Passenger Car Accessories Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

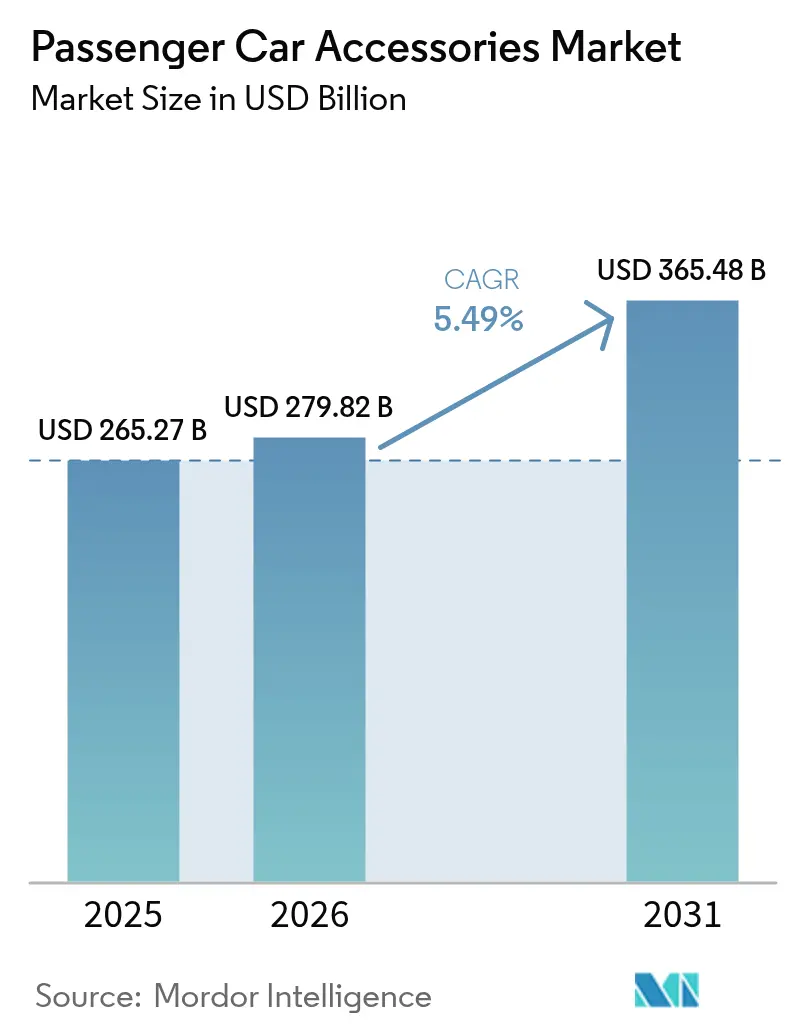

| Market Size (2026) | USD 279.82 Billion |

| Market Size (2031) | USD 365.48 Billion |

| Growth Rate (2026 - 2031) | 5.49% CAGR |

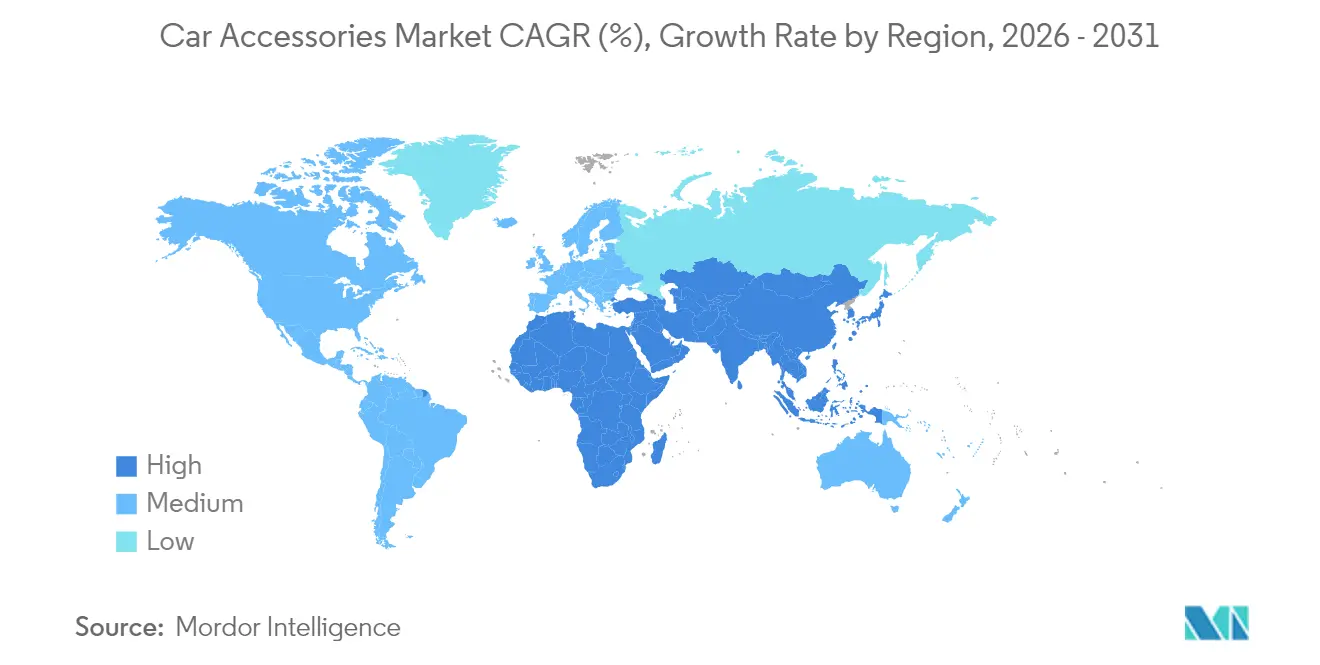

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

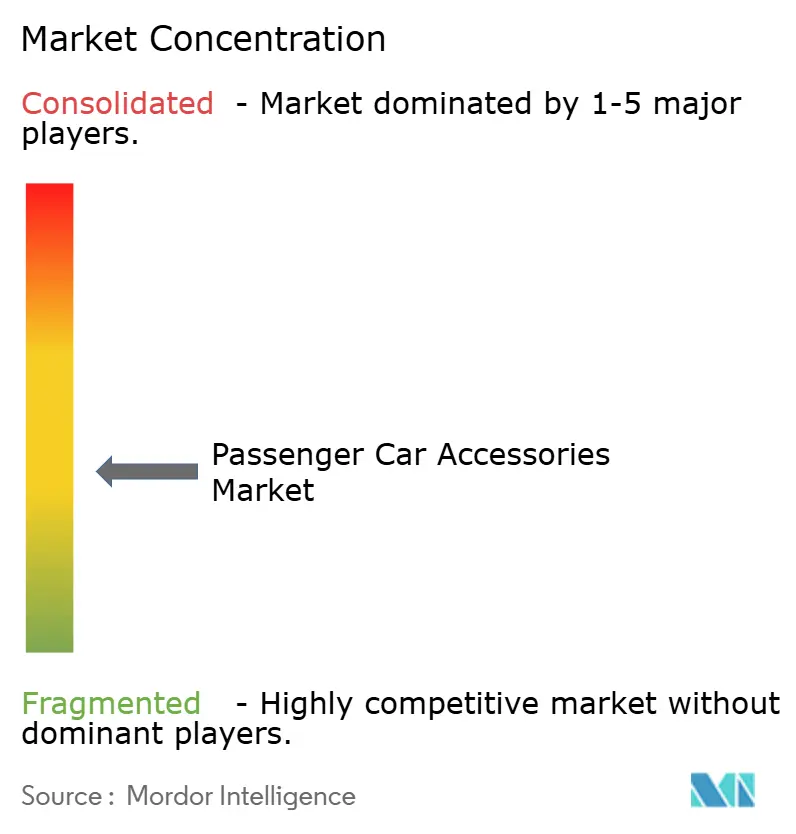

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Passenger Car Accessories Market Analysis by Mordor Intelligence

The passenger car accessories market size was valued at USD 265.27 billion in 2025 and estimated to grow from USD 279.82 billion in 2026 to reach USD 365.48 billion by 2031, at a CAGR of 5.49% during the forecast period (2026-2031). Steady growth stems from rising SUV and crossover sales, e-commerce-led aftermarket expansion, and OEM moves toward subscription-based connected-car features. Asia-Pacific retains demand leadership, reflecting China’s component manufacturing scale and India’s rapid electric-mobility adoption. Interior upgrades, especially infotainment and smart-surface solutions, drive recurring revenue, while exterior categories gain momentum from lifestyle modifications and lightweight EV-compatible designs. Competitive intensity remains moderate as platform consolidations, ADAS-ready accessories, and sustainable material innovations reshape value pools within the wider car accessories market.

Key Report Takeaways

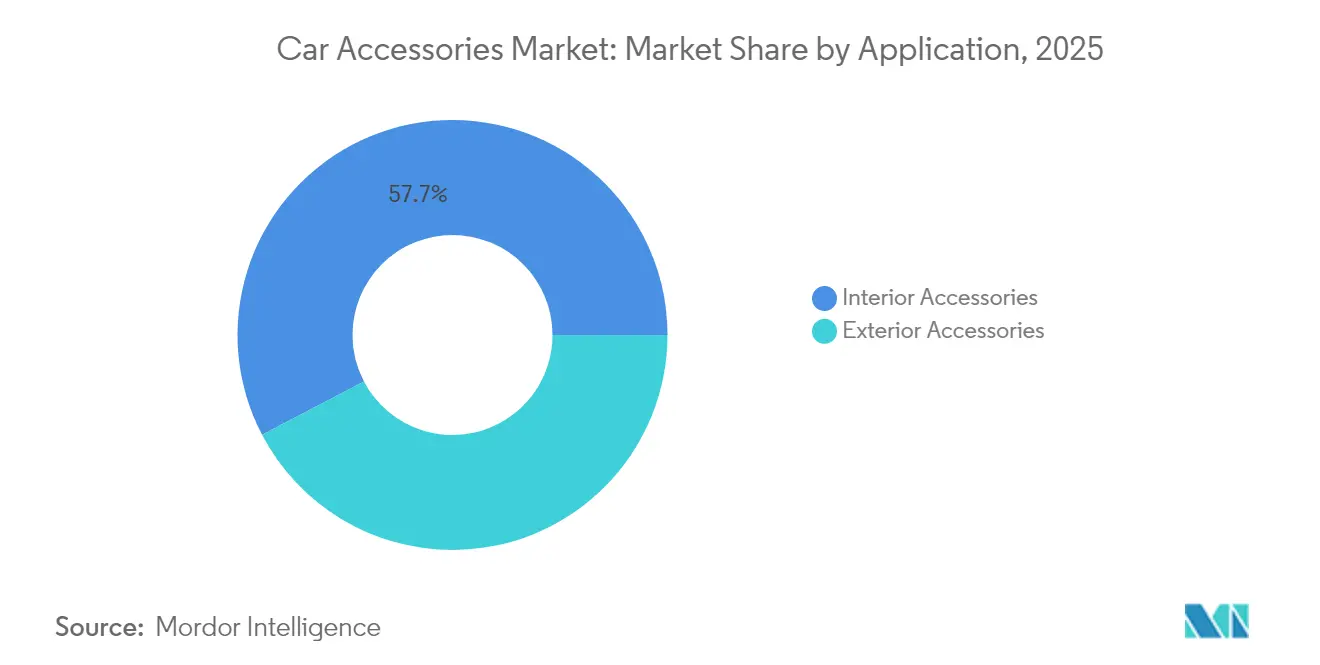

- By application, interior accessories led with 57.68% revenue share in 2025; exterior accessories are projected to grow at an 8.18% CAGR through 2031.

- By sales channel, the OEM segment held 75.63% of the car accessories market share in 2025, while the aftermarket is set to expand at a 9.71% CAGR to 2031.

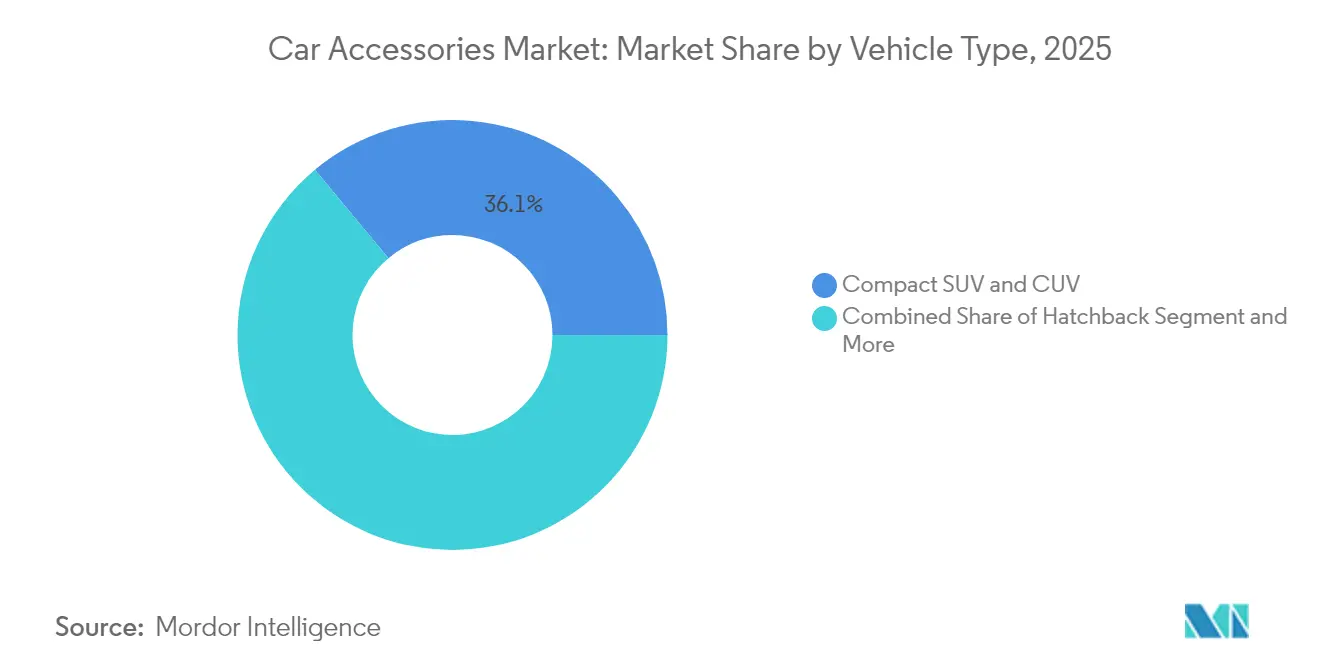

- By vehicle type, compact and mid-size SUVs and CUVs captured 36.05% of the car accessories market size in 2025; electric vehicles are forecast to record the fastest 8.61% CAGR during 2026-2031.

- By material, plastic maintained 49.54% share of the overall market in 2025, whereas vegan and synthetic leather alternatives are expected to rise at an 8.08% CAGR.

- By geography, Asia-Pacific commanded 63.78% revenue share in 2025 and is projected to post the strongest 7.63% CAGR over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Passenger Car Accessories Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in SUV and CUV Accessorizing | +1.2% | Global, strongest in North America and APAC | Medium term (2-4 years) |

| Growth of E-Commerce-Led Aftermarket | +1.1% | Global, led by North America and China | Short term (≤ 2 years) |

| OEM Focus On Connected-Car Upgrade Cycles | +0.9% | Global, premium segments first | Medium term (2-4 years) |

| Rising Average Vehicle Age In Core Markets | +0.8% | North America and Europe primarily | Long term (≥ 4 years) |

| Lightweight Modular Accessories For EV Range-Boost | +0.7% | APAC core, spill-over to EU and North America | Long term (≥ 4 years) |

| Smart Interior Surfaces (HMI/Gesture) Adoption | +0.6% | Global, luxury trickle-down pattern | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in SUV and CUV Accessorizing

Sport-utility and crossover platforms increasingly dictate accessory demand, spurring the development of roof carriers, running boards, and protective cladding that sedans rarely require. Compact SUVs in urban areas accelerate personalization needs, while Chinese consumers now mirror Western accessory trends. The shift lifts exterior-category revenue yet forces ADAS-compatible redesigns so sensors remain unobstructed. Accessory suppliers certifying sensor integrity products secure premium positioning across the broader car accessories market[1]“Emerging Trends Among SUV Enthusiasts,” Specialty Equipment Market Association, sema.org.

Growth of E-Commerce-Led Aftermarket

Online parts portals outpace brick-and-mortar growth as AI-powered fitment tools boost conversion and reduce returns. NAPA Online alone processed 217,385 transactions in May 2025, evidencing scale economics for pure-play sites. Global reach helps smaller brands bypass distributors and tap long-tail demand. Yet digital marketplaces also facilitate counterfeit flow, prompting authentication tech investments that preserve trust and protect the expanding online slice of the car accessories market.

OEM Focus on Connected-Car Upgrade Cycles

Manufacturers now treat accessories as software-enabled services rather than one-time hardware sales. Panasonic Automotive’s Neuron compute platform reduces control units by up to 80% and supports over-the-air feature activation, creating subscription revenue streams[2]“Neuron High-Performance Compute Platform,” Panasonic Corporation, panasonic.com. Harman forecasts infotainment and connected services to become the second-largest automotive software pool by 2030, underscoring this pivot. Early adoption in premium lines will cascade to volume models, though tighter OEM control may restrict independent aftermarket coding access, reshaping competitive boundaries across the car accessories market.

Rising Average Vehicle Age

The average U.S. vehicle is 12.5 years old, pushing owners to upgrade interiors, electronics, and protective products rather than purchase new cars. Extended ownership windows energize replacement cycles for floor mats, seat covers, and lighting kits, especially as repair costs climb. Similar patterns emerge in Europe, where older fleets transition from dealer service to independent channels once warranties expire. This demographic favors interior comfort and connectivity add-ons, delivering steady demand that offsets cyclical new-car sales within the car accessories industry.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and Grey-Market Parts Penetration | -0.9% | Global, strongest impact in emerging markets | Short term (≤ 2 years) |

| Reduced Parts Count In BEVs Curbing Demand | -0.8% | APAC and EU primarily, spreading globally | Long term (≥ 4 years) |

| Safety-Critical ADAS Sensors Limiting Exterior Mods | -0.7% | Global, led by EU and North America regulations | Medium term (2-4 years) |

| Raw-Material Price Volatility (Plastics and Alloys) | -0.5% | Global, manufacturing-heavy regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Counterfeit and Grey-Market Parts Penetration

Illicit parts erode consumer confidence and trigger safety recalls. The industry-led “Brakes on Fakes” campaign highlights risks from sub-standard brake components that can fail under load[3]“Brakes on Fakes Initiative,” Auto Care Association, autocare.org. E-commerce anonymity worsens exposure, particularly in price-sensitive regions. Blockchain-based provenance systems and QR-code authentication on packaging aim to curb the issue, but implementation costs strain small suppliers.

Safety-Critical ADAS Sensors Limiting Exterior Mods

Mandatory safety suites such as emergency lane-keeping and automatic braking require unobstructed radar and camera zones. The EU’s General Safety Regulation II applies to all new vehicles from July 2024, effectively outlawing bull bars or grille guards that block sensor grids[4]“Understanding EU General Safety Regulation II,” Continental AG, continental.com. Accessory makers now engineer ADAS-friendly bumper covers and badge mounts, yet redesign cycles increase production costs and lengthen time-to-market for exterior innovations.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Interior Dominance Meets Exterior Innovation

Interior accessories controlled 57.68% of the car accessories market in 2025 as consumers prioritized infotainment upgrades, premium seat coverings, and electronic security systems. The segment benefits from OEM moves toward software-defined vehicles that allow seamless integration of new features via over-the-air updates. Flooring products, thermal-comfort seat covers, and AI-enhanced ambient lighting sustain recurring sales throughout extended vehicle lifecycles.

Exterior accessories remain the fastest-growing slice at an 8.18% CAGR. LED lighting kits, aerodynamic body enhancements, and multi-sport roof rack systems appeal to SUV owners seeking personalization and utility. Demand is especially strong where off-road tourism and active lifestyle demographics intersect. Increasing EV adoption steers design toward lightweight composites that avoid range penalties, ensuring the car accessories market size for exterior products expands faster than the average.

By Sales Channel: OEM Control Versus Aftermarket Agility

The OEM channel retained 75.63% market share in 2025 by bundling factory-approved parts with warranty protection. Automakers leverage connected-car telemetry to market service plans and subscription-based accessory features directly through infotainment screens. This integrated approach locks consumers into branded ecosystems and helps stabilize margins across the car accessories market.

The aftermarket grows at a brisk 9.71% CAGR, propelled by e-commerce convenience, broader assortment, and competitive pricing. AI-driven inventory tools allow independents to mirror OEM-quality fitment confidence. The car accessories industry, therefore, sees a slow rebalancing as digital platforms lower entry barriers for niche brands and encourage cross-border sales, even while OEMs defend their share through software locks and proprietary data protocols.

By Vehicle Type: SUV Platforms Drive Accessorization Trends

Compact and mid-size SUVs represented 36.05% of the car accessories market size in 2025, underlining consumers’ shift toward versatile vehicles that accommodate roof storage, step boards, and protective cladding. Accessory bundling at dealerships further amplifies SUV attachment rates, especially in North America and China.

Electric vehicles deliver the swiftest 8.61% CAGR through 2031. Lightweight modular components, aerodynamic wheel covers, and specialized charging-port protectors cater to efficiency-minded owners. Suppliers that certify electromagnetic compatibility and maintain battery-cooling airflow secure early-mover advantages, reinforcing EV-centric diversification across the wider car accessories market.

By Material: Sustainability Reshapes Supply Chains

Plastic retained a 49.54% share in 2025 due to cost-effective molding and integration capabilities that support complex interior geometries and exterior styling parts. Biobased resins and recycled polycarbonate advances introduce circular-economy credentials without sacrificing performance or price.

Vegan and synthetic leather alternatives expand at an 8.08% CAGR as carmakers and consumers align on animal-free and lower-carbon materials. Covestro’s INSQIN water-based polyurethane coating cuts water use by 95% and CO2 emissions by 45%, positioning sustainable trim surfaces as mainstream options. Market adoption is fastest in premium EVs, then cascades to volume segments as cost curves improve, lifting the car accessories market share of eco-friendly upholstery solutions.

Geography Analysis

Asia-Pacific held 63.78% revenue in 2025 and is projected to grow 7.63% CAGR through 2031. China’s component manufacturing output expands exponentially and feeds OEM and aftermarket pipelines. India’s electric-mobility push widens demand for lightweight modular add-ons suited to local road conditions. Japan contributes design and HMI leadership, while South Korea supports supply-chain depth for display and battery integration. ASEAN markets ride rising disposable incomes and online retail proliferation, which enlarges the car accessories market.

North America remains a vital profit center. Aging fleets and a strong DIY culture spur floor mats, lighting, and towing equipment sales. Although differing safety regulations fragment accessory homologation, Canada and Mexico anchor manufacturing and distribution corridors.

Europe confronts regulatory complexity but leverages engineering heritage. The EU’s General Safety Regulation II curbs certain exterior add-ons but fosters a premium for ADAS-compatible solutions that preserve sensor integrity. Continental’s 2024 aftermarket expansion added 700 SKUs, raising European market coverage by 50%. Germany and the United Kingdom dominate demand for premium interior tech, while France, Italy, and Spain emphasize cost-effective replacements. Eastern Europe’s role as a manufacturing hub grows as suppliers seek proximity to EU markets under resilient trade agreements.

Competitive Landscape

The car accessories market is moderately fragmented. Top players pursue scale and technology depth via acquisitions and partnerships, while hundreds of regional specialists target niche categories. FORVIA’s merger of Faurecia and HELLA unites seating, lighting, and electronics platforms, enabling bundled cockpit solutions for OEM programs. Panasonic’s strategic pact with Arm to standardize software-defined vehicle architecture reduces development time for connected accessories.

Aftermarket distributors also consolidate. Carlyle’s purchase of Worldpac from Advance Auto Parts in August 2024 reshaped parts logistics and intensified competition for installer loyalty. Suppliers invest in AI personalization engines that tailor accessory recommendations based on driving data, reinforcing customer lock-in. Yet, entrepreneurial brands flourish by launching ADAS-ready grille inserts, sustainable seat fabrics, or EV-specific cargo kits on global e-commerce platforms, highlighting persistent entry pathways within the car accessories industry.

Mergers and acquisitions occurred in reccent years were aimed at securing connected-tech capability, vertical integration, or regional expansion. Strategic moves such as Continental’s impending spin-off of its Automotive business and Adient’s automation pact with Paslin illustrate focus on agility and cost optimization as profit pools migrate from mechanical components to software-enabled services.

Passenger Car Accessories Industry Leaders

Lear Corporation

Faurecia SE

Continental AG

Denso Corporation

Panasonic Holdings Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Panasonic Automotive Systems and Qualcomm expanded their collaboration to deploy Snapdragon Cockpit Elite with generative AI multimedia in vehicles starting 2026.

- November 2024: Panasonic Automotive Systems and Arm partnered to align software-defined vehicle architectures using VirtIO for zonal computing parity.

- September 2024: Continental launched a 700-SKU aftermarket expansion covering ADAS sensors, steering, and high-pressure fuel pumps.

- May 2024: Genuine Parts Company bought Motor Parts & Equipment Corporation, adding 181 NAPA stores to its network.

Global Passenger Car Accessories Market Report Scope

An automobile accessory is defined as a supplementary component or kit which improves the exterior appeal and interior functionality of a passenger vehicle, thus improving the overall comfort and convenience levels for the occupants of the passenger vehicle.

The Passenger Car Accessories Market is segmented by Application (Interior Accessories (Infotainment System, Floor Carpets and Mats, Seat Covers, Electrical Systems, Security Systems, and Others) and Exterior accessories (LED Lights, Alloy Wheels, Body Kits, Racks, Window Films, Covers, Crash Guards, and Others)), by Sales Channel (OEM and Aftermarket), and by Geography (North America, Europe, Asia-Pacific, and Rest of the World).

| Interior Accessories | Infotainment Systems |

| Floor Carpets and Mats | |

| Seat Covers | |

| Electrical and Electronic Systems | |

| Security Systems | |

| Others | |

| Exterior Accessories | LED and Auxiliary Lighting |

| Alloy Wheels | |

| Body Kits and Aero Parts | |

| Roof Racks and Carriers | |

| Window Films and Tinting | |

| Covers (Car, Wheel, Spare-tire) | |

| Crash Guards and Bull Bars | |

| Others |

| OEM Fitted |

| Aftermarket |

| Hatchback |

| Sedan |

| Sports and Luxury Cars |

| Compact SUV and CUV |

| Mid and Full-size SUV |

| Pick-up Trucks and Light Trucks |

| Plastic |

| Metal |

| Leather |

| Others |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Application | Interior Accessories | Infotainment Systems |

| Floor Carpets and Mats | ||

| Seat Covers | ||

| Electrical and Electronic Systems | ||

| Security Systems | ||

| Others | ||

| Exterior Accessories | LED and Auxiliary Lighting | |

| Alloy Wheels | ||

| Body Kits and Aero Parts | ||

| Roof Racks and Carriers | ||

| Window Films and Tinting | ||

| Covers (Car, Wheel, Spare-tire) | ||

| Crash Guards and Bull Bars | ||

| Others | ||

| By Sales Channel | OEM Fitted | |

| Aftermarket | ||

| By Vehicle Type | Hatchback | |

| Sedan | ||

| Sports and Luxury Cars | ||

| Compact SUV and CUV | ||

| Mid and Full-size SUV | ||

| Pick-up Trucks and Light Trucks | ||

| By Material Type | Plastic | |

| Metal | ||

| Leather | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the car accessories market?

The car accessories market size reached USD 279.82 billion in 2026 and is projected to rise to USD 365.48 billion by 2031.

Which region dominates demand for car accessories?

Asia-Pacific leads with 63.78% revenue share in 2025 and is also forecast to post the fastest 7.63% CAGR through 2031.

Which product category holds the largest share?

Interior accessories commanded 57.68% of 2025 sales, driven by infotainment upgrades, seat covers, and connectivity add-ons.

How fast is the aftermarket channel growing?

Aftermarket sales are expected to expand at a 9.71% CAGR between 2026 and 2031, outpacing the OEM channel.

What is the biggest restraint facing accessory suppliers?

Counterfeit and grey-market parts reduce consumer trust and impose negative impact on the market’s CAGR, especially in emerging economies.

How will electric vehicles influence accessory demand?

EVs create an 8.61% CAGR opportunity for lightweight, modular accessories that preserve driving range while adding utility and personalization.

Page last updated on: