Automotive Transmission Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

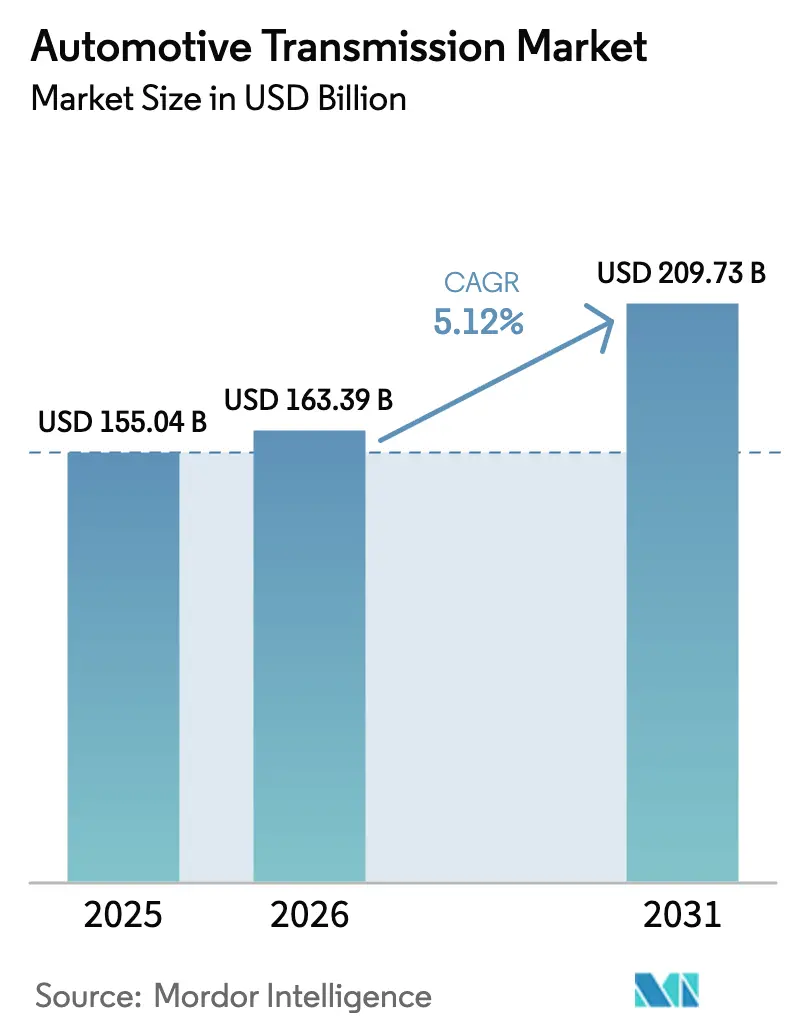

| Market Size (2026) | USD 163.39 Billion |

| Market Size (2031) | USD 209.73 Billion |

| Growth Rate (2026 - 2031) | 5.12% CAGR |

| Fastest Growing Market | South America |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Transmission Market Analysis by Mordor Intelligence

The automotive transmission market size is expected to grow from USD 155.04 billion in 2025 to USD 163.39 billion in 2026 and is forecast to reach USD 209.73 billion by 2031, growing at a 5.12% CAGR during the forecast period (2026-2031). Growth hinges on the rapid pivot from manual gearboxes toward software-defined, electrified drivelines, reinforced by tighter Corporate Average Fuel Economy standards in the United States and parallel mandates across the European Union and China. Automatic units retained demand leadership, yet dual-clutch systems are outpacing all rivals as performance-minded buyers seek sub-200-millisecond shifts without sacrificing fuel economy. Passenger-car domination continues, but light commercial fleets are electrifying more quickly as e-commerce logistics firms retrofit vans with automated manual transmissions to address driver shortages.

Key Report Takeaways

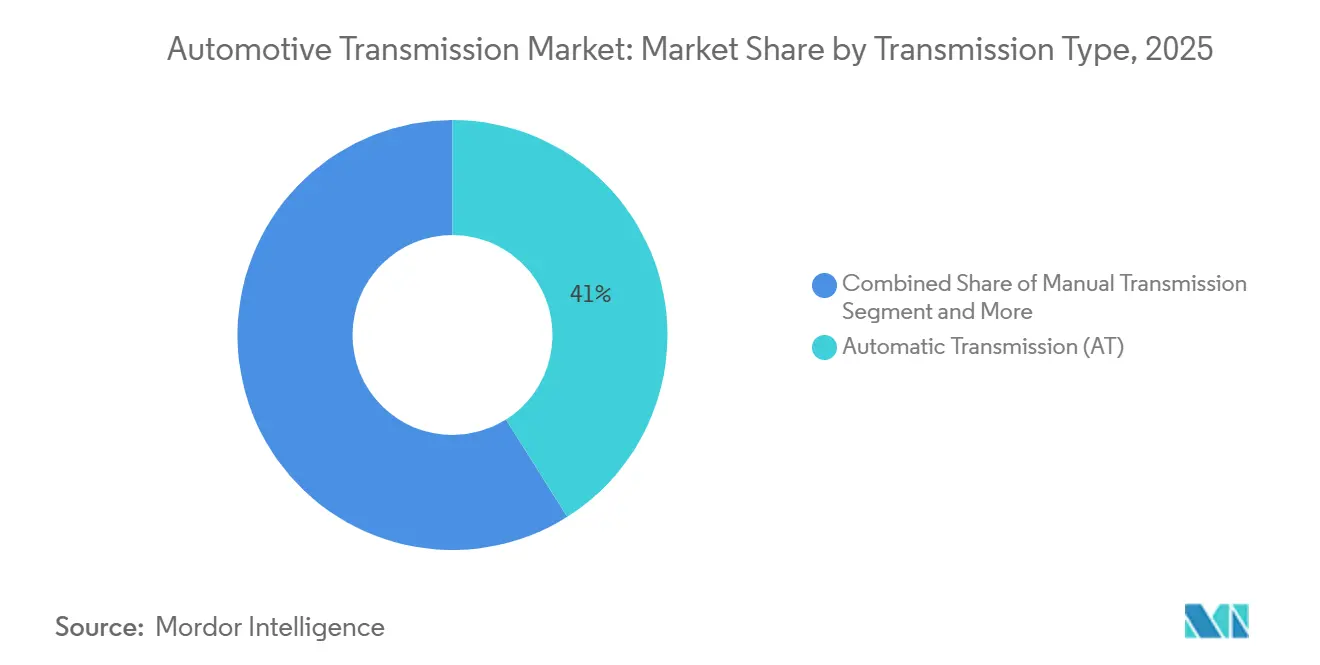

- By transmission type, automatic systems led the automotive transmission market, accounting for a 41.03% revenue share in 2025. Meanwhile, dual-clutch units are forecast to grow at a 5.89% CAGR through 2031.

- By vehicle type, passenger cars accounted for 64.79% of the automotive transmission market share in 2025; light commercial vehicles posted the fastest growth at a 5.62% CAGR through 2031.

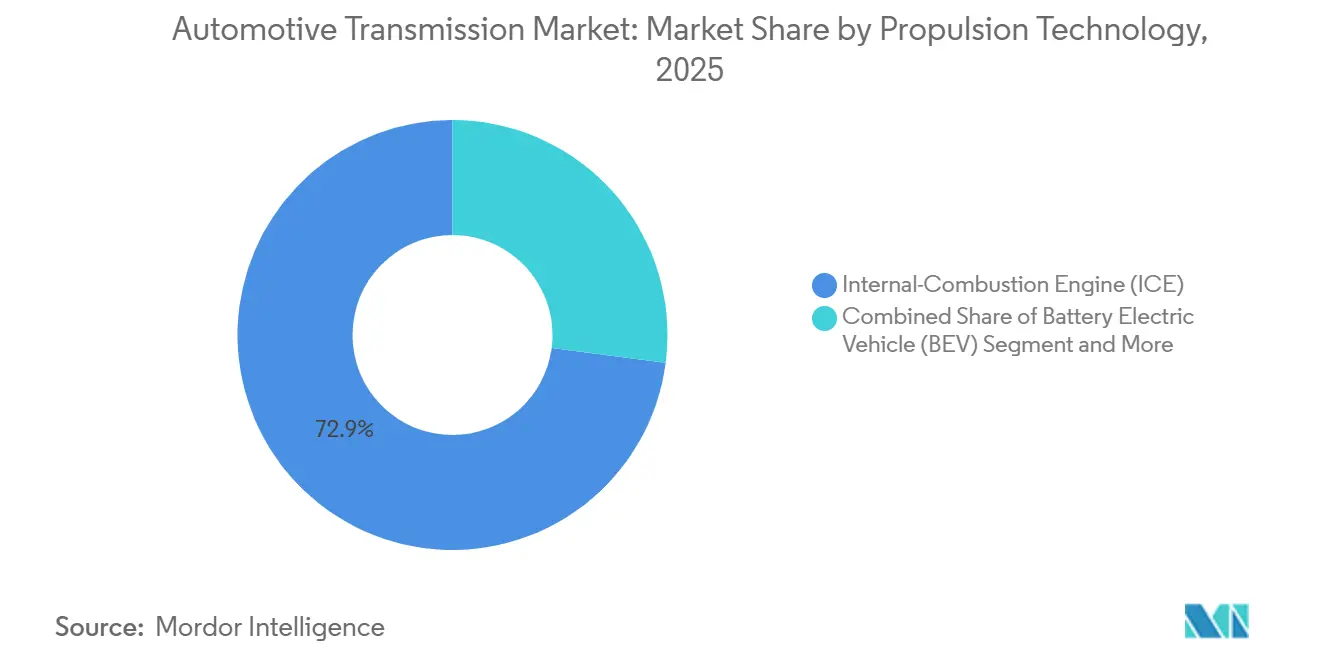

- By propulsion technology, internal-combustion engines accounted for 72.94% of the automotive transmission market size in 2025, yet fuel cell electric vehicles registered the highest 6.34% CAGR through 2031.

- By sales channel, OEM fitments dominated the automotive transmission market with a 90.88% share in 2025, whereas the aftermarket expanded at a 6.21% CAGR through 2031.

- By geography, the Asia-Pacific region led the automotive transmission market with a 43.67% revenue share in 2025, while South America is projected to post the fastest growth at a 6.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Automotive Transmission Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of Hybrid and BEV E-axle | +1.5% | Global, with China and Europe leading adoption | Short term (≤ 2 years) |

| Tightening Global CO₂ Regulations | +1.2% | Global, with EU and North America leading | Medium term (2-4 years) |

| Consumer Shift Toward Automatic and DCT | +0.8% | Asia-Pacific core, expanding to emerging markets | Long term (≥ 4 years) |

| Commercial-Vehicle Demand for AMT | +0.6% | North America and Europe primarily | Medium term (2-4 years) |

| Silicon-Carbide Inverter Cost Decline | +0.4% | Global, with early adoption in premium segments | Long term (≥ 4 years) |

| Software-Defined "shift-by-wire" Enabling OTA Feature Monetization | +0.3% | North America and Europe initially | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of Hybrid and BEV E-Axle Transmissions

Electrified drivelines merge motor, inverter, and reduction gear into compact e-axles that can cut weight by 18 kilograms versus six-speed automatics, as demonstrated by BYD’s 8-in-1 unit on the Seal in 2024. Hyundai’s P1+P2 hybrid layout, launched in April 2025, features a 44-kilowatt motor positioned between the engine and a six-speed automatic transmission, allowing for a pure-electric launch without separate transmission control[1]"NextGen Hybrid Power: Hyundai Motor Group’s Advanced Transmission and Engine Technologies," Hyundai Motor Group, hyundaimotorgroup.com. NIO’s four-in-one drive in the ET7 achieves 91.5% system efficiency by integrating torque vectoring into the inverter firmware.

Tightening Global CO₂/Fuel-Economy Regulations

The U.S. 2027-2031 CAFE rules finalized in 2024 demand a 58-mile-per-gallon fleet average by 2031, compelling eight-plus-speed automatics that keep engines in optimum efficiency bands[2]"Corporate Average Fuel Economy Standards," National Highway Traffic Safety Administration (NHTSA), nhtsa.gov. Euro 7, effective January 2025, limits on-road nitrogen oxides to 60 mg/km, pushing diesel models toward 10-speed units that curb transient spikes. China’s revised dual-credit system rewards plug-in hybrids that exceed 80 km electric range, accelerating clutchless hybrid gearboxes. India’s CAFE Phase 2 imposes penalties of INR 25,000 per gram of CO₂ above 113 g/km, thereby accelerating the adoption of intelligent manuals with automated clutches.

Consumer Shift Toward Automatic and DCT for Comfort/Performance

Automatic penetration in India jumped in 2024 as urban stop-and-go traffic amplified driver fatigue from clutch use. Hyundai’s eight-speed wet DCT, fitted to the Sonata N Line in 2024, achieved 95% mechanical efficiency and a 0.4 l/100 km fuel benefit. Volkswagen’s DQ381 seven-speed DCT posts sub-150-millisecond shifts, removing torque interruption during hard acceleration. As costs converge, dual-clutch systems are increasingly appearing in C-segment sedans priced below USD 25,000, reinforcing momentum for the automotive transmission market worldwide. Gains in comfort and performance together sustain the migration away from stick shifts in both mature and emerging regions.

Commercial-Vehicle Demand for AMT to Address Driver Shortage

The United States faced 78,000 unfilled heavy-truck driver positions in 2024, motivating fleets to adopt automated manuals that reduce training from six weeks to 10 days[3]"Truck Driver Shortage Facts," Ryder System, Inc., ryder.com. Allison’s TC10 AMT introduced predictive grade-based logic in 2024, resulting in a 3-5% reduction in fuel consumption compared to manual driving. Eaton’s Cummins Endurant HD handled 1,850 Nm torque and shipped 45,000 units in 2024, proving heavy-haul readiness. Consequently, fleets view AMTs as indispensable for retention and safety, while strengthening the trajectory of the automotive transmission market.

Restraints Impact Analysis of Automotive Transmission Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High System Cost | -0.9% | Global, with premium segments less affected | Short term (≤ 2 years) |

| Supply-Chain Volatility | -0.7% | Global, with Asia-Pacific manufacturing concentration | Medium term (2-4 years) |

| Limited Thermal Window for Ultra-Low-Viscosity ATF | -0.5% | Global, with hot climate regions most affected | Medium term (2-4 years) |

| Cyber-Security Compliance Costs | -0.4% | North America and EU primarily, expanding globally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High System Cost and Complexity of Multi-Speed Electrified Drivelines

Adding an extra ratio inflates EV drivetrain cost by USD 400–600. It increases weight by 22 kilograms, as seen in Porsche’s Taycan, which also requires dedicated cooling to manage oil temperatures of up to 180 °C. Tesla and BYD avoid this cost by optimizing single-speed gearing for 90% of driving cycles. Hybrid e-CVTs face similar bill-of-materials pressure, with Toyota’s e-CVT requiring a battery capable of 50 kW continuous discharge, which raises pack cost by USD 1,200. These premiums limit near-term proliferation beyond premium nameplates, tempering broader growth in the automotive transmission market.

Supply-Chain Volatility in Precision-Forged Gears and Bearings

A January 2025 fire at SKF’s Gothenburg bearing facility removed 18% of European needle-roller output, forcing ZF and Aisin to air-freight inventory from Japan at a 22% cost penalty. Ring-gear lead times lengthened to 28 weeks in mid-2025 as alloy steel suppliers rationed nickel amid market turbulence. Schaeffler’s effort to qualify an Indian bearing source delayed its P2+ hybrid launch by two quarters. Dual-clutch units bear a significant risk because they use four to six tapered-roller bearings each, compared to two in classic automatics. The disruption highlights the fragility of the automotive transmission supply chain.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Automotive Transmission Market Segment Analysis

By Transmission Type:

Automatic Dominance Faces DCT ChallengeAutomatic transmissions retained a leading 41.03% share of the automotive transmission market in 2025, anchored by North American pickups and SUVs that value towing and refinement. Dual-clutch units are projected to grow at a 5.89% CAGR through 2031. Continuously variable designs, once favored for their infinite ratio spread, now struggle to satisfy performance expectations despite JATCO’s CVT9 launch with a 9.0:1 ratio range. Manual gearboxes persist mainly in entry-level Asian models, thanks to a USD 300 cost advantage over intelligent manuals.

Automatic dominance in full-size pickups, dual-clutch acceleration in compact cars, and emerging two-speed EV gears together shape the future mix. The automotive transmission market for dual-clutch units is expected to expand as tooling amortization reduces per-unit costs. Two-speed EV boxes count as “Others” but carry strategic weight for premium range extension in models like Audi’s e-tron GT. Suppliers, therefore, diversify portfolios across all mechanisms to defend relevance.

By Vehicle Type:

Commercial Segments Drive InnovationPassenger cars accounted for a 64.79% share of the automotive transmission market in 2025, while light commercial vehicles are expected to record a 5.62% CAGR through 2031, as e-commerce fleets prioritize low-maintenance electric drivetrains. Ford’s E-Transit reduced service expenses 40% versus diesel predecessors through a single-speed reduction gear rated at 430 Nm. Mercedes-Benz’s eSprinter adopted a two-speed gearbox to sustain a payload advantage of 1,045 kilograms.

The automotive transmission market for AMT-equipped heavy trucks is poised to grow steadily as carriers link safety gains to lower insurance premiums. Passenger cars bifurcate into eight-speed automatics for ICE platforms and single-speed drives for mainstream BEVs under USD 40,000. Tata’s Ace EV shows intelligent manual viability within small electrified commercial vehicles in India. Volvo Trucks’ FH Electric features a two-speed I-Shift for improved gradeability, though its USD 350,000 price currently limits adoption.

By Propulsion Technology:

Electrification AcceleratesInternal-combustion engines represented a 72.94% share of the automotive transmission market in 2025. Still, fuel-cell electric vehicles will advance at a segment-leading 6.34% CAGR through 2031, as Toyota and Hyundai push hydrogen for payload-sensitive commercial fleets. Battery-electric cars priced under USD 40,000 often utilize single-speed gearsets because adding a second ratio can erode their margin. BYD’s Dolphin employs a fixed 10.39:1 gear to achieve 0–100 km/h in 7.5 seconds.

The automotive transmission market size for dedicated hybrid gearboxes expands as dual-motor architectures meet revised Chinese credit multipliers. ICE powertrains have evolved to 10-speed automatics, such as Ford’s 10R80, which keeps the 3.5-liter EcoBoost under 2,000 rpm at highway speeds. Premium BEVs, led by Porsche’s Taycan, validate two-speed layouts that extend range on high-speed cycles. Consequently, suppliers must balance traditional planetary expertise with emerging e-axle competencies.

By Sales Channel:

Aftermarket Complexity Creates OpportunitiesOEM factory-fit units captured a 90.88% share of the automotive transmission market in 2025, as deeply integrated control software discourages component swapping. Continental’s shift-by-wire module requires a cryptographic handshake with the body controller, effectively locking out unauthorized replacements. Still, the remanufacturing aftermarket is expected to post a 6.21% CAGR through 2031, as fleets pursue life-cycle cost savings of 40–60% compared to new units.

The automotive transmission market size within remanufacturing could expand further, as Class 8 trucks typically undergo 1.2 replacements over a one-million-mile lifespan. Powertrain warranties such as Ford’s 10-year/150,000-mile plan introduced in 2024 heighten genuine parts demand. Battery-electric single-speed drives pose a structural headwind for the aftermarket, yet heavy-duty fleets keep the channel buoyant.

Geography Analysis

APAC Automotive Transmission Market

In 2025, the Asia-Pacific region held a 43.67% share of the automotive transmission market, fueled by strong BEV sales in China and significant growth in India's adoption of intelligent manuals, especially for sedans priced below USD 15,000. China's revised dual-credit system now allocates 1.6 credits per plug-in hybrid, encouraging OEMs to utilize dedicated hybrid transmissions, such as BYD's DM-i.

The Americas Automotive Transmission Market

South America represents the fastest-growing territory, with a 6.28% CAGR through 2031, as Brazil’s Rota 2030 initiative subsidizes locally built automatics to achieve 12% fleet-level efficiency by 2028. Argentina’s import tariff on fully built gearboxes spurred local dual-clutch assembly for Volkswagen and Fiat. In 2025, North America's automotive transmission market experienced a notable increase, with 10-speed automatics dominating pickups like the Ford F-150, while single-speed drives became the preferred choice for crossovers, exemplified by the Mustang Mach-E.

Europe Automotive Transmission Market

Meanwhile, Europe is gravitating towards dual-clutch systems, highlighted by Germany's substantial share of DCTs in passenger vehicles in 2025. In 2025, the United Kingdom experienced a surge in new BEV registrations, dampening the demand for conventional automatics. Concurrently, France is expanding Renault's clutchless four-speed E-Tech across its mainstream models.

Competitive Landscape

The top five suppliers accounted for a significant portion of the global passenger-car volume in 2025, indicating moderate concentration. JATCO focused on CVT leadership, while Hyundai Transys captured internal demand for six-speed and hybrid models.

Smaller innovators target white-space niches. Punch Powertrain’s dedicated hybrid gearbox enables 130 km/h electric cruising, making it an appealing option for European cities that are enforcing diesel bans. Schaeffler’s 100 kW P2+ module enables automakers to retrofit existing eight-speed cases, thereby shortening launch cycles by a year.

Technology leadership now revolves around software. Continental’s shift-by-wire unlocks subscription revenues and hardens cybersecurity. Magna filed a 2024 patent for an integrated coolant pathway that trims e-axle mass by 4.2 kilograms. Meanwhile, ZF’s ReLife and Allison’s ReTran aim to dominate remanufacturing as sustainability metrics rise. Competitive intensity thus pivots from volume share to IP depth and software monetization within the evolving automotive transmission market.

Automotive Transmission Industry Leaders

-

ZF Friedrichshafen AG

-

Aisin Corporation

-

Schaeffler AG

-

Magna International Inc.

-

JATCO Ltd.

- *Disclaimer: Major Players sorted in no particular order

Automotive Transmission Market Companies Covered in this Report

- ZF Friedrichshafen AG

- Aisin Corporation

- JATCO Ltd.

- Hyundai Transys Inc.

- Magna International Inc.

- Allison Transmission Inc.

- Schaeffler AG

- Eaton Corporation plc

- BorgWarner Inc.

- Continental AG

- Punch Powertrain NV

- GKN Automotive Limited

- Toyota Motor Corp. (Hybrid e-CVT)

- Valeo SA

- Tremec Corporation

- Dana Incorporated

Recent Industry Developments in Automotive Transmission Market

- May 2025: At the Brisbane Truck Show, Cummins unveiled its heavy-duty X15 Euro 6 engine, which is fully integrated and paired with the Eaton Cummins Endurant 18-speed transmission. This display highlighted a fuel-agnostic HELM platform boasting an impressive 660 hp and 2,360 lb-ft of torque.

- January 2025: JATCO Ltd has opened a manufacturing plant in Northeast England, investing USD 57.12 million. The facility, covering 138,840 square feet, is located at the International Advanced Manufacturing Park in Sunderland. It will produce electrified powertrains for the nearby Nissan plant, initially focusing on a compact 3-in-1 system that integrates the motor, inverter, and reducer.

Global Automotive Transmission Market Report Scope

It is a multi-speed gearbox used in vehicles where the driver does not need to change forward gears under typical driving conditions. A planetary gearset, hydraulic controls, and torque converter are included. The engine is connected to a torque converter, which in turn is connected to a gear system, ultimately linked to the gearbox. Some sections of the torque converter interact with one another. The flywheel, which rotates the whole device, is housed in the outermost section.

The automotive transmission market is segmented by transmission type, vehicle type, fuel type, and geography.

Transmission Type segments the Automotive Transmission Market, comprising Manual Transmission, Intelligent Manual Transmission (IMT), Automated Manual Transmission (AMT), Automatic Transmission (AT), Dual-clutch Transmission, and Others. By Vehicle Type, the market is segmented into Passenger Cars, Light Commercial Vehicles, Heavy Commercial Vehicles, and Buses and Coaches. By fuel type, the market is segmented into Gasoline and Diesel. By Geography, the market is segmented into North America, Europe, Asia-Pacific, and the Middle East and Africa. For each segment, market sizing and forecasting have been conducted based on value (USD).

Segmentation Overview

| Manual Transmission |

| Intelligent Manual Transmission (iMT) |

| Automated Manual Transmission (AMT) |

| Automatic Transmission (AT) |

| Dual-Clutch Transmission (DCT) |

| Continuously Variable Transmission (CVT) |

| Others (Planetary, 2-speed EV gearboxes etc.) |

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

| Buses and Coaches |

| Internal-Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV/PHEV) |

| Battery Electric Vehicle (BEV) |

| Fuel Cell Electric Vehicles (FCEV) |

| Original Equipment Manufacturer (OEM) Factory-Fit |

| Aftermarket/Remanufactured |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | Turkey |

| United Arab Emirates | |

| Saudi Arabia | |

| South Africa | |

| Rest of Middle East and Africa |

| By Transmission Type | Manual Transmission | |

| Intelligent Manual Transmission (iMT) | ||

| Automated Manual Transmission (AMT) | ||

| Automatic Transmission (AT) | ||

| Dual-Clutch Transmission (DCT) | ||

| Continuously Variable Transmission (CVT) | ||

| Others (Planetary, 2-speed EV gearboxes etc.) | ||

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| Buses and Coaches | ||

| By Propulsion Technology | Internal-Combustion Engine (ICE) | |

| Hybrid Electric Vehicle (HEV/PHEV) | ||

| Battery Electric Vehicle (BEV) | ||

| Fuel Cell Electric Vehicles (FCEV) | ||

| By Sales Channel | Original Equipment Manufacturer (OEM) Factory-Fit | |

| Aftermarket/Remanufactured | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Turkey | |

| United Arab Emirates | ||

| Saudi Arabia | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive transmission market by 2031?

The market is forecast to reach USD 209.73 billion by 2031, growing at a 5.12% CAGR.

Which transmission type is expected to grow the fastest through 2031?

Dual-clutch transmissions are set to register the quickest 5.89% CAGR, driven by their efficiency and rapid shift capability.

How are tightening fuel-economy rules shaping transmission design?

Regulations such as U.S. CAFE and Euro 7 push automakers toward eight-plus-speed automatics and hybrid-dedicated gearboxes that keep engines in peak efficiency ranges.

Why are automated manual transmissions gaining traction in heavy trucks?

AMTs reduce driver training time, improve fuel economy up to 5%, and help fleets cope with chronic driver shortages.

Which region leads global revenue, and which is growing fastest?

Asia-Pacific leads with 43.67% of 2025 revenue, while South America is the fastest-growing at a 6.28% CAGR to 2031.

What role does software play in modern transmissions?

Shift-by-wire systems enable over-the-air feature unlocks, allowing OEMs to sell subscription-based driving modes without hardware changes.

Page last updated on: