Pakistan Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

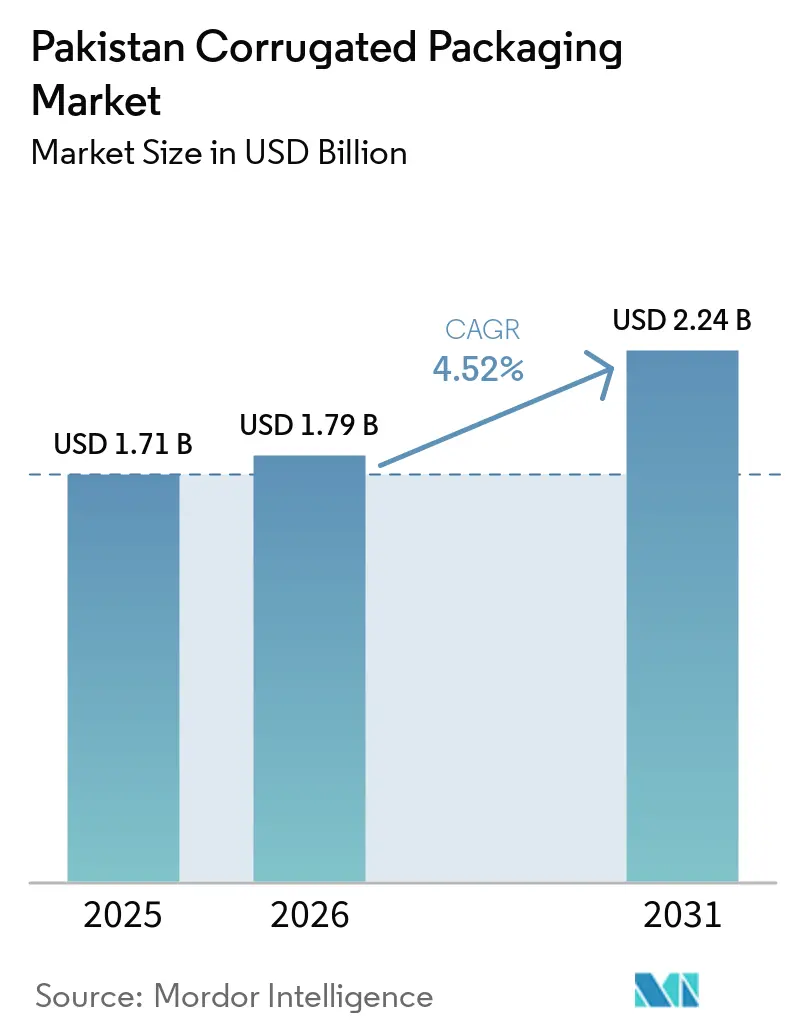

| Base Year Market Size (2025) | USD 1.71 Billion |

| Market Size (2026) | USD 1.79 Billion |

| Market Size (2031) | USD 2.24 Billion |

| Growth Rate (2026 - 2031) | 4.52% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pakistan Corrugated Packaging Market Analysis by Mordor Intelligence

The Pakistan corrugated packaging market size is expected to increase from USD 1.79 billion in 2026 to USD 2.24 billion by 2031, growing at a CAGR of 4.52% over 2026-2031. Demand is buoyed by e-commerce fulfillment investments, processed-food export incentives under the GSP Plus scheme, and the federal ban on single-use plastics that encourages fiber-based substitutes. Converters with backward integration into recycled linerboard mitigate raw-material volatility, while premium suppliers adopt virgin kraft to meet European buyers’ audit requirements. However, chronic energy load-shedding and imported kraft-pulp price swings compress margins and restrain the pace at which the Pakistan corrugated packaging market captures regional export orders. Mid-tier players are narrowing the gap with integrated majors by installing digital inkjet presses that shorten lead times for short production runs, an advantage when serving online sellers that require rapid artwork changes. Foreign participation remains limited because currency weakness and power insecurity raise perceived risk, yet local groups leverage the GSP Plus tariff window to position corrugated boxes as value-added, audit-compliant shipping solutions.

Key Report Takeaways

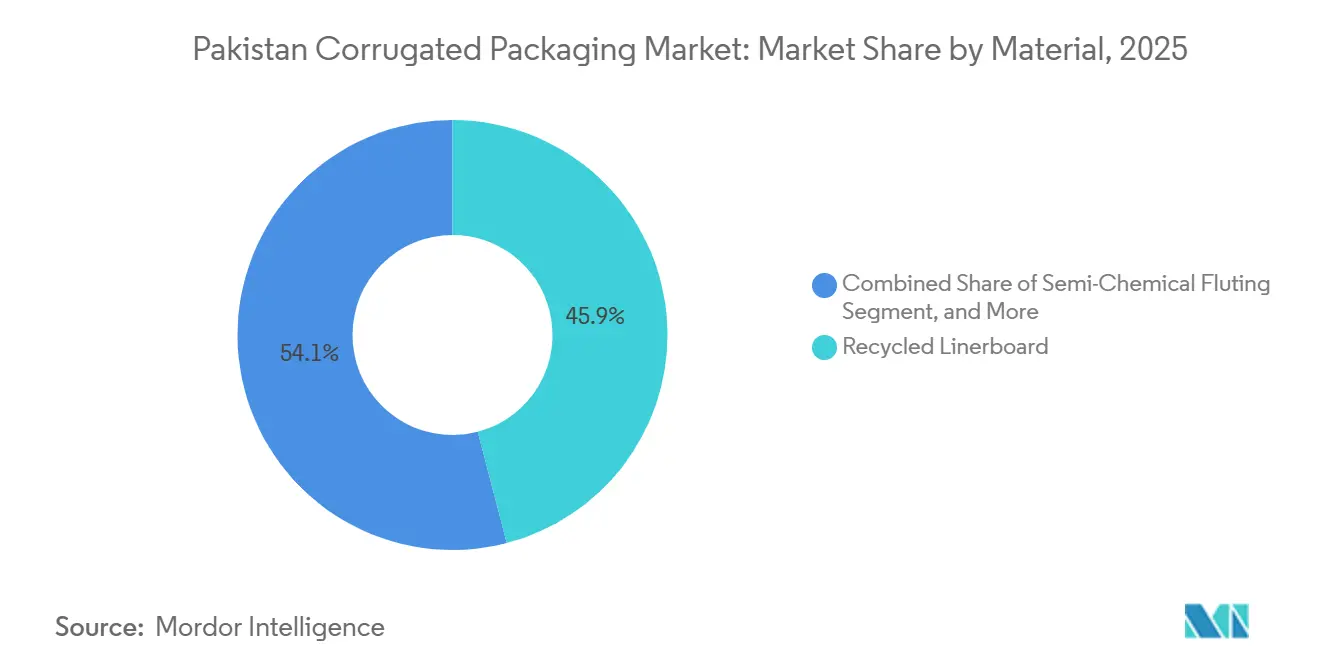

- By material, recycled linerboard captured 45.94% of the Pakistan corrugated packaging market share in 2025.

- By flute type, the Pakistan corrugated packaging market size for the E flute segment is forecast to advance at a 6.19% CAGR through 2031.

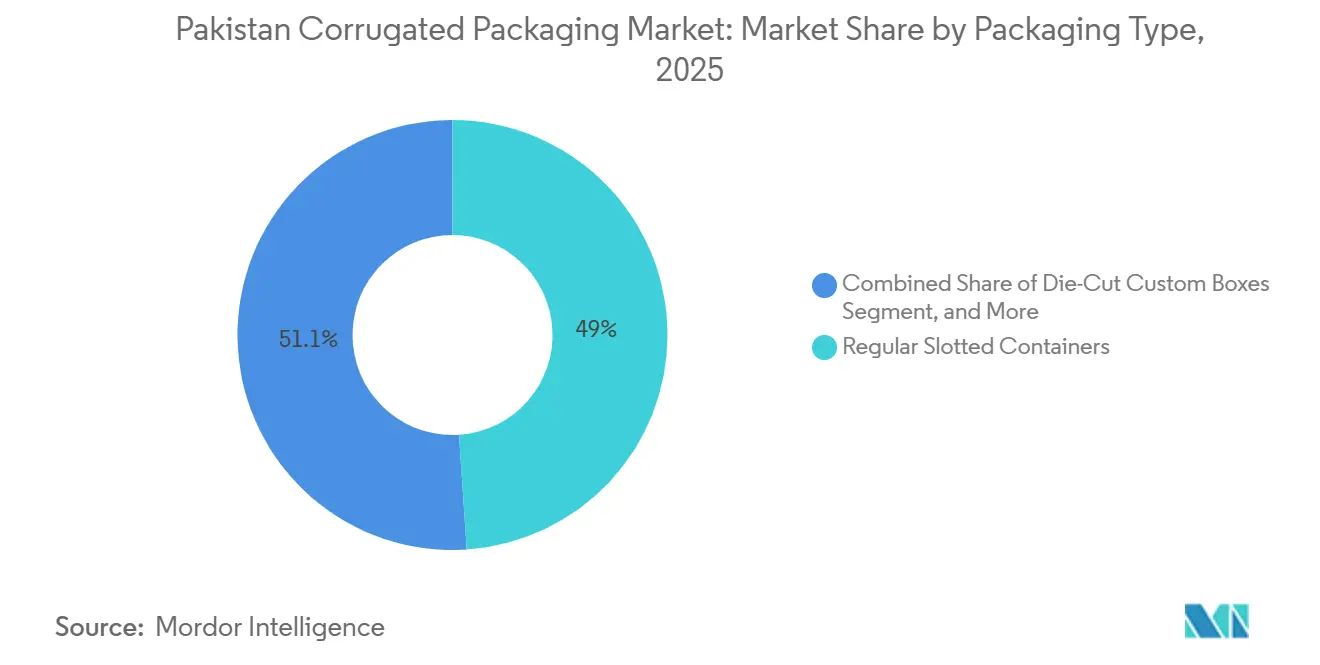

- By packaging type, regular slotted containers captured 48.95% of the Pakistan corrugated packaging market share in 2025.

- By wall construction, the Pakistan corrugated packaging market size for the triple-wall solutions segment is forecast to advance at a 5.81% CAGR through 2031.

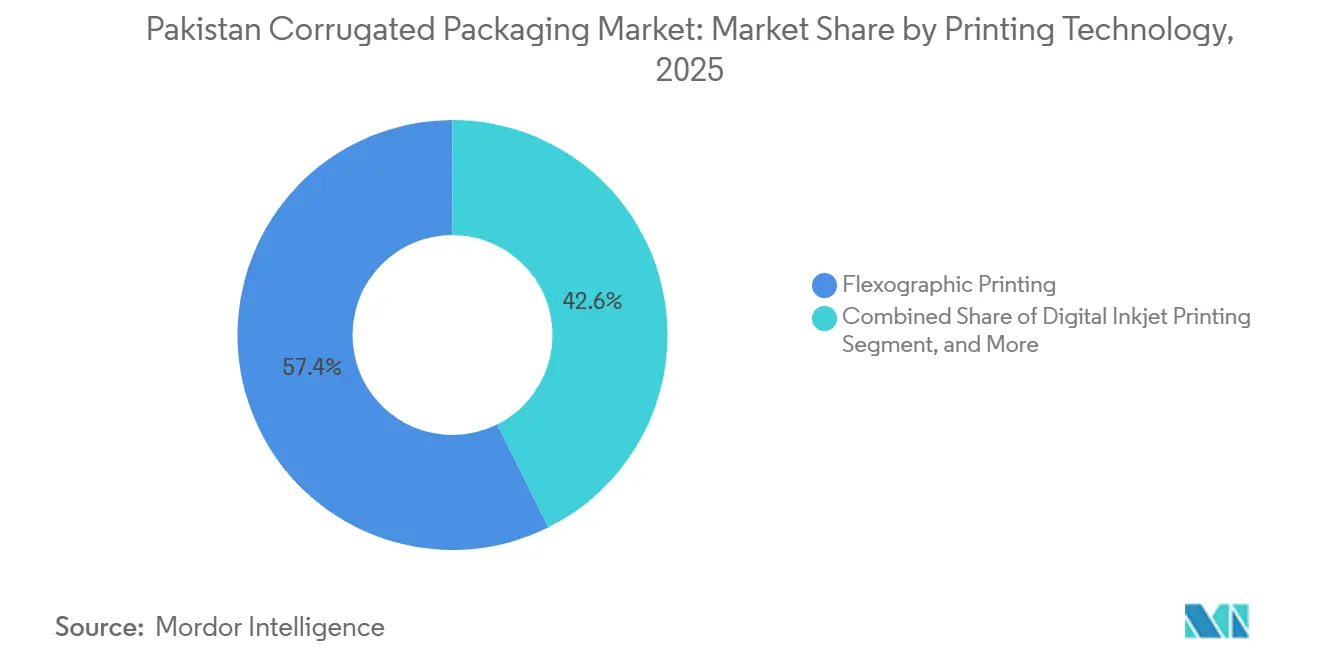

- By printing technology, flexographic presses captured 57.37% of the Pakistan corrugated packaging market share in 2025.

- By end-user, the Pakistan corrugated packaging market size for the e-commerce fulfillment centers segment is forecast to advance at a 5.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Pakistan Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion Of E-Commerce Fulfillment Infrastructure | +1.2% | National, concentrated in Karachi, Lahore, Islamabad | Short term (≤ 2 years) |

| Growth In Processed Food Exports Under GSP Plus Scheme | +0.9% | National, with export hubs in Karachi, Sialkot, Faisalabad | Medium term (2-4 years) |

| Government Push For Sustainable Packaging Standards | +0.7% | National, early adoption in Sindh, Punjab | Long term (≥ 4 years) |

| Rising Penetration Of Organized Retail Chains | +0.6% | Urban centers: Karachi, Lahore, Islamabad, Rawalpindi | Medium term (2-4 years) |

| SME Demand For Low-Volume Digital Printing Capability | +0.4% | National, clusters in Lahore, Karachi | Short term (≤ 2 years) |

| Adoption Of Fruit And Vegetable Crates To Reduce Post-Harvest Losses | +0.3% | Agricultural zones: Punjab, Sindh, Khyber Pakhtunkhwa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Expansion Of E-Commerce Fulfillment Infrastructure

Pakistan’s online retail value climbed to PKR 350 billion (USD 1.25 billion) in 2024, making corrugated cartons the default choice for last-mile handling. Daraz operates 12 fulfillment centers and secures 60% of boxes locally to sustain same-day promises, while the Pakistan Single Window platform reduced average customs clearance from 7 days to 48 hours in 2025, a milestone that allows cross-border sellers to run leaner inventories.[1]Pakistan Single Window Secretariat, “PSW Integration and Customs Clearance,” Government of Pakistan, psw.gov.pk Courier groups TCS, Leopards, and Pakistan Post invested PKR 5 billion (USD 0.017 billion) in automated sortation and installations that require standardized dimensions to maximize belt throughput. Mobile-wallet payments now account for 42% of checkout volume, and consumers expect visually appealing cartons that double as unboxing theatre. These preferences accelerate the adoption of die-cut, digitally printed boxes and fuel the growth trajectory of the Pakistan corrugated packaging market.

Growth In Processed Food Exports Under GSP Plus Scheme

The European Union renewed Pakistan’s GSP Plus status through 2027, eliminating tariffs on 66% of lines, including rice, confectionery, and canned fruit. Processed-food shipments to Europe totaled 285,000 tons in 2024 and generated USD 1.1 billion, with corrugated packaging accounting for up to 10% of landed costs.[2]Trade Development Authority of Pakistan, “Processed Food Exports to EU Under GSP Plus,” tdap.gov.pk Exporters now request virgin kraft liners that meet Forest Stewardship Council sourcing rules and European food-contact norms, prompting integrated mills to certify pulp chains. Rules-of-origin clauses push manufacturers to source cartons domestically rather than import printed blanks, thereby increasing local plant utilization. While Karachi and Sialkot conglomerates capitalize first, smaller converters across interior Punjab must raise quality control to enter audit-intensive European supply chains.

Government Push For Sustainable Packaging Standards

A 2023 ban on single-use plastic bags spurred retailers and produce markets to switch to corrugated crates. Draft Extended Producer Responsibility regulations circulated in late 2024 would obligate packaging companies to recover 40% of their output by 2028, mirroring frameworks in neighboring India.[3]Ministry of Climate Change, “Draft Extended Producer Responsibility Regulations,” mocc.gov.pk Sindh began enforcing recycled-content labels in February 2025, and Punjab plans similar rules, encouraging vertically integrated recyclers to scale capacity.[4]Sindh Environmental Protection Agency, “Guidelines on Recycled Content Labeling,” sepa.gos.pk Although compliance audits remain patchy, brand owners increasingly shortlist converters with internal waste-paper collection and traceability records. Over time, these measures expand the addressable market for Pakistan's corrugated packaging market among sustainability-minded customers.

Rising Penetration Of Organized Retail Chains

Modern retailers expanded floor space by 18% in 2024, reaching 320 outlets nationwide. Chains such as Carrefour and Metro Cash and Carry insist on ISO 12192 pallet stability and litho-laminated, shelf-ready trays that lower in-store labor costs. Brand owners pay 20-30% premiums for high-graphic corrugated displays that elevate shelf presence, and converters replied by installing faster die-cutters and digital printers. Trial launches often start with 500-1,000 printed boxes, a minimum order size well served by inkjet presses. This channel evolution augments revenue diversity and underpins margin resilience for Pakistan corrugated packaging industry participants targeting premium formats.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility In Imported Kraft Pulp Prices | -0.8% | National, acute for import-dependent converters | Short term (≤ 2 years) |

| Chronic Energy Supply Interruptions Raising Production Costs | -0.6% | National, severe in Punjab, Khyber Pakhtunkhwa | Medium term (2-4 years) |

| Fragmented Collection Of Recyclable Paper Waste | -0.3% | Urban centers: Karachi, Lahore, Faisalabad | Long term (≥ 4 years) |

| Limited Design Competency Among Small-Scale Converters | -0.2% | National, concentrated in secondary cities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility In Imported Kraft Pulp Prices

Pakistan satisfies 85% of its kraft-pulp demand through imports priced between USD 800 and 1,100 per metric ton during 2024-2025. Total volumes reached 420,000 tons, valued at USD 380 million, in 2024, ranking pulp as the sector’s third-largest raw-material import. Currency depreciation from PKR 278 (USD 0.99) to PKR 305 (USD 2.31) per USD lifted local-currency cost by 9.7%, squeezing converters with 8-12% gross margins. Lacking scale to lock multi-year contracts, medium and small plants buy on spot terms and absorb 15-20% quarterly price swings. An industry petition to cut the pulp import duty from 11% to 5% remains pending, prolonging exposure and dampening the cost competitiveness of the Pakistan corrugated packaging market.

Chronic Energy Supply Interruptions Raising Production Costs

Industrial load-shedding averaged eight to ten hours a day in 2024, forcing plants onto diesel generators that yield electricity at PKR 45-50 (USD 0.34-0.37) per kWh versus the grid’s PKR 28 (USD 0.21) rate. Energy accounts for up to 15% of unit cost, so each hour of outage erodes price parity with Indian and Bangladeshi suppliers served by steadier grids. Planned liquefied-natural-gas terminals and renewables will relieve shortages only after 2027, meaning converters must budget premium fuel spend for most of the forecast horizon. The persistence of this constraint tempers expansion plans among foreign strategic investors who assess the Pakistan corrugated packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Linerboard Retains Scale as Virgin Kraft Gains Audit-Driven Acceptance

Recycled linerboard accounted for 45.94% of 2025 revenue, reflecting Pakistan's corrugated packaging market buyers’ preference for the province-wide scrap network that supplies low-cost furnish to mills in Lahore and Karachi. Local scrap dealers aggregate used cartons at PKR 15-20 (USD 0.11-0.15) per kilogram, a feedstock price that cushions converters from the volatility of imported pulp. Virgin Kraft linerboard, however, is projected to record the fastest CAGR of 5.14%, as European customers now demand Forest Stewardship Council certificates and higher-burst-strength boxes for cold-chain exports. Semi-chemical fluting and barrier-coated substrates serve niche orders tied to moisture-sensitive produce and pharmaceuticals, but contribute little volume.

Investment patterns illustrate a clear split commodity box producers double down on recycled inputs to protect margins, while export-oriented plants purchase higher-grade pulp to satisfy traceability audits. These divergent strategies enlarge the addressable Pakistan corrugated packaging market size for integrated mills that can toggle between fiber streams without disrupting run rates. Yet, converters focused on recycled furnish remain exposed to spot shortages whenever informal scrap networks divert board to tissue makers during peak demand months. The dual-track trajectory is therefore expected to persist through 2031 as long as the GSP Plus window rewards audit-compliant packaging.

By Flute Type: E Flute Moves From Niche to Mass Retail Shelf Favorite

C flute controlled 34.26% share in 2025, thanks to its 3.5 mm profile that balances stacking strength with unit cost for processed foods and beverages. B flute supports mid-weight applications such as paper products, while A flute’s thicker profile protects fragile goods traveling long road distances. The E flute, only 1.5 mm thick, is forecast to expand at a 6.19% CAGR, as cosmetics, over-the-counter drugs, and online apparel sellers prefer thin, printable board that reduces freight costs.

E flute’s surge forces converters to invest in precision slotters and high-graphic presses capable of 120-lpi line screens, equipment that historically only large plants could justify. Lower flute height also improves pallet fill, a metric that organized retailers now measure to cut aisle restocking time. Together, these factors embed E flute as the high-visibility face of the Pakistan corrugated packaging market, while legacy A and B flutes remain essential for heavy payloads moving to the Gulf in un-refrigerated containers.

By Packaging Type: Die-Cut Custom Boxes Outpace Commodity Regular Slotted Containers

Regular slotted containers (RSCs) accounted for 48.95% of 2025 revenue, as automated folder-gluer systems deliver consistent quality at high speeds for rice, confectionery, and tissue rolls. Despite dominance, die-cut custom boxes are projected to expand at 5.25% CAGR as brands pursue shelf impact and social-media “unboxing” aesthetics. Folding cartons intersect with corrugated at the lightweight end of the spectrum, particularly in personal-care and stationery lines demanding litho-laminated graphics.

Point-of-purchase displays generate premium margins because design labor, not flute board, drives price. Meanwhile, pallet boxes combine triple-wall plies with corner posts to meet forklift abuse tolerance for export electrical goods. The shift toward bespoke structures, therefore, widens revenue prospects for mid-tier firms adopting digital cutting tables that turn artwork uploads into finished blanks within 48 hours, enhancing agility in the Pakistan corrugated packaging market.

By Wall Type: Triple-Wall Captures Export Flows While Single-Wall Dominates Domestic Runs

Single-wall cases represented 62.24% of shipments in 2025, retaining leadership in supermarket staples that travel short hauls on mixed pallets. Double-wall boxes handle moderate loads, such as bottled beverages, where vibration and moisture make an extra ply prudent. Triple-wall output is forecast to grow at a 5.81% CAGR, as electrical-goods exporters shipping to the Gulf require burst strengths above 275 psi and edge-crush values exceeding 12 kN m⁻¹.

New pallet-box regulations expected in 2027 will formalize those thresholds, nudging additional buyers toward heavy-duty builds. Yet, triple-wall commands a 40-50% cost premium that price-sensitive domestic buyers often reject, so its penetration will remain export-centric. This two-speed adoption pattern nonetheless enlarges the premium tier of the Pakistan corrugated packaging market, rewarding converters that can toggle flute combinations without re-threading starch systems.

By Printing Technology: Digital Inkjet Shrinks Order Minimums and Lead Times

Flexographic presses accounted for 57.37% of 2025 revenue and are favored for runs exceeding 5,000 boxes, where plate amortization keeps unit cost below PKR 6 (USD 0.04) per square meter. Digital inkjet lines are on track for the fastest 5.53% CAGR, as SME brands launch capsule collections or regional flavor trials that rarely top 2,000 pieces. Inkjet also unlocks variable data, such as QR codes and personalization, that fuel social-commerce campaigns.

Litho-lamination retains a luxury niche, bonding offset-printed liners to micro flute blanks used in cosmetics or confectionery gift packs. Screen and UV-curable systems round out the toolkit for metallic inks or moisture-barrier overprints. As converters retool, the Pakistan corrugated packaging market benefits from a wider service spectrum that meets both mass-production economics and fast-fashion branding cycles.

By End-User Industry: E-Commerce Fulfillment Centers Deliver the Fastest Upside

Processed foods accounted for 29.53% of 2025 revenue, with shipments of rice, spices, and snacks to Middle Eastern and European buyers under GSP Plus duty waivers. Fresh produce is shipped in wax-coated crates, but growth is capped by cold-chain gaps that push shrinkage to 30%. Electrical products demand triple-wall pallet boxes to secure fans, cables, and switchgear against mechanical shocks on sea legs.

E-commerce fulfillment centers are projected to post a 5.93% CAGR as Daraz, TCS, and Leopards automate sortation hubs that mandate dimension-controlled cartons. Personal-care and cosmetics brands adopt litho-laminated folding cartons to capture impulse buys in organized retail aisles. Pharmaceuticals layer desiccant and tamper indicators to comply with Drug Regulatory Authority rules, while automotive and construction trades absorb residual tonnage during public-sector project peaks. Each segment enlarges specialized corners of the Pakistan corrugated packaging market, ensuring diversified demand even when one vertical cools.

Geography Analysis

Punjab and Sindh together accounted for about 75-80% of 2025 demand, anchoring the Pakistan corrugated packaging market in the industrial corridors that link Lahore, Faisalabad, and Karachi. Punjab’s Sundar, Kot Lakhpat, and Sheikhupura estates host an estimated 60% of national converting capacity, supplying processed-food exporters and organized retail chains. Load-shedding remains acute in these clusters, pushing energy costs 40-60% above grid tariffs and narrowing price parity with Indian suppliers. Provincial draft rules that mandate recycled-content labels by 2027 will favor integrated mills able to certify waste-paper provenance. The confluence of export hubs, agricultural hinterlands, and regulatory pressure keeps Punjab central to future Pakistan corrugated packaging market expansion.

Sindh’s share centers on Karachi, the country’s primary seaport and gateway for kraft-pulp imports that feed integrated plants such as Packages Limited and Roshan Packages. Karachi’s metro area also concentrates multinational FMCG buyers that stipulate European Conformity standards for food-contact cartons, stimulating uptake of virgin kraft linerboard. The Sindh Environmental Protection Agency’s 2025 recycled-content guidelines add paperwork costs, but converters that install traceability software secure preferred-supplier status. Container throughput of 2.1 million TEUs in 2024 underpins steady call-offs for export-grade boxes, reinforcing Sindh’s role as the logistics spine of the Pakistan corrugated packaging market. Still, informal scrap-collection networks dominate waste supply and create 20-30% price swings when volumes tighten.

Khyber Pakhtunkhwa and Balochistan contribute the remaining share, hampered by scarce industrial estates and higher overland freight from seaports that inflate box delivered cost. China-Pakistan Economic Corridor highways have shortened Lahore-Quetta transit by several hours, yet cold-chain gaps curtail fresh-produce crate volumes that could diversify demand. Provincial incentives for agro-processing parks may lift local consumption from 2027 forward, but near-term momentum stays with Punjab-Sindh corridors where the Pakistan corrugated packaging market already commands scale advantages. Altogether, geography continues to shape investment choices, labor availability, and fiber sourcing strategies for converters seeking growth.

Competitive Landscape

The top five converters, Packages Limited, Roshan Packages, Bulleh Shah Packaging, Century Paper and Board Mills, and Reliance Packages, held roughly 40-45% Pakistan corrugated packaging market share in 2025, leaving a long tail of 400-500 small enterprises that compete on price and locality. Packages Limited pairs kraft paper mills with high-speed corrugators topping 150,000 tons of annual capacity, enabling national service to multinational FMCG accounts. Roshan Packages follows a similar integration path to hedge imported pulp volatility and has pivoted toward export-grade food cartons that command audit premiums. Bulleh Shah and Century Paper target mid-tier volumes, while Reliance Packages invests in regional capacity additions that shorten lead times for Punjab exporters.

Mid-tier firms differentiate through digital inkjet and litho-lamination, supplying point-of-purchase displays and e-commerce boxes that require variable graphics. These capabilities lift margins above commodity levels and help retain clients migrating to organized retail. White-space opportunities appear in wax-coated fruit crates and tamper-evident pharmaceutical cartons, but both niches demand capital for specialty lines that only a fraction of converters can fund. International majors such as Mondi and International Paper remain advisory partners rather than direct investors, citing energy insecurity and currency swings that weigh on EBITDA forecasts inside the Pakistan corrugated packaging market.

Regulatory tightening on edge-crush and burst-strength metrics may accelerate consolidation as under-capitalized plants struggle to finance laboratory upgrades and third-party audits. The prospect of duty relief on imported pulp would ease raw-material strain, but has yet to clear fiscal committees. Until then, integrated groups leverage scale to lock pulp lots and hedge fuel costs, while small shops survive by servicing local FMCG vendors that accept thin profit cushions. Competitive positioning, therefore, turns on integration depth, print sophistication, and compliance readiness, all key levers that shape value capture in the Pakistan corrugated packaging market.

Pakistan Corrugated Packaging Industry Leaders

Packages Limited

Roshan Packages Limited

Bulleh Shah Packaging (Pvt.) Limited

Century Paper & Board Mills Limited

International Paper Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Packages Limited expanded its sustainable corrugated packaging operations through Bulleh Shah Packaging.

- March 2025: Packages Limited announced a PKR 3.5 billion (USD 11.5 million) expansion of its corrugating capacity in Kasur, Punjab, adding 25,000 tons per year of single-face and double-wall production to serve export-oriented processed-food manufacturers.

- February 2025: Bulleh Shah Packaging received ISO 12192 certification for pallet stability, enabling bids for organized-retail accounts that mandate standardized corrugated displays.

- January 2025: The Pakistan Single Window system went live, digitizing customs clearance and cutting average processing time from seven days to 48 hours, a catalyst for just-in-time e-commerce logistics.

Pakistan Corrugated Packaging Market Report Scope

The Pakistan Corrugated Packaging Market report encompasses a comprehensive analysis of fiber-based and polymer-based corrugated materials used for the containment, protection, and transport of goods across diverse industrial and retail sectors. The market refers to the industry that produces multi-layered boards, typically consisting of a fluted medium sandwiched between linerboards, designed to provide high strength-to-weight ratios and crush resistance for secondary and tertiary packaging.

The Pakistan Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Paper Products |

| Electrical Products |

| Personal Care and Cosmetics |

| E-Commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Paper Products | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-Commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the 2026 value of the Pakistan corrugated packaging market size?

The Pakistan corrugated packaging market size stands at USD 1.79 billion in 2026 and is forecast to reach USD 2.24 billion by 2031, according to Mordor Intelligence.

Which material leads demand in Pakistan's corrugated sector?

Recycled linerboard leads with 45.94% 2025 share, though virgin kraft is the fastest-growing material at a 5.14% CAGR.

Why is E flute gaining popularity among converters?

E flute's thin 1.5 mm profile supports high-resolution graphics and lowers freight cost, making it attractive for cosmetics, pharmaceuticals, and e-commerce packaging.

How are energy outages affecting corrugated box prices?

Load-shedding forces factories to rely on diesel generators that cost PKR 45-50 (USD 0.34-0.37) per kWh, raising production expenses by up to 60% versus grid power.

Which end-user segment will grow fastest through 2031?

E-commerce fulfillment centers will post the highest 5.93% CAGR as automated sorting hubs demand dimension-controlled cartons.

What regulatory trend is reshaping packaging sustainability?

Draft Extended Producer Responsibility rules aim for 40% recovery and recycling of packaging by 2028, steering buyers toward converters with closed-loop waste systems.

Page last updated on: