Therapeutic Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

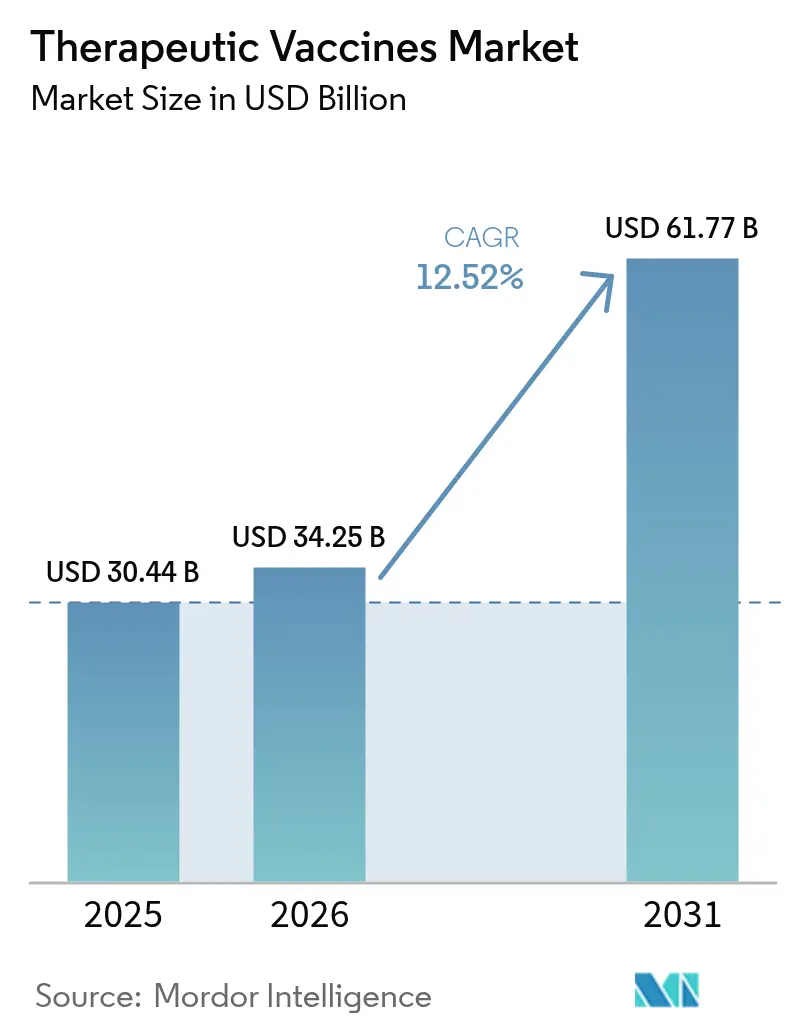

| Market Size (2026) | USD 34.25 Billion |

| Market Size (2031) | USD 61.77 Billion |

| Growth Rate (2026 - 2031) | 12.52% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Therapeutic Vaccines Market Analysis by Mordor Intelligence

The therapeutic vaccines market size is projected to expand from USD 30.44 billion in 2025 and USD 34.25 billion in 2026 to USD 61.77 billion by 2031, registering a CAGR of 12.52% between 2026 and 2031. Solid demand pivots from prophylactic immunization to active immunotherapy as stakeholders pursue treatments that mobilize a patient’s own defenses against established disease. Cancer programs captured the largest revenue, yet neurological disease pipelines are accelerating on the back of Phase II read-outs in Alzheimer’s and Parkinson’s cohorts. Tightened regulatory scrutiny surfaced in February 2026 when FDA issued a complete response letter for Moderna’s seasonal influenza mRNA vaccine, a decision that underscores higher evidentiary standards for all therapeutic vaccine modalities.

Key Report Takeaways

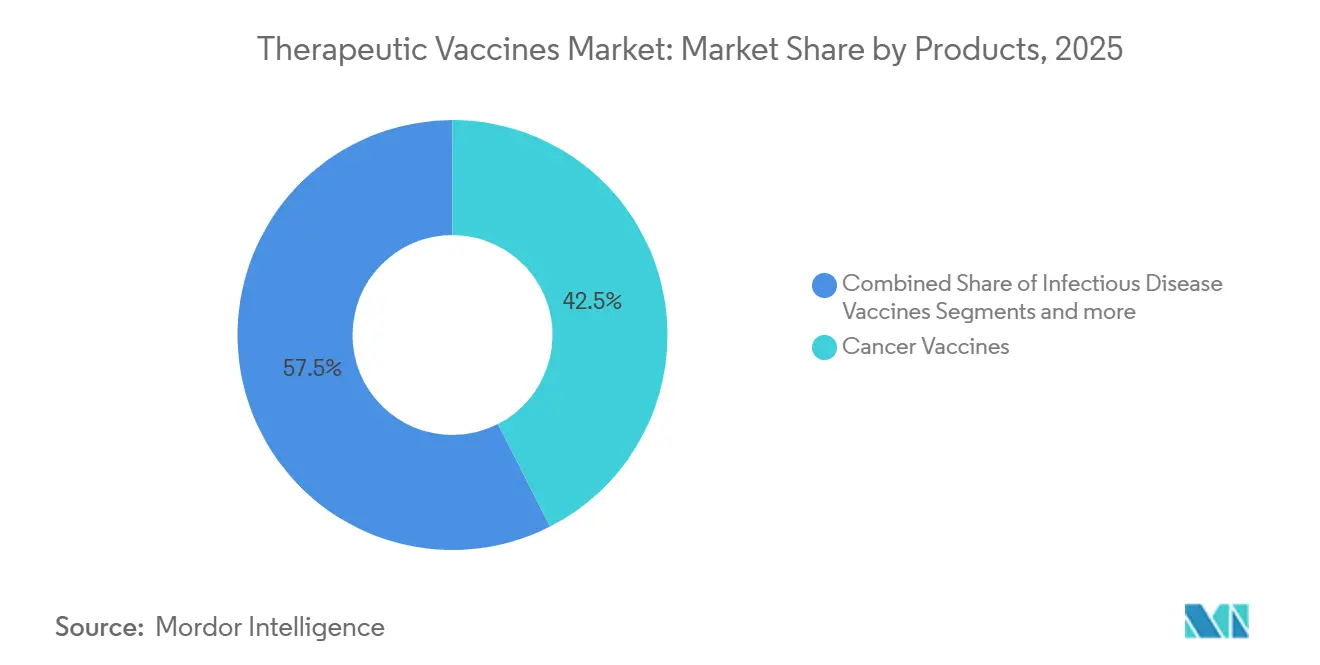

- By product category, cancer vaccines led with 42.55% therapeutic vaccines market share in 2025. Neurological disease vaccines are forecast to advance at a 15.85% CAGR through 2031.

- By technology, allogeneic constructs held 55.53% therapeutic vaccines market size in 2025, while autologous platforms are projected to post a 16.75% CAGR to 2031.

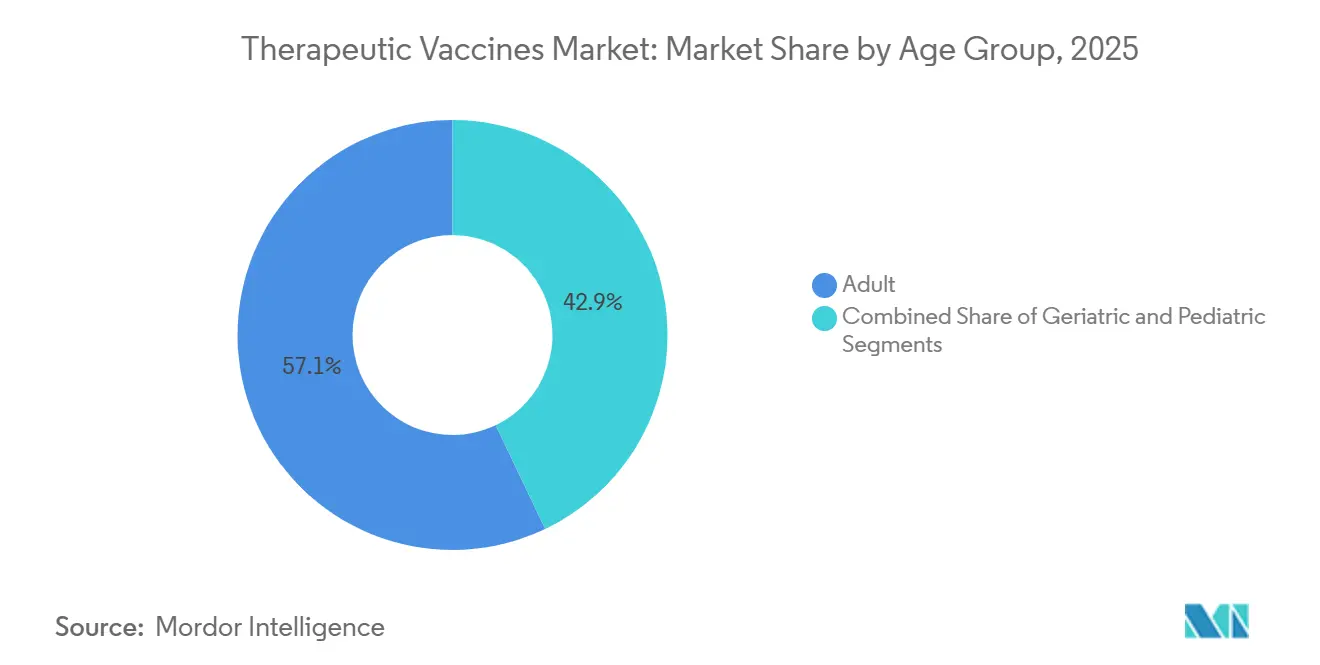

- By age group, geriatric applications are expected to rise at a 13.82% CAGR between 2026 and 2031, outpacing the adult cohort.

- By distribution channel, private outlets are advancing at a 13.12% CAGR through 2031 despite public systems retaining 64.52% of 2025 sales.

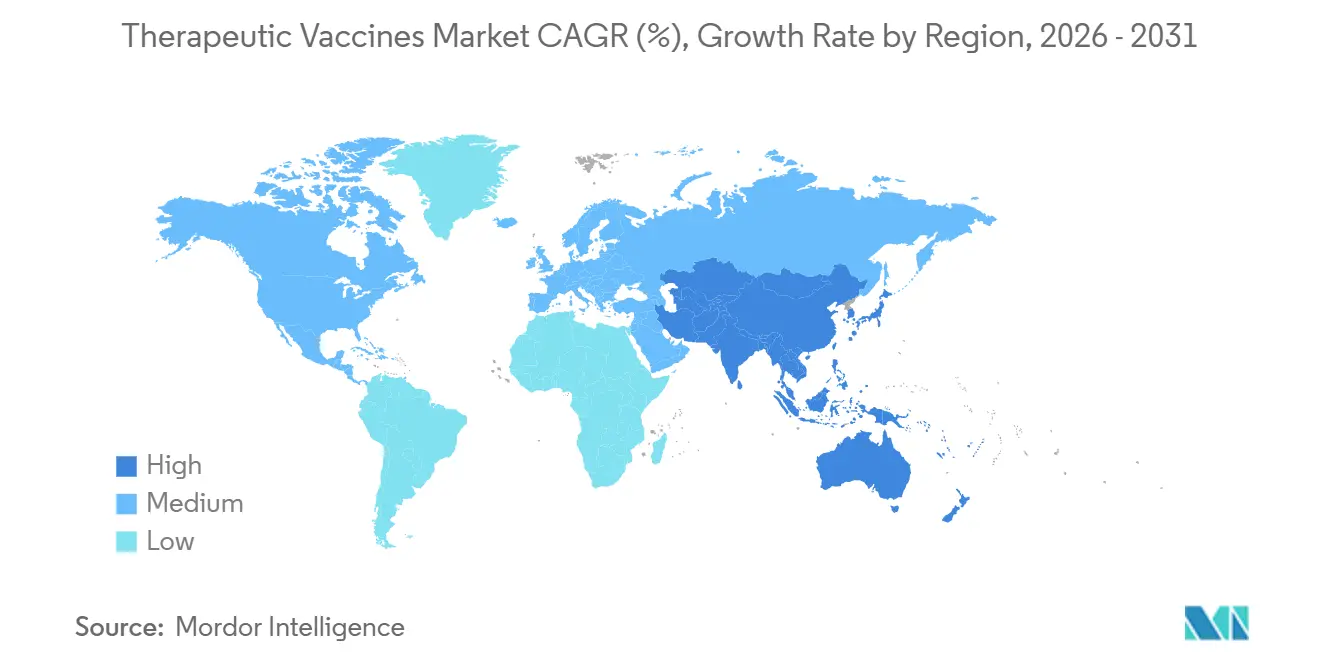

- By geography, Asia-Pacific is set to record the fastest 13.72% CAGR through 2031, although North America commanded 42.55% revenue in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Therapeutic Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Prevalence of Chronic & Infectious Diseases | +2.8% | Global with acute burden in Asia-Pacific and Sub-Saharan Africa | Long term (≥ 4 years) |

| Government Funding Intensification for Vaccine R&D | +1.9% | North America, Europe, China | Medium term (2-4 years) |

| Pharma/Biotech Surge in Oncology Vaccine Pipelines | +3.2% | North America, Europe, Asia-Pacific | Long term (≥ 4 years) |

| Breakthrough Approvals of mRNA-Based Therapeutic Vaccines | +2.4% | North America, Europe | Short term (≤ 2 years) |

| AI-Driven Neoantigen Discovery Accelerating Personalization | +1.6% | North America, Europe, China | Medium term (2-4 years) |

| On-Site Modular Micro-Factory Manufacturing Models | +1.1% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Chronic & Infectious Diseases

Therapeutic vaccines have moved to the center of multimodal care as chronic conditions coexist with infectious outbreaks. WHO’s 2024 Global Health Estimates found non-communicable diseases responsible for 74% of worldwide deaths, a statistic that amplifies oncology and cardiometabolic vaccine demand. Concurrently, global cancer incidence is projected to top 30 million new cases annually by 2030, intensifying the hunt for individualized neoantigen vaccines that target patient-specific mutations[1]International Agency for Research on Cancer, “Global Cancer Statistics 2024,” iarc.who.int. Infectious-disease candidates now pursue functional cures in HIV and shortened regimens in tuberculosis, broadening the therapeutic vaccines market beyond oncology.

Government Funding Intensification for Vaccine R&D

Project NextGen allocated USD 5 billion in 2024 to advance next-generation COVID-19 countermeasures and spin-off technologies, yet BARDA’s August 2025 cancellation of USD 500 million in mRNA contracts indicates that future disbursements will hinge on multipurpose clinical value. In China, expedited pathways for domestic cancer vaccines have unlocked fresh capital, while Horizon Europe grants continue to support mRNA and viral-vector platforms. These region-specific policies collectively expand the therapeutic vaccines market, though sponsors must still deliver compelling cost-effectiveness dossiers to secure reimbursement.

Pharma/Biotech Surge in Oncology Vaccine Pipelines

Global pipelines grew by 40% between 2023 and 2025 as checkpoint inhibitor revenues plateaued. High-profile data such as Moderna and Merck’s KEYNOTE-942 study, which showed a 44% recurrence-risk reduction with mRNA-4157 plus pembrolizumab, validate a combination-driven strategy and reinforce the centrality of therapeutic vaccines market participants in oncology care.

Breakthrough Approvals of mRNA-Based Therapeutic Vaccines

EMA’s February 2025 clearance of Kostaive, a self-amplifying RNA product, signaled European openness to next-gen formulations[2]European Medicines Agency, “EMA Authorizes Kostaive,” ema.europa.eu. Yet FDA’s 2026 rejection of a seasonal flu mRNA candidate reminds sponsors that therapeutic vaccines market authorization rests on nuanced risk-benefit calculus.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensive, High-Risk Clinical Development Cycle | -2.1% | Global, acute in emerging markets | Long term (≥ 4 years) |

| Stringent Multi-Jurisdictional Regulatory Hurdles | -1.4% | North America, Europe, Japan | Medium term (2-4 years) |

| Shortage of GMP Viral-Vector/Plasmid Capacity | -1.8% | Global bottleneck in North America and Europe | Short term (≤ 2 years) |

| Late-Stage I-O Trial Failures Dampening Investor Sentiment | -1.3% | Global with focus on North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive, High-Risk Clinical Development Cycle

End-to-end expenses reach USD 200-500 million per candidate, while success odds linger below 10%. Personalized neoantigen trials add USD 150,000 per patient in sequencing and bespoke GMP costs. Emerging-market innovators often license out assets to deep-pocketed partners, a dynamic that curtails independent commercialization and tempers growth in the therapeutic vaccines market.

Stringent Multi-Jurisdictional Regulatory Hurdles

Divergent agency views widen launch timelines. FDA’s refusal of Moderna’s flu mRNA product contrasted with EMA’s friendlier stance toward similar technologies, highlighting costly duplications in clinical evidence requirements. Separate HTA reviews across Europe further delay uptake.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Products: Oncology Dominates, Neurology Surges

Cancer vaccines held 42.55% therapeutic vaccines market share in 2025, buoyed by combination regimens that prolong progression-free survival. Neurological disease vaccines are projected to clock a 15.85% CAGR to 2031, supported by mid-stage trials of ACI-24.060 and UB-612 that target Alzheimer’s pathology.

Autoimmune and advanced infectious-disease candidates add diversification but remain earlier in development, constrained by the need to demonstrate antigen-specific tolerance without compromising systemic immunity. Regulatory requirements differ by indication. Oncology programs often leverage surrogate endpoints such as recurrence-free survival, whereas neurological applications must showcase multi-year cognitive maintenance, a higher evidentiary bar that slows approval yet could deliver large-scale value once met.

By Technology: Allogeneic Scale Versus Autologous Precision

Allogeneic formulations generated 55.53% of 2025 revenue thanks to batch economies and rapid distribution. Autologous constructs are set to expand at a 16.75% CAGR through 2031 as AI accelerates neoantigen discovery, shrinking manufacturing cycles to 30-60 days and widening clinical eligibility.

Efficacy divides the two modalities. Allogeneic programs rarely exceed 30% objective response rates, whereas autologous vaccines cross 40% in melanoma and non-small cell lung cancer, a gap that justifies higher production costs among payers keen on durable outcomes.

By Age Group: Adult Dominance, Geriatric Acceleration

Adults represented 57.15% of consumption in 2025, but geriatric cohorts are forecast to grow at 13.82% CAGR as adjuvant advances counter immunosenescence. Added demand for senior-focused dosing regimens and safety monitoring drives innovation across the therapeutic vaccines market.

By Distribution Channel: Public Infrastructure, Private Velocity

Government channels delivered 64.52% of 2025 revenue, yet private settings are advancing at a 13.12% CAGR amid high-net-worth demand for custom oncology regimens. Medicare’s narrow coverage has nudged some U.S. patients toward self-pay models, a pattern mirrored by European price-effectiveness thresholds.

Geography Analysis

North America led with 42.55% share in 2025, propelled by FDA fast-track designations and concentrated venture backing. Europe follows, leveraging centralized EMA approvals but facing post-authorization pricing delays. Asia-Pacific is the fastest growing therapeutic vaccines market, advancing 13.72% CAGR through 2031 as China streamlines approvals and India attracts lower-cost pivotal trials[3]National Medical Products Administration China, “Therapeutic Vaccine Approvals 2024-2025,” nmpa.gov.cn. Japan’s local safety data requirements add 18-24 months to launch cycles but ensure age-tailored protocols for its sizable elderly population.

Latin America, the Middle East, and Africa collectively remain small contributors but display rising interest as expedited reliance pathways let regulators lean on FDA or EMA decisions while domestic sponsors pursue technology transfers.

Competitive Landscape

Competition remains moderate. BioNTech and Moderna exploit pandemic-era mRNA scale to dominate individualized pipelines, yet smaller biotechs fill gaps in viral-vector and DNA constructs. Platform alliances abound—BioNTech has inked deals with Regeneron, OncoC4, DualityBio, and Genmab to integrate BNT122 into antibody combinations. AI-native entrants such as Gritstone and NEC capture mindshare by collapsing neoantigen design timelines from months to weeks. Technology, not sheer volume, now defines edge: autologous leaders race to 30-day manufacturing windows, while allogeneic suppliers widen epitope breadth to improve response rates.

Therapeutic Vaccines Industry Leaders

Merck & Co., Inc.

GSK plc

Pfizer Inc.

Sanofi SA

Moderna Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Anixa Biosciences presented final Phase 1 data on its investigational breast cancer vaccine at SABCS.

- July 2025: Helmholtz Munich and DZIF launched the first clinical trial of TherVacB, a therapeutic vaccine for chronic hepatitis B.

Global Therapeutic Vaccines Market Report Scope

As per the scope of the report, a therapeutic vaccine is applied after an infection or disease occurs in order to induce antiviral immunity and alter the course of the disease. Therapeutic vaccines are used to cure diseases because, rather than immunizing for future disease protection, they work with the patient's own immune system to fight infection.

The segmentation for the therapeutic vaccines market is categorized by products, technology, age group, distribution channel, and geography. By products, the market includes vaccines for autoimmune diseases, vaccines for neurological disorders, oncology vaccines, vaccines for infectious diseases, and miscellaneous products. By technology, it is segmented into allogeneic vaccines and autologous vaccines. By age group, the market is divided into adults, children, and seniors. By distribution channel, it is classified into the public sector and the private sector. By geography, the market covers North America, Europe, Asia-Pacific, the Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions globally. The report offers the value (in USD) for the above segments.

| Autoimmune Disease Vaccines |

| Neurological Disease Vaccines |

| Cancer Vaccines |

| Infectious Disease Vaccines |

| Other Products |

| Allogeneic Vaccines |

| Autologous Vaccines |

| Adult |

| Pediatric |

| Geriatric |

| Public |

| Private |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Products | Autoimmune Disease Vaccines | |

| Neurological Disease Vaccines | ||

| Cancer Vaccines | ||

| Infectious Disease Vaccines | ||

| Other Products | ||

| By Technology | Allogeneic Vaccines | |

| Autologous Vaccines | ||

| By Age Group | Adult | |

| Pediatric | ||

| Geriatric | ||

| By Distribution Channel | Public | |

| Private | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the therapeutic vaccines market expected to become by 2031?

It is projected to reach USD 61.77 billion by 2031, growing at a 12.52% CAGR from 2026.

Which therapeutic vaccine product category currently leads sales?

Cancer vaccines led with 42.55% share in 2025 and remain the main revenue driver through the forecast period.

What is driving rapid growth in Asia-Pacific?

Streamlined Chinese approvals and India's lower clinical trial costs help the region post a 13.72% CAGR through 2031.

Why are autologous vaccines gaining traction despite higher costs?

AI-enabled neoantigen discovery has cut manufacturing lead-times to 30-60 days, while response rates often exceed 40% in solid tumors.

How did FDA's 2026 decision affect market sentiment?

The refusal of a seasonal flu mRNA vaccine underscored stricter efficacy expectations, prompting sponsors to refine evidence packages.

What role do private distribution channels play?

Private clinics and concierge oncology centers are expanding at a 13.12% CAGR as high-net-worth patients self-fund personalized regimens.

Page last updated on: