Plant-Based Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

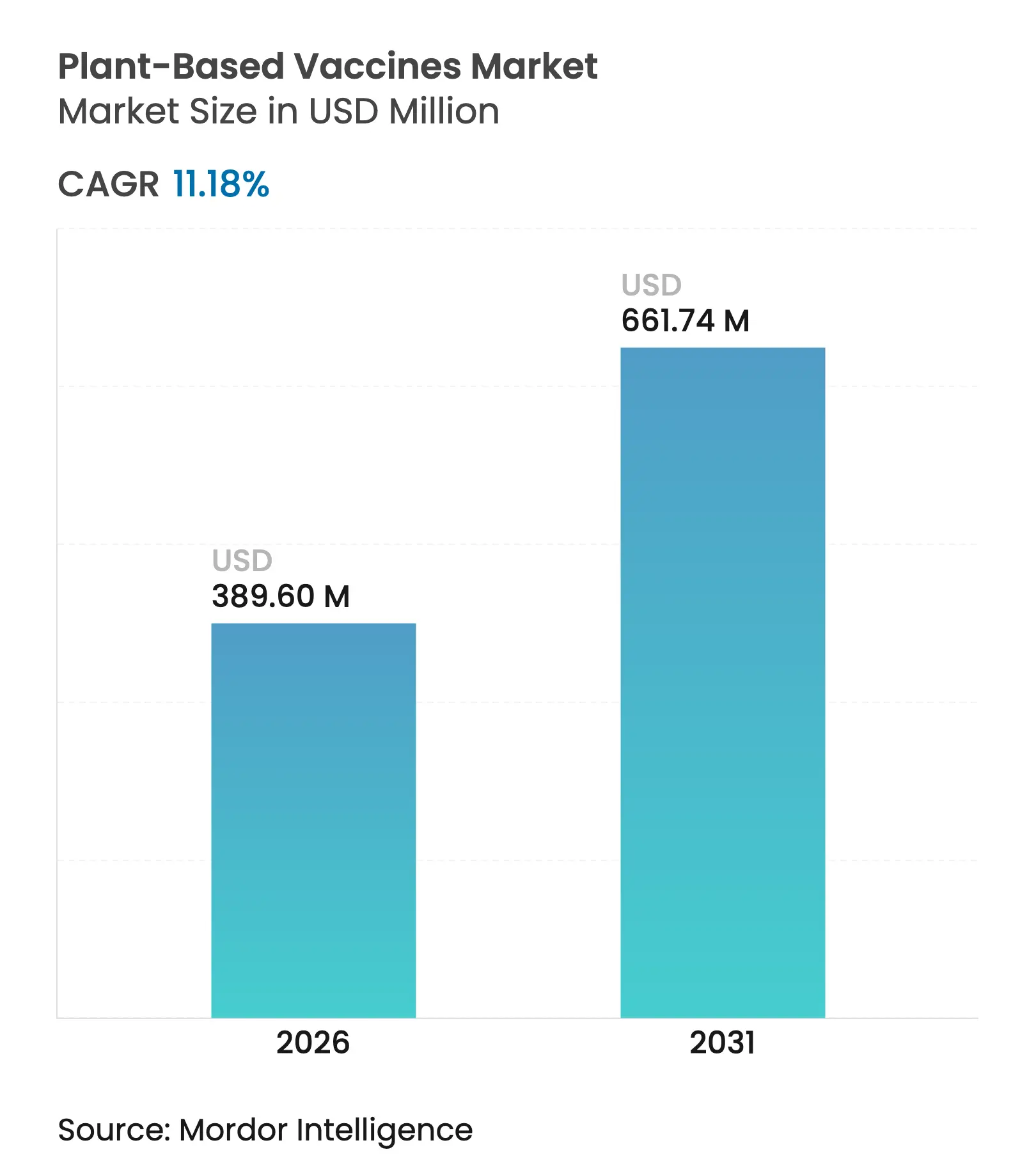

| Market Size (2026) | USD 389.6 Million |

| Market Size (2031) | USD 661.74 Million |

| Growth Rate (2026 - 2031) | 11.18 % CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Plant-Based Vaccines Market Analysis by Mordor Intelligence

Plant-based vaccines market size in 2026 is estimated at USD 389.6 million, growing from 2025 value of USD 350.44 million with 2031 projections showing USD 661.74 million, growing at 11.18% CAGR over 2026-2031. This rapid trajectory signals that plant-derived platforms are becoming a cornerstone of pandemic-response strategies as governments look for manufacturing technologies that can bypass egg-based and mammalian cell bottlenecks. Substantial public funding—in particular the USD 5 billion Project NextGen program and the USD 79.5 billion PHEMCE multi-year budget—continues to de-risk private investment, while patent expiries on legacy vaccines lower the competitive bar for newcomers [1]U.S. Department of Health and Human Services, “Project NextGen Factsheet,” hhs.gov. The plant-based vaccines market is also benefiting from next-generation chloroplast-expression methods that raise antigen yields, making commercial-scale output achievable even for smaller developers. Growing interest in edible formulations for low- and middle-income countries, combined with a wave of licensing agreements that knit together research hubs in North America, Europe and Asia-Pacific, further supports sustained double-digit growth.

Key Report Takeaways

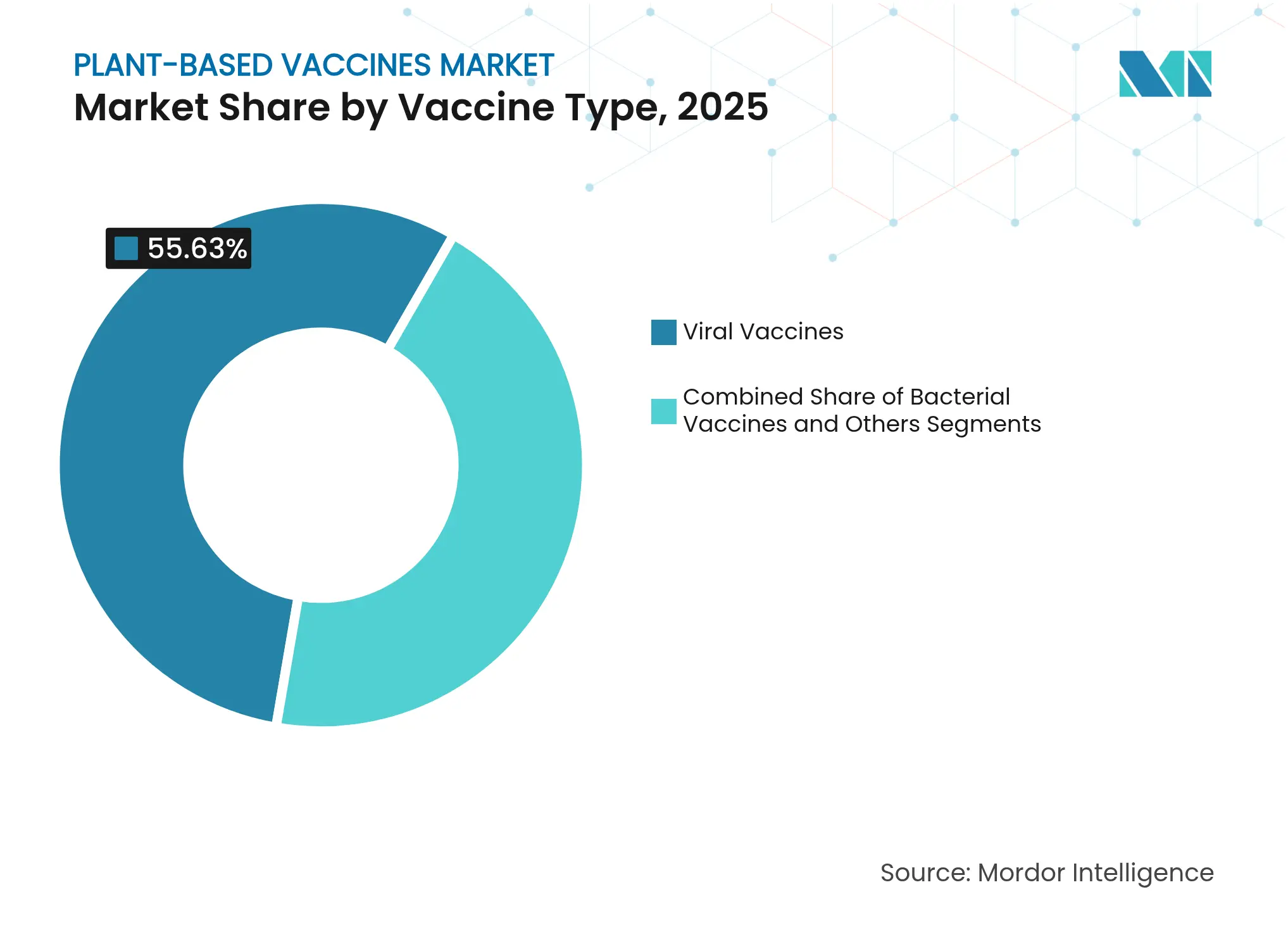

- By vaccine type, viral vaccines led with 55.63% of plant-based vaccines market share in 2025, while bacterial vaccines are projected to expand at a 11.83% CAGR through 2031.

- By plant source, tobacco systems held 61.88% of the plant-based vaccines market size in 2025; potato platforms are expected to post a 11.95% CAGR to 2031.

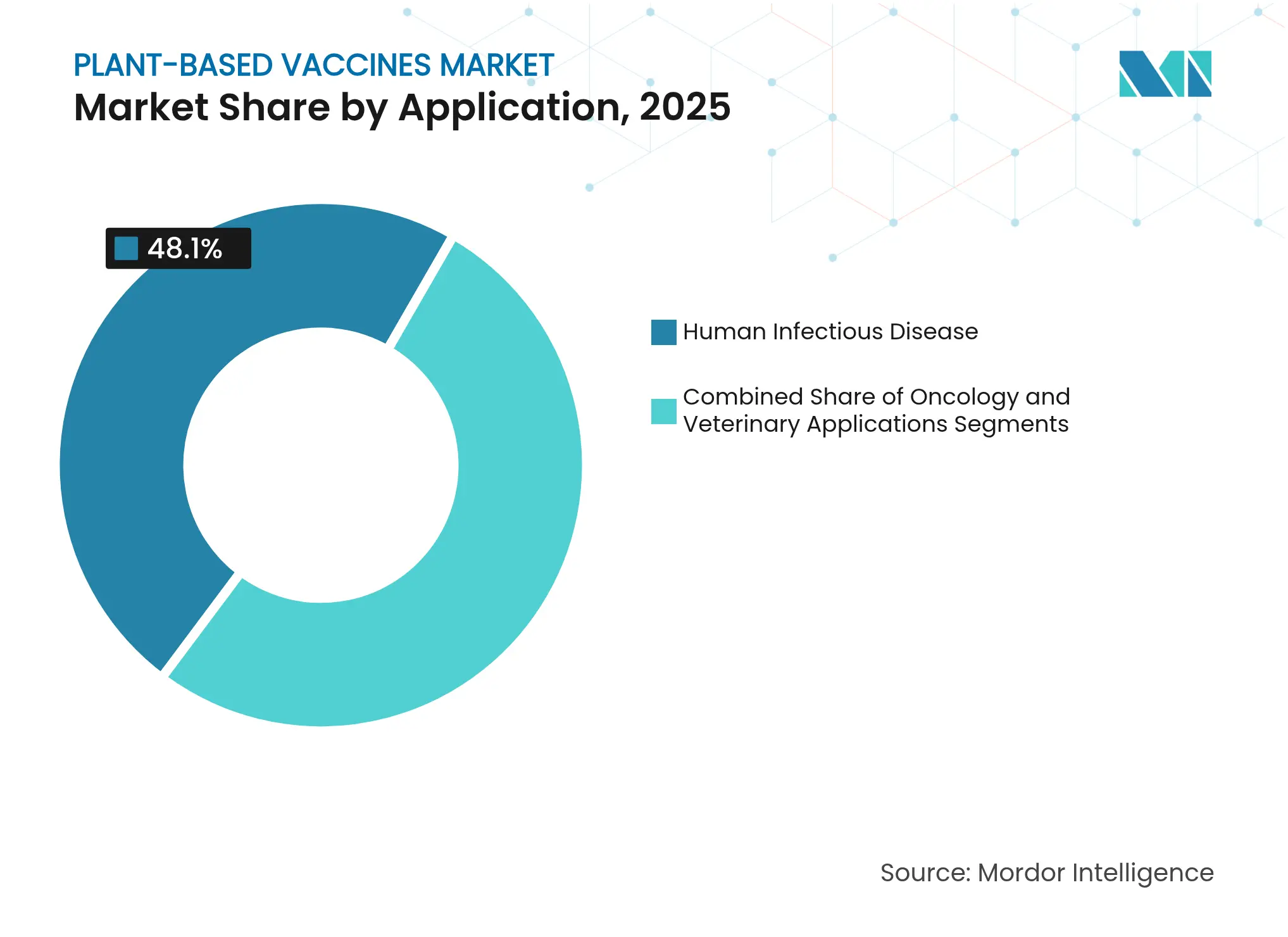

- By application, human infectious-disease products commanded 48.10% of revenue in 2025, whereas oncology candidates are advancing at a 12.08% CAGR.

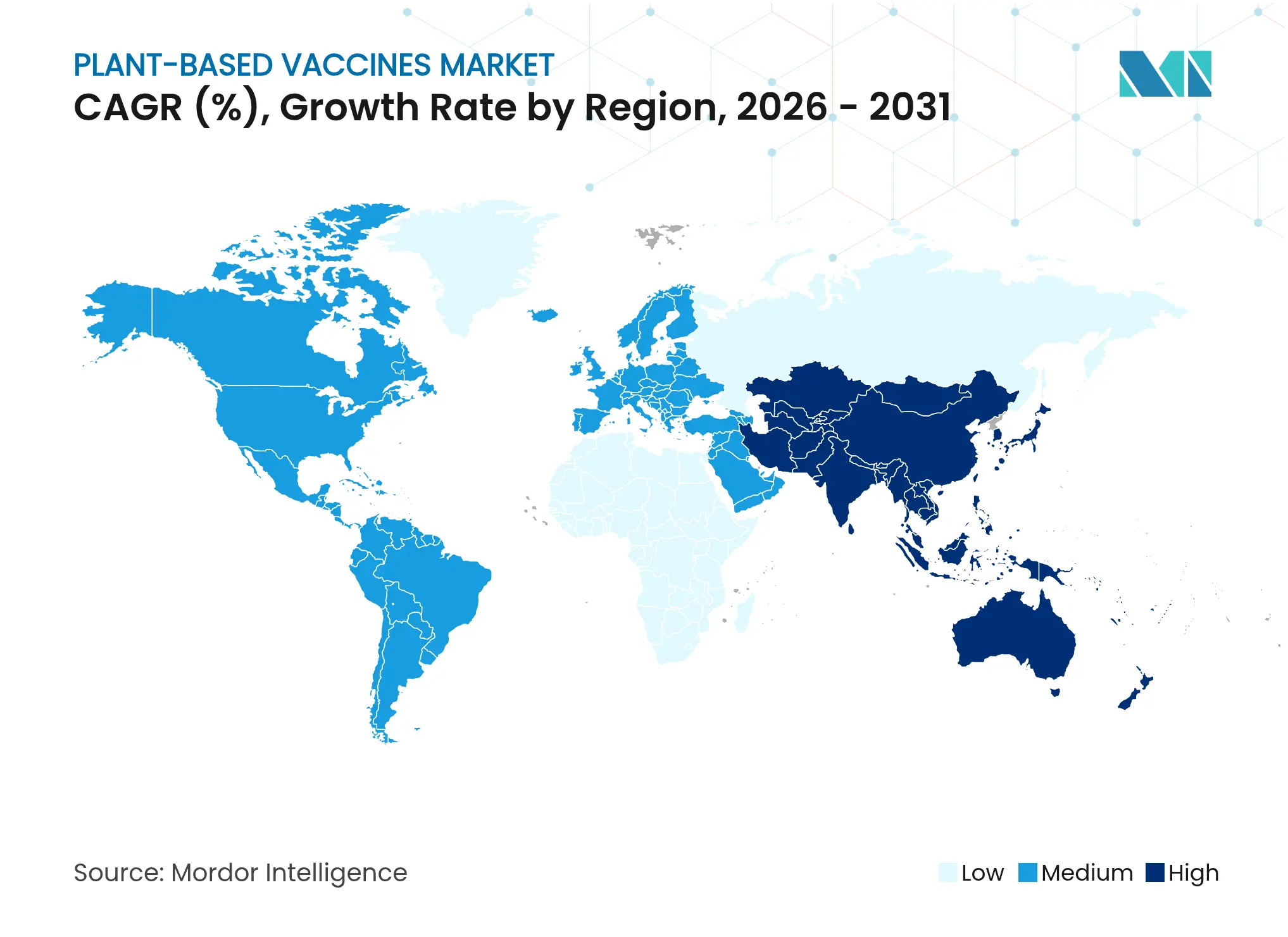

- By geography, North America contributed 44.55% of 2025 sales, but Asia-Pacific is forecast to grow the fastest at 12.11% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Plant-Based Vaccines Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Growing demand for rapid pandemic-response platforms

Growing demand for rapid pandemic-response platforms

| +2.8% | Global; early adoption in North America & EU | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

+2.8%

|

Geographic Relevance

:

Global; early adoption in North America & EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Cost-effective, scalable bioreactors versus egg & cell

culture

Cost-effective, scalable bioreactors versus egg & cell

culture

| +2.1% | Global; pronounced in APAC production hubs | Long term (≥ 4 years) | |||

Expiring patents for legacy vaccines

Expiring patents for legacy vaccines

| +1.7% | North America & EU | Short term (≤ 2 years) | |||

Government funding for emerging infectious-disease

preparedness

Government funding for emerging infectious-disease

preparedness

| +2.3% | North America & EU with spillover to APAC | Medium term (2-4 years) | |||

Next-gen chloroplast expression boosts antigen yield

Next-gen chloroplast expression boosts antigen yield

| +1.9% | Global R&D centers; commercial roll-out in North America | Long term (≥ 4 years) | |||

Edible-vaccine concepts for LMIC immunisation

Edible-vaccine concepts for LMIC immunisation

| +1.2% | Sub-Saharan Africa, Southeast Asia, Latin America | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Growing Demand for Rapid Pandemic-Response Platforms

Plant-derived systems shorten discovery-to-fill timelines from months to just weeks, a capability that proved decisive when conventional influenza and COVID-19 vaccines struggled to meet early global demand. CEPI is financing ALiCE cell-free technology that can generate clinical vaccine lots in 20 days, a 90% time saving relative to egg-based processes [2]CEPI, "Transforming vaccine manufacturing," cepi.net. Governments are taking note: the U.S. Department of Health and Human Services has earmarked USD 590 million for advanced pandemic influenza platforms able to pivot quickly to new viral strains. Agricultural biotechnology groups are also advancing edible mRNA candidates in lettuce chloroplasts that remain stable at ambient temperatures, removing cold-chain dependence and enabling community-level production [3]Carson Campbell, "Edible mRNA vaccine in lettuce chloroplasts," Nature Reviews Bioengineering, nature.com. Such innovations expand the addressable market beyond industrialized nations and create first-mover advantages for firms that can demonstrate validated chemistry-manufacturing-controls packages.

Cost-Effective, Scalable Bioreactors Versus Egg & Cell Culture

Tobacco, lettuce and potato plants act as living bioreactors that replace stainless-steel fermenters and permit open-field or vertical-farm cultivation. Academic modeling shows per-dose cost reductions of up to 90% compared with mammalian cell platforms, chiefly because plants do not require expensive containment suites or pathogen-free eggs. One acre of Nicotiana benthamiana can generate the full annual anthrax vaccine requirement for the United States within eight weeks, highlighting the land-use efficiency of the technology. The John Innes Centre has also synthesized the critical adjuvant QS-21 in tobacco, eliminating supply constraints tied to endangered South American trees and reducing ingredient lead times by 12 months. These savings are pivotal in Asia-Pacific, where capital budgets remain tight yet demand for pandemic stockpiles is expanding at double-digit rates.

Government Funding for Emerging Infectious-Disease Preparedness

The United States, European Union and a growing list of G-20 economies are underwriting next-generation vaccine infrastructure. Project NextGen alone channels USD 5 billion into modern platforms, with plant-based vaccines market developers eligible for milestone-based tranches. In parallel, the National Institute of Allergy and Infectious Diseases is prioritizing grant calls for antimicrobial-resistant pathogens, an area in which plant-derived protein expression offers low-cost antigen diversity. The European Commission’s 2025 Biotechnology Strategy further encourages public-private consortia focused on plant molecular farming, promising regulatory fast-tracking for qualifying programs. Cross-border initiatives, such as CEPI and BioNTech’s USD 145 million mRNA hub in Rwanda, illustrate how blended finance can anchor regional manufacturing nodes that also host plant-based systems.

Next-Gen Chloroplast Expression Boosts Antigen Yield

Researchers have raised recombinant-protein output in chloroplasts ten-fold by optimizing leucoplast transit peptides, unlocking multivalent formulations that previously exceeded plant expression capacity. Spinach and Chlorella microalgae now show transformation efficiencies matching Nicotiana platforms, offering new latitude to tailor glycosylation patterns for complex viral glycoproteins. University of Central Florida trials confirmed that chloroplast-derived anthrax vaccines deliver full protection in animal models while occupying less than one acre of farmland per national stockpile cycle. Such productivity shifts reduce scale-up risk and make smaller, distributed facilities viable in middle-income economies.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Ambiguous regulatory pathways for plant molecular farming

Ambiguous regulatory pathways for plant molecular farming

| -1.8% | Global; most complex in EU | Medium term (2-4 years) |

(~) % Impact on CAGR Forecast

:

-1.8%

|

Geographic Relevance

:

Global; most complex in EU

|

Impact Timeline

:

Medium term (2-4 years)

|

Limited cGMP capacity for large-scale transient expression

Limited cGMP capacity for large-scale transient expression

| -2.1% | Global manufacturing hubs; acute in APAC | Short term (≤ 2 years) | |||

Investor caution after Medicago shutdown

Investor caution after Medicago shutdown

| -1.4% | North America & EU | Short term (≤ 2 years) | |||

Allergen-profiling concerns for tobacco-derived vaccines

Allergen-profiling concerns for tobacco-derived vaccines

| -0.9% | Jurisdictions with stringent allergen rules | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Ambiguous Regulatory Pathways for Plant Molecular Farming

Developers must satisfy overlapping mandates from the FDA’s Center for Biologics Evaluation and Research, the U.S. Department of Agriculture’s APHIS division and the Environmental Protection Agency when field-growing transgenic vaccine plants, an administrative maze that can extend pre-IND timelines by 24 months. In Europe, the 2025 New Genomic Techniques framework establishes a two-track approval process that risks fragmenting market access, compelling firms to run parallel compliance strategies for Category 1 and Category 2 plants. These uncertainties raise capital costs, especially for small and mid-cap companies reliant on venture funding cycles.

Limited cGMP Capacity for Large-Scale Transient Expression

Global biomanufacturing capacity totaled only 17.4 million liters in 2024, and less than 2% of that footprint is configured for plant transient-expression workflows. Building a new, fully qualified 2,000-liter plant-based facility can exceed USD 100 million, a figure that deters first-time entrants. Geographic imbalances worsen the issue: APAC demand is growing fastest, yet most cGMP plant-based suites are in the United States and Western Europe, forcing costly transcontinental tech transfers.

Segment Analysis

By Vaccine Type: Viral Dominance, Bacterial Momentum

Viral vaccines accounted for 55.63% of revenue in 2025, confirming their position as the cornerstone of the plant-based vaccines market. The segment’s leadership rests on the success of virus-like particle designs that can be updated within days of a new genomic sequence, as Medicago’s former COVID-19 program illustrated before its 2024 closure. As a result, viral candidates continue to capture procurement contracts tied to national stockpile mandates. In contrast, bacterial vaccines are the smallest slice of the current plant-based vaccines market size, but they register the fastest expansion at a 11.83% CAGR thanks to global pressure to combat antimicrobial resistance. Developers leverage plant platforms to present multiple conserved bacterial antigens in a single dose, a feature that aligns with WHO’s 2030 AMR roadmap. The heightened pace of bacterial pipeline additions indicates that the plant-based vaccines market can broaden beyond pandemic-response niches and into routine immunization schedules by decade’s end.

Pipeline depth underscores the divergence. More than 40% of active INDs in 2025 target viral pathogens such as H5N1 and Lassa fever, whereas bacterial projects number fewer than 20 yet enjoy accelerated review under NIAID’s 2026 omnibus funding call. Because many bacterial diseases lack commercial incentives, sponsors expect advanced purchase agreements and BARDA contracts to underpin returns. The net effect is that the plant-based vaccines market share of viral products should retain an absolute majority through 2030, albeit with modest dilution as bacterial assets reach late-stage trials. Strategic differentiation will hinge on cross-protective efficacy data and cost-of-goods metrics that remain favorable for plants versus recombinant protein or conjugate vaccine alternatives.

Note: Segment shares of all individual segments available upon report purchase

By Plant Source: Tobacco Keeps the Lead as Potatoes Surge

Tobacco systems delivered 61.88% of 2025 revenue, benefitting from three decades of molecular-farming know-how and a mature supply chain for Nicotiana seedlings. The platform excels at transient expression, permitting developers to scale from lab to 3 million clinical doses in roughly eight weeks—a throughput no other current plant species matches. This speed anchors tobacco’s dominant plant-based vaccines market share; however, regulators are heightening scrutiny of alkaloid carryover and allergen signatures, prompting some firms to hedge with alternative crops. Potato-derived platforms, though only a fraction of the current plant-based vaccines market size, are expanding at 11.95% CAGR. Potatoes appeal because they are globally cultivated food staples with clear allergen-profiling precedents, reducing perceived consumer risk. Companies exploiting this crop also benefit from processing infrastructure already optimized for starch extraction, which can be repurposed for protein capture at minimal incremental capex.

Diversification continues as spinach and lettuce demonstrate transformation yields competitive with tobacco, and Chlorella microalgae gain traction for fully enclosed photobioreactor production that bypasses field-crop regulations. Early adopters position these “other plants” as a hedge against potential regulatory restrictions on genetically engineered tobacco cultivation. If allergen concerns further tighten, potatoes may become the preferred frontline platform, yet most analysts expect tobacco to remain the workhorse of the plant-based vaccines market through at least 2028 because of entrenched expertise and validated master-seed banks.

By Application: Infectious Disease Today, Oncology Tomorrow

Human infectious-disease indications contributed 48.10% of 2025 revenue, reflecting COVID-19 aftermath funding and mandatory national influenza stockpile refreshes. The segment gains additional momentum from government calls for universal coronavirus or pan-influenza candidates that can eliminate annual strain matching, a task well suited to plant platforms that allow high-throughput antigen variant screening. Oncology programs, although representing a smaller slice of the plant-based vaccines market size today, are registering a 12.08% CAGR as mRNA-encoded neoantigen strategies transition into tumor-specific virus-like particles produced in plants. Early-phase trials are reporting durable cytotoxic T-cell responses in melanoma and pancreatic cancer cohorts, outcomes that could allow plant-derived approaches to compete with individualized cell therapies at a fraction of the cost.

Veterinary applications remain a steady niche, attracting sponsors that value plants’ ability to sidestep religious or cultural objections associated with porcine or bovine cell-line inputs. The European Medicines Agency’s 2024 guideline on plasmid DNA vaccines has clarified animal-health regulatory pathways, and PlantForm Corporation’s licensing deal for Classical Swine Fever vaccines across the Americas illustrates how veterinary lines can commercialize faster than human counterparts. Over the forecast window, oncology’s share of the plant-based vaccines market is projected to rise, yet infectious-disease revenues should still exceed 40% because of periodic pandemic preparedness surges.

Note: Segment shares of all individual segments available upon report purchase

Geography Analysis

North America retained 44.55% of global revenue in 2025, underpinned by deep NIH grant allocations, a dense network of cGMP suites, and a favorable venture-capital ecosystem. Yet growth is moderating to high single digits as developers digest new FDA mandates for placebo-controlled trials across all platforms, a policy that lengthens pivotal study timelines and raises budget forecasts. The region also confronts post-Medicago investor skepticism, though British American Tobacco’s KBio and Kentucky BioProcessing continue to push Nicotiana-based COVID-19 boosters through Phase II and prepare commercial launch plans. The plant-based vaccines market nevertheless benefits from bipartisan Congressional backing for next-generation biothreat countermeasures, ensuring stable procurement demand.

Asia-Pacific is the fastest-growing cluster, posting a 12.11% CAGR through 2031 as China, India and South Korea expand sovereign biomanufacturing capacity. The Serum Institute of India’s memorandum with CEPI to adopt plant systems for low-cost vaccine output illustrates how local champions can combine price advantages with large, ready domestic markets. China already hosts 89 registries for plant-related cancer vaccine trials, second only to the United States, a sign that regional R&D hubs are maturing quickly. Governments in Japan and Australia are also offering tax credits for molecular-farming investments, which is enticing multinationals to establish satellite facilities rather than export bulk drug substance from North America.

Europe offers sizable addressable volume but is complicated by the 2025 New Genomic Techniques regulation that splits genetically modified plants into two categories. While the European Commission’s biotech strategy signals political will to foster innovation, divergent national implementations can impose staggered approval timelines. Mitsubishi Tanabe Pharma’s tobacco-based influenza candidate advancing through EU Phase III demonstrates that commercial success is possible, yet companies must budget for parallel regulatory submissions to multiple competent authorities. Latin America and the Middle East & Africa remain emerging plays; however, licensing agreements such as PlantForm-POSCO’s veterinary deal in Brazil and CEPI’s Rwanda mRNA project suggest these regions could leapfrog directly to advanced platforms, integrating plant lines alongside mRNA hubs.

Competitive Landscape

Market Concentration

The competitive arena is moderately concentrated after Medicago’s 2024 shutdown ceded early-mover advantage to other players. British American Tobacco’s KBio currently operates the largest dedicated Nicotiana capacity, able to output 3 million doses a week for pandemic surges. PlantForm Corporation leverages a cost-sharing model with Canadian universities to run multi-indication pipelines spanning Ebola, rabies and veterinary diseases, reducing single-asset risk. Kentucky BioProcessing is advancing Phase II COVID-19 and RSV candidates, banking on its long-standing tobacco agronomy expertise and established seed-stock libraries for rapid scale-up. The invalidation of key Moderna patents by the U.S. Patent Trial and Appeal Board has also lowered intellectual-property barriers, enabling smaller entrants to explore mRNA-on-plant delivery without fear of immediate litigation.

Platform differentiation is intensifying. Several start-ups focus on cell-free expression kits that generate vaccine antigens within 24 hours for regional fill-finish sites, a model that could displace traditional transient infiltration if cost curves continue to fall. Other ventures are pushing edible formulations into first-in-human trials, betting that oral delivery will open pediatric and LMIC segments.

Strategic partnerships dominate deal flow as players seek manufacturing redundancy; for example, CEPI’s ALiCE program ties together German contract manufacturers with North American formulation labs to guarantee 20-day end-to-end timelines. Because government stockpile contracts emphasize readiness over price, firms with validated rapid-response supply chains stand to capture premium margins. Consolidation remains plausible once a major program wins full licensure, but near-term the plant-based vaccines market is likely to maintain a diverse roster of platform specialists.

Plant-Based Vaccines Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Aramis Biotechnologies and CPPB signed a strategic agreement to formulate and produce clinical material for Aramis’s seasonal influenza vaccine candidate.

- December 2024: Aramis Biotechnologies closed a CAD 30 million Series A round led by company employees and Québec entrepreneurs.

- February 2024: LenioBio received up to USD 2 million from CEPI to test its cell-free plant extract technology for rapid vaccine protein production within 20-40 days.

Table of Contents for Plant-Based Vaccines Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Growing Demand for Rapid Pandemic-Response Platforms

- 4.2.2Cost-Effective, Scalable Bioreactors Versus Egg & Cell Culture

- 4.2.3Expiring Patents for Legacy Vaccines Opening White Space

- 4.2.4Government Funding for Emerging Infectious-Disease Preparedness

- 4.2.5Next-Gen Chloroplast?Expression Boosts Antigen Yield

- 4.2.6Edible-Vaccine Concepts for LMIC Immunisation

- 4.3Market Restraints

- 4.3.1Ambiguous Regulatory Pathways for Plant Molecular Farming

- 4.3.2Limited Cgmp Capacity for Large-Scale Transient Expression

- 4.3.3Investor Caution After Medicago COVID Shutdown

- 4.3.4Allergen-Profiling Concerns for Tobacco-Derived Vaccines

- 4.4Regulatory Landscape

- 4.5Porters Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Intensity of Competitive Rivalry

5. Market Size & Growth Forecasts (Value, USD)

- 5.1By Vaccine Type

- 5.1.1Bacterial Vaccines

- 5.1.2Viral Vaccines

- 5.1.3Others

- 5.2By Plant Source

- 5.2.1Tobacco

- 5.2.2Potato

- 5.2.3Others

- 5.3By Application

- 5.3.1Human Infectious Disease

- 5.3.2Oncology

- 5.3.3Veterinary Applications

- 5.4By Geography

- 5.4.1North America

- 5.4.1.1United States

- 5.4.1.2Canada

- 5.4.1.3Mexico

- 5.4.2Europe

- 5.4.2.1Germany

- 5.4.2.2United Kingdom

- 5.4.2.3France

- 5.4.2.4Italy

- 5.4.2.5Spain

- 5.4.2.6Rest of Europe

- 5.4.3Asia-Pacific

- 5.4.3.1China

- 5.4.3.2Japan

- 5.4.3.3India

- 5.4.3.4Australia

- 5.4.3.5South Korea

- 5.4.3.6Rest of Asia-Pacific

- 5.4.4Rest of the World

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1Aramis Biotechnologies Inc.

- 6.3.2iBio Inc.

- 6.3.3Kentucky BioProcessing

- 6.3.4Creative Biolabs

- 6.3.5PlantForm Corporation

- 6.3.6Baiya Phytopharm

- 6.3.7Lumen Bioscience

- 6.3.8Nomad Bioscience

- 6.3.9Leaf Expression Systems

- 6.3.10Protalix BioTherapeutics

- 6.3.11Ventria Bioscience

- 6.3.12Mazen Animal Health

- 6.3.13Cape Biologix Technologies

- 6.3.14Zea Biosciences

- 6.3.15Caliber Biotherapeutics

- 6.3.16KBio (BAT)

- 6.3.17Boost Biopharma

- 6.3.18Takis Biotech

- 6.3.19Leaf Pharmaceuticals

- 6.3.20ExpressTec Ventria

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-Need Assessment

Global Plant-Based Vaccines Market Report Scope

A plant-based vaccine is a type of vaccine produced using genetically modified plants or plant cells that express specific antigens, which are components that stimulate an immune response. Plant-based vaccines offer advantages such as lower production costs, scalability, and reduced risk of contamination compared to traditional vaccine manufacturing methods. The scope includes human as well as veterinary plant-based vaccines.

The plant-based vaccines market is segmented into type, deployment model, end user, and geography. By type, the market is segmented into bacterial vaccines, viral vaccines, and others (parasite vaccines and immunocontraceptive vaccines, among others). By plant source, the market is segmented into tobacco, potato, and others (maize, lettuce, among others). By application, the market is segmented into infectious agents, anti-cancer, and others (autoimmune disorders, allergies, among others). By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa. For each segment, the market sizing and forecasts have been done on the basis of value (USD).