Preventive Vaccines Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

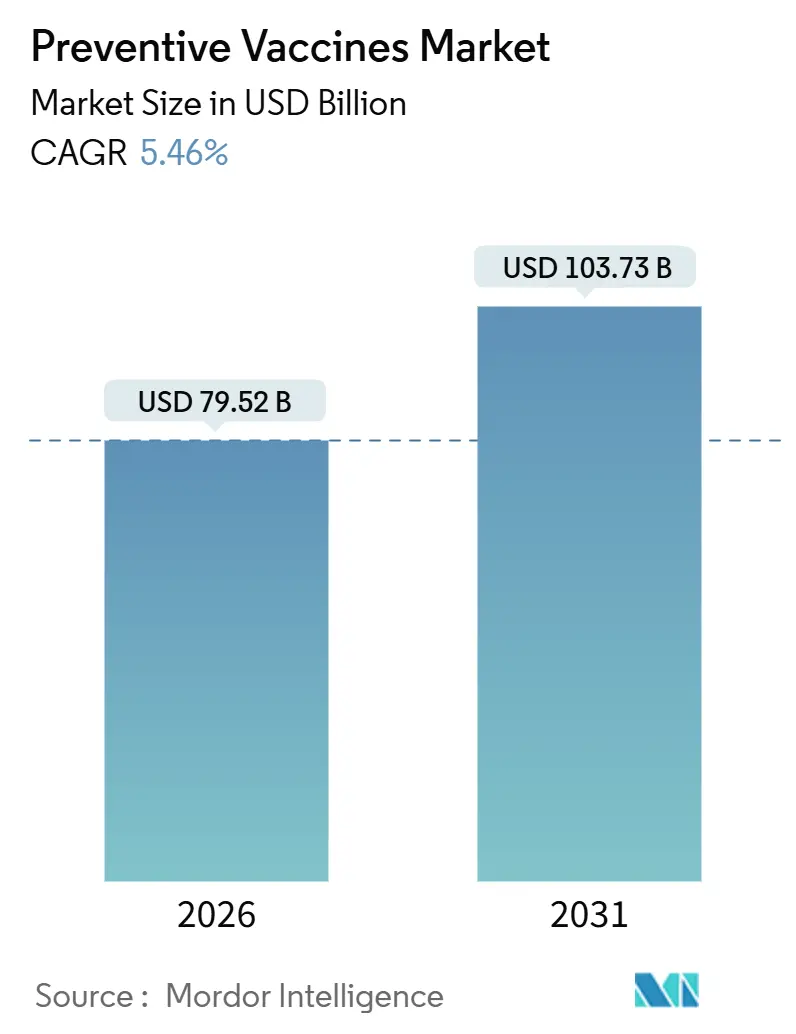

| Market Size (2026) | USD 79.52 Billion |

| Market Size (2031) | USD 103.73 Billion |

| Growth Rate (2026 - 2031) | 5.46% CAGR |

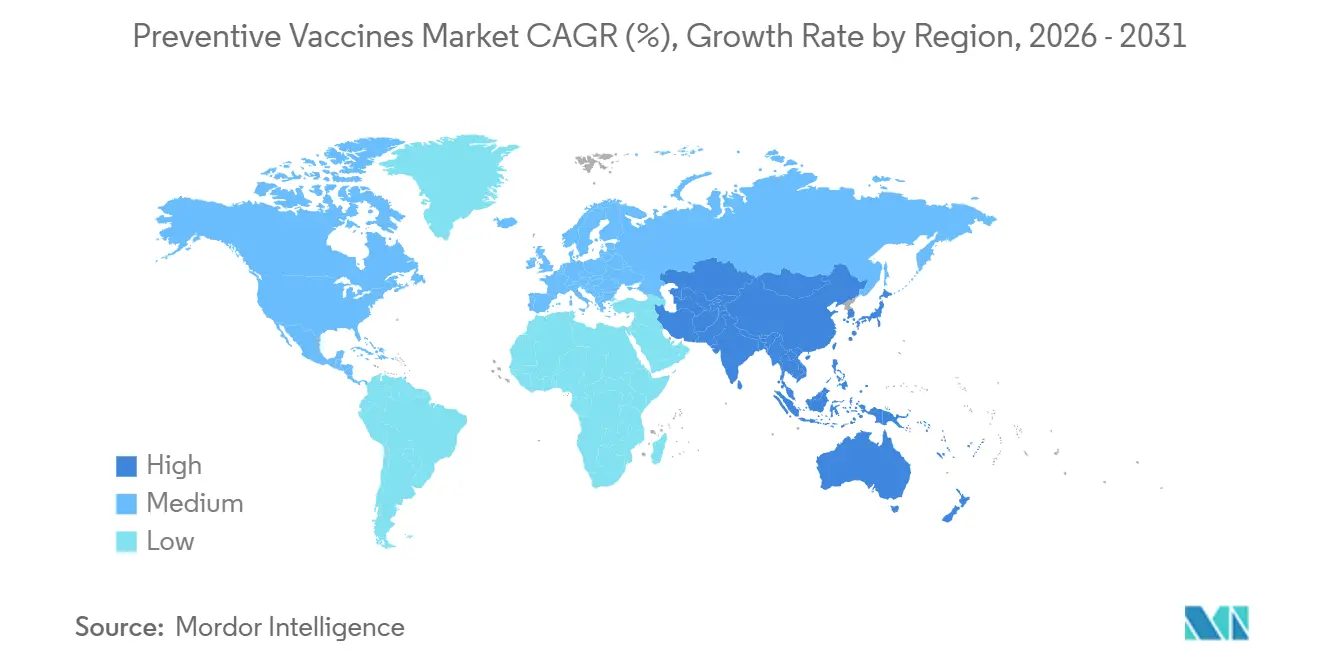

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

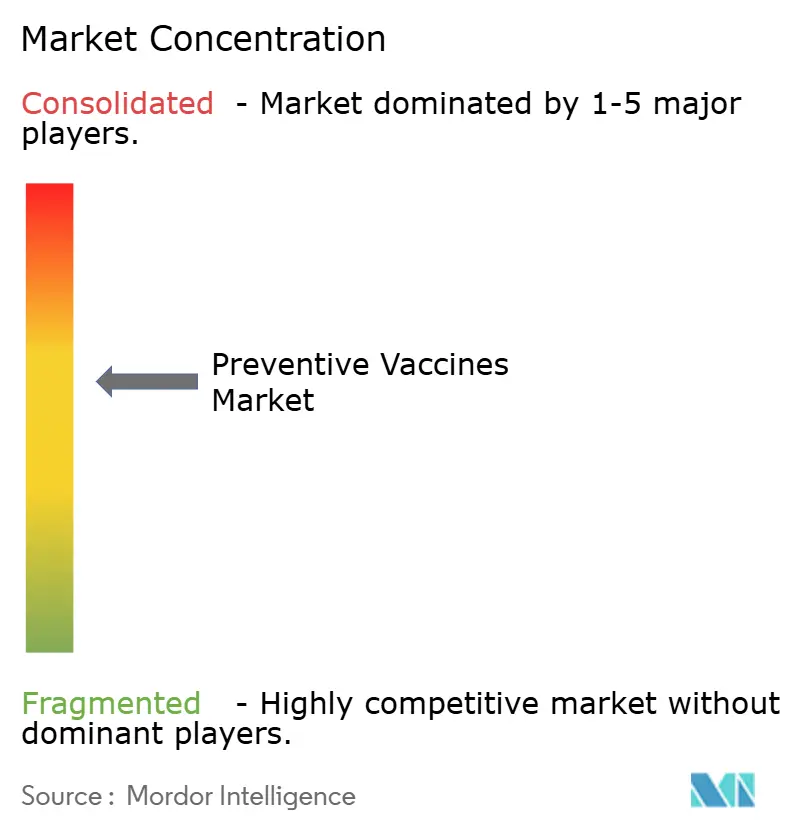

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Preventive Vaccines Market Analysis by Mordor Intelligence

The Preventive Vaccines Market size is estimated at USD 79.52 billion in 2026, and is expected to reach USD 103.73 billion by 2031, at a CAGR of 5.46% during the forecast period (2026-2031).

Robust platform migrations to mRNA, 90-day strain-update cycles, and life-course immunization mandates are the principal levers behind this expansion. Governments in low- and middle-income economies have digitized registries, enabling micro-targeted outreach that lifts completion rates while supporting premium adult formulations. Capacity localization in Asia-Pacific, coupled with 2 billion annual fill-finish doses added since 2024, has shifted price competition toward regional manufacturers offering 30%–40% cost advantages in tenders. High-margin adult and senior programs now divert revenue pools from childhood schedules as employers quantify productivity losses from respiratory infections. Meanwhile, regulatory fast-tracks for subunit and recombinant constructs remove cold-chain constraints and reversion risks, attracting capital to next-generation pipelines.

Key Report Takeaways

- By vaccine type, live and attenuated formulations led with 26.55% of preventive vaccines market share in 2025, while subunit and recombinant platforms are advancing at a 6.25% CAGR through 2031.

- By disease type, influenza captured 20.53% revenue in 2025; measles-mumps-rubella vaccines are forecast to expand at a 6.85% CAGR to 2031.

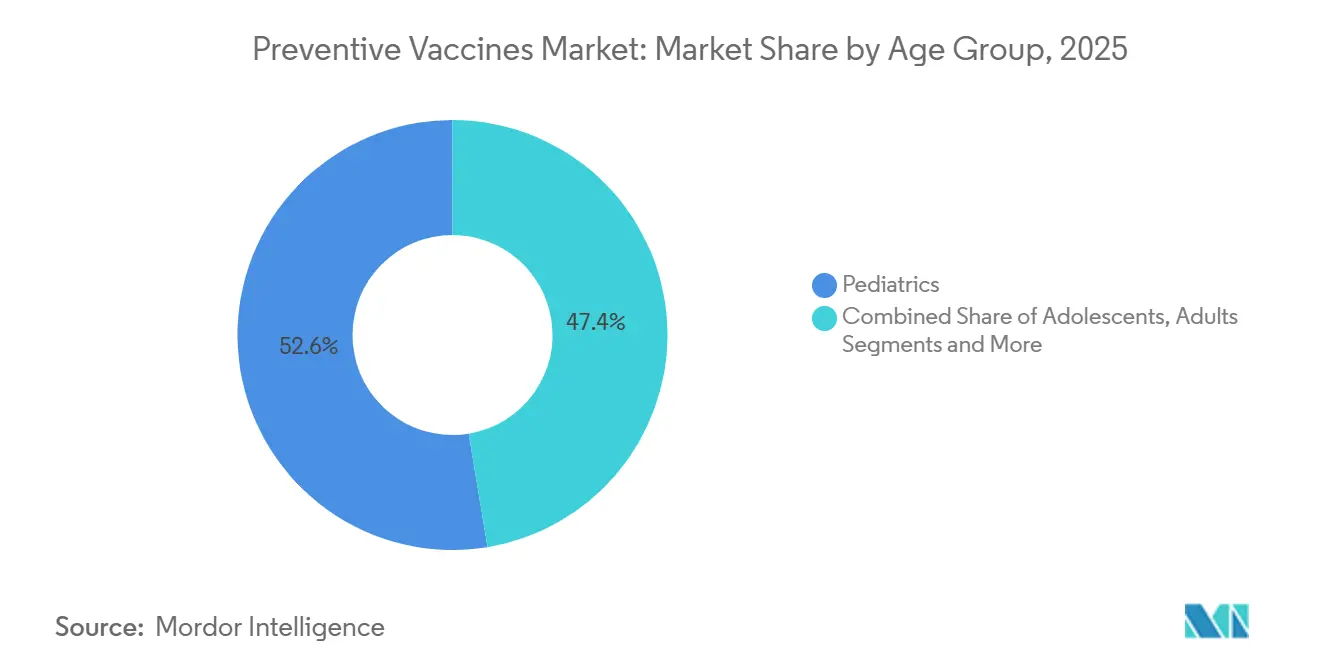

- By age group, pediatrics accounted for 52.63% share of the preventive vaccines market size in 2025, whereas adult vaccination is growing at a 7.87% CAGR over the outlook period.

- By end-user, government programs commanded 40.33% revenue in 2025, but online and tele-pharmacy channels are scaling at an 8.70% CAGR through 2031.

- By geography, North America captured 39.13% of the preventive vaccines market share in 2025, yet Asia-Pacific is forecast to expand at a 7.51% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Preventive Vaccines Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing prevalence of infectious diseases | +1.2% | APAC, Sub-Saharan Africa, global hotspots | Medium term (2-4 years) |

| Government immunization funding & mandates | +1.5% | North America, Europe, China, India | Long term (≥ 4 years) |

| Breakthroughs in mRNA & modular platforms | +0.9% | North America, Europe, secondary nodes in APAC | Medium term (2-4 years) |

| Expansion of life-course vaccination | +1.1% | North America, Europe, urban APAC | Long term (≥ 4 years) |

| Digital immunization registries | +0.6% | APAC, Sub-Saharan Africa, Latin America | Medium term (2-4 years) |

| Thermostable formulations | +0.4% | Sub-Saharan Africa, rural APAC, Latin America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence of Infectious Diseases

Measles cases climbed 15% across Southeast Asia and Sub-Saharan Africa from 2024 to 2025, reversing a decade of gains and triggering 60-day emergency procurements that reward suppliers with modular fill-finish lines. Vector expansion linked to urbanization and climate change is pushing clinicians to prioritize prevention for pathogens such as pneumococcus. U.S. RSV hospitalizations among infants rose 22% in the 2024-2025 season, prompting a maternal vaccination recommendation that opens an additional 3.7 million annual births to immunization. The net effect is a surge in base demand that reinforces the preventive vaccines market as a long-term growth platform.

Government Immunization Funding & Mandates

Global public budgets for vaccination escalated to USD 18.3 billion in 2025, up from USD 14.1 billion in 2023, as policymakers internalize outbreak costs[1]UNICEF, “Global Immunization Funding Report 2025,” unicef.org. The U.S. Vaccines for Children program widened eligibility to uninsured adults aged 19–26, adding 4.2 million beneficiaries for HPV and meningococcal coverage. India’s nationwide pneumococcal tender worth USD 420 million split evenly between Serum Institute and Bharat Biotech, underscoring domestic supply preference. Tightening school and workplace mandates in Europe are closing exemption loopholes and shoring up baseline uptake.

Breakthroughs in mRNA & Modular Vaccine Platforms

Moderna and BioNTech each brought online suites that can switch to any mRNA construct and output 100 million doses inside 90 days, demonstrated during the 2025 H3N2 influenza season[2]Moderna, “Annual Report 2025,” modernatx.com. Pfizer’s USD 1.2 billion capital program for lipid nanoparticle capacity aims to trim cost of goods by 40% by 2027. Thermostable mRNA candidates remain potent at 25 °C for 30 days and entered Phase III trials in 2025, allowing rural deployment without ultra-cold storage. The FDA’s Project NextGen bridges approval processes and shrinks variant timelines to 6 months, accelerating commercial cycles.

Expansion of Life-Course (Adult & Senior) Vaccination Programs

Adult vaccine revenue surpassed pediatric revenue in high-income economies during 2025 as employers financed workplace clinics and Medicare dropped cost-sharing for RSV, shingles, and pneumococcal shots. GSK’s Arexvy and Pfizer’s Abrysvo together delivered USD 2.8 billion in first-year sales, validating demand among seniors. Routine pneumococcal vaccination now targets adults aged 50–64 with chronic conditions, expanding the eligible U.S. market by 18 million people. Bundled visit protocols for flu, COVID-19, and pneumococcus lifted adherence to 67% in 14 U.S. health systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Risk of adverse events & hesitancy spikes | -0.8% | North America, Europe, global | Short term (≤ 2 years) |

| High R&D and compliance costs | -0.6% | Global, acute for SMEs | Long term (≥ 4 years) |

| Glass-vial & fill-finish bottlenecks | -0.5% | APAC, Latin America, global | Medium term (2-4 years) |

| Margin squeeze in MIC tenders | -0.4% | APAC, Latin America, Sub-Saharan Africa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Risk of Adverse Events & Hesitancy Spikes

The European Medicines Agency logged 1,847 serious events per 100 million doses in 2025, a flat rate versus 2023, yet social amplification temporarily depressed uptake[3]European Medicines Agency, “Vaccine Safety and Efficacy Data 2025,” ema.europa.eu. A well-publicized myocarditis case cut U.S. confidence by 9 points but rebounded within 8 months after updated risk-benefit data showed only 12.6 myocarditis cases per million doses against 450 hospitalizations averted per million COVID-19 infections. WHO’s Vaccine Safety Net flagged 3,200 misinformation posts reaching 50 million users, necessitating real-time fact-checking deals with platforms.

High R&D and Compliance Costs

Full cycle vaccine development costs USD 800 million–1.2 billion over 8–12 years, fencing out under-capitalized innovators. GMP compliance adds another USD 15–25 million in annual fixed overhead per line. Novavax spent USD 180 million on Phase III trials for its combo COVID-flu candidate, delaying profitability by 18 months. Merck is investing USD 600 million in next-generation Gardasil constructs ahead of European biosimilar entry in 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vaccine Type: Subunit Platforms Gain on Safety Profile

Live and attenuated products retained 26.55% preventive vaccines market share in 2025, anchored by MMR and varicella schedules. Subunit and recombinant platforms are forecast to advance at a 6.25% CAGR as regulators favor constructs that remove reversion risk and simplify logistics. Pfizer’s 20-valent Prevnar 20 secured 38% of the U.S. adult market within 12 months of its June 2024 launch by expanding serotype coverage. Inactivated polio and hepatitis A vaccines continue to dominate mass campaigns where dose cost rules procurement. Toxoid options retain steady booster demand tied to obstetric care and injury prophylaxis.

Momentum for mRNA vaccines extends beyond COVID-19 into influenza and RSV indications. Moderna began Phase III testing of a combined mRNA flu-COVID shot in January 2025, eyeing a 2027 launch that consolidates two annual injections into one. BioNTech’s malaria candidate entered Phase IIb in Tanzania and Mozambique during 2025, reusing its lipid nanoparticle platform to shave 3–4 years off typical timelines. Viral-vector and virus-like particle constructs play niche roles such as Ebola rings and HPV campaigns in cost-sensitive markets.

By Disease Type: MMR Resurgence Outpaces Influenza

Influenza held 20.53% of disease revenue in 2025, sustained by annual reformulation and employer programs. Measles-mumps-rubella vaccines are projected to grow 6.85% CAGR through 2031 as pandemic-era coverage gaps spark outbreaks; WHO tallied 120,000 measles cases in 2024, a 40% jump year over year. Pneumococcal vaccines benefit from wider age indications addressing resistant strains circulating in hospitals.

COVID-19 boosters transitioned to endemic status in 2025 with annual recommendations for older adults, generating USD 6.2 billion revenue in Q4 2025 alone for Pfizer and Moderna. HPV uptake accelerates in LMICs thanks to single-dose Gavi guidelines that cut costs 60% while maintaining efficacy. RSV shots for older adults and maternal schedules constitute the fastest-growing slice, a category absent before mid-2023.

By Age Group: Adult Vaccination Redefines Growth

Pediatrics held 52.63% of preventive vaccines market size volume in 2025, underpinned by entrenched birth-through-18 schedules. Adult uptake is tracking a 7.87% CAGR, driven by workplace clinics and expanded Medicare reimbursement that removed cost-sharing in January 2025. Influenza alone caused 8 million lost U.S. workdays in 2025, costing USD 3.2 billion, quadruple the price tag of universal employee vaccination.

Adolescents remain tied to HPV and meningococcal mandates, while geriatric cohorts gain priority as immune senescence magnifies hospitalization risk. Pfizer’s Abrysvo realized USD 1.4 billion in first-year sales, 68% derived from the 60-plus demographic. Retail pharmacies such as CVS and Walgreens delivered 42 million flu shots during the 2025-2026 season, a 15% uptick as extended hours cut scheduling friction.

By End-User: Online Channels Disrupt Traditional Models

Government programs maintained 40.33% revenue in 2025, leveraging tender power to fund mass campaigns. Online and tele-pharmacy distribution is set for an 8.70% CAGR, propelled by Amazon Pharmacy’s 2025 home-visit launch across 12 states and India’s 1mg platform embedding vaccine bookings within telemedicine flows. Hospitals and specialty clinics cater to immunocompromised populations needing bespoke schedules.

Retail pharmacies captured 28% of U.S. adult volume in 2025 as 48 states empowered pharmacists to deliver all CDC-recommended shots without prescriptions. Employers invested USD 1.1 billion in on-site clinics in 2025, slicing absenteeism by 2.3 days per worker during respiratory season. The preventive vaccines market continues to decentralize as digital platforms shrink scheduling friction and extend reach.

Geography Analysis

North America commanded 39.13% of preventive vaccines market share in 2025, sustained by high per-capita spending and rapid approval frameworks such as the FDA’s Project NextGen, which cut variant clearance timelines to 6 months. Medicare’s removal of cost-sharing expanded the senior addressable pool by 12 million individuals, and Canada synchronized RSV guidance in 2025, creating a unified continental demand curve.

Asia-Pacific is forecast to post a 7.51% CAGR to 2031, the swiftest worldwide. India’s USD 420 million pneumococcal tender split between Bharat Biotech and Serum Institute exemplifies capacity localization. China’s regulator cleared 14 new vaccines in 2025, including Sinopharm’s quadrivalent flu and CanSino’s inhaled COVID-19 booster, consistent with its Five-Year Plan innovation targets. Japan broadened HPV recommendations to boys in 2024, while Australia fast-tracked GSK’s RSV shot in 2025 to maintain synchronicity across high-income APAC nodes.

Europe relies on EMA harmonization and pooled procurement that amplify bargaining power. France and Germany mandated MMR for daycare entry in 2025, lifting demand by 1.2 million doses. Digital registries across 28 African countries cut zero-dose children 19% during 2024-2025 via mobile outreach. South American momentum centers on Brazil’s national program and PAHO tenders that trim unit costs up to 35%, while Argentina added meningococcal B for infants in 2025, opening a USD 28 million procurement lane.

Regulatory Landscape

Regulatory Landscape. Vaccine regulation continues to focus on quality, safety, and post-market surveillance across US FDA oversight, EMA guidance, and WHO prequalification processes. The FDA continues to guide strain selection and formulation updates through VRBPAC and related postmarketing commitments for respiratory vaccines.

In June 2026, WHO revised its prequalification procedures to reinforce GMP and production consistency for large international tenders. EMA’s 2026/2027 influenza composition guidance excludes the B/Yamagata lineage, which increases pressure on timely filings and synchronized manufacturing changes. The IA2030 immunization agenda also remains a reference point for regulatory strengthening and safety surveillance in LMIC markets.

Competitive Landscape

The preventive vaccines market sits at moderate concentration: the top firms, Pfizer, GSK, Sanofi, Merck, and others, collectively controlled a significant share of 2025 global revenue, yet regional challengers are eroding tender positions. Pfizer allocated USD 1.2 billion to lipid nanoparticle capacity in 2025 to lock down mRNA inputs, while Sanofi bought a French fill-finish specialist for USD 780 million to secure turnaround during seasonal peaks. Combination candidates such as Moderna’s Phase III flu-COVID shot could unlock a USD 4.5 billion segment by consolidating visits and cold-chain loads.

India’s Biological E won WHO prequalification for a thermostable typhoid conjugate in 2025, underpricing incumbents by 40% and capturing 18% of Gavi tenders inside six months. BioNTech’s modular factories can pivot to produce 100 million doses of any construct inside 90 days, creating cycle-time advantages amplified during influenza strain shifts. Pfizer filed 47 vaccine patents in 2025, 60% aimed at adjuvants that boost senior immune responses, underscoring corporate focus on the fastest-growing demographic.

Manufacturing missteps carry financial penalties: Takeda lost an estimated USD 320 million in 2024 revenue due to dengue vaccine supply delays, highlighting operational risk in a supply-constrained environment. Contract manufacturers able to guarantee glass-vial and aseptic capacity capture premium pricing as persistent shortages linger through mid-term horizons.

Preventive Vaccines Industry Leaders

Merck & Co

GSK plc

Johnson & Johnson Services, Inc.

Pfizer Inc.

Sanofi

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Market Opportunities and Future Outlook. Regional manufacturing and fill-finish capacity expansion is a visible theme in emerging markets. In Africa, Biovac announced an April 2026 expansion in Cape Town supported by a EUR 75 million quasi-equity investment from the EIB Group and a USD 20 million senior loan from IFC, with a target to produce 30-40 million doses annually.

Platform modernization and Industry 4.0 capabilities are creating commercialization lanes for suppliers that reduce changeovers while maintaining compliance standards. Separately, Merck opened a USD 1 billion vaccine manufacturing facility in Durham, North Carolina in March 2025, reinforcing scale-up capacity aimed at improving supply reliability. The EMA 2026/2027 guidance and WHO prequalification updates in 2026 also increase the demand for specialized quality, analytics, and validation services across the vaccine supply chain.

Recent Industry Developments

- June 2026: The US FDA approved an expanded indication for Merck's CAPVAXIVE (Pneumococcal 21-valent Conjugate Vaccine) for children and adolescents aged 2 through 17 at increased risk for pneumococcal disease. The label expansion extends competitive positioning in pneumococcal prevention across pediatric cohorts and reinforces breadth of serotype coverage.

- May 2026: Pfizer initiated a pivotal pediatric Phase 3 program for its 25-valent pneumococcal conjugate vaccine candidate (PF-07872412) following Phase 2 readouts. The program supports lifecycle management in pediatric and adult segments and strengthens the company's position in next-generation pneumococcal vaccines.

- January 2026: Merck completed its acquisition of Cidara Therapeutics, adding the long-acting antiviral candidate CD388 aimed at prevention of symptomatic influenza in high-risk individuals. The acquisition expands Merck's respiratory prevention footprint and aligns with immunization strategies for high-risk populations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the preventive vaccines market covers revenue from vaccines given to help stop infectious diseases before they occur, across routine immunization and broader public health programs in the covered geographies.

Scope exclusions: This sizing excludes therapeutic vaccines and revenue from pure vaccination services where the vaccine product value is not the priced unit.

Segmentation Overview

- By Vaccine Type

- Live / Attenuated Vaccines

- Inactivated Vaccines

- Subunit / Recombinant Vaccines

- Toxoid Vaccines

- mRNA Vaccines

- Other Vaccine Types

- By Disease Type

- Pneumococcal

- Poliovirus

- Hepatitis (A, B, E)

- Influenza

- Measles, Mumps & Rubella (MMR)

- COVID-19

- Human Papillomavirus (HPV)

- Respiratory Syncytial Virus (RSV)

- Other Disease Types

- By Age Group

- Pediatrics (0-18 yrs)

- Adolescents (12-18 yrs)

- Adults (19-59 yrs)

- Geriatrics (?60 yrs)

- By End-User

- Government Immunization Programs

- Hospitals & Specialty Clinics

- Retail & Community Pharmacies

- Online / Tele-pharmacy Channels

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build market context and to anchor major demand and supply signals before modeling. We typically reviewed public sources such as World Health Organization immunization datasets, UNICEF procurement and supply dashboards, US CDC vaccination coverage statistics, and national health ministry immunization program releases.

To turn these signals into workable inputs, we also checked vaccine approvals and product labels from regulators such as the US FDA and the European Medicines Agency, plus selected peer reviewed articles on vaccine schedules and coverage gaps. Company annual reports, investor presentations, and reputable press were reviewed to understand portfolio exposure, manufacturing expansions, and pricing commentary, and then a paid subscription for company financials and a patent database were used selectively for cross checks. These examples are not exhaustive, and many other sources were also referred to for data collection, validation, and clarification during the research.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with stakeholders across vaccine manufacturing, distribution, public health procurement, and provider settings, since these groups see real adoption and ordering patterns. We used these discussions to confirm which vaccines sit inside routine schedules in each region, how tender timing and stock rebuilding feed into annual sales, and where pricing and mix are changing.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 32% | CXOs: 17% | APAC: 50% |

| Mid tier: 51% | Functional/Unit leaders: 34% | EMEA: 32% |

| Smaller Players: 17% | Managers: 49% | Americas: 18% |

Market-Sizing & Forecasting

Sizing started with a top-down build where country level immunization demand pools were reconstructed from birth cohorts, routine schedule intensity, coverage rates, and public procurement volumes, then converted into value using typical dose pricing and mix assumptions. Results were corroborated with selective bottom-up checks, such as sampled vaccine price per dose multiplied by estimated administered doses for a short list of high volume antigens, plus supplier and channel checks to correct obvious gaps.

The model used practical inputs that can be traced and updated, including live birth trends, target age group populations, vaccine coverage for key programs, tender cadence and stock replenishment behavior, antigen level mix shifts, and expected price movement after new product introductions or lifecycle changes. Where direct data was thin for smaller countries, proxy rules were applied using regional peers with similar schedules and healthcare funding patterns, and then adjusted after expert feedback.

For forecasting, we relied mainly on scenario analysis supported by simple time series checks, because policy changes and campaign intensity can move demand faster than a straight line. Assumptions for coverage expansion, new vaccine uptake, and pricing were reviewed with interviewees, then applied consistently across regions so the steps stay repeatable.

Data Validation & Update Cycle

Outputs were checked against independent signals such as reported immunization coverage, public procurement announcements, and major capacity or supply events, and then variances were investigated before sign-off. When a number looked off, the underlying driver was rechecked, which often meant revalidating coverage, dose assumptions, or the applied price level.

A multi step internal review was followed so that calculations, unit conversions, and regional roll-ups were consistent and explainable. Reports are refreshed annually, and interim updates are made when material events occur, such as program additions, major shortages, or regulatory changes. Before delivery, a fresh final pass is done so clients receive the latest updated view.

Mordor Intelligence's Preventive Vaccines Market Sizing Compared With Other Published Estimates

Published market sizes for preventive vaccines can differ a lot, even when the topic name looks the same, because the counted product boundaries and the timing assumptions are not aligned. Differences also show up when one study leans more on broad healthcare spending ratios, while another leans more on program level demand signals.

By tracking cohort based dose demand and then refreshing price and mix assumptions with validation checks, Mordor Intelligence keeps the estimate tied to routine immunization reality, instead of blending in therapeutic vaccines, one-off outbreak spend, or service-only revenues that do not represent vaccine product value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 79.52 B (2026) | |

| Industry Publisher A | USD 65.72 B (2025) | Uses an earlier base year and a different forecast window, and the scope emphasis appears closer to a broader preventive vaccines basket that may mix procurement value with channel level revenues in some regions. |

| Industry Publisher B | USD 88.34 B (2023) | Starts from an older base year and shows a low growth path, which can happen when coverage expansion, new vaccine introductions, and pricing progression are treated conservatively or not updated for recent program changes. |

The spread in the table is mainly explained by timing (base year and currency year), plus what gets counted as vaccine product revenue versus adjacent categories. Our approach stays traceable to demand pool drivers like cohorts, coverage, and schedule intensity, which makes updates simpler when policies or prices change.

Key Questions Answered in the Report

What is the forecast value for the preventive vaccines market by 2031?

The preventive vaccines market is projected to reach USD 103.73 billion by 2031.

Which age group is expected to grow fastest in vaccine uptake?

Adult vaccination is set to expand at a 7.87% CAGR from 2026 to 2031, outpacing all other age cohorts.

How much market share did live and attenuated vaccines hold in 2025?

They accounted for 26.55% of preventive vaccines market share in 2025.

Why are online pharmacies gaining traction as a distribution channel?

Tele-pharmacy models combine digital booking with home visits, enabling an 8.70% CAGR as consumers seek convenience and last-mile delivery.

Which region is expected to record the quickest growth through 2031?

Asia-Pacific is forecast to expand at a 7.51% CAGR, driven by localized manufacturing and supportive government mandates.

Which technological platform is shortening vaccine update cycles to 90 days?

Modular mRNA manufacturing platforms can pivot quickly, enabling rapid strain updates and accelerating market response times.

Page last updated on: