Tetanus Toxoid Vaccine Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 6.47 Billion |

| Market Size (2031) | USD 8.49 Billion |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

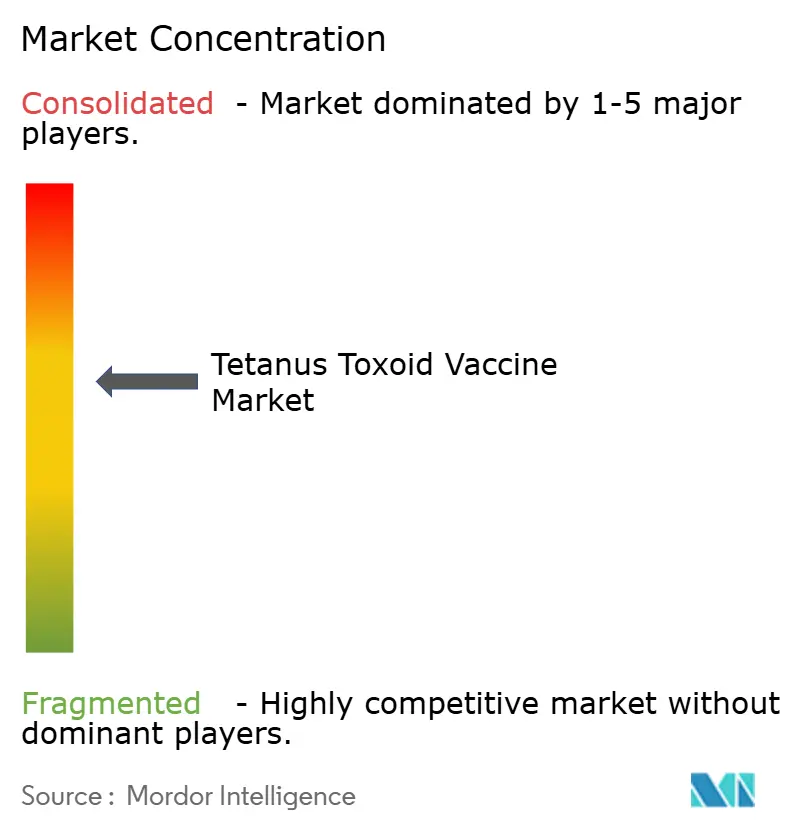

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tetanus Toxoid Vaccine Market Analysis by Mordor Intelligence

The tetanus toxoid vaccine market size in 2026 is estimated at USD 6.47 billion, growing from 2025 value of USD 6.13 billion with 2031 projections showing USD 8.49 billion, growing at 5.59% CAGR over 2026-2031. Demand momentum stems from national immunization programs, rising preference for combination formulations, expanding adult booster policies and sustained multilateral procurement funding. Combination products—especially Tdap—are expanding fastest at 7.9% CAGR, helped by life-course immunization initiatives. North America leads with a 36% revenue share on the strength of mature reimbursement systems, yet Asia Pacific is the high-growth arena, projected at 7.2% CAGR, as governments scale manufacturing capacity, broaden access and increase public-health budgets. Thermostable technologies are poised to reshape supply chains; Phase 1 trials of a fridge-free Td vaccine began in April 2025 and aim to cut cold-chain wastage by more than half1. Supply resilience remains a concern because manufacturer exits—such as MassBiologics ending Td output—have exposed concentrated production nodes. Overall, regulatory moves toward Td rather than standalone TT are re-directing tender volumes and influencing product pipelines.

Key Report Takeaways

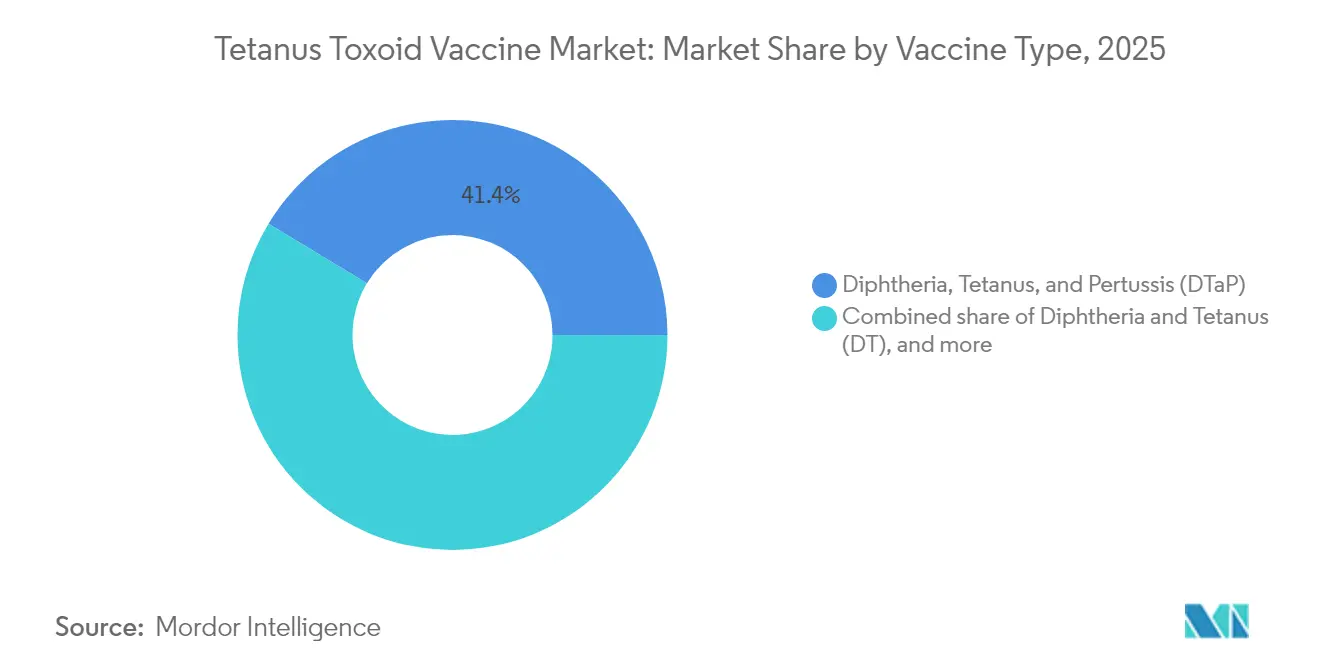

- By vaccine type, DTaP led with 41.35% of tetanus toxoid vaccine market share in 2025, whereas Tdap is forecast to grow at a 7.75% CAGR through 2031.

- By age group, the paediatric segment accounted for 84.30% share of the tetanus toxoid vaccine market size in 2025; the adult cohort is projected to advance at a 6.33% CAGR between 2026-2031.

- By end user, hospitals and trauma centres commanded 67.10% of 2025 revenue; public immunization clinics represent the fastest trajectory at 6.82% CAGR to 2031.

- By distribution channel, government procurement accounted for 62.20% of 2025 volume, while the private/self-pay channel is expected to register a 7.03% CAGR to 2031.

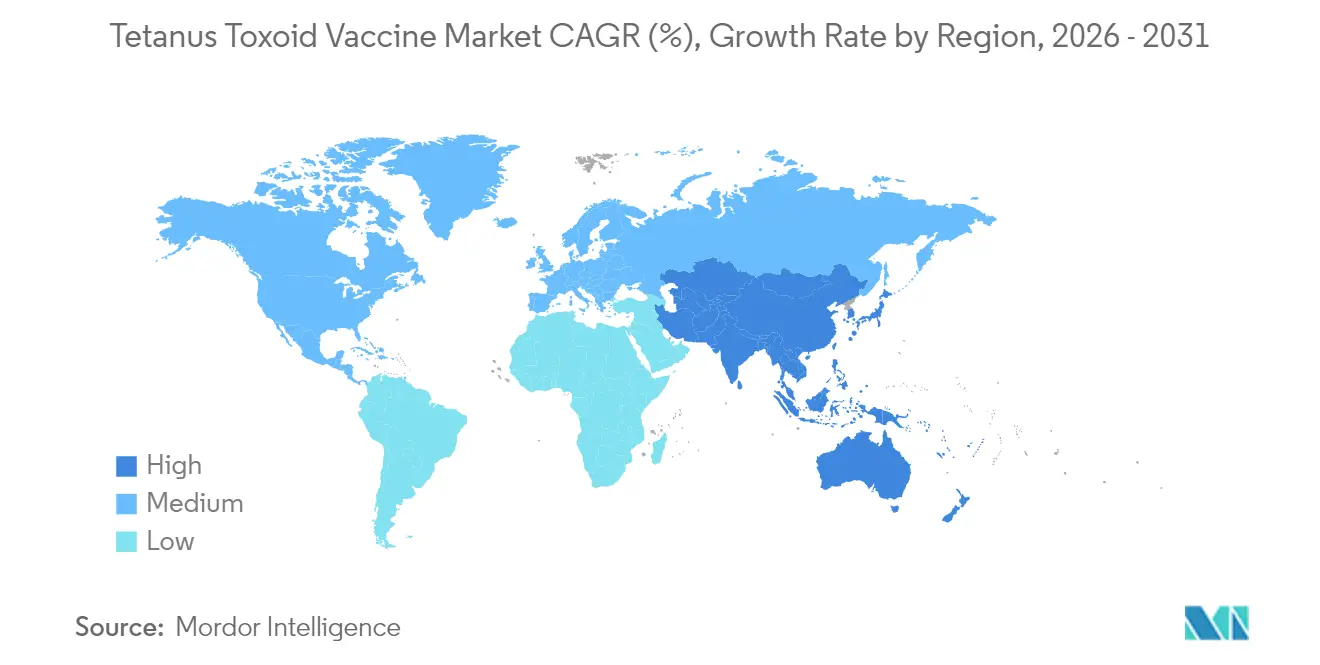

- By geography, North America controlled 35.60% revenue in 2025, while Asia Pacific is set to expand at a 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Tetanus Toxoid Vaccine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of national immunisation programmes & booster updates | +1.2% | Global (LMIC focus) | Medium term (2-4 years) |

| Higher-valent pentavalent & hexavalent adoption | +1.8% | North America, Europe, Asia Pacific | Long term (≥4 years) |

| Sustained UNICEF, Gavi & PAHO procurement funding | +1.0% | Africa, South Asia, Latin America | Medium term (2-4 years) |

| Rising adult booster awareness | +0.8% | North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Entry of cost-competitive manufacturers via WHO prequalification pathway | +0.5% | Asia, Africa | Short term (≤2 years) |

| Advancements in low-dose adjuvant & thermostable formulation technologies | +0.9% | Global | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expansion of National Immunisation Programmes & Booster Policy Updates

Global programmes now emphasise cradle-to-senior coverage, supported by WHO’s Immunization Agenda 2030 that targets 90% DTP3 coverage. Countries such as South Sudan reaffirmed this approach during African Vaccination Week 2025, pairing new vaccine launches with tetanus-booster outreach[2]UNICEF Supply Division, “Diphtheria Tetanus Pertussis Containing Vaccines: Market and Supply Update,” unicef.org. ‘The Big Catch-Up’ campaign seeks to close pandemic-era gaps among under-fives, while many ministries are embedding adolescent and adult boosters into schedules, enlarging the addressable segments of the tetanus toxoid vaccine market. These broadened policies underpin forecasts for incremental multi-age demand over the medium term and provide tailwinds for manufacturers positioned with life-course formulations.

Growing Adoption of Pentavalent & Hexavalent Combination Vaccines

Higher-valent combinations shorten clinic visits, lift completion rates and simplify logistics. Evidence shows children receiving combination vaccines achieve superior on-time coverage. CanSino’s DTcP candidate holds Chinese priority-review status, while its DTcP-Hib-MCV4 product entered clinical trials in February 2025 . Annual pentavalent demand is projected at 135 million doses across 2023-2025 in transitioning middle-income economies. The ability to dovetail diphtheria, pertussis and tetanus antigens into a single shot reinforces the tetanus toxoid vaccine market’s combination pivot and is expected to dominate long-term growth.

Sustained Procurement Funding from UNICEF, Gavi & PAHO Revolving Fund

UNICEF purchases >2 billion doses yearly, a sizeable share containing tetanus antigens, ensuring long-term agreements through 2027 that span 130-140 million Td doses annually. Gavi’s Vaccine Investment Strategy 2024 outlines continued support for tetanus-containing portfolios into the 2026-2030 finance window. PAHO’s revolving fund secures bulk pricing for Latin American ministries. Predictable tenders guide manufacturers’ capacity plans, underpin price stability and de-risk R&D for thermostable and adult-formulation lines, bolstering the tetanus toxoid vaccine market outlook.

Rising Awareness of Adult Booster Immunisation in Developed & Emerging Markets

Adult immunisation campaigns address waning immunity; studies show only 4% of patients on biologics were up-to-date for Tdap. Market modelling indicates the broader adult vaccine category may reach USD 27.65 billion in 2028, with tetanus boosters an essential component. Life-course concepts are gaining ground in Vietnam where private sales exceed USD 300 million. Public-health agencies are therefore reshaping messaging, deploying workplace and pharmacy channels—moves that directly enlarge the tetanus toxoid vaccine market footprint.

Entry of Cost-competitive Manufacturers via WHO Prequalification Pathway

Prequalification enables emerging suppliers to bid for global tenders. India’s Serum Institute lifted its global vaccine share from 19% to 24% between 2021-2023[3]Biotechnology Industry Research Assistance Council, “India BioEconomy Report 2024,” birac.nic.in. Africa’s AVMA will inject up to USD 1 billion over 10 years to localise production. These entrants diversify supply, mitigate shortages and exert pricing pressure, changing competitive dynamics inside the tetanus toxoid vaccine market.

Advancements in Low-dose Adjuvant & Thermostable Formulation Technologies

Nano-engineered adjuvants promise targeted delivery and improved safety. Stablepharma’s SPVX02, now in Phase 1, remains potent without refrigeration, potentially applicable to 60 vaccines[4]BioIndustry Association, “How Stablepharma is Pioneering the World’s First Fridge-Free Vaccine,” bioindustry.org. mRNA-based DTP concepts have also shown favourable immunogenicity in preclinical work. Such innovations will likely reduce wastage, cut logistics costs and open previously inaccessible geographies—structural upsides for the tetanus toxoid vaccine market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vaccine hesitancy & misinformation | -0.9% | Global (variable) | Medium term (2-4 years) |

| Concentrated manufacturing base | -0.7% | Import-dependent regions | Short term (≤2 years) |

| Budgetary constraints for Td/Tdap transition in low- & middle-income countries | -0.6% | Africa, South Asia, Latin America | Medium term (2-4 years) |

| Adverse events & litigation risks linked to combination vaccines | -0.5% | North America, Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Vaccine Hesitancy & Misinformation Undermining Uptake Across All Age Groups

Declining trust in institutions and circulating myths depress uptake. Fourteen-and-a-half million children missed routine vaccines in 2023, many in fragile settings. Adult boosters suffer from low prioritisation; surveys indicate awareness gaps about decennial Td/Tdap schedules. Lower demand translates into expired stock, complicating inventory planning and undermining efficient delivery within the tetanus toxoid vaccine market.

Concentrated Manufacturing Base Creating Supply-chain Vulnerability

MassBiologics’ 2024 Td exit left a single US supplier, triggering short-term allocation limits. Similar bottlenecks have surfaced in large LMIC programmes due to forecasting errors and stock-management challenges. Regulatory heterogeneity further slows alternative suppliers’ entry. Such fragilities introduce volatility into the tetanus toxoid vaccine market until diversification efforts mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vaccine Type: Combination Vaccines Driving Market Evolution

DTaP secured 41.35% of tetanus toxoid vaccine market share in 2025 on the back of five-dose paediatric schedules. The tetanus toxoid vaccine market size for this segment is forecast to exhibit mid-single-digit growth as guidelines remain unchanged. Tdap’s 7.75% CAGR outpaces the wider market because adolescent, maternal and adult boosters are scaling; CDC endorses Tdap during every pregnancy, with >90% infant pertussis protection.

Standalone TT products are declining as tenders pivot to Td, and mRNA DTP prototypes could disrupt pricing and manufacturing paradigms by late forecast. The tetanus toxoid vaccine industry therefore concentrates R&D on higher-valent, thermostable or genetic-platform formulations to preserve relevance amid evolving schedules.

By Age Group: Adult Segment Gaining Momentum Despite Paediatric Dominance

Paediatrics held 84.30% share of the tetanus toxoid vaccine market size in 2025, sustained by school-entry mandates and VFC entitlements. Nonetheless, adults show a 6.33% CAGR as immunosenescence and injury-prone lifestyles highlight booster gaps. Evidence of disproportionate tetanus cases among seniors with lapsed immunity underscores an unmet need.

Policy levers such as Medicare cost caps remove financial barriers, while rapid saliva testing enables targeted outreach within minutes. These factors collectively reposition the adult cohort as a growth lever in the tetanus toxoid vaccine market.

By End User: Public Immunization Clinics Gaining Ground in Fragmented Landscape

Hospitals and trauma centres generated 67.10% revenue in 2025 due to their central role in wound management protocols. Their integrated electronic records ensure immediate prophylaxis decisions, anchoring volume density. Yet community clinics, supported by mobile teams and culturally adapted campaigns, will post 6.82% CAGR, reflecting equity-driven funding rounds such as Wisconsin’s RICE grants.

Low-fee schedules—USD 21.23 for Td in San Antonio, USD 40.20 for Tdap—draw price-sensitive users. Expansion of pharmacy and workplace channels widens convenience, steering incremental syringes to the tetanus toxoid vaccine market.

By Distribution Channel: Government Procurement Dominates While Private Sector Expands

National tendering under EPI, NEPI or similar constructs anchors aggregate demand and shapes technical specs. Vietnam’s public programme supplies Td free-of-charge, with pricing set centrally. UNICEF alone met 40% of global Td volumes in 2022, illustrating the heft of institutional buyers.

The private/self-pay channel is rising because insurers must cover ACIP-listed vaccines in-network at zero cost-share as of October 2023. Upgraded regional distribution centres promise scale economies that reduce landed costs and curtail wastage. Competitive tenders and private adoption together expand accessibility, growing the tetanus toxoid vaccine market.

Geography Analysis

North America delivered 35.60% of 2025 revenue, supported by mature coverage systems and the Inflation Reduction Act’s zero cost-share adult vaccine clause. Nonetheless, the 2024 Td shortfall revealed vulnerabilities and forced clinics to substitute with Tdap in certain settings. California has intensified Tdap outreach amid pertussis spikes, especially targeting pregnancies week 27-36. Sustained legislative and funding support maintain the region’s central role in the tetanus toxoid vaccine market.

Asia Pacific stands out with a 7.12% CAGR to 2031. India supplies 60% of vaccines for global immunisation programmes, while China covers 90% of its domestic need. Government incentives and WHO prequalification pathways bolster exports. Vietnam’s private vaccine turnover above USD 300 million underscores rising middle-class demand. Regional capacity—Serum Institute’s 3 billion doses and Bharat Biotech’s 4 billion—supports scalable supply, underscoring the region’s next-wave influence on the tetanus toxoid vaccine market.

Europe, the Middle East, Africa and South America exhibit heterogeneous drivers. Europe maintains high coverage but confronts pockets of hesitancy. Forty-seven of 59 high-risk nations have now eliminated maternal and neonatal tetanus, many in Africa, reflecting successful donor-backed drives. AVMA’s USD 1 billion initiative seeks to lift Africa’s share of global output beyond today’s 0.2%. PAHO bulk-procurement models stabilise South American pricing. Collectively these regions broaden geographic diversity and mitigate concentration risks within the tetanus toxoid vaccine market.

Regulatory Landscape

Regulation of tetanus toxoid-containing vaccines is grounded in widely used quality, safety, and potency expectations for toxoid manufacture and batch release. WHO maintains tetanus vaccine standardization norms (including guidance referenced under TRS frameworks) and runs the WHO Prequalification (PQ) program to qualify DT/Td and related products for UNICEF, Gavi, and other international procurement, making PQ status a practical gatekeeper for multilateral tenders. In the United States, FDA oversight of licensed tetanus-containing products and post-approval changes is handled under biologics regulation and labeling controls, including product-specific regulatory documentation for Td vaccines such as TENIVAC.

In Europe, vaccine development and lifecycle management is shaped by EMA scientific vaccine guidelines and pediatric development requirements, including standard Paediatric Investigation Plans (PIPs) for common combination-vaccine classes. Separately, the European Pharmacopoeia (Ph. Eur.) Commission has updated tetanus-vaccine monographs to rationalize toxicity testing requirements while preserving batch release safeguards, which affects QC strategies and comparability packages for manufacturers supplying the region. Across markets, the regulatory trajectory continues to favor combined formulations (DT/Td/Tdap and higher-valent pediatric combinations) over standalone TT, with potency requirements assessed for each antigenic component in multivalent products.

Competitive Landscape

Global supply is moderately concentrated among Sanofi, GSK, Pfizer, Merck and Serum Institute of India. The latter lifted its share to 24% by 2023, benefiting from cost competitiveness and prequalification wins. Emerging Asian firms such as CanSino, Bharat Biotech and multiple Chinese biologics manufacturers are scaling capabilities, especially in combination and adult-dose formulations, increasing rivalry inside the tetanus toxoid vaccine market.

Strategic themes include thermostable R&D—Stablepharma’s SPVX02 could up-end cold-chain economics —and monoclonal antitoxin therapies such as Trinomab’s Sintetol, which offers rapid antibody delivery for post-exposure management. Regulatory environments are diverging; compliance agility therefore becomes a competitive differentiator. Price pressure persists as pooled tenders weigh suppliers against one another, yet differentiation through platform science and adult-specific dossiers promises margin defence. White-space exists in Africa-based manufacturing where local players may leverage AVMA grants to secure regional tenders, slowly diluting import dependence in the tetanus toxoid vaccine market.

Post-2027, mRNA combination candidates could redefine barriers to entry by compressing lead times and enabling flexible antigen swaps, causing incumbent toxoid producers to invest in new platform capabilities. Consolidation risk remains if smaller suppliers cannot fund next-generation upgrades, possibly raising the tetanus toxoid vaccine industry’s concentration over the long term.

Tetanus Toxoid Vaccine Industry Leaders

Sanofi (Sanofi Pasteur, Inc)

Pfizer, Inc

GSK plc

Serum Institute of India Pvt. Ltd.

Merck & Co., Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Life-course immunization policies and procurement mechanisms are creating specific whitespace in adult and adolescent Td/Tdap supply, particularly where schedules move away from standalone TT and where tenders shift specifications toward DT/Td. Multilateral procurement remains a core opportunity channel, since UNICEF contracting dynamics and WHO PQ access determine which suppliers can participate at scale, and WHO’s Vaccines Prequalification Priority List for 2024-2026 explicitly includes DT and adult Td, reinforcing development and registration focus on these SKUs. Separately, the size of institutional demand and the concentration of qualified supply are underscored by WHO-prequalified manufacturers collectively maintaining around 500 million doses per year of Td production capacity, which supports a case for entrants to pursue PQ and strengthen dossier readiness for tender eligibility.

Technology and product-format upgrades provide a second set of opportunities. Thermostable and cold-chain-light approaches, alongside advanced purification methods used to meet modern safety and potency expectations for multivalent combinations, target wastage and distribution constraints that limit coverage in remote and resource-constrained settings. Demand is also reinforced by the broader shift toward combination vaccines that include tetanus toxoid as a component or carrier platform in larger immunization portfolios, including multivalent constructs such as MenACWY-TT and higher-valent pediatric combinations, which ties tetanus-antigen pull to schedule modernization rather than only monovalent booster cycles. On the access side, WHO’s May 2026 move to mandate use of its electronic Prequalification System (ePQS) for vaccine applications introduces a specific operational compliance requirement for manufacturers competing in internationally procured channels.

Recent Industry Developments

- April 2026: Central Research Institute (CRI), Kasauli, committed to supplying 55 lakh doses of its new tetanus and adult diphtheria (Td) vaccine to India’s Universal Immunization Programme (UIP). The supply commitment supports India’s program shift from TT to Td, expanding the domestic public-sector addressable market for Td formulations and strengthening supply security through indigenous production.

- May 2025: UK health authorities reiterated routine immunization messaging through the UK Vaccine Update, including schedule adherence for tetanus-containing vaccines and booster awareness. Ongoing official communications support sustained demand through primary care channels and reinforce policy-driven uptake for combined formulations used in routine and booster settings.

- June 2024: CDC’s ACIP voted to add VAXELIS (Sanofi and Merck’s pediatric hexavalent combination vaccine that includes tetanus toxoid) to preferential recommendations to help prevent invasive Hib disease in American Indian and Alaska Native infants. Preferential positioning reinforces the role of higher-valent combination products in pediatric schedules, supporting continued volume pull-through for tetanus-containing antigens within combination vaccine portfolios.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market tracks revenues generated from tetanus toxoid containing human vaccines that are used for routine immunization, boosters, maternal programs, and post-injury prophylaxis, measured at the point of sale by manufacturers and normalized to USD across countries.

Scope exclusions: Veterinary tetanus vaccines and hyper immune tetanus antitoxin sera are excluded.

Segmentation Overview

- By Vaccine Type

- Diphtheria, Tetanus, and Pertussis (DTaP)

- Diphtheria and Tetanus (DT)

- Tetanus, Diphtheria, And Pertussis (Tdap)

- Other Vaccine Types

- By Age Group

- Paediatric (0-16 yrs)

- Adult (>16 yrs)

- By End User

- Hospitals & Trauma Centres

- Public Immunisation Clinics & EPI Sites

- Other End Users

- By Distribution Channel

- Government Procurement

- Private / Self-pay

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia-Pacific

- Middle-East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research starts by mapping a demand picture by country, then applying the revenue math. We review public immunization schedules, booster recommendations, and maternal vaccination guidance from sources such as the World Health Organization, UNICEF program materials, and national public health agencies.

Next, we add pricing and supply signals so the model does not depend on a single data series. Inputs such as government tender portals, publicly available procurement award notices, customs trade statistics, and peer-reviewed articles on vaccine coverage are used to shape volume, mix, and price bands by geography. Company filings and investor presentations are used to confirm where sales are weighted between public channel procurement and private market demand, and a paid subscription for company financials plus a shipment-level trade database are used selectively when public disclosures are limited. The desk inputs listed are illustrative only, and many other public and paid sources were also referenced for collection, cross-checks, and clarification.

Primary Interviews and Surveys

Primary work is used to pressure-test assumptions that cannot be read directly from public documents, such as tender winning price ranges, realistic wastage buffers, and how combination vaccines shift demand away from monovalent boosters. We speak with procurement stakeholders, immunization program advisors, distributors, and hospital pharmacy contacts across major regions so the final sizing reflects how vaccines are actually bought, stored, and administered.

These discussions also help confirm what is counted as tetanus toxoid containing revenue in practice, particularly where bundled pediatric doses and maternal booster programs share the same supply chain.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 12% | APAC: 42% |

| Mid tier: 50% | Functional/Unit leaders: 36% | EMEA: 36% |

| Smaller Players: 18% | Managers: 52% | Americas: 22% |

Market-Sizing & Forecasting

Sizing is built using a top-down demand pool that reconstructs doses from immunization schedules, target populations, and measured coverage, then converts those doses into revenue using country-level price bands. Key inputs include birth cohort size, booster timing adherence, maternal vaccination uptake, program coverage rates, and the share of combination vaccines in pediatric schedules, which together explain why dose volumes and product mix differ by country.

After the demand pool is formed, we cross-check outputs with selective bottom-up approximations, such as sampled tender volumes multiplied by observed award prices, and manufacturer-level revenue splits where disclosures are available. If country data is missing or irregular, we handle gaps using peer-country analogs based on schedule similarity, income band, and procurement channel mix, then adjust the outputs after interview feedback.

For forecasting, we run scenario analysis because policy and procurement can change in steps rather than smoothly. Assumptions are moved using expected changes in coverage, booster policy enforcement, combination vaccine adoption, and tender pricing behavior, then reviewed with experts to keep the forward view realistic.

Data Validation & Update Cycle

Outputs are validated through cross-checks that compare modeled revenues with independent signals, including published coverage trends, tender activity patterns, and trade-flow direction for key producing countries. If a country result looks unusually high or low, we re-check the dose build-up, pricing inputs, and currency conversion timing, and we trigger follow-up calls when the difference cannot be explained.

Before sign-off, the model and assumptions go through a multi-step analyst review so arithmetic, unit conversions, and growth drivers line up with the underlying drivers. Reports are refreshed annually, and interim updates are made when material events occur, such as guideline shifts, major procurement changes, or supply disruptions. Right before delivery, a final pass is done to reflect the latest available public releases and interview learnings.

Mordor Intelligence's Tetanus Toxoid Vaccine Market Size Compared Against Other Published Estimates

Published market values for tetanus toxoid vaccines do not always match because the scope can shift between monovalent versus combination products, the price basis can differ between list pricing and tender awards, and the update timing can vary by publisher.

Veterinary tetanus vaccines sit outside Mordor Intelligence's scope, and that alone can move totals when a publisher blends human and animal immunization revenues. Other gaps usually come from whether pentavalent and hexavalent products are fully counted as tetanus toxoid containing revenue, how factory gate versus downstream pricing is treated, and whether currency conversion uses an average year rate or a point-in-time rate.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 6.47 B (2026) | |

| Industry Publisher A | USD 5.81 B (2024) | Different base year and forecast window can shift the reported current value, and the public summary does not clearly state whether combination vaccines are fully included or how tender pricing is normalized across countries. |

| Global Consultancy B | USD 5.41 B (2025) | Uses a factory gate framing and may apply a tighter price basis than blended public tender and private channel pricing, which can reduce totals even when similar vaccine types are listed as covered. |

Looking across the table, the spread is mainly explained by year selection and what is assumed for pricing and channel mix in public procurement heavy countries. By keeping the dose pool tied to coverage, schedule-driven demand, and realistic price bands, the estimate stays traceable to inputs that can be checked and updated as new program and tender signals appear.

Key Questions Answered in the Report

What is the current size of the tetanus toxoid vaccine market?

The tetanus toxoid vaccine market is valued at USD 6.47 billion in 2026 and is projected to reach USD 8.49 billion by 2031.

Which vaccine segment is growing fastest?

The Tdap segment posts the strongest momentum with a 7.75% CAGR through 2031, driven by adolescent, maternal and adult booster recommendations.

Why is Asia Pacific considered the high-growth region?

Asia Pacific combines expanding immunization programmes, large-scale manufacturing capacity in India and China and rising private-sector demand, leading to a 7.12% CAGR forecast.

How will thermostable technology affect the market?

Thermostable formulations like Stablepharma’s SPVX02 aim to eliminate cold-chain dependence, potentially cutting wastage and broadening reach in remote areas, thereby unlocking new demand pockets.

What are the main risks to supply continuity?

The manufacturing base remains concentrated; recent exits such as MassBiologics have caused regional shortages, and any similar disruptions can impact global availability until more suppliers gain WHO prequalification.

Are adult booster campaigns making a difference?

Yes. Adult uptake still lags paediatrics, but booster awareness, Medicare cost caps and rapid immunity tests are propelling a 6.33% CAGR in the adult segment, signalling a growing life-course market opportunity.

Page last updated on: