Automotive Smart Antenna Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 4.13 Billion |

| Market Size (2031) | USD 7.37 Billion |

| Growth Rate (2026 - 2031) | 12.27% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Smart Antenna Market Analysis by Mordor Intelligence

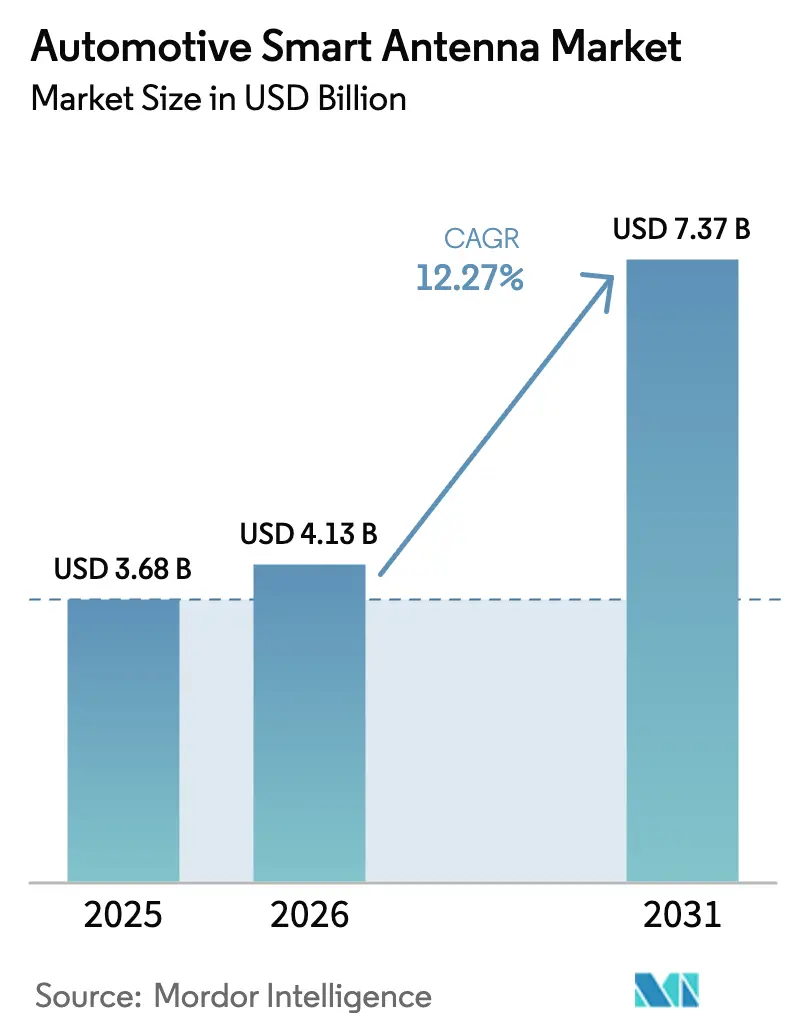

The automotive smart antenna market size is expected to grow from USD 3.68 billion in 2025 to USD 4.13 billion in 2026 and is forecast to reach USD 7.37 billion by 2031, representing a 12.27% CAGR during the forecast period (2026-2031). Multiple factors are propelling this expansion, including the rapid deployment of 5G, European mandates for vehicle-to-everything (V2X) connectivity, and the growing production of battery-electric vehicles (BEVs) that require multi-band reception. Automakers are replacing legacy mast designs with integrated roof modules that cut wiring weight by up to 12% and improve range in electric platforms. Suppliers are accelerating vertical integration to secure radio-frequency (RF) chipsets, while fleet operators are retrofitting older vehicles to maintain network access as 3G services sunset. Regionally, the Asia Pacific leads in volume due to China’s 5G-Advanced build-out, whereas the Middle East delivers the fastest CAGR, driven by smart-city programs.

Key Report Takeaways

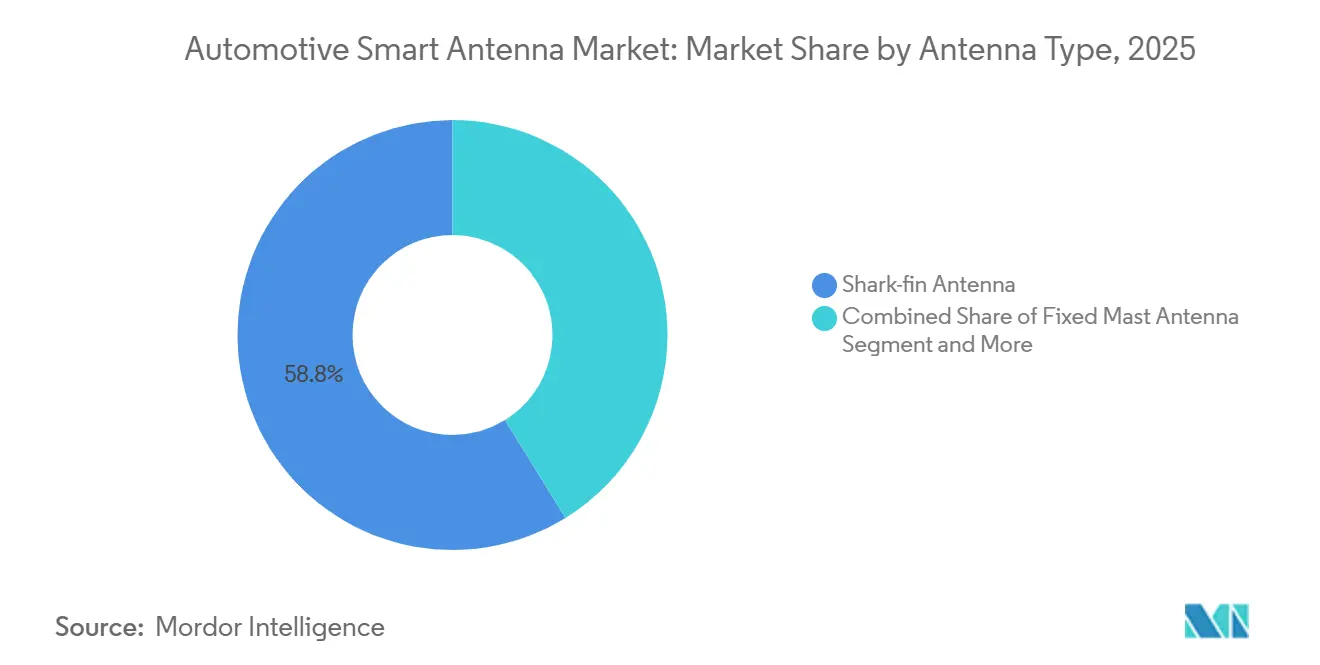

- By antenna type, shark-fin antennas accounted for 58.79% of the automotive smart antenna market share in 2025, while embedded antenna modules are projected to grow at the highest CAGR of 12.53% through 2031.

- By frequency band, Very High Frequency (VHF) dominated the automotive smart antenna market, accounting for a 45.87% share in 2025. In contrast, Super-High Frequency (SHF/mmWave) is expected to register the fastest growth at a 13.62% CAGR through 2031.

- By connectivity technology, 3G/4G/LTE solutions held a 49.96% market share in the automotive smart antenna market in 2025, with 5G NR projected to experience the fastest growth at an 18.31% CAGR through 2031.

- By vehicle type, passenger cars led the market with 75.42% of the automotive smart antenna market share in 2025, while light commercial vehicles are anticipated to grow at the highest rate of 10.33% CAGR during the forecast period.

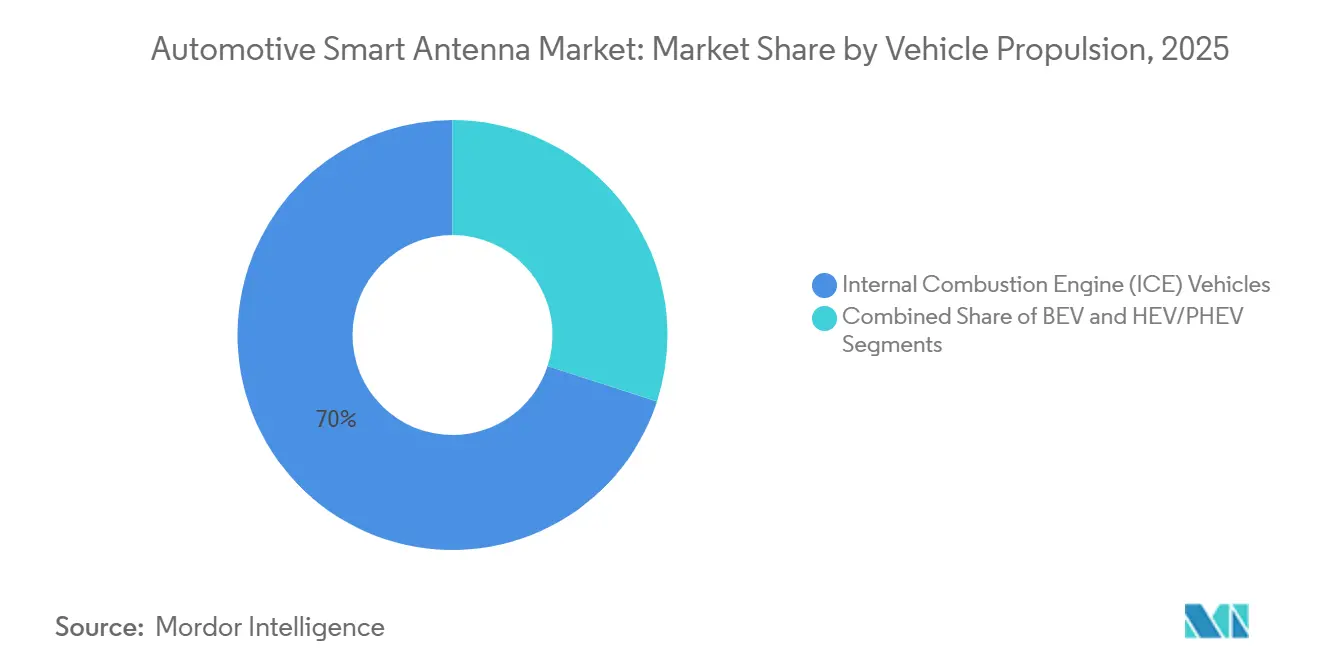

- By vehicle propulsion, ICE vehicles maintained dominance, accounting for 69.97% of the automotive smart antenna market in 2025. However, battery-electric vehicles are set to grow at the fastest rate, with a 16.28% CAGR in the coming years.

- By installation location, roof-mounted antennas accounted for 61.98% of the automotive smart antenna market share in 2025, while embedded solutions in TCUs/bumpers are forecast to grow at a 14.21% CAGR through 2031.

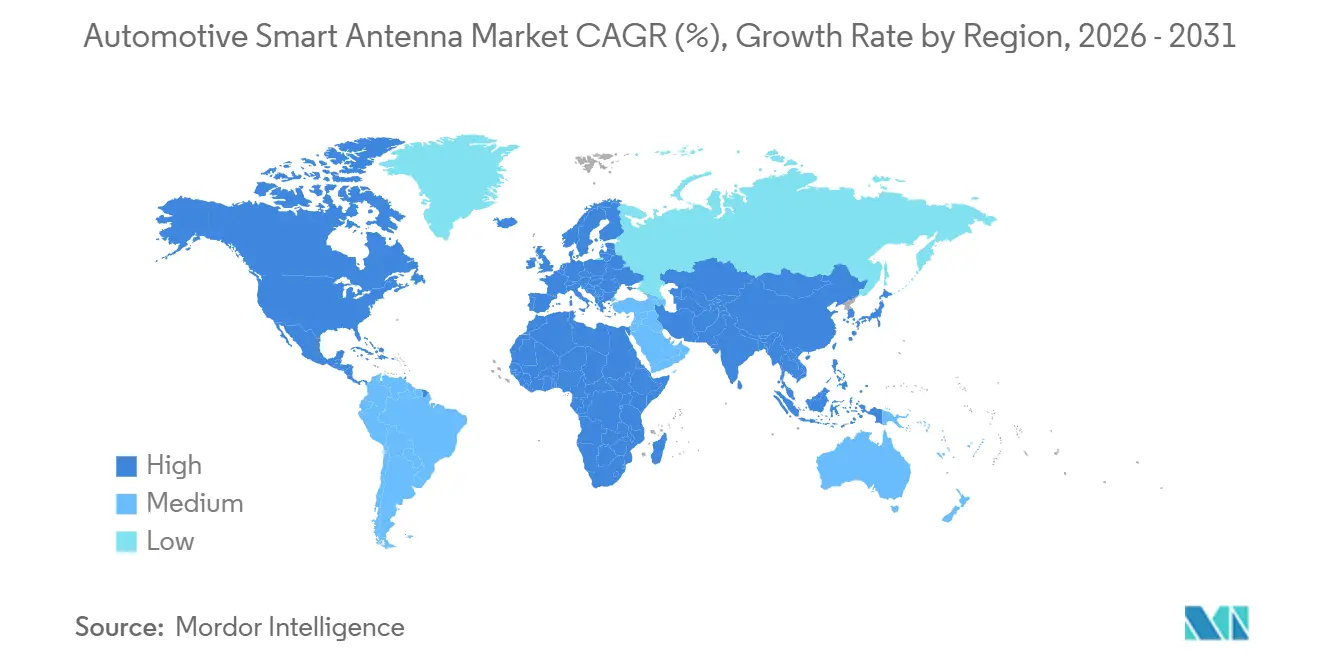

- By geography, the Asia Pacific commanded the largest market share at 41.62% of the automotive smart antenna market in 2025, while the Middle East is expected to witness the highest growth rate at a 12.18% CAGR from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Smart Antenna Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G Rollouts | +2.8% | Asia and Europe, spillover to North America | Medium term (2-4 years) |

| OEM Mandates for V2X Antenna Integration | +2.3% | Europe, global alignment following | Medium term (2-4 years) |

| Electrified Vehicle Platforms Needing Multi-Band Antennas | +1.7% | Global, high EV regions | Medium term (2-4 years) |

| Increasing OEM Adoption | +1.5% | North America, spreading to Europe | Short term (≤ 2 years) |

| Autonomous Driving Sensors Creating Demand | +0.9% | North America, Europe, China | Long term (≥ 4 years) |

| Emerging Demand for Satellite-Based Connectivity | +0.8% | North America and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G Roll-outs Accelerating Antenna Replacement Cycles

Mobile operator EE has rolled out major upgrades, expanding the availability of the UK's most reliable mobile technology, 5G standalone, to more towns and cities. In September 2024, EE launched its 5G standalone network, further expanding its reach. This advanced network now serves over 28 million individuals in 50 prominent towns and cities across the UK[1]"EE unveils 5G standalone upgrade for more than 28 million people," EE, newsroom.ee.co.uk. China Mobile activated 5G-Advanced sites in 300[2]MA SI, "Nation spearheads 5G-A network across 300 cities," China Daily, govt.chinadaily.com.cn cities, enabling network slicing that relies on dedicated RF paths for ultra-reliable communications. Premium models now integrate phased-array beamforming, while cost-optimized variants adopt single-element designs with software tuning. The aftermarket follows suit, with fleet operators retrofitting 5G modules to secure real-time diagnostics and traffic analytics.

Increasing OEM Adoption of Roof-Integrated TCUs to Cut Wiring Weight

Volkswagen’s MEB architecture trims 4.2 m of coaxial cable and 1.8 kg of harness weight by embedding the telematics control unit beneath the shark-fin housing. Tesla mirrored the approach in its 2025 Model 3 update, citing higher over-the-air success rates. Tier-1 suppliers now co-locate power amplifiers inside the module, reducing component counts by up to 40% and supporting BEV range targets that reward every kilogram saved.

OEM Mandates for V2X Antenna Integration from 2026 in EU Passenger Cars

Delegated Regulation 2022/1426 obliges new European passenger cars to carry C-V2X or DSRC hardware from July 2026, creating a captive pool of roughly 12.5 million antenna units yearly[3]"Commission Implementing Regulation (EU) 2022/1426," EUR-Lex, eur-lex.europa.eu. Stellantis opted for C-V2X, citing lower chipset costs, which prompted antenna designs with tighter phase-noise specifications. Compliance frameworks under ETSI EN 302 663 and ISO 21218 raise certification complexity but unify benchmarks across suppliers.

Electrified Vehicle Platforms Needing Multi-band Antennas to Reduce EMI

DC-DC converters in BEVs inject switching noise up to 6 GHz, so antennas require superior filtering that adds USD 8-12 to the bill of materials. General Motors’ Ultium platform calls for 14-band reception to support OnStar Guardian and future satellite links. The push to 800-V systems in 2025-2026 models intensifies shielding needs as higher voltages magnify electromagnetic emissions.

Restraints Impact Analysis*

| Restraint | (~) % Point Impact on Market CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shortage of RF Substrates | -2.1% | Supply chain dependent regions | Short term (≤ 2 years) |

| Complex Global Homologation | -1.3% | Fragmented regulatory regions | Medium term (2-4 years) |

| High Smart-Antenna Cost | -1.2% | Global, higher in price-sensitive markets | Short term (≤ 2 years) |

| RF Performance Degradation | -0.7% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Smart-Antenna BOM Cost vs. Legacy Mast in Entry-Level Models

Fixed-mast antennas cost USD 3-5, versus USD 35-50 for integrated designs, stalling adoption in entry-level cars across India and Southeast Asia. Maruti Suzuki Alto and Hyundai Grand i10 retained legacy masts in 2025 revisions. Suppliers are targeting USD 18-22 stripped-down smart antennas, yet these single-band units lack future upgrade paths and risk a two-tier connectivity landscape.

RF Performance Degradation Caused by Metallic Paint and Roof Rails

Metallic pigments reduce RF signal strength by up to 6 dB, triggering warranty claims, as seen in BMW’s 2025 5 Series. Roof rails and panoramic sunroofs exacerbate multipath losses by 2-3 dBi. Glass-integrated antennas bypass metal but raise repair costs when windshields crack. Coating firms are testing low-conductivity pigments, although unit paint costs rise by USD 15-20.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Antenna Type: Embedded Modules Challenging Shark-fin Dominance

Shark-fin units captured 58.79% of the automotive smart antenna market share in 2025, reflecting their ability to integrate cellular, GNSS, and broadcast elements into a single, aerodynamic housing. This configuration supported an installed base that drove the segment’s automotive smart antenna market size to exceed USD 2.1 billion in the base year. European brands aiming to lower drag coefficients and reduce wiring harness weight are now favoring embedded modules that slot into bumpers, spoilers, and mirrors. Continental’s 2025 launch of a configurable embedded platform that lets OEMs mix two to eight radiating elements illustrates the pivot toward tool-agnostic designs that reduce engineering overhead.

Embedded modules, although priced 20-30% higher today, are projected to grow at a 12.53% CAGR through 2031 as scale economies narrow the cost gap. BEV makers, particularly in Germany and South Korea, are early adopters because every 2-3% drag reduction translates into tangible range gains. In China, shark fins remain prevalent due to easier mid-cycle swaps, whereas North American pickup platforms typically retain roof-mounted designs for accessory compatibility. Regional divergence will persist until embedded solutions reach cost parity around 2028-2029, when volume ramps on global BEV platforms are expected to drive tooling amortization below USD 1 per unit.

By Frequency Band: mmWave Adoption Accelerates with Autonomous Features

Very high frequency (VHF) antennas maintained a 45.87% share of the automotive smart antenna market in 2025, driven by the requirement for AM/FM reception to support emergency alerts. The segment’s resiliency keeps it relevant even as in-car listening shifts to streaming, preserving roughly USD 1.7 billion of the automotive smart antenna market size in the base year. At the same time, super-high frequency (mmWave) products are projected to accelerate at a 13.62% CAGR through 2031, driven by 24-40 GHz 5G New Radio (NR) deployments that enable gigabit data rates for advanced infotainment and over-the-air map updates.

Yet mmWave’s 200-400 m range forces vehicles to hop between mmWave and sub-6 GHz links, raising the importance of dual-band tuning and phase-noise control. Qualcomm’s Snapdragon Auto demo in 2025 showed a 4 GB map download in under 90 seconds—a stark contrast to the 15-20 minutes required on LTE. The VHF segment, meanwhile, rests on regulatory mandates unlikely to disappear this decade. OEMs, therefore, need multi-band architectures that support legacy broadcasts, sub-6 GHz cellular, and mmWave, ensuring future proofing without sacrificing compliance or rural coverage.

By Connectivity Technology: 5G NR Outpaces Legacy Standards

LTE held 49.96% of the automotive smart antenna market share in 2025. However, 5G NR volumes are forecast to surge at an 18.31% CAGR through 2031, fueled by standalone network cores that promise network slicing and ultra-reliable low-latency lanes for safety-critical V2X. In contrast, North American and European adoption hinges on coverage densification, which is funded under recent infrastructure bills.

C-V2X demand is set for a sharp uptick after Europe’s July 2026 mandate, adding roughly 12.5 million antenna units a year to regional demand pools. GNSS components remain the backbone for navigation and autonomy, while in-cabin Wi-Fi/Bluetooth radios benefit from growth in multi-device streaming and smartphone mirroring. The technology mix will continue to evolve toward integrated multi-protocol antennas, reducing component count and easing homologation in a landscape where 3G sunsetting and 5G rollouts overlap.

By Vehicle Type: SUVs Drive Passenger Car Segment Growth

Passenger cars accounted for 75.42% of the automotive smart antenna market share in 2025. SUVs and multi-utility vehicles dominate this pool because their rooflines easily accommodate multi-element shark fins. Sedans and hatchbacks follow, especially in Europe and India, where urban density and price sensitivity steer buyers toward compact body styles with fewer embedded antennas.

Light commercial vehicles (LCVs) are forecast to expand at a 10.33% CAGR through 2031, outperforming medium- and heavy-duty trucks. The e-commerce boom pushes fleet owners to adopt smart antennas for real-time routing, driver scoring, and predictive maintenance. Off-highway vehicles, such as mining trucks and agricultural machinery, make up a small but lucrative segment; their ruggedized antennas can command a 40-50% premium over passenger-car equivalents, owing to higher ingress protection and vibration standards.

By Vehicle Propulsion: BEVs Demand Advanced EMI Mitigation

Internal combustion engine (ICE) vehicles still represented 69.97% of the automotive smart antenna market share in 2025. Nonetheless, tightening emissions rules and declining battery costs are driving BEVs ahead at a 16.28% CAGR through 2031. BEV platforms introduce higher electromagnetic interference from high-voltage inverters, prompting antenna designs that incorporate ferrite beads and common-mode chokes, as seen on Tesla’s 2025 Model Y.

Regionally, Norway’s BEV penetration surpassed 90% of new registrations, while China reached 35-40%. The EU is targeting a 2035 ban on ICE vehicles. Hybrids serve as a transitional bridge but complicate RF filtering, as both the alternator and inverter noise must be mitigated. BEV growth also enables more creative antenna placement; floor-mounted battery packs allow designers to position antennas higher for better sky view, thereby improving GNSS accuracy and cellular link budgets.

By Installation Location: Embedded Solutions Gain Momentum

Roof-mounted units held 61.98% of the automotive smart antenna market share in 2025, underpinned by their superior line-of-sight and ease of assembly on legacy lines. However, bumper and spoiler embeddings are projected to grow at a 14.21% CAGR as automakers pursue drag coefficients below 0.20 on flagship BEVs such as the Mercedes-Benz EQS.

Embedded designs face RF hurdles, including near-field coupling and reduced elevation, which can trim GNSS gain by up to 3 dBi in urban canyons. Windshield-printed antennas address aesthetics but lift insurance costs when glass breaks. Regional preferences differ: European OEMs rely on embedded solutions for aerodynamic gains, North American pickups retain roof fins for accessory compatibility, and Chinese brands strike a balance between both approaches to accelerate model-year updates without costly body re-engineering.

Geography Analysis

Asia Pacific accounted for 41.62% of the automotive smart antenna market share in 2025. China's expanding annual builds, coupled with 95% urban 5G coverage, have culminated in the nation's dominance with the largest installed base. In Japan, the ambition to achieve majority V2X penetration by 2028 is driving a surge in antenna upgrades. South Korea, with an investment of USD 1.2 billion, is embedding antennas into Hyundai's E-GMP platform. While India is known for its price sensitivity, a looming telematics mandate for commercial vehicles could introduce an additional 900,000 units annually starting in 2027.

North America and Europe show slower growth but higher antenna counts per vehicle. The United States' progress hinges on infrastructure funding under the 2021 law, while Canada mirrors the United States with pockets of high adoption in colder provinces for extreme-weather validation.

The Middle East posts the quickest CAGR at 12.18% as Saudi Arabia’s NEOM orders 10,000 autonomous vehicles requiring precision GNSS by 2031. The UAE’s target for 25% autonomous travel by 2030 drives multi-band demand in desert regions with sparse terrestrial coverage. South America grows unevenly; Brazil’s ANATEL cleared C-V2X spectrum in 2024, seeding pilots in São Paulo. Africa remains relatively nascent, although South African mines are retrofitting haul trucks with telemetry packages for enhanced safety.

Competitive Landscape

The top five suppliers accounted for a significant share of 2025 revenue. Continental’s Q3 2024 acquisition of a phased-array chipset designer strengthens its in-house RF capabilities and mitigates semiconductor shortages. Taoglas, Amphenol RF, and Hirschmann win niche contracts by engineering custom designs in under 12 weeks, compared to the industry standard of 16 weeks.

Patent filings reveal shifting priorities. Bosch lodged 14 applications on adaptive tuning that compensates for metallic paint attenuation, while Ficosa focuses on low-loss glass-embedded solutions. Certification remains a hurdle as ISO 11452 and CISPR 25 testing costs can hit USD 300,000 per variant, discouraging smaller firms and reinforcing incumbent leverage.

The market for solutions optimized for electric-only platforms, as well as cost-effective versions for emerging markets, offers significant growth opportunities. Suppliers capable of addressing diverse homologation requirements without necessitating hardware redesigns are expected to gain a competitive edge. Industry consensus suggests that future market leaders will integrate agile engineering practices with robust supply chain management to mitigate the impact of commodity price fluctuations, as evidenced by recent RF substrate shortages.

Automotive Smart Antenna Industry Leaders

-

HELLA GmbH & Co. KGaA

-

Robert Bosch GmbH

-

TE Connectivity

-

Continental AG

-

Harman International Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: FORVIA HELLA began mass-producing fifth-generation 77 GHz radar in China. The unit achieves 360° detection, suggesting synergies between radar cooling and antenna packaging.

- February 2024: HARMAN introduced the Ready Connect 5 G TCU at Mobile World Congress. It utilizes Snapdragon Auto 5G Modem-RF Gen 2 silicon, enabling carmakers to deploy high-speed connectivity faster.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the automotive smart antenna market as global revenue from factory-installed, multi-band modules that merge RF front-end, GNSS, cellular (3G-5G), Wi-Fi, Bluetooth, and V2X radios inside one housing fixed to passenger cars and light commercial vehicles. These modules support infotainment, telematics, over-the-air updates, and driver-assistance links.

Scope exclusion: passive rod or film antennas sold solely for AM/FM reception.

Segmentation Overview

-

By Antenna Type

- Shark-fin Antenna

- Fixed Mast Antenna

- Glass/Integrated Antenna

- Embedded Antenna Module

- Others (Pillar, Element)

-

By Frequency Band

- High Frequency (HF)

- Very High Frequency (VHF)

- Ultra-High Frequency (UHF)

- Super High Frequency (SHF/mmWave)

-

By Connectivity Technology

- 3G/4G/LTE

- 5G NR

- V2X – DSRC/C-V2X

- GNSS/GPS

- Wi-Fi/Bluetooth

-

By Vehicle Type

-

Passenger Cars

- Hatchback

- Sedan

- Sports Utility Vehicles (SUVs)

- Multi-Utility Vehicles (MUVs)

- Light Commercial Vehicles

- Medium and Heavy Commercial Vehicles

- Off-Highway Vehicles

-

Passenger Cars

-

By Vehicle Propulsion

- Internal Combustion Engine (ICE)

- Battery Electric Vehicle (BEV)

- Hybrid and Plug-in Hybrid (HEV/PHEV)

-

By Installation Location

- Roof-Mounted

- Windshield/Glass-Mounted

- Embedded in TCU/Bumper

-

Geography

-

North America

- United States

- Canada

- Rest of North America

-

South America

- Brazil

- Argentina

- Rest of South America

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia Pacific

-

Middle East and Africa

- Saudi Arabia

- United Arab Emirates

- Turkey

- South Africa

- Rest of Middle East and Africa

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed antenna engineers, tier-1 procurement leads, and fleet connectivity managers across Asia, Europe, and North America; these talks validated fitment rates, price spreads, and realistic lead times for regulation-driven upgrades.

Desk Research

We began by pulling yearly vehicle output from OICA and checking registration files at the EU Commission and NHTSA. UN Comtrade flows confirmed cross-border supply. Papers from the 5G Automotive Association, ETSI, and the European Commission clarified V2X deadlines shaping penetration curves. Financial filings and patent sets accessed through D&B Hoovers, Questel, and Dow Jones Factiva mapped supplier footprints and average selling prices. The sources named are illustrative; many other public and paid datasets underpinned data checks.

Market-Sizing & Forecasting

A top-down build starts with regional light-vehicle output and applies smart-antenna penetration refined through our interviews. Supplier shipment roll-ups and sampled ASP × volume checks provide bottom-up sense tests. Key variables include 5G telematics take rate, battery-electric share, the EU-2026 V2X milestone, and ASP deflation. Multivariate regression projects each driver, while scenario analysis covers regulation uncertainty.

Data Validation & Update Cycle

Outputs run through anomaly screens versus history, peer numbers, and live news flags; unresolved gaps trigger senior review. Figures refresh every year, with interim updates after any material policy or technology shift.

Why Mordor's Automotive Smart Antenna Baseline Commands Reliable Insight

Published estimates often diverge because firms choose unlike scopes, refresh cadences, and price paths.

Major gaps involve whether aftermarket sales or heavy trucks are counted and how 5G premiums are modeled.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 3.38 B | Mordor Intelligence | - |

| USD 3.33 B | Global Consultancy A | Aftermarket excluded; fixed 2022 FX rate |

| USD 4.69 B (2024) | Industry Association B | Counts passive replacements and heavy trucks |

| USD 3.62 B (2024) | Regional Consultancy C | Constant 5G ASP uplift through 2030 |

These contrasts show how Mordor's disciplined scope, transparent driver tracking, and yearly refresh give decision-makers a balanced baseline they can trace, replicate, and trust.

Key Questions Answered in the Report

How fast is 5G NR adoption growing in vehicle antennas?

Shipments linked to 5G NR are projected to expand at an 18.31% CAGR from 2026-2031.

Which region led unit demand for automotive smart antennas in 2025?

Asia Pacific commanded 41.62% of global volume, driven overwhelmingly by China.

Which antenna type held the largest automotive smart antenna market share in 2025?

Shark-fin designs led with 58.79% of revenue that year.

Why are embedded bumper antennas gaining traction?

They support cleaner rooflines, cut aerodynamic drag, and are forecast to grow at a 14.21% CAGR through 2031.

Which companies together held under 40% of global revenue in 2025?

Continental, TE Connectivity, and Harman.

Page last updated on: