Automotive Drive Shaft Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 12.41 Billion |

| Market Size (2031) | USD 16.42 Billion |

| Growth Rate (2026 - 2031) | 5.77% CAGR |

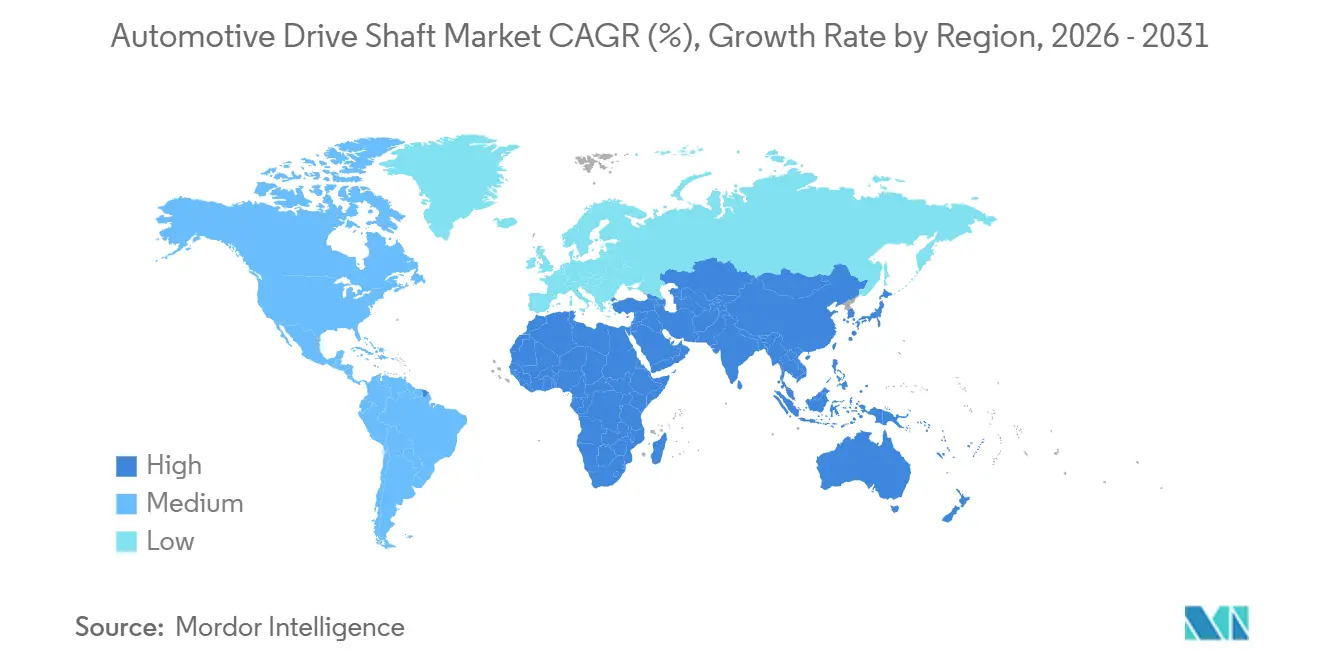

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Drive Shaft Market Analysis by Mordor Intelligence

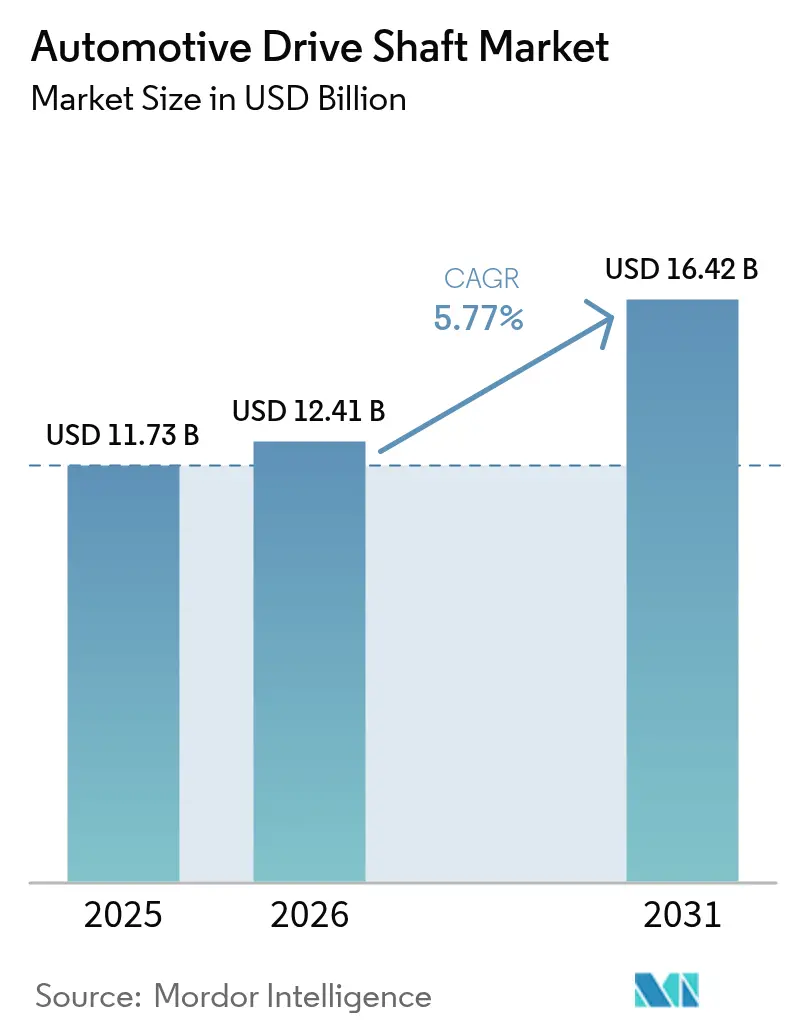

The Automotive Drive Shaft Market size is expected to grow from USD 11.73 billion in 2025 to USD 12.41 billion in 2026 and is forecast to reach USD 16.42 billion by 2031 at 5.77% CAGR over 2026-2031. Electrification is reshaping driveline architectures, substituting multi-piece half-shafts in many battery electric vehicles (BEVs) with compact e-axles while simultaneously increasing demand for ultra-precise, lightweight propeller shafts that can withstand instant motor torque. Rear-wheel-based all-wheel-drive (AWD) systems power the majority of newly registered U.S. light trucks, sustaining pull for inter-axle propshafts even as front-wheel-drive sedans retreat. Composite materials are narrowing the cost gap with steel, enabling premium brands to specify hollow carbon-fiber propshafts that cut unsprung mass by up to two-fifths while preserving torsional rigidity. Commercial-vehicle production in ASEAN, Egypt, and South Africa offsets passenger-car headwinds in China and the European Union, anchoring steady global demand for robust steel and high-strength alloy shafts [1]“2024 Africa Automotive Value Chain,” United Nations Conference on Trade and Development, unctad.org.

Key Report Takeaways

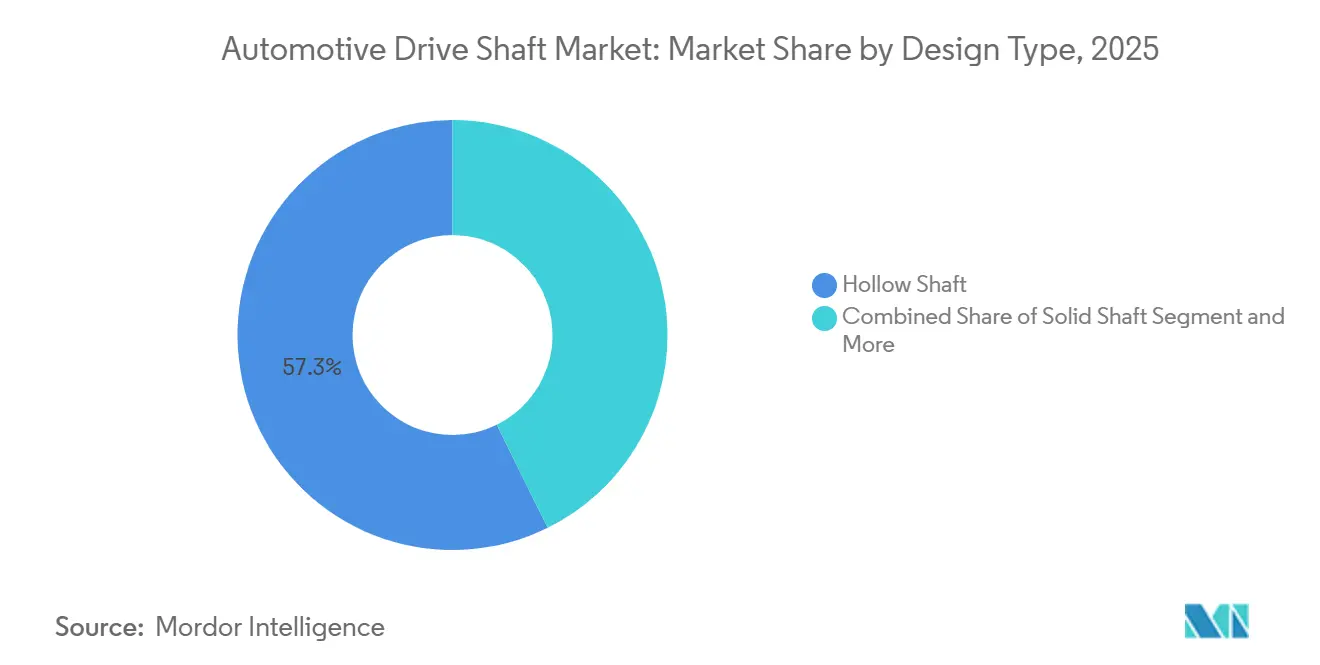

- By design type, hollow shafts led with 57.31% automotive drive shaft market share in 2025, while composite variants are projected to expand at a 5.79% CAGR through 2031.

- By material, conventional steel accounted for 63.35% of sales in 2025; carbon-fiber shafts are expected to climb at a 5.85% CAGR to 2031.

- By position, rear axle shafts captured 67.16% of revenue in 2025, whereas inter-axle/prop-shafts for AWD will advance at 5.91% CAGR over the forecast window.

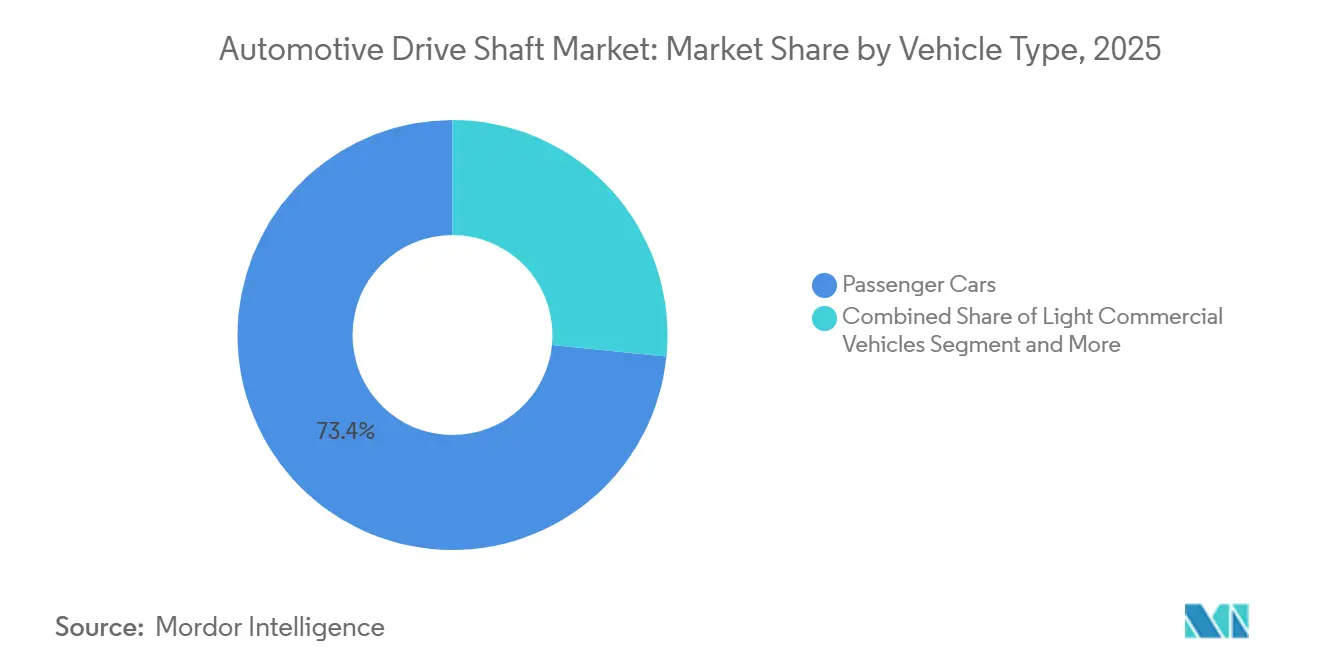

- By vehicle type, passenger cars held a 73.37% share in 2025, and light commercial vehicles are forecast to post a 5.81% CAGR through 2031.

- By powertrain, internal-combustion platforms accounted for 83.31% of the 2025 base, yet BEV applications are on track for a 5.93% CAGR through 2031.

- By sales channel, the OEM segment held 87.18% of revenue in 2025, while the aftermarket is forecast to grow at a 5.83% CAGR through 2031.

- By geography, Asia-Pacific commanded 43.36% of revenue in 2025, while the Middle East & Africa region is projected to grow the fastest at 5.88% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Drive Shaft Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Booming CV production in ASEAN and Africa industrial corridors | +1.0% | ASEAN core (Thailand, Indonesia, Vietnam), Africa (South Africa, Egypt) | Long term (≥ 4 years) |

| E-axle integration in BEVs reduces need for multi-piece shafts | +0.9% | Global, with concentration in China, EU, North America | Medium term (2-4 years) |

| Shift toward rear-wheel-based AWD for SUVs | +0.8% | North America and EU | Medium term (2-4 years) |

| Rapid adoption of carbon-fiber composite shafts | +0.7% | North America and EU, spill-over to Asia Pacific premium segments | Short term (≤ 2 years) |

| Increasing government incentives | +0.6% | North America (IRA), EU (DRIVE35), India (PLI), China (NEV subsidies) | Long term (≥ 4 years) |

| Over-the-air driveline analytics unlocking predictive-maintenance retrofits | +0.5% | Global, early adoption in North America and EU fleet operators | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Booming Commercial-Vehicle Output in ASEAN and Africa

In 2024, JTEKT expanded its Nagoya driveline plant, underscoring supplier confidence in the sustained demand for commercial vehicles. UNCTAD highlights that while Thailand and Indonesia are bolstering their roles as export hubs for medium- and heavy-duty trucks, Egypt and South Africa are ramping up capacity to facilitate intra-African trade, in line with the AfCFTA. Furthermore, the African Export-Import Bank projects a significant increase in the demand for new trucks in the coming years, driven by corridor projects.

E-Axle Integration in BEVs Reduces Need for Multi-Piece Shafts but Drives Demand for High-Precision Lightweight Prop-Shafts

BEV layouts place the motor, inverter, and reduction gear inside a compact e-axle, eliminating two-piece slip-in-tube shafts on many front-wheel-drive platforms while creating new demand for hollow carbon-fiber prop shafts in rear- or dual-motor configurations. ZF’s 2025 electric SUV platform uses a carbon-fiber shaft that removes most of driveline mass while transmitting more than 12,000 Nm per degree of torsional stiffness [2]“Modular e-Drive Platform,” ZF Friedrichshafen AG, zf.com . The U.S. Department of Energy reports a significant fall in carbon-fiber costs since 2020, shrinking the premium over steel to 1.8 times at volume scale. Every kilogram trimmed from the driveline extends BEV range by a minimal rate, making lightweight shafts cheaper than fitting extra battery capacity. OEMs in China and Europe are therefore adopting composite shafts in premium BEVs ahead of volume mid-segment rollout expected post-2027.

Shift Toward Rear-Wheel-Based AWD for SUVs

In the recent model year, a significant portion of new light trucks in the U.S. featured either AWD or 4WD, with most of these using rear-drive-biased systems with a front-to-rear prop shaft, according to EPA data. Meanwhile, in Europe, SUVs accounted for a substantial share of total passenger-car sales. This surge comes as premium brands shift to rear-drive platforms, capitalizing on the benefits of towing and handling. Dana, in the same period, reported a notable increase in Spicer prop-shaft volumes, driven entirely by these SUV programs.

Rapid Adoption of Carbon-Fiber Composite Shafts in Performance and Premium Vehicles

Carbon-fiber-reinforced polymer (CFRP) shafts, once confined to motorsports, are now standard in BMW M3/M4 models and Lamborghini’s Revuelto hybrid, supporting driveline speeds up to 9,000 rpm without resonance. Fraunhofer Institute tests confirm two-fifths higher specific stiffness versus high-strength alloy steel over 10 million load cycles [3]“Resin-Transfer-Molded CFRP Shafts Study,” Fraunhofer Institute for Chemical Technology, fraunhofer.de . Mercedes-Benz made CFRP shafts standard on 2025 E-Class plug-in hybrids, signaling mainstream acceptance among volume premium nameplates. ElringKlinger reported a slight surge in composite-shaft orders during 2024, booking programs for three model-year 2027 launches.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining ICE passenger-car sales | -0.9% | China, EU | Long term (≥ 4 years) |

| Raw-material price volatility | -0.6% | Global, acute in North America and EU due to higher composite adoption | Short term (≤ 2 years) |

| Supply-chain concentration of precision tube-drawing | -0.4% | Global, most acute for Western OEMs dependent on Chinese and Japanese suppliers | Medium term (2-4 years) |

| Warranty-liability risks from composite shaft delamination | -0.3% | North America and EU, driven by extended powertrain warranties | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Declining ICE Passenger-Car Sales in China and EU

In 2024, China saw a significant decline in ICE-only passenger car registrations, while BEVs and plug-in hybrids captured a substantial share of the market. In Europe, under stricter CO₂ regulations, ICE demand fell sharply, reducing the need for two-piece shafts critical to transverse ICE layouts. GKN's conventional driveline unit reported a considerable decrease in volume, even as eDrive shipments increased, underscoring the margin pressures associated with this transition.

Raw-Material Price Volatility

By mid-2024, rising energy-intensive polyacrylonitrile costs, a key ingredient in carbon fiber production, had significantly increased prices. This trend has tightened the profit margins on composite shafts. In 2024, nickel prices rose substantially. This increase not only heightened input costs for alloy steel but also led to a noticeable reduction in margins for Dana's driveline segment. While short-term hedging tools and localized precursor production offer some risk mitigation, suppliers with weaker balance sheets find themselves at heightened vulnerability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Design Type: Hollow Shafts Dominate, Composites Surge

Hollow shafts secured 57.31% of 2025 revenue, balancing cost and mass reduction, while composite designs are forecast to post the fastest 5.79% CAGR due to premium OEM adoption. The automotive drive shaft market size for hollow products is buoyed by mature hydroforming techniques that deliver 2.5 mm wall thickness without exotic materials. Composite-shaft growth hinges on automated fiber placement, which cut per-unit cycle times to 7 minutes in 2024, edging toward cost parity at volumes above 50,000 units a year.

Two-piece slip-in-tube assemblies remain common on front-wheel-drive ICE sedans but shrink alongside that body style. Solid shafts persist in heavy-duty trucks that transmit torque pulses above 8,000 Nm, where hollow designs need walls so thick they lose the weight advantage. BMW’s carbon-fiber shaft in the 2024 M3 handles 9,000 rpm without resonance, exemplifying the performance leap composites offer premium vehicles.

By Material: Steel Leads, Carbon Fiber Accelerates

Conventional steel maintained a 63.35% share in 2025, sustained by global availability and ease of machining, yet carbon-fiber shafts are projected to grow 5.85% a year through 2031. Rising nickel prices stressed alloy-steel economics during 2024, nudging OEMs toward aluminum and CFRP for certain applications. The automotive drive shaft market share for carbon fiber will expand as DOE credits and EU eco-design rules reward mass-efficient drivelines.

High-strength steels containing nickel, chromium, and molybdenum still dominate Class-8 truck shafts that require yield strengths beyond 1,200 MPa. Aluminum extrusions carve out niches in mid-engine sports cars but need larger diameters to match torsional rigidity. Automated recycling pilots underway in Germany and the United States could resolve end-of-life CFRP hurdles by the end of the decade.

By Position Type: Rear Axles Command Share, AWD Prop-Shafts Grow Fastest

Rear axle shafts represented 67.16% of 2025 turnover because pickups, SUVs, and heavy trucks transmit peak torque through the rear end. Inter-axle propshafts will post a 5.91% CAGR as rear-drive-biased AWD spreads across light-truck nameplates. The automotive drive shaft market for AWD propshafts is rising in lockstep with growing wheelbase and towing requirements, especially in North America.

Front axle shafts shrink as transverse-engine sedans retreat and single-motor BEVs jettison discrete half-shafts in favor of stub shafts or direct hubs. Dual-motor BEVs, though, create a fresh class of short, high-torque carbon-fiber shafts connecting in-board motors to wheels to curb unsprung mass.

By Vehicle Type: Passenger Cars Largest, LCVs Fastest

Passenger cars accounted for 73.37% of 2025 shipments; however, light commercial vehicles (LCVs) will expand by 5.81% annually through 2031 as e-commerce boosts van and small-truck production. The automotive drive shaft market size for LCVs benefits from rear- or AWD layouts that retain propshafts even after electrification.

Medium and heavy commercial vehicles maintain a stable base, demanding solid or thick-wall shafts with induction-hardened splines for severe duty. Emerging markets in Africa and ASEAN add fresh demand as corridor projects unlock regional logistics.

By Powertrain: ICE Dominates, BEV Surges

ICE platforms delivered 83.31% of 2025 volume, but BEV applications will register the highest 5.93% CAGR through 2031. Hybrid vehicles keep conventional drivelines, cushioning suppliers during the transition. The automotive drive shaft market size for BEV-specific hollow composite designs is small today, yet poised for rapid scale as dual-motor layouts proliferate.

ICE content erosion remains gradual in North America, where towing and range requirements keep gasoline and diesel pickups in demand. By contrast, China and the EU are pivoting swiftly to e-axles that eliminate multi-piece shafts in compact cars, compressing unit value but adding precision requirements for remaining components.

By Sales Channel: OEM Leads, Aftermarket Gains

OEMs secured 87.18% of 2025 revenue, driven by high capital intensity and zero-defect certification, which tilts the business toward entrenched Tier 1s. The aftermarket is set for a 5.83% CAGR as fleets adopt predictive maintenance and modular retrofits. Neapco and GSP sell composite replacement kits that install without modifying legacy platforms, winning business from operators seeking lightweight benefits at end-of-life overhaul.

Sensor-equipped shafts create new service contracts, balancing longer replacement intervals with higher average selling prices. Latin America and Southeast Asia, where average fleet age exceeds 12 years, underpin steady aftermarket growth through 2031.

Geography Analysis

Asia-Pacific accounted for 43.36% of 2025 sales, anchored by China’s scale and ASEAN truck output, yet growth moderates as Chinese ICE demand falls and BEVs adopt integrated e-axles. India’s incentive program is luring investment in carbon-fiber and aluminum shafts, partly offsetting soft Chinese demand. The Middle East & Africa is forecast to post the fastest CAGR of 5.88% through 2031, driven by AfCFTA transport corridors and Gulf logistics diversification.

North America remains stable due to sustained momentum in SUVs and pickups. EPA data show 61% AWD penetration in light trucks, preserving a large installed base for inter-axle shafts. The U.S. DOE’s USD 12 billion ATVM loans, tied to a domestic-content threshold, spur the reshoring of composite precursor and precision tube-drawing lines.

Europe faces a slight drop in ICE registrations, yet compensates partly with premium BEVs that specify carbon-fiber propshafts. The UK’s DRIVE35 and Germany’s cluster investments aim to close raw-material gaps and push recycling pilots before the anticipated 2028 producer-responsibility rules. South America’s outlook is modest; Brazil’s flex-fuel hybrids keep conventional shafts relevant, while Argentina’s truck factories serve Mercosur routes amid currency volatility.

Competitive Landscape

With the top five players commanding nearly half of OEM revenue, the arena is moderately concentrated, where technology, not price, dictates competition. GKN's significant eDrive expansion in China bolsters its role as a primary supplier of shafts and e-axles for premium BEVs. Meanwhile, Dana, capitalizing on hybrid penetration, safeguards its steel-shaft volumes and reports strong driveline revenue during the period.

Specialists like ElringKlinger and Neapco are carving out niches in CFRP and retrofitting, areas often overlooked by traditional players. Nexteer's strategic investment in EV drivelines highlights a merging of interests with the steering and braking sectors. Today's suppliers must adeptly navigate automated fiber placement, real-time balancing algorithms, and recycling solutions, especially as the EU's circular-economy regulations approach.

Asian manufacturers, including Wanxiang Qianchao, Hyundai Wia, and various Japanese tube-drawers, dominate steel output, playing a pivotal role in global pricing and shielding OEMs from supply disruptions. However, these manufacturers face geopolitical challenges, as tariffs and localization demands push Western automakers to explore sourcing options nearer to their markets.

Automotive Drive Shaft Industry Leaders

Dana Incorporated

GKN PLC (Melrose Industries PLC)

JTEKT Corporation

Hyundai Wia Corporation

American Axle and Manufacturing Holdings Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: American Axle & Manufacturing has inked a deal to acquire Dowlais Group plc, the parent company of GKN Automotive and GKN Powder Metallurgy, for a sum of USD 1.44 billion, a mix of cash and stock. This merger is set to forge a global powerhouse in driveline solutions, boasting anticipated yearly revenues of USD 12 billion. With an eye on achieving USD 300 million in cost synergies, the newly formed entity is poised to dominate driveline technologies, catering to internal combustion engines, hybrids, and electric vehicles alike.

- February 2024: JTEKT developed an ultra-compact product series covering Differential (JUCD), Ball Bearing (JUCB), Conductive Ball Bearing (JUEB), and Oil Seal (JUCS) to reduce eAxle size and weight.

Global Automotive Drive Shaft Market Report Scope

The scope of the report includes Design Type (Hollow Shaft and More), Material (Conventional Steel and More), Position Type (Rear Axle Shafts and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Powertrain/Propulsion (ICE and More), Sales Channel (OEM and Aftermarket), and Geography.

| Hollow Shaft |

| Solid Shaft |

| Two-piece/Slip-in Tube |

| Composite/Carbon-Fiber Shaft |

| Conventional Steel |

| High-Strength Alloy Steel |

| Aluminum |

| Carbon-Fiber/CFRP |

| Rear Axle Shafts |

| Front Axle Shafts |

| Inter-axle/Propeller Shafts for AWD |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Internal Combustion Engine (ICE) |

| Hybrid (HEV and PHEV) |

| Battery Electric Vehicle (BEV) |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Design Type | Hollow Shaft | |

| Solid Shaft | ||

| Two-piece/Slip-in Tube | ||

| Composite/Carbon-Fiber Shaft | ||

| By Material | Conventional Steel | |

| High-Strength Alloy Steel | ||

| Aluminum | ||

| Carbon-Fiber/CFRP | ||

| By Position Type | Rear Axle Shafts | |

| Front Axle Shafts | ||

| Inter-axle/Propeller Shafts for AWD | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Powertrain / Propulsion | Internal Combustion Engine (ICE) | |

| Hybrid (HEV and PHEV) | ||

| Battery Electric Vehicle (BEV) | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What CAGR will global demand for automotive drive shafts likely record between 2026-2031?

The automotive drive shaft market is forecast to expand at a 5.77% CAGR over 2026-2031.

Which design type currently holds the largest revenue share?

Hollow shafts led with 57.31% share in 2025 because they combine mature hydroforming processes with meaningful weight savings.

Why are composite shafts gaining popularity in premium BEVs?

Carbon-fiber shafts deliver up to 40% mass reduction and higher critical-speed margins, directly extending battery-electric vehicle driving range.

Which region is expected to be the fastest-growing market through 2031?

The Middle East & Africa is projected to post the highest regional CAGR at 5.88% thanks to infrastructure-driven commercial-vehicle demand.

How are predictive-maintenance technologies changing aftermarket dynamics?

Sensor-equipped shafts feed vibration data to cloud analytics, enabling fleets to replace components based on condition, lowering emergency repairs but raising average transaction value.

What is the primary raw-material risk for composite-shaft suppliers?

Volatile carbon-fiber precursor prices, which jumped 18% in 2024 due to energy-cost swings, can squeeze supplier margins when OEM pricing is locked in advance.

Page last updated on: