India Automotive Connectors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

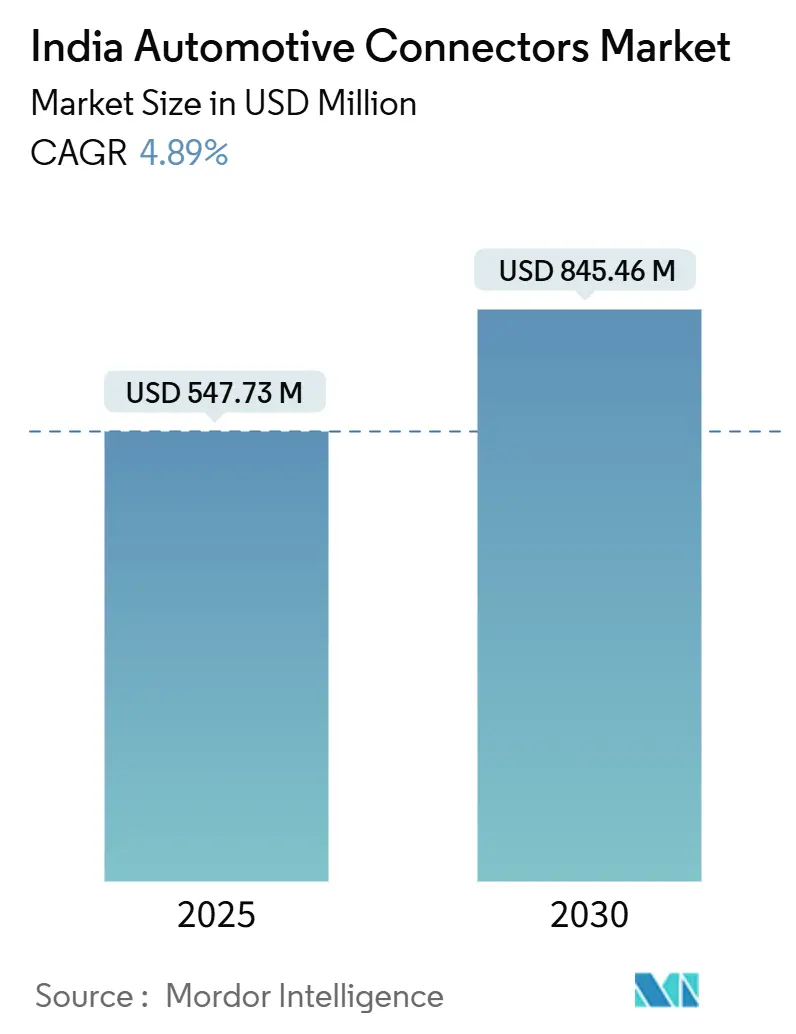

| Market Size (2025) | USD 547.73 Million |

| Market Size (2030) | USD 845.46 Million |

| Growth Rate (2025 - 2030) | 4.89% CAGR |

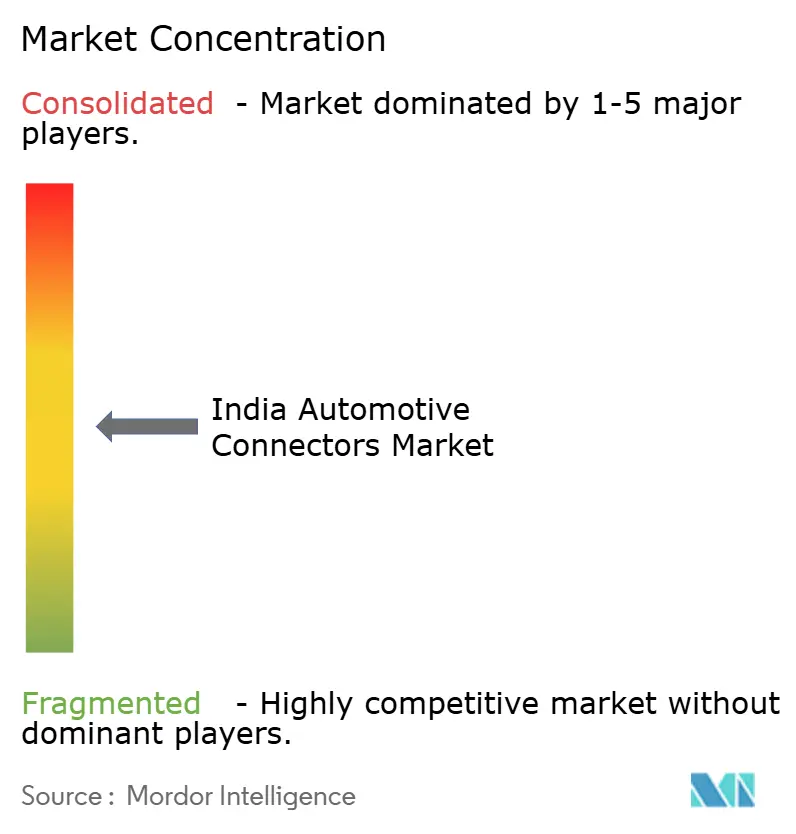

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

India Automotive Connectors Market Analysis by Mordor Intelligence

The India automotive connectors market size stands at USD 547.73 million in 2025 and is projected to reach USD 845.46 million by 2030, reflecting a 4.89% CAGR through the forecast period. Policy momentum under FAME-II and PM E-DRIVE, together allocating more than USD 3.5 billion to electric mobility and charging infrastructure, is shifting demand from traditional internal-combustion applications to high-voltage battery electric systems. Localization incentives under the USD 3.5 billion PLI-Auto scheme are drawing global suppliers to set up precision manufacturing across Tamil Nadu, Gujarat, and Haryana, improving supply-chain resilience and cutting import dependence

Key Report Takeaways

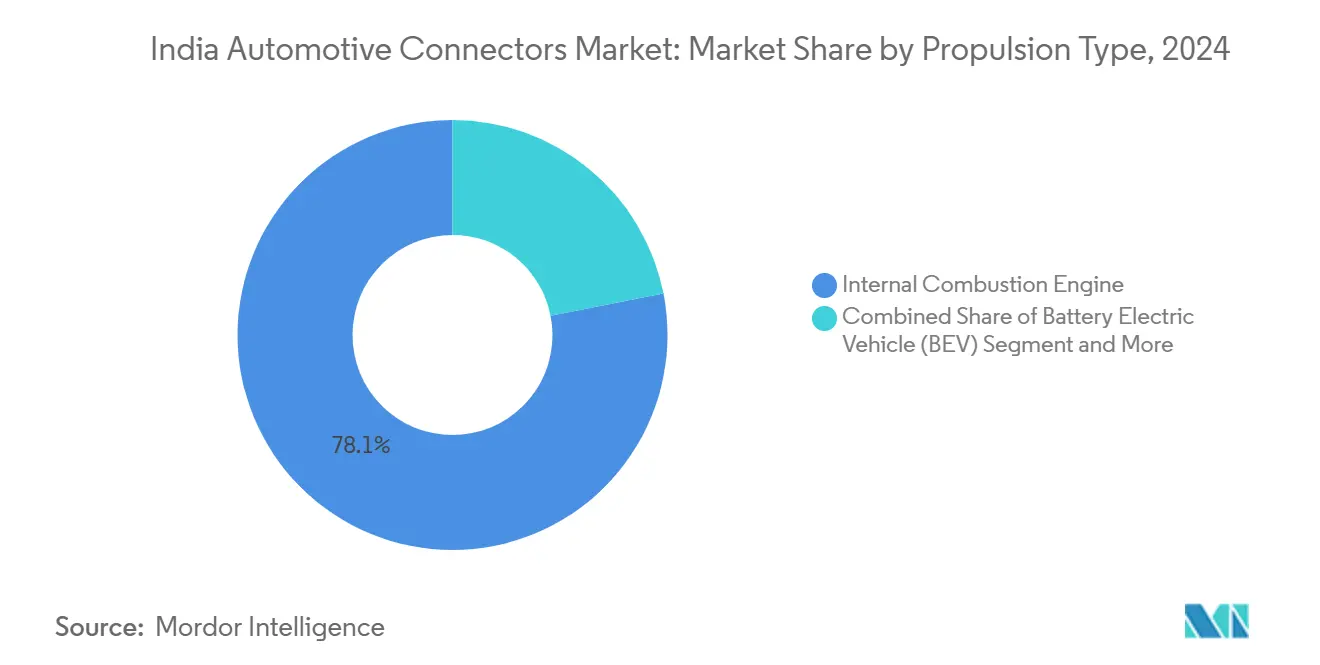

- By propulsion type, internal-combustion engines led with 78.11% of the Indian automotive connectors market share in 2024, and battery electric vehicles are forecast to advance at a 23.41% CAGR through 2030.

- By connection type, wire-to-board interfaces held 39.52% of the Indian automotive connectors market size in 2024, and board-to-board connectors are expected to grow at a 17.63% CAGR over 2025-2030.

- By voltage, low-voltage circuits below 60 V accounted for 68.07% of the Indian automotive connectors market size in 2024, and high-voltage segments above 300 V are projected to post a 21.12% CAGR during the forecast period.

- By component, terminals captured 42.08% of the Indian automotive connectors market size in 2024, and housings are set to expand at an 18.02% CAGR to 2030.

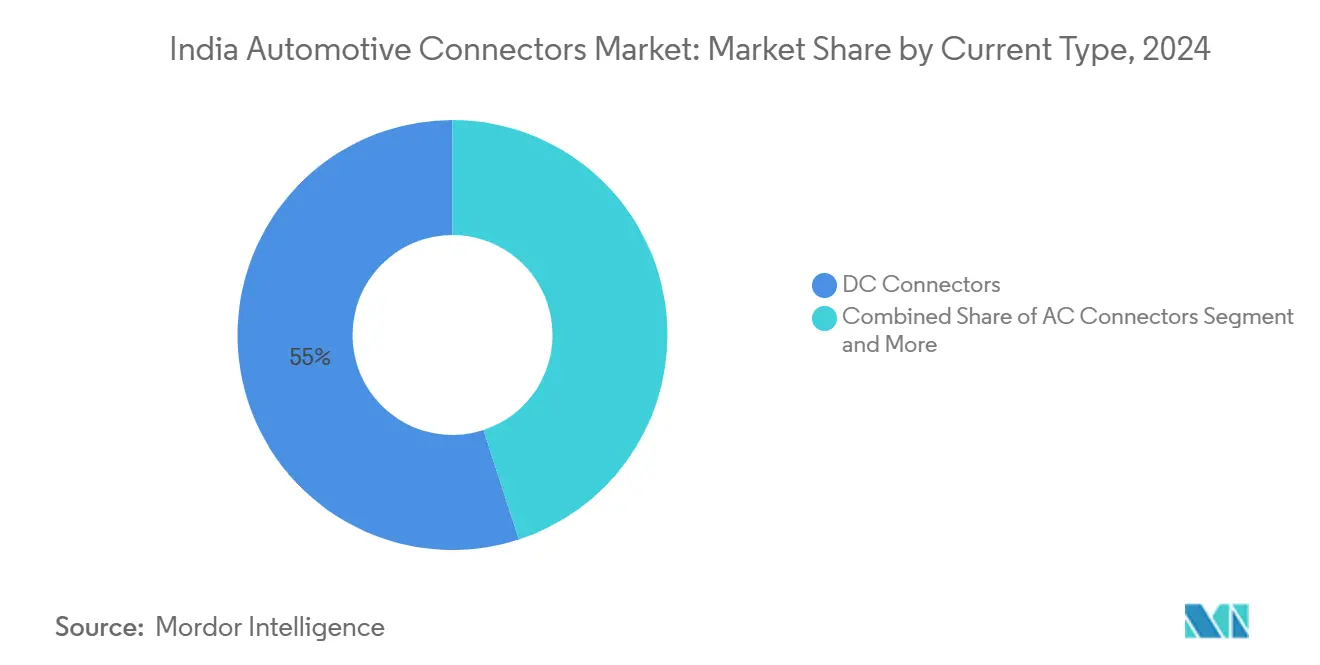

- By current type, DC connectors dominated with 55.04% of the India automotive connectors market share in 2024, and combined CCS/GB-T units are anticipated to record a 24.31% CAGR through 2030.

- By application, engine-management and powertrain systems accounted for 27.06% of the India automotive connectors market share in 2024 and ADAS and safety systems are expected to register a 27.53% CAGR between 2025 and 2030.

India contributes to a system defined not by any single country or region but by the interaction of many. The global automotive connector market data by Mordor Intelligence represents that combined structure.

India Automotive Connectors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid EV Penetration Under FAME-II PM E-DRIVE Schemes | +1.2% | National, with early gains in Delhi, Maharashtra, Karnataka | Medium term (2-4 years) |

| Rising On-Board Electronics for ADAS Safety Compliance | +0.9% | West India and South India automotive clusters | Short term (≤ 2 years) |

| PLI-Auto Incentives Accelerating Localisation of Connector Production | +0.8% | National, concentrated in Tamil Nadu, Gujarat, Haryana | Medium term (2-4 years) |

| High-Voltage Architecture Shift (More Than 400 V) in New BEVs | +0.7% | National EV manufacturing hubs | Long term (≥ 4 years) |

| Surge in E-2W/E-3W Volumes Requiring Rugged Low-Cost Connectors | +0.6% | National, with concentration in North and West India | Short term (≤ 2 years) |

| BIS Draft on HVIL Safety Driving Design Upgrades | +0.3% | National manufacturing compliance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid EV Penetration Under FAME-II PM E-DRIVE Schemes

Government policy architecture through FAME-II and the newly launched PM E-DRIVE scheme represents a paradigm shift in India's automotive electrification strategy, directly impacting connector demand patterns across vehicle segments. The PM E-DRIVE scheme's USD 2.4 billion allocation over 2024-2026 specifically targets e-bus deployment and charging infrastructure expansion, creating concentrated demand for high-current DC charging connectors and vehicle-side interfaces. This policy momentum has triggered a cascade effect where OEMs are accelerating EV program timelines, with Tata Motors and Mahindra & Mahindra collectively planning over 15 new EV models by 2026, each requiring specialized connector solutions for battery management, thermal control, and high-voltage power distribution. The scheme's emphasis on domestic manufacturing creates a supply chain localization imperative, positioning Indian connector manufacturers to capture value previously dominated by imports. BIS standards IS 18590:2024 and IS 18606:2024 for EV safety compliance further reinforce the regulatory framework supporting this transition.

Rising On-board Electronics for ADAS Safety Compliance

India's automotive electronics content evolution reflects a structural shift toward software-defined vehicles, with ADAS penetration accelerating beyond premium segments into mass-market applications. The implementation of AIS-140 GPS tracking mandates for commercial vehicles and the upcoming Bharat NCAP safety ratings have created regulatory pull for advanced driver assistance technologies, directly translating into higher connector content per vehicle. This electronics proliferation manifests in increased demand for high-speed data connectors supporting camera modules, radar sensors, and LiDAR systems, with each ADAS-equipped vehicle requiring 15-20% more connector content compared to conventional powertrains. The trend toward centralized computing architectures and zonal vehicle designs further amplifies connector requirements, as traditional point-to-point wiring gives way to high-bandwidth Ethernet backbones requiring specialized automotive-grade interconnects. Molex's recent launch of the MX-DaSH family specifically addresses this zonal architecture demand, combining power, signal, and high-speed data transmission in unified connector solutions.

PLI-Auto Incentives Accelerating Localization of Connector Production

The PLI-Auto scheme's USD 3.5 billion incentive structure has fundamentally altered the economics of automotive component manufacturing in India, creating compelling business cases for connector localization across global suppliers. This policy framework offers production-linked incentives ranging from 8-16% of incremental sales value over five years, with higher rates for advanced automotive technologies, including electric vehicle components and electronics. The scheme's impact extends beyond direct manufacturing incentives to encompass supply chain ecosystem development, with companies like Aptiv expanding their Chennai facility and Syrma SGS establishing new PCB manufacturing capabilities to serve automotive electronics demand. This localization momentum creates opportunities for domestic connector manufacturers to establish technology partnerships with global players, while simultaneously reducing import dependency and improving supply chain resilience. The scheme's emphasis on value addition and technology transfer ensures that localized production involves sophisticated manufacturing processes rather than simple assembly operations.

High-Voltage Architecture Shift (More than 400 V) in New BEVs

India's electric vehicle architecture evolution toward 400V+ systems represents a fundamental engineering transition with profound implications for connector technology and manufacturing requirements. This voltage escalation, driven by charging efficiency optimization and cable weight reduction imperatives, necessitates specialized connector designs capable of handling increased electrical stress while maintaining safety and reliability standards. The transition creates demand for HVIL (High Voltage Interlock Loop) compliant connectors, with BIS draft standards mandating specific safety protocols for high-voltage vehicle systems, including connector design requirements for fault detection and emergency disconnection capabilities. Molex's 48V system evolution report highlights the technical challenges and opportunities associated with mid-voltage applications, positioning 48V as a bridge technology toward full high-voltage architectures. This architectural shift requires precision manufacturing capabilities for contact plating, insulation materials, and environmental sealing, creating barriers to entry that favor established suppliers with advanced materials science expertise and automotive qualification experience.

Restraints Impact Analys*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper Precious-Metal Price Volatility Squeezing Margins | -0.6% | National manufacturing base | Short term (≤ 2 years) |

| Connector Reliability Issues in India's Hot/Humid Climate | -0.4% | National, acute in coastal and tropical regions | Medium term (2-4 years) |

| Fragmented Quality Standards Among Tier-2 Suppliers | -0.3% | National supplier ecosystem | Medium term (2-4 years) |

| Skilled-Labour Shortage in Precision Plating Processes | -0.2% | Manufacturing clusters in Tamil Nadu, Karnataka, Gujarat | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Copper Precious-Metal Price Volatility Squeezing Margins

Raw material cost pressures represent a persistent challenge for India's automotive connector manufacturers, with copper prices experiencing volatility in 2024[1]Jingyue Hsiao, "Rare earth shortage reportedly threatens to delay Tata Electronics' wafer fab plans," DIGITIMES Asia, digitimes.com. amid global supply chain disruptions and Chinese export restrictions. This price instability directly impacts connector manufacturing economics, as copper constitutes 30-40% of material costs in high-current applications, while precious metals like gold and silver used in contact plating add further cost complexity. The situation has been exacerbated by rare-earth element shortages affecting automotive electronics, with electric two-wheeler (e2W) companies upset with some of their suppliers of heavy rare-earth magnet–powered electric motors[2]Surajeet Das Gupta, "Rare-earth squeeze puts electric two-wheeler firms, suppliers at odds," Rediff, rediff.com.. Manufacturers are responding through strategic material sourcing, with companies like Modison Ltd implementing long-term supply contracts and multi-sourcing strategies to mitigate price volatility impacts, while simultaneously investing in material science research to develop cost-effective alternatives. The challenge is compounded by the need to maintain automotive-grade quality standards while managing cost pressures, creating a delicate balance between material optimization and performance requirements.

Skilled-Labor Shortage in Precision Plating Processes

India's automotive connector manufacturing expansion faces a critical bottleneck in specialized workforce availability, particularly for precision manufacturing processes requiring clean-room environments and micro-level quality control. The semiconductor industry's parallel growth has intensified competition for skilled technicians, with companies like Applied Materials and Kaynes Technology implementing global training rotations and expatriate knowledge transfer programs to address capability gaps[3]Suraksha P, "Skills gap forces chip cos to seek global training & talent rotation," Economic Times, economictimes.indiatimes.com. . This shortage is particularly acute in precision plating processes essential for connector contact manufacturing, where surface finishes must meet automotive specifications for corrosion resistance and electrical conductivity over vehicle lifecycles. Companies are responding through industry-academia partnerships and internal training programs, with firms like Zetwerk Electronics partnering with ICT Academy and Nasscom Skill Council to develop specialized curricula for precision manufacturing applications.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Internal-Combustion Foundation, Battery-Electric Momentum

Internal-combustion engines accounted for a commanding 78.11% of the India automotive connectors market share in 2024, underpinning stable demand for 12 V and 48 V harnesses across passenger and commercial vehicles. Dependable volumes from legacy platforms keep production lines full, yet price pressure and tightening emissions rules cap growth.

Battery-electric vehicles are set to expand connector revenue at a 23.41% CAGR over 2025-2030, supported by FAME-II subsidies, lower battery costs, and the rollout of 400 V + charging ecosystems. Each BEV integrates up to five times the contact points of a comparable ICE model, lifting the India automotive connectors market size in high-voltage categories and pushing suppliers toward plated copper-alloy terminals that meet HVIL safety rules.

By Connection Type: Wire-to-Board Stronghold and Board-to-Board Upswing

Wire-to-board interfaces represented the largest 2024 slice at 39.52% of the India automotive connectors market size, thanks to their versatility in powertrain control units, lighting modules, and infotainment stacks. Low profile, cost-efficient housings keep them entrenched in mass-market models.

Board-to-board solutions will accelerate at a 17.63% CAGR, propelled by zonal architectures that centralize compute power and require 28 Gbps signal integrity within millimeter-pitch footprints. As OEMs migrate to domain controllers, demand rises for stack-height-adjustable connectors with robust EMI shields, enlarging the India automotive connectors market share for high-speed data products.

By Voltage: Low-Voltage Legacy, High-Voltage Growth Vector

Low-voltage circuits below 60 V held 68.07% of 2024 revenue, anchored by the 12 V architecture that powers body electronics, lighting, and mild-hybrid accessories. Incremental 48 V systems in start-stop modules sustain incremental value without major design upheaval.

High-voltage segments above 300 V will surge at a 21.12% CAGR as BEVs shift toward 400 V and 800 V packs, cutting charge times and cable mass. Compliance with IS 18590:2024 elevates barriers to entry, steering the India automotive connectors market size toward players equipped for partial-discharge testing and laser-welded shielding.

By Component: Terminal Core and Housing Acceleration

Terminals contributed 42.08% of the Indian automotive connectors market share in 2024, reflecting their crucial role in current conduction and mechanical retention. Investments target crimp-force control and gold-flash plating to ensure less than 2 mΩ contact resistance over life-cycle vibration profiles.

Housing units will grow at an 18.02% CAGR through 2030, driven by IP6K9K sealing mandates and pin-density jumps in ADAS and battery modules. Advanced glass-fiber-reinforced PA66 and PBT compounds enable thinner walls without sacrificing heat resistance, expanding the Indian automotive connectors market size for value-added overmolded shells.

By Current Type: DC Bedrock, Combined-Standard Lift

Direct-current connectors dominated 2024 with a 55.04% share, serving batteries, inverters, and auxiliary loads across ICE and electric models. Cost-optimized knife contacts and tin over nickel plating keep ASPs contained for volume programs.

Combined CCS/GB-T designs will post a 24.31% CAGR, as national charging networks pivot to global standards and OEMs' future-proof export models. Liquid-cooled 500 A pins and smart-lock mechanisms raise margins, enlarging the Indian automotive connectors market share for multi-standard fast-charge couplers.

By Application: Engine-Management Base, ADAS Takeoff

Engine-management and powertrain systems retained 27.06% of the Indian automotive connectors market size in 2024, ensuring baseline volume for sensors, injectors, and turbo actuators under BS VI-B norms. Ongoing ICE production stabilizes demand even as electrification gains pace.

ADAS and safety connectors will climb at a 27.53% CAGR, driven by Bharat NCAP timelines that embed camera, radar, and LiDAR arrays into mainstream trims. Each Level 2-ready vehicle adds more than 150 high-speed contacts, accelerating revenue growth and lifting the India automotive connectors market share for shielded, low-latency interfaces.

Geography Analysis

North India emerges as a significant automotive connector market driven by the National Capital Region's automotive manufacturing concentration and Haryana's established OEM presence, including Maruti Suzuki's Gurugram and Manesar facilities that collectively produce over 1.5 million vehicles annually. The region benefits from proximity to major commercial vehicle manufacturers and the government's policy implementation hub, creating demand for both conventional and emerging EV connector applications.

South India represents the fastest-growing regional market, leveraging established electronics manufacturing capabilities in Karnataka and Tamil Nadu to capture automotive connector production opportunities. The region's automotive ecosystem centers on Bengaluru's R&D capabilities, Chennai's automotive manufacturing concentration, and Hosur's component supplier network, creating integrated value chains that support both domestic demand and export opportunities.

West India maintains strong market presence through Maharashtra and Gujarat's automotive manufacturing leadership, with Pune serving as a major automotive hub and Gujarat emerging as a preferred destination for EV manufacturing investments. Maharashtra's automotive ecosystem encompasses major OEM facilities from Tata Motors, Mahindra & Mahindra, and Bajaj Auto, creating diversified demand across passenger vehicles, commercial vehicles, and two-wheelers that require specialized connector solutions for different applications and price points. Gujarat's strategic positioning as an EV manufacturing destination, supported by state government incentives and infrastructure development, creates growth opportunities for connector suppliers serving electric vehicle applications.

The automotive connector market is analyzed by Mordor Intelligence across multiple other geographies. This is complemented by country-specific insights for United States, reflecting various localized market behavior and policy environments' coverage.

Competitive Landscape

The India Automotive Connectors Market exhibits moderate fragmentation with established global suppliers competing alongside domestic manufacturers for market share across different vehicle segments and application areas. Market concentration patterns favor companies with automotive qualification capabilities, advanced manufacturing processes, and established OEM relationships, creating barriers to entry that protect incumbent suppliers while limiting new entrant opportunities. Strategic patterns emphasize localization investments, technology partnerships, and vertical integration initiatives that enable suppliers to capture value across the automotive electronics supply chain while managing cost pressures and quality requirements.

Global suppliers, including TE Connectivity, Yazaki Corporation, and Amphenol India, leverage established automotive relationships and advanced technology capabilities to maintain premium market positions, while domestic players like Samvardhana Motherson Group and Spark Minda compete through cost advantages and local market knowledge. White-space opportunities exist in specialized EV connector applications, high-speed data transmission solutions, and ruggedized connectors for commercial vehicle applications where technical requirements exceed traditional automotive specifications.

Technology adoption patterns focus on automated manufacturing processes, advanced materials science, and integrated design capabilities that enable suppliers to deliver miniaturized, high-performance connector solutions while maintaining automotive-grade reliability standards. Companies are investing in precision manufacturing capabilities, clean-room facilities, and specialized testing equipment to meet evolving automotive electronics requirements, with particular emphasis on EV applications that demand high-voltage insulation, thermal management, and safety compliance capabilities

India Automotive Connectors Industry Leaders

-

TE Connectivity

-

Yazaki Corporation

-

Samvardhana Motherson Group

-

Amphenol India

-

Sumitomo Electric

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Hirose Electric expanded its automotive connector portfolio with the AU1 Series USB 3.2 compatible wire-to-board connectors specifically designed for automotive applications, addressing the growing demand for high-speed data transmission in vehicle infotainment and connectivity systems.

- November 2024: Inteva Products announced a USD 3.3 million expansion of its Chakan manufacturing facility in Pune, increasing production capacity by 70% and adding 100 new jobs to support growing automotive demand in India's domestic and export markets.

Key Questions Answered in the Report

Which connection type leads demand today?

Wire-to-board connectors hold the highest share at 39.52% in 2024 due to their versatility across control units and infotainment modules.

Which region is expanding fastest for suppliers?

South India is the fastest-growing geography, supported by strong electronics manufacturing in Chennai and Bengaluru and robust OEM presence.

How are policy incentives shaping localization?

The USD 3.5 billion PLI-Auto program reimburses 8-16% of incremental sales, encouraging global and domestic firms to establish connector plants and deepen supply chains.

What challenges do manufacturers face in scaling capacity?

Copper price volatility and a skilled-labor shortage in precision plating processes are compressing margins and lengthening ramp-up timelines for new facilities.

Page last updated on: