Ghana Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 260.12 Million |

| Market Size (2026) | USD 270.37 Million |

| Market Size (2031) | USD 330.46 Million |

| Growth Rate (2026 - 2031) | 4.10% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ghana Corrugated Packaging Market Analysis by Mordor Intelligence

The Ghana Corrugated Packaging Market size is projected to be USD 260.12 million in 2025, USD 270.37 million in 2026, and reach USD 330.46 million by 2031, growing at a CAGR of 4.10% from 2026 to 2031. Structural shifts in retail distribution, a phased national plastic ban, and export-packing rules in the European Union are powering sustained demand even as household consumption growth remains moderate. Government directives that eliminate lightweight plastic carry bags are accelerating the switch to recyclable paper-based formats in takeaway food, fresh produce, and grocery channels. Fulfilment centers such as Jumia’s 6,000-square-meter Tema hub are standardizing shipping cartons for electronics, apparel, and fast-moving consumer goods, creating predictable high-volume orders. Exporters of cocoa, pineapples, and mangos face the July 2025 EU Packaging and Packaging Waste Regulations that tighten recycled-content and traceability requirements, spurring the adoption of premium triple-wall boxes.

Key Report Takeaways

- By material type, the recycled linerboard segment captured 43.58% of the Ghana corrugated packaging market share in 2025.

- By flute type, the Ghana corrugated packaging market size for f flute is projected to grow at an 5.61% CAGR through 2031.

- By packaging type, the regular slotted containers segment captured 39.24% of the Ghana corrugated packaging market share in 2025.

- By wall type, the Ghana corrugated packaging market size for triple-wall is projected to grow at an 5.87% CAGR through 2031.

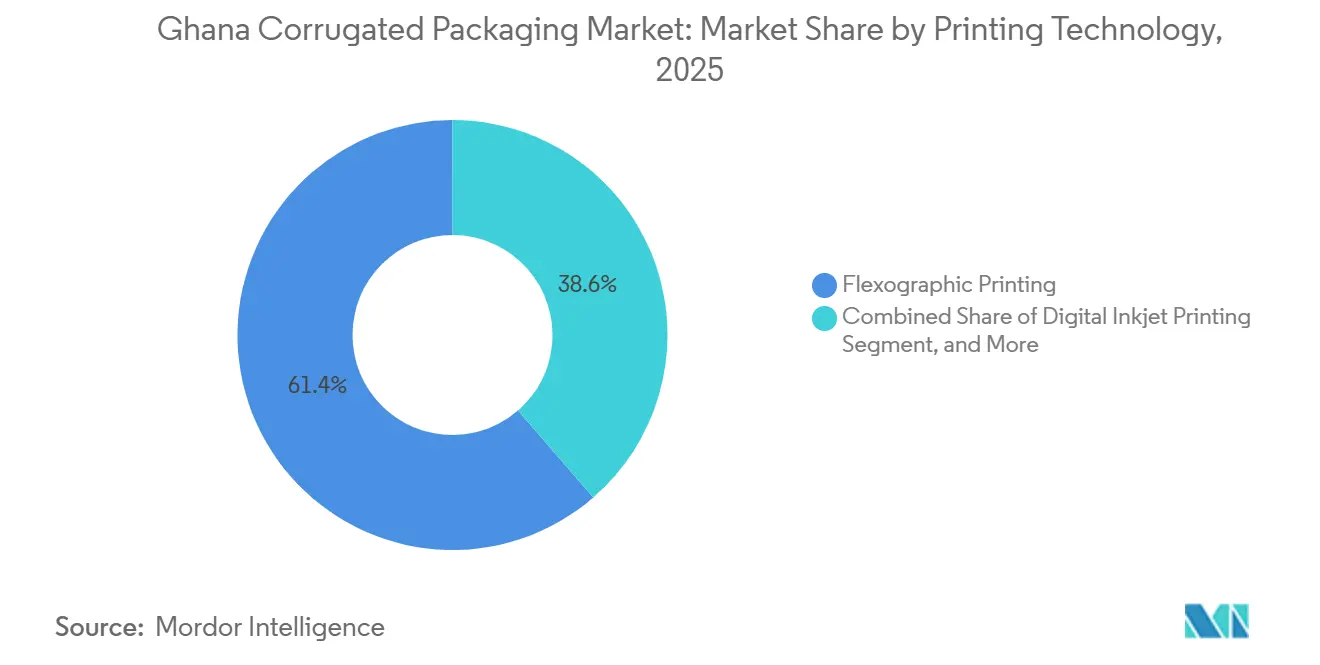

- By printing technology, the flexographic printing segment captured 61.37% of the Ghana corrugated packaging market share in 2025.

- By end-user industry, the Ghana corrugated packaging market size for pharmaceuticals is projected to grow at an 5.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Ghana Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of E-Commerce Fulfilment Infrastructure | +1.2% | National, concentrated in Greater Accra | Medium term (2-4 years) |

| Government Ban on Lightweight Plastic Carry Bags Elevating Paper Alternatives | +1.5% | National, early enforcement in Accra, Kumasi, Takoradi | Short term (≤ 2 years) |

| Proliferation of Organized Retail Chains in Urban Centers | +0.8% | Greater Accra and Ashanti Region | Medium term (2-4 years) |

| Export-Oriented Produce Requiring Robust Transit Packaging | +1.0% | Tema Port and Kotoka International Airport | Long term (≥ 4 years) |

| Increasing Investments in Ghana’s Food Processing Clusters | +0.7% | Central, Ashanti, Eastern Regions | Long term (≥ 4 years) |

| Adoption of Digital Printing for Short-Run Promotional Boxes | +0.3% | Accra and Kumasi | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Expansion of E-Commerce Fulfilment Infrastructure

Jumia’s purpose-built Tema facility processes large, SKU-rich orders for Black Friday and day-to-day deliveries, enforcing strict box dimension standards that reward converters with consistent compression strength and print registration.[1]Jumia Technologies AG, “Jumia Ghana Expands Operations with New State-of-the-Art Warehouse,” jumia.com The building’s location, minutes from the port, lowers inbound linerboard logistics costs and facilitates late-stage customization for regional cross-docking. Local producers that supply branded mailer and shipper designs with QR codes and tamper seals enjoy dependable offtake throughout peak cycles, smoothing capacity utilization. Secondary logistics operators replicating Jumia’s model in Kumasi and Takoradi further multiply the opportunities in Ghana's corrugated packaging market. Rising e-commerce penetration from 4.3% of total retail sales in 2025 to a forecast 7.5% in 2030 will sustain incremental corrugated demand.

Government Ban on Lightweight Plastic Carry Bags Elevating Paper Alternatives

The 2025 “Ghana Beyond Plastics” blueprint imposes phased restrictions on styrofoam clamshells and single-use pouches, channeling restaurants, wet-markets, and supermarkets toward paperboard trays and takeaway cartons. Backlog conversion surged 18% quarter-over-quarter following the June 2025 pronouncement, as vendors stockpiled grease-resistant pizza boxes and fold-flat meal kits. Provincial authorities in Central and Northern Regions are piloting extended producer responsibility levies to subsidize recycled linerboard mills, helping offset collection bottlenecks. SMEs that lacked die-cutting and food-contact certification in 2024 have since invested in inline folder-gluers and ISO 22000 audits to secure municipality contracts. A nationwide rollout is expected to cut plastic landfill volumes by 60% by 2030, translating into steady incremental tonnage for Ghana's corrugated packaging market converters.

Proliferation of Organized Retail Chains in Urban Centers

Carrefour’s rebranding of seven ex-Shoprite hypermarkets by April 2026 will introduce European procurement templates that favor shelf-ready cases with high-fidelity flexo graphics and perforated tear strips. Master packers that hold FSSC 22000 credentials now negotiate three-year preferred-supplier contracts covering poultry, dry groceries, and household consumables. Standardized secondary packaging trims back-room labor and shrinkage, expanding converter gross margins on die-cut pop-up displays and half-slotted trays. Parallel openings of discount formats in secondary cities create a cascading demand wave for lightweight B flute cartons that travel well on mixed-load trucks. Over time, organized retail’s share is forecast to climb above 25%, strengthening the revenue base for stakeholders in Ghana's corrugated packaging market.

Export-Oriented Produce Requiring Robust Transit Packaging

The July 2026 EU packaging regulation requires fruit exporters to certify recycled content levels, void-space ratios, and BPA-free liners. Triple-wall, wax-coated crates with ventilated die-cuts dominate purchase orders for cocoa liquor blocks and fresh mangos bound for Rotterdam. Niche Cocoa’s 60,000-tonne processing line configures palletized outer cases that withstand 16-day sea voyages without panel collapse. Converter Labs now run edge-crush and humidity tests mimicking Gulf of Guinea microclimates, allowing Ghana corrugated packaging market suppliers to guarantee less than 1% carton failure on arrival. EU-aligned declarations of conformity bolster brand equity for Ghanaian produce, opening premium-price niches in Scandinavian supermarkets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exchange-Rate Volatility Inflating Imported Kraft Linerboard Costs | -0.9% | Tema and Accra converter clusters | Short term (≤ 2 years) |

| Chronic Electricity Price Hikes Raising Conversion Cost | -0.6% | National high-voltage industrial users | Medium term (2-4 years) |

| Fragmented Domestic Wastepaper Collection Network | -0.4% | Accra, Kumasi, Takoradi | Long term (≥ 4 years) |

| Limited Availability of Technical Training for Corrugator Operators | -0.2% | Greater Accra and Ashanti | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Exchange-Rate Volatility Inflating Imported Kraft Linerboard Costs

A 23.3% GHS slide to 16.09 per USD in November 2024 inflated kraft linerboard CIF Tema prices and slashed converter margins on fixed-price contracts. Mid-tier plants that lacked forward-cover facilities trimmed gsm, risking higher reject rates. Currency support from the Bank of Ghana steadied rates around GHS 12.61 per USD by May 2025, but the episode underscored raw-material vulnerability in Ghana's corrugated packaging market. Larger firms now diversify their suppliers and lock in six-month contracts that peg invoices to weighted-average rates, mitigating subsequent swings.

Chronic Electricity Price Hikes Raising Conversion Cost

Tariff hikes of 9.86% in January 2026 and a 15% rollback three months later highlight policy unpredictability that complicates capital planning for corrugators drawing continuous loads above 1. Plants that invested in 850-kVA standby gensets limit downtime but divert funds from capacity expansions and digital print retrofits. While April 2026 relief trims variable cost, the thermal-heavy national grid still exposes Ghana's corrugated packaging industry to import-parity diesel prices. Energy-efficiency retrofits, such as waste-heat recovery on medium-pressure boilers, now feature prominently in converter payback analyses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Boards Dominate but Virgin Kraft Gains with Exporters

Recycled linerboard held 43.58% of 2025 demand, reflecting tight household budgets and moderate stacking requirements for domestic groceries. Virgin kraft, although costlier, attracts exporters and pharmaceutical shippers that value burst strength, moisture resistance, and EU food-contact compliance, and is forecast to chart a 5.39% CAGR. Domestic wastepaper recovery supplies only a fraction of the mill's needs, and Super Paper Product Company’s 11-tonne daily shortfall demonstrates the structural feedstock gap. Nixin Paper Mill’s July 2025 certification for testliner and fluting represents rare backward integration, promising to shave logistics premiums and smooth Ghana corrugated packaging market price cycles.

Converters weigh cost against performance each time they quote an order because high-graphics shelf-ready packs cannot risk warp or glue-joint failure. Brands that export juice concentrate from the Ekumfi factory increasingly stipulate 100% virgin kraft outers to avoid humidity-induced bulge during ocean transit. Municipalities are piloting eco-levies that subsidize baled waste-paper deliveries, but informal collectors still account for 51% of urban sourcing, limiting immediate scale. Until extended producer responsibility schemes mature, recycled supply is expected to trail demand, and virgin kraft will retain its quality premium in Ghana corrugated packaging market contracts.

By Flute Type: B Flute Workhorse Meets Rapid F Flute Upswing

B flute won 42.71% share in 2025 by balancing cushioning and printability for canned foods and beverages. F flute, with a thinner profile and smoother surface, is scoring 5.61% CAGR as e-commerce shippers specify compact mailers that lower volumetric freight charges. The Tema fulfillment hub prints variable data directly on F flute mailers, marrying precision graphics with QR codes for last-mile tracking. C flute remains indispensable for palletized soft-drink trays requiring crush resistance, while A and E flute serve specialist cushioning and display niches.

The Ghana corrugated packaging market rewards converters that can swap flute combinations without tool-change delays, and inline rotary die-cutters capable of multi-flute passes are emerging as competitive differentiators. Producers experimenting with microflute X-profiles report 3% savings in board weight and crisper flexo dots. As digital inkjet penetrates, thin flutes that accept high-resolution imagery will continue to displace legacy B flute in promotional runs, carving fresh share pockets across the Ghana corrugated packaging industry.

By Packaging Type: Slotted Containers Anchor Volume as Custom Die-Cut Boxes Accelerate

Regular slotted containers delivered 39.24% of 2025 revenue thanks to automation-friendly blank sizes that ship flat and erect quickly on tape machines. Die-cut custom boxes, growing at a 5.47% CAGR, let brands stage eye-catching retail displays and meet Carrefour’s shelf-ready spec, which mandates pop-open perforations. FON Packaging leverages four-color flexo print-slot-glue lines that crank out bespoke beverage carriers in 48 hours, compressing campaign lead times for FMCG marketers.

Folding cartons are increasingly used in cosmetics and OTC medicines as tamper-evident seals and holographic hotspots become commonplace. Value pools are shifting: while slotted containers dominate tonnage, die-cut formats deliver 20-30% higher margins because of design complexity and small-batch runs, which command price premiums. Ghana corrugated packaging market buyers will increasingly expect CAD-driven prototyping and ISTA-certified drop tests to be bundled into quotations, positioning integrated solution providers for outsized gains.

By Wall Type: Single-Wall Efficiency Versus Triple-Wall Export Durability

Single-wall boxes accounted for 52.91% of the market in 2025, handling light groceries and consumer electronics that move within Ghana’s borders. Triple-wall boxes, however, are advancing at a 5.87% CAGR because cocoa processors and fresh-produce exporters demand uncompromising crush strength during 16-day sea voyages. Cocoa liquor blocks shipped to Antwerp specify triple-wall with moisture-barrier poly liners to withstand West African humidity spikes.

Double-wall fills a mid-market niche for agro-chemicals and white goods that require moderate stacking performance. Investments in rigid flute profiles and humidity-controlled storage rooms minimize warpage and delamination, allowing converters to guarantee ≤1% carton failure. As Ghana corrugated packaging market exporters scale aseptic beverage output, demand for triple-wall coded outers will compound, nudging single-wall’s share gradually lower in high-value channels.

By Printing Technology: Flexo Keeps Scale Advantage, Digital Inkjet Unlocks Speed

Flexographic presses produced 61.37% of boxes in 2025 because low plate costs amortize efficiently across long runs for rice, detergent, and sardine brands. Digital inkjet, growing at a 5.82% CAGR, is gaining ground where variable data, anti-counterfeit features, and test-market graphics trump unit cost. FlexoHub’s local plate library reduces downtime, yet converters installing single-pass inkjet heads on corrugators report 48-hour concept-to-carton cycles that woo cosmetics and nutraceutical start-ups.[2]FlexoHub, “All Flexography,” flexohub.com

Litho-lam remains a premium niche for gift confectionery where photographic finishes justify higher spend. The Ghana corrugated packaging market’s print ecosystem is thus bifurcating: scale-driven FMCG lines favor flexo’s economy, while niche brands embrace digital agility. Hybrid workflows that print variable expiry dates on pre-printed flexo blanks have emerged, helping converters hedge technology bets as buyer expectations evolve.

By End-User Industry: Processed Foods Anchor Volume, Pharma Spurs Premiumization

Processed foods accounted for 33.28% of 2025 shipments, driven by One District One Factory plants that bottle juices and can tomatoes. Each new pineapple packhouse requires steady flows of 5-kg ventilated trays, translating into baseline corrugator uptime. Pharmaceuticals are expanding 5.31% CAGR because the Food and Drug Authority import rules force protective shippers with ≥60% shelf-life residue and tamper-proof batch labels. Cold-chain vaccine vials now travel in triple-wall outers lined with phase-change gel inserts.

E-commerce, beverages, and personal-care categories together represent a growing tail that values design, brand storytelling, and QR-enabled engagement. As Jumia extends next-day delivery beyond Accra, demand for compact mailer boxes and returnable inserts will escalate. The Ghana corrugated packaging industry is therefore shifting from bulk commodity cartons toward differentiated, compliance-driven SKUs that sustain higher average selling prices.

Geography Analysis

Greater Accra and the adjoining Tema industrial zone account for more than half of Ghana's corrugated packaging market shipments because of proximity to the country’s largest port, a high-voltage grid substation, and customs-bonded warehouses, which reduce turnaround time for both imported linerboard and finished cartons. Certified converters clustering around Tema enjoy same-day audit access at the Ghana Standards Authority laboratory, enabling faster renewal of GS 170:2020 marks and ISO 9001 surveillance visits.[3]Ghana Standards Authority, “Product Certification,” gsa.gov.gh The Jumia fulfillment hub and Carrefour’s regional distribution center together anchor year-round demand for shipper cases, offsetting seasonal dips in cocoa exports.

Kumasi in the Ashanti Region is the second major demand node, supplying cartons to agro-processors, timber merchants, and beverage fillers that service the northern and central corridors. Logistics corridors linking Kumasi to produce belts in Sunyani and Obuasi rely on 5-ply double-wall trays that withstand rough feeder roads. Growing organized retail in Kumasi’s malls encourages shelf-ready packs with perforated fronts, stimulating design innovation and small-lot digital runs. The confluence of processing clusters and improved trunk roads along the Kumasi-Techiman axis is expected to lift regional corrugated consumption at compounded rates above the national mean, enlarging the Ghana corrugated packaging market footprint.

Western and Northern Regions presently trail on volume but offer greenfield opportunities as mining supply chains and cashew exporters pivot toward traceable packaging. However, unreliable grid power and sparse waste-paper collection raise landed costs by up to 12% versus Tema. Municipalities such as Tamale experiment with source-segregation pilots, yet recovery rates remain too low to feed a mid-sized mill. Until infrastructure matures, converters will truck blanks from Accra, constraining margin upside but planting early stakes in territories that could accelerate once road and cold-chain projects materialize. Nationwide, differential infrastructure maturity ensures that the Ghana corrugated packaging market evolves in concentric waves moving outward from Accra and Kumasi.

Competitive Landscape

Royal Crown Packaging and FON Packaging headline a field of locally owned converters that together form a mid-concentration structure characteristic of a developing supply base. Royal Crown operates a high-speed corrugator and two inline converting lines, targeting regional exports to Togo and Benin while capturing premium projects that demand custom sampling and lab validation. FON Packaging supplies 80 multinational and regional brand owners, leveraging water-resistant carton technology and ISO 22000 certification to defend anchor accounts in beverage and dairy.

Upstream, Nixin Paper Mill’s testliner and fluting plant, certified in July 2025, introduces the first credible domestic substitute for imported kraft linerboard. Although production scale remains modest, early trials report 8% cost savings versus Asian imports, and converters have begun dual-sourcing strategies to hedge forex risk. Imports from China and Vietnam continue to serve ultra-thin F flute and specialty white-top grades that domestic mills cannot yet replicate, preserving a degree of external dependency within Ghana's corrugated packaging market supply chains.

Digital disruption is underway as ePac Flexible Packaging opens a 2,200-square-meter inkjet pouch factory in Accra, offering lead times below 15 days and competing directly for promotions that historically used litho-laminated cartons.[4]ePac Flexible Packaging, “Official Opening of Accra Plant,” epacflexibles.com Mid-tier box plants lacking design studios, rapid prototyping tables, or FSSC credentials face escalating risk of margin erosion as multinational buyers consolidate approved-vendor lists. Nevertheless, informal converters continue to service open-air markets and transport crates, ensuring that price-centric niches remain contested, and preventing full commoditization in the Ghana corrugated packaging industry.

Ghana Corrugated Packaging Industry Leaders

Mohinani Group (Polytanks Ghana Ltd – Kraft Division)

Royal Crown Packaging Ltd.

SONAPACK Ghana Limited

Fine Print Ltd.

FON Packaging Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Public Utilities Regulatory Commission reduced industrial electricity tariffs by 15% for high-voltage users, reversing the January 2026 hike.

- April 2026: Carrefour finalized rebranding of seven hypermarkets and signalled plans for five new outlets by 2028.

- October 2025: Tetra Pak and Niche Cocoa introduced 180 ml shelf-stable Daily Milk drinks, boosting demand for corrugated shipper trays.

- July 2025: Nixin Paper Mill secured Ghana Standards Authority certification for testliner and fluting grades.

Ghana Corrugated Packaging Market Report Scope

This report provides a comprehensive analysis of the corrugated packaging market in Ghana. It examines market trends, growth drivers, challenges, and opportunities within the industry. Corrugated packaging refers to packaging solutions made from corrugated fiberboard, widely used for shipping, storage, and product protection across various industries. The study covers market dynamics, competitive landscape, and forecasts for the defined study period.

The Ghana Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material Type | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and projected value of the Ghana corrugated packaging market?

The Ghana Corrugated Packaging Market size is projected to expand from USD 270.37 million in 2026 to USD 330.46 million by 2031, registering a CAGR of 4.10% between 2026 to 2031.

Which flute profile is most widely used in Ghana?

B flute dominates with a 2025 market share of 42.71%, favored for its balance of cushioning and printability.

How will the national plastic ban influence corrugated demand?

Phased restrictions on styrofoam and lightweight bags are directing food service and grocery sectors toward paper-based boxes, adding an estimated 1.5% points to forecast CAGR.

Why are triple-wall boxes gaining popularity among exporters?

Cocoa and fresh-produce shippers need superior crush resistance and EU-compliant recycled-content declarations, making triple-wall formats the fastest-growing wall type at 5.87% CAGR.

What printing technology is expanding the fastest?

Digital inkjet, advancing at 5.82% CAGR, allows short-run customization, variable data, and rapid prototyping for e-commerce sellers and pharmaceutical brands.

Which regions consume the most corrugated packaging within Ghana?

Greater Accra, anchored by Tema Port, and Ashanti Region centered on Kumasi together account for the bulk of national demand due to dense industrial clusters and organized retail activity.

Page last updated on: