Automotive Fasteners Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 61.37 Billion |

| Market Size (2031) | USD 75.42 Billion |

| Growth Rate (2026 - 2031) | 4.21% CAGR |

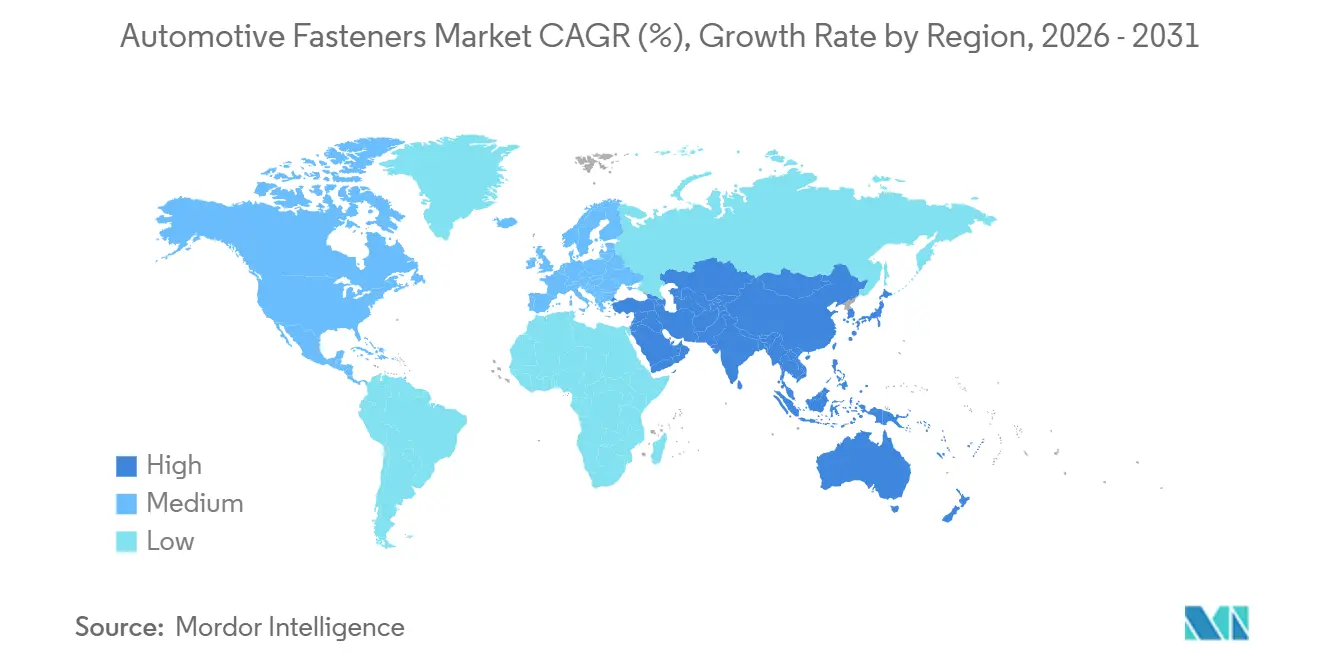

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Fasteners Market Analysis by Mordor Intelligence

The automotive fasteners market size is expected to grow from USD 58.89 billion in 2025 to USD 61.37 billion in 2026 and is forecast to reach USD 75.42 billion by 2031 at a 4.21% CAGR over 2026–2031. The measured expansion reflects a delicate balance in the automotive fasteners market between higher electronics content that multiplies fastening points and battery-electric vehicle (BEV) platforms that remove many powertrain-related joints. Lightweighting targets in the United States and European Union, the rebound of global vehicle production toward multiple units in 2026, and stricter liability rules around safety-critical joints continue to lift value per vehicle even as unit counts trend lower in BEVs. At the same time, adhesive bonding and laser welding are eroding the penetration of mechanical fasteners in premium body structures, while trade-defense duties on Chinese steel fasteners keep raw-material costs volatile for North American assemblers. Consolidation among tier-2 suppliers is accelerating as modular vehicle architectures concentrate procurement with a handful of globally certified vendors.

Key Report Takeaways

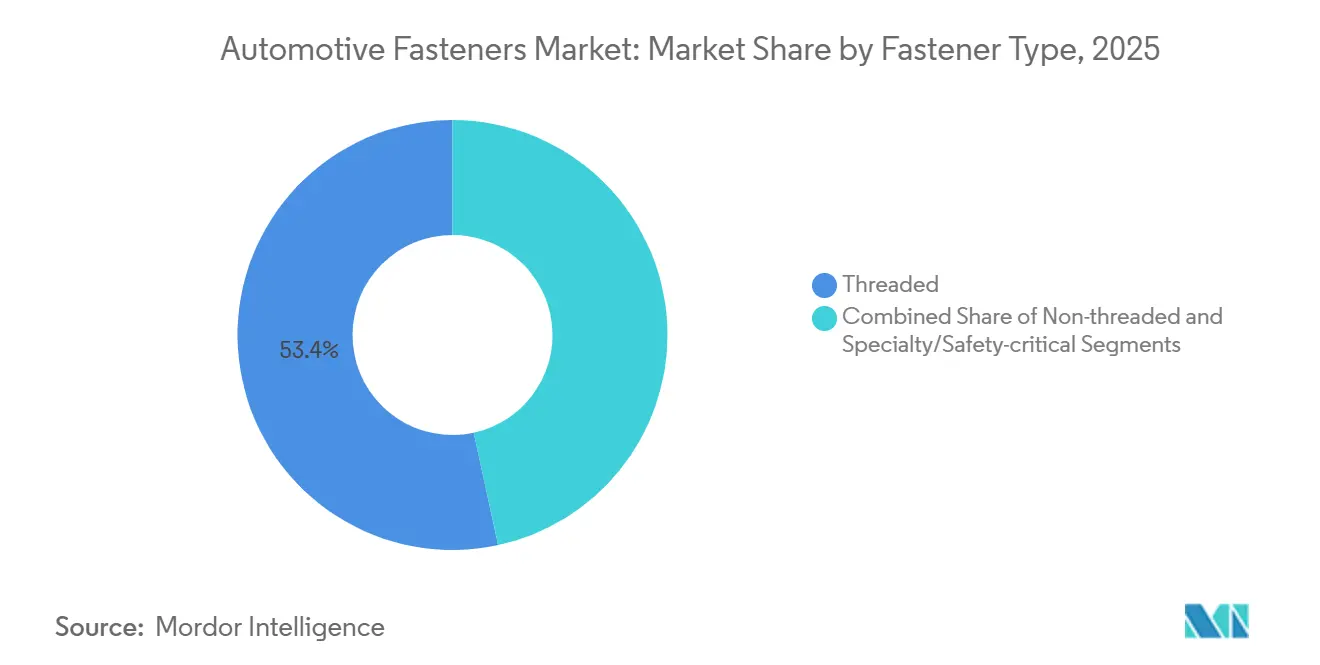

- By fastener type, threaded fasteners led with 53.41% revenue share in 2025; specialty and safety-critical variants are projected to expand at a 4.23% CAGR through 2031.

- By vehicle type, passenger cars accounted for 67.73% of demand in 2025, while two-wheelers recorded the fastest 4.37% CAGR to 2031.

- By propulsion, internal-combustion engine vehicles held 81.15% of the automotive fasteners market share in 2025, while battery-electric vehicles are forecast to expand at a 4.35% CAGR through 2031.

- By function, detachable fasteners captured 77.81% of the automotive fasteners market size in 2025; non-detachable variants are projected to grow at a 4.24% CAGR to 2031.

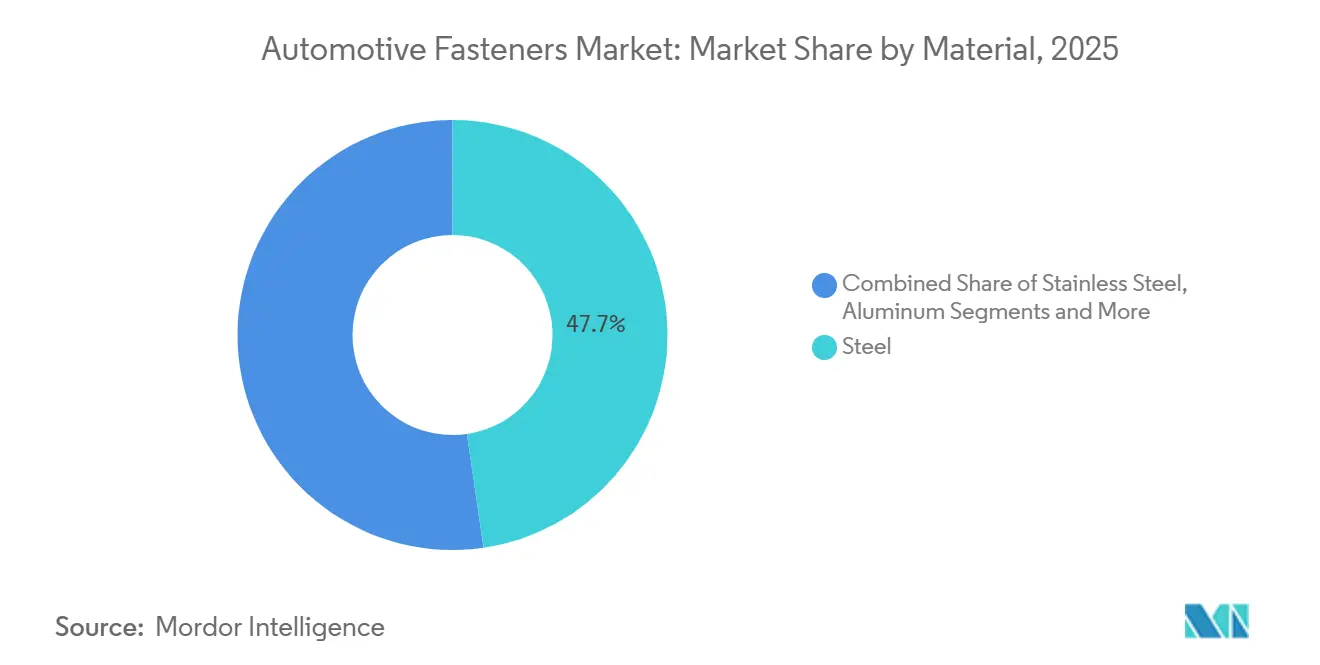

- By material, steel retained a 47.74% share in 2025; aluminum fasteners are forecast to grow at a 4.38% CAGR through 2031.

- By coating, zinc finishes commanded 38.72% share in 2025; organic and dry-film technologies posted the highest 4.41% CAGR to 2031.

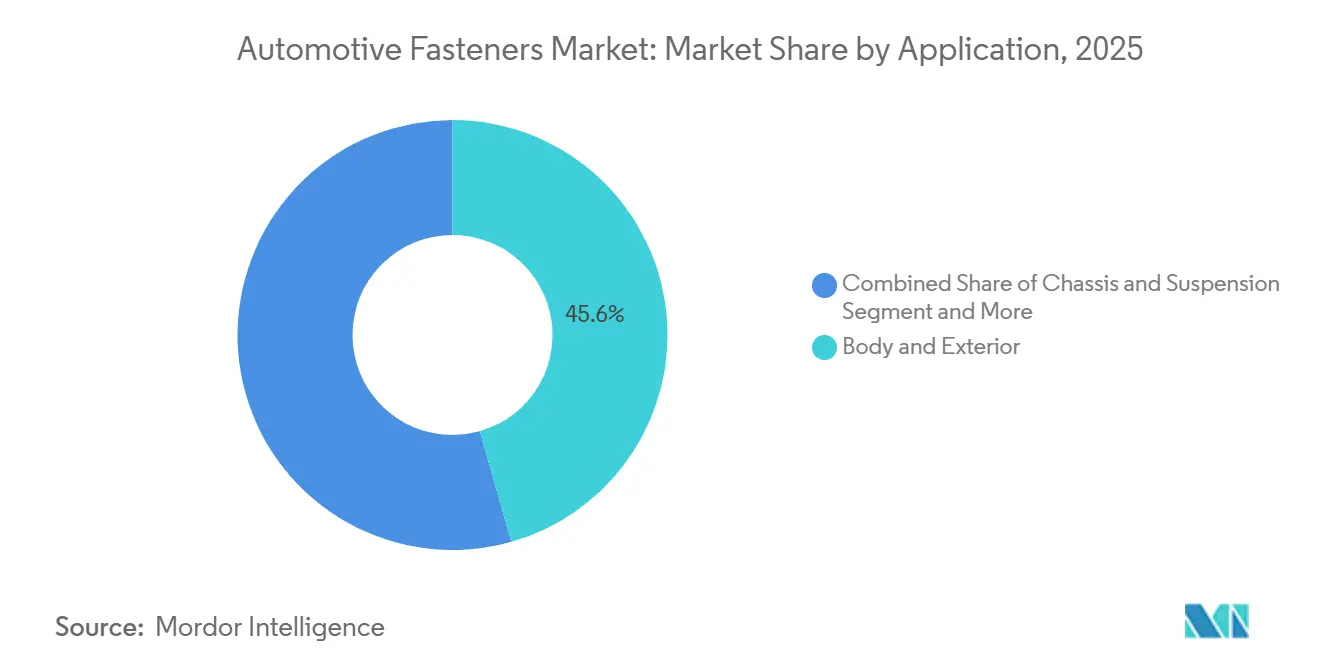

- By application, body and exterior captured 45.56% share in 2025; electronics and electrical joints advance at a 4.27% CAGR to 2031.

- By distribution channel, the OEM segment held 87.83% share in 2025, while the aftermarket rose at a 4.33% CAGR through 2031.

- By region, Asia Pacific dominated with a 37.86% share in 2025 and also delivers the quickest 4.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Fasteners Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lightweighting Accelerating Demand | +0.9% | Europe and North America, spill-over to China | Medium term (2-4 years) |

| Recovery of Global Vehicle Production | +0.8% | Global, with strongest gains in Asia Pacific and North America | Short term (≤ 2 years) |

| Growing Electronics Content Requiring Micro-Fasteners | +0.7% | Global, led by premium segments in Europe and Asia Pacific | Medium term (2-4 years) |

| Modular Vehicle Architectures | +0.6% | Global, concentrated among top 10 OEMs | Long term (≥ 4 years) |

| Aging Vehicle Parc Driving Aftermarket Replacements | +0.5% | North America and Europe | Long term (≥ 4 years) |

| Re-Use and Circular-Economy Mandates Spurring Demand | +0.4% | Europe, early adoption in California and Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lightweighting Accelerating Demand for Advanced Fasteners

In response to the U.S. Corporate Average Fuel Economy (CAFE) updates and the European Union's 2025 fleet-average CO₂ targets, automakers are under pressure to significantly reduce vehicle weight. This focus on weight reduction has brought attention to fasteners, which contribute a small but notable percentage of a vehicle's curb weight. While aluminum bolts offer substantial weight savings compared to steel, they require isolation sleeves or zinc-nickel coatings to prevent galvanic corrosion. These additional measures slightly increase the cost of each fastener. On the other hand, titanium fasteners, which are considerably more expensive than Grade 8.8 steel, are making their way from the world of Formula E racing to high-end luxury electric vehicles (EVs). Here, the appeal lies in the significant weight reduction that justifies the higher cost. Furthermore, the complexity of fastener requirements has increased: a body-in-white that previously relied on a few steel bolt sizes now demands a wider variety of SKUs. These include aluminum, stainless steel, and coated steel options. This expansion has led to a notable rise in working capital needs for tier-2 vendors, with requirements increasing considerably [1]“Corporate Average Fuel Economy Standards,” National Highway Traffic Safety Administration, nhtsa.gov .

Recovery of Global Vehicle Production

In 2024, light-vehicle output experienced a significant rebound and is projected to grow further by 2026. This resurgence signals a restoration of baseline demand in the automotive fasteners market, following the semiconductor shortfall of recent years. During this period, China emerged as a major contributor, with India and Southeast Asia also playing substantial roles in driving demand for fasteners. Together, these regions accounted for a considerable share of the increased demand. Buoyed by an infrastructure stimulus in India and emissions mandates in California, commercial-vehicle production saw notable growth, particularly in heavy-duty segments. This surge benefits Asian suppliers, who boast rapid delivery windows, giving them a distinct advantage over European mills that rely on pre-positioned inventory. While Europe's production remained steady, the global momentum in unit builds serves as a supportive tailwind [2]“2024 Production Statistics,” International Organization of Motor Vehicle Manufacturers, oica.net .

Growing Electronics Content Requiring Micro-Fasteners

In 2025, the average vehicle featured numerous electronic control units, each secured by several micro-fasteners with small thread sizes. Digital cockpits, over-the-air update modules, and Level 2+ ADAS contributed to this increase. Camera and radar housings now utilize stainless-steel or nylon screws, adhering to IP67 standards, slightly raising costs per unit. Premium OEMs, now equipping roof-mounted lidar, require multiple precision fasteners per sensor, ensuring sub-millimeter alignment across a wide temperature range. To ensure traceability, Tier-1 electronics suppliers are vertically integrating their fastener sourcing, consolidating a significant portion of the global micro-fastener volume with a limited number of vendors [3]“ISO 16750 Road Vehicles—Environmental Conditions,” International Organization for Standardization, iso.org .

Modular Vehicle Architectures Boosting Platform-Based Demand

Volkswagen's MEB, Stellantis's STLA, and Geely's SEA platforms are standardizing a significant portion of fastener part numbers across various models. This strategy allows them to make bulk purchases, achieving notable cost savings. Furthermore, validated crash-test and corrosion data are now seamlessly transferring between derivatives, significantly reducing development times for new variants. However, this has led to a decline in supplier diversity. As tenders increasingly demand a global footprint and ISO/TS 22163 certification, smaller regional players find themselves leaning towards consolidation.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV Architecture Reducing Fastener Count Per Vehicle | -0.6% | Global, most pronounced in Europe and China | Medium term (2-4 years) |

| Adhesive Bonding and Laser Welding Substitution | -0.5% | Europe and North America, premium segments | Long term (≥ 4 years) |

| Raw-Material Price Volatility and Supply Disruptions | -0.3% | Global | Short term (≤ 2 years) |

| Trade-Defense Measures and Anti-Dumping Duties Disrupting Supply Chains | -0.2% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

EV Architecture Reducing Fastener Count Per Vehicle

Battery-electric vehicles (BEVs) shed components like engine blocks, transmissions, exhaust systems, and fuel tanks. This change results in a significant reduction in the number of fasteners per unit when compared to traditional internal-combustion vehicles. For instance, Tesla’s Model Y employs fewer fasteners than a gasoline crossover, marking a notable reduction. Additionally, structural battery designs further decrease the number of fasteners required. While the value of high-strength Grade 10.9 bolts in BEVs has increased, partially compensating for the reduced volume, the overall impact on the automotive fasteners market remains negative.

Adhesive Bonding and Laser Welding Substitution

In 2024, Audi's e-tron GT utilizes structural adhesives to bond a significant portion of its body joints, a move that replaces numerous rivets and bolts and considerably reduces assembly time. By employing laser-welded tailored blanks, Audi eliminates flanges and overlaps, leading to a notable reduction in fastener demand for roof panels and door frames. While concerns over repair complexity and recyclability restrict adhesive usage to premium segments, this trend continues to exert significant pressure on the volumes of commodity bolts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Fastener Type: Safety-Critical Variants Command Premiums

Threaded fasteners held 53.41% of 2025 revenue, underlining their versatility in chassis, powertrain, and interior systems. Specialty and safety-critical units, including torque-to-yield bolts and self-locking nuts, will post a 4.23% CAGR to 2031 as stringent crash-test protocols make them indispensable for seat-belt anchorages and battery-pack retention. Commodity threaded parts face gradual volume erosion in BEVs, yet their absolute demand in hybrids and traditional internal-combustion cars keeps the automotive fasteners market size substantial for this segment.

Specialty fasteners command 2–5× higher prices by integrating thread-locking compounds or captive washers that cut warranty claims and line rework. Non-threaded clips and rivets, while essential in interior trim, grow slower as adhesives gain favor in premium body-in-white. The premium attached to specialty items shields margins even in a platform-standardized procurement environment.

By Vehicle Type: Two-Wheelers Outpace Passenger Cars

Passenger cars consumed 67.73% of all units in 2025, reflecting higher fastener intensity and global builds of 68 million vehicles. Two-wheelers, however, will log the fastest 4.37% CAGR through 2031 as India and China electrify scooter fleets, adding threaded bolts for battery enclosures and motor mounts. Light commercial vehicles and heavy trucks together account for 18% of volume, supported by last-mile delivery electrification.

Average fastener content per electric scooter is climbing exponentially, while electric passenger cars lose 220–280 bolts versus ICE models. Fleet operators adopting modular cargo bed designs standardize fastener SKUs across 3-5 payload classes, lowering parts inventories by up to two-fifths.

By Propulsion: BEVs Reshape Mix Despite Lower Counts

Internal-combustion vehicles still generated 81.15% of fastener demand in 2025, yet BEVs will expand at a 4.35% CAGR due to zero-emission rules in China and the EU. Although BEVs use fewer fasteners per vehicle, the shift toward Grade 10.9 bolts and stainless-steel variants lifts value per unit. Hybrid cars occupy a transitional niche, keeping most ICE fasteners while adding 40–60 new battery-related joints.

Tesla’s 4680 pack, for instance, employs 112 M8 zinc-nickel-coated bolts torqued to 25 Nm to prevent hydrogen embrittlement, illustrating value-rich opportunities even as counts decline.

By Function: Detachable Joints Align With Circular Economy

Detachable fasteners captured 77.81% share in 2025, cementing their role in serviceable areas and supporting circular-economy targets. The updated EU End-of-Life Vehicles Directive discourages permanent joints, bolstering detachable solutions in interiors and electronics. Non-detachable options - self-piercing rivets, clinch nuts - still grow at 4.24% due to their 8–12 second assembly-time advantage in high-volume body shops.

Luxury models are incorporating a high percentage of detachable joints to enhance repairability. In contrast, mass-market vehicles include a comparatively lower percentage, prioritizing material cost savings. With proposed California regulations on battery pack recyclability, the adoption of detachable joints in U.S. BEVs could reach significantly higher levels, starting in 2027.

By Material: Aluminum Fasteners Gain Despite Corrosion Hurdles

Steel remained the workhorse at 47.74% share in 2025, but aluminum fasteners will clock a 4.38% CAGR as every vehicle weight reduction yields a minimum fuel-efficiency gain. Stainless steel retains an 18% share for corrosive underbody and battery-pack areas, while brass stays niche in electrical terminals.

Aluminum’s weight advantage comes with galvanic-corrosion risks; zinc-nickel or ceramic isolation sleeves add USD 0.08–0.15 per unit. Still, European and Californian regulations make aluminum substitutions attractive in non-structural brackets where tensile loads stay below 4 kN.

By Coating and Finish: Organic Films Replace Hexavalent Chromium

Zinc coatings led at 38.72% share in 2025, yet organic and dry-film finishes will rise at 4.41% CAGR after REACH banned hexavalent chromium in 2024. Geomet's zinc-flake systems provide exceptional salt-spray resistance, aligning with OEMs' long-term corrosion warranties. Meanwhile, dry-film lubricants significantly reduce friction coefficients, effectively averting thread galling during automated assembly.

Nickel and chrome finishes maintain their premium status, whether for decorative purposes or in areas prone to severe corrosion. Phosphate coatings hold a notable market share by ensuring paint adhesion for body-in-white studs heading to e-coat lines.

By Application: Electronics Fasteners Multiply with ADAS Uptake

Body and exterior systems commanded a 45.56% share in 2025, but electronics and electrical joints will accelerate at a 4.27% CAGR as radar, lidar, and camera modules add 30–50 micro-fasteners per vehicle. Battery-pack mounting in BEVs strengthens the chassis and suspension segment, which holds a significant share, helping to counterbalance a slight decline in powertrain applications.

Camera housings require stainless-steel or nylon screws, torqued to a specific level, adhering to ISO vibration standards. Audi’s e-tron GT, by significantly reducing body fasteners through adhesive use, showcases the transformative impact of structural bonding on the automotive fasteners market, especially in exterior segments.

By Distribution Channel: Aftermarket Rises with Vehicle Age

OEMs purchased 87.83% of fasteners in 2025, but the aftermarket will expand at a 4.33% CAGR as U.S. vehicle age reaches 12.6 years and European fleets near 12.3 years. Smaller production runs and retail margins push aftermarket prices significantly above their OEM counterparts.

Platforms like McMaster-Carr are making specialty torque-to-yield bolts more accessible, leading to a noticeable increase in retail demand. While BEVs have fewer service items, which temper aftermarket volumes per vehicle, their fleet share is expected to remain relatively low until 2031, thereby mitigating the impact.

Geography Analysis

Asia Pacific held 37.86% of global demand in 2025 and is expected to grow at a 4.31% CAGR to 2031. China's significant automotive output, coupled with India's rapid growth, underscores the region's automotive prowess. Southeast Asia, with its growing vehicle production, is becoming a magnet for new fastener plants as OEMs pivot their sourcing strategies away from China. Notably, domestic suppliers in China are now meeting nearly half of local OEM demands, boasting swift delivery times and competitive pricing compared to their European counterparts. India's booming electric two-wheeler market has further solidified Asia's dominance in the automotive fasteners arena.

Europe, which represented a substantial portion of global demand in 2025, experienced a slower growth rate, attributed to production stagnation and a shift by premium brands towards adhesive bonding. In Germany, with its significant automotive output, a large volume of fasteners was consumed, predominantly high-strength grades supplied by industry leaders KAMAX and Bossard. The revision of the End-of-Life Vehicles Directive continues to favor detachable joints, bolstering the demand for threaded fasteners, even as body-shop volumes wane. Meanwhile, Stellantis's consolidation of legacy brands under the STLA platform has led to a notable reduction in SKUs and a more streamlined supplier roster.

North America, accounting for a significant share of global demand in 2025, is set to achieve steady growth through 2031. U.S. production of light trucks and SUVs has been robust, with the Inflation Reduction Act's content stipulations channeling fastener orders towards domestic suppliers like Illinois Tool Works and Stanley Engineered Fastening. Additionally, anti-dumping duties have shifted imports from China to Vietnam and Mexico, resulting in increased landed costs. Mexico's burgeoning automotive output has attracted significant investment in new fastener capacity, while Ontario's plants in Canada are heavily dependent on efficient cross-border supply chains.

Competitive Landscape

In 2025, the top suppliers accounted for a significant portion of global revenue, highlighting a moderately fragmented market. As OEMs increasingly prefer vendors with a global presence and relevant certifications, platform standardization is driving consolidation. Deployed in 2024, Illinois Tool Works’ automated torque-verification system significantly reduced rework and now commands a notable price premium. Meanwhile, LISI Group’s foray into net-shape cold-forming not only reduced per-unit costs but also secured a long-term contract for fasteners.

Asian players like Shanghai Tianbao are capitalizing on rapid lead times and substantial cost advantages, successfully capturing market share from their European counterparts. This shift has spurred near-shoring and automation investments, significantly reducing labor's contribution to costs. In niche markets, suppliers are commanding considerably higher prices for specialized products like battery-specific torque-to-yield bolts and IP67-rated micro-fasteners tailored for ADAS modules. While patent activities in self-piercing rivets and friction-stir welding signal a potential structural upheaval, the capital-intensive nature of these innovations has ensured that a large portion of the automotive fasteners market will remain dependent on mechanical joints for the foreseeable future.

Regulatory compliance has emerged as a significant competitive advantage. Vendors with credentials like ISO 9001, IATF 16949, and REACH not only enjoy notable price premiums but also gain pre-qualification for global tenders. In contrast, those lacking such certifications find themselves relegated to aftermarket niches or exiting commodity segments, especially in the face of raw-material price fluctuations.

Automotive Fasteners Industry Leaders

Illinois Tool Works Inc.

LISI Group

Nifco Inc.

Stanley Black & Decker Inc. (Stanley Engineered Fastening)

SFS Group AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Fontana Gruppo agreed to acquire a 60% stake in India-based Right Tight Fasteners for around INR 1,000 crore, strengthening its position in the country’s expanding vehicle-manufacturing hub.

- January 2025: Bossard Group completed the takeover of Ferdinand Gross, boosting European coverage in high-precision automotive fasteners.

- March 2024: Auto Fasteners Ltd secured an additional 15,000 sq ft at Sucham Park, Southam, extending its UK production footprint to meet growing international demand.

Global Automotive Fasteners Market Report Scope

Automotive fasteners include nuts, bolts, screws, retainers, spring clips, and washers. The main types of automotive fasteners are nuts, bolts, and washers.

The automotive fasteners market is segmented by fastener type, vehicle type, vehicle propulsion type, function, material type, and geography. By fastener type, the market is segmented as threaded and non-threaded. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By vehicle propulsion type, the market is segmented into IC engine vehicles and electric vehicles. By function, the market is segmented into detachable and non-detachable. By material type, the market is segmented into iron, steel, aluminum, brass, and plastic. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World.

The market sizes and forecasts for the market are provided in terms of value (USD) for all the above segments.

| Threaded |

| Non-threaded |

| Specialty/Safety-critical |

| Two-Wheelers |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Off-Highway Vehicles |

| IC Engine Vehicles |

| Battery Electric Vehicles |

| Hybrid and Fuel-Cell Vehicles |

| Detachable |

| Non-detachable |

| Steel |

| Stainless Steel |

| Aluminum |

| Brass |

| Plastics and Composites |

| Zinc |

| Phosphate |

| Nickel and Chrome |

| Organic and Dry Film |

| Body and Exterior |

| Chassis and Suspension |

| Powertrain and Engine |

| Interior and Seating |

| Electronics and Electrical |

| OEM |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Turkey | |

| Rest of Middle East and Africa |

| By Fastener Type | Threaded | |

| Non-threaded | ||

| Specialty/Safety-critical | ||

| By Vehicle Type | Two-Wheelers | |

| Passenger Cars | ||

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Off-Highway Vehicles | ||

| By Propulsion | IC Engine Vehicles | |

| Battery Electric Vehicles | ||

| Hybrid and Fuel-Cell Vehicles | ||

| By Function | Detachable | |

| Non-detachable | ||

| By Material | Steel | |

| Stainless Steel | ||

| Aluminum | ||

| Brass | ||

| Plastics and Composites | ||

| By Coating/Finish | Zinc | |

| Phosphate | ||

| Nickel and Chrome | ||

| Organic and Dry Film | ||

| By Application | Body and Exterior | |

| Chassis and Suspension | ||

| Powertrain and Engine | ||

| Interior and Seating | ||

| Electronics and Electrical | ||

| By Distribution Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current value of the automotive fasteners market?

The market is valued at USD 61.37 billion in 2026 and is projected to climb to USD 75.42 billion by 2031.

How fast is the demand for aluminum fasteners growing?

Aluminum fasteners are expected to expand at a 4.38% CAGR through 2031 as OEMs pursue lightweighting targets.

Which region leads global demand?

Asia Pacific accounted for 37.86% of 2025 consumption and is projected to deliver the quickest 4.31% CAGR through 2031.

How are electric vehicles affecting fastener consumption?

BEVs remove 220–280 traditional fasteners per vehicle but add value-rich Grade 10.9 bolts for battery packs, reshaping the mix rather than eliminating demand.

What impact do trade-defense duties have on supply chains?

U.S. antidumping duties of up to 118% on Chinese steel fasteners are shifting procurement to Vietnam and Taiwan, raising landed costs by 12–18% for North American buyers.

Which coatings are replacing hexavalent chromium zinc plating?

Organic zinc-flake and dry-film lubricants are gaining favor, delivering 1,000–1,500 hours of salt-spray resistance while meeting REACH compliance.

Page last updated on: