outside the Big Four orbit. Meanwhile, Vaxcyte’s 31-valent conjugate ambitions show that venture-backed biotechs can command attention by leapfrogging valency limits with novel chemistries. Together these shifts are gradually pulling competitive intensity upward in the pediatric vaccines market.

Pediatric Vaccines Industry Leaders

-

Sanofi SA

-

Merck & Co., Inc.

-

Pfizer Inc.

-

Sinovac Biotech Ltd.

-

AstraZeneca plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Merck secured FDA approval for Enflonsia, an RSV monoclonal antibody for infants that can be dosed irrespective of weight, enabling July launch ahead of the RSV season.

- March 2025: Bavarian Nordic introduced Vimkunya, the first virus-like particle chikungunya vaccine for individuals ≥ 12 years, showing 97.8% antibody response within 21 days.

- March 2025: The European Commission authorised Pfizer’s PREVENAR 20 covering 20 pneumococcal serotypes for children aged 6 weeks to < 18 years.

- February 2025: GSK received FDA approval for a 5-in-1 meningococcal conjugate vaccine that protects against key serogroups in paediatric populations.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the pediatric vaccines market as all prescription or program-funded immunizations formulated and labeled for birth through fifteen years of age, covering routine schedule shots against bacterial and viral pathogens across public and private channels worldwide. According to Mordor Intelligence, values reflect manufacturer sales translated to end-year USD and exclude bundled pediatric drug lines.

Scope exclusion: Travel-only boosters and emergency COVID-19 pediatric campaigns lie outside this scope.

Segmentation Overview

-

By Vaccine Valence

- Monovalent

- Multivalent

-

By Technology Platform

- Live Attenuated

- Inactivated

- Toxoid

- Conjugate

- Recombinant

- Others

-

By Indication

- DTP (Diphtheria-Tetanus-Pertussis)

- Pneumococcal Disease

- Influenza

- Measles-Mumps-Rubella (MMR)

- Others

-

By Distribution Channel

- Public

- Private

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

-

Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts hold structured calls and short surveys with pediatricians, procurement officers in Africa, state immunization chiefs in the United States, and vaccine distributors across Asia. These discussions confirm schedule changes, typical public-private price gaps, and volume slippage during stock-outs, filling data holes and guiding model adjustments.

Desk Research

We begin by reviewing trusted open sources such as WHO/UNICEF Joint Reporting Forms, CDC National Immunization Survey tables, ECDC uptake dashboards, UN Comtrade HS 3002 trade flows, and World Bank birth-cohort statistics, which anchor baseline dose volumes and prices. Company filings, investor decks, and reputable press updates complement these figures, while D&B Hoovers and Dow Jones Factiva add paid insights on producer splits and fresh tender wins, letting us map supply, demand, and price drift over ten historic years.

Additional literature (peer-reviewed journals on conjugate efficacy, patent filings for next-generation platforms, and health-ministry tender documents) supplies clinical and procurement nuance that shapes scenario assumptions. The sources listed are illustrative; many further references were consulted for data collection, validation, and clarification.

Market-Sizing & Forecasting

We apply a top-down build that starts with live-birth cohorts per country, multiplies them by schedule uptake and recommended dose counts, and layers weighted average selling prices. Supplier roll-ups and targeted channel checks provide bottom-up reasonableness tests before totals are refined. Key variables in our multivariate regression include birth-rate trajectory, Gavi graduation status, dose-wastage trends, pipeline conjugate approvals, and regional funding shifts. When reported prices or uptake lag, gaps are bridged with proxy averages from demographically similar markets.

Data Validation & Update Cycle

Outputs pass peer review, variance flags trigger reruns, and anomalies are rechecked with respondents. Reports refresh annually, with interim updates after material tenders or regulatory actions. Before delivery, an analyst reruns the model so clients receive the latest view.

Why Mordor's Pediatric Vaccines Baseline Proves Dependable

Published estimates often diverge because firms adopt different age cut-offs, revenue recognition points, or refresh cadences, and our disciplined scope keeps numbers aligned with actual procurement flows.

Key gap drivers include providers that fold adolescent booster shots into totals or convert shipment values at static exchange rates while relying on outdated uptake assumptions.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 40.24 B (2025) | Mordor Intelligence | - |

| USD 46.95 B (2025) | Regional Consultancy A | Includes adolescent boosters and counts ex-factory shipments rather than paid doses |

| USD 44.87 B (2023) | Trade Journal B | Older base year, excludes pooled UNICEF/Gavi procurement, uses static FX averages |

The comparison shows our transparent cohort-based logic, validated by on-ground experts, offers a balanced baseline that decision-makers can replicate and trust.

Key Questions Answered in the Report

What is the current pediatric vaccines market size?

The pediatric vaccines market size is USD 42.53 billion in 2026, with expectations to reach USD 56.06 billion by 2031.

Which segment holds the largest pediatric vaccines market share?

Multivalent vaccines hold the largest pediatric vaccines market share at 61.83% in 2025.

Which region is growing fastest in the pediatric vaccines market?

Asia-Pacific is projected to expand at a 6.46% CAGR through 2031, the fastest among all regions.

What technology platform is advancing most quickly?

Recombinant platforms are forecast to grow at 6.31% CAGR, reflecting strong pipeline momentum.

Why are combination vaccines gaining popularity?

They reduce needle burden, improve compliance and lower logistical costs, driving expanded adoption in routine schedules.

How is digital technology reducing vaccine wastage?

Blockchain-based systems such as VaccineLedger improve end-to-end traceability, helping cut the one-in-three wastage rate and saving up to USD 30 billion annually.

Page last updated on: