Austria Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

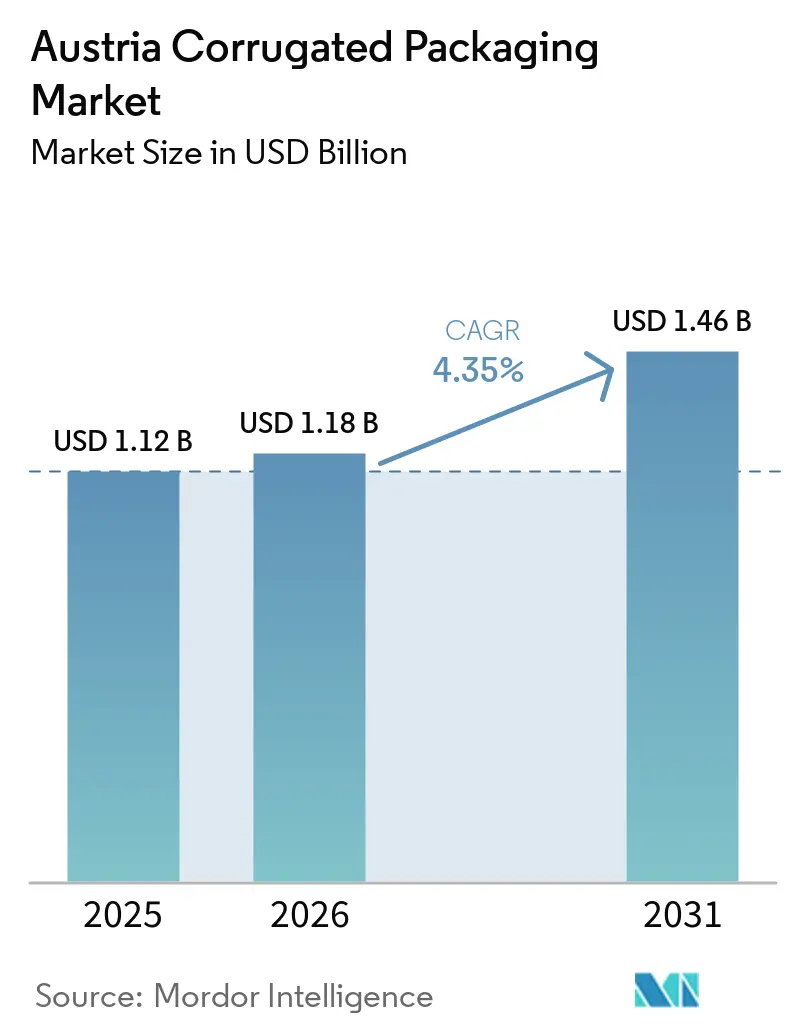

| Base Year Market Size (2025) | USD 1.12 Billion |

| Market Size (2026) | USD 1.18 Billion |

| Market Size (2031) | USD 1.46 Billion |

| Growth Rate (2026 - 2031) | 4.35% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Austria Corrugated Packaging Market Analysis by Mordor Intelligence

The Austria corrugated packaging market size is expected to grow from USD 1.12 billion in 2025 to USD 1.18 billion in 2026 and is forecast to reach USD 1.46 billion by 2031 at 4.35% CAGR over 2026-2031. Solid e-commerce momentum, recyclable-packaging mandates, and the resilience of the domestic food sector underpin demand even as manufacturing output only begins to recover. Distance-trade spending has shifted the Austria corrugated packaging market away from a tight correlation with industrial production, while return logistics and parcel-locker usage lift repeat-cycle volumes. Producers are redesigning boxes to meet the upcoming 50% empty-space ceiling, investing in digital printing for SKU versioning, and qualifying higher recycled-fiber content to align with circular-economy rules. Integrated paper-to-box players leverage captive linerboard supply and on-site power projects to buffer raw-material and energy volatility, positioning the Austria corrugated packaging market for steady, policy-driven growth rather than cyclical surges.

Key Report Takeaways

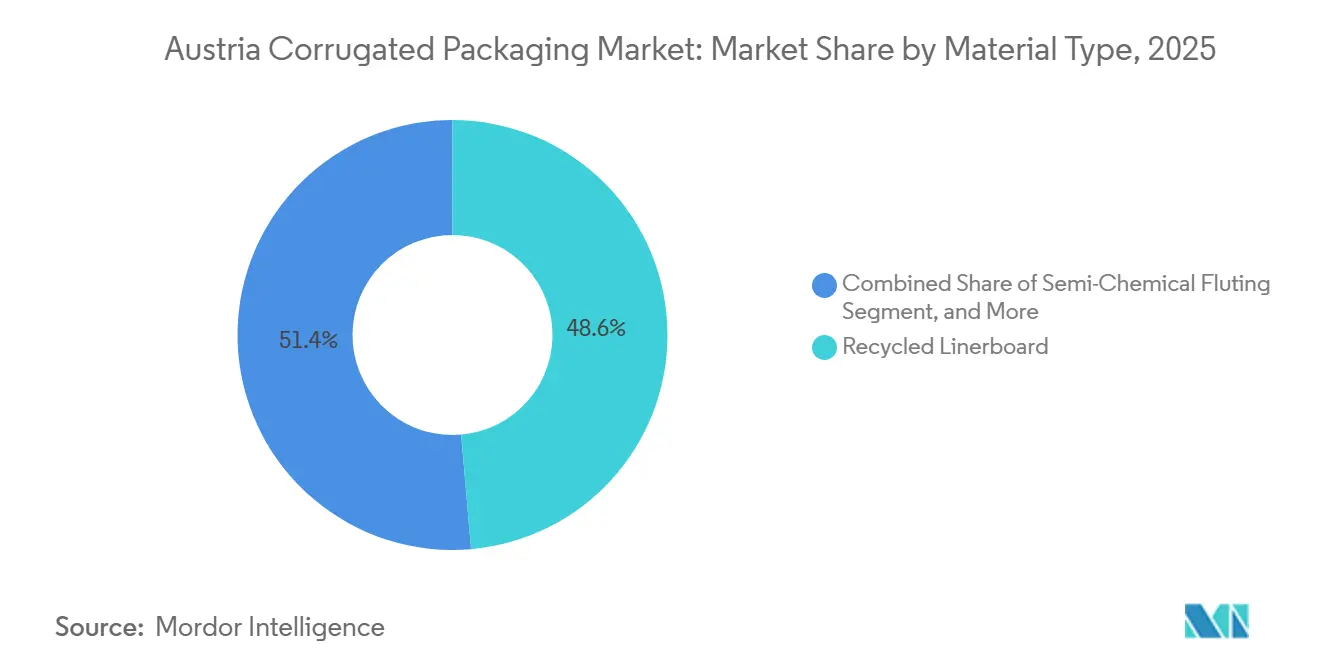

- By material type, the recycled linerboard segment captured 48.62% of the Austria corrugated packaging market share in 2025.

- By flute type, the Austria corrugated packaging market size for e flute is projected to grow at an 5.23% CAGR through 2031.

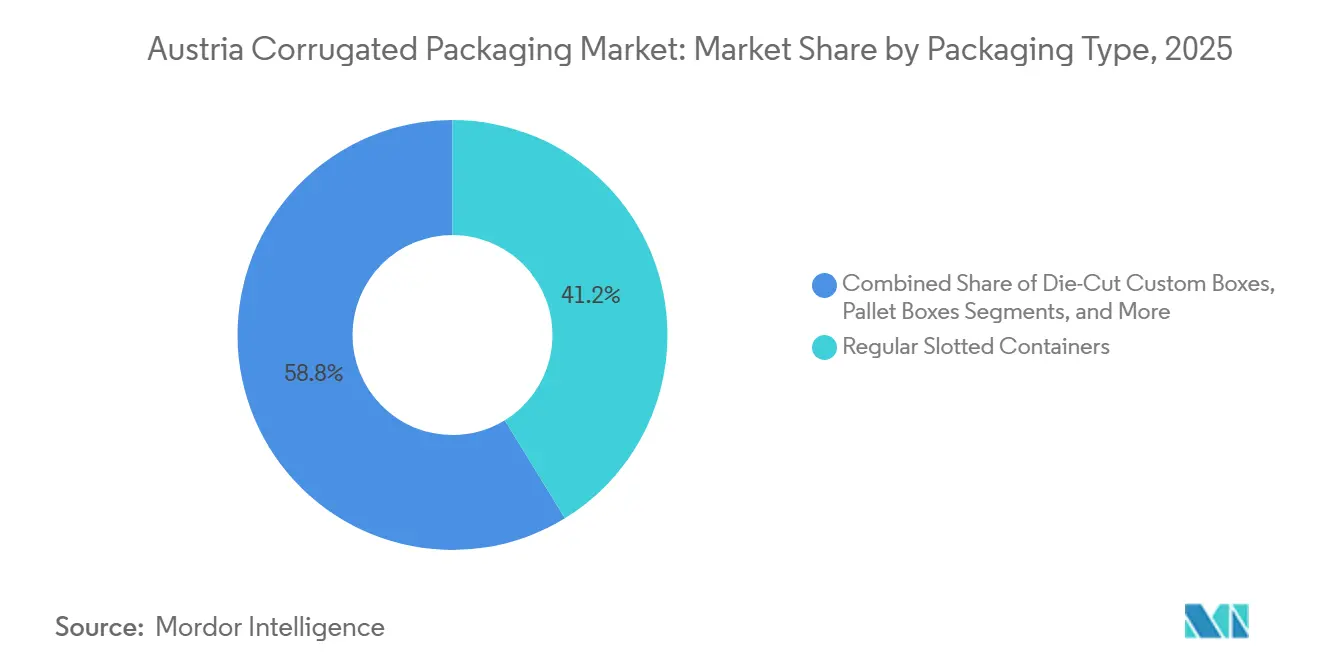

- By packaging type, the regular slotted containers segment captured 41.24% of the Austria corrugated packaging market share in 2025.

- By wall type, the Austria corrugated packaging market size for double-wall is projected to grow at an 5.73% CAGR through 2031.

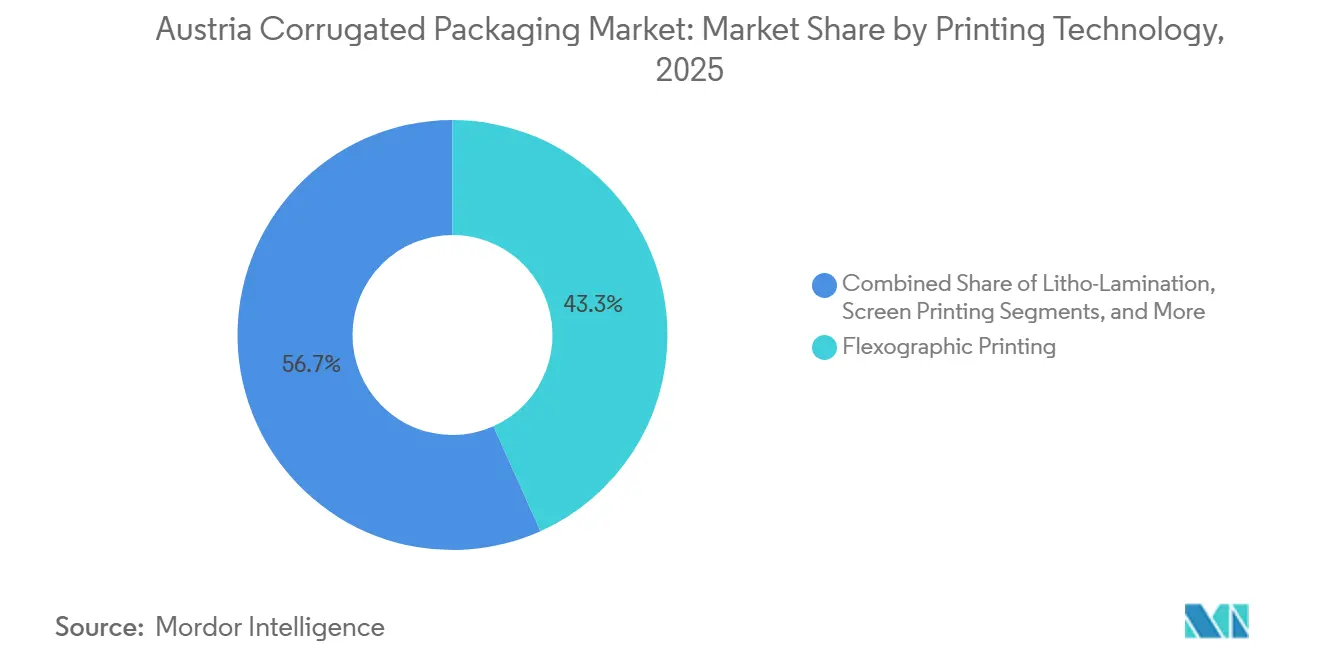

- By printing technology, the flexographic printing segment captured 43.29% of the Austria corrugated packaging market share in 2025.

- By end-user industry, the Austria corrugated packaging market size for e-commerce fulfillment centers is projected to grow at an 5.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Austria Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-Commerce Logistics Acceleration | +1.2% | National - Vienna, Upper Austria, Styria | Short term (≤ 2 years) |

| Regulatory Shift Toward Recyclable Packaging | +0.9% | EU-wide, Austria compliance August 2026 | Medium term (2-4 years) |

| Growth in Processed Food and Beverage Exports | +0.7% | National export corridors to Germany, Italy, USA | Medium term (2-4 years) |

| AI-Driven Box Optimisation Adoption by SMEs | +0.5% | Upper Austria and Vienna industrial clusters | Medium term (2-4 years) |

| Nearshoring-Led Electronics Output | +0.3% | Central Europe spillover to Austria | Long term (≥ 4 years) |

| Alpine Tourism Souvenir Logistics Demand | +0.2% | Tyrol, Salzburg, Carinthia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce Logistics Acceleration

Annual distance-trade spending climbed 14% in 2025, fueled by mobile purchases and high return rates that require second-cycle cartons. Locker networks now cover 41% of households, so shippers specify slimmer E flute formats that slide into automated compartments. These patterns deepen volume elasticity in the Austrian corrugated packaging market by decoupling demand from GDP and channeling it toward parcel throughput intensity.

Regulatory Shift Toward Recyclable Packaging

The PPWR imposes recyclability, empty-space, and reuse thresholds that reset converter design rules. Because fines and market-access barriers escalate from 2026, brand owners are front-loading redesign programs, triggering early orders for mono-material boards and digital variable-data labels.[1]Ioannis Antonopoulos, “Packaging and Packaging Waste Regulation (EU) 2025/40,” European Commission, marketac.eu The Austrian corrugated packaging market, therefore, gains structural pull from compliance timetables rather than discretionary marketing cycles.

Growth in Processed Food and Beverage Exports

Food shipments weather macro slowdowns better than capital goods, and Austria’s premium grocery brands require high-graphic transit trays and shelf-ready packs. Export corridors to Germany and Italy amplify cross-border flows, so converters near those borders capture recurring volumes. Consistent food-sector momentum steadies linerboard mill utilization, anchoring the Austrian corrugated packaging market against industrial volatility.

AI-Driven Box Optimisation Adoption by SMEs

Algorithmic sizing platforms cut void fill and board grammage, lowering freight and EPR fees for smaller shippers. Early adopters report material savings near 25%, validating payback for mid-scale converters facing tight labor markets. As electricity rebates arrive in 2027, capital budgets will free up for further automation, spreading AI benefits across the fragmented SME tier of the Austrian corrugated packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recycled Paper Price Volatility | -0.8% | National, tied to European OCC markets | Short term (≤ 2 years) |

| Competition from Returnable Plastic Crates | -0.6% | Fresh-produce retail logistics | Medium term (2-4 years) |

| Water-Scarcity Constraints on Mills | -0.3% | Styria, Upper Austria sites | Long term (≥ 4 years) |

| Dependence on Imported Virgin Fibre | -0.3% | National, Nordic supply links | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Recycled Paper Price Volatility

Price hikes of EUR 70-100 per tonne (USD 75-107 per tonne) for kraft and EUR 85 per tonne (USD 90 per metric tonne) for recycled containerboard erode converter margins before downstream contracts reset. Smaller plants lacking captive mills feel the squeeze most acutely, sometimes cutting shifts to conserve cash, which dampens short-term tonnage in the Austrian corrugated packaging market. Brand owners, therefore, diversify board sources, nudging non-integrated converters to stock higher safety buffers and accept elevated working-capital costs.

Competition from Returnable Plastic Crates

Retailers deploying plastic produce crates report 23% end-to-end cost savings compared with corrugated crates. The PPWR’s 40% transport-packaging reuse quota by 2030 could widen RPC uptake, siphoning away some fresh-food volumes. Corrugated producers respond with lightweight, reusable pallet boxes, yet infrastructure gaps and capital costs slow the pace of parity. Longer-term, corrugators will substitute lighter recycled top liners wherever print fidelity allows, but high-burst export trays will retain some currency-linked cost exposure.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Linerboard Widens Its Lead

Recycled linerboard captured 48.62% of Austria's corrugated packaging market share in 2025 as converters embraced circular-fiber mandates. The Austria corrugated packaging market size for this grade expands at a 6.14% CAGR through 2031, paced by major mill conversions, such as Heinzel’s PM 11 line, which now yields 500,000 tpy of testliner from 100% recovered OCC. Brand owners still specify virgin kraft for export trays that face humidity shocks, yet growth for those higher-cost grades trails the recycled surge demanded by EU design-for-recycling rules. Composite or plastic-lined linerboards retreat as PFAS curbs and recyclability scoring frameworks disincentivize multi-material constructions that complicate municipal recovery streams.

Virgin Kraft linerboard remains essential for export trays demanding high burst strength, yet its growth trails overall volumes as brand owners prefer post-consumer content. Composite and plastic-lined boards retreat under PFAS and recyclability rules, while closed-loop collection systems operated by ARA secure fiber streams, stabilizing pricing for recycled grades. Those plant upgrades, together with mandated empty-space limits, will further expand the Austria corrugated packaging market for recycled linerboard throughout the forecast window.

By Flute Type: Thin Profiles Gain On Logistics Efficiency

B flute held 35.23% of 2025 demand, yet shippers increasingly adopt lighter E flute, which posted the fastest 5.23% CAGR on the back of parcel locker standardization and retail-ready shelf trays. Dunapack’s D flute launch offers 16% stronger compression than E flute at equivalent basis weights, accelerating trades toward hybrid micro-flutes. Cosmetics and personal-care shippers dabble in ultra-thin F flutes, whose smooth surfaces pair well with litho-laminated photo graphics for gift-ready multipacks.

The forthcoming 50% empty-space ceiling set for 2030 will accelerate micro-flute penetration, because thinner profiles free up internal volume without enlarging external dimensions. Together, those drivers position thin flutes as the structural growth engine within the broader Austria corrugated packaging market share profile. A and C flutes stay relevant for palletized loads but cede packaging lines running lighter household SKUs. F flute, though niche, grows in cosmetics cartons where graphics trump stacking strength, leveraging high-resolution digital presses installed by Rondo Ganahl.[2]Koenig and Bauer Release, “Supplies large-format offset technology to Rondo,” at.koenig-bauer.com

By Packaging Type: Custom Die-Cut Formats Accelerate

Regular slotted containers accounted for 41.24% of shipments in 2025, due to their compatibility with automated case erectors. Custom die-cut boxes, however, drive growth at a 5.51% CAGR because variable-data inkjet lines eliminate tooling costs and enable brands to print season-specific QR codes on demand. Retailers favor these formats for shelf-ready displays that double as e-commerce shippers, eliminating redundant inner cartons and advancing the Austria corrugated packaging market size dedicated to omnichannel use cases.

Shelf-ready trays, point-of-purchase displays, and folding cartons converge as retailers shorten campaign cycles, further tilting mix toward digitally enabled blanks. The Austrian corrugated packaging market now rewards converters that can deliver web-to-pallet jobs within 36 hours, a service level pioneered by packit! with BOBST Masterflute Touch lines. As PPWR empty-space ceilings approach, box designers merge cushioning, branding, and returns-ready tape into one dieline, elevating value per square meter and sustaining superior margins for short-to-medium runs.

By Wall Type: Double-Wall Strengthens in Heavy Loads

Double-wall board posts have the fastest 5.73% CAGR because electronics exporters need higher edge crush resistance to withstand rail hauls through humid Adriatic corridors. Machinery shippers in Upper Austria also specify CB or BC combinations to avoid punctures from protruding metal parts, a risk that thin single-wall boards cannot mitigate. Single-wall still accounts for 52.43% of tonnage because it offers the lowest gram cost for grocery and personal-care cartons, which seldom exceed 14 kg payload.

Triple-wall remains a specialty for machinery exporters, while single-face sheets serve cushioning wraps. Industrial Strategy 2035 subsidies that cut electricity tariffs by up to EUR 0.05/kWh (USD 0.06/kWh) from 2027 will further lower unit costs for power-intensive double-wall corrugators. Triple-wall remains niche, yet order books lengthened in 2025 after Austrian wind-turbine tower sections adopted heavy multi-wall spacers for ocean freight to U.S. Gulf Coast projects.

By Printing Technology: Digital Inkjet Captures Short-Run Value

Flexographic preprint lines held 43.29 % share because beverage trays and detergent boxes still run million-meter campaigns with price-sensitive ink coverage. Digital inkjet advances at a 5.32% CAGR as brand managers demand localized slogans, influencer codes, and PPWR-required recyclability icons that change weekly. Mondi’s water-based white primer layer now enhances color vibrancy on brown recycled liners, enabling photo-realistic graphics without switching to costlier bleached kraft flexibles.

Offset-laminated topsheets remain entrenched in premium confectionery and cosmetics packs but lose share where inkjet’s speed and variable-data capability outweigh gloss-coat aesthetics. Economies of scale are shifting: converters that once considered seven-day makeready cycles normal now promise 48-hour artwork-to-delivery windows, fundamentally rewiring customer expectations across the Austria corrugated packaging market.

By End-User Industry: Fulfilment Centers Outpace Legacy Segments

Processed foods led with 28.31% in 2025, a position buttressed by supermarket private-label expansion that favors branded shelf-ready trays. E-commerce fulfillment centers, though smaller, are the fastest-growing, with a 5.18% CAGR, as returns logistics double corrugated turns per order. Electronics and small-appliance merchants now pre-kit double-wall inserts that meet ISTA 6-Amazon drop criteria, protecting fragile goods through reverse logistics loops.

Fresh produce boxes face RPC substitution risk, whereas electronics, personal care, and pharmaceuticals inject value through protective double-wall and litho-laminated graphics. With 70% of grocery share held by three retailers that now mandate fiber-based mono-material packs, downstream pull for the Austrian corrugated packaging market stays broad-based. Pharmaceuticals, exempt from new U.S. tariffs, rely on tamper-evident E flute outers lined with humidity indicators, a micro-segment where compliance premiums exceed 25% of board cost and steadily expand the Austria corrugated packaging market share allocated to regulated healthcare freight.

Geography Analysis

Vienna, Upper Austria, Styria, and Lower Austria collectively account for more than 66% of Austrian exports, anchoring regional box demand near large industrial and logistics parks. Vienna’s 51% parcel-locker penetration accelerates thin-flute adoption, while Burgenland edges higher at 52% as rural e-commerce densifies. Regional investment grants covering up to 14% of capex for digital presses persuade converters to colocate printing assets near high-volume shippers, shaving transport lead times for urgent promotional sleeves.

Styria and Upper Austria together ship over 60% of machinery and electronics exports to the United States, which amplifies demand for double-wall export cartons with moisture-barrier coatings.[3]Robert Schwarz, “Tariff shock from the USA: Regional Impacts,” bankaustria.at Prinzhorn’s EUR 50 million (USD 56.5 million) power-plant upgrade at Pitten secures linerboard supply for Lower Austrian converters and cuts CO₂ emissions, aligning with regional climate targets.Those integrated supply loops anchor the Austria corrugated packaging market within short trucking radii, minimizing carbon taxes anticipated under EU road-charging reforms.

Alpine regions Tyrol, Salzburg, and Carinthia boost seasonal souvenir logistics, yet still trail industrial clusters in absolute volume. Rail-centric shipping corridors out of Sappi’s Gratkorn mill near Graz move 60% of output by rail, reducing truck kilometers and improving the sustainability scores of boxes sold into Germany and Italy. As Industrial Strategy 2035 incentives roll out, brownfield upgrades in all four core provinces will raise automated corrugator density, locking freight loops inside Austria corrugated packaging market boundaries.

Competitive Landscape

Integrated suppliers Rondo Ganahl, Dunapack Packaging, and Mondi control pulp, paper, and conversion assets, securing feedstock amid OCC price swings that destabilize non-integrated rivals. Rondo’s EUR 16.5 million (USD 18.6 million) BHS line added 220 million m² of annual board in January 2025 and feeds captive sheet plants in Vorarlberg and Tyrol, tightening internal loops that lower logistics miles.[4]Rondo Ganahl AG, “New corrugated board plant at Frastanz,” rondo-ganahl.comPrinzhorn’s D flute innovation, available across four countries since September 2025, differentiates performance while its Pitten site’s new gas turbines insulate energy costs, a key hedge as unit electricity prices rose 5% in 2025.

Mondi’s March 2025 purchase of Schumacher’s Western Europe assets added 2,200 employees and expanded its Austrian converting reach, and its September 2025 white-inkjet launch opened premium graphics without coated liners. Digital-first challengers such as packit! and Cardbox Packaging scale BOBST lines that promise web-to-box in 36 hours, targeting fast-fashion and influencer brands that traditional three-week lead times cannot serve. AI-enabled platforms like paxly.ai negotiate mill capacity and box geometry in real time, compressing procurement cycles for SMEs.

Although Smurfit Westrock has no domestic mills, its European network and USD 14 billion in free cash flow projections for 2026-2030 keep price discipline tight for commoditized SKUs. Ultra-lightweight E and F flute constructions tailored to Austria’s growing single-household demographic represent another niche, particularly as parcel shippers trim void space to minimize carbon disclosures. Investors monitoring the Austria corrugated packaging market share trajectory should watch for merger activity around SME digital specialists whose rapid SKU cycling skills complement larger firms’ mill-based economies of scale.

Austria Corrugated Packaging Industry Leaders

Prinzhorn Holding GmbH

Greif, Inc.

Rondo Ganahl AG

Mondi plc

Smurfit WestRock plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Rondocarton earmarked EUR 6 million (USD 6.8 million) for 2026 to automate in-plant transport at Târgovişte and install photovoltaics in Cluj.

- September 2025: Mondi plc launched white digital inkjet printing for corrugated packaging.

- September 2025: Prinzhorn commissioned on-site gas turbines at the Pitten containerboard mill after EUR 50 million (USD 56.5 million) spent.

- January 2025: Rondo Ganahl started up a EUR 16.5 million (USD 18.6 million) 2.8 m BHS Speed Line in Frastanz.

Austria Corrugated Packaging Market Report Scope

The Austria corrugated packaging market is defined as the industry focused on the production of fiber-based containers such as slotted boxes, folder boxes, and trays constructed from a fluted corrugated medium sandwiched between linerboards. Additionally, the analysis examines the impact of European Union sustainability mandates, such as the Single-Use Plastics Directive and circular-economy initiatives, on regional manufacturing strategies and on the adoption of recycled versus virgin containerboard within the Austrian supply chain.

The Austria Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material Type | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 value of the Austria corrugated packaging market?

The market is estimated at USD 1.18 billion in 2026, on track to reach USD 1.46 billion by 2031.

Which material grows fastest through 2031?

Recycled linerboard leads growth at a 6.14% CAGR as policy favors post-consumer fiber.

Why is E flute demand accelerating?

Locker-compatible parcel sizes and retail-ready shelf trays push shippers toward thinner, lighter boards that cut void space and freight.

How are converters coping with OCC price swings?

Integrated mills, on-site power plants, and AI box-design tools help control fiber spend and lift plant productivity.

What impact will PPWR reuse targets have?

Brands must shift 40% of transport packs into reuse systems by 2030, opening niches for durable corrugated pallet boxes and boosting demand for traceable digital printing.

Which region creates the most box demand?

Upper Austria generates the highest volume thanks to dense machinery, electronics, and food-processing clusters tied to export corridors.

Page last updated on: