H1N1 Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 2.24 Billion |

| Market Size (2031) | USD 2.92 Billion |

| Growth Rate (2026 - 2031) | 5.50% CAGR |

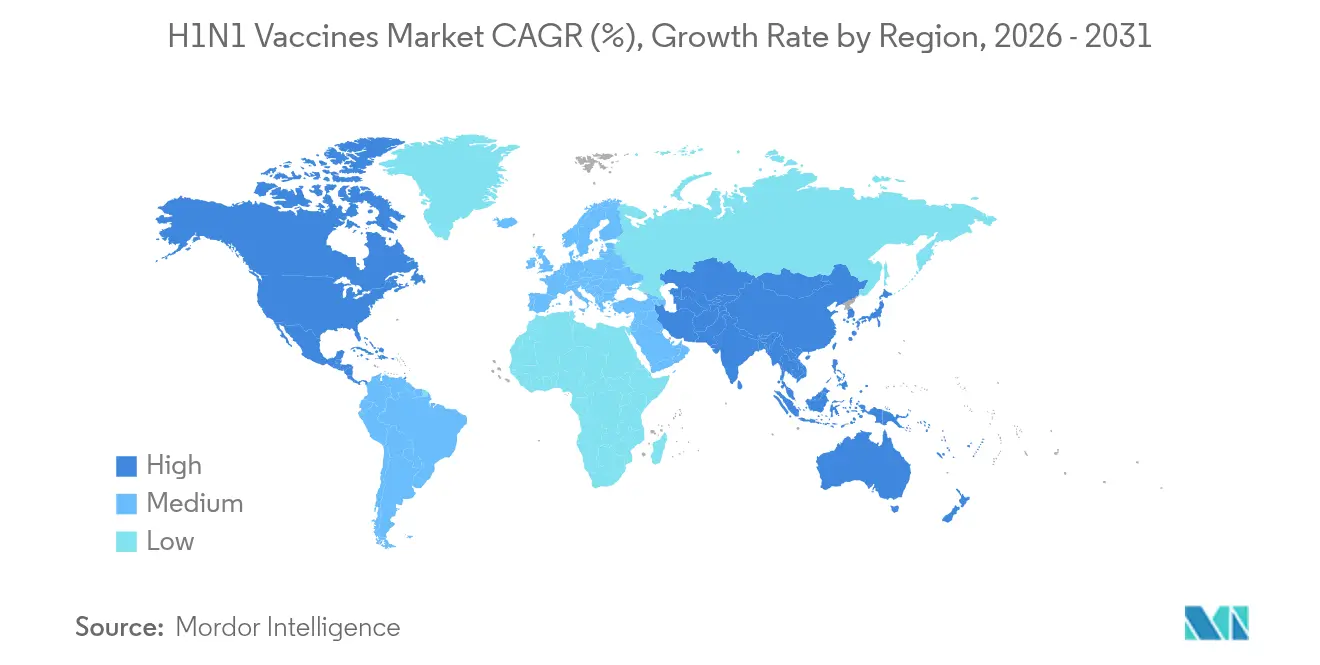

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

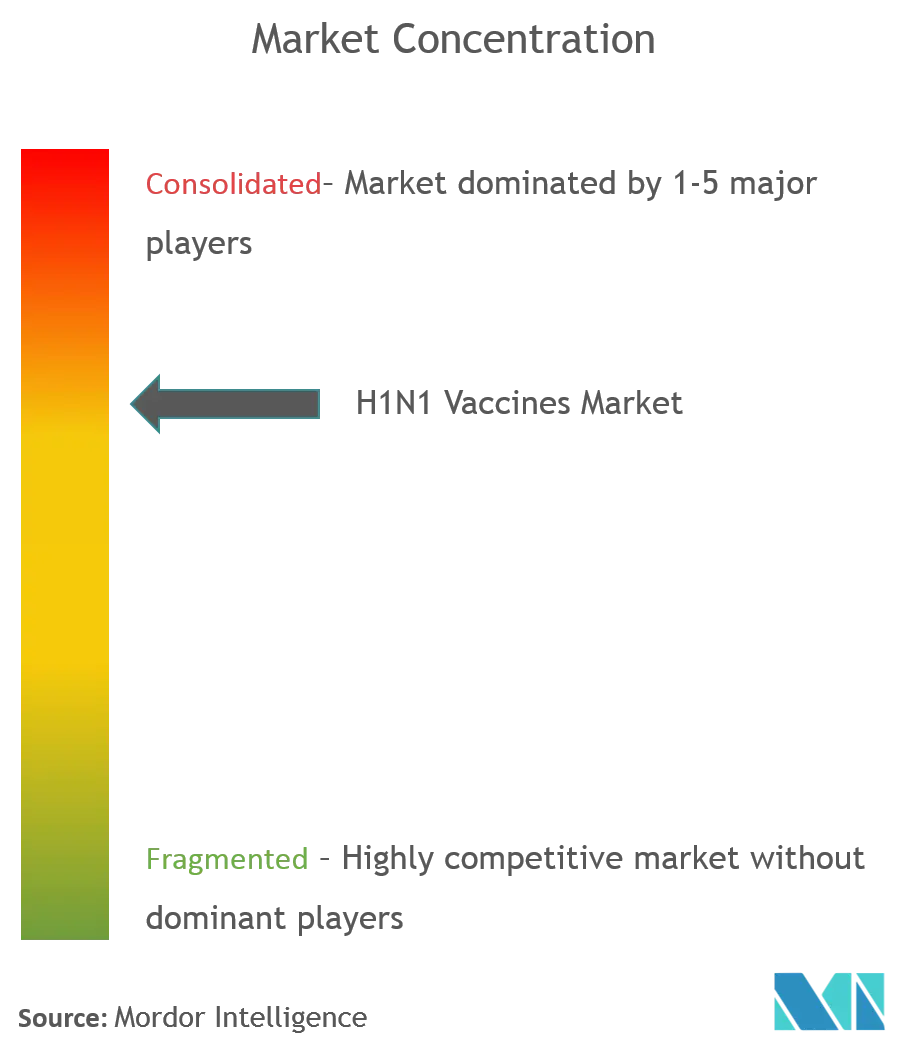

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

H1N1 Vaccines Market Analysis by Mordor Intelligence

H1N1 vaccines market size in 2026 is estimated at USD 2.24 billion, growing from 2025 value of USD 2.12 billion with 2031 projections showing USD 2.92 billion, growing at 5.5% CAGR over 2026-2031. Demand remains resilient because recurring epidemic waves and waning immunity require annual reformulation, while advances in mRNA and recombinant platforms shorten development timelines and improve antigen matching. Government stockpiling mandates tied to expiry-driven replenishment cycles anchor predictable procurement, and investments exceeding USD 2 billion in domestic capacity strengthen surge readiness. Live attenuated and recombinant products are gaining momentum, yet inactivated, egg-based vaccines continue to dominate due to large installed manufacturing bases and well-established safety profiles. Regionally, North America leads on the back of BARDA funding and established distribution networks, while Asia-Pacific posts the fastest growth as manufacturing hubs expand and healthcare budgets rise.

Key Report Takeaways

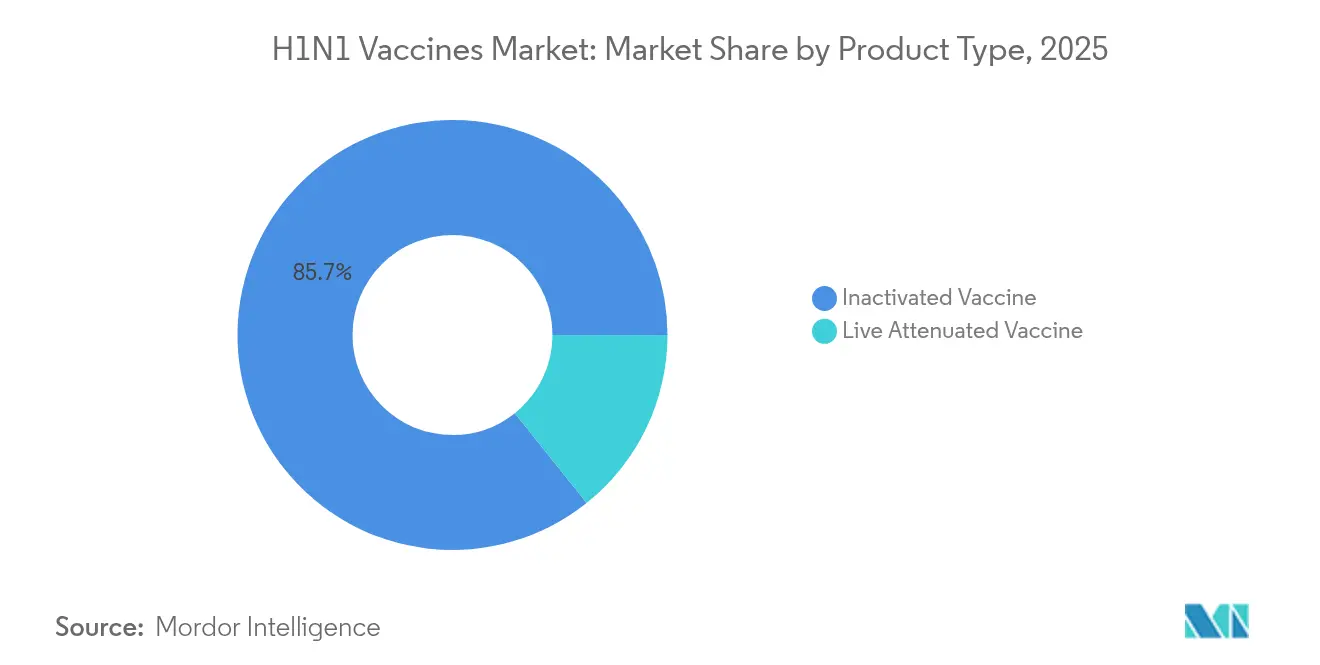

- By product type, inactivated formulations led with an 85.72% share of the H1N1 vaccines market in 2025, while live attenuated products are projected to expand at a 6.05% CAGR to 2031.

- By technology, egg-based production held 74.85% of the H1N1 vaccines market share in 2025; recombinant protein platforms show the highest projected CAGR at 6.02% through 2031.

- By route of administration, intramuscular delivery commanded 64.95% share of the H1N1 vaccines market size in 2025, whereas intradermal delivery is set to rise at a 5.98% CAGR between 2026 and 2031.

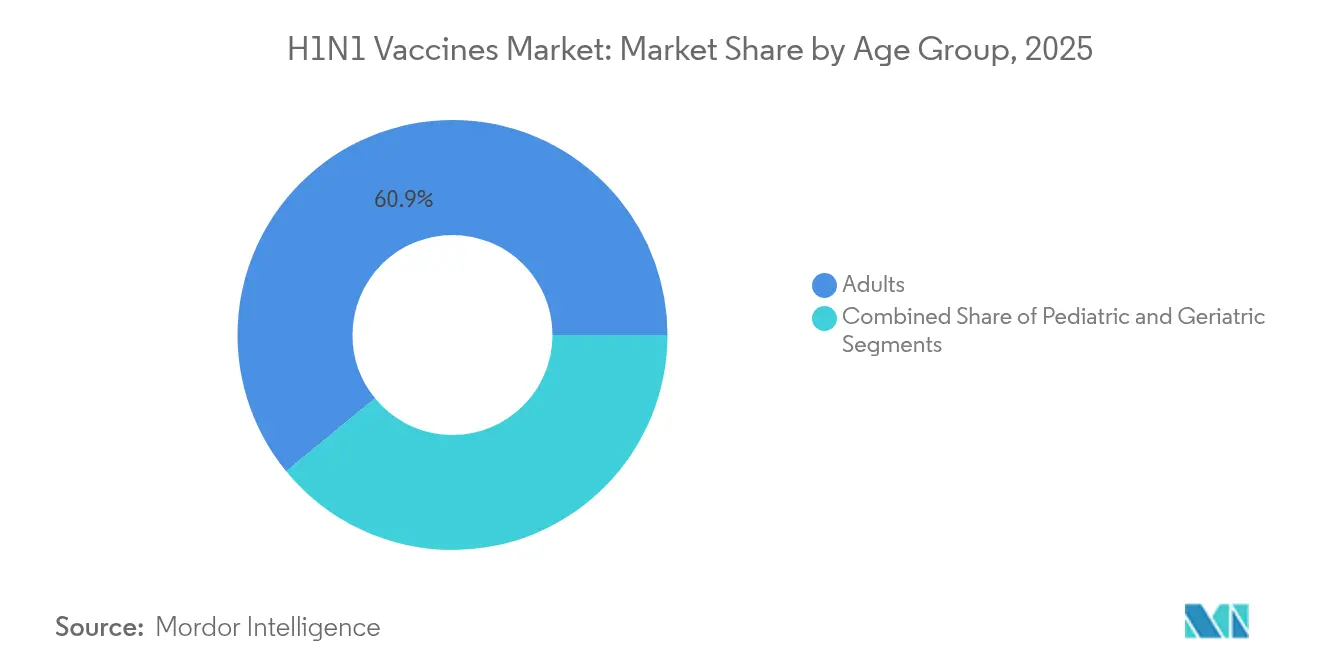

- By age group, adults represented 60.92% of the H1N1 vaccines market size in 2025; pediatric uptake is the fastest-growing at a 6.12% CAGR through 2031.

- By geography, North America captured 40.12% of the H1N1 vaccines market in 2025; Asia-Pacific is advancing at a 6.3% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global H1N1 Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising epidemic H1N1 infection waves & waning immunity | +1.2% | Global, with acute impact in North America and Europe | Medium term (2-4 years) |

| Rapid advances in vaccine platform technologies | +0.9% | Global, led by North America and Europe | Long term (≥ 4 years) |

| Government stockpiling mandates & expiry-driven replenishment cycles | +0.8% | North America, Europe, Asia-Pacific core markets | Short term (≤ 2 years) |

| Expansion of contract fill-finish capacity for surge production | +0.6% | North America and Europe, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Adoption of needle-free micro-array patch delivery in LMICs | +0.4% | Asia-Pacific, Middle East and Africa, South America | Long term (≥ 4 years) |

| Development of influenza–SARS-CoV-2 combo vaccines boosting volumes | +0.7% | Global, early adoption in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Epidemic H1N1 Infection Waves & Waning Immunity

Record hospitalizations during the 2024-2025 season, with influenza A H1N1 as the dominant strain, reaffirm the need for yearly vaccination to prevent healthcare system stress. Vaccine effectiveness slipped to 42% in 2023-2024, highlighting immunity decay that fuels consistent revaccination cycles. Zoonotic spill-over events, such as Vietnam’s swine-origin H1N1 case in August 2024, keep pandemic preparedness on policy agendas [1]World Health Organization, "Influenza A(H1N1) variant virus - Viet Nam," who.int. Variant detections in Brazil and Spain underscore the importance of global surveillance and rapid strain updates. These recurring threats stabilize revenue streams and incentivize platform investments that cut adaptation time.

Rapid Advances in Vaccine Platform Technologies

mRNA, recombinant, and cell-based systems now challenge egg-based dominance. Moderna’s mRNA-1083 Phase 3 data showed stronger immune responses than licensed comparators while enabling refrigerator storage. The U.S. government’s USD 176 million grant for Moderna’s pandemic influenza program demonstrates institutional commitment to next-generation platforms. Cell-based production from CSL Seqirus improved effectiveness across age bands and avoided egg-adaptation drift [2]CSL Seqirus, "CSL Seqirus Presents Data at IDWeek 2024 Highlighting the Urgent Need to Increase Influenza Vaccination Rates and the Benefits of Cell-Based Influenza Vaccines," cslseqirus.us. Recombinant approaches shorten lead times and bypass poultry supply vulnerabilities accentuated by recent H5N1 outbreaks. Early adopters gain agility advantages, prompting legacy players to upgrade or risk erosion.

Government Stockpiling Mandates & Expiry-Driven Replenishment Cycles

Multi-year contracts such as the U.S. pre-pandemic influenza stockpile, valued at more than USD 1.1 billion, secure baseline volumes and support manufacturer cash-flow visibility. The UK’s order for 5 million H5N1 doses from CSL Seqirus and Canada’s purchase of 500,000 Arepanrix doses illustrate the global convergence on proactive stockpiling [3]Government of Canada, "Government of Canada purchases avian influenza vaccine to protect individuals most at risk, " canada.ca. Typical 2-3-year shelf lives trigger routine replacements, smoothing demand even in interpandemic periods. Stockpiles also underpin surge capacity commitments, justifying capital investments in flexible facilities.

Expansion of Contract Fill-Finish Capacity for Surge Production

BARDA’s BioMaP-Consortium and a cumulative USD 2 billion funding stream elevate domestic fill-finish readiness, a historical bottleneck during pandemics. CSL Seqirus’s Holly Springs plant can supply 150 million doses within six months of a pandemic declaration, showcasing next-generation cell-based scale. Supply-chain partners follow suit; Croda International invested USD 133 million in lipid systems for mRNA vaccines, half of which is U.S.-funded, demonstrating ecosystem expansion. These initiatives reinforce resilience and create first-mover advantages for participants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High vaccine cost & reimbursement gaps | -0.8% | Global, acute in emerging markets and uninsured populations | Short term (≤ 2 years) |

| Lengthy, complex manufacturing processes | -0.6% | Global, particularly affecting egg-based production | Medium term (2-4 years) |

| Social-media-driven antivaccine sentiment targeting flu shots | -0.5% | North America and Europe, spill-over to social media connected populations globally | Short term (≤ 2 years) |

| Supply-chain fragility for eggs & cell-culture media during avian outbreaks | -0.4% | Global, acute impact in regions with concentrated poultry production | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Vaccine Cost & Reimbursement Gaps

Adult coverage in India remains only 1.5% despite 21% 2025 growth, showing affordability barriers in emerging economies. The U.S. Medicare 2025 final rule sets a USD 33.71 fee for administration in rural clinics, reflecting ongoing policy work to close payment gaps. Economic models in 88% of LMIC scenarios find vaccination cost-effective, yet budget constraints delay adoption. Private-sector uptake is rising at 6.39% CAGR as employers promote onsite clinics, but premium-priced combination vaccines still struggle for reimbursement. Access challenges slow penetration despite strong clinical value propositions.

Lengthy, Complex Manufacturing Processes

Egg-based systems, supplying over 80% of seasonal doses, need six months of lead time and face avian influenza risks. Production delays compress shipping windows and can result in lost revenue when strain mismatches occur. Outbreaks that decimate poultry stocks expose fragile supply chains, as seen during recent H5N1 events. Cell-based and mRNA alternatives cut timelines but require high capital costs and regulatory adaptation, limiting entry for smaller firms. Maintaining dual platforms raises costs though it also hedges risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Live Attenuated Gains Despite Inactivated Dominance

Inactivated vaccines accounted for 85.72% of the H1N1 vaccines market in 2025, confirming their entrenched role in mass programs built on decades of safety data. Live attenuated formulations, however, post the fastest 6.05% CAGR to 2031 as intranasal delivery and strong mucosal immunity enhance uptake. The Serum Institute’s Nasovac® deployment to more than 2.5 million individuals during the 2009 pandemic validated large-scale live attenuated use. Regulatory alignment with the 2024-2025 move to trivalent compositions affects both product classes equally, pushing manufacturers to refine strain selection without B/Yamagata. Pediatric and needle-phobic adult populations increasingly favor intranasal formats, boosting segment momentum.

Live attenuated manufacturers differentiate by emphasizing convenience and reduced staffing needs, advantageous in low-resource contexts. Post-marketing data confirm favorable safety profiles, encouraging expansion into larger age brackets. Despite regulatory vigilance on reversion risks, the segment’s agility in updating antigens positions it for share gains when rapid response is critical. Consequently, market entrants focusing on intranasal platforms may capture incremental volumes even as inactivated products remain the backbone of seasonal campaigns.

By Technology: Recombinant Platforms Challenge Egg-Based Supremacy

Egg-based production held 74.85% of the H1N1 vaccines market share in 2025, but recombinant platforms are advancing at a 6.02% CAGR through 2031 amid mounting supply-chain and antigenic drift concerns. Recombinant systems avoid egg adaptation, enabling closer antigen fidelity and quicker scale-up. The University at Buffalo’s nanoliposome hexaplex candidate illustrates superior H1N1 protection over current recombinant comparators. Cell-based technologies occupy a middle ground, offering improved effectiveness yet retaining existing regulatory precedents, easing adoption for large producers.

Investment programs from WHO and Gavi are guiding technology transfer to emerging markets, narrowing capacity gaps that threaten equitable pandemic access. Leading recombinant manufacturers leverage flexible single-use bioreactors, contributing to faster changeover between seasons. As evidence grows on improved immunogenicity, payer willingness to reimburse at modest premiums supports a gradual share shift toward recombinant and cell-based candidates.

By Route of Administration: Intradermal Innovation Drives Growth

Intramuscular delivery retained 64.95% share of the H1N1 vaccines market size in 2025 because of well-established protocols and extensive provider training. Intradermal vaccines, expanding at 5.98% CAGR, offer dose-sparing advantages vital during shortages. Studies show equivalent immunity with only 20% of the standard dose, highlighting cost savings during supply constraints. Micron Biomedical’s BARDA-funded dissolvable microarray patch exemplifies next-generation intradermal platforms poised for LMIC deployment.

Intranasal administration remains niche but essential for live attenuated products, appealing to pediatric segments and individuals with needle aversion. Innovations in dry powder intranasal formulations aim to extend shelf life without cold chain, broadening access in remote regions. Together, diverse administration routes allow health systems to tailor delivery based on infrastructure and population needs.

By Age Group: Pediatric Segment Accelerates Despite Coverage Challenges

Adults commanded 60.92% of the H1N1 vaccines market size in 2025, yet pediatric doses are expanding at 6.12% CAGR through 2031. Despite declining U.S. child coverage to 46% in 2024-2025, growing evidence of 77% effectiveness in children aged 6-59 months underscores clinical benefit. Policymakers and pediatric societies continue recommending universal vaccination starting at six months, pushing health systems to enhance outreach.

Manufacturers increasingly design age-tailored formulations, such as reduced-antigen live attenuated products for toddlers, to improve tolerability. Digital reminder tools and school-based clinics aim to reverse coverage declines. The pediatric segment’s long-run growth rests on building confidence through transparent safety data and user-friendly delivery, areas that live attenuated and intradermal technologies can address.

By Distribution Channel: Private Sector Momentum Builds

Public procurement accounted for 69.25% of the H1N1 vaccines market in 2025, anchored by national immunization programs and defense stockpiles. Private channels, expanding at 6.18% CAGR, benefit from employer mandates, retail pharmacy convenience, and consumer preference for premium combination shots. Regulatory adjustments allowing same-day reimbursement in Rural Health Clinics improve cash flow, encouraging provider participation.

Retail chains leverage extended hours and online appointment platforms to capture busy urban consumers. Bulk purchasing agreements help maintain competitive pricing even for high-value combo vaccines. As health insurers seek cost-effective preventive offerings, partnerships with pharmacies and urgent-care centers are broadening private-sector access.

Geography Analysis

North America led the H1N1 vaccines market with a 40.12% share in 2025. The region benefits from BARDA contracts exceeding USD 2 billion that support capacity expansion, including CSL Seqirus’s Holly Springs plant capable of producing 150 million doses within six months. FDA fast-track designations for combination vaccines accelerate approvals, and recent USD 176 million federal funding for Moderna’s mRNA program signals sustained commitment to technological leadership. Nevertheless, declining uptake among seniors and children challenges public health targets, prompting renewed educational campaigns.

Asia-Pacific is the fastest-growing region at a 6.3% CAGR, propelled by local manufacturing investments and heightened urban health awareness. India’s 2025 influenza market expanded 21%, though only 1.5% of adults aged 45+ were vaccinated, indicating vast latent potential. The Serum Institute can scale output from 300,000 to beyond 1 million doses, showcasing regional production scalability. China is gradually recognizing foreign clinical data to expedite approvals, while South Korea’s active surveillance demonstrates regulatory maturity.

Europe represents a mature but innovative market. EMA guidance released in January 2025 streamlines updated strain approvals, cutting administrative lead times. The UK’s purchase of 5 million pandemic doses underscores ongoing preparedness, and EU cohesion funds back cross-border capacity investments. While growth is slower than in emerging regions, demand for combination and high-dose products sustains revenue.

Competitive Landscape

The market exhibits moderate concentration as vertically integrated leaders leverage manufacturing scale and tendering expertise. Sanofi quickly adopted FDA-selected 2025-2026 strains for FLUZONE, FLUBLOK, and FLUZONE High-Dose lines, illustrating agility in updating portfolios. GSK’s 4% vaccine revenue decline in 2024 revealed vulnerability to shifting product mixes, spurring pipeline refocus on adjuvanted formulations. CSL Seqirus consolidates egg-based and cell-based assets to serve public stockpiles and seasonal markets, while its fill-finish agreements with BARDA lock in pandemic surge volumes.

Disruptors are carving niches via mRNA, microarray patches, and universal antigens. Moderna’s mRNA-1083 showed superior immunogenicity in Phase 3 and is positioned for 2026 filing, potentially reshaping adult booster dynamics. Micron Biomedical’s dissolvable patches could extend access to remote geographies once scalability and regulatory hurdles are cleared. Smaller biotech firms focus on nucleoprotein antigens for broader cross-strain coverage, hoping to secure targeted contracts or licensing deals with larger manufacturers.

Strategic collaborations are intensifying. Sanofi and Novavax co-develop a combination flu-COVID program to hedge against seasonality swings. Contract manufacturing organizations are scaling lipid nanoparticle supply, vital for mRNA partners. As health authorities emphasize resilience, suppliers that demonstrate platform flexibility and secure supply chains are favored in competitive tenders, reinforcing consolidation trends.

H1N1 Vaccines Industry Leaders

-

AstraZeneca Plc

-

Sanofi (Sanofi Pasteur AG)

-

GlaxoSmithKline Plc

-

CSL Limited (Seqirus GmbH)

-

Pfizer Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: The U.S. Department of Health and Human Services and the National Institutes for Health announced the Generation Gold Standard universal vaccine platform using BPL-inactivated whole virus.

- March 2025: Sanofi adopted FDA-selected influenza strains for the 2025-2026 season and increased output of FLUZONE, FLUBLOK, and FLUZONE High-Dose vaccines.

- March 2025: The FDA issued virus-strain recommendations for 2025-2026 U.S. flu vaccines covering egg-based, cell-based, and recombinant formulations.

- January 2025: Micron Biomedical received a USD 2 million BARDA award to develop a needle-free mRNA influenza vaccine using dissolvable microarray technology.

Global H1N1 Vaccines Market Report Scope

The H1N1 virus, commonly known as swine flu is an infectious disease in humans caused by the swine H1N1 virus, which is characterized by a persistent cough, cold, high fever, red watery eyes, body aches, headache, and general discomfort. H1N1 Vaccines Market is segmented By Product Type, By Route of Administration and Geography.

| Inactivated Vaccine |

| Live Attenuated Vaccine |

| Egg-based |

| Cell-based |

| Recombinant |

| Intradermal |

| Intramuscular |

| Intranasal |

| Pediatric |

| Adult |

| Geriatric |

| Public |

| Private |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Inactivated Vaccine | |

| Live Attenuated Vaccine | ||

| By Technology | Egg-based | |

| Cell-based | ||

| Recombinant | ||

| By Route of Administration | Intradermal | |

| Intramuscular | ||

| Intranasal | ||

| By Age Group | Pediatric | |

| Adult | ||

| Geriatric | ||

| By Distribution Channel | Public | |

| Private | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the H1N1 vaccines market?

The H1N1 vaccines market stands at USD 2.24 billion in 2026 and is projected to reach USD 2.92 billion by 2031.

Which product type dominates the H1N1 vaccines market?

Inactivated formulations dominate, holding 85.72% market share in 2025, although live attenuated products are growing fastest at a 6.05% CAGR.

Why is Asia-Pacific the fastest-growing region?

Asia-Pacific benefits from expanding local manufacturing, rising healthcare expenditure, and large unvaccinated populations, driving a 6.3% CAGR to 2031.

How are mRNA platforms impacting competition?

MRNA platforms enable quicker strain adaptation and higher immunogenicity, allowing companies like Moderna to challenge traditional egg-based leaders.

What are the main restraints on market growth?

High vaccine costs with reimbursement gaps and lengthy egg-based manufacturing processes slow wider adoption, especially in low-income settings.

Page last updated on: