Connected Car Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

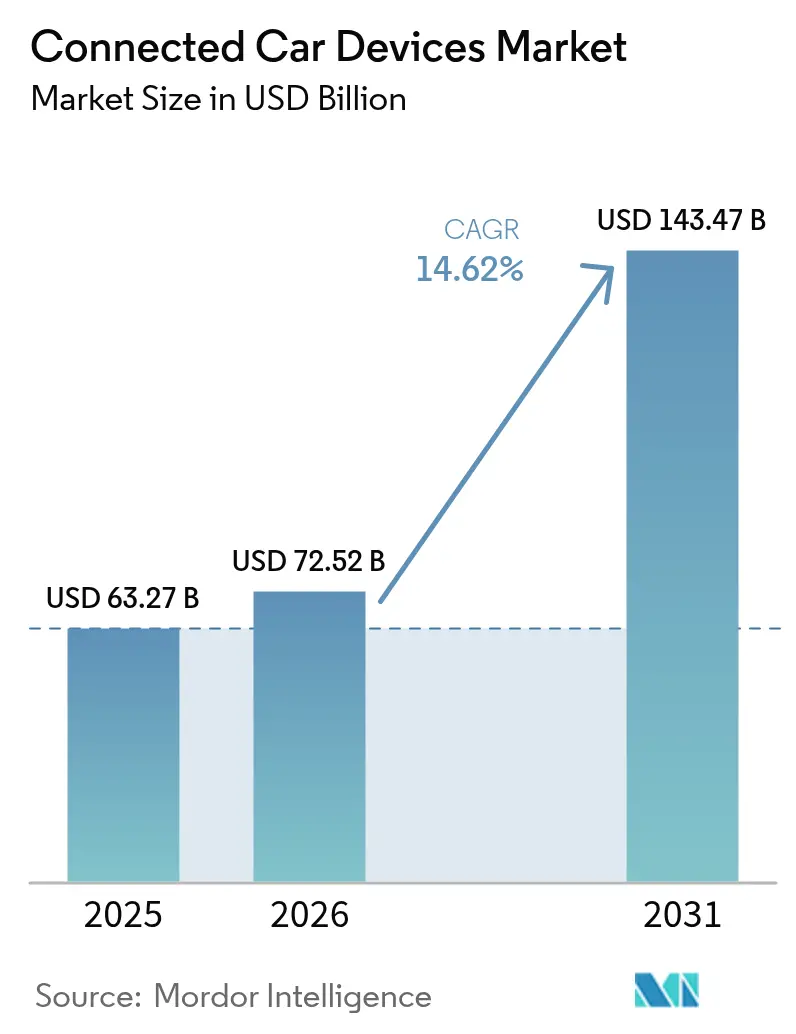

| Market Size (2026) | USD 72.52 Billion |

| Market Size (2031) | USD 143.47 Billion |

| Growth Rate (2026 - 2031) | 14.62% CAGR |

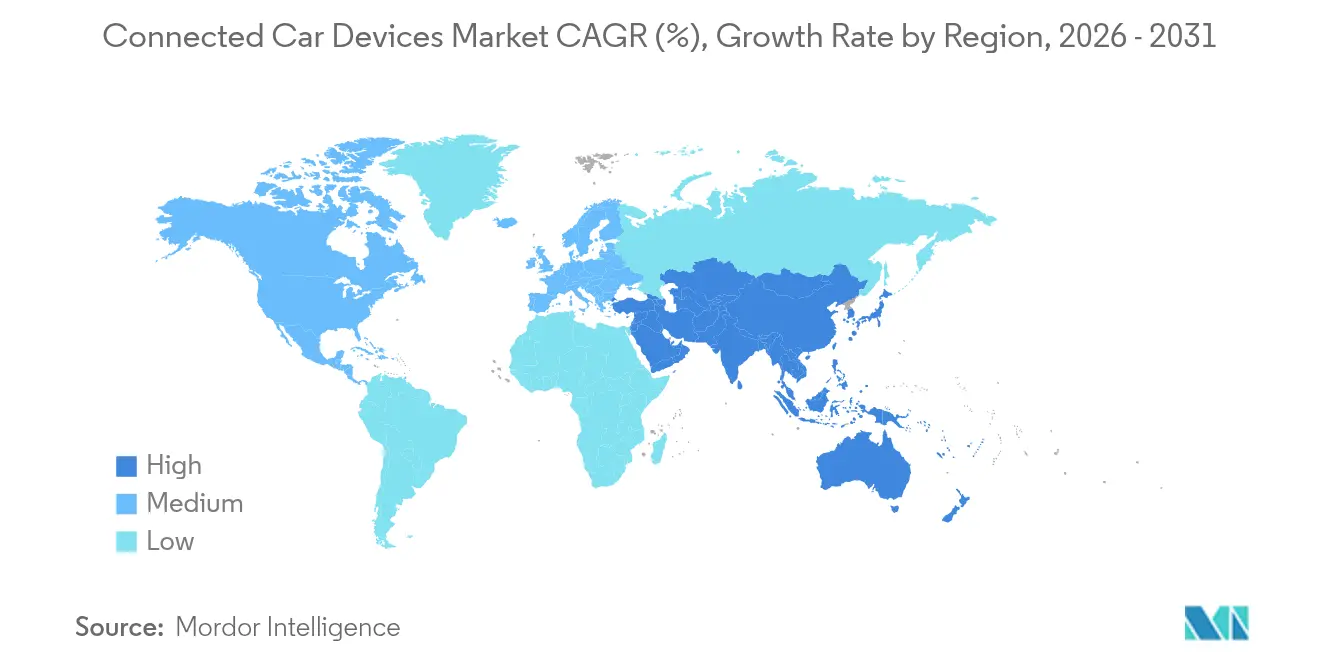

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Connected Car Devices Market Analysis by Mordor Intelligence

Connected Car Devices market size in 2026 is estimated at USD 72.52 billion, growing from 2025 value of USD 63.27 billion with 2031 projections showing USD 143.47 billion, growing at 14.62% CAGR over 2026-2031. Demand stems from rapid 5G roll-outs, new e-Call and ADAS mandates, and the shift toward software-defined vehicles that rely on seamless connectivity. OEMs view embedded modules as the backbone for subscription services and data monetization, with potential revenue of USD 1,600 per vehicle from connected offerings. Growth is bolstered by the spread of cellular vehicle-to-everything (C-V2X) standards and edge AI chipsets that lower latency for safety-critical functions.

Key Report Takeaways

- By end-user type, OEM channels led with 62.68% of connected car devices market share in 2025, while aftermarket solutions are projected to advance at a 15.51% CAGR to 2031.

- By communication type, vehicle-to-vehicle technology accounted for 39.05% of the connected car devices market size in 2025; vehicle-to-grid is poised for the fastest 14.92% CAGR through 2031.

- By product type, driver assistance systems commanded 40.74% share of the connected car devices market size in 2025, whereas cybersecurity hardware will expand the quickest at 14.67% CAGR.

- By connectivity technology, embedded solutions dominated with 48.22% revenue share in 2025, and the C-V2X segment is on course for a 15.19% CAGR.

- By vehicle propulsion type, internal-combustion models retained 75.62% share in 2025; battery electric vehicles will register the highest 14.93% CAGR this decade.

- By geography, North America held 38.26% connected car devices market share in 2025, although Asia Pacific is forecast to post the strongest 15.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Connected Car Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid 5G Roll-Out and Carrier-OEM | +3.2% | Global, with early gains in China, South Korea, US | Medium term (2-4 years) |

| Mandatory E-Call and ADAS Regulations | +2.8% | North America and EU core, China implementation | Short term (≤ 2 years) |

| Subscription-Based Revenue Targets | +2.1% | Global, premium segments first | Medium term (2-4 years) |

| Edge AI Chips Enabling | +1.9% | Global, led by premium and EV segments | Long term (≥ 4 years) |

| Usage-Based-Insurance Driving | +1.7% | North America and EU, expanding to Asia-Pacific | Medium term (2-4 years) |

| Cross-Industry App-Store Ecosystems | +1.4% | Global, concentrated in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid 5G Roll-Out and Carrier-OEM Partnerships

Automotive 5G connections are forecast to grow exponentially in enablement revenues by 2027. Cisco and TELUS already provision more than 1.5 million 5G vehicles on automated platforms, cutting latency to near-real-time levels critical for autonomous features. Partnerships now bundle connectivity, edge computing, and developer tools into unified offerings that let OEMs launch new services faster. These alliances change the supplier landscape because carriers shift from bandwidth providers to strategic technology partners. The resulting service platforms underpin premium infotainment, remote diagnostics, and high-definition maps, supporting higher average revenue per user.

Mandatory E-Call and ADAS Regulations

The National Highway Traffic Safety Administration requires automatic emergency braking with pedestrian detection on all light vehicles by September 2029, carrying USD 354 million in annual compliance costs and lifetime benefits topping USD 5.82 billion[1]“Automatic Emergency Braking Final Rule,” National Highway Traffic Safety Administration, nhtsa.gov . Europe enforces e-Call and a suite of driver-assistance functions under the General Safety Regulation, while China scales vehicle-road-cloud pilots with more than 7,000 5G-A base stations in Beijing. These mandates remove uncertainty around timelines, prompting OEMs to integrate connected sensors as standard equipment. Suppliers benefit from predictable volumes, and consumers gain universal safety features that lower accident rates.

Subscription-Based Revenue Targets

Automakers seek recurring income as hardware margins tighten. Volvo’s EX90 electric SUV runs Qualcomm’s digital cockpit to unlock features on demand, and Volkswagen’s Cariad unit explores paid automated-driving packages. Industry projections show software accounting for more than three-fourths of vehicle innovation. Success rests on delivering clear consumer value while avoiding pushback over paywalls for basic functions. Platforms must support secure over-the-air updates, usage analytics, and flexible billing so brands can personalise offerings without compromising safety or performance.

Edge AI Chips for In-Vehicle Inferencing

NXP’s S32N55 and Honda-Renesas’ forthcoming 2,000 TOPS processor illustrate the migration to centralised, AI-ready architectures[2]“S32N55 Vehicle Super-Integration Platform,” NXP Semiconductors, nxp.com. Putting compute at the edge reduces cloud reliance, enabling real-time driver monitoring, sensor fusion, and predictive maintenance even when connectivity is poor. Due to advanced AI hardware, semiconductor content per vehicle is forecast to double by 2030. Consolidating multiple electronic control units into domain controllers trims wiring, saves weight, and simplifies updates, yet requires robust thermal management and cybersecurity protections baked into silicon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-Security Vulnerabilities | -2.4% | Global, acute in premium segments | Short term (≤ 2 years) |

| High BOM Cost of Multi-Band V2X | -1.8% | Global, concentrated in emerging markets | Medium term (2-4 years) |

| Data-Cloud Egress Fees Eroding OEM | -1.6% | Global, concentrated in North America and EU | Medium term (2-4 years) |

| Semiconductor Supply-Chain Fragility | -1.4% | Global, acute in Asia Pacific manufacturing | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Vulnerabilities and Recalls

The Pwn2Own Automotive 2024 contest exposed a zero-click exploit in Alpine’s Halo9 infotainment unit with a 96% success rate, highlighting the ease of remote compromise[3]“Automotive 2024 Contest Results,” Pwn2Own, pwn2own.com. Software-related recalls affected over 30 million vehicles in 2023, and the NIST-listed CVE-2023-6248 flaw enables full device takeover of popular telematics gateways. As vehicles become rolling data centres, their attack surface expands, raising the cost of post-sale patches and reputational damage. Regulators demand security-by-design, pushing suppliers to embed hardware root-of-trust, secure over-the-air frameworks, and continuous penetration testing.

High BOM Cost of Multi-Band V2X Modules

Supporting DSRC, C-V2X, and emerging 5G sidelink in one box elevates RF complexity and production cost. Automotive semiconductors are on track to top the chart by 2027, with V2X radios among the most expensive components. OEMs face a choice: diversify SKUs by region to cut costs or fit universal modules that preserve global platforms. The interim overlap of DSRC and C-V2X limits economies of scale, and price-sensitive markets weigh connectivity against core mechanical content. Until volumes rise and standards converge, high module pricing will restrain adoption outside premium segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Type: OEM Dominance Drives Integration

OEM installations captured 62.68% of the connected car devices market share in 2025 because factory-fitted hardware integrates deeply with vehicle diagnostics, power management, and warranty frameworks. Automakers embed modules during assembly to ensure compliance with e-Call and ADAS mandates, streamline over-the-air upgrades, and bolster brand control over data. Growing reliance on software-defined architectures cements this channel’s leadership as OEMs link connectivity to revenue-generating services such as remote feature activation and predictive maintenance.

However, aftermarket providers are expanding quickly, with a 15.51% CAGR, as insurers and fleet managers retrofit legacy assets. Plug-and-play dongles and hardwired black boxes supply real-time usage data that underpins behaviour-based premiums and asset tracking. HARMAN’s ready-upgrade kits exemplify solutions tailored for mixed fleets needing installation speed and cross-brand compatibility. While OEM control remains strong, price-sensitive owners and commercial operators continue to drive a parallel aftermarket, ensuring competitive variety within the connected car devices market.

By Communication Type: V2V Leads Current Deployment

Vehicle-to-vehicle links represented 39.05% of the connected car devices market revenue share in 2025 because they deliver collision warnings without requiring roadside units. Mature standards and demonstrated safety gains encourage OEMs to adopt V2V first, particularly in high-volume models aiming for five-star safety ratings. Retrofits also proliferate in commercial fleets where forward-collision alerts cut downtime and insurance costs.

Vehicle-to-grid capability is projected to post a 14.92% CAGR to 2031 as energy utilities partner with automakers to stabilise renewable-heavy grids. Bidirectional chargers paired with connectivity let electric cars feed stored power back to the network, creating new revenue for owners and grid operators. Growth in vehicle-to-infrastructure and vehicle-to-pedestrian segments follows smart-city spending, yet these depend on broader public investment. Over time, integrated V2X suites will blend all modes, but V2V will remain the cornerstone while ecosystems mature around it.

By Product Type: ADAS Systems Command Market Leadership

Driver assistance systems held a 40.74% share of the connected car devices market in 2025, reflecting regulatory deadlines for automatic emergency braking, lane-keeping, and intelligent speed assistance. Combining radar, camera, and LiDAR data with connectivity allows vehicles to access cloud-based maps and traffic information that sharpen sensor performance. Consumers perceive immediate safety benefits, justifying higher sticker prices in mass-market segments.

Cybersecurity hardware, though niche in revenue today, will expand fastest at 14.67% CAGR as software-centric vehicles demand dedicated processors for anomaly detection, encryption, and secure boot. Telematics boxes remain essential for fleet monitoring, utilisation, and maintenance cycles, while infotainment platforms evolve into digital cockpits that unify entertainment, navigation, and climate controls. Suppliers that bundle ADAS, infotainment, and security into modular architectures can capture greater value as product boundaries blur within the connected car devices market.

By Connectivity Technology: Embedded Solutions Dominate

Embedded modems secured 48.22% revenue share in 2025 because buyers always expect on-demand services without extra devices. Native SIMs simplify provisioning, updates, and diagnostics, allowing automakers to guarantee performance across global roaming partners. Subscription bundling through carriers further entrenches embedded designs as the default for premium and volume models.

Cellular V2X adoption will climb at a 15.19% CAGR as 5G Standalone networks enable higher throughput, enhanced sidelink range, and future automated-driving features. Integrated and tethered options persist in niche applications: tethered dongles suit lower-priced cars and aftermarket retrofits, while integrated solutions balance flexibility and cost for mid-tier trims. Convergence toward software-defined radios that toggle between 4G, 5G, and Wi-Fi will reduce SKUs, but embedded architectures will remain the anchor of the connected car devices market.

By Vehicle Propulsion Type: ICE Vehicles Maintain Share Leadership

Internal-combustion platforms contributed 75.62% of 2025 unit shipments, ensuring they stay the largest revenue pool for connected hardware this decade. Retrofits of e-Call, telematics, and basic infotainment to ICE models allow OEMs to monetise data and comply with safety rules while capitalising on existing production lines. These volumes underpin scale economies that lower component costs across all propulsion types.

Battery electric vehicles will grow at 14.93% CAGR as zero-emission mandates tighten. Their high-voltage architectures and centralised software stacks make them ideal hosts for advanced connected services such as intelligent charging, route-based energy optimisation, and vehicle-to-home power export. Hybrid and fuel-cell variants also gain from connectivity that synchronises propulsion modes and maintenance cycles. Even as BEV share rises, the sheer installed base of ICE vehicles will keep them a cornerstone customer group within the connected car devices market.

Geography Analysis

North America accounted for 38.26% of the connected car devices market share in 2025. Uptake is driven by federal funding under the Infrastructure Investment and Jobs Act and consumer appetite for premium SUVs brimming with ADAS, high-definition infotainment, and 5G hotspots. Ongoing pilots with the U.S. Department of Transportation and the 5G Automotive Association boost confidence in C-V2X, while tight cybersecurity and privacy rules shape procurement specifications. Canada and Mexico benefit from integrated supply chains, enabling regional OEM plants to standardise connected modules and software stacks. These factors sustain healthy replacement cycles and after-sales subscriptions across North America.

Asia-Pacific is on track for the fastest 15.02% CAGR to 2031. China’s vehicle-road-cloud blueprint anchors public and private spending, with Beijing alone hosting more than 7,000 5G-A base stations for intelligent mobility. Domestic brands embed connectivity to differentiate in a crowded electric-vehicle arena, while regional suppliers deliver cost-optimised telematics for two-wheelers and microcars. Japan and South Korea leverage chip-making prowess and early 5G roll-outs to test next-generation C-V2X sidelink features. India emerges as a high-volume opportunity as safety norms tighten and smartphone-savvy buyers demand always-on infotainment, though price sensitivity keeps tethered solutions relevant.

Europe maintains steady momentum under harmonised regulations such as mandatory e-Call and the General Safety Regulation. Germany, the United Kingdom, and France lead adoption as luxury marques bundle connectivity into premium trim lines, and mid-range brands follow suit. Energy-efficiency and carbon-reduction goals drive interest in vehicle-to-grid pilots that align EV charging with renewable output. Strict data sovereignty laws influence cloud-hosting choices, giving European-based providers an edge. Pan-EU standards for cybersecurity certification are under development, promising to streamline cross-border homologation and further stimulate the connected car devices market.

Regulatory Landscape

Regulation is tightening around safety-critical connectivity and lifecycle cybersecurity management. In the United States, the National Highway Traffic Safety Administration (NHTSA) finalized a rule requiring automatic emergency braking with pedestrian detection on all light vehicles by September 2029, which accelerates OEM integration of connected sensing, compute, and update-capable ECUs used for ADAS feature performance and compliance documentation.

In Europe, the EU Data Act (Regulation (EU) 2023/2854) entered into force in September 2025, creating a compliance driver for standardized vehicle data access and sharing with users and designated third parties, which reshapes telematics back ends and in-vehicle data pipelines. UN ECE WP.29 remains the anchor for global vehicle cybersecurity and software-update governance through UN Regulation No. 155 (CSMS) and No. 156 (SUMS). In June 2026, the United Kingdom Vehicle Certification Agency (VCA) mandated full compliance for all new vehicles with UN R155 and UN R156, and UNECE WP.29/GRVA advanced proposals in 2026 to tighten oversight by linking management-system certificates more directly to the vehicle type-approval authority.

Value Chain Analysis

The connected car devices value chain covers semiconductor and RF content (modems, GNSS, secure elements), Tier 1 integration (telematics control units, digital cockpit/infotainment, ADAS domain controllers, and cybersecurity hardware), OEM E/E architecture and software integration, and post-sale operations (OTA update platforms, cloud data storage and analytics, billing and subscription management, and fleet and insurance applications). As software-defined vehicle programs scale, value capture is shifting toward platform software, cloud operations, and data services, while embedded connectivity (eSIM/iSIM provisioning, carrier platforms, and roaming) increasingly sits in the bill-of-materials and the service delivery stack.

Constraints and leverage points sit at integration and compliance boundaries. Multi-band V2X hardware raises BOM and validation complexity, and cybersecurity management requirements (CSMS/SUMS) add ongoing process costs across suppliers and OEMs. Geopolitics is also reshaping sourcing and vendor qualification, including the U.S. Department of Commerce final rule (January 2025) restricting certain connected-vehicle hardware and software transactions with supply-chain links to China and Russia, which pushes OEMs and Tier 1s to re-map module sourcing, software components, and cloud back ends to maintain market access. Partnerships that combine component specialists and platform enablers, such as FocalPoint working with STMicroelectronics to integrate S-GNSS Auto onto Teseo devices (July 2026), also show the growing emphasis on reference designs and interoperable building blocks to shorten design-in cycles.

Competitive Landscape

The connected car devices market is moderately fragmented, yet competition intensifies as semiconductor houses, cloud hyperscalers, and telecom equipment firms challenge established Tier 1 suppliers. Infineon’s purchase of Marvell’s Automotive Ethernet unit underscores a push toward vertical integration of high-bandwidth networking with power electronics and microcontrollers. Qualcomm’s acquisition of Autotalks adds dual-mode DSRC/C-V2X capabilities to the Snapdragon Digital Chassis, signaling a race to offer turnkey platforms that blend connectivity, compute, and AI accelerators.

Partnerships now set the pace of innovation. Bosch and Microsoft combine domain expertise with generative AI to automate software-validation workflows, shortening release cycles for over-the-air updates. AWS collaborates with Toyota to host connected service back-ends, while Google extends Android Automotive OS and app services to multiple European brands. These alliances let carmakers tap cloud scale without relinquishing brand identity, accelerating service deployment across model ranges.

White-space opportunities abound in cybersecurity and edge inference. Specialists such as Blaize offers energy-efficient graph-streaming processors for real-time perception. As architectures converge on centralised compute, suppliers that can deliver secure, upgradeable, and standards-compliant modules gain bargaining power. At the same time, price pressure and overlapping portfolios spur consolidation, suggesting further mergers as players seek scale in the connected car devices market.

Connected Car Devices Industry Leaders

Continental AG

Denso Corporation

Robert Bosch GmbH

Autoliv Inc.

Valeo SA

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Data-access compliance and standardization are creating concrete whitespace for interoperable telematics and data-sharing layers across OEM and aftermarket ecosystems. The EU Data Act (in force since September 2025) is pushing manufacturers and suppliers toward technical approaches for sharing vehicle-generated data, and COVESA has positioned Vehicle Signal Specification (VSS) and Vehicle Information Service Specification (VISS) as practical standards to operationalize data exchange across platforms. Suppliers that can pair in-vehicle security hardware (root-of-trust, secure boot, secure OTA) with compliant data interfaces can reduce rework across regions and brands.

Platform consolidation across cockpit, connectivity, and ADAS is also opening opportunities for suppliers with scalable, upgradeable device architectures aligned to software-defined vehicle roadmaps. In May 2026, Stellantis expanded its partnership with Qualcomm to adopt Snapdragon Digital Chassis capabilities (connectivity, cockpit, and driver assistance) alongside its STLA Brain platform, reflecting demand for pre-integrated compute and connectivity stacks that simplify multi-brand rollouts. On the carrier side, Verizon began providing 5G Standalone and LTE connectivity for newly manufactured BMW Group vehicles in the United States via KDDI's Global Communications Platform (July 2026), reinforcing an opportunity for device and module vendors that can meet carrier certification, enable remote provisioning, and support low-latency services for connected safety, diagnostics, and subscription delivery.

Recent Industry Developments

- June 2026: Denso's MobiQ C-V2X roadside unit module achieved OmniAir Module Certification after testing at a DEKRA laboratory in Spain. Certification strengthens interoperability claims for infrastructure-to-vehicle deployments and supports procurement by agencies and integrators that require standardized conformance evidence.

- June 2025: Continental began supplying its CoSmA ultra-wideband (UWB) digital access system for the Audi Q6 e-tron. The start of series supply signals growing OEM adoption of secure, smartphone-based access features that depend on robust in-vehicle connectivity and cybersecurity design.

- April 2024: Trend Micro's Zero Day Initiative ran the Pwn2Own Automotive 2024 contest, where researchers demonstrated a zero-click exploit against Alpine's Halo9 infotainment unit. The result reinforced how infotainment and telematics endpoints expand the attack surface, accelerating demand for hardware-backed security and secure update pipelines across connected car device programs.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the connected car devices market covers the in-vehicle hardware and embedded device layer that enables vehicle connectivity, data exchange, and driver and vehicle interaction through telematics, V2X communication, and connected safety and infotainment functions.

Scope exclusions: We exclude recurring connectivity service subscriptions, standalone smartphone apps, and pure software-only platforms when they are sold without an associated in-vehicle device.

Segmentation Overview

- By End-User Type

- OEM

- Aftermarket

- By Communication Type

- V2V

- V2I

- V2P

- V2N

- V2G

- By Product Type

- Driver Assistance System (ADAS)

- Telematics

- In-Car Infotainment

- Cyber-security Hardware

- By Connectivity Technology

- Embedded

- Integrated

- Tethered

- DSRC

- C-V2X (4G/5G)

- By Vehicle Propulsion Type

- Internal-Combustion Engine Vehicles

- Electric Vehicles

- Battery Electric Vehicle

- Hybrid Electric Vehicle

- Fuel-cell Electric Vehicle

- Plug-in Hybrid Electric Vehicle

- By Geography

- North America

- United States

- Canada

- Rest of North America

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Italy

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to build the starting structure of the market and to anchor the model to measurable signals like vehicle production, parc, and connectivity rollouts. We referred to public sources such as national transport agencies, telecom regulators and standards bodies, ITU releases, UNECE and other vehicle safety regulations, and statistics from groups such as OICA for production and registrations. To keep assumptions realistic, supporting reads were also taken from peer-reviewed mobility and V2X research papers, patent databases, and reputable automotive and electronics press.

Alongside public sources, we used paid subscriptions for company financials and intelligence, news and financials, and patent coverage to map product positioning and to sanity-check revenue exposure to connected device lines. Where trade flows mattered (for modules and electronic sub-assemblies), shipment-level import and export datasets were consulted to validate directionally if supply trends matched adoption claims. The sources listed here are illustrative only, and many additional public documents and filings were reviewed for clarification and cross-checking.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with OEM-side program teams, Tier-2 and module suppliers, aftermarket channel participants, and engineering focused subject experts across APAC, EMEA, and the Americas. These conversations helped us convert broad adoption statements into usable inputs, such as device content per vehicle, typical feature bundles by trim, and timing of C-V2X versus DSRC transitions. When conflicting views appeared, follow-ups were done so assumptions could be tightened before finalizing the model.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 14% | APAC: 40% |

| Mid tier: 48% | Functional/Unit leaders: 32% | EMEA: 34% |

| Smaller Players: 19% | Managers: 54% | Americas: 26% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand reconstruction where vehicle production and parc were translated into an addressable connected device pool, and then filtered by connectivity penetration and feature fit by vehicle class and region. That first pass was then corroborated with selective bottom-up checks, such as sampled device ASPs multiplied by implied unit volumes for key device categories, plus channel checks for aftermarket attachment rates, which helped adjust totals when a region looked overstated.

Inputs used in the model were practical and observable, including new vehicle production and registration trends, share of connected trims, telematics control unit and V2X module fitment rates, 4G to 5G and C-V2X rollout timing, typical per-vehicle electronics content changes, and regulatory markers like eCall related requirements where applicable. Forecasting relied on scenario analysis supported by a simple multivariate regression layer, where penetration, vehicle output, and connectivity technology mix were the main drivers discussed and stress-tested with industry experts. If a bottom-up check had missing data for a device type in a smaller country, proxy ASPs and adoption ratios were applied from a comparable market and then revalidated through additional calls.

Data Validation & Update Cycle

Validation was done through step-by-step triangulation across independent indicators, where model outputs were compared against vehicle build plans, connectivity adoption signals, and reported electronics content trends. Outliers were investigated at the variable level so we could see whether the gap came from unit assumptions, ASP paths, or regional mix, and then it was reworked before sign-off.

A second analyst review was conducted to confirm math integrity, consistent scope application, and that the final growth path matched the stated drivers. The report is refreshed annually, and interim updates are made when material events occur, such as regulation changes or sharp shifts in vehicle output. Before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Connected Car Devices Market Estimate Compared With Other Published Estimates

Published numbers for connected car devices rarely match perfectly because the term can cover different things, and each publisher picks its own mix of hardware, software, and service revenue. Differences also show up from the year chosen as the starting point, the currency conversion timing, and how fast technology mix shifts are assumed.

Connectivity service subscriptions sit outside Mordor Intelligence's scope for this market, which is a key reason the 2026 value looks lower than estimates that blend device value with recurring data plans and platform fees. The remaining gaps usually come from whether aftermarket devices are counted the same way as OEM-fit units, how ADAS versus telematics device content is treated, and whether C-V2X adoption is modeled as an early jump or a gradual ramp tied to network and vehicle platform cycles.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 72.52 B (2026) | |

| Global Consultancy A | USD 138.03 B (2025) | Uses an earlier base year and appears to include a broader definition that can blend device value with connected services and platform related revenues, which pushes up the 2025 starting point. |

| Industry Publisher B | USD 62.10 B (2025) | Focuses on a sales-market lens with narrower product groupings and different technology splits, which can undercount higher value device categories when feature bundling and OEM-fit content per vehicle are treated conservatively. |

The table shows that the spread is mostly explained by scope and timing, rather than arithmetic. When device-only revenue is kept separate from recurring services and the adoption ramp is tied to vehicle production cycles, the resulting market size becomes easier to trace back to clear variables and to re-check during updates.

Key Questions Answered in the Report

What is the current size of the connected car devices market?

The connected car devices market size reached USD 72.52 billion in 2026 and is projected to double to about USD 143.47 billion by 2031 on a 14.62% CAGR.

Which region leads the market?

North America held 38.26% market share in 2025 due to regulatory mandates and high premium-vehicle penetration.

Why are OEMs focusing on subscription services?

OEMs aim to offset tightening hardware margins by unlocking recurring revenue, with potential connected-service earnings of USD 1,600 per vehicle.

What segments are growing the fastest?

Vehicle-to-grid communication, cybersecurity hardware and battery electric vehicles each post CAGRs above 13.5% through 2031.

How are cybersecurity risks being addressed?

Automakers now embed hardware root-of-trust, run continuous penetration tests and partner with specialist firms to meet emerging security-by-design regulations.

What role will 5G play in connected vehicles?

Standalone 5G cuts latency to near-real-time, enabling advanced driver assistance, high-definition mapping and future autonomous driving functions while supporting new carrier-OEM service platforms.

Page last updated on: