Automotive Connector Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 8.21 Billion |

| Market Size (2031) | USD 11.69 Billion |

| Growth Rate (2026 - 2031) | 7.33% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Connector Market Analysis by Mordor Intelligence

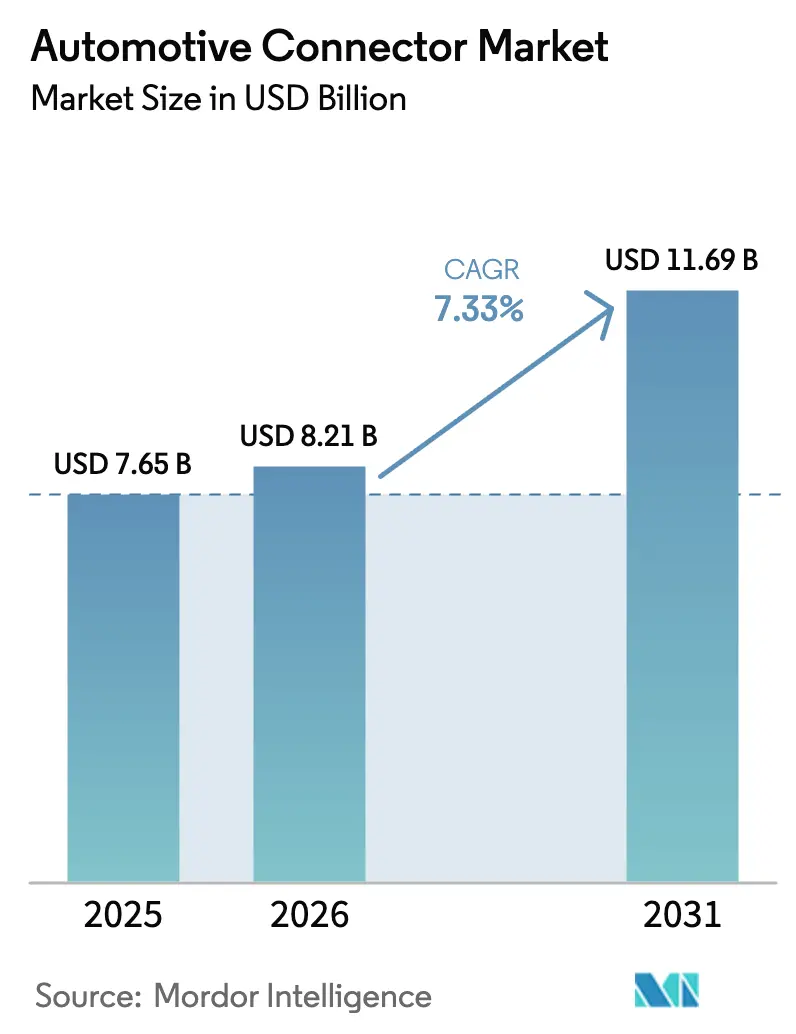

The automotive connector market size is expected to grow from USD 7.65 billion in 2025 to USD 8.21 billion in 2026 and is forecast to reach USD 11.69 billion by 2031 at a 7.33% CAGR over 2026-2031. Momentum in the automotive connector market stems from a rapid transition toward zonal electrical architectures that collapse dispersed control units into regional compute hubs, trimming copper weight and opening head-room for higher-pin-density interfaces. Electrification mandates in every major region now oblige suppliers to qualify high-voltage, high-speed, and high-sealing connectors concurrently, a requirement that advantages incumbents with accredited testing chambers and deeply tooled product families. Accelerating adoption of advanced driver-assistance features is lifting demand for shielded, impedance-controlled connectors capable of maintaining signal integrity at multi-gigabit data rates, while software-defined vehicle strategies lengthen service-life expectations and elevate material-quality standards. Supply-side dynamics remain sensitive to copper and specialty-resin price swings, intensifying interest in selective plating, vertical integration, and long-term offtake agreements with resin producers. Strategic opportunities are most visible in high-speed data links for centralized ADAS processing and in modular charging interfaces as commercial electrification broadens.

Key Report Takeaways

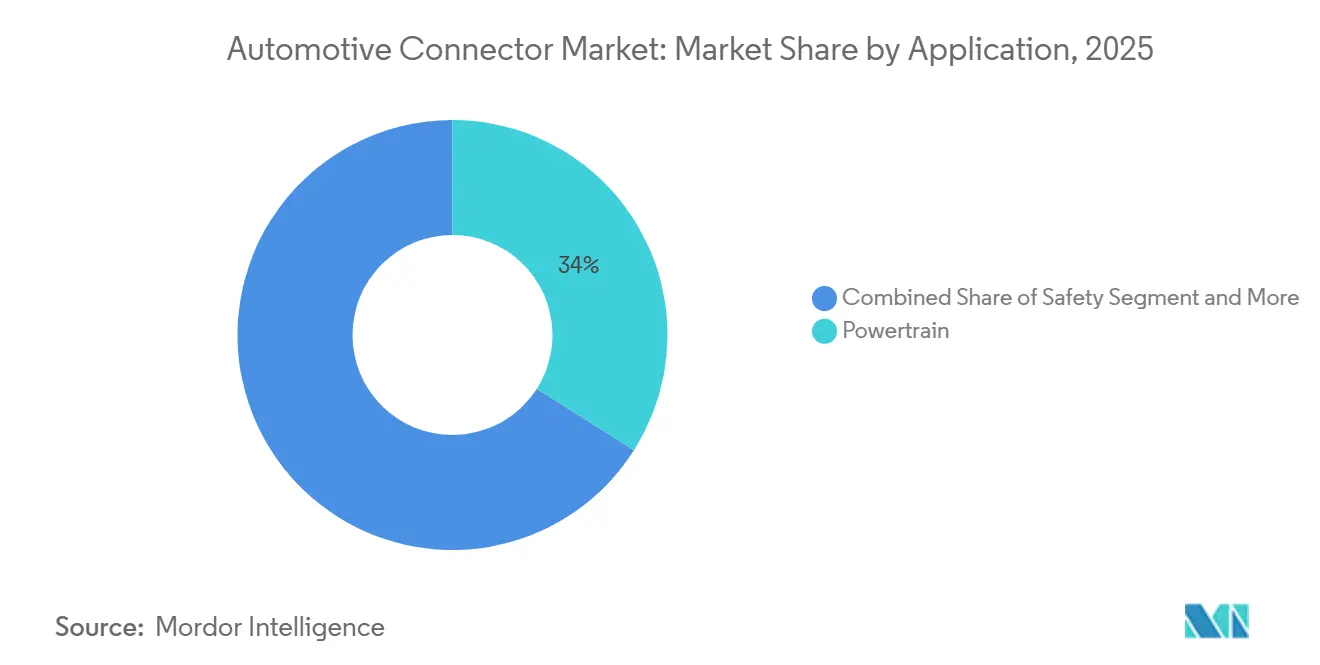

- By application, powertrain systems commanded 34.01% of the automotive connector market share in 2025; ADAS and autonomous solutions are projected to expand at a 17.76% CAGR through 2031.

- By vehicle type, passenger cars led with 54.87% of the automotive connector market revenue share in 2025, while two-wheelers are pacing a swift 11.48% CAGR to 2031.

- By propulsion, ICE vehicles accounted for 47.68% of the automotive connector market size in 2025, whereas battery electric platforms are accelerating at a 27.54% CAGR to 2031.

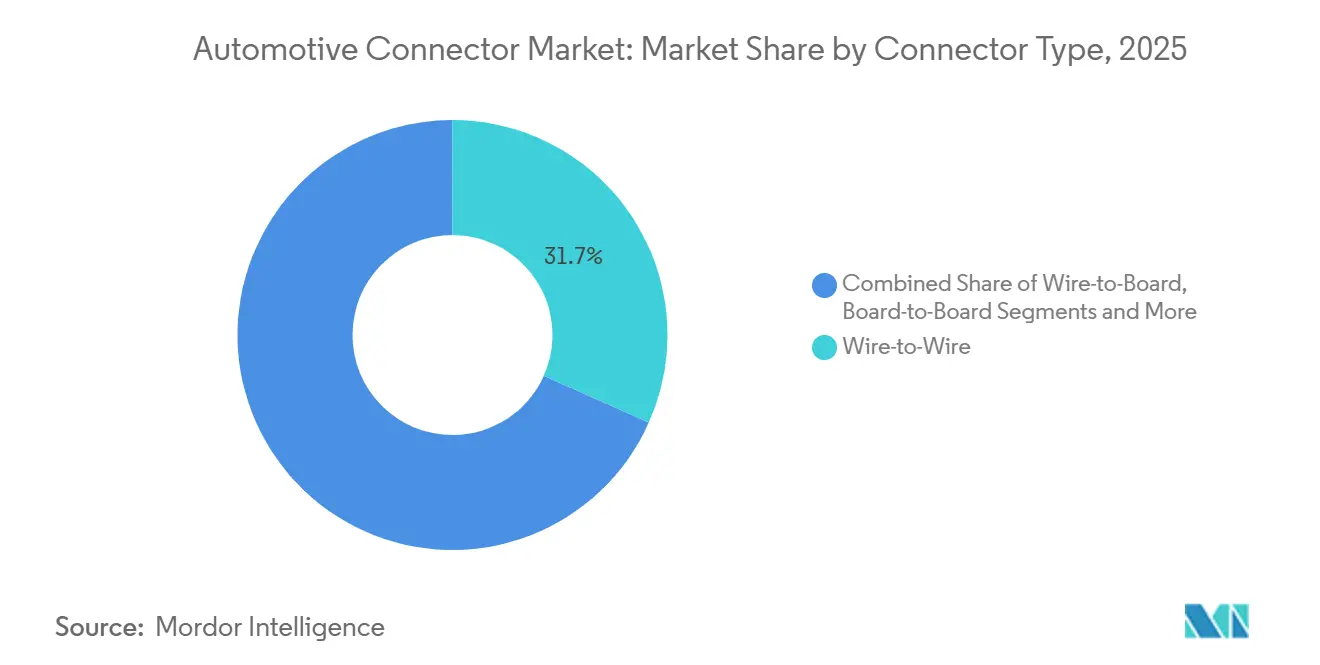

- By connector type, wire-to-wire interfaces held 31.68% of the automotive connector market share in 2025, and high-speed/high-voltage formats are climbing at an 18.86% CAGR.

- By connection sealing, sealed variants represented 68.33% of the automotive connector market size in 2025 and are growing at an 8.08% CAGR across all segments.

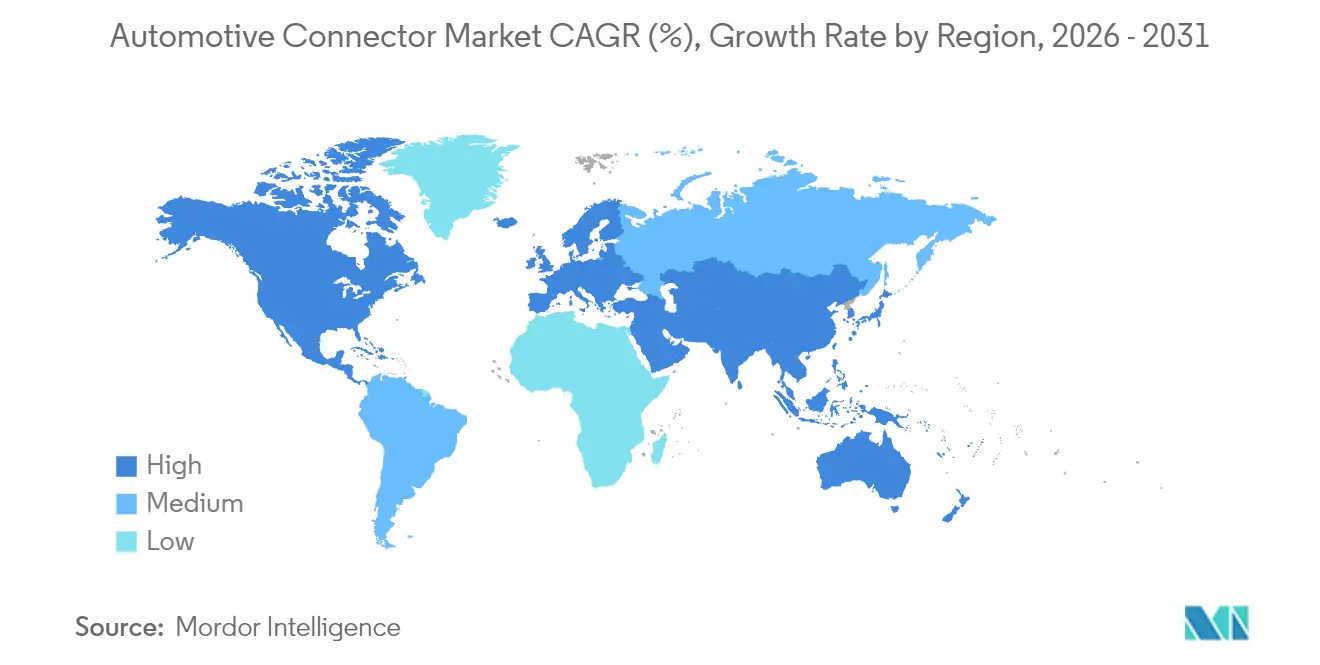

- By geography, Asia-Pacific captured 39.07% of the automotive connector market in 2025; the Middle East and Africa region is forecast to record a 15.17% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Connector Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Electrification | +2.0% | Global, led by China, EU, North America | Medium term (2-4 years) |

| Shift to Zonal E/E Architectures | +1.9% | North America & EU, spill-over to APAC | Long term (≥ 4 years) |

| Autonomous Functionality Penetration | +1.5% | Global, early adoption in North America, EU | Medium term (2-4 years) |

| High-Speed Data Link Requirements | +0.9% | Global, concentrated in premium segments | Long term (≥ 4 years) |

| In-Vehicle Infotainment and Connectivity Units | +0.7% | APAC core, North America, EU | Short term (≤ 2 years) |

| Safety and Emission Mandates | +0.5% | EU, North America, China | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Accelerating Electrification and Higher-Voltage E-Powertrains

High-energy architectures are shifting from 400-volt to 800-volt packs, compelling connectors to sustain a significantly higher level of continuous current with low contact resistance [1]"The Future of Electric Cars: Will high voltage systems become a new standard?", E-Mobility Technology International, e-motec.net. The CharIN Megawatt Charging System, completed in 2024, ratified interfaces that deliver up to 3.75 MW to commercial trucks, forcing redesigns of terminal geometries and liquid-cooling channels [2]"Megawatt Charging System: Charging at 3.75 MW", Vector Group, cdn.vector.com. Lithium-ion thermal-runaway concerns push OEMs toward flame-retardant housings compliant with UL 94 V-0, narrowing resin options and nudging costs higher. Redundant high-voltage interlock pins add two to four positions per connector, increasing pin density and tightening tolerance envelopes. Collectively, these demands are rewriting supply-chain priorities and steering capital toward high-voltage test labs and automated sealing lines.

Shift to Zonal E/E Architectures Driving High-Density Connectors

Zonal strategies aggregate scores from electronic control units into regional compute nodes, reducing wiring mass by up to 30% while centralizing data traffic through fewer physical interfaces. Connectors in these nodes routinely exceed 50 positions, enlarging the consequence of a single mating fault and prompting OEMs to require secondary-lock features and keyed color coding. Suppliers are standardizing housings across voltage and signal types to curb inventory complexity, a choice that also accelerates global platform rollouts. The consolidation cuts unique part numbers but elevates performance expectations, favoring connector families that scale from low-power sensor links to high-current power trunks without dimensional changes.

Rapid ADAS and Autonomous Functionality Penetration

Camera, radar, and LiDAR arrays produce data streams above 10 Gbps, requiring fully shielded connectors with controlled impedance across broad vibration and temperature ranges. The MIPI A-PHY protocol debuted in commercial programs in 2025, enabling 16 Gbps over 15 m cables without repeaters [3]"MIPI Alliance Releases A-PHY v2.0, Doubling Maximum Data Rate of Automotive SerDes Interface To Enable Emerging Vehicle Architectures", MIPI Alliance, mipi.org. Established solutions, such as Rosenberger’s Mini-FAKRA, provide 360-degree shielding and gold-plated contacts with low insertion loss at multi-GHz frequencies. Redundant sensor meshes in pilot autonomous fleets are doubling connector counts per vehicle, underscoring the need for pre-terminated harnesses that integrate self-diagnostic lines. UNECE WP.29 cybersecurity rules add hardware-authentication requirements, encouraging the design of tamper-resistant connector shells.

Software-Defined Vehicles Requiring High-Speed Data Links

Central compute architectures are adopting 10GBASE-T1 Ethernet, as specified in IEEE 802.3ch, which enables high-speed transmission over unshielded twisted pairs, thereby reducing dependence on optical fiber. TE Connectivity’s MATE-AX integrates power and data contacts into a single housing, streamlining assembly steps and facilitating more compact gateway designs. Ecosystems for over-the-air updates necessitate connectors with minimal electromagnetic emissions to comply with CISPR 25 Class 5 standards. This benchmark is consistently achieved only by suppliers boasting in-house anechoic facilities. Aiming for extended durability, there's a notable shift towards gold or palladium plating, chosen for their resistance to fretting corrosion, especially under prolonged vibration exposure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Commodity Prices | -1.2% | Global | Short term (≤ 2 years) |

| Shortage of High-Performance Resins | -0.9% | Global, acute in APAC | Medium term (2-4 years) |

| Reliability Challenges | -0.6% | Global | Long term (≥ 4 years) |

| EMI Compliance Hurdles | -0.4% | North America, EU, Japan | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Copper and Metal Commodity Prices

In 2025, copper remained a critical component in connector production. Supply disruptions in key regions, combined with speculative trading, led to significant price fluctuations. While tier-one suppliers hedged, they still faced risks from varying premiums, which squeezed their margins. Palladium, vital for high-reliability plating, followed a similar trajectory as copper, peaking early in the year and then declining alongside a dip in auto output. In response, major manufacturers reduced the number of plating layers and implemented selective deposition techniques, thereby cutting their precious metal consumption. Conversely, smaller firms lacking hedging strategies felt significant margin pressures, especially when bound by long-term contracts that limited their ability to adjust prices.

Shortage of High-Performance Resins (PPS, LCP)

In 2025, PPS and LCP proved essential for housing components, ensuring they could endure high-temperature environments while maintaining dimensional accuracy during reflow. As demand surged from the aerospace, 5G, and data center sectors, supply tightened, significantly extending lead times. Automotive connectors transitioning to PEI or high-temperature nylons encountered AEC-Q200 requalification delays, resulting in significant project slowdowns. To counter these challenges, players are turning to long-term offtake agreements and forward integration into resin compounding. Additionally, some suppliers are streamlining their portfolios, reducing the number of unique resin grades to alleviate allocation pressures during tight market cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Powertrain Dominance Faces ADAS Disruption

Powertrain connectors hold a commanding 34.01% share in 2025, reflecting their foundational role in enabling engine control, emissions management, and drivetrain efficiency. This dominance is driven by the sheer volume of ICE and hybrid vehicles on the road, where robust connector systems ensure reliable signal transmission in harsh thermal and mechanical environments. Automakers continue to prioritize powertrain reliability, which reinforces demand for high‑durability connectors that withstand vibration, moisture, and temperature fluctuations. At the same time, OEM modernization and the shift toward intelligent powertrain architectures keep this segment structurally significant even as electrification accelerates.

On the other hand, ADAS and autonomous systems are the fastest-growing application areas, with a projected CAGR of 17.76% through 2031. The increasing use of sensors, radars, lidars, cameras, and domain controllers is driving demand for high-speed, high-density connectors that enable quick, reliable data transmission. This trend reflects the automotive industry’s move toward higher levels of autonomy, such as Level 2+ and Level 3, which require advanced data pathways and highly reliable connectivity systems.

By Vehicle Type: Commercial Segments Drive Innovation

Passenger cars account for the largest share at 54.87% in 2025, underscoring their dominance in global vehicle production and the diversity of electronic systems they incorporate. As comfort, safety, and connectivity features proliferate in mainstream models, the number of connectors per vehicle continues to rise sharply. Automotive OEMs are increasingly embedding advanced infotainment, ADAS, and energy‑efficient power distribution systems, all of which depend heavily on connector density and reliability. This broad feature expansion in mass‑market segments anchors the sustained demand for connectors in passenger cars across mature and emerging markets.

In contrast, two‑wheelers are the fastest‑growing segment, with an 11.48% CAGR, driven by rapid electrification in Asia and the rising adoption of connected two-wheelers. As scooters and motorcycles integrate telematics, battery management systems, and LED lighting, connector sophistication and unit count per vehicle are steadily increasing, elevating this traditionally low-electronics segment into a high‑growth opportunity.

By Propulsion Type: Electrification Accelerates Despite ICE Persistence

Internal Combustion Engine (ICE) vehicles dominate the market in 2025 with a 47.68% share, supported by their continuing presence in the global vehicle fleet and entrenched production volumes, especially in developing regions. Despite regulatory pressures, ICE platforms remain deeply relevant due to the longevity of the installed base and ongoing demand in commercial and rural mobility applications. Connectors in ICE setups must withstand harsh conditions, extreme temperatures, oil exposure, and vibration, reinforcing the market value of durable, automotive‑grade interconnect solutions.

Additionally, hybrid powertrains still rely heavily on ICE components, underscoring the segment's significance. However, battery electric vehicles (BEVs) are the fastest‑growing propulsion type, with a 27.54% CAGR, benefiting from strong regulatory incentives, falling battery costs, and expanding charging infrastructure. BEVs demand a significantly higher number of specialized connectors, including high‑voltage, high‑current, and thermal‑resistant interfaces for battery packs, inverters, and e‑axles, creating an exponential growth pathway for connector suppliers.

By Connector Type: High-Speed/High-Voltage Emergence

Wire-to-wire units captured 31.68% share in 2025, covering everything from low-current illumination lines to 50 A battery feeds. Their ubiquity drives intense price competition, pressuring suppliers to automate crimping and terminal insertion. Wire-to-board connectors dominate electronic control units and infotainment modules, and recent migrations to surface-mount designs have improved vibration resistance and coplanarity.

High-speed and high-voltage connectors are rising at an 18.86% CAGR, fueled by 800-V battery nets and multi-gigabit Ethernet backbones. Suppliers are investing in vector network analyzer labs and power-cycling rigs to simultaneously validate signal integrity and temperature rise, a capability not universally available among regional players. Flexible flat cable (FFC) and flexible printed circuit (FPC) connectors are steady in display and camera subsystems but may plateau as wireless alternatives handle non-critical data.

By Connection Sealing: Environmental Protection Drives Sealed Dominance

Sealed designs held 68.33% of the automotive connector market size in 2025 and are predicted to grow at an 8.08% CAGR, reflecting ISO 20653 ingress-protection rules that apply even in underbody and powertrain zones. Elastomer choices vary from silicone to fluoroelastomers based on temperature and fluid exposure, while innovative ultrasonic-welded hybrid seals aim to eliminate micro-leak paths. Unsealed variants linger in cabin locations shielded from moisture, but OEM platform consolidation often defaults to sealed interfaces to standardize across trim levels.

Electric-vehicle duty cycles and public-charging scenarios drive IP67 and IP6K9K ratings to prevent water ingress after pressure washing. Light-weighting programs add aluminum housings with sealed gaskets that mitigate galvanic corrosion, lowering overall mass without sacrificing endurance. Collectively, sealing requirements push suppliers toward advanced materials science and precision molding to ensure long-term performance.

Geography Analysis

Asia-Pacific led with 39.07% of global revenue in 2025 and maintains robust momentum as China increases battery electric vehicle adoption under its dual-credit policy. Local suppliers such as Luxshare Precision situate factories next to major EV plants, shrinking logistics footprints and meeting just-in-time schedules. India accelerates two-wheeler electrification through the FAME II incentive, uplifting demand for cost-sensitive yet durable connectors suited to tropical climates. Japan leans on decades of micro-connector expertise to deliver high-reliability links for early autonomous prototypes, while South Korea funds high-voltage validation labs aligned with its battery-cell capacity build-out. Southeast Asian countries, including Indonesia and Vietnam, gain assembly program commitments from global OEMs seeking diversification beyond China, encouraging connector makers to add regional technical centers.

North America advances as domestic EV production scales under IRA domestic-content rules, prompting several large connector companies to expand U.S. assembly lines to secure eligibility for federal tax credits. Mexico’s Bajío corridor reinforces its standing as a near-shoring nexus, where proximity and free-trade benefits lower lead times for United States plants. Europe sustains technology leadership through Germany’s push for 800-V systems and software-defined platforms, demanding low-inductance, high-speed connectors across powertrain and body domains. The United Kingdom remains active in autonomous pilot projects seeking ultra-low-latency links, although regulatory divergence post-Brexit heightens certification complexity. France, Italy, and Spain steady their connector demand amid platform electrification, while Russia sees constrained imports due to sanctions, prompting sourcing shifts toward regional alternatives.

South America revives production volumes as Brazil recovers from pandemic disruptions; local connector content grows slowly yet steadily as OEMs localize more subsystems. The Middle East and Africa post the fastest regional CAGR of 15.17% through 2031, anchored by Saudi Arabia’s EV manufacturing drive, supported by the Public Investment Fund, and by Egypt’s trade-agreement-catalyzed assembly activity. The United Arab Emirates leverages its logistics strengths to become a regional distribution hub. Turkey consolidates its tier-two supply chains around export-oriented vehicle programs, while South Africa progresses toward hybrid and battery-electrification in its coastal manufacturing clusters. Sub-Saharan markets, including Nigeria and Kenya, see initial uptake of electric two-wheelers, which demand rugged, easily serviceable connectors well suited to local repair infrastructure.

Mordor Intelligence provides coverage of the automotive connector market across other key regional markets. Detailed country-level analysis extends to United States and India incorporating local coverage and market participation, as required.

Competitive Landscape

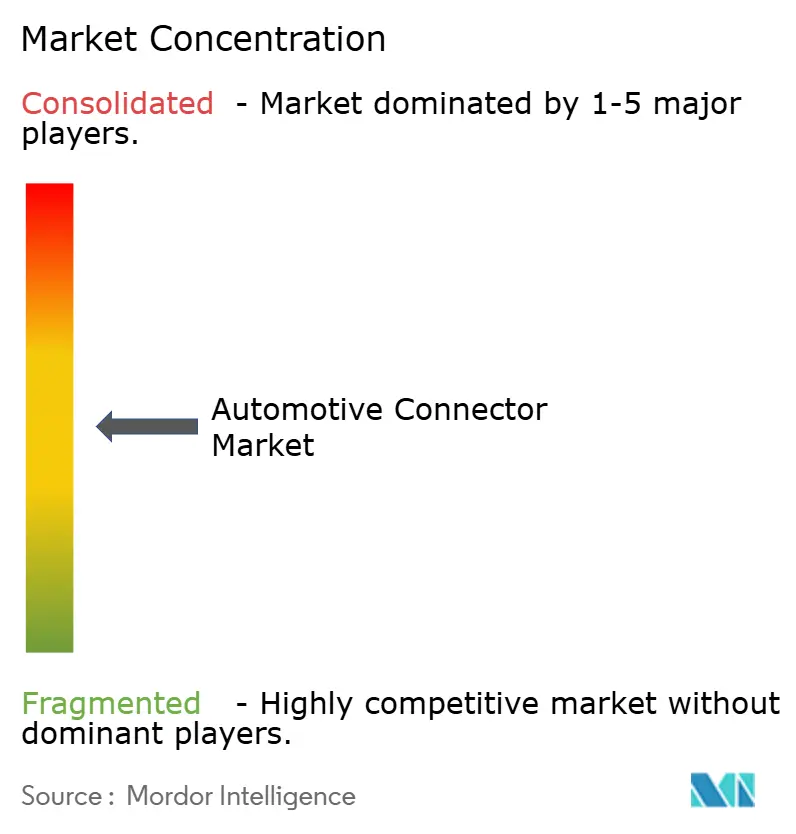

The automotive connector market shows moderate concentration, with TE Connectivity, Yazaki, Aptiv, Molex, and Amphenol collectively holding a sizeable share built on multi-decade design-in relationships and expansive patent libraries. Platform lifecycles ranging from 5 to 8 years lock in specific part numbers, creating entry barriers for latecomers. White spaces flourish in high-speed data and modular charging connectors, where specialists such as Rosenberger and Hirose leverage deep RF and optical expertise to secure sockets in premium ADAS and zonal platforms.

Chinese producers, led by Luxshare Precision, expand footprint by bundling cables and connectors, de-risking OEM procurement, and compressing lead times, particularly for start-up EV manufacturers focused on speed to market. Process technology is becoming a key differentiator. Major players deploy machine-learning-enabled vision inspection to detect crimp and seal defects in-line, reducing warranty claim exposure. Vertical moves into resin compounding and contact stamping enhance supply security when high-temperature plastics tighten, while also shortening design-to-production lead times.

Smaller competitors carve niches in battery disconnect units and high-current busbars, areas underserved by broad-line catalogues of the larger players. Participation in IEEE, ISO, and CharIN working groups grants early visibility into emerging specifications and positions contributors as preferred development partners. Industry analysts anticipate selective consolidation as suppliers chase scale economies to underwrite escalating R&D costs. However, regional challengers with agile engineering and proximity advantages will retain meaningful shares where local content mandates prevail.

Automotive Connector Industry Leaders

-

TE Connectivity Ltd

-

Aptiv PLC

-

Amphenol Corporation

-

Yazaki Corporation

-

Molex Inc. (Koch Industries)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Molex rolled out its MX-DaSH Modular Wire-to-Wire Connectors, which integrate power and signal terminals into a unified modular system. This innovation streamlines wiring harnesses, reducing weight and simplifying complexity, especially in automotive zonal architectures. The solution not only enhances design flexibility but also meets the needs of global OEMs.

- October 2025: TE Connectivity (TE) unveiled its new connectivity portfolio, tailored for the dynamic demands of automotive electronic control units (ECUs) and the next-gen vehicle platforms, notably software-defined vehicles. This portfolio boasts a range of solutions, including board-to-board, wire-to-board, flex-to-board, and wire-to-wire connectors, all engineered for compact, high-performance applications.

- May 2025: TE Connectivity launched the GRACE INERTIA multi-load connectors through Mouser Electronics, featuring a low mating height of 14.1mm, designed for space-constrained automotive applications, including intelligent buildings, HVAC equipment, and automation systems. The product addresses growing demand for compact, high-performance connectors in automotive and adjacent markets.

- May 2025: Hirose unveiled the KM32A Series, an automotive wire-to-board connector that complies with the GMW3191 standard for low-voltage automotive applications. This series boasts an innovative contact spring structure that enhances vibration resistance and a robust center lock to prevent mis-mating. With a tensile/pry strength of up to 75N, the KM32A Series also offers impressive heat resistance, enduring temperatures up to 125°C.

Global Automotive Connector Market Report Scope

Connectors are primarily used to connect or disconnect electrical lines. In automobiles, different types of connectors, such as wire-to-wire connections, board-to-wire connections, and device connections, are used to connect or disconnect prefabricated parts or devices to the given wiring harness.

The automotive connector market is segmented by application, vehicle type, propulsion type, connector type, connection sealing, and geography. By application, the market is segmented into Powertrain, Safety and Security, Body Wiring and Power Distribution, Comfort and Convenience, Navigation and Instrumentation, ADAS and Autonomous Driving, and Charging and Energy Management. By vehicle type, the market is segmented into Passenger Cars, Light Commercial Vehicles, Medium and Heavy Commercial Vehicles, Two-Wheelers, and Bus and Coach. By propulsion type, the market is segmented into Internal Combustion Engine, Hybrid Electric Vehicles, Plug-in Hybrid Electric Vehicles, Battery Electric Vehicles, and Fuel-Cell Electric Vehicles. By connector type, the market is segmented into Wire-to-Wire, Wire-to-Board, Board-to-Board, I/O and Circular, FFC/FPC and Micro, and High-Speed/High-Voltage. By connection sealing, the market is segmented into Sealed and Unsealed. By geography, the market is segmented into North America, South America, Europe, Asia-Pacific, and Middle East and Africa.

The report provides market sizing and forecasts in terms of value (USD) and volume (units).

| Powertrain |

| Safety and Security |

| Body Wiring and Power Distribution |

| Comfort, Convenience and Entertainment |

| Navigation and Instrumentation |

| ADAS and Autonomous Systems |

| Charging and Energy Management (EV) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Two-Wheelers |

| Bus and Coach |

| Internal Combustion Engine (ICE) Vehicles |

| Hybrid Electric Vehicles (HEV) |

| Plug-in Hybrid Electric Vehicles (PHEV) |

| Battery Electric Vehicles (BEV) |

| Fuel-Cell Electric Vehicles (FCEV) |

| Wire-to-Wire |

| Wire-to-Board |

| Board-to-Board |

| I/O and Circular |

| FFC/FPC and Micro |

| High-Speed / High-Voltage |

| Sealed |

| Unsealed |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Indonesia | |

| Vietnam | |

| Philippines | |

| Australia | |

| New Zealand | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| South Africa | |

| Egypt | |

| Nigeria | |

| Rest of Middle East and Africa |

| By Application | Powertrain | |

| Safety and Security | ||

| Body Wiring and Power Distribution | ||

| Comfort, Convenience and Entertainment | ||

| Navigation and Instrumentation | ||

| ADAS and Autonomous Systems | ||

| Charging and Energy Management (EV) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Two-Wheelers | ||

| Bus and Coach | ||

| By Propulsion Type | Internal Combustion Engine (ICE) Vehicles | |

| Hybrid Electric Vehicles (HEV) | ||

| Plug-in Hybrid Electric Vehicles (PHEV) | ||

| Battery Electric Vehicles (BEV) | ||

| Fuel-Cell Electric Vehicles (FCEV) | ||

| By Connector Type | Wire-to-Wire | |

| Wire-to-Board | ||

| Board-to-Board | ||

| I/O and Circular | ||

| FFC/FPC and Micro | ||

| High-Speed / High-Voltage | ||

| By Connection Sealing | Sealed | |

| Unsealed | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Indonesia | ||

| Vietnam | ||

| Philippines | ||

| Australia | ||

| New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| South Africa | ||

| Egypt | ||

| Nigeria | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large will the automotive connector market be by 2031?

It is projected to reach USD 11.69 billion by 2031, advancing at a 7.33% CAGR from 2026.

Which application area is growing fastest?

ADAS and autonomous systems show the highest growth trajectory at 17.76% CAGR through 2031.

Which vehicle category currently buys the most connectors?

Passenger cars lead demand, accounting for 54.87% of 2025 revenue.

Which region is expanding most rapidly?

The Middle East and Africa region is forecast to log the fastest CAGR at 15.17% through 2031.

What connector type commands the largest share today?

Wire-to-wire connectors dominate with 31.68% of 2025 revenue.

Page last updated on: