Market Overview

| Study Period | 2020 - 2031 |

|---|---|

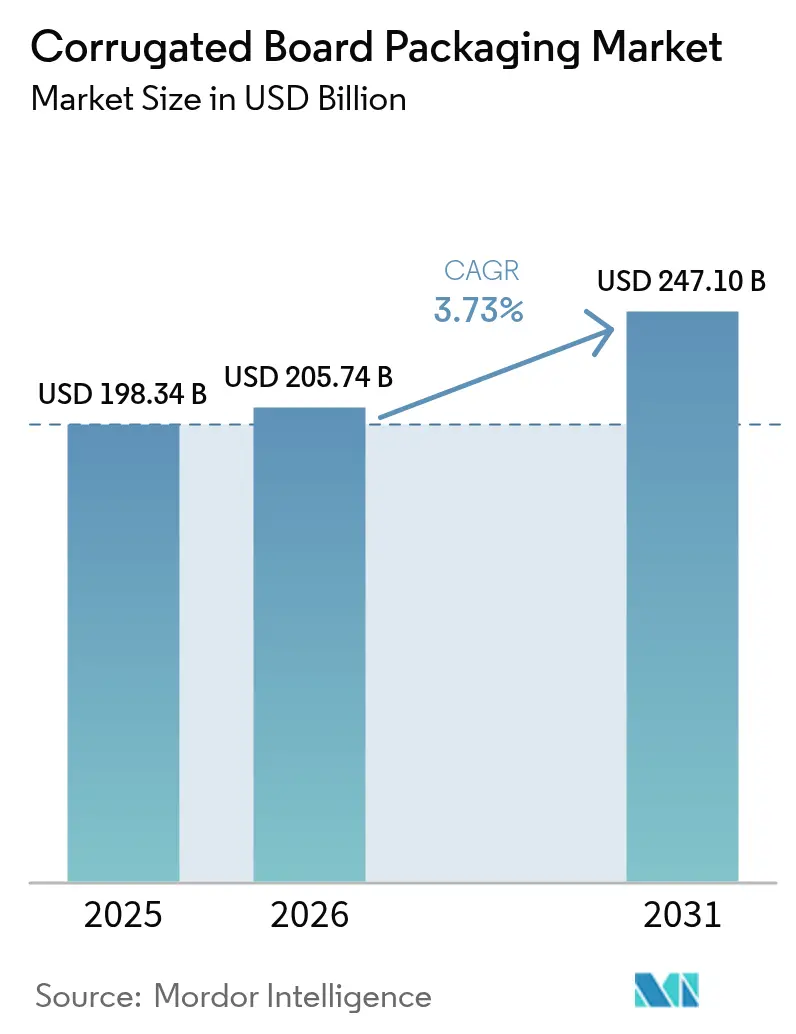

| Market Size (2026) | USD 205.74 Billion |

| Market Size (2031) | USD 247.1 Billion |

| Growth Rate (2026 - 2031) | 3.73% CAGR |

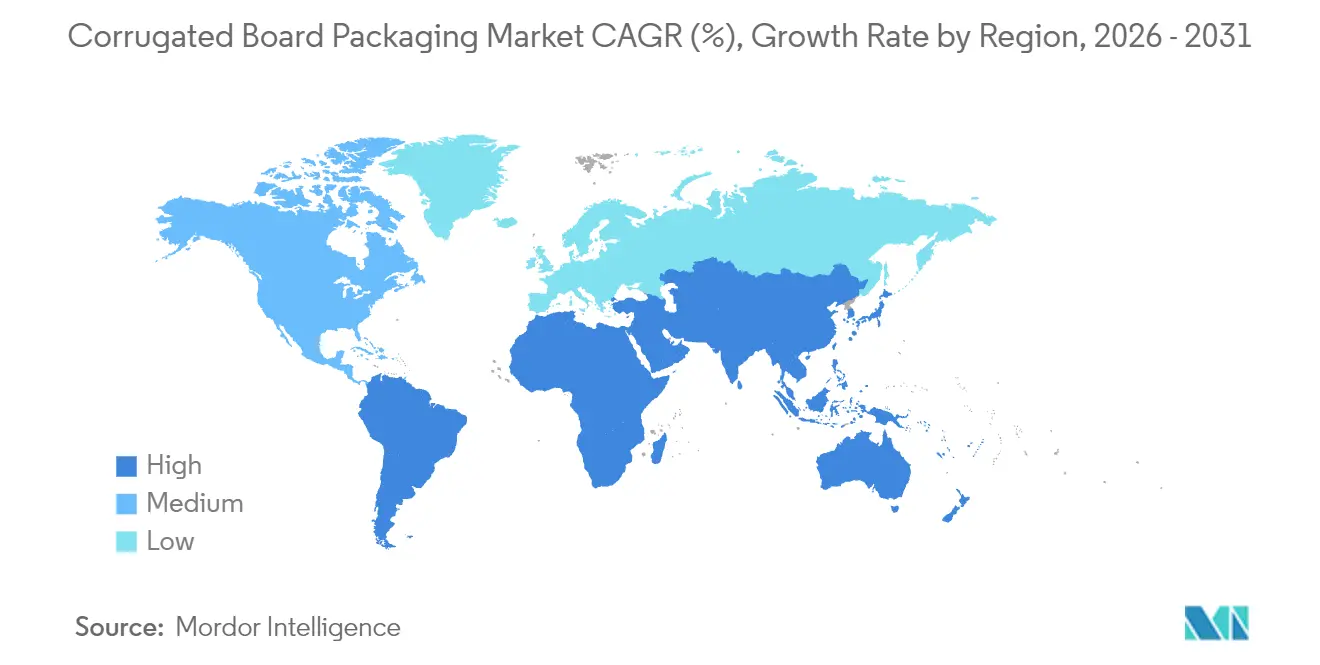

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

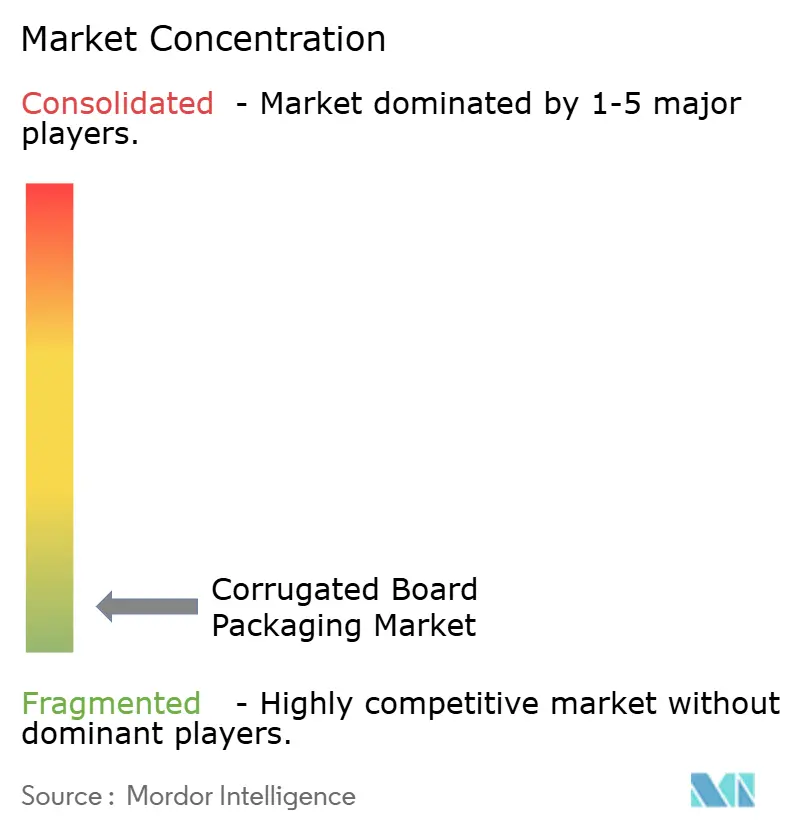

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Corrugated Board Packaging Market Analysis by Mordor Intelligence

The Corrugated Board Packaging Market size in 2026 is estimated at USD 205.74 billion, growing from 2025 value of USD 198.34 billion with 2031 projections showing USD 247.1 billion, growing at 3.73% CAGR over 2026-2031.

The measured expansion reflects policy-driven substitution of plastics, fast-growing e-commerce volumes, and rapid adoption of digital and AI manufacturing tools. Regulatory pressure, led by the European Union’s Packaging and Packaging Waste Regulation and five U.S. state Extended Producer Responsibility laws, is accelerating fiber demand as brand owners pivot toward readily recyclable formats. Supply-side tightness—caused by volatile old-corrugated-cardboard (OCC) prices and energy costs—supports pricing discipline, while downstream technology such as hybrid digital-flexo presses unlocks mass customization opportunities. Competitive advantage is shifting toward vertically integrated producers able to secure raw fiber, invest in energy-efficient mills, and deploy AI-enabled box-design optimization.

Key Report Takeaways

- By material type, recycled containerboard captured 55.05% of the corrugated board packaging market share in 2025; agricultural-waste fiber grades are expected to expand at a 6.54% CAGR to 2031.

- By box style, traditional slotted boxes held 32.05% share in 2025, whereas folder boxes are poised for 5.48% CAGR as e-commerce specifications evolve.

- By end-user industry, food applications dominated with 30.92% share of the corrugated board packaging market size in 2025, while e-commerce fulfillment is forecast to rise at an 8.12% CAGR to 2031.

- By board type, single-wall formats accounted for 65.05% share in 2025; double-wall boards are projected to post a 5.93% CAGR through 2031.

- By printing technology, flexography retained 58.10% share in 2025, but digital presses are advancing at a 5.12% CAGR on the back of short-run customization demand.

- By geography, Asia-Pacific led with 39.85% revenue share of the corrugated board packaging market in 2025, while South America is projected to register the fastest 7.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Corrugated Board Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Eco-friendly material mandates | +1.2% | Global, with EU and North America leading | Medium term (2-4 years) |

| E-commerce parcel explosion | +1.8% | Global, with Asia-Pacific and North America core | Short term (≤ 2 years) |

| Advances in digital and flexo hybrid presses | +0.8% | North America and EU, spill-over to Asia-Pacific | Medium term (2-4 years) |

| Light-weight containerboard economics | +0.6% | Global manufacturing regions | Long term (≥ 4 years) |

| AI-driven box-design optimisation | +0.4% | Asia-Pacific core, spill-over to North America | Medium term (2-4 years) |

| Agricultural-waste fibre pulping | +0.5% | Global, with early gains in Europe and Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Eco-friendly material mandates drive fiber substitution

New recyclability rules are tilting packaging material choices toward fiber. The EU requirement that all packaging be recyclable by 2030, alongside minimum recycled-content quotas for plastics, has made corrugated the low-risk compliance option. [1]European Parliament, “Packaging and packaging waste,” europarl.europa.eu Five U.S. states impose fee scales that reward recyclable substrates, creating cost advantages of up to 15% versus plastic formats. [2]International Paper, “The Landscape of U.S. State EPR Packaging Laws,” internationalpaper.com Brands are accelerating specification changes because plastic recycling infrastructure lag times exceed the 2030 deadline. Corrugated’s 71-76% recovery rate simplifies audit trails, supports corporate ESG pledges, and limits penalty exposure. Mill operators report order lead-times for fiber-based SKUs shortening by two weeks as converters re-tool lines to meet retailer scorecard requirements.

E-commerce parcel explosion reshapes packaging specifications

Global e-commerce shipping volumes grew from 220 billion parcels in 2024 to a projected 340 billion by 2029, elevating functional priorities such as drop-test durability and dimensional-weight efficiency. Double-wall and micro-flute boards now constitute over one-quarter of parcels shipped via major integrators. Equipment suppliers respond with on-demand boxmaking systems that trim labor by 40% while reducing void-fill needs, thereby cutting per-order materials cost by 15%. Subscription-commerce operators are specifying printable interiors for brand storytelling, which further boosts the loading of digitally printed graphics inside the shipping container. These shifts cement corrugated’s role as both a transport medium and a marketing surface.

Advances in digital and flexo hybrid presses enable mass customization

Hybrid lines that combine CMYK digital engines with high-speed flexo stations cut changeover times to under five minutes and allow run-lengths of 100 boxes without cost penalties. Ink suppliers have introduced water-based formulations compliant with food-contact regulations, enabling direct plate-to-box printing for grocery customers. Converters gain the agility to service promotional campaigns and seasonal SKUs with zero inventory of pre-printed sheets. Wider adoption is expected as capex per hybrid line falls below USD 4 million, 30% lower than in 2023. Integration of AI color-management suites maintains delta-E tolerances under 2.0, ensuring graphic consistency across plants.

AI-driven box-design optimisation reduces material consumption

Machine-learning algorithms simulate compression performance across flute patterns and stacking heights, allowing converters to shave 8-10% board weight without compromising edge-crush strength. Vision systems spot score-line defects at speeds of 250 m min-1, curbing scrap rates. Predictive maintenance modules cut unplanned downtime by 12% and extend corrugator roll life. Early adopters report annual savings exceeding USD 3 million on medium-sized production footprints while improving recycling compatibility due to reduced mixed-material laminations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Reusable plastics and RPCs adoption | -0.8% | North America and EU, with retail sector focus | Short term (≤ 2 years) |

| Volatile OCC and energy prices | -1.1% | Global manufacturing regions | Short term (≤ 2 years) |

| Corrugator electricity-intensity caps | -0.3% | EU and regulated markets | Medium term (2-4 years) |

| Industrial-water withdrawal limits at mills | -0.4% | Water-stressed regions globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Reusable plastics and RPCs adoption challenges single-use demand

Retailers expand returnable-plastic-container (RPC) pools for produce and meat because they cut shrinkage and reduce labor at the store level. France, Germany, and South Korea have introduced reuse quotas or deposit schemes that favor durable crates over single-use corrugated. Automated wash-back networks lower per-trip RPC cost below USD 0.25 when cycle counts exceed 25, undercutting single-use units for predictable fresh-food supply chains. Corrugated converts defend share using high-barrier moisture-resistant coatings and tamper-evident locking tabs, but face margin squeeze in high-turnover channels.

Volatile OCC and energy prices compress manufacturing margins

OCC prices rose USD 7.10 per ton y-o-y in January 2025 amid tightening recovered-paper supply linked to logistics chokepoints and competing demand from Asian mills. [3]Editorial Team, “Old Corrugated Cardboard Market increases $0.40 USD/TON,” RecycleNet, recyclenet.com Spot electricity prices in Europe exceeded EUR 150 MWh during winter 2024–25, inflating corrugator operating costs by up to USD 28 per short ton. Mills is unable to pass through surcharges, reporting EBITDA margin contraction of 180 basis points. Larger integrated groups counter volatility through captive power projects and fiber procurement hedges, widening the cost gap over stand-alone sheet feeders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled fiber retains the lead but agri-waste trials accelerate

Recycled grades commanded 55.05% of the corrugated board packaging market share in 2025, buoyed by mature collection networks and favorable EPR fee structures. The segment is forecast to grow at 4.56% CAGR as brand owners raise post-consumer-content thresholds. Virgin Kraft liner retains relevance for heavy-duty export cartons, but its volume share continues to erode. Wheat-straw, rice-husk, and tomato-stem pulps are entering commercial pilots; laboratory work shows tensile strength gains of up to 25% over conventional recycled pulp. Investment in regional decentralized pulping units is crucial to control raw-material moisture and logistics costs. Successful scale-up would temper OCC price cycles and diversify fiber sourcing, strengthening supply-chain resilience.

Agricultural-waste pulps also deliver environmental gains, trimming carbon intensity by 20-25% relative to virgin wood fiber because they bypass forest-harvesting steps. Early adopters in Italy and India are integrating agri-waste at 15-20% blend ratios without modifying corrugator settings. Though certification frameworks for food-contact compliance remain nascent, producers expect regulatory alignment by 2027. These innovations signal that the corrugated board packaging market will shift from a binary virgin-versus-recycled narrative to a broader multi-fiber portfolio, reinforcing its adaptability to regional resource constraints.

By Box Style/Construction: Folder boxes outpace slotted standards

Traditional regular slotted containers (RSCs) held a 32.05% share in 2025, but folder-type formats are projected to increase at a 5.48% CAGR through 2031, propelled by e-commerce brand owners seeking quick-assembly designs that enhance the unboxing experience. Automated erecting equipment processes folder styles at 35 boxes min-1, 40% faster than manual RSC lines, saving fulfillment centers significant labor. In the corrugated board packaging market size context, this shift translates into incremental revenue of USD 8.9 billion between 2026 and 2031.

Slotted boxes retain cost advantages where cube efficiency and palletization are paramount, such as industrial spare parts distribution. Telescope and rigid-set boxes occupy premium niches, including luxury electronics, where visual aesthetics and crush prevention outweigh material cost. Digital print-ready folder constructions increasingly integrate tear-strips and returnable seals, aligning with omnichannel logistics flows. The evolving construction landscape illustrates how performance criteria, automation capability, and consumer engagement jointly influence specification trends within the corrugated board packaging market.

By End-User Industry: E-commerce narrows the gap with food leadership

Food packaging represented 30.92% of the corrugated board packaging market size in 2025, underpinned by moisture-resistant coatings that satisfy FDA contact norms and maintain produce freshness. Growth stabilizes at 3.12% CAGR as mature grocery channels plateau. Conversely, e-commerce and fulfillment applications are forecast to expand at 8.12% CAGR, adding USD 13.4 billion in incremental value by 2031. Subscription kits, direct-to-consumer fashion, and same-day electronics deliveries all demand right-sized, protective, and brandable boxes.

Healthcare shipments require serialization windows and tamper-evident tapes, with stringent validation driving premium price points. Industrial users are pivoting from wooden crates to triple-wall corrugated alternatives, attracted by 30% weight savings that lower freight costs. These dynamics confirm that end-use diversification reinforces structural growth opportunities for the corrugated board packaging market.

By Board Type: Double wall captures share through performance economics

Single-wall sheets remained dominant at 65.05% share in 2025, yet double-wall options are set to grow at 5.93% CAGR as parcel services tighten drop-test standards. Incorporating BC or EB flute combinations boosts edge-crush strength by up to 45% while preserving printable surfaces. The corrugated board packaging market size for double-wall constructions is predicted to exceed USD 79.6 billion by 2031.

Triple-wall grades compete with plywood for heavy industrial motors and batteries. Meanwhile, micro-flute variants encroach on folding-carton territory, offering superior rig stiffness and e-commerce-friendly graphics. Producers investing in quick-flute-change corrugators can switch from B to E flute in under 10 minutes, tailoring board profiles to order mix and minimizing work-in-process inventory. Such flexibility cements corrugated’s role as a multifunctional substrate.

By Printing Technology: Digital accelerates amid flexo dominance

Flexography maintained 58.10% share in 2025 because of its unmatched throughput on long runs. Even so, digital presses are slated for a 5.12% CAGR through 2031, raising their revenue contribution to 15.10% of the corrugated board packaging market. Lower ink-coverage costs, on-the-fly artwork changes, and reduced plate inventories underpin this shift.

Hybrid press installations grew 22% in 2024, blending flexo base colors with digital variable data to serve personalized marketing campaigns. Food-contact compliant digital inks clear regulatory hurdles and open new growth in frozen and chilled segments. Screen and litho remain niche for metallic finishes and ultra-high-resolution photographic work, respectively. Together, these technology choices reflect an industry migrating from mass production toward mass customization at scale.

Geography Analysis

Asia-Pacific accounted for 39.85% of global corrugated board packaging market revenue in 2025 and continues to leverage manufacturing integration and cost-effective fiber sourcing. Nine Dragons Paper expanded annual capacity to 25.37 million tonnes, underpinning the region’s supply dominance. China’s stimulus measures stimulate domestic consumption, yet export-oriented plants in Vietnam and Malaysia now serve Belt-and-Road trade corridors. Investment in waste-paper-import quotas also encourages local agri-waste pulping pilots, mitigating OCC dependency.

South America represents the fastest-growing corridor, with a 7.05% CAGR projected to 2031. Brazil’s containerboard shipments increased despite macro headwinds as producers realigned mills for export markets. Klabin’s new Paraná facility exemplifies forward-capacity bets, while Chilean and Colombian converters invest in folder-gluer automation to meet e-commerce box styles. Fiber self-sufficiency, anchored in abundant sugar-cane bagasse and eucalyptus plantations, positions the region as a future agri-waste supply hub.

North America and Europe exhibit steady mid-single-digit growth anchored in regulatory compliance and value-added innovation. The EU recyclability mandate that took effect in 2025 has already shifted 6% of plastic transit-packaging volume into corrugated. International Paper’s USD 7.2 billion buyout of DS Smith extends its sustainable-packaging footprint across both continents and is expected to unlock USD 600-700 million in synergy by 2027. European mill upgrades prioritize energy conservation, with Stora Enso’s Oulu line claiming 20% lower greenhouse-gas intensity than legacy paper machines. In the United States, digital press penetration exceeds 18% of installed corrugated print capacity, accelerating mass customization in consumer packaged goods.

Competitive Landscape

The corrugated board packaging market features fragmentation. International Paper’s acquisition of DS Smith and Smurfit WestRock’s formation elevated combined capacity, yet regional champions such as Nine Dragons and Lee & Man preserve share through captive fiber loops and lower delivered-cost positions. Vertical integration across pulp, paper, and converting lines shields large players from OCC volatility and positions them to comply with tightening emission rules at lower marginal cost.

Technology adoption has become a differentiator more than scale alone. Smurfit WestRock’s 100% recyclable paper pallet wrap replaces polyethylene stretch film and cuts customer scope-3 emissions, illustrating how product innovation feeds premium-price segments. Midland Paper Packaging leverages AI-guided optical inspection to reduce trim waste, illustrating competitive gains for mid-tier converters agile enough to pilot new tools. Agricultural-waste fiber processing still favors nimble regional mills, although international groups have started strategic joint ventures to secure supply.

Price competition remains rational because energy and fiber shortages favor value-added contracts with pass-through clauses. Brand owners increasingly award multi-year agreements based on recyclability metrics and carbon-footprint dashboards, raising the bar for participants lacking in-house LCA capabilities. M&A activity is expected to continue as producers seek geographic diversification and technology portfolios that de-risk compliance exposures.

Corrugated Board Packaging Industry Leaders

International Paper Company

Mondi Group

Smurfit WestRock

Sealed Air Corporation

Nine Dragons Paper (Holdings) Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Stora Enso completed the EUR 1 billion conversion of its Oulu paper machine into a 750,000-ton-capacity folding box board and coated unbleached kraft line.

- February 2025: International Paper finalized the USD 7.2 billion purchase of DS Smith, creating a sustainable-packaging leader with operations in 30 countries.

- January 2025: The European Union’s Packaging and Packaging Waste Regulation entered into force, mandating recyclability for all packaging by 2030.

- January 2025: Smurfit WestRock launched 100% recyclable Nertop Stretch Kraft paper pallet wrap at its Nervion mill in Spain.

Global Corrugated Board Packaging Market Report Scope

Corrugated board packaging offers a versatile and cost-efficient method of protecting, preserving, and transporting various products. Its attributes, such as lightweight, biodegradability, and recyclability, have made it an integral component in the packaging industry.

Corrugated Board Packaging Market is Segmented by End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Personal and Household Care, and E-Commerce) and by Geography (North America (United States, and Canada), Europe (United Kingdom, Germany, France, Italy, Spain, Poland, and Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Indonesia, Thailand, and Rest of Asia Pacific), Latin America (Brazil, Argentina, Mexico, and Rest of Latin America), and Middle East and Africa (United Arab Emirates, Saudi Arabia, South Africa, and Rest of Middle East and Africa)). The Market Sizes and Forecasts are Provided in Terms of Value in USD for all the Above Segments.

By Material Type

| Virgin Containerboard |

| Recycled Containerboard |

By Box Style / Construction

| Slotted Boxes |

| Telescope Boxes |

| Rigid Boxes |

| Folder Boxes |

By End-User Industry

| Food | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Personal and Household Care | |

| E-commerce and Fulfilment | |

| Healthcare and Pharmaceuticals | |

| Electrical and Electronics | |

| Industrial | |

| Other End-user Industry |

By Board Type

| Single Wall |

| Double Wall |

| Triple Wall |

| Micro-flute |

By Printing Technology

| Flexography |

| Digital |

| Lithography |

| Screen |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Netherlands | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material Type | Virgin Containerboard | ||

| Recycled Containerboard | |||

| By Box Style / Construction | Slotted Boxes | ||

| Telescope Boxes | |||

| Rigid Boxes | |||

| Folder Boxes | |||

| By End-User Industry | Food | Processed Foods | |

| Fresh Food and Produce | |||

| Beverages | |||

| Personal and Household Care | |||

| E-commerce and Fulfilment | |||

| Healthcare and Pharmaceuticals | |||

| Electrical and Electronics | |||

| Industrial | |||

| Other End-user Industry | |||

| By Board Type | Single Wall | ||

| Double Wall | |||

| Triple Wall | |||

| Micro-flute | |||

| By Printing Technology | Flexography | ||

| Digital | |||

| Lithography | |||

| Screen | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Netherlands | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Singapore | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

How large is the corrugated board packaging market in 2026?

It is valued at USD 205.74 billion and is forecast to reach USD 247.1 billion by 2031 at a 3.73% CAGR.

Which region leads global corrugated board packaging revenues?

Asia-Pacific holds the largest share at 39.85%, supported by substantial containerboard capacity and e-commerce logistics growth.

What is driving double-wall board adoption?

Rising parcel-drop durability standards and automated warehouse handling needs are boosting double-wall demand, which is projected to grow at 5.93% CAGR.

How are regulations influencing material choices?

EU and U.S. recyclability mandates raise compliance costs for plastics, prompting brand owners to shift toward fiber-based corrugated formats.

Which printing technology is growing fastest?

Digital and hybrid presses are expanding at 5.12% CAGR because they enable cost-effective short runs and mass customization for online retail.

Page last updated on: