Asia-Pacific Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

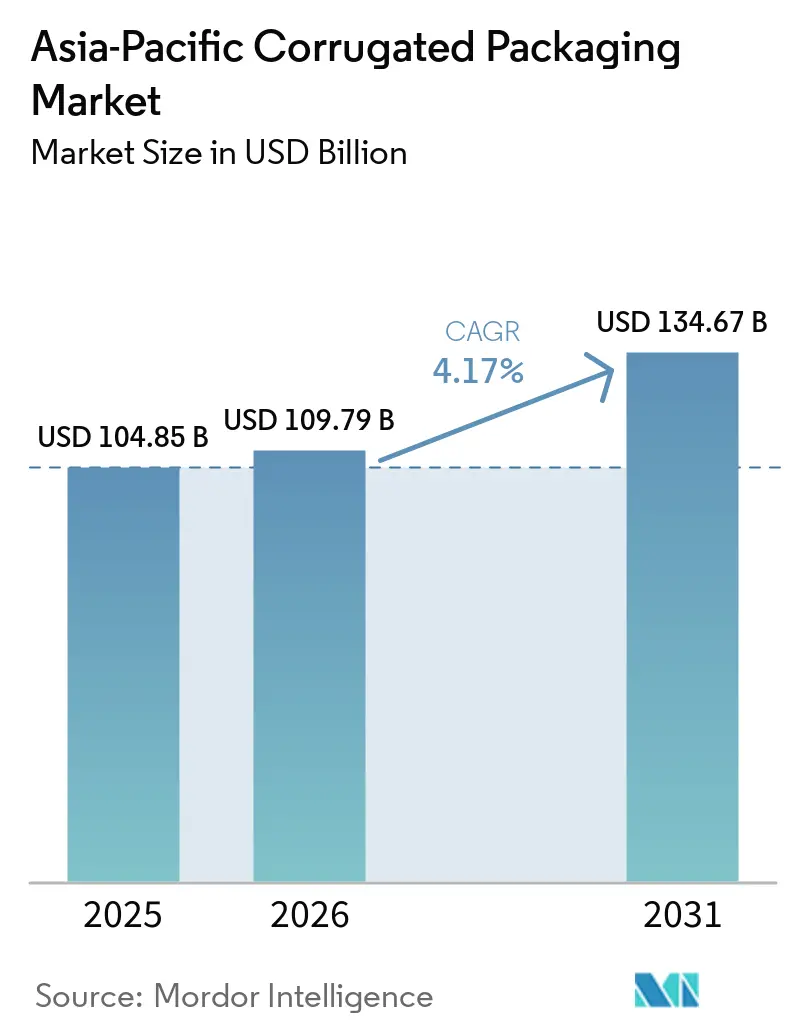

| Base Year Market Size (2025) | USD 104.85 Billion |

| Market Size (2026) | USD 109.79 Billion |

| Market Size (2031) | USD 134.67 Billion |

| Growth Rate (2026 - 2031) | 4.17% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia-Pacific Corrugated Packaging Market Analysis by Mordor Intelligence

The Asia-Pacific corrugated packaging market size is expected to grow from USD 104.85 billion in 2025 to USD 109.79 billion in 2026 and is forecast to reach USD 134.67 billion by 2031 at 4.17% CAGR over 2026-2031. Robust e-commerce activity in China and India, expanding pharmaceutical cold-chain networks, and government mandates that favor recyclable substrates are accelerating demand at a pace that is stretching legacy converting capacity. Recycled linerboard dominance is anchoring cost structures, yet premium food and healthcare applications are steadily shifting toward virgin kraft grades, creating a dual-track material landscape. Integrated producers are capitalizing on vertical control of fiber and energy inputs to cushion raw-material volatility, while non-integrated converters are facing margin compression, forcing consolidation, automation, and tighter supplier agreements. Regulatory pressure to minimize packaging waste and tighten effluent standards is reshaping capital-investment priorities toward water-efficient mills, closed-loop recycling, and advanced printing lines that support variable data and serialization.

Key Report Takeaways

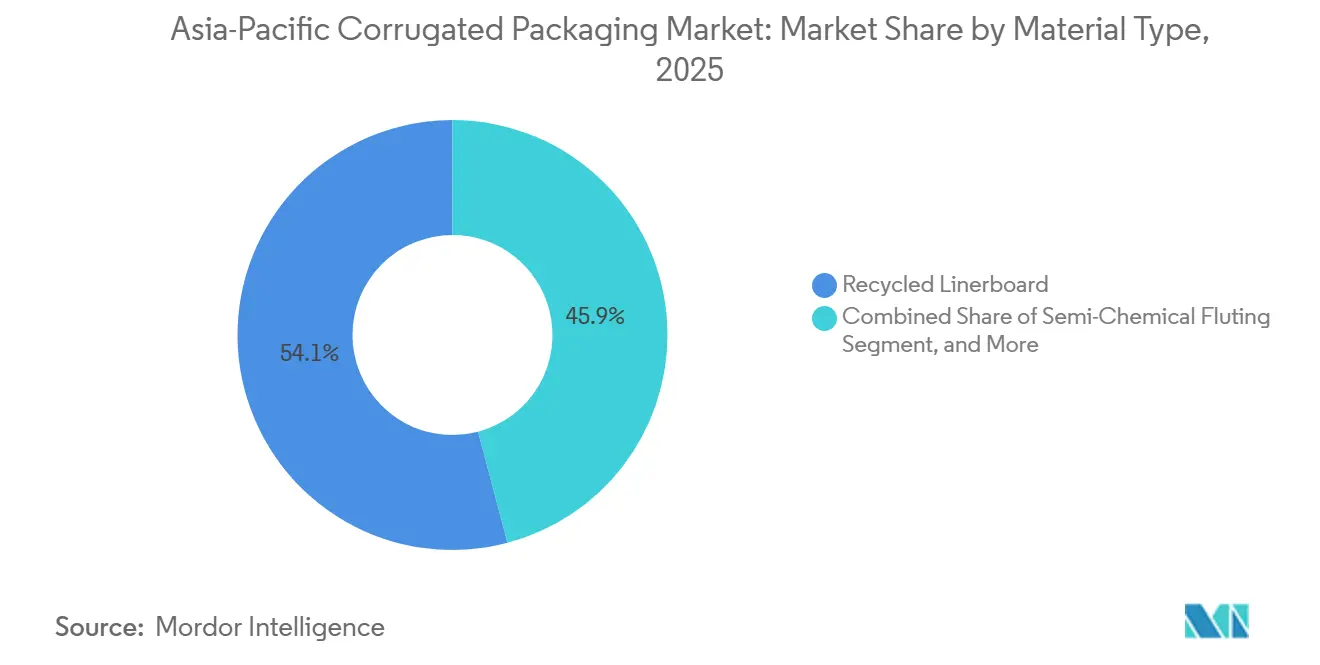

- By material type, the recycled linerboard segment captured 54.12% of the Asia-Pacific corrugated packaging market share in 2025.

- By flute type, the Asia-Pacific corrugated packaging market size for e flute is projected to grow at an 5.23% CAGR through 2031.

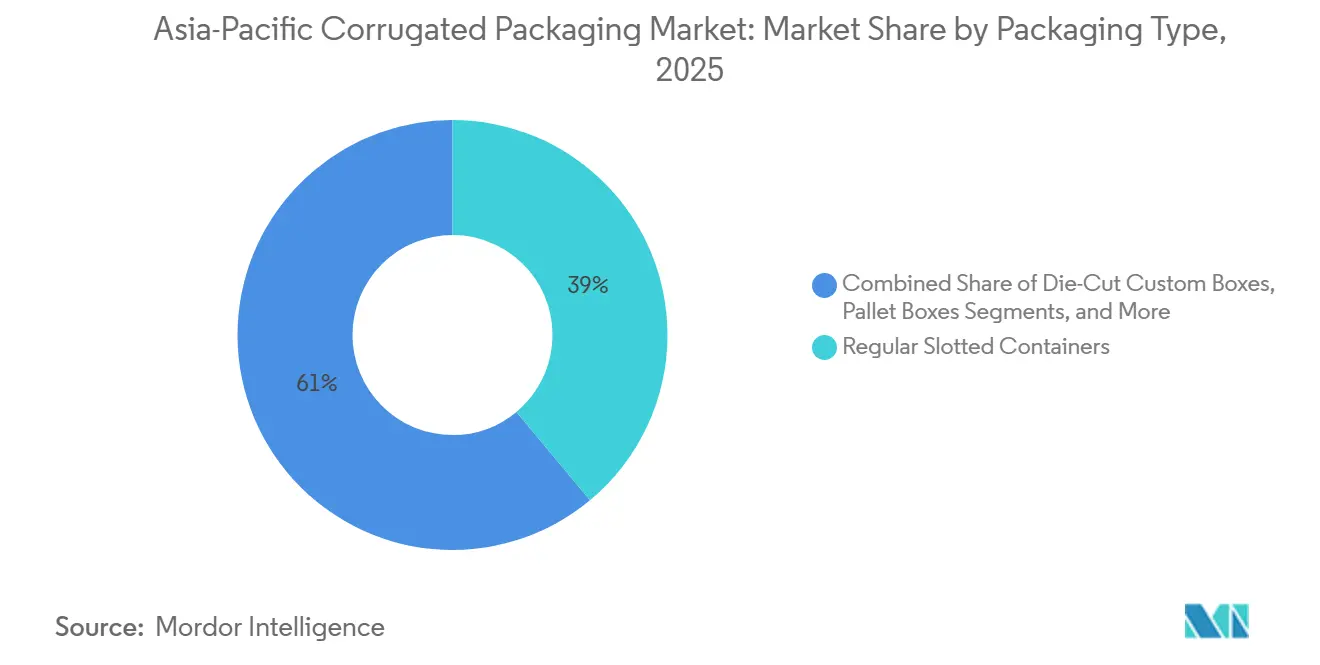

- By packaging type, the regular slotted containers segment captured 38.96% of the Asia-Pacific corrugated packaging market share in 2025.

- By wall type, the Asia-Pacific corrugated packaging market size for double-wall is projected to grow at an 5.56% CAGR through 2031.

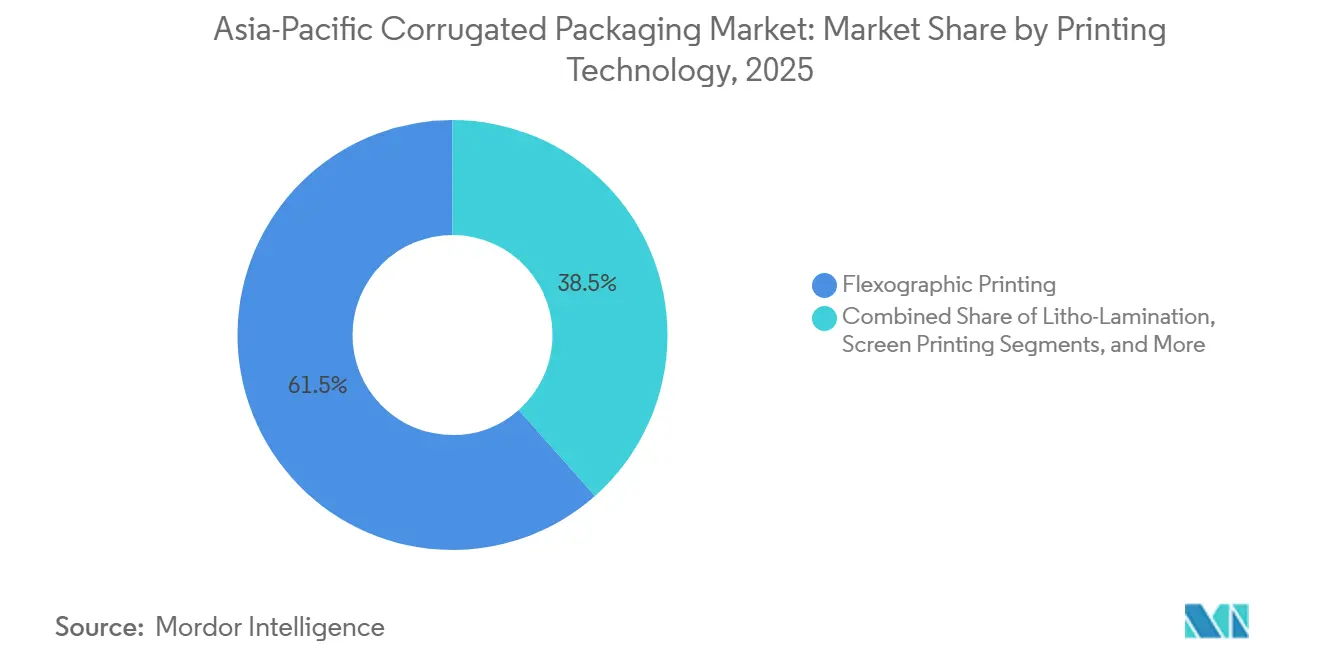

- By printing technology, the flexographic printing segment captured 61.53% of the Asia-Pacific corrugated packaging market share in 2025.

- By end-user industry, the Asia-Pacific corrugated packaging market size for e-commerce fulfillment centers is projected to grow at an 5.68% CAGR through 2031.

- By geogrophy, the China region captured 49.63% of the Asia-Pacific corrugated packaging market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia-Pacific Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Food and Beverage Consumption in Emerging Asian Economies | +1.2% | China, India, ASEAN core (Vietnam, Indonesia, Thailand) | Medium term (2-4 years) |

| Shift Toward Sustainable and Recyclable Packaging Materials | +0.9% | Japan, South Korea, Australia, and broader Asia-Pacific | Long term (≥4 years) |

| Rapid Expansion of E-Commerce and Omni-Channel Retail | +1.0% | China, India, Southeast Asia urban corridors | Short term (≤2 years) |

| Increasing Pharmaceutical Production and Healthcare Spending | +0.6% | India, China, ASEAN pharma hubs | Medium term (2-4 years) |

| Government-Led Subsidies for High-Color Digital Carton Printing | +0.3% | India, Vietnam, and Indonesia are export zones | Medium term (2-4 years) |

| Adoption of Fungus-Based Barrier Coatings Replacing Plastic Liners | +0.2% | Japan, South Korea, Australia pilots; China, India scale-up | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Food and Beverage Consumption in Emerging Asian Economies

Rising urban incomes across China, India, and core ASEAN nations are boosting per capita purchases of packaged produce, processed foods, and beverages. Corrugated demand benefits directly because perishable exports require ventilated, moisture-resistant shippers that protect against temperature swings during multimodal transport. China’s express-delivery network handled over 175 billion parcels in 2024, a surge that is translating into secondary demand for fruit and meal-kit shippers as e-grocers widen same-day coverage. Stringent food-contact rules, such as Indonesia’s SNI 8218:2024 and Thailand’s TIS standards, have raised compliance costs, prompting converters to migrate premium SKUs to virgin kraft. India’s 2025 anti-subsidy probe on imported paperboards is already shifting supply chains toward domestic mills, tightening recovered-fiber markets, and incentivizing investment in high-basis-weight machines.

Shift Toward Sustainable and Recyclable Packaging Materials

Extended producer responsibility schemes in Japan and South Korea require brand owners to document recycled content and end-of-life pathways, a structure that is quickly influencing purchasing teams across the wider region. Recycled linerboard already held 54.12% share in 2025, yet food and pharma brands are paying premiums for virgin grades with certified chain-of-custody to meet global audit requirements. The University of Maine demonstrated that Trametes versicolor fungus-derived coatings can replace polyethylene liners while maintaining moisture resistance and improving repulpability.[1]University of Maine, “Trametes versicolor Fungus-Derived Hydrophobic Coatings,” acs.org Multinationals such as Mondi are responding with EUR 1.2 billion (USD 1.3 billion) in mill upgrades that raise recovered-fiber utilization without sacrificing mechanical strength, positioning their kraft portfolio for a future in which carbon and recyclability scores sit alongside unit cost in sourcing decisions.

Rapid Expansion of E-Commerce and Omni-Channel Retail

E-commerce fulfillment centers are expanding at 5.68% CAGR through 2031, far outpacing traditional retail channels. China’s June 2025 courier regulation banning excessive wrapping is pushing platforms toward right-sized boxes and reusable strapping, reducing material intensity per shipment. JD Logistics eliminated more than 1 billion secondary packs in 2024 by shipping appliances in original manufacturer cartons, proving that optimized design can cut costs and emissions simultaneously.

Increasing Pharmaceutical Production and Healthcare Spending

Asia-Pacific governments are funneling stimulus into vaccine plants, biologics clusters, and medical-device parks. Insulated corrugated shippers that house phase-change materials are therefore gaining ground as cost-effective exteriors for cold-chain payloads. Zuellig Pharma’s Philippine network now spans 59,000 m² of temperature-controlled warehousing, a footprint that translates into millions of tertiary cartons annually. India’s Budget 2026 earmarked INR 12.2 lakh crore (USD 145 billion) for infrastructure, with a dedicated MSME fund that lowers financing costs for box plants targeting export pharma corridors. Because corrugated’s fluted structure provides natural insulation and excellent print real estate for regulatory barcodes, the segment is expected to maintain resilient high-single-digit growth despite competing foam-based systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Paperboard Raw Material Prices | -0.7% | Global, acute in import-dependent Southeast Asia and Australia | Short term (≤2 years) |

| Competition from Flexible Packaging Formats | -0.5% | Urban centers in China, India, and Southeast Asia | Medium term (2-4 years) |

| Tightening Regional Water-Use Regulations Increasing Mill Operating Costs | -0.3% | India and China's water-stressed provinces | Long term (≥4 years) |

| Shortage of Skilled Technicians for High-Speed Folding-Gluing Lines | -0.2% | India, Vietnam, Indonesia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Paperboard Raw Material Prices

Capacity closures totaling 2.5 million tons in North America and logistics snarls in the Panama Canal have whipsawed kraft linerboard spot prices, compressing converter margins. Integrated giants such as Nine Dragons and Lee and Man posted triple-digit profit jumps in 2025 because captive fiber insulated them from spikes, while small converters operating on spot contracts saw working-capital cycles stretch dangerously. India’s anti-subsidy probe on Chinese and Indonesian boards is reshaping Asia-Pacific trade flows, yet new domestic mills will not come online until 2027, meaning price turbulence will persist in the near term.

Competition from Flexible Packaging Formats

Flexible pouches and bags weigh less, cut freight bills, and run efficiently on high-speed form-fill-seal lines, luring snack and personal-care brands away from corrugated secondary packs. Mondi’s flexible division generated EUR 558 million (USD 610 million) EBITDA in 2024 despite margin pressure, underlining the scale of capital moving into film lines. Corrugated converters are countering by adopting E flute and F flute micro-profiles that save material without sacrificing crush strength, and by touting superior curb-side recyclability to align with circular-economy mandates.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Dual-Track Growth Shapes Fiber Strategies

Recycled linerboard secured 54.12% of the Asia-Pacific corrugated packaging market share in 2025 as cost-sensitive e-commerce and industrial users optimize transportation budgets. Virgin Kraft is expanding at 5.62% CAGR, capturing high-margin niches where direct food contact and pharmaceutical purity standards dictate certified fiber chains. This divergence is sharpening supplier specialization; Indonesian mills are adding virgin capacity, while Chinese converters deepen recovered-fiber loops to insulate against import curbs.

Converters reliant on recycled grades must now invest in optical sorters and moisture-control systems to meet China’s GB/T 6543-2025 squareness and compression mandates, which come into force in December 2025.[2]GB/T 6543-2025 Standard Committee, “Single and Double Corrugated Boxes for Transport Packages,” sac.gov.cn Meanwhile, premium exporters of seafood and fresh produce are locking in multi-year virgin kraft contracts to secure moisture tolerance during trans-Pacific voyages, widening the price delta between commodity and specialty grades.

By Flute Type: Micro-Profiles Accelerate Lightweighting

C flute retained 53.78% share in 2025, balancing cushioning and compression strength for general shipping needs, but E flute is advancing at 5.23% CAGR as retailers pursue thinner profiles that slash cube utilization and freight emissions. DS Smith’s 2026 investment in a Göpfert rotary die-cutter illustrates the race to deliver micro-flute accuracy at an industrial scale, as cosmetics, electronics, and personal-care brands demand litho-like print fidelity on corrugated substrates. F-flute, though smaller in volume, is gaining traction in luxury gift packs and subscription boxes, where tactile unboxing experiences must coexist with drop-test robustness.

The pivot toward micro-flutes obliges mills to supply smoother, high-stiffness linerboard that tolerates tighter caliper tolerances, again favoring integrated producers that can blend virgin and recovered fibers on the same machine. Converters must weigh the higher capital outlay for fine-flute corrugators against the logistical savings clients achieve via lighter, flatter boxes that fill truck decks more efficiently. As e-commerce algorithms optimize dimensional weight billing, brand owners will push box makers toward ever-thinner profiles, cementing E flute and F flute as the fastest-growing niches within the Asia-Pacific corrugated packaging market over the next five years.

By Packaging Type: Custom Die-Cut Formats Redefine Brand Storytelling

Regular slotted containers accounted for 38.96% share in 2025 because standardized die libraries, rapid set-ups, and universal pallet fit keep costs low for commodity goods, yet die-cut custom boxes are growing at 5.45% CAGR as omnichannel merchants crave shelf-ready designs that double as brand theater. Wide-format digital cutters paired with CAD-driven design software let converters launch complex geometries within days, bringing formerly premium aesthetics to mid-volume campaigns and flash sales. Folding cartons and point-of-purchase displays remain important for high-impact merchandising, though their growth is checked by cheaper flexible stand-up pouches in snack and confectionery aisles.

Bulk bins and pallet boxes, while niche, remain irreplaceable for heavy machinery, auto parts, and agricultural exports where triple-wall builds prevent corner-crush failures. Smurfit WestRock’s 2026 Cartomanabí acquisition underscores the strategic value of regional converting footprints that can deliver bespoke die-cuts with just-in-time reliability, eliminating costly inter-regional transfers. Over the forecast window, the Asia-Pacific corrugated packaging market will see custom die-cuts move from marketing novelty to mainstream requirement as retailers cut store labor by placing shelf-ready cartons directly onto gondolas.

By Wall Type: Double-Wall Designs Cushion Supply-Chain Shocks

Single-wall constructions held a 34.78% share in 2025 because light consumer goods seldom exceed compression limits, but double-wall boxes are increasing at a 5.56% CAGR as automated warehouses boost stacking heights and beverages adopt heavier unit loads for export. China’s GB/T 6543-2025 imposes tougher empty-box compression thresholds, prompting exporters of electronics, household appliances, and wine to up-gauge walls despite higher paper consumption. Triple-wall remains restricted to industrial motors, EV battery packs, and bulk chemicals where drop damage or puncture risk outweighs material cost.

Visy’s AUD 30 million (USD 20 million) Brisbane mill upgrade and AUD 20 million (USD 13 million) Tasmania hub illustrate the investment needed to run heavier basis-weight kraft and multi-wall laminations at scale. Converters that perfect adhesive uniformity and flute-to-liner bonding will command premiums because failed seams in a double-wall cost far more in product recalls than the incremental paper. As multimodal logistics proliferate, combining road, rail, and sea in the same shipment, the Asia-Pacific corrugated packaging market will continue to tilt toward double-wall for any product where secondary handling cycles exceed legacy norms.

By Printing Technology: Digital Inkjet Closes the Cost Gap

Flexographic presses captured 61.53% share in 2025 due to unmatched throughput on long runs, low ink costs, and broad operator familiarity, yet digital inkjet is rising at a 5.78% CAGR on the back of falling click rates and government subsidies that shorten payback periods for presses costing over USD 2 million. Wide-web inkjet machines now run up to 400 m per minute, pushing the economic break-even against mid-tier flexo to jobs below 10,000 linear m, a volume sweet spot for fast-fashion brands and limited-edition promotions. India and Vietnam subsidize up to 30% of capital outlay for Industry 4.0 digital lines, spurring smaller converters to leapfrog directly into variable-data workflows that embed QR codes and serial numbers for track-and-trace.

Hybrid pressrooms that lay down base coats on flexo units and overlay buyer-specific graphics via inkjet are emerging as the operational gold standard for export hubs that juggle many SKUs with volatile order sizes. Litho-lamination still rules ultra-premium alcohol and cosmetic boxes where metallic foils and tactile varnishes justify high unit prices, but environmental audits examining solvent use and laminate recyclability could cap its upside. Over the next decade, the Asia-Pacific corrugated packaging market will see digital inkjet move from the fringe to the foundational as brand owners demand both agility and data-rich packaging that flexo alone cannot provide.

By End-User Industry: Fulfillment Hubs Reshape Specification Dashboards

Fresh food and produce represented 43.56% of end-user demand in 2025 to Asia-Pacific region’s leading share of global fruit, vegetable, and seafood exports that rely on ventilated, moisture-resistant cartons. E-commerce fulfillment centers are projected to grow fastest at 5.68% CAGR because platforms now treat packaging as an extension of the customer experience, linking right-sized boxes to lower returns, happier unboxing videos, and simplified reverse logistics. Processed food, beverages, electrical appliances, and personal-care items together provide a steady baseline tonnage, though each vertical’s packaging spec is diverging based on sustainability pledges and automation compatibility.

Pharmaceutical shippers require temperature assurance, contamination barriers, and serial number integrity, pushing converters toward multi-layer corrugated solutions that pair phase-change packs with RFID-ready print zones. Industrial goods, automotive parts, and building materials still lean on heavy-duty pallet boxes, yet cyclical capital-goods cycles mean their growth fluctuates with macro investment trends. Altogether, the Asia-Pacific corrugated packaging market will see fulfillment centers overtake fresh produce as the prime innovation sandbox, forcing converters to master both rugged structural engineering and consumer-facing aesthetics within the same production run.

Geography Analysis

China retained 49.63% of the Asia-Pacific corrugated packaging market share in 2025, driven by 175 billion parcel movements that year. The June 2025 courier regulation mandating minimal packaging and the GB/T 6543-2025 structural standard are forcing converters to upgrade quality-control sensors and shift toward reusable strapping. Scale players such as Nine Dragons posted 225% profit spikes in the first half of fiscal 2026 by leveraging captive fiber and new 2 million tons Beihai capacity.[3]Nine Dragons Paper Holdings, “Interim Report FY 2026,” ndpaper.com

India, advancing at 6.15% CAGR, is benefiting from a USD 145 billion capex push and a dedicated MSME fund that reduces borrowing costs for corrugators investing in high-color digital lines. The September 2025 tightening of effluent norms, effective 2027, will raise water-treatment costs, accelerating consolidation in a sector where many small mills still run legacy boilers. Mature markets of Japan, South Korea, Australia, and New Zealand exhibit slower tonnage growth but higher revenue per box thanks to EPR mandates that elevate recycled-content documentation and barrier-coating certifications.

Oji Holdings’ JPY 16 billion (USD 150 million) liquid carton plant in Vietnam underscores a geographic pivot that enables Japanese firms to supply ASEAN growth corridors without incurring domestic energy premiums.The rest of Asia-Pacific, notably Vietnam, Indonesia, and Thailand, is absorbing manufacturing reroutes from China-plus-one strategies. APP Group’s 1.2 million tones Indonesian kraft expansion and Tetra Pak’s EUR 97 million (USD 103 million) Vietnam line increase reflect investor confidence in regional demand, although fragmented logistics and port congestion still inflate damage rates and buffer-stock levels.

Competitive Landscape

The Asia-Pacific corrugated packaging market remains moderately concentrated, with the top five groups holding a combined share of 35-40%. Vertical integration is the defining moat, buffering players from linerboard price spikes and securing fiber in an era of volatile recovered-paper flows. Nine Dragons, Lee and Man, and Smurfit WestRock each reported double-digit margin expansion in 2025 even as raw-material indices swung wildly, confirming the earnings leverage of captive mills and recycling networks.

Strategic thrusts center on bio-based barriers, high-speed digital printing, and cold-chain engineered formats. Panasonic Connect’s VIXELL reusable vacuum-insulated box, capable of -90 °C stability for 216 hours, exemplifies a niche where material innovation can command outsized premiums.[4]Panasonic Connect, “VIXELL Temperature-Controlled Box Specifications,” connect.panasonic.com Converters lacking scale are either courting acquisition or retreating to hyper-local service niches where speed trumps price. Smurfit WestRock’s acquisition of Cartomanabí in Ecuador, though outside Asia, signals a continuing appetite for bolt-ons that add regional converting volume feeding captive paper machines.

Labor scarcity rounds out the competitive chessboard, with the PMMI 2025 survey showing 95% of consumer-packaged-goods firms struggling to recruit skilled folding-gluer or corrugator operators. To counter wage inflation and retention risk, leading converters are deploying collaborative robots for palletizing, automated splicers for zero-speed roll changes, and cloud analytics that flag quality drifts before they trigger scrap. Smaller plants lacking capital for automation face rising downtime and higher defect rates, nudging them toward toll-conversion partnerships or outright sale. Over the medium term, competitive intensity will hinge less on geographic footprint and more on the ability to blend scale economics with digital agility.

Asia-Pacific Corrugated Packaging Industry Leaders

Nine Dragons Paper (Holdings) Limited

Oji Holdings Corporation

Rengo Co., Ltd.

Mondi plc

International Paper Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2026: Mondi completed 80% of its EUR 1.2 billion (USD 1.28 billion) mill and converting upgrade program.

- March 2026: Visy invested AUD 20 million (USD 13 million) in a Tasmania hub to serve produce and food processors with rapid-turn corrugated solutions.

- September 2025: Visy upgraded its Brisbane mill with AUD 30 million (USD 20 million) to boost recycled corrugated output.

- April 2025: Rengo took a 28.6% stake in Kinki Danboru to deepen its Japanese corrugated network.

Asia-Pacific Corrugated Packaging Market Report Scope

The Asia-Pacific Corrugated Packaging Market report encompasses a comprehensive analysis of fiber-based and polymer-based (PP) corrugated materials used for the containment, protection, and transport of goods across diverse industrial and retail sectors. The market refers to the industry that produces multi-layered boards, typically consisting of a fluted medium sandwiched between linerboards, designed to provide high strength-to-weight ratios and crush resistance for secondary and tertiary packaging.

The Asia-Pacific Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries), and Geography (China, India, Japan, South Korea, Australia and New Zealand, and Rest of Asia-Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| China |

| India |

| Japan |

| South Korea |

| Australia and New Zealand |

| Rest of Asia-Pacific |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries | |

| By Geography | China |

| India | |

| Japan | |

| South Korea | |

| Australia and New Zealand | |

| Rest of Asia-Pacific |

Key Questions Answered in the Report

How large will the Asia-Pacific demand for corrugated packaging become by 2031?

It is projected to reach USD 134.67 billion by 2031, reflecting a 4.17% CAGR from 2026.

Which country is growing fastest in regional corrugated consumption?

India leads with a projected 6.15% CAGR through 2031, driven by government capex, export incentives, and pharma manufacturing expansion.

What material trend is reshaping box specifications for food and pharma exports?

A dual track of recycled linerboard for cost-sensitive goods alongside rising virgin kraft uptake for certified food-contact and moisture-barrier applications.

How is e-commerce influencing corrugated design in Asia-Pacific?

Fulfillment centers are prioritizing right-sized, die-cut boxes and reusable strapping to cut cube utilization, boosting demand for digital printing and micro-flute profiles.

Why are integrated producers outperforming stand-alone converters?

Vertical control of fiber and energy inputs shields margins from raw-material volatility, enabling profit expansion even amid linerboard price swings.

What innovation could replace plastic liners in moisture-sensitive boxes?

Fungus-based hydrophobic coatings developed by University of Maine researchers offer comparable barrier performance while improving recyclability.

Page last updated on: