North America Cancer Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

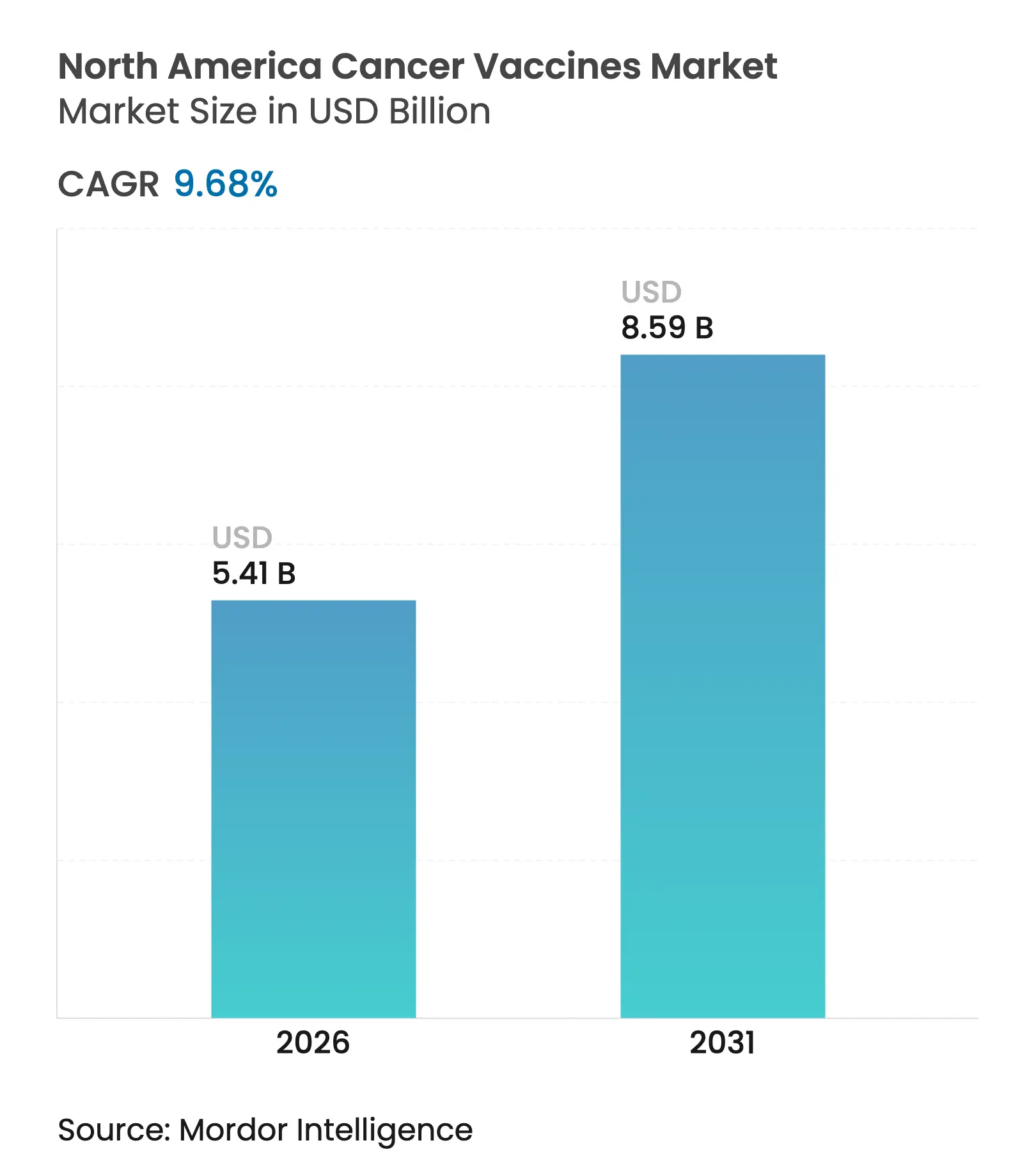

| Market Size (2026) | USD 5.41 Billion |

| Market Size (2031) | USD 8.59 Billion |

| Growth Rate (2026 - 2031) | 9.68 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

North America Cancer Vaccines Market Analysis by Mordor Intelligence

North America cancer vaccines market size in 2026 is estimated at USD 5.41 billion, growing from 2025 value of USD 4.93 billion with 2031 projections showing USD 8.59 billion, growing at 9.68% CAGR over 2026-2031. Rising clinical success of mRNA platforms, supportive public funding, and broader reimbursement policies are moving therapeutic vaccines from experimental status to mainstream precision-oncology tools. The American Cancer Society expects more than 2.04 million new cancer diagnoses in 2025, enlarging the eligible population for preventive and therapeutic vaccination programs. mRNA-driven pipelines, particularly for melanoma, are gaining momentum after breakthrough therapy designations, while hospital systems invest in point-of-care manufacturing hubs that shorten lead times for individualized products. Meanwhile, stronger coverage decisions by the Centers for Medicare & Medicaid Services (CMS) improve physician confidence that vaccine-based regimens will be reimbursed.

Key Report Takeaways

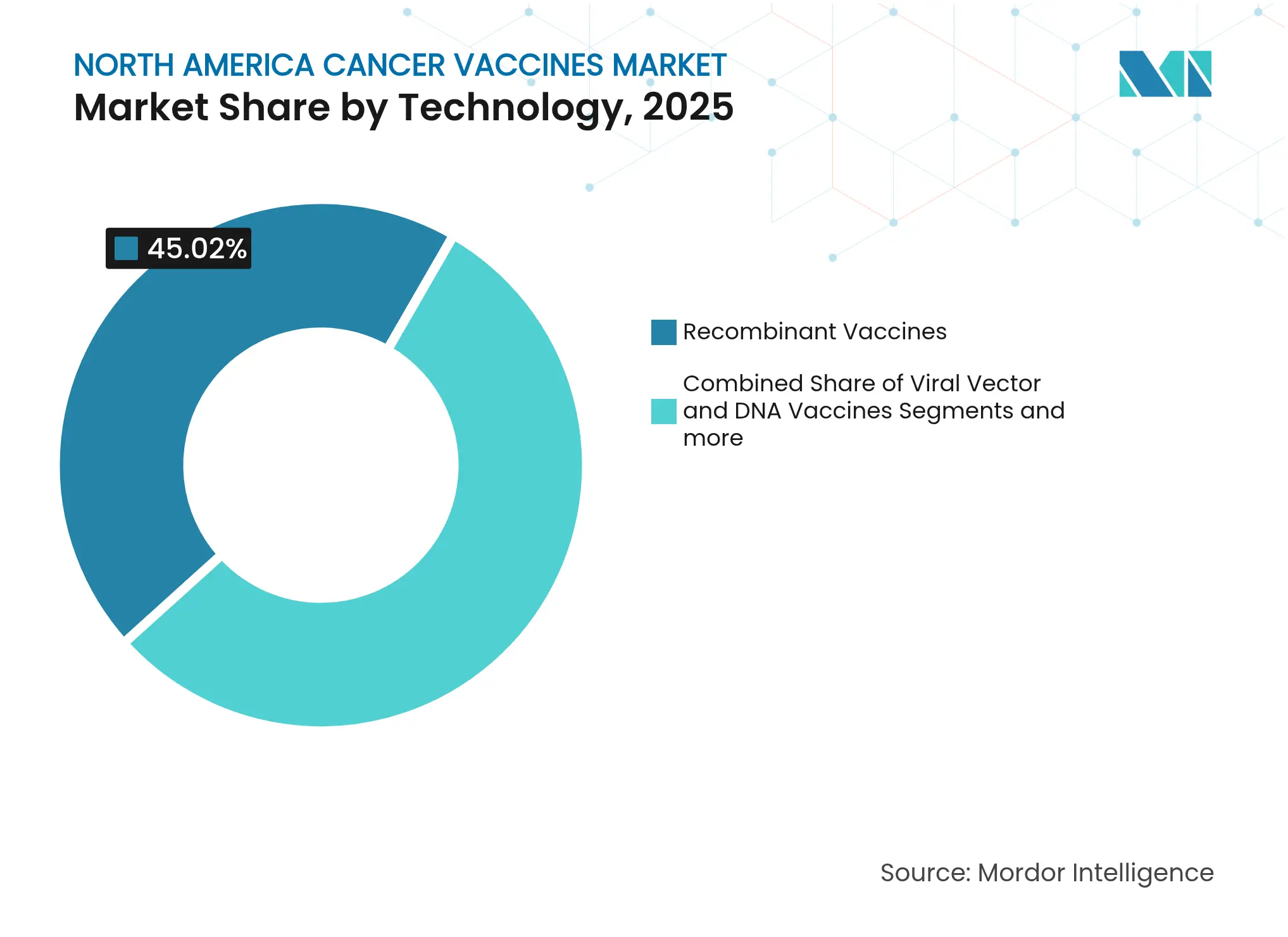

- By technology, recombinant vaccines led with 45.02% of North America cancer vaccines market share in 2025; mRNA/neoantigen platforms are slated to grow the fastest at a 10.22% CAGR to 2031.

- By treatment method, preventive products commanded 90.12% revenue share in 2025, while therapeutic vaccines are projected to expand at a 10.35% CAGR through 2031.

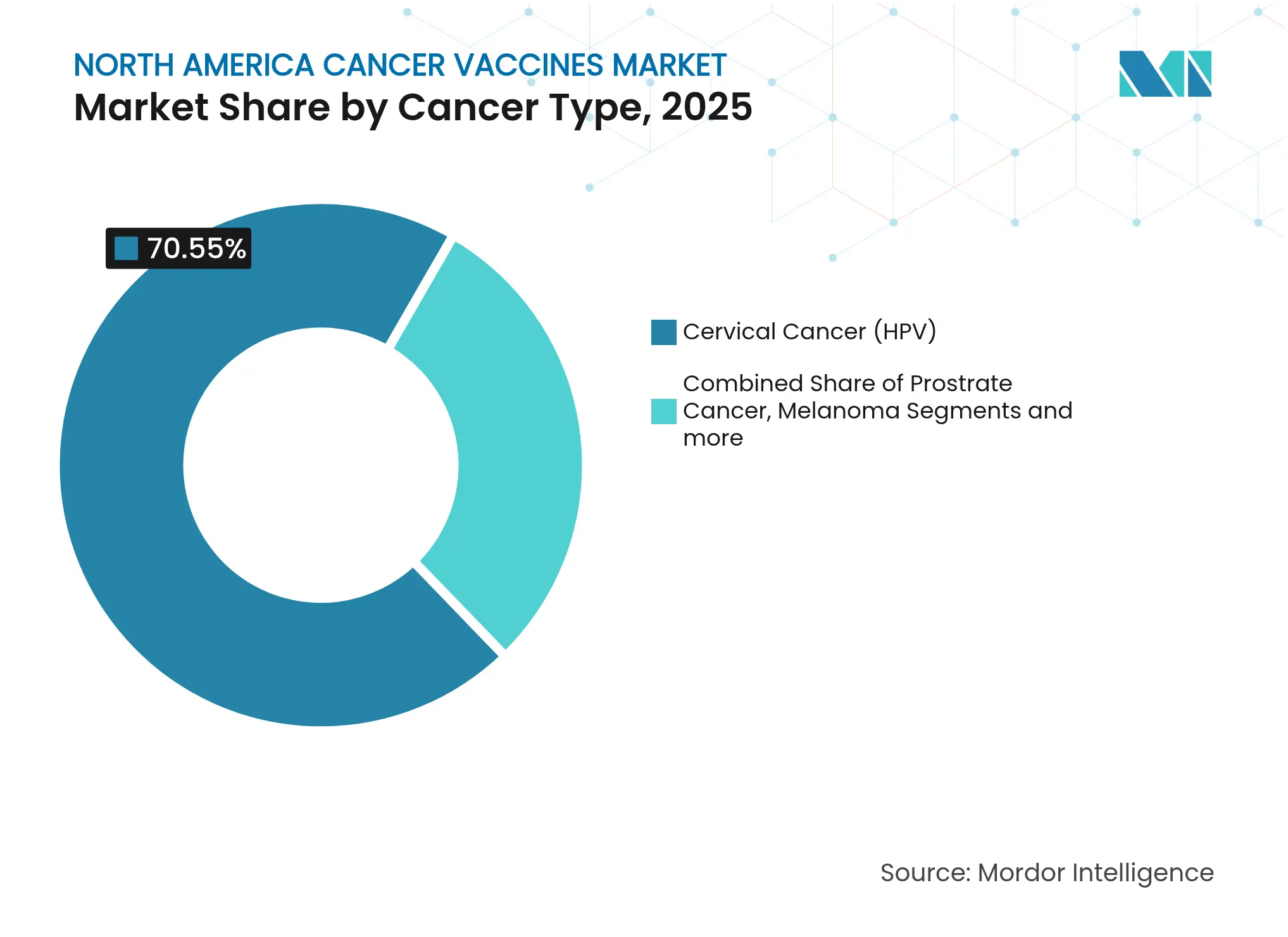

- By cancer type, cervical cancer (HPV) vaccines accounted for 70.55% of the North America cancer vaccines market size in 2025; melanoma vaccines show the highest growth at a 10.44% CAGR to 2031.

- By delivery route, intramuscular administration secured 63.92% revenue share in 2025, whereas intravenous delivery is advancing at a 10.37% CAGR over the forecast period.

- By geography, the United States held 85.88% of the North America cancer vaccines market size in 2025; Canada is set to post the fastest 10.28% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Cancer Vaccines Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Surging cancer incidence & screening rates

Surging cancer incidence & screening rates

| +2.1% | Global, concentrated in North America | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

+2.1%

|

Geographic Relevance

:

Global, concentrated in North America

|

Impact Timeline

:

Medium term (2-4 years)

|

Accelerating government & VC funding for vaccine

pipelines

Accelerating government & VC funding for vaccine

pipelines

| +1.8% | United States & Canada primary, Mexico emerging | Short term (≤ 2 years) | |||

Rapid advances in mRNA & neo-antigen platforms

Rapid advances in mRNA & neo-antigen platforms

| +2.3% | United States leadership, Canada following | Medium term (2-4 years) | |||

CMS reimbursement expansion for therapeutic vaccines

CMS reimbursement expansion for therapeutic vaccines

| +1.2% | United States exclusive | Short term (≤ 2 years) | |||

Hospital-based personalized manufacturing hubs

Hospital-based personalized manufacturing hubs

| +0.9% | United States & Canada major medical centers | Long term (≥ 4 years) | |||

Cross-border clinical-trial harmonization within USMCA

Cross-border clinical-trial harmonization within USMCA

| +0.7% | USMCA region-wide | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Surging Cancer Incidence & Screening Rates

Early detection programs are identifying cancers at stages where vaccine-based interventions can add meaningful benefit. The United States expects more than 2.04 million new cancer cases in 2025, a historic first above the 2 million mark [1]American Cancer Society, “Cancer Facts & Statistics 2025,” cancer.org . Canada projects 247,100 new cases in 2024, with male incidence surpassing female levels, opening room for gender-specific vaccine campaigns [2]Darren R. Brenner, "Projected estimates of cancer in Canada in 2024," CMAJ, cmaj.cacmaj.ca. Provincial HPV-based screening in British Columbia is enabling earlier cervical lesion detection, which strengthens the clinical value proposition of both preventive and therapeutic vaccines. Routine skin imaging for high-risk individuals is likewise catching melanoma at stages where mRNA vaccines have shown benefit. Together, rising incidence and better screening broaden the pool of treatable patients, helping the North America cancer vaccines market grow at nearly double-digit speed.

Accelerating Government & VC Funding for Vaccine Pipelines

Federal agencies are positioning advanced vaccine science as a national security priority that extends well beyond infectious-disease preparedness. The U.S. Department of Health and Human Services granted USD 590 million to Moderna in January 2025 for pandemic influenza work, but the same production lines can pivot to oncology payloads [3]U.S. Department of Health and Human Services, “Moderna Award Notice,” hhs.gov . BARDA’s Accelerator Network 2.0 is channeling multi-year grants into rapid-response therapeutics, including cancer vaccines, which lowers venture-capital risk. The National Cancer Institute earmarked USD 4.25 million in FY2024 for the Cancer Immunoprevention Network to finance early research. ARPA-H’s APECx program is applying artificial intelligence to antigen discovery, shrinking development cycles from years to months. With layered public and private capital, platform companies can scale manufacturing quickly, supporting the long-run expansion of the North America cancer vaccines market.

Rapid Advances in mRNA & Neo-antigen Platforms

mRNA design, automation, and AI-driven epitope selection are converging to make fully personalized vaccines a commercial reality. Moderna and Merck’s mRNA-4157/V940 cut recurrence or death risk by 49% in high-risk melanoma over a 3-year follow-up, confirming durable antitumor immunity. BioNTech’s autogene cevumeran sustained immune responses in 8 of 16 pancreatic cancer patients over the same period. Machine-learning models now screen thousands of tumor mutations in days, isolating the few epitopes most likely to trigger robust T-cell activity. Automated production suites reduce batch release from months to weeks, enabling real-time manufacture following tumor sequencing. These breakthroughs help the North America cancer vaccines market outpace legacy biologic modalities.

CMS Reimbursement Expansion for Therapeutic Vaccines

Regulatory clarity and payment certainty are catalyzing uptake. CMS updated its billing code set for genetic oncology testing in 2025, ensuring that tumor-sequencing costs critical to neoantigen identification are reimbursed. Medicare now covers preventive vaccines such as HPV at 100%, eliminating coinsurance hurdles that previously dampened uptake. Coverage decisions for emerging melanoma vaccines establish pathways for broader solid-tumor indications. Payer endorsement reduces provider hesitation and signals that vaccine-based regimens will be treated similarly to monoclonal antibodies or small-molecule targeted therapies. As a result, the North America cancer vaccines market gains momentum from both clinical and economic standpoints.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Stringent CMC validation & long lead-times

Stringent CMC validation & long lead-times

| -1.4% | Global, particularly stringent in United States | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:

-1.4%

|

Geographic Relevance

:

Global, particularly stringent in United States

|

Impact Timeline

:

Medium term (2-4 years)

|

Competition from next-gen cell & gene therapies

Competition from next-gen cell & gene therapies

| -1.1% | United States & Canada advanced markets | Long term (≥ 4 years) | |||

Limited cold-chain infrastructure for novel lipid-NP

vaccines

Limited cold-chain infrastructure for novel lipid-NP

vaccines

| -0.8% | Rural North America, Mexico infrastructure gaps | Short term (≤ 2 years) | |||

Public vaccine-safety skepticism

Public vaccine-safety skepticism

| -0.6% | United States & Canada, rural populations | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Stringent CMC Validation & Long Lead-times

Chemistry, Manufacturing, and Controls (CMC) rules are rigorous for products that change from patient to patient. The Coalition for Epidemic Preparedness Innovations notes that stability and analytics reviews alone can add 18-24 months to timelines. Each personalized mRNA batch must pass individual sterility and potency checks, lengthening production by 4-6 weeks. The U.S. Food and Drug Administration is still drafting guidance on AI algorithms used in neoantigen prediction, introducing regulatory ambiguity. Firms with deep quality-control expertise can absorb the overhead, but smaller entrants may struggle, which tempers near-term growth in the North America cancer vaccines market.

Competition from Next-gen Cell & Gene Therapies

Advanced cell therapies are capturing physician mindshare and hospital infrastructure budgets. Bristol Myers Squibb’s USD 11.1 billion alliance with BioNTech for the BNT327 bispecific program illustrates big-pharma appetite for cell-engaging technologies. Academic centers report that 63% now manufacture CAR-T products on-site, creating alternative pathways for patients who might otherwise enroll in vaccine trials. In hematologic malignancies, CAR-T outcomes remain stronger than vaccine monotherapy, and reimbursement frameworks are well established. While vaccines are gaining share in solid tumors, competition from cell and gene modalities can divert capital and clinical-trial enrollment, modestly dampening the North America cancer vaccines market trajectory.

Segment Analysis

By Technology: mRNA Platforms Disrupt Recombinant Dominance

Recombinant products led the North America cancer vaccines market with 45.02% share in 2025, powered by mature supply chains and decades of regulatory familiarity. However, the segment is forecast to cede momentum to mRNA vaccines, which are expanding at a 10.22% CAGR through 2031. Moderna and Merck’s V940 secured FDA breakthrough status after demonstrating a 49% risk reduction for melanoma recurrence. Other mRNA candidates, such as BioNTech’s BNT111, are posting meaningful response rates when combined with checkpoint inhibitors. The shift underscores a structural advantage: synthetic RNA avoids cell-culture bottlenecks, letting producers pivot quickly to new indications.

Automation and AI are now embedded in end-to-end workflows, trimming development cycles from several years to under twelve months for follow-on products. Viral-vector and DNA platforms continue to play niche roles but face limits in immunogenicity and scalability. Whole-cell and dendritic approaches carry high costs tied to individualized processing. As these realities become clearer, capital reallocates toward RNA specialists, anchoring medium-term expansion of the North America cancer vaccines market.

Note: Segment shares of all individual segments available upon report purchase

By Treatment Method: Therapeutic Vaccines Accelerate Despite Preventive Dominance

Preventive modalities still dominate, accounting for 90.12% revenue in 2025, largely due to nationwide HPV programs with robust CMS coverage. Yet therapeutic products are accelerating at 10.35% CAGR as real-world evidence validates their role in adjuvant and neoadjuvant settings. Canada’s updated guidelines endorse single-dose HPV schedules for ages 9-20, improving coverage while freeing budgets for therapeutic pilots.

Mount Sinai’s PGV001 study maintains 5-year survival in almost half of participants across multiple tumor types. Vvax001 has shown a 94% reduction in cervical intraepithelial neoplasia lesions. Health-system pilots increasingly combine prophylactic and treatment strategies, envisioning lifetime immunization pathways. These developments reinforce strong growth prospects for therapeutic injections, sustaining the North America cancer vaccines market expansion toward 2030.

By Cancer Type: Melanoma Vaccines Challenge HPV Dominance

Cervical cancer (HPV) vaccines held 70.55% of the 2025 market, reflecting decades of epidemiologic validation and school-based inoculation programs. However, melanoma products are set to grow at 10.44% CAGR on the back of favorable biology: high mutational burden yields abundant neoantigen targets. Moderna and Merck launched multiple Phase 3 trials with 680 participants across North America and Europe to evaluate adjuvant use in both melanoma and non-small-cell lung settings.

Prostate and pancreatic candidates are gaining regulatory momentum, with CAN-2409 receiving FDA RMAT designation after cutting recurrence risk by 30% in combination with radiation. As databases catalog tumor-specific epitopes, platform companies can spin out new trials without rebuilding manufacturing assets, boosting addressable revenue. The disease-specific expansion ensures that the North America cancer vaccines market sustains double-digit pace even after HPV penetration plateaus.

Note: Segment shares of all individual segments available upon report purchase

By Delivery Route: Intravenous Innovation Challenges Intramuscular Standards

Intramuscular injection accounted for 63.92% market share in 2025, benefitting from existing supply chains and clinician familiarity. Yet intravenous formulations are moving ahead at a 10.37% CAGR because complex biologics often need controlled infusion. Dendritic-cell and lipid-NP vaccines are too large for typical intramuscular volumes, and infusion centers already accommodate monoclonal antibodies, making the shift operationally smooth.

Hospital oncology suites are retrofitting with closed-system bioreactors so that patient-specific material can be produced and infused in the same facility. Intradermal and subcutaneous techniques stay relevant for dose-sparing protocols and for rural outreach where cold-chain logistics are limited. Nonetheless, infrastructure build-outs at academic hubs point toward intravenous anchoring of future regimens, contributing to the broadened scope of the North America cancer vaccines market.

Geography Analysis

The United States retains 85.88% market control, fueled by dense biopharma clusters, a decisive FDA, and extensive CMS reimbursement. Federal stimulus—USD 590 million for Moderna’s platform and BARDA’s multibillion-dollar medical countermeasure fund—cements a pipeline of trial-ready candidates. With more than 2.04 million new diagnoses expected in 2025, demand for both prophylactic and therapeutic solutions remains strong. Streamlined coverage for genetic testing shortens patient journeys from biopsy to vaccine formulation, while hospital-based manufacturing hubs speed delivery. Such enablers keep the North America cancer vaccines market anchored in the United States for the foreseeable future.

Canada is the fastest riser, projected at a 10.28% CAGR through 2031. The Public Health Agency’s endorsement of single-dose HPV schedules for ages 9-20 aims for 90% coverage by decade’s end. British Columbia’s 10-Year Plan seeks cervical cancer elimination by 2034. The country expects 247,100 new cases in 2024. Federally funded biomanufacturing initiatives in Ontario and Quebec encourage local production, and Health Canada’s alignment with FDA guidelines accelerates clinical trial approvals. These moves widen the North America cancer vaccines market footprint north of the border.

Mexico shows early promise but faces systemic challenges. Its national HPV campaign demonstrates public-health readiness, yet therapeutic access is spotty, partly for cost reasons. USMCA’s clinical-trial harmonization could invite greater cross-border collaboration, but incomplete intellectual-property enforcement reduces foreign direct investment. Large geography and rural cold-chain gaps complicate distribution of lipid-NP vaccines. Unless regulatory predictability improves, Mexico will likely remain a slow-growing but important long-term component within the North America cancer vaccines market.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

Competitive Landscape

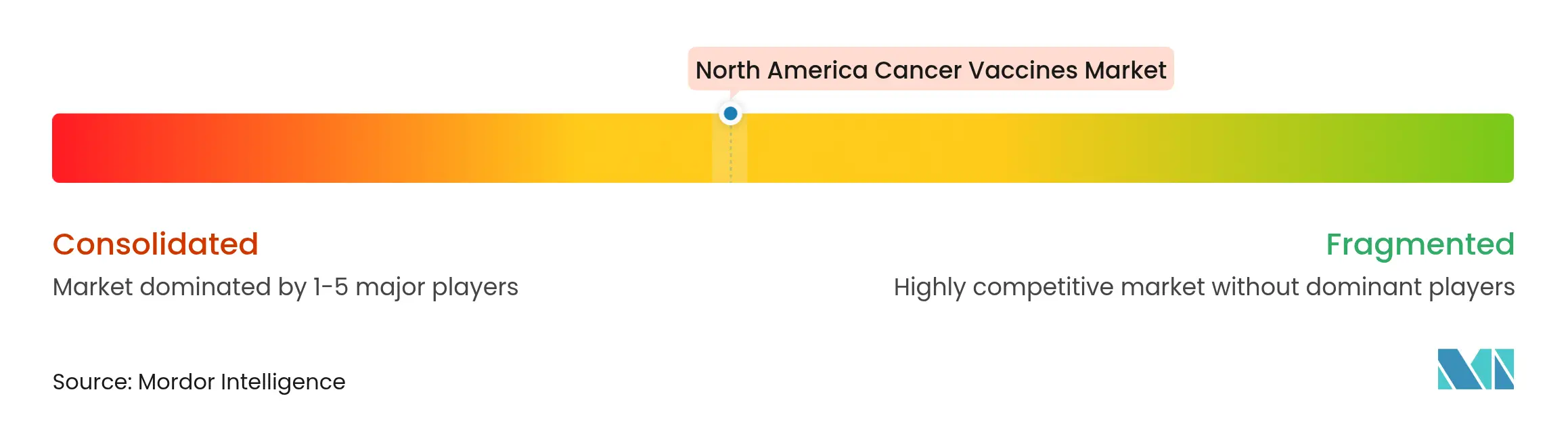

Market Concentration

The North America cancer vaccines market shows moderate concentration, with platform specialists and legacy vaccine houses vying for leadership. Bristol Myers Squibb’s USD 11.1 billion tie-up with BioNTech for BNT327 signals a strategic pivot toward bispecific combinations that integrate vaccine priming with antibody-mediated cytotoxicity. Merck exercised a USD 250 million option on Moderna’s V940, underscoring big-pharma confidence in mRNA personalization. Pfizer and Gritstone are advancing a self-amplifying RNA candidate for lung cancer, leveraging manufacturing built during the COVID-19 era.

Academic centers such as Memorial Sloan Kettering and MD Anderson are investing in GMP suites to make patient-specific doses on-site, reducing logistical hurdles. AI-native firms like NEC Bio are licensing epitope-prediction engines, forging software–wet-lab alliances.

On the downside, cold-chain intensity and stringent CMC oversight impose high fixed costs that smaller entrants struggle to absorb. As market leaders consolidate, mid-tier firms may gravitate toward niches like tumor-associated antigen (TAA) vaccines. The resulting landscape reinforces the scale advantages enjoyed by top players, guiding the North America cancer vaccines market toward gradual concentration over the next five years.

North America Cancer Vaccines Industry Leaders

*Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Anixa Biosciences received a USPTO Notice of Allowance covering novel breast-cancer vaccine compositions licensed from Cleveland Clinic.

- March 2025: Researchers at Icahn School of Medicine, Mount Sinai, reported positive Phase 1 data for PGV001, a personalized multi-peptide vaccine that maintained durable immune responses.

- March 2025: The U.S. FDA cleared Everest Medicines’ IND for EVM14, a tumor-associated antigen (TAA) vaccine aimed at solid tumors.

- October 2024: Merck and Moderna began a Phase 3 trial of adjuvant V940 (mRNA-4157) plus Keytruda in certain non-small-cell lung cancers, expanding beyond melanoma.

Table of Contents for North America Cancer Vaccines Industry Report

1. Introduction

- 1.1Study Assumptions & Market Definition

- 1.2Scope of the Study

2. Research Methodology

3. Executive Summary

4. Market Landscape

- 4.1Market Overview

- 4.2Market Drivers

- 4.2.1Surging cancer incidence & screening rates

- 4.2.2Accelerating government & VC funding for vaccine pipelines

- 4.2.3Rapid advances in mRNA & neo-antigen platforms

- 4.2.4CMS reimbursement expansion for therapeutic vaccines

- 4.2.5Hospital-based personalized manufacturing hubs

- 4.2.6Cross-border clinical-trial harmonization within USMCA

- 4.3Market Restraints

- 4.3.1Stringent CMC validation & long lead-times

- 4.3.2Competition from next-gen cell & gene therapies

- 4.3.3Limited cold-chain infrastructure for novel lipid-NP vaccines

- 4.3.4Public vaccine-safety skepticism

- 4.4Regulatory Landscape

- 4.5Porters Five Forces Analysis

- 4.5.1Threat of New Entrants

- 4.5.2Bargaining Power of Buyers

- 4.5.3Bargaining Power of Suppliers

- 4.5.4Threat of Substitutes

- 4.5.5Competitive Rivalry

5. Market Size & Growth Forecasts

- 5.1By Technology

- 5.1.1Recombinant Vaccines

- 5.1.2Viral Vector & DNA Vaccines

- 5.1.3mRNA/Neoantigen Personalised Vaccines

- 5.1.4Whole-cell & Dendritic Cell Vaccines

- 5.1.5Other Technologies

- 5.2By Treatment Method

- 5.2.1Preventive Vaccines

- 5.2.2Therapeutic Vaccines

- 5.3By Cancer Type

- 5.3.1Cervical Cancer (HPV)

- 5.3.2Prostate Cancer

- 5.3.3Melanoma

- 5.3.4Other Cancers

- 5.4By Delivery Route

- 5.4.1Intramuscular

- 5.4.2Intradermal / Sub-cutaneous

- 5.4.3Intravenous

- 5.5By Geography

- 5.5.1United States

- 5.5.2Canada

- 5.5.3Mexico

6. Competitive Landscape

- 6.1Market Concentration

- 6.2Market Share Analysis

- 6.3Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1Astellas Pharma Inc.

- 6.3.2Merck & Co. Inc.

- 6.3.3GlaxoSmithKline plc

- 6.3.4Bristol-Myers Squibb

- 6.3.5Dendreon

- 6.3.6Aduro BioTech Inc.

- 6.3.7Sanofi S.A.

- 6.3.8F. Hoffmann-La Roche AG (Genentech)

- 6.3.9Moderna Inc.

- 6.3.10BioNTech SE

- 6.3.11Inovio Pharmaceuticals

- 6.3.12Gritstone bio Inc.

- 6.3.13Agenus Inc.

- 6.3.14ImmunoGen Inc.

- 6.3.15Bavarian Nordic

- 6.3.16Northwest Biotherapeutics

- 6.3.17Celldex Therapeutics

- 6.3.18Vaccinex Inc.

- 6.3.19Transgene SA

- 6.3.20Geneos Therapeutics

7. Market Opportunities & Future Outlook

- 7.1White-space & Unmet-need Assessment

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Segmentation Overview

- By Technology

- Recombinant Vaccines

- Viral Vector & DNA Vaccines

- mRNA/Neoantigen Personalised Vaccines

- Whole-cell & Dendritic Cell Vaccines

- Other Technologies

- Recombinant Vaccines

- By Treatment Method

- Preventive Vaccines

- Therapeutic Vaccines

- Preventive Vaccines

- By Cancer Type

- Cervical Cancer (HPV)

- Prostate Cancer

- Melanoma

- Other Cancers

- Cervical Cancer (HPV)

- By Delivery Route

- Intramuscular

- Intradermal / Sub-cutaneous

- Intravenous

- Intramuscular

- By Geography

- United States

- Canada

- Mexico

- United States

Detailed Research Methodology and Data Validation

Primary Research

Desk Research

Market-Sizing & Forecasting

Data Validation & Update Cycle

Why Mordor's North America Cancer Vaccines Baseline Earns Trust

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 4.93 B (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 4.38 B (2024) | Regional Consultancy A | Earlier base year and combines prophylactic HPV procurement budgets without dose-level incidence checks | ||

USD 2.88 B (2023) | Global Consultancy A | Relies on historical sales, omits emerging mRNA/neoantigen pipeline and Mexico data | ||

USD 3.90 B (2024) | Industry Association B | Excludes therapeutic vaccines still under commercial compassionate use and applies flat ASP across technologies |