Qatar Corrugated Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

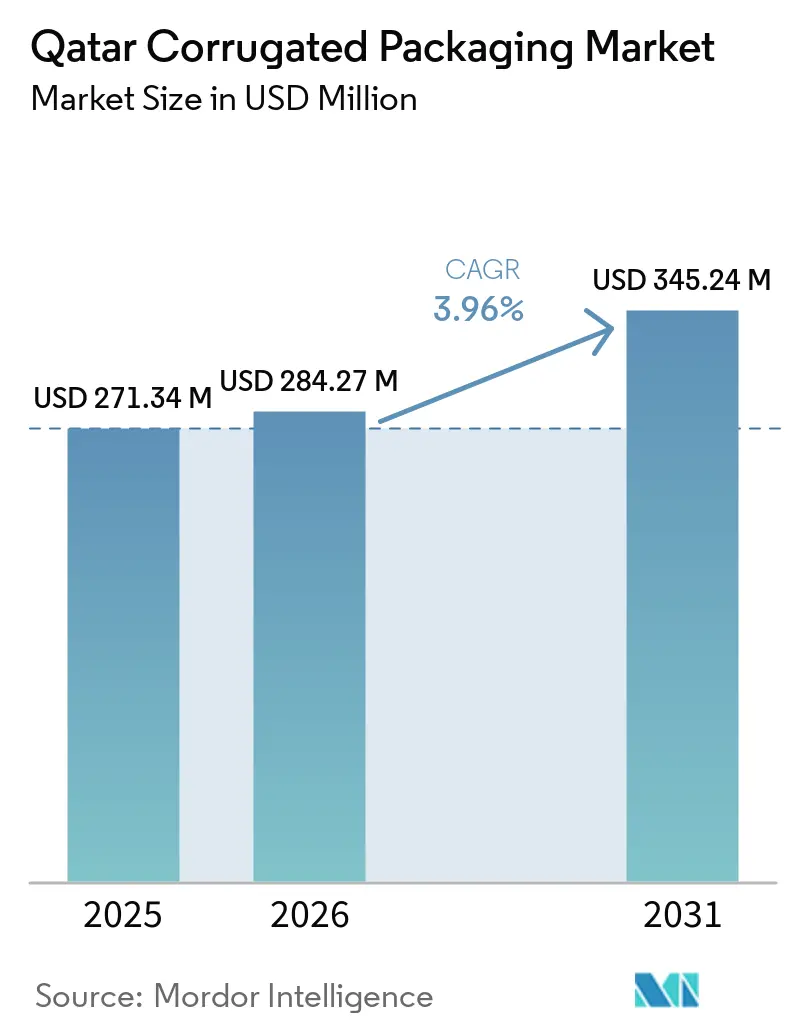

| Base Year Market Size (2025) | USD 271.34 Million |

| Market Size (2026) | USD 284.27 Million |

| Market Size (2031) | USD 345.24 Million |

| Growth Rate (2026 - 2031) | 3.96% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Qatar Corrugated Packaging Market Analysis by Mordor Intelligence

The Qatar Corrugated Packaging Market size is expected to increase from USD 271.34 million in 2025 to USD 284.27 million in 2026 and reach USD 345.24 million by 2031, growing at a CAGR of 3.96% over 2026-2031. Government procurement rules that favor recyclable materials, the post-FIFA 2022 cold-chain legacy, and Hamad Port’s efficiency collectively give converters a structural edge in export-grade, temperature-controlled solutions. Virgin Kraft linerboard currently dominates due to its strength advantages, yet accelerating e-commerce activity is shifting attention toward lighter substrates and digitally printed graphics that support last-mile delivery efficiency. Regulatory deadlines attached to the Green Packaging Qatar Cleaner initiative compress the window for converters still dependent on virgin-only supply chains, while high natural-gas costs compel investments in energy-efficient corrugators. Companies that secure recycled-fiber feedstock, adopt digital printing, and engineer triple-wall constructions for heavy re-export loads are positioned to capture the most profitable niches in the Qatar corrugated packaging market.

Key Report Takeaways

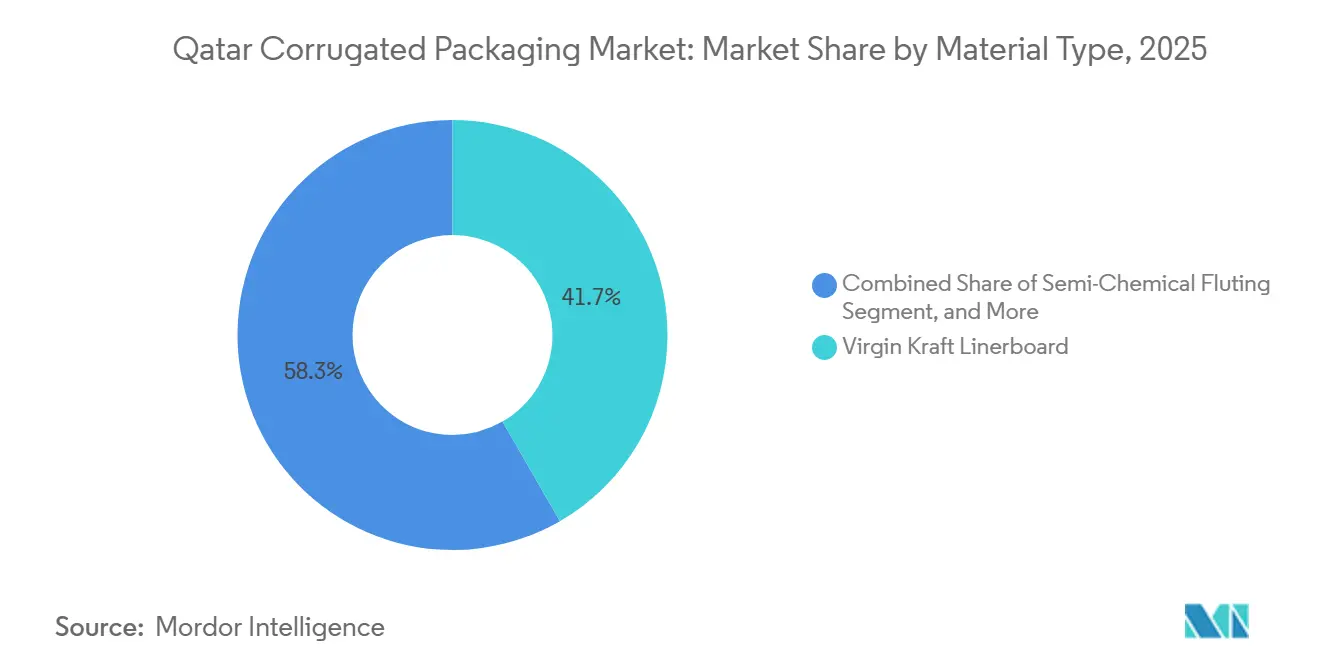

- By material type, the virgin kraft linerboard segment captured 41.67% of the Qatar corrugated packaging market share in 2025.

- By flute type, the Qatar corrugated packaging market size for e flute is projected to grow at a 5.14% CAGR through 2031.

- By packaging type, the regular slotted container segment accounted for 46.61% of the Qatar corrugated packaging market share in 2025.

- By wall type, the Qatar corrugated packaging market size for triple-wall is projected to grow at a 5.43% CAGR through 2031.

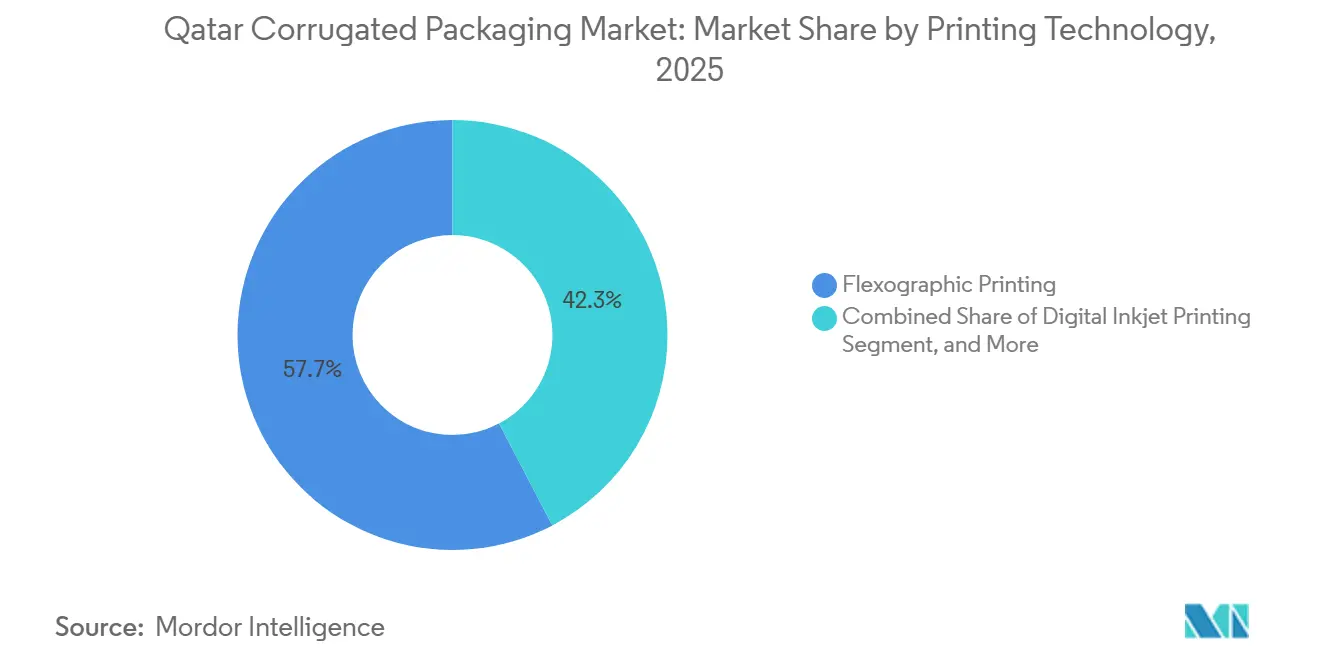

- By printing technology, the flexographic printing segment captured 57.69% of the Qatar corrugated packaging market share in 2025.

- By end-user industry, the Qatar corrugated packaging market size for pharmaceuticals is projected to grow at a 5.24% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Qatar Corrugated Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging E-Commerce Order Volumes in Qatar | +1.2% | National, Doha and Al Rayyan | Short term (≤ 2 years) |

| FIFA-Driven Legacy of Cold-Chain Logistics Infrastructure | +0.9% | National, spillover to GCC routes | Medium term (2-4 years) |

| Mandatory Sustainability Targets for Government Procurement | +0.8% | National, aligned with Qatar Vision 2030 | Medium term (2-4 years) |

| Accelerated Shift Toward Lightweight Shelf-Ready Packaging | +0.6% | National, led by modern-trade retailers | Short term (≤ 2 years) |

| Rapid Capacity Expansion at Hamad Port Free Zones | +0.5% | National, with regional export implications | Long term (≥ 4 years) |

| Digital Printing Adoption for Hyper-Localized Promotions | +0.4% | National, FMCG and e-commerce clusters | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging E-Commerce Order Volumes in Qatar

Qatar’s e-commerce turnover reached USD 3.3 billion in 2024, and the Ministry of Communications and Information Technology projects double-digit growth, which will directly expand demand for shipped secondary packaging.[1]Ministry of Communications and Information Technology, “National E-Commerce Strategy Aligned with Digital Agenda 2030,” MCIT, mcit.gov.qa FedEx’s Ras Bufontas hub, opened in September 2025, shortens delivery cycles and raises expectations for custom-sized corrugated boxes. Converters with digital presses can print variable data, enabling brands to tailor unboxing messages that reduce return rates. Doha and Al Rayyan account for the majority of parcel volume, concentrating growth pressure on nearby box plants. As order frequency rises, die-cut formats that minimize shipping air and dimensional weight become the default choice across the Qatar corrugated packaging market.

FIFA-Driven Legacy of Cold-Chain Logistics Infrastructure

Stadium catering needs left Qatar with refrigerated warehouses now repurposed for pharmaceuticals and produce. This infrastructure requires corrugated packaging engineered for moisture resistance and insulation stability. The freight and logistics sector was valued at USD 10.14 billion in 2024 and is expected to reach USD 13.49 billion by 2030, underscoring long-run volume growth for cold-chain-grade boxes. Wax-alternative coatings and high-performance fluting achieve the required burst strength without compromising recyclability. Converters that supply triple-wall options and moisture-barrier finishes gain a competitive moat among pharmaceutical distributors. The enduring FIFA infrastructure legacy thus underpins a resilient cold-chain corridor for the Qatar corrugated packaging market.

Mandatory Sustainability Targets for Government Procurement

The Ministry of Commerce and Industry’s 2025 proposal mandates recyclable or biodegradable packaging for public contracts within 12 months. FSC or PEFC certification becomes an effective gatekeeper for tender eligibility. Domestic recycled-fiber scarcity forces converters to import certified linerboard, lengthening lead times and raising working-capital needs. Firms that secure local waste-paper partnerships will curb freight costs and reinforce supply resilience. Compliance earns preferred-supplier status, translating into long-term contract visibility across the Qatar corrugated packaging market.

Accelerated Shift Toward Lightweight Shelf-Ready Packaging

Modern retailers stipulate shelf-ready cartons to reduce in-store labor and enhance product visibility. E flute, forecast to grow at 5.14% CAGR, balances print quality with stacking strength, provided moisture levels are controlled. Lightweighting reduces fiber use, trimming carbon footprints in line with the National Climate Change Action Plan. Engineering trade-offs revolve around maintaining edge-crush strength in Qatar’s humid climate. Converters that apply moisture-resistant coatings and precise perforation lines fulfill retailer checklists and gain specification-led repeat business in the Qatar corrugated packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-Side Pressure from Imported Low-Cost Board | -0.7% | National, with spillover effects on regional pricing | Short term (≤ 2 years) |

| High Natural Gas Prices Inflating Steam and Energy Costs | -0.5% | National, concentrated in energy-intensive converting operations | Medium term (2-4 years) |

| Limited Domestic Recycled Fiber Availability | -0.4% | National, with reliance on European imports | Medium term (2-4 years) |

| Constrained Landfill Space Raising Disposal Fees | -0.3% | National, with acute pressure in Doha and Al Rayyan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Side Pressure from Imported Low-Cost Board

Asian suppliers price linerboard 15-25% below local output, a gap widened by export subsidies and scale economies. GCC customs unions ease inflows, compressing domestic margins. Currency volatility compounds cost uncertainty for Qatari plants locked into virgin imports for strength-critical applications. Strategic options include service differentiation design, small-lot flexibility, and sustainability assurances that overseas mills struggle to replicate quickly. Converters that invest in digital printing and rapid prototyping defend price premiums in the Qatar corrugated packaging market.

High Natural Gas Prices Inflating Steam and Energy Costs

Subsidy rationalization lifts industrial gas tariffs, raising steam-generation expenses for corrugators. Aging plants with inefficient burners bear the brunt, widening cost spreads versus automated facilities. Volatile energy inputs complicate multi-year customer contracts unless index-linked clauses are adopted. Investments in waste-heat recovery and high-efficiency dryers can trim operating costs by double digits, cushioning margin pressures. Energy-resilient converters, therefore, carve out a sturdier earnings profile within the Qatar corrugated packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Virgin Kraft Dominance Meets Recycled Fiber Momentum

Virgin Kraft linerboard held 41.67% of the Qatar corrugated packaging market share in 2025, reflecting local demand for high burst strength in heavy machinery and chemical exports. Recycled linerboard, although smaller, is forecast to outpace all other substrates with a 5.71% CAGR, propelled by looming government sustainability thresholds and multinational circular-economy mandates. Importing certified recycled fiber from Europe currently plugs the domestic collection gap, but freight and lead-time challenges are sparking interest in onshore waste-paper aggregation. Converters that blend virgin facings with recycled cores optimize print fidelity and compliance without sacrificing stacking integrity. Such hybrid recipes position suppliers to meet the twin imperatives of performance and sustainability across the Qatar corrugated packaging market.

Growing demand for recycled content realigns bargaining power along the supply chain. Mills can guarantee FSC or PEFC chain-of-custody credentials, which qualify for preferential bidding status in public tenders tied to the Green Packaging Qatar Cleaner initiative.[2]Ministry of Commerce and Industry, “Green Packaging Qatar Cleaner Initiative Report,” MOCI, moci.gov.qa Conversely, plants locked into virgin-only furnishes risk exclusion from profitable government frameworks. As recycled linerboard matures, its volatility in fiber length and contaminant load will necessitate tighter process controls. The learning curve, once scaled, offers cost competitiveness that further diversifies the Qatar corrugated packaging market.

By Flute Type: E Flute Gains Ground in Shelf-Ready Applications

B flute led usage at 38.15% in 2025, favored for its balance of cushioning and stacking strength in export cartons. E flute, however, is predicted to grow the fastest, with a 5.14% CAGR through 2031, as retailers migrate to shelf-ready designs that double as point-of-purchase displays. E flute’s finer profile boosts print resolution, enabling high-impact graphics crucial for brand differentiation in crowded aisles. Yet its thinner caliper poses edge-crush challenges under Qatar’s humid conditions, prompting converters to test moisture-lock adhesives. Plants mastering climate-adapted E flute production become preferred partners for modern trade chains throughout the Qatar corrugated packaging market.

Hybrid multi-flute architectures further blur traditional segment lines. Pairing E flute outer liners with B or C flute cores yields cartons that satisfy both visual and structural requirements. These laminated structures carry a cost premium, yet they eliminate the need for secondary retail-ready units, saving handling time. The engineering sophistication necessary to manufacture multi-flute boards erects a capability barrier that insulates early adopters from price commoditization. Consequently, flute-profile innovation remains a live battlefield, shaping the trajectory of the Qatar corrugated packaging market.

By Packaging Type: Customization Outpaces Standardization

Regular slotted containers captured 46.61% of the revenue share in 2025, owing to their ubiquity in bulk grocery and industrial flows. However, die-cut custom boxes are projected to accelerate at a 4.91% CAGR to 2031 as e-commerce brands emphasize unboxing aesthetics and dimensional-weight savings. Digital inkjet enables cost-effective short runs, empowering converters to offer order-specific graphics that reinforce loyalty programs. Folding cartons and point-of-purchase displays serve premium FMCG campaigns, while pallet boxes tackle heavy-duty exports of mining or energy equipment transiting Hamad Port. The diverse format spectrum underscores an escalating customer expectation for packaging that performs logistical, marketing, and anti-counterfeit functions simultaneously within the Qatar corrugated packaging market.

Service-rich converters invest in CAD design suites and prototyping labs, shortening development cycles for new SKUs. Just-in-time manufacturing aligns with fulfillment center schedules, reducing brand owners' inventory risk. Standard RSC producers lacking customization capacity confront margin compression as commodity supply swells. Therefore, packaging-type differentiation has emerged as a decisive battleground for value creation in the Qatar corrugated packaging industry.

By Wall Type: Triple-Wall Formats Surge in Re-Export Applications

Single-wall cartons maintained a 51.27% share in 2025 because light and mid-weight goods dominate domestic consumption, yet triple-wall boxes are forecast to register a robust 5.43% CAGR as Qatar consolidates its role as a re-export hub. Triple-wall designs safely accommodate over-ton pallet loads and long intermodal transit, critical for heavy machinery bound for African or South Asian markets through Hamad Port. While material-intensive, the added protection minimizes costly product damage claims. Converters advancing lightweight facings and high-rim protection meet customer performance benchmarks while controlling material spend, bolstering competitiveness in the Qatar corrugated packaging market.

Supply-chain partners increasingly seek packaging engineers who simulate vibration, drop, and compression dynamics specific to sea-air logistics corridors. Plants offering in-house ISTA testing secure long-term contracts with industrial exporters. As diversification under National Vision 2030 channels more non-oil products through Qatar, demand for heavy-duty triple-wall solutions will heighten. This scenario pushes wall-type innovation to the forefront of strategic planning for box makers active in the Qatar corrugated packaging market size equation.

By Printing Technology: Digital Inkjet Disrupts Flexographic Incumbency

Flexographic presses accounted for 57.69% of the market in 2025, dominating high-volume commodity runs with low unit costs and water-based inks. Digital inkjet, however, is projected to grow at 5.16% CAGR, driven by SKU fragmentation and hyper-localized promotions in e-commerce and FMCG sectors. Variable-data capability moves serialization, personalized messaging, and anti-counterfeit codes onto the box surface without plate changes, slashing lead times. Pre-treatment coatings and inline spectrophotometers overcome board porosity challenges, improving color accuracy.

Early adopters thus capture high-margin short runs that flexography cannot service profitably, tilting future print-technology investment patterns across the Qatar corrugated packaging market. Hybrid workflows combine digital for changeable elements and flexography for static backgrounds, optimizing the total cost of ownership. Capital outlays drop as OEMs deliver mid-speed corrugated-specific inkjet lines, lowering entry barriers. Plants unwilling to modernize risk relegation to price-taker positions. Therefore, technological agility will increasingly determine competitive endurance in the Qatar corrugated packaging industry.

By End-User Industry: Pharmaceuticals Outpace E-Commerce in Growth Rate

E-commerce fulfillment centers represented 28.19% of volume in 2025, validating the sector’s centrality to box demand. Pharmaceuticals, although smaller, are set to expand more rapidly at a 5.24% CAGR to 2031, driven by serialization mandates under the National Health Strategy 2024. Moisture-barrier coatings, tamper-evident seals, and temperature-stable fluting elevate technical specifications, enabling premium pricing. Processed foods and beverages continue to anchor baseline volume, while fresh produce benefits from post-FIFA cold-chain logistics, albeit at lower growth rates. Electrical products and personal care add segment diversity, each with distinct cushioning and branding requirements.

Collectively, these patterns sustain a broad customer base that cushions cyclical swings in any single vertical within the Qatar corrugated packaging market. Pharmaceutical buyers favor converters that can document clean-room production zones, audit-ready traceability, and validated ink systems. These hurdles filter out smaller competitors and concentrate share among technically adept plants. As Qatar targets regional pharma-hub status, box makers proficient in regulatory compliance secure defensible revenue streams, reinforcing the Qatar corrugated packaging market share hierarchy.

Geography Analysis

Hamad Port’s 7.5 million TEU capacity and 8th-place global efficiency ranking create a funnel effect that channels regional trade through Qatar, stimulating nationwide corrugated-box consumption. Government workshops in February 2026 outlined 24 initiatives to boost port competitiveness, including customs digitalization and berth expansions, ensuring throughput growth persists into the next decade. Rising container swaps drive demand for export-grade triple-wall cartons that withstand multiple handlings and humidity swings during transshipment. Consequently, logistics-centric packaging volumes swell even when domestic consumption plateaus, anchoring the Qatar corrugated packaging market.

Within national borders, Doha and Al Rayyan dominate retail, industrial output, and parcel-sorting activity. Digital Agenda 2030 fast-tracks last-mile delivery nodes and e-payment adoption, funneling a disproportionate share of e-commerce packages through these municipalities. Box plants located within industrial zones near Doha’s ring roads leverage proximity advantages, shortening lead times for fulfillment centers that make same-day delivery promises.[3]Qatar Chamber of Commerce and Industry, “Qatar Freight and Logistics Market Valuation and Forecast,” QCCI, qatarchamber.com Sustainability directives embedded in municipal solid-waste bylaws reinforce recycling imperatives, nudging converters toward local fiber-collection pilots that stabilize supply costs. The interplay of urban consumption density and policy incentives therefore shapes geographic demand contours in the Qatar corrugated packaging market size landscape.

Cross-border forces add a second dimension. Gulf Cooperation Council customs harmonization streamlines linerboard inflows and carton outflows, exposing Qatari converters to price competition yet also enabling exports of high-value specialty boxes. Free zones adjacent to Hamad Port offer tax incentives for value-added conversion, attracting foreign players seeking a GCC launchpad. As a result, geography acts both as a growth catalyst and a competitive filter, rewarding firms that exploit Qatar’s logistics hub status while managing import-cost headwinds in the broader Qatar corrugated packaging market.

Competitive Landscape

Market concentration is moderate, with Arabian Packaging Co. LLC, United Carton Industries, Napco National, and Gulf Carton Factory leading the commodity and food-service segments, yet avenues remain open for specialists in pharmaceutical, digitally printed, and heavy-duty export cartons. Vertical integration into linerboard or waste-paper recovery protects margins by controlling critical inputs. FSC or PEFC certification, once optional, is emerging as a threshold requirement for public tenders, pruning the field of uncertified rivals. Players that pair sustainability credentials with rapid design support and on-time delivery earn a reputation premium across the Qatar corrugated packaging market.

Leading plants operate seven-color flexo folders, high-speed die-cutters, and automatic bundle strappers that churn out cost-efficient long runs. Early inkjet adopters leverage short-run economics to win e-commerce assignments with 48-hour turnarounds. Smaller converters relying on manual slotters remain confined to local artisan brands, limiting scale advantage. As digital adoption widens, hybrid workflows blending inkjet personalization with flexo base layers will become the operational norm, further stratifying capabilities inside the Qatar corrugated packaging industry.

Regulatory currents reshape rivalry dynamics. Energy subsidy reforms favor mills that retrofit corrugators with efficient burners or waste-heat recovery. Import pressures from low-cost Asian board test price resilience, pushing domestic converters toward service-led differentiation. Environmental regulations act as both sword and shield: they raise compliance costs but also close doors on non-conforming imports.[4]Planning and Statistics Authority, “National Climate Change Action Plan 2030,” PSA, psa.gov.qa Collectively, these forces signal an industry on the cusp of technological and regulatory realignment, redefining competitive advantage in the Qatar corrugated packaging market.

Qatar Corrugated Packaging Industry Leaders

Arabian Packaging Co. LLC

United Carton Industries

Napco National

Union Paper Mills

Gulf Carton Factory

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Qatar’s Ministry of Transport outlined 24 port-enhancement projects to elevate Hamad Port’s competitiveness.

- February 2026: The Ministry of Commerce and Industry had initiated talks on a mandatory procurement list prioritizing eco-friendly local product.

- September 2025: FedEx inaugurated a 1,249 square-meter fulfillment facility in Ras Bufontas Free Zone to deepen regional e-commerce coverage.

- August 2025: The Ministry of Commerce and Industry released its report, advocating the Green Packaging Qatar Cleaner initiative with a 6- to 12-month compliance horizon.

Qatar Corrugated Packaging Market Report Scope

The Qatar corrugated packaging market report scope examines the industry's structural evolution as it aligns with Qatar National Vision 2030, prioritizing economic diversification and food security. It evaluates the transformative impact of e-commerce and retail modernization in urban hubs like Doha and Lusail, where demand for right-sized, high-graphics secondary packaging is surging to meet the needs of luxury consumers.

The Qatar Corrugated Packaging Market Report is Segmented by Material (Virgin Kraft Linerboard, Recycled Linerboard, Corrugating Medium, Semi-Chemical Fluting, and Other Materials), Flute Type (A Flute, B Flute, C Flute, E Flute, and F Flute), Packaging Type (Regular Slotted Containers, Die-Cut Custom Boxes, Folding Cartons, Point-of-Purchase Displays, Pallet Boxes, and Other Packaging Types), Wall Type (Single-Wall, Double-Wall, Triple-Wall, and Single Face), Printing Technology (Flexographic Printing, Digital Inkjet Printing, Litho-Lamination, Screen Printing, and Other Printing Technologies), End-User Industry (Processed Foods, Fresh Food and Produce, Beverages, Electrical Products, Personal Care and Cosmetics, E-commerce Fulfillment Centers, Pharmaceuticals, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Kraft Linerboard |

| Recycled Linerboard |

| Corrugating Medium |

| Semi-Chemical Fluting |

| Other Materials |

| A Flute |

| B Flute |

| C Flute |

| E Flute |

| F Flute |

| Regular Slotted Containers |

| Die-Cut Custom Boxes |

| Folding Cartons |

| Point-of-Purchase Displays |

| Pallet Boxes |

| Other Packaging Types |

| Single-Wall |

| Double-Wall |

| Triple-Wall |

| Single Face |

| Flexographic Printing |

| Digital Inkjet Printing |

| Litho-Lamination |

| Screen Printing |

| Other Printing Technologies |

| Processed Foods |

| Fresh Food and Produce |

| Beverages |

| Electrical Products |

| Personal Care and Cosmetics |

| E-commerce Fulfillment Centers |

| Pharmaceuticals |

| Other End-User Industries |

| By Material | Virgin Kraft Linerboard |

| Recycled Linerboard | |

| Corrugating Medium | |

| Semi-Chemical Fluting | |

| Other Materials | |

| By Flute Type | A Flute |

| B Flute | |

| C Flute | |

| E Flute | |

| F Flute | |

| By Packaging Type | Regular Slotted Containers |

| Die-Cut Custom Boxes | |

| Folding Cartons | |

| Point-of-Purchase Displays | |

| Pallet Boxes | |

| Other Packaging Types | |

| By Wall Type | Single-Wall |

| Double-Wall | |

| Triple-Wall | |

| Single Face | |

| By Printing Technology | Flexographic Printing |

| Digital Inkjet Printing | |

| Litho-Lamination | |

| Screen Printing | |

| Other Printing Technologies | |

| By End-User Industry | Processed Foods |

| Fresh Food and Produce | |

| Beverages | |

| Electrical Products | |

| Personal Care and Cosmetics | |

| E-commerce Fulfillment Centers | |

| Pharmaceuticals | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the current and projected size of the Qatar corrugated packaging market?

The Qatar Corrugated Packaging Market size is expected to increase from USD 271.34 million in 2025 to USD 284.27 million in 2026 and reach USD 345.24 million by 2031, growing at a CAGR of 3.96% over 2026-2031.

Which material segment is expected to grow the fastest through 2031?

Recycled linerboard leads in growth, with a projected 5.71% CAGR driven by sustainability mandates and brand-owner commitments.

Why is digital inkjet printing gaining traction among Qatari converters?

Digital presses enable short runs, variable data, and faster turnaround, all critical for e-commerce packaging and localized promotions.

What makes triple-wall cartons increasingly important for exporters?

Triple-wall designs offer the compression and vibration resistance required for heavy machinery and electrical equipment moving through Hamad Port.

How are government sustainability policies influencing material choices?

Mandatory recyclable or biodegradable requirements under the “Green Packaging Qatar Cleaner” initiative are accelerating the shift toward recycled-content boards and certified fiber.

What is driving stronger packaging demand from the pharmaceutical sector?

Cold-chain infrastructure built for FIFA 2022 and new serialization rules under the National Health Strategy 2024 are pushing up requirements for moisture-resistant, traceable cartons.

Page last updated on: