Bangladesh Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

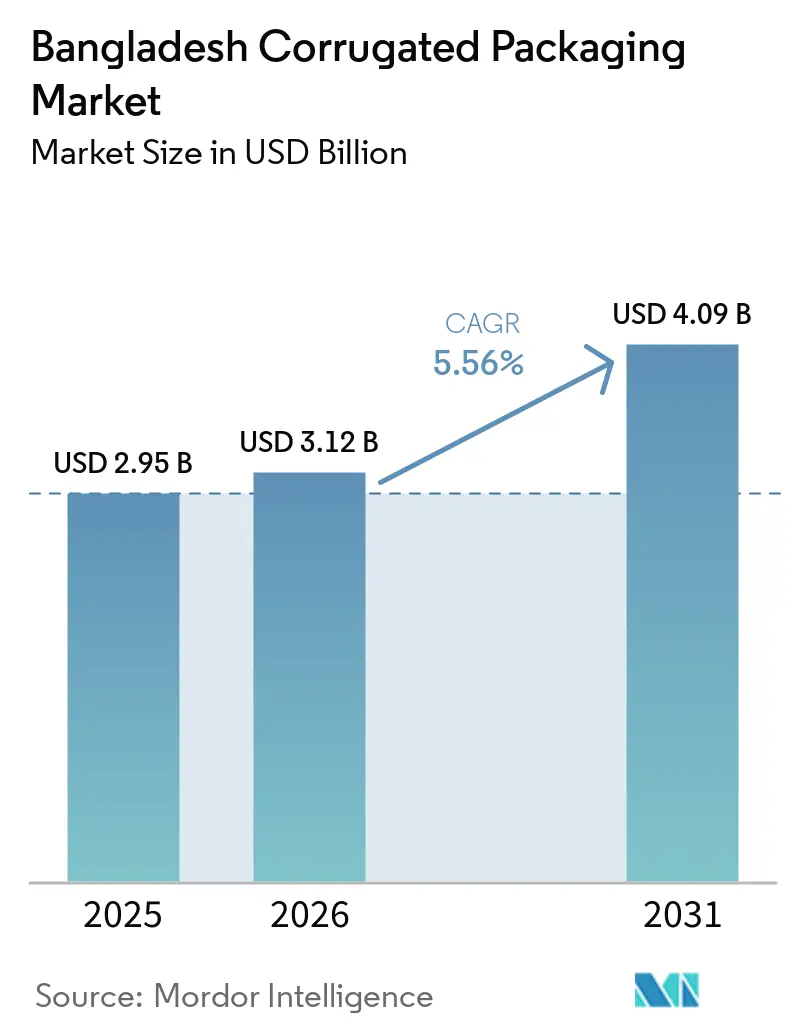

| Base Year Market Size (2025) | USD 2.95 Billion |

| Market Size (2026) | USD 3.12 Billion |

| Market Size (2031) | USD 4.09 Billion |

| Growth Rate (2026 - 2031) | 5.56% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bangladesh Corrugated Packaging Market Analysis by Mordor Intelligence

The Bangladesh corrugated packaging market size is expected to grow from USD 2.95 billion in 2025 to USD 3.12 billion in 2026 and is forecast to reach USD 4.09 billion by 2031 at a 5.56% CAGR over 2026-2031. Robust e-commerce adoption, supported by nationwide mobile-payment usage and a young consumer base, continues to propel volume growth even as converters face imported kraft-pulp cost swings and periodic power shortages. Stringent tariff barriers on finished cartons grant domestic players pricing power, which they leverage to offset elevated energy and freight expenses. Government cash incentives for paper and agro-processed exports encourage capacity additions in Mirsarai and Gazipur, yet the looming loss of least-developed-country privileges in late 2026 is forcing companies to fast-track long-term supply contracts. Meanwhile, the Bangladesh corrugated packaging market benefits from rising investments in digital inkjet equipment that shortens setup times and enables economical short-run personalization.

Key Report Takeaways

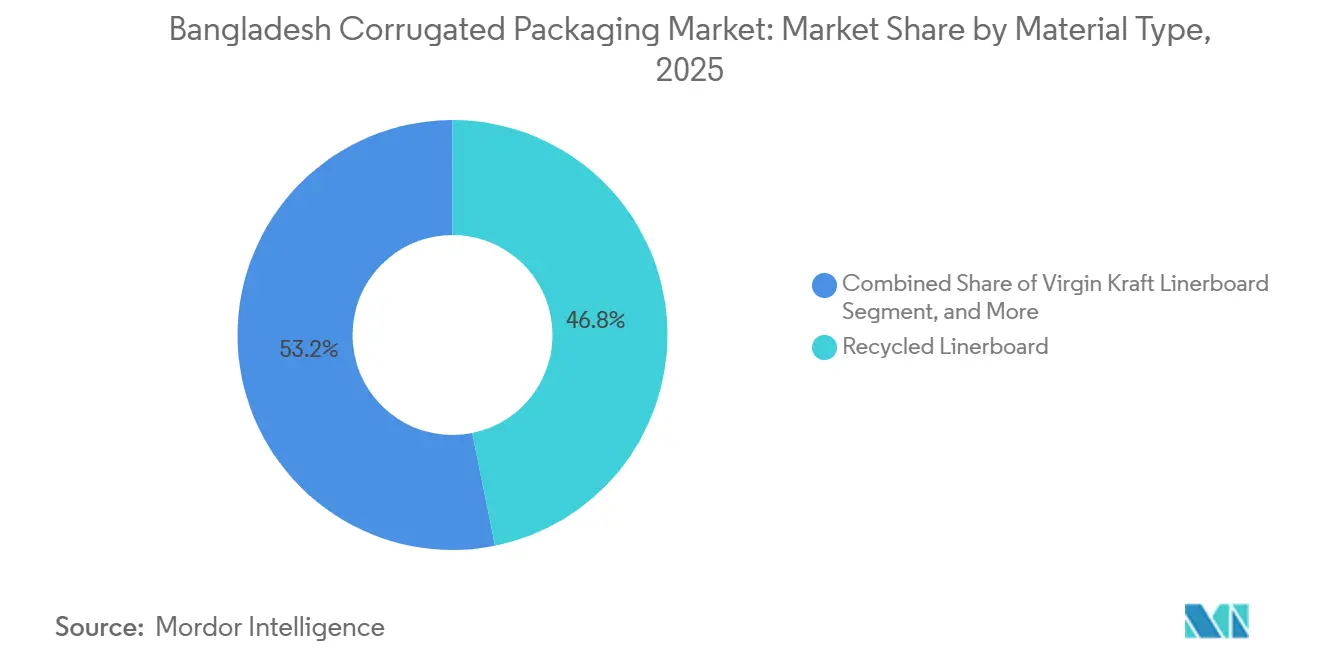

- By material type, the recycled linerboard segment captured 46.83% of the Bangladesh corrugated packaging market share in 2025.

- By flute type, the Bangladesh corrugated packaging market size for e flute is projected to grow at an 7.31% CAGR through 2031.

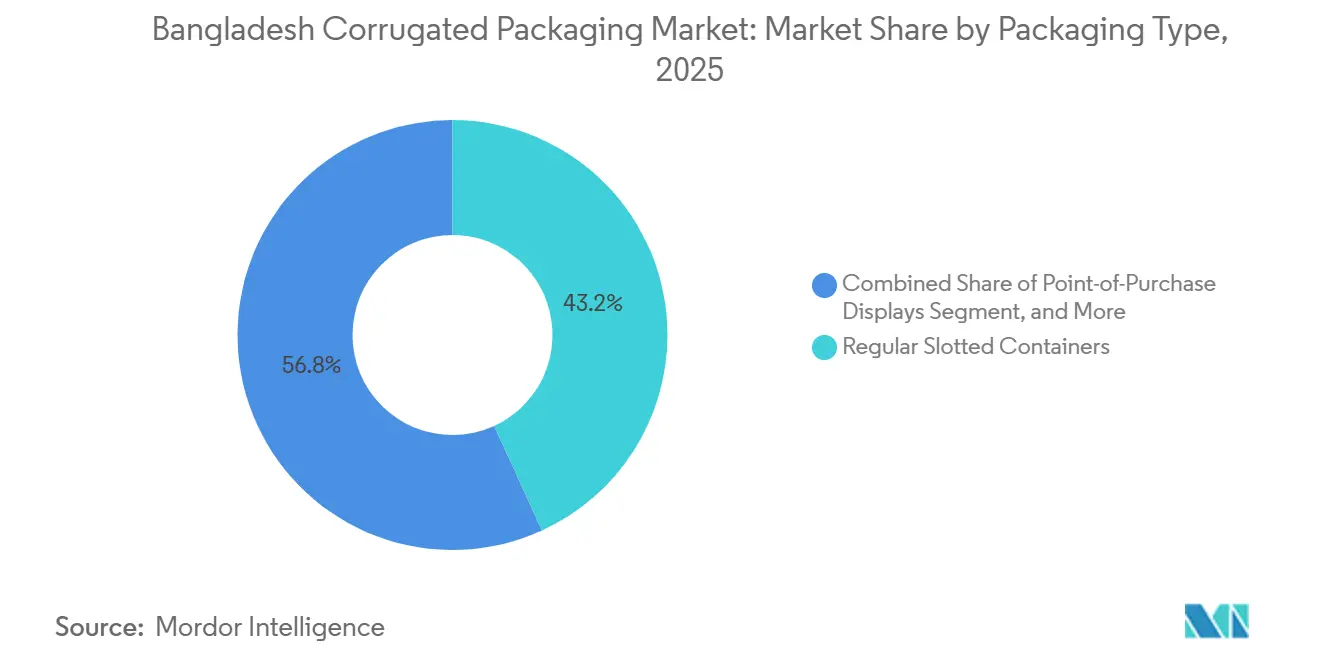

- By packaging type, the regular slotted containers segment captured 43.16% of the Bangladesh corrugated packaging market share in 2025.

- By wall type, the Bangladesh corrugated packaging market size for double-wall is projected to grow at an 6.78% CAGR through 2031.

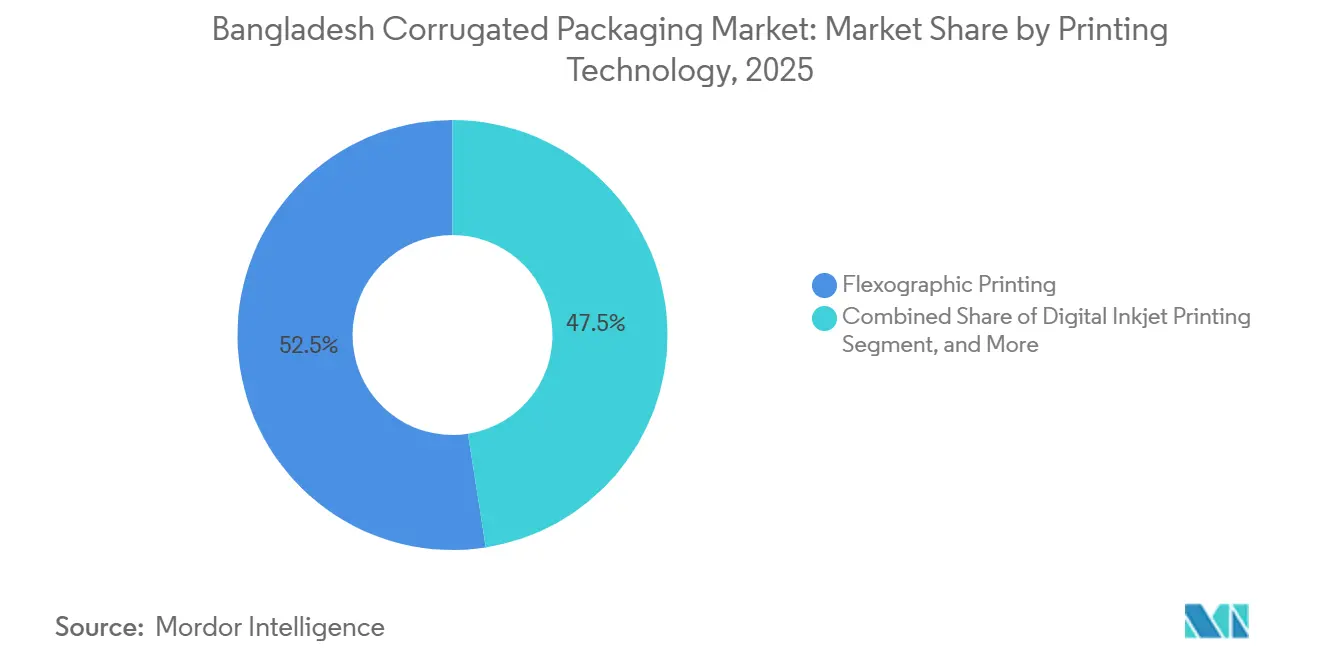

- By printing technology, the flexographic printing segment captured 52.48% of the Bangladesh corrugated packaging market share in 2025.

- By end-user industry, the Bangladesh corrugated packaging market size for e-commerce fulfillment centers is projected to grow at an 6.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Bangladesh Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Expansion of Bangladesh E-commerce Sector | +1.5% | National, urban spill-over to tier-2 cities | Short term (≤ 2 years) |

| Growing FMCG Output and Retail Penetration | +1.2% | National, concentrated in Dhaka, Chattogram, Sylhet divisions | Medium term (2-4 years) |

| Government Incentives for Export-Oriented Agro-Processing | +0.9% | National, export hubs in Mirsarai, Gazipur, Mongla | Medium term (2-4 years) |

| Stringent Import Tariff on Finished Packaging | +0.8% | National | Long term (≥ 4 years) |

| Adoption of Lightweight High-Ring-Crush Media | +0.6% | National, early adopters in Dhaka and Chattogram | Medium term (2-4 years) |

| Rising Use of Renewable Biomass Adhesives | +0.3% | National, pilot projects in Gazipur | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing FMCG Output and Retail Penetration

Nationwide FMCG turnover surpassed USD 4 billion in 2025, driven by organized retail chains that now reach many secondary cities. Longer supply routes increase the need for stackable, crush-resistant corrugated formats that protect branded goods on rough highways. As supermarkets replace traditional markets, shelf-ready die-cut boxes with multicolor flexo graphics gain favor, prompting converters to upgrade their four-color folder-gluer presses. Brand owners also demand smaller shipper counts to match faster inventory turns, leading to higher box-to-product ratios. Collectively, these factors keep the Bangladesh corrugated packaging market on a steady demand trajectory.

Rapid Expansion of Bangladesh E-commerce Sector

User penetration crossed 55 million in 2024, and gross merchandise value hit USD 6.2 billion, supported by seamless mobile wallets. Fulfillment centers require E and F flute profiles that lower dimensional-weight fees without sacrificing edge-crush strength. Logistics firms such as Pathao and Paperfly consolidate orders in regional hubs, pressuring converters to implement just-in-time deliveries. Digital inkjet presses now print high-resolution graphics on thin substrates, enhancing unboxing aesthetics for direct-to-consumer brands. These dynamics add fresh volume streams to the Bangladesh corrugated packaging market in the near term.

Government Incentives for Export-Oriented Agro-Processing

The Export Policy 2024-2027 offers 10% cash incentives on agro-processed shipments and 6% on paper products, spurring investments in wax-coated boxes that meet cold-chain demands. Seafood and vegetable processors lock in multi-year packaging contracts before incentives phase out after LDC graduation in 2026. Converters respond by adding moisture-resistant liners and upgrading quality labs to satisfy European phytosanitary rules. As these capacities mature, export packaging is lifting the Bangladesh corrugated packaging market, though margins may tighten once subsidies taper. Still, first-mover plants are likely to retain sticky customer relationships.

Stringent Import Tariff On Finished Packaging

A combined duty load of approximately 65.5% makes importing ready-made cartons uneconomical, insulating domestic plants from regional competition. Bashundhara Paper Mills and Meghna Group maximize this protection by expanding captive liner mills, securing 18-22% gross margins even amid energy shocks. Nevertheless, tariffs also reduce pressure to modernize equipment, which may dampen long-run productivity if regional trade blocs harmonize duties.[1]National Board of Revenue, “Customs Tariff Schedule 2025,” nbr.gov.bd For now, the wall allows local firms to pass on raw-material price increases to customers, sustaining profitable growth in Bangladesh's corrugated packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic Power Supply Disruptions | -1.1% | National, acute in industrial zones of Dhaka, Chattogram | Short term (≤ 2 years) |

| High Volatility of Imported Kraft Pulp Prices | -0.9% | National, import-dependent mills nationwide | Short term (≤ 2 years) |

| Persistent Shortage of Skilled Machine Operators | -0.5% | National, concentrated in Gazipur, Mirsarai | Medium term (2-4 years) |

| Lack of Domestic Recovery Systems for Waste Paper | -0.4% | National, urban collection gaps in Dhaka, Chattogram | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Volatility of Imported Kraft Pulp Prices

Global bleached hardwood kraft prices oscillated between USD 550 and USD 750 per tonne in 2024-2025, while taka depreciation amplified landed costs. Only a handful of large mills hedge currency exposure, leaving mid-tier converters vulnerable to margin erosion. Pulpy price swings also deter investments in high-speed corrugators because payback calculations become uncertain. Several planned lines were postponed in 2026, softening near-term capacity additions in the Bangladesh corrugated packaging market.

Chronic Power Supply Disruptions

Voltage drops idled half of garment output during the 2026 energy crisis and forced 30% of Dhaka Export Processing Zone factories to halt operations in April 2025. Corrugators require stable three-phase power; unplanned shutdowns create warp registration defects and add scrap. Diesel generators lift box costs by USD 0.02-0.03 per square meter, eroding price competitiveness. While large firms plan rooftop solar and biomass units, smaller converters lack capital, widening efficiency gaps and slowing the growth momentum of Bangladesh's corrugated packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Fiber Remains Cost Leader

Recycled linerboard accounted for 46.83% of revenue in 2025, as converters favored lower-cost secondary fiber amid high virgin fiber prices, anchoring demand in the Bangladesh corrugated packaging market. Semi-chemical fluting is expanding at 6.83% CAGR as plants shift to 120 g/m² basis weights that trim freight bills while preserving ring-crush strength. Virgin Kraft linerboard serves niche export applications that require superior burst and moisture performance, but its share is constrained by limited domestic pulp supply and tapering duty exemptions. Corrugating medium producers are trialing starch-reinforced formulations that lift compression strength by up to 15%, targeting processed-food shippers that stack tall pallet loads.

The transition toward lighter semi-chemical fluting aligns with sustainability mandates but raises supply-chain risk because Bangladesh imports most hardwood pulp from Indonesia and Vietnam worldbank.org. Lipy Paper Mills invested BDT 100 crore (USD 8.3 million) in recovered-fiber lines, yet only 3.15% of municipal solid waste enters formal recycling, forcing mills to import old corrugated containers at 5% duty.[2]ANDRITZ Group, “Lipy Paper Mills Installs RCF Line,” andritz.com Government paper export incentives partly offset input costs for virgin grades, thereby sustaining their presence in seafood and pharmaceutical cartons destined for Europe. All told, divergent fiber strategies heighten competitive differentiation within the Bangladesh corrugated packaging market.

By Flute Type: E Flute Accelerates in Parcel Logistics

B flute held 38.87% of 2025 volume owing to its cushioning-to-weight balance, yet E flute is rising at 7.31% CAGR as e-commerce shippers chase thinner profiles that lower dimensional-weight surcharges. C flute continues to serve bulk goods, although its growth moderates as light weighting spreads. A flute remains a niche for fragile merchandise, and F flute gains traction in cosmetics where smooth print surfaces matter.

Inkjet systems such as the Domino X630i now print variable data directly on thin profiles, opening up serialization and consumer-engagement use cases. Converters increasingly bundle double-wall combinations that pair E or F flutes with B flute cores to balance strength and freight savings. The Bangladesh corrugated packaging market, therefore, sees a gradual migration toward micro-flutes without wholesale abandonment of traditional profiles, preserving equipment utilization across mixed production schedules.

By Packaging Type: Die-Cut Custom Boxes Capture Branding Budgets

Regular slotted containers delivered 43.16% of 2025 revenue thanks to automated case-erector compatibility and cost efficiency. Die-cut custom boxes, however, are growing at a 6.49% CAGR as direct-to-consumer brands weaponize unboxing videos to expand their marketing reach. Converters meet this need with rotary die-cutters and digital finishing that economically handle 500-unit runs. Folding cartons overlap in lightweight E flute, supporting pharmaceuticals and personal care lines.

Point-of-purchase displays proliferate in modern retail, while pallet boxes protect bulk produce and industrial parts. Spending on experiential elements now claims as much as 10% of brand packaging budgets, sustaining premium graphics demand. This mix shift keeps the Bangladesh corrugated packaging market vibrant by rewarding agile converters that pivot between high-volume shippers and bespoke short runs. Point-of-purchase displays are expanding in tandem with modern trade, but their growth is capped by the slower rollout of air-conditioned retail formats in rural areas, where traditional kiranas still account for the majority of consumer transactions.

By Wall Type: Double-Wall Supports Export-Grade Loads

Single-wall constructions captured 53.91% of the 2025 demand for domestic distribution corridors under 500 kilometers. Double-wall formats are advancing at a 6.78% CAGR because seafood and vegetable exporters need boxes that resist condensation during 30-day ocean voyages. Triple-wall remains confined to heavy machinery, while single-face serves as a protective wrap for furniture shipments. Export incentives encourage the use of wax-coated liners and moisture-resistant adhesives, albeit at a 15-20% price premium.

Domestic shippers still favor single-wall for cost reasons, yet improved refrigerated-truck fleets are lengthening transit times and gradually tilting demand toward stronger constructions. This dynamic diversifies product lines and stabilizes utilization rates across the Bangladesh corrugated packaging market. Single-face corrugated benefits from the furniture and home-appliance sectors, which are expanding as urbanization drives household formation, yet its growth lags overall market expansion because flexible films and molded pulp are capturing share in protective-packaging applications.

By Printing Technology: Inkjet Disrupts Short-Run Economics

Flexographic printing retained 52.48% of 2025 spending based on 300 m/min throughput and low per-unit ink cost. Digital inkjet grows at a 6.84% CAGR as plate-free workflows slash setup from 4 hours to 30 minutes, reduce changeover scrap, and enable versioned campaigns. Litho-lamination keeps a foothold in luxury electronics, yet solvent-reduction mandates and inkjet’s 1,200 dpi resolution erode its edge. Screen printing services specialty metallic finishes for point-of-sale displays but lack growth. Hybrid lines that marry flexo solids with inkjet variable data give converters process flexibility without duplicating capital.

Inkjet’s advances align with compressed product life cycles, forcing converters to recalibrate their asset portfolios as the Bangladesh corrugated packaging market embraces mass customization. Litho-lamination faces pressure from environmental regulations targeting solvent-based adhesives, prompting converters to explore water-based and UV-curable alternatives, yet the process remains indispensable for luxury packaging where tactile finishes and spot varnishes drive brand perception. Screen printing's niche is stable but not growing, as digital finishing modules on inkjet presses can now replicate many specialty effects at higher speeds.

By End-User Industry: E-Commerce Fulfillment Delivers Peak Growth

Processed foods consumed 34.67% of the 2025 volume by virtue of rising incomes and longer shelf-life preferences. E-commerce fulfillment centers grow at a brisk 6.95% CAGR as Daraz, Chaldal, and others extend networks into Sylhet, Rajshahi, and Khulna. Fresh produce exports rely on wax-coated boxes, while beverage brands demand partitioned carriers to curb breakage. Electrical products require die-cut inserts for fragile components, and personal care lines favor micro-flutes for premium graphics. Automotive parts and industrial components occupy stable niches with bespoke cushioning.

Fulfillment hubs also push converters to offer late-stage print personalization, ensuring the Bangladesh corrugated packaging market evolves alongside omnichannel retail formats that blur lines between manufacturing and distribution. Electrical products and personal care are growing in line with consumer spending, while pharmaceuticals face regulatory complexity that limits the number of qualified converters able to meet serialization and tamper-evidence requirements.

Geography Analysis

Dhaka and Chattogram divisions jointly account for roughly 70% of national consumption, reflecting their dominance in manufacturing clusters and port logistics. Dhaka hosts most garment and processed-food factories, which source regular slotted containers and die-cut boxes on daily truckloads. Chattogram’s deep-water port anchors seafood and vegetable exports that require moisture-resistant double-wall grades, linking local converter output to global cold-chain corridors.[3]The Business Standard, “Industrial Land Costs Outside Dhaka,” tbsnews.net

Secondary cities such as Sylhet, Rajshahi, and Khulna are emerging distribution nodes as e-commerce platforms expand last-mile reach. Converters set up satellite plants here because industrial land is 40-50% cheaper than in Dhaka, lowering freight to northern tea estates and agro-processing clusters. Yet weak grid reliability and a shortage of skilled labor temper rapid scaling, keeping the Bangladesh corrugated packaging market heavily centered on the original industrial belt.

The Mirsarai economic zone promises purpose-built power and gas pipelines, along with a container terminal, attracting several mills seeking tariff advantages and quicker port access. However, the average port congestion dwell time exceeded 12 days in 2025, which continues to push converters to carry higher finished-goods inventory, thereby inflating working capital needs. Planned improvements at Mongla and Payra ports could ease Chattogram bottlenecks by 2028, potentially redistributing volume across the Bangladesh corrugated packaging market if hinterland connectivity materializes.

Competitive Landscape

Meghna Group, Bashundhara Paper Mills, and Akij Group together hold about 40% of industrial-grade liner and fluting capacity, giving the Bangladesh corrugated packaging market a moderate concentration profile. Meghna’s 800 TPD paper mill feeds a 12-million-box converting unit, insulating margins from pulp volatility. Bashundhara committed BDT 4,000 crore (USD 333 million) to a 2,000 TPD Valmet line in Mirsarai, scheduled to start up in 2027, a project that underscores confidence in export-led demand despite impending subsidy withdrawals.

Akij Group diversified into flexible films, operating 90,000 tonnes of BOPP and BOPET capacity, enabling hybrid packaging solutions for processed foods and pharmaceuticals.[4]Akij Group, “Annual Report FY 2025,” akij.net Mid-tier players such as Sonali Aansh Industries exploit niche demand for jute-corrugated hybrids, posting 119% revenue growth in fiscal 2025 as European buyers seek sustainable substrates. Technology adoption draws a dividing line: top-tier firms install automated roll-handling and inkjet presses that cut labor costs by 30%, whereas smaller converters stick with legacy flexo lines, limiting responsiveness to short runs.

Input cost exposure remains uniform because all mills import most pulp and adhesives, yet large groups secure better credit terms and volume discounts, translating into 2-3% point gross-margin advantages. Government incentives sustain backward integration, but gradual duty normalization post-LDC graduation could invite regional entrants and heighten competitive intensity within the Bangladesh corrugated packaging market.

Bangladesh Corrugated Packaging Industry Leaders

Meghna Group of Industries

Bashundhara Paper Mills Ltd.

AkijBashir Group

Geopack

Padma Accessories Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Bashundhara Paper Mills finalized Valmet contracts for a BDT 4,000 crore (USD 333 million) kraft-liner complex in Mirsarai, targeting a 2,000 TPD design capacity with completion in late 2027.

- January 2026: Sonali Aansh Industries reported BDT 1.73 billion (USD 14.4 million) revenue for FY 2025, a 119% jump fueled by jute-corrugated hybrid box demand from European buyers.

- September 2025: Magura Multiplex invested BDT 11 crore (USD 1.1 million) to upgrade its Gazipur plant with a high-speed rotary die-cutter optimized for E and F flute runs.

- November 2025: Meghna Group disclosed a 12-million-box-per-month output milestone, supported by its 800 TPD linerboard mill.

Bangladesh Corrugated Packaging Market Report Scope

The Bangladesh Corrugated Packaging Market Report provides a comprehensive analysis of the market, focusing on the production, consumption, and trade of corrugated packaging solutions within Bangladesh. It examines key trends, growth drivers, challenges, and opportunities shaping the market. The report also evaluates the competitive landscape, supply chain dynamics, and regulatory environment, offering valuable insights for stakeholders and decision-makers.

The Bangladesh Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material Type | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current Bangladesh corrugated packaging market size and projected growth?

The Bangladesh corrugated packaging market size stands at USD 3.12 billion in 2026 and is forecast to reach USD 4.09 billion by 2031 at a 5.56% CAGR.

Which segment will record the fastest CAGR through 2031?

E-commerce fulfillment centers are expected to expand at a 6.95% CAGR as online retail penetration deepens beyond Dhaka and Chattogram.

Who are the leading companies in Bangladeshi corrugated packaging?

Meghna Group, Bashundhara Paper Mills, and Akij Group collectively command roughly 40% of national liner and fluting capacity, giving them scale advantages in raw-material sourcing.

Why is E flute gaining share over B flute?

E flute delivers similar edge-crush strength while reducing box height and weight, saving dimensional-weight fees for parcel shippers and allowing higher-resolution graphics.

How will LDC graduation affect packaging exporters?

Cash incentives of 10% on agro-processed goods and 6% on paper products will phase out after November 2026, pressuring margins and accelerating contract renegotiations with export customers.

What are the main supply-side risks for converters?

Imported kraft-pulp price volatility and chronic grid instability add cost uncertainty and unplanned downtime, especially for mid-tier plants without captive power or hedging strategies.

Page last updated on: