Rabies Vaccine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 1.4 Billion |

| Market Size (2031) | USD 1.79 Billion |

| Growth Rate (2026 - 2031) | 5.04% CAGR |

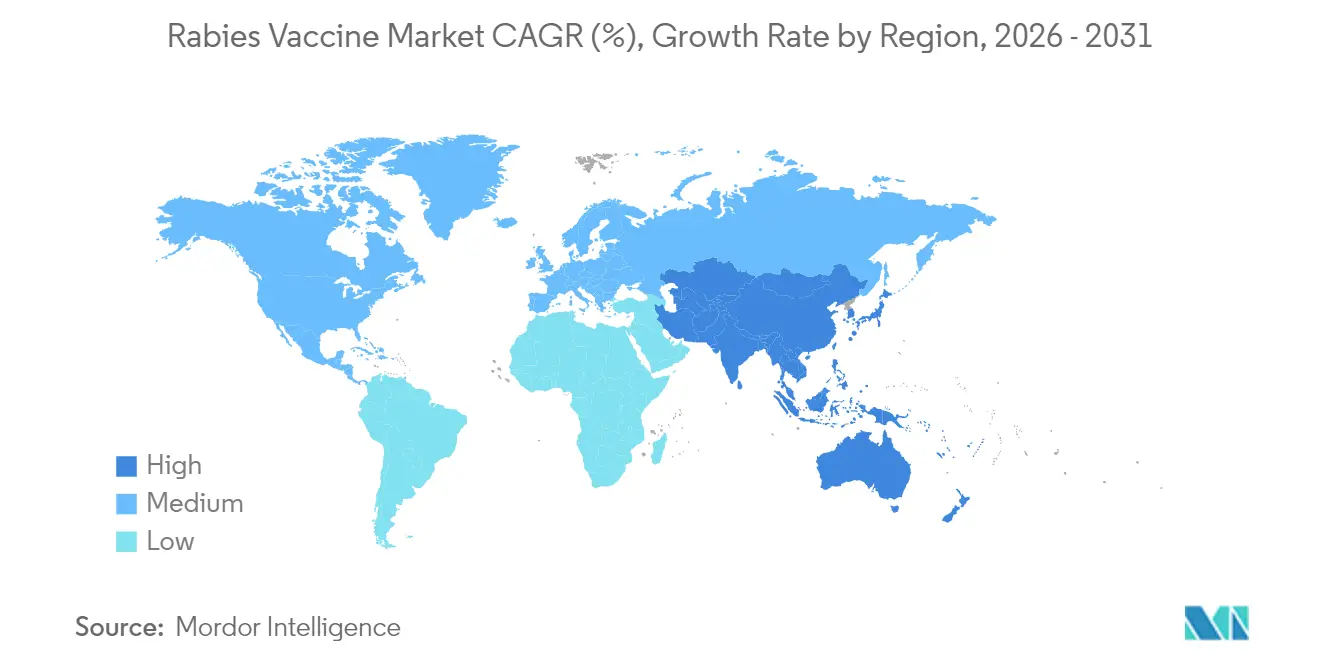

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

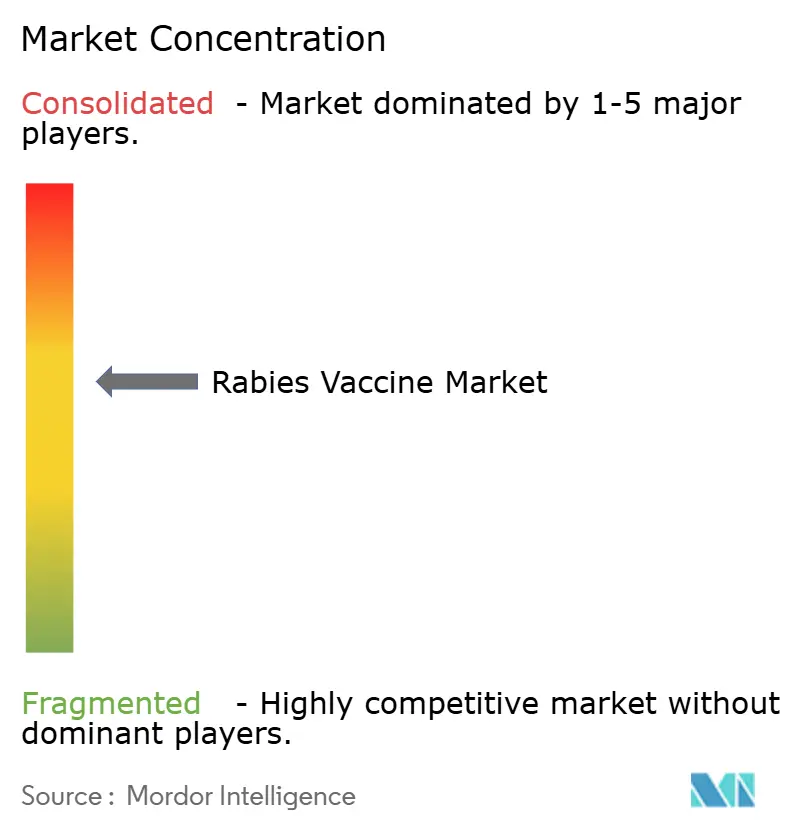

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Rabies Vaccine Market Analysis by Mordor Intelligence

The rabies vaccine market size is expected to grow from USD1.33 billion in 2025 to USD1.40 billion in 2026 and is forecast to reach USD1.79 billion by 2031 at 5.04% CAGR over 2026-2031. Growth rests on multilateral funding unlocked by the WHO-led “Zero by 30” campaign and on technology shifts from nerve-tissue to advanced cell-culture and mRNA platforms, which together lift production efficiency and improve safety profiles. Gavi’s 2024 decision to finance human post-exposure prophylaxis (PEP) across more than 50 eligible countries sharply widens demand by lowering affordability barriers in the highest-burden regions[1]. Meanwhile, rising stray-dog density in Asia and Africa sustains reactive vaccination needs, even as companion-animal ownership in North America and Europe drives preventive uptake. Supply shortages persist because of limited fill-finish capacity and fragile cold-chain networks, creating space for cost-efficient Asian entrants. Sanofi’s late-stage mRNA candidate SP0087, slated for US and EU filings in 2H 2025, could accelerate the premium segment and stimulate competitive responses.

Key Report Takeaways

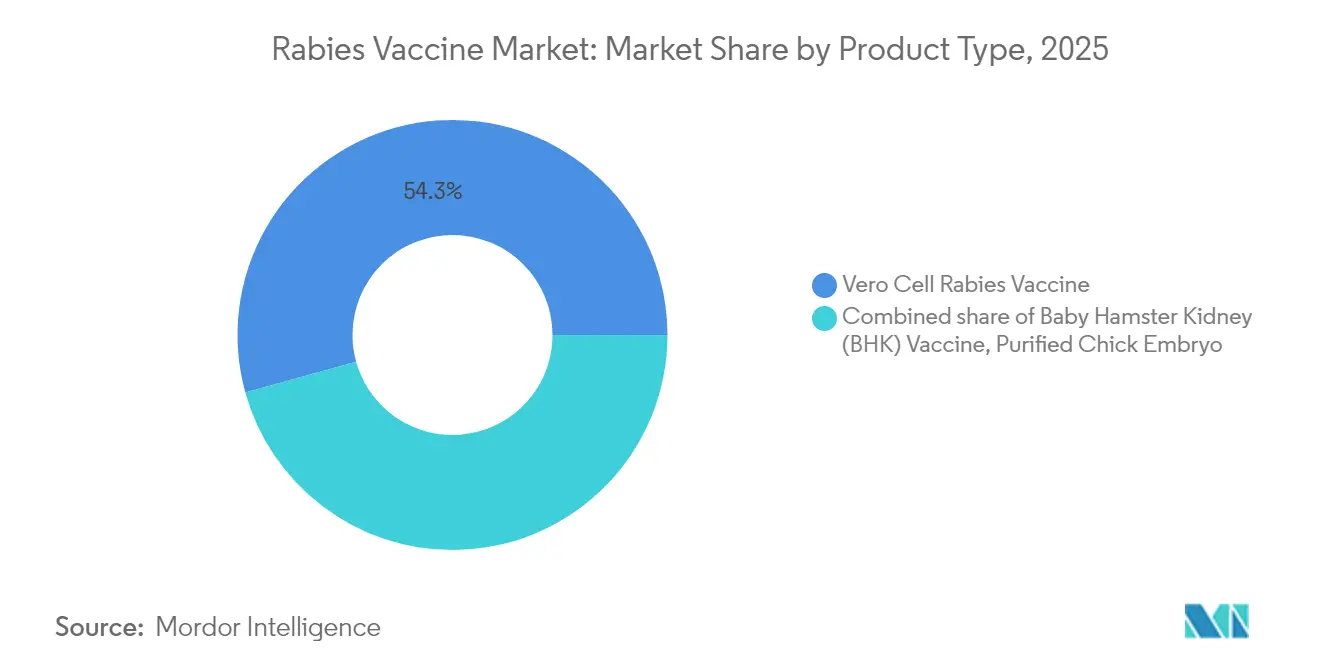

- By product type, vero cell vaccines captured 54.30% of the rabies vaccine market share in 2025; other product types are advancing at a 9.4% CAGR to 2031.

- By vaccination type, PEP accounted for 77.20% share of the rabies vaccine market size in 2025, whereas PrEP is growing at a 6.55% CAGR.

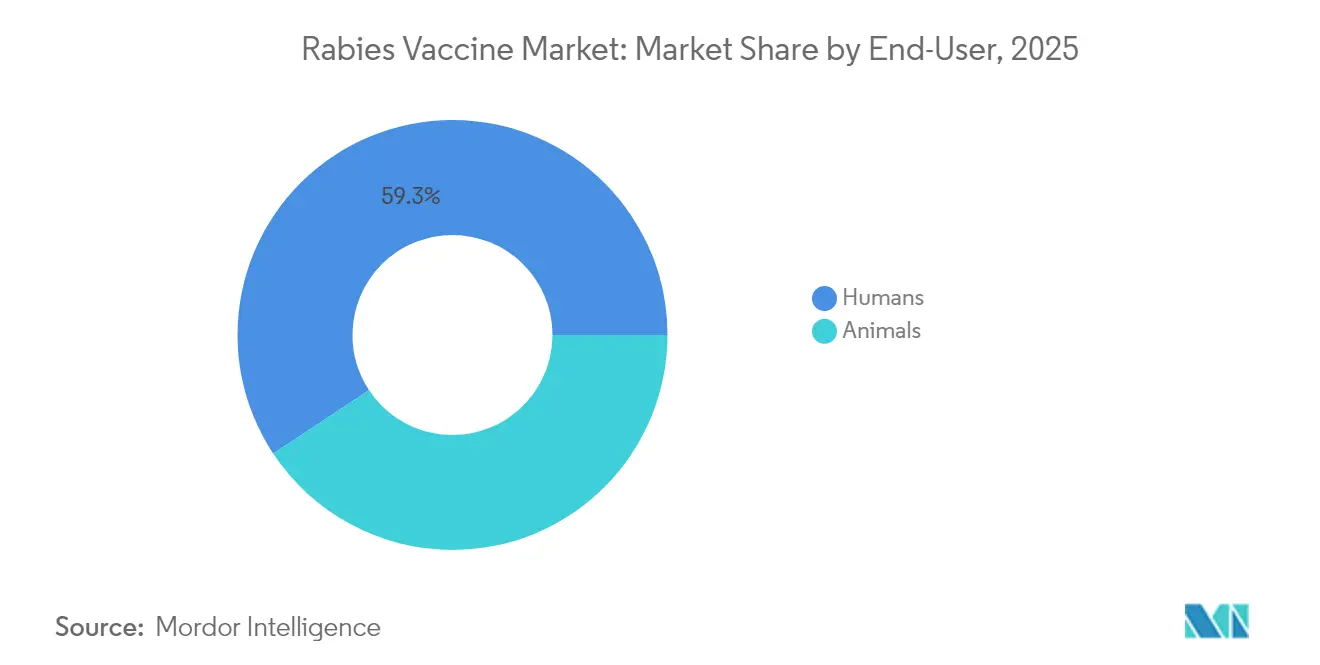

- By end-user, the human segment commanded 59.30% share in 2025; the animal segment is rising at a 6.32% CAGR.

- By distribution channel, public procurement programs held 39.40% share in 2025, while retail and online pharmacies are forecast to grow at 6.76% CAGR.

- By geography, North America led with 40.20% revenue share in 2025, while Asia Pacific is projected to expand at a 6.32% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Rabies Vaccine Market Trends and Insights

Driver Impact Analysis*

| Drivers Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Global “Zero by 30” funding surge | +1.8% | Africa & Asia | Long term (≥ 4 years) |

| Shift to cell-culture & mRNA platforms | +1.2% | North America & Europe first | Medium term (2-4 years) |

| Escalating animal-bite incidence | +0.9% | Asia Pacific, Africa, Latin America | Long term (≥ 4 years) |

| Companion-animal ownership uptrend | +0.7% | North America, Europe, Urban APAC | Medium term (2-4 years) |

| Expanded public procurement | +0.6% | Africa, South Asia, Latin America | Medium term (2-4 years) |

| Novel modalities (mRNA, mAbs) | +0.5% | Global | Long term (≥ 4 years) |

| Expanded Government Procurement & Donor Support Mechanisms Improving Vaccine Accessibility | +0.7% | Africa & Asia | Medium term (2-4 years) |

| Robust R&D Pipeline in Novel Modalities (mRNA, Monoclonal Antibodies) Broadening Addressable Market | +0.5% | North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Global “Zero by 30” Rabies Elimination Initiative Boosting Multilateral Funding

The WHO-led goal of ending dog-mediated human rabies deaths by 2030 has unlocked unprecedented multilateral funding streams that guarantee long-term vaccine demand. Gavi now finances post-exposure prophylaxis in more than 50 eligible countries, removing the biggest affordability hurdle in low-income settings. Bulk tenders created under this framework give manufacturers better visibility into future volumes, encouraging capacity expansions. Integrated Bite Case Management tools rolled out with the program improve surveillance, which sharpens demand forecasts and cuts wastage. Together, these elements convert previously unpredictable humanitarian purchases into a stable commercial pipeline.

Shift from Nerve-Tissue to Advanced Cell-Culture & mRNA Platforms Enhancing Safety and Uptake

Manufacturers are phasing out nerve-tissue vaccines in favor of Vero, BHK, and mRNA technologies that deliver higher efficacy and better safety records. mRNA candidates show full protection in animal models with just two doses, which improves patient compliance and lowers program costs. Serum-free production under review in China eliminates animal serum risks and supports premium pricing in quality-sensitive markets. Higher yields from suspension cultures reduce per-dose cost, making advanced platforms attractive even for public tenders. These shifts collectively expand supply, enhance trust, and open doors to dose-sparing schedules.

Expanded Government Procurement & Donor Support Mechanisms Improving Vaccine Accessibility

Centralized purchasing through Gavi, PAHO, and national health ministries now accounts for 40% of global distribution, giving suppliers secure, multiyear contracts. WHO-approved intradermal regimens cut vial needs by two-thirds, stretching budgets and enabling broader coverage. Procurement frameworks emphasize WHO prequalification, pushing manufacturers to upgrade quality systems for eligibility. Predictable tenders reduce inventory risk and encourage investment in capacity. As more countries graduate from donor aid, structured national buying keeps volumes steady.

Robust R&D Pipeline in Novel Modalities (mRNA, Monoclonal Antibodies) Broadening Addressable Market

Monoclonal antibody cocktails such as TwinRab overcome supply limits of conventional immunoglobulins and offer consistent potency. Plant-based and microarray patch technologies are under evaluation, promising simpler administration and better thermostability.

mRNA platforms open optionality for rapid scale-up during outbreaks, appealing to preparedness budgets. These innovations attract venture funding and strategic partnerships, injecting fresh capital into the sector. A broader tool kit ultimately enlarges the addressable market by meeting diverse clinical and logistical needs.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited rural cold-chain capacity | –0.8% | Africa, South Asia, Rural Latin America | Medium term (2-4 years) |

| High total cost of full PEP regimen | –0.7% | Low- and middle-income countries | Short term (≤ 2 years) |

| Intermittent Supply Shortages & Manufacturing Capacity Constraints Impacting Global Availability | –0.9% | Global | Short term (≤ 2 years) |

| Complex, Price-Sensitive Tender and Regulatory Processes Delaying New Vaccine Market Entry | –0.6% | Africa & Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Cold-Chain & Healthcare Infrastructure Restricting Rural Distribution in Endemic Regions

The absence of reliable electricity means that up to 30% of vaccines spoil before reaching remote clinics in several African and South Asian countries, wiping out scarce public-health budgets. WHO’s Vaccine Innovation Prioritisation Strategy now places thermostable rabies formulations in its top tier of needed technologies, signalling future tender preference for products that tolerate 40 °C excursions for at least three days. Pilot field studies with deep-cold borosilicate vials introduced in 2024 cut breakage rates by 70% during last-mile transport on motorcycles over unpaved roads. Even where storage exists, clinics often lack calibrated temperature monitoring, leading to batch-by-batch quality uncertainty that erodes clinician confidence and depresses demand. Thermostable human rabies immune globulin (HRIG) now in late-stage development could further ease logistics by eliminating strict 2-8 °C handling requirements, but commercial launch is not expected before 2027.

High Total Cost of Full PEP Regimen Creating Affordability Barriers

A complete five-dose intramuscular PEP course plus rabies immunoglobulin can cost USD55–70 in many low-income settings, outstripping the average monthly household health budget in rural India and Kenya. WHO-endorsed intradermal schedules lower per-patient vaccine volume by almost 60% and reduce clinic visits from five to three, yet adoption remains below 25% because many facilities lack trained staff for the ID technique. Economic modelling shows that routine childhood PrEP becomes cost-effective at incidence rates above 3 per 100 000, with incremental cost-effectiveness ratios falling under USD500 per QALY in high-burden provinces of the Philippines and Tanzania. Gavi co-financing currently subsidises vaccine purchase but not ancillary costs such as syringes, travel, and lost wages, which together can equal the vaccine outlay itself and deter compliance. Ministries evaluating bulk purchase contracts are therefore experimenting with vial-sharing hubs and community outreach to trim per-dose delivery costs and push coverage closer to the 70% threshold needed for herd-level protection.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Vero Cell Dominance Amid Technology Transition

The Vero Cell segment holds 54.30% of the rabies vaccine market share in 2025. Robust antigen recovery and 99.99% host-DNA removal deliver reliable safety benchmarks, while serum-free suspension culture pushes yields to 5.2 × 10^7 FFU/mL. As emerging mRNA and BHK products grow at 9.4% CAGR, manufacturers hedge portfolios to retain relevance. Continuous process intensification positions Vero Cell plants to defend volumes even as niche premium segments accelerate.

Other product types form the quickest-growing cluster. mRNA candidates promise two-dose schedules, smaller batch sizes, and rapid scalability during shortages, aligning with future tender criteria. AIM Vaccine filed the first serum-free human rabies vaccine with regulators in 2025, signalling wider competition in upper-middle-income markets. These innovations are likely to lift the rabies vaccine market size for non-Vero formats above USD418 million by 2031.

By Vaccination Type: PEP Necessity Drives Demand

PEP accounts for 77.20% of the rabies vaccine market in 2025. WHO’s 1-week intradermal protocol lifts compliance: 87% of recipients maintain protective antibody titres after 1 year. Monoclonal antibody combinations now entering practice cut adverse reactions and standardize potency, strengthening PEP’s clinical edge.

PrEP grows at 6.55% CAGR as travel rebounds and occupational guidelines shift. CDC now endorses a 2-dose PrEP series, lowering cost and clinic visits. With longer booster intervals, the rabies vaccine industry sees new opportunities in employer-funded schemes for veterinarians, laboratory staff, and adventure tourists.

By End-User: Human Segment Leads While Animal Segment Accelerates

Human applications constitute 59.30% of current volume because of high mortality risk and mandatory response protocols. Four-dose 2-1-1 regimens in freeze-dried Vero formulations yield 100% seroconversion with fewer visits, an attractive feature for busy urban clinics. Public health agencies continue bulk tenders, locking in baseline volumes. The animal segment posts a 6.32% CAGR, underpinned by stricter pet vaccination rules and combination shots such as Core EQ Innovator for horses. Oral baits for wildlife are now validated in urban raccoon programs, opening adjacent demand in wildlife management.

By Distribution Channel: Public Programs Anchor Supply While Retail Rises

Government procurement represents 39.40% of output, ensuring tender stability and favoring WHO-prequalified suppliers. Pan-American dog-cat campaigns that delivered 236.0 million doses between 2017-2022 exemplify the scale public channels can reach. Retail and online pharmacies expand at 6.76% CAGR as pharmacies push to administer all adult vaccines. Workflow investments made during COVID-19 now support refrigerated biologics, and single-use transfer devices introduced in 2025 improve safety for point-of-care injections. This channel’s convenience resonates with urban pet owners and frequent travelers, broadening the rabies vaccine market base.

Geography Analysis

North America retains 40.20% share of the rabies vaccine market in 2025, propelled by airtight regulatory oversight and widespread insurance coverage. Canada’s Immunization Guide mandates risk-based regimens for veterinarians and laboratory workers, promoting steady baseline uptake. Community programs such as Brownsville’s free 2025 clinic reinforce equitable access.

Asia Pacific records the fastest regional CAGR at 6.32%. India and China now deliver more than 1 billion vaccine doses annually and self-supply over 85% of regional demand. China’s rabies vaccine market size is forecast to surpass RMB15.56 billion (USD 2.17 billion) by 2031 on the back of rising urban pet ownership and local innovation pipelines. Serum-free and combination formulations are expected to be early adopters in this environment. Europe, Middle East & Africa, and South America form a diversified opportunity set. In Europe, Bavarian Nordic’s Rabipur/RabAvert exceeded sales expectations in 2024, highlighting resilient premium demand. African Union initiatives such as PAVM aim to grow local manufacturing through finance and technology transfer, signalling long-run supply-side changes. South America showcases sustained progress: dog-transmitted human cases dropped 98% since 1983, yet governments still prioritize canine campaigns to maintain ≥80% coverage.

Competitive Landscape

The rabies vaccine market features a moderately consolidated structure. Western multinationals—Sanofi SA, GlaxoSmithKline plc, and Merck & Co., Inc.—control premium channels in high-income countries through continual formulation upgrades and strong tender track records. Asian manufacturers—Bharat Biotech, AIM Vaccine Co., Ltd., Indian Immunologicals Ltd.—pursue value leadership and localized distribution in cost-sensitive markets, often leveraging technology transfers to accelerate scale. YS Biopharma’s PIKA adjuvant candidate underscores how biotech entrants are carving out differentiated positions with accelerated immunity profiles.

Strategic alliances and public-preparedness contracts underpin profitability. Bavarian Nordic booked DKK441 million (USD 67.59 million) operating profit in H1 2024 as contractual demand cushioned market volatility. Technology co-development—such as serum-free production partnerships—mitigates regulatory risks and broadens geographic access. White-space innovation around thermostable formulations and microarray patches offers differentiation paths, while AI-driven discovery platforms highlighted by Zoetis herald cross-pollination between animal and human pipelines.

Clinical supply constraints create entry windows for agile producers capable of meeting surge orders. Companies integrating vertical cold-chain or adopting regional fill-finish models are best positioned to capture incremental tenders. Portfolio balance between PEP mainstays and PrEP, mRNA, or monoclonal extensions will likely determine long-term share gains.

Rabies Vaccine Industry Leaders

Sanofi SA

GlaxoSmithKline plc

Merck & Co., Inc.

Zoetis Inc.

Boehringer Ingelheim International GmbH

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: AIM Vaccine filed for approval of the world’s first serum-free human rabies vaccine after positive Phase III outcomes, with large-scale production lines already validated

- April 2025: LakeShore Biopharma released YSJA vaccine with a single-use liquid transfer device, targeting retail pharmacy channels

- June 2024: Gavi launched funding for human PEP vaccines in 50+ countries under “Zero by 30,” expanding the addressable rabies vaccine market in Africa and Asia.

- August 2024: Bavarian Nordic exceeded H1 sales targets, triggering a DKK186 million milestone payment to GSK for Rabipur/RabAvert.

- April 2024: LakeShore Biopharma released YSJA vaccine with a single-use liquid transfer device, targeting retail pharmacy channels.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the global rabies vaccine market as every GMP-compliant biologic that elicits active immunity against the rabies virus in humans or animals, spanning cell-culture and chick-embryo vaccines distributed through public tenders, hospitals, travel clinics, veterinary practices, and retail or online pharmacies worldwide.

Scope Exclusions: Therapeutic rabies immunoglobulins, wound-care consumables, and experimental DNA or monoclonal-antibody candidates are outside scope.

Segmentation Overview

- By Product Type

- Baby Hamster Kidney (BHK) Vaccine

- Purified Chick Embryo Cell Rabies Vaccine

- Vero Cell Rabies Vaccine

- Other Product Types

- By Vaccination Type

- Pre-Exposure Vaccination (PrEP/PEV)

- Post-Exposure Prophylaxis (PEP)

- By End-User

- Humans

- Animals

- By Distribution Channel

- Public Health Procurement & Mass Immunization Programs

- Hospitals & Travel Clinics

- Veterinary Clinics

- Retail & Online Pharmacies

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed infectious-disease clinicians, national immunization officers, veterinary public-health heads, and procurement chiefs across Asia, Africa, Europe, and the Americas. Follow-ups were arranged whenever draft uptake, buffer-stock, or price figures clashed with on-ground realities.

Desk Research

We began with World Health Organization prevalence tables, US CDC bite-incidence files, and OIE dog-vaccination dashboards, which let us size potential demand by country. Customs records in UN Comtrade and shipment tracker Volza revealed cross-border dose flows and typical transfer prices. Questel patent scans, peer-reviewed journals, and manufacturer 10-Ks exposed pipeline shifts and cost drivers. Our paid access to D&B Hoovers and Dow Jones Factiva helped trace company revenues and tender awards. The sources named are illustrative; many additional public and proprietary datasets supported this phase.

Market-Sizing & Forecasting

We first built the baseline top-down from human and canine bite counts, dose protocols, and procurement budgets. We then cross-checked it with selective bottom-up supplier roll-ups and channel audits. Five market fingerprints, dog-vaccination coverage, PEP kits issued, average course price, pace of nerve-tissue vaccine phase-out, and veterinary-clinic density, anchor volume and value outputs. Multivariate regression blended with scenario analysis projects each driver through the forecast period, while currency and input-cost outlooks refine price curves. Regional averages backfill any bottom-up gaps flagged for review.

Data Validation & Update Cycle

We run anomaly checks against WHO and customs benchmarks, escalate variances above five percent to a senior reviewer, and refresh the model annually, with interim updates after major tenders or safety alerts. A final analyst pass before publication guarantees clients the latest view.

Why Mordor's Rabies Vaccine Baseline Commands Reliability

Published figures often diverge; some split human and veterinary segments, use older base years, or value subsidized tenders at cost. Our 2025 model covers both segments at manufacturer selling price and rests on epidemiology-backed demand pools, which is where Mordor Intelligence stands apart.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.33 B (2025) | Mordor Intelligence | - |

| USD 1.20 B (2022) | Global Consultancy A | Older base year; public-sector prices unadjusted |

| USD 1.10 B (2023) | Industry Portal B | Excludes human PrEP; limited field validation |

| USD 0.64 B (2018) | Regional Consultancy C | Five-nation scope; inflation not normalized |

By uniting current epidemiology, dual-segment coverage, and explicit assumptions, we deliver a balanced baseline users can reproduce and trust.

Key Questions Answered in the Report

What is the current size of the rabies vaccine market?

The market is valued at USD1.40 billion in 2026 and is forecast to grow to USD1.79 billion by 2031.

Which region leads the rabies vaccine market?

North America holds the largest share at 40.20% in 2025, benefiting from strong healthcare infrastructure and preventive vaccination norms.

Why does post-exposure prophylaxis dominate demand?

PEP represents 77.20% of volume because rabies is nearly always fatal once symptoms appear, making immediate vaccination after exposure essential

How fast is the Asia-Pacific market growing?

Asia Pacific is projected to expand at a 6.32% CAGR between 2026 and 2031, driven by government programs and local manufacturing scale.

What technological shifts are shaping future products?

Cell-culture refinements, mRNA constructs with two-dose schedules, and monoclonal antibody alternatives to immunoglobulins are key innovations expected to widen access and improve safety.

How are retail pharmacies influencing vaccine distribution?

Investments in cold-chain handling and single-use safety devices allow pharmacies to administer rabies shots conveniently, supporting a 6.76% CAGR for this channel through 2031.

Page last updated on: