Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

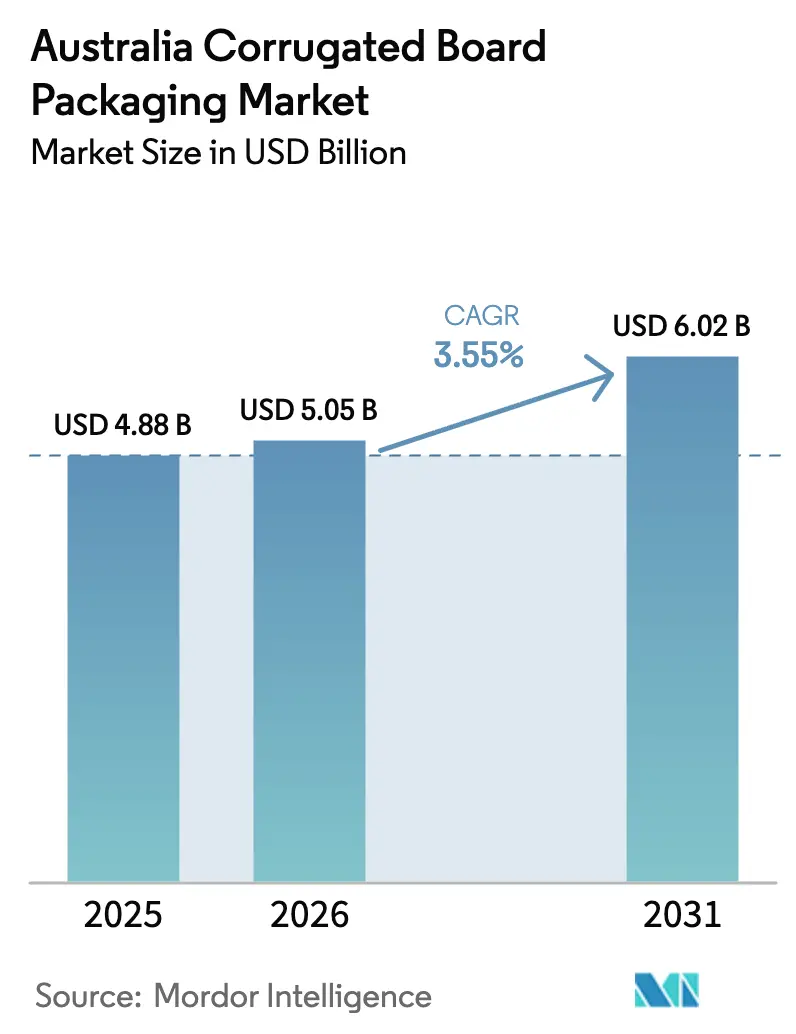

| Base Year Market Size (2025) | USD 4.88 Billion |

| Market Size (2026) | USD 5.05 Billion |

| Market Size (2031) | USD 6.02 Billion |

| Growth Rate (2026 - 2031) | 3.55% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Corrugated Board Packaging Market Analysis by Mordor Intelligence

The Australia corrugated board packaging market size is expected to grow from USD 4.88 billion in 2025 to USD 5.05 billion in 2026 and is forecast to reach USD 6.02 billion by 2031 at 3.55% CAGR over 2026-2031. Expansion is underpinned by e-commerce parcel growth, state-backed recycling modernization, and manufacturers’ pivot toward box-on-demand systems that cut inventory waste while boosting customization. Domestic food and beverage demand ensures baseline volume stability even as private-label strategies raise the bar for shelf differentiation. Export-oriented fresh-produce and wine sectors further diversify volume streams, buffering the industry from cyclical swings in household consumption. At the same time, automation and digital printing are lowering minimum economic run lengths, enabling smaller converters to compete for niche accounts traditionally locked up by large integrated producers. Collectively, these structural shifts position the sector as a regional test bed for circular-economy innovation and technology-enabled fulfillment models.

Key Report Takeaways

- By end-user, food and beverage commanded 34.62% of the Australian corrugated board packaging market share in 2025, while e-commerce is projected to expand at a 5.05% CAGR through 2031.

- By board type, single-wall products represented 38.74% of the Australian corrugated board packaging market size in 2025, whereas triple-wall grades are set to grow at a 4.18% CAGR to 2031.

- By flute profile, C-flute led with 31.93% of the Australian corrugated board packaging market size in 2025, while microflute formats are advancing at a 4.71% CAGR through 2031.

- By printing technology, flexographic presses accounted for 28.08% of the Australian corrugated board packaging market size in 2025; digital printing is the fastest mover with a 5.78% CAGR projected to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Australia Corrugated Board Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce parcel volume boom | +1.2% | National, concentrated in Sydney, Melbourne, Brisbane metro areas | Short term (≤ 2 years) |

| Retail grocery private-label expansion | +0.8% | National, with stronger impact in regional markets | Medium term (2-4 years) |

| State recycling-modernisation funding | +0.6% | Queensland, NSW, Victoria, Western Australia | Medium term (2-4 years) |

| Warehouse automation and box-on-demand uptake | +0.4% | National, early adoption in major distribution hubs | Long term (≥ 4 years) |

| Cold-chain fresh-produce exports | +0.3% | Export-focused regions: Tasmania, South Australia, Western Australia | Medium term (2-4 years) |

| AI-enabled fit-to-product packaging lines | +0.2% | National, concentrated in major manufacturing centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce Parcel Volume Boom

Record parcel dispatches are forcing converters to engineer boxes that survive automated sortation, multi-handoff last-mile routes, and customer-friendly returns processes.[1]Australian Bureau of Statistics, “Retail Trade, Australia,” abs.gov.au Dimensional-weight pricing from Australia Post rewards right-sized packaging, accelerating adoption of precision-cut designs that minimize void fill. Triple-wall board, though a smaller slice of consumption, is growing as online merchants pay a premium for enhanced crush resistance. The boom also stimulates demand for track-and-trace graphics printed in small batches, a sweet spot for digital presses. Because parcel hubs sit near the nation’s three largest metros, converters with decentralized plants cut delivery lead times and win service-level contracts that traditional, centrally located mills struggle to match.

Retail Grocery Private-Label Expansion

Supermarket chains are leaning on private-label lines to defend margins, and packaging has become a frontline branding tool. Retailers now commission short-run holiday themes and region-specific SKUs that justify digital printing’s higher per-unit cost while slashing plate-change downtime. Rising input expenses-corrugated costs have climbed roughly 30% since 2022-press food manufacturers to rethink pack formats that optimize both shelf presence and pallet density. Converters offering design services help grocers reconcile branding ambitions with APCO recyclability rules, creating fee-based advisory revenue beyond the blank-box sale. This collaboration is particularly pronounced in produce crates, where shelf-life extenders such as breathable coatings bolster fresh quality.

State Recycling-Modernization Funding

Aggregate state spending that tops USD 100 million is building fiber-recovery hubs adjacent to major consuming regions, tightening the supply loop for recycled liner. Guaranteed bale offtake gives mills predictable raw-material input, reducing exposure to kraft-liner imports and volatile currency swings. Queensland’s ReMiQ program, for instance, funds contamination-detection sensors that boost recovered-fiber yield, sharpening mill economics without federal subsidies. Plants located within trucking distance of these hubs lock in freight savings and preferential access to high-grade secondary fiber, underscoring how policy is shaping competitive geography.

Warehouse Automation and Box-on-Demand Uptake

In-line pack stations that generate custom boxes at the pack-out lane cut SKU-specific inventory and free up warehouse space. Visy’s purchase of Packsize embeds this capability within an integrated containerboard–converting value chain, giving the market leader a solution few rivals can replicate. The equipment also overprints variable data such as last-mile routing codes, marrying structural and graphic customization in a single pass. Although capital-heavy, early adopters report measurable cuts in corrugated scrap, an environmental win that resonates with retailers pursuing APCO’s 100% recyclable goal. Smaller converters face a build-or-partner dilemma as the technology reshapes service expectations.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Kraft liner pulp price volatility | -0.9% | National, with higher impact on import-dependent manufacturers | Short term (≤ 2 years) |

| Rail-freight capacity bottlenecks | -0.5% | Interstate routes, particularly Melbourne-Sydney-Brisbane corridor | Medium term (2-4 years) |

| Skilled-labour shortages in converting | -0.4% | National, concentrated in major manufacturing centers | Medium term (2-4 years) |

| Carbon-border adjustment risk on imports (under-reported) | -0.3% | National, affecting import-dependent manufacturers and customers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Kraft Liner Pulp Price Volatility

Limited domestic pulp capacity exposes converters to global price swings amplified by exchange-rate shifts. Spikes during 2024 forced several independents to renegotiate quarterly supply or carry higher inventories financed at rising interest rates. Larger integrated producers hedge with longer-term fiber contracts, widening cost gaps that manifest in bid rounds. Volatility also complicates fixed-price commitments sought by big-box retailers and beverage fillers, prompting more frequent renegotiations and eroding trust in long-term frameworks.

Rail-Freight Capacity Bottlenecks

Australia’s east-coast intermodal network operates near saturation, and any disruption reverberates across raw-material inflow and finished-box deliveries.[2]Department of Infrastructure, Transport and Regional Development, “Freight and Supply Chain Priorities,” infrastructure.gov.au When wagons are unavailable, mills resort to truckload moves that inflate per-kilometer costs and carbon emissions-contradicting APCO targets. Converters located outside congestion pinch-points, such as regional NSW hubs, increasingly market supply-chain resilience as a differentiator, re-routing sheet stock by road only for the “last 100 kilometers.”

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: E-commerce Drives Packaging Innovation

E-commerce demand is reshaping the Australia corrugated board packaging market, even though food and beverage led 2024 volume. Single-parcel shipments require impact-resistant designs, multi-depth formats, and readable codes for automated sorters. Online electronics sales layer in electrostatic discharge protection, while cosmetics brands pay premiums for unboxing aesthetics that reinforce social-media marketing. Food processors, hit by a 30% rise in packaging costs since 2022, now co-develop modular inserts that stabilize products across multiple SKU sizes without tooling changes.

As returns policies become a competitive lever, reverse-logistics-friendly boxes equipped with easy-tear strips win retailer favor. Meanwhile, the Australia corrugated board packaging market size tied to export-oriented fresh produce grows as growers trial water-resistant coatings compliant with Asian phytosanitary rules. Collectively, these shifts divert capital toward R&D rather than sheer capacity, signaling a move from commodity supply to solution-based selling.

By Board Type: Single-Wall Dominance Faces Triple-Wall Growth

Single-wall still accounts for the plurality of tonnage thanks to its cost-weight ratio in grocery and display units. Yet the tolerance for transit damage in direct-to-consumer channels is lower, nudging some buyers toward triple-wall crates that replace wood in bulky goods. Weight savings reduce airfreight surcharges on premium fruit exports, providing a margin offset against higher board cost. Manufacturers capitalize by offering hybrid double-wall with reinforced edge crush, balancing protection and pricing.

Investments in lighter-basis paper grades also help defend single-wall’s share, enabling downgauging without compromising stacking strength. APCO recyclability mandates favor corrugated over composite substrates, keeping the Australia corrugated board packaging market size for single-wall relatively stable even as new niches emerge for heavier construction.

By Flute Type: C-Flute Leadership Challenged by Microflute Innovation

C-flute’s middle-ground performance profile secures its dominance in standard shippers, but evolving shelf-ready designs turn attention to thinner microflutes that accept high-resolution graphics. Retailers appreciate the space savings on the shelf while maintaining enough compressive strength for mixed logistics. Microflute paired with digital print bridges the gap between corrugated and folding cartons, opening doorways for premium confectionery packs seeking plastic alternatives.

Temperature-controlled solutions such as DS Smith’s TailorTemp illustrate how flute engineering underwrites functional innovations by embedding insulation cavities without exotic foams. Although microflute material costs remain elevated, scale and print-on-demand economics are narrowing the gap, hinting at broader substitution ahead.

By Printing Technology: Digital Transformation Accelerates

Flexography’s entrenched network and economics keep it in pole position for high-volume FMCG work. Nonetheless, digital’s annualized growth eclipses any other process as converters chase on-demand color changes, serial coding, and versioned graphics. Opal Fibre Packaging’s 2024 investment demonstrates capacity shifting toward single-pass inkjet that eliminates plates and formulation wash-ups.

Hybrid workflows-digital for variable data atop pre-printed flexo bases-are meanwhile squeezing litho-lamination in mid-volume runs. Capital productivity metrics support the thesis: digital line changeovers measured in minutes unlock profitability even at a few hundred boxes per design, aligning perfectly with proliferating private-label SKUs.

Geography Analysis

Population-dense New South Wales and Victoria dominate consumption and house most integrated mills. Sydney and Melbourne also anchor e-commerce fulfillment zones, making rapid-response converting capacity indispensable. Queensland leverages USD 55 million in recycling grants to foster a closed-loop fiber supply near produce-export corridors, attracting box plants that cut inbound raw-material mileage. Western Australia’s mineral exports and agricultural bulk drive heavy-duty corrugated demand; geographic isolation incentivizes local factories that sidestep costly cross-continent truck legs.

South Australia’s wine route pushes specialty moisture-resistant liners that stabilize humidity during barrel-aging transit. Tasmania, while small in population, achieves outsized relevance through high-value cherry shipments needing vented, temperature-stable packs that secure premium shelf prices in Asia. Northern Territory’s industrial base is modest, yet mining projects periodically spike bulk packaging orders, rewarding converters with flexible capacity.

Rail-freight pinch-points along the east-coast spine steer some investment toward satellite converting in regional NSW, reducing reliance on congested intermodal links. These distributed footprints enable next-day delivery of sheets to independent box plants, a service differentiator that entrenched metro behemoths struggle to match without duplicating assets.

Competitive Landscape

The market is moderately concentrated: Visy, Opal, Pratt Industries, and global incumbents such as DS Smith hold critical mass in linerboard supply, converting capacity, and recovered-fiber collection. Vertical integration from paper mill to recycling bins fortifies procurement advantages, particularly during kraft-liner spikes. Visy’s Packsize purchase embeds proprietary on-demand technology inside its network, while Pratt’s USD 5 billion expansion earmarks multi-wall capacity that could tilt future market share. Opal’s workforce realignment underscores cost-discipline imperatives as digital presses displace labor-intensive set-ups.

Niche disruptors deploy AI-driven cut-to-order lines, targeting mid-market e-commerce businesses frustrated by rigid minimum orders. Patent filings on water-resistant barrier coatings suggest new battlegrounds in produce export packaging. Sustainable substrate partnerships-Amcor with Kolon Industries on chemically recycled PET, for example-signal that corrugated producers are hedging with adjacent material R&D, broadening customer wallet share.

The APCO compliance regime raises the table stakes: converters adept at documentation and traceability secure retailer contracts wary of reputational risk. Automation investment cycles will likely widen the performance gulf between technology leaders and laggards, driving selective consolidation but stopping short of a monopoly due to diverse regional demand nodes.

Australia Corrugated Board Packaging Industry Leaders

Visy Industries Holdings Pty Ltd

Opal Fibre Packaging (Paper Australia Pty Ltd)

Oji Fibre Solutions (Australia) Pty Ltd

Amcor plc

Orora Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Pratt Industries confirmed an AUD 5 billion domestic investment program aimed at new containerboard capacity and box plants, heralding a supply-side step-change.

- March 2025: James Hardie moved to acquire AZEK for USD 8.75 billion, illustrating cross-material diversification that could shift construction-sector substrate demand.

- January 2025: DS Smith introduced TailorTemp, a fully recyclable corrugated thermal shipper targeting pharmaceutical cold-chain lanes.

- November 2024: mcor and Kolon Industries partnered to scale chemically recycled PET and bio-based polyethylene furanoate, expanding sustainable substrate options.

Australia Corrugated Board Packaging Market Report Scope

Corrugated board packaging offers a versatile and cost-efficient method to protect, preserve, and transport various products. The corrugated board's attributes, such as lightweight, biodegradability, and recyclability, have made it an integral component in the packaging industry. This type of packaging is used across various end-user industries, such as Food (Processed & Fresh Food), beverages, Personal & Household Care, E-commerce, Manufacturing & Automotive and Other End-user Verticals (Healthcare, Electrical & Electronics, Ceramic & Glass, etc.). Further the study encompasses the impct od covid-19 on the Australia Corrgated Baord Packaging Market,

By End-User Industry

| Food | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| E-commerce | |

| Electrical and Electronics | |

| Personal Care and Cosmetics | |

| Other End-User Industries |

By Board Type

| Single Face |

| Single Wall |

| Double Wall |

| Triple Wall |

By Flute Type

| A-Flute |

| B-Flute |

| C-Flute |

| E-Flute |

| F-Flute and Micro-Flutes |

By Printing Technology

| Flexographic |

| Digital |

| Litho-lamination |

| Other Printing Technologies |

| By End-User Industry | Food | Processed Foods |

| Fresh Food and Produce | ||

| Beverages | ||

| E-commerce | ||

| Electrical and Electronics | ||

| Personal Care and Cosmetics | ||

| Other End-User Industries | ||

| By Board Type | Single Face | |

| Single Wall | ||

| Double Wall | ||

| Triple Wall | ||

| By Flute Type | A-Flute | |

| B-Flute | ||

| C-Flute | ||

| E-Flute | ||

| F-Flute and Micro-Flutes | ||

| By Printing Technology | Flexographic | |

| Digital | ||

| Litho-lamination | ||

| Other Printing Technologies |

Key Questions Answered in the Report

What is the current value of the Australia corrugated board packaging market?

It is valued at USD 5.05 billion in 2026, with a projection to reach USD 6.02 billion by 2031.

How fast is e-commerce driving corrugated demand in Australia?

The e-commerce segment is growing at a 5.05% CAGR over 2026-2031, surpassing all other end-use categories.

Which board type is gaining the most momentum?

Triple-wall grades are forecast to expand at a 4.18% CAGR over 2026-2031, fueled by heavy-duty export and bulky e-commerce shipments.

Why are microflutes important for retail packaging?

They combine space-saving thinness with high-resolution print compatibility, enhancing shelf appeal without sacrificing protection.

How will state recycling funding affect supply security?

Investments exceeding USD 100 million are creating regional fiber-recovery hubs, reducing raw-material volatility for local mills.

What technologies are reshaping the competitive landscape?

Digital printing and box-on-demand automation allow precise, short-run production, giving early adopters a service advantage.

Page last updated on: