Automotive Belts And Hoses Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

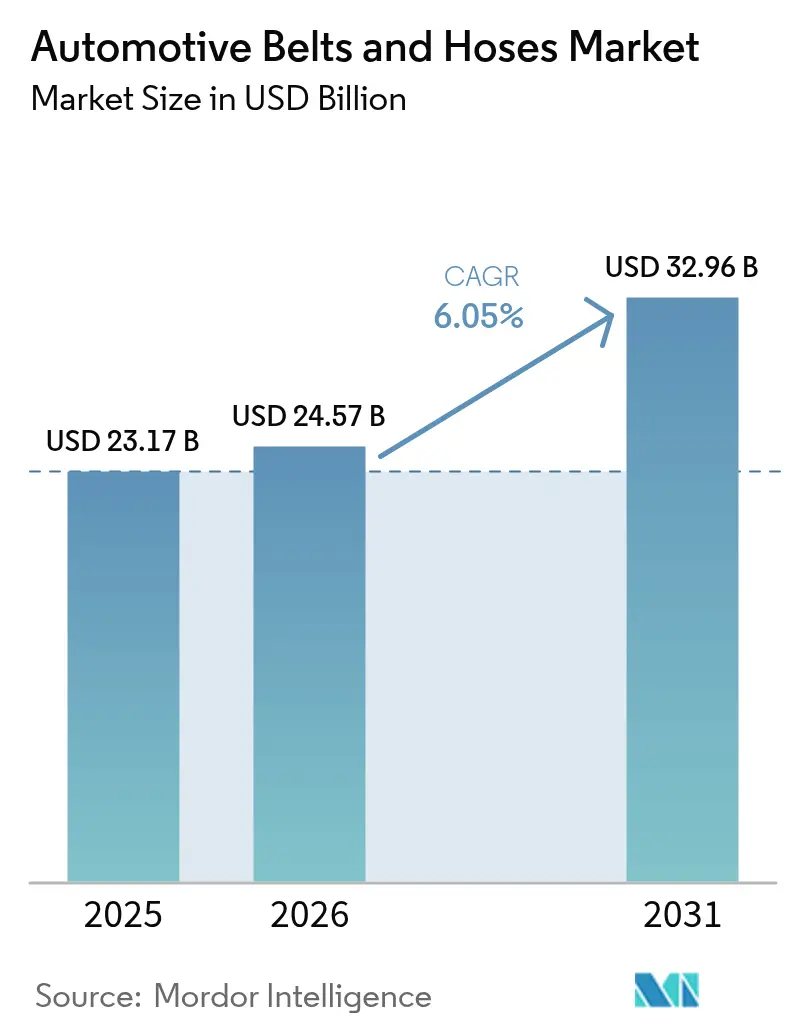

| Market Size (2026) | USD 24.57 Billion |

| Market Size (2031) | USD 32.96 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

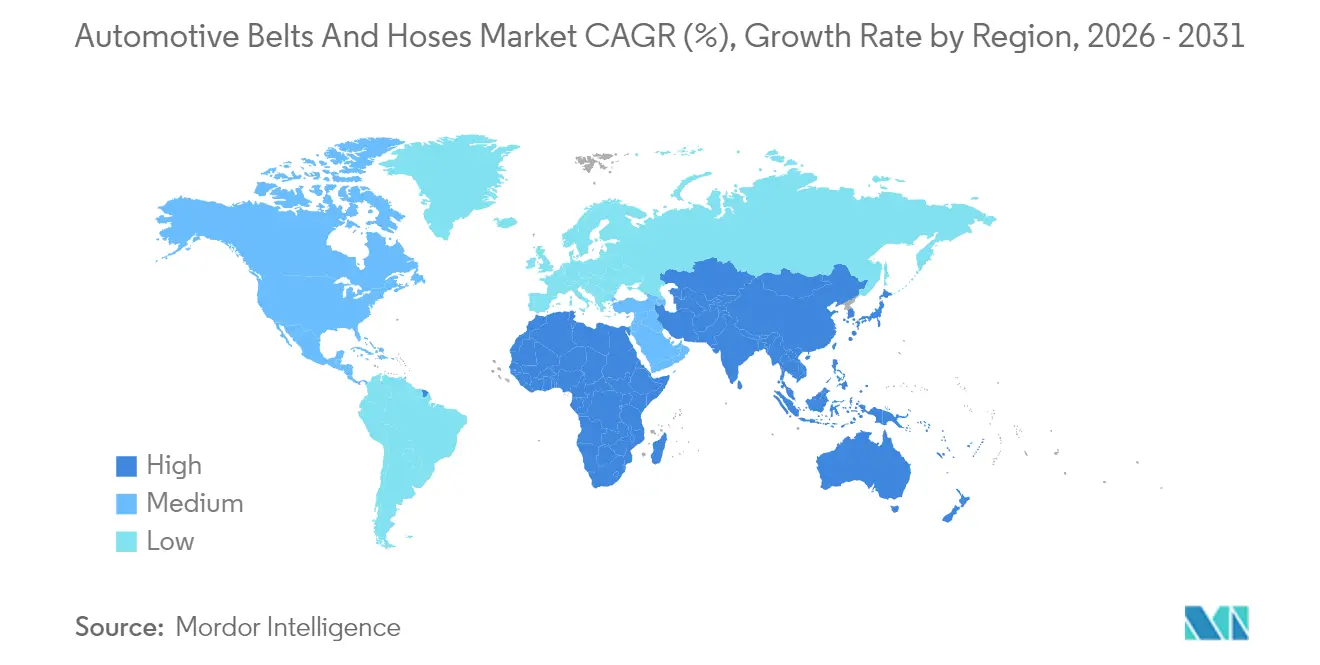

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Belts And Hoses Market Analysis by Mordor Intelligence

The Automotive Belts And Hoses Market size is expected to grow from USD 23.17 billion in 2025 to USD 24.57 billion in 2026 and is forecast to reach USD 32.96 billion by 2031 at 6.05% CAGR over 2026-2031. Powertrain electrification, tightening fuel-efficiency mandates, and stringent emissions rules are reshaping component specifications and lifting demand for lightweight, heat-resistant products. Asia Pacific continues to anchor global volume with expanding OEM output and a rapidly maturing aftermarket, while premiumization trends in North America and Europe raise average selling prices. Lengthening vehicle life, now averaging more than a decade in the United States, sustains replacement cycles and strengthens the aftermarket channel. Raw-material inflation, led by a spike in natural-rubber prices in 2024, squeezes supplier margins yet accelerates the search for bio-based elastomers that can stabilize long-term cost structures. Competitive intensity remains moderate, with tier-one suppliers racing to deliver EV-ready thermal-management solutions and to defend branded positions against counterfeit influx in emerging economies.

Key Report Takeaways

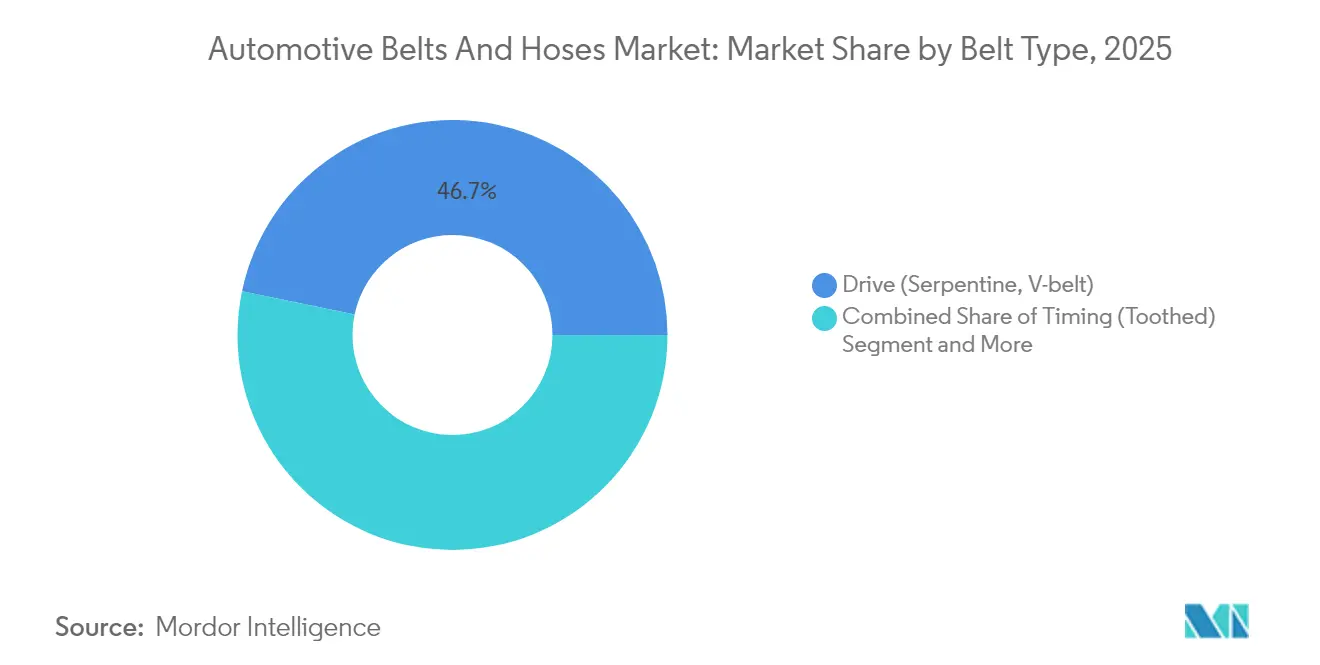

- By belt type, drive belts captured 46.73% of the automotive belts and hoses market share in 2025, while accessory and stretch-fit belts recorded the highest projected CAGR at 6.25% through 2031.

- By hose type, heating and cooling hoses held a 29.12% share of the automotive belts and hoses market size in 2025 and emission as well as EV thermal-management hoses are advancing at a 6.32% CAGR through 2031.

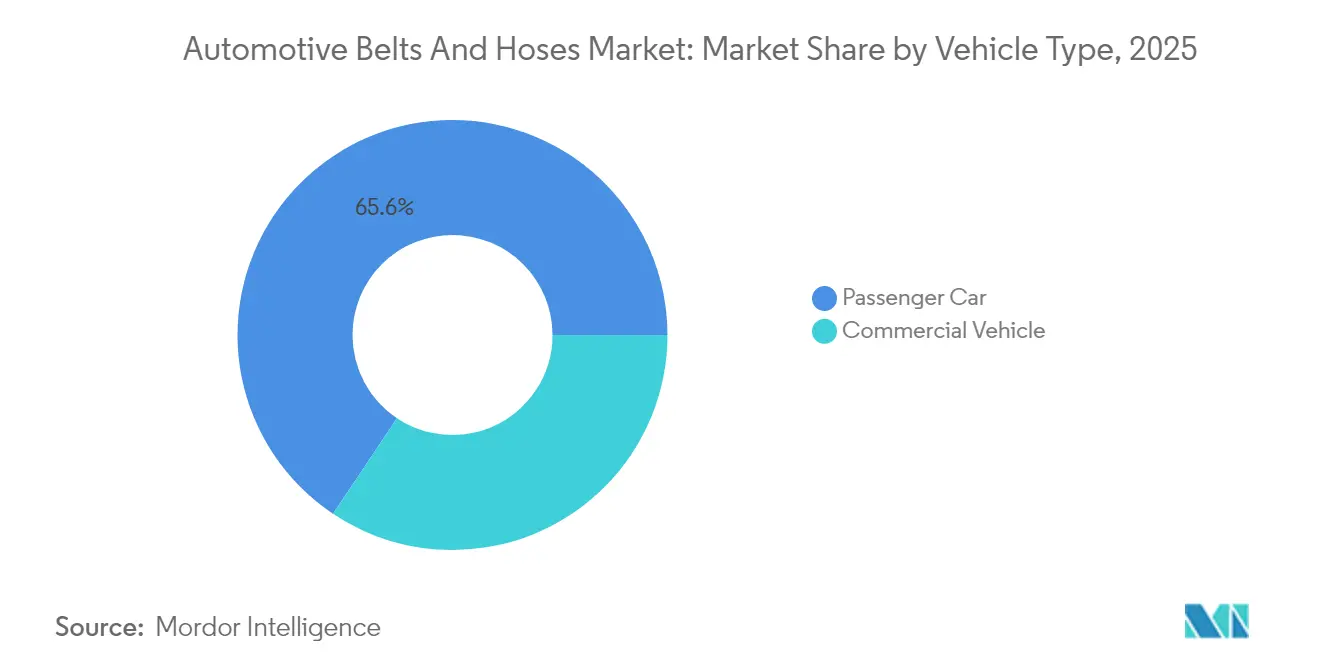

- By vehicle type, passenger cars accounted for 65.62% of the automotive belts and hoses market share in 2025; commercial vehicles are forecast to expand at a 6.38% CAGR to 2031.

- By sales channel, the aftermarket commanded 56.15% of the automotive belts and hoses market share in 2025, and is growing at a 6.29% CAGR through 2031.

- By geography, Asia Pacific led with 44.08% of the automotive belts and hoses market share in 2025, while the Middle East and Africa region is set to grow fastest at a 6.42% CAGR during the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Belts And Hoses Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Vehicle Parc Growth In Asia | +1.2% | Asia Pacific, with spillover to Middle East and Africa | Medium term (2-4 years) |

| Turbo-Downsizing Lifts High-Temp Silicone Hoses | +0.9% | Global, concentrated in developed markets | Short term (≤ 2 years) |

| BEV/Tesla-Style Auxiliary Belt Elimination | +0.8% | Global, led by North America and EU | Long term (≥ 4 years) |

| OTA Predictive Maintenance | +0.7% | North America and EU, expanding to Asia Pacific | Long term (≥ 4 years) |

| Tier-1 Push For Lower NVH | +0.6% | Global | Medium term (2-4 years) |

| Hydrogen ICE Prototypes | +0.3% | EU and Japan, pilot programs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Vehicle Parc Growth In Asia Boosts Service Belt Replacements

Rapid expansion of the vehicle population across China, India, and ASEAN economies is generating a compound effect on replacement demand. As warranty coverage lapses, independent workshops gain business, creating more opportunities for branded belts and hoses. Chinese OEM investments in Thai EV production under the EV3.5 program, which targets up to 525,000 units anually by 2027, exemplify the regional momentum[1]“EV3.5 Incentive Program Targets 525,000 EVs by 2027,” Thailand Board of Investment, boi.go.th . Even battery-electric models retain belt-driven components for air conditioning and thermal management, ensuring continuous relevance for high-performance belts. Regulatory inspection mandates in markets such as India formalize replacement intervals and discourage counterfeit parts, while the Indian automotive aftermarket is on track to grow expoenentially by 2028[2]“Indian Automotive Aftermarket Report 2024,” Automotive Component Manufacturers Association of India, acma.in . Suppliers able to scale localized distribution will benefit most as workshops seek reputable components for increasingly sophisticated drivetrains.

Turbo-Downsizing Lifts High-Temp Silicone Hoses

Smaller displacement engines with higher boost pressure expose charge-air pathways to extreme heat and pulsation. Conventional rubber loses flexibility above 150 °C, whereas silicone maintains mechanical strength beyond 200 °C, preventing micro-leaks that degrade turbo efficiency. Adoption is strongest in Europe and North America, where stringent fuel-economy rules incentivize downsized turbo engines. Commercial-vehicle operators also favor silicone because extended service intervals lower total cost of ownership. The shift benefits hose makers with automated multi-layer extrusion lines capable of bonding silicone to fluorosilicone liners that block oil permeation. As turbocharging remains integral to meeting near-term emissions targets, silicone hoses are expected to outpace overall market growth.

BEV/Tesla-Style Auxiliary Belt Elimination Spurs Lightweight Belts

Electric-vehicle architectures consolidate or remove traditional serpentine systems, yet the remaining belt applications must deliver higher power density with minimal service intervention. Tesla’s integration of electric compressors cuts belt count but raises thermal-management demands, accelerating OEM adoption of stretch-fit and micro-V designs. Continental responded with its CONTI NXT Multi V-belt that uses renewable materials without sacrificing tensile strength. The value per unit rises because each retained belt must exhibit minimal noise, vibration, and harshness while withstanding wider temperature swings. EPDM and aramid-reinforced constructions thus gain share, allowing tier-one suppliers to charge premium prices despite lower overall unit volumes in fully electric platforms. Over the forecast horizon, lightweight belts are projected to capture a growing slice of accessory-drive applications as OEMs pursue efficiency gains.

OTA Predictive Maintenance Drives Aftermarket Replacements

Connected-vehicle platforms analyze belt tension and hose pressure to forecast failure and schedule replacements before breakdowns occur. Fleets exploit this data to reduce unplanned downtime, raising demand for OE-equivalent components recommended by predictive algorithms. The European aftermarket, is rapidly digitizing service workflows, a trend mirrored in the United States where average fleet size per operator is increasing. Components that integrate RFID tags or QR-based authentication align with remote diagnostics and discourage counterfeit substitution. Over-the-air updates further refine replacement windows, compressing the traditional three-to-five-year cycle and adding incremental volume for premium suppliers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ICE Phase-Out Shrinks Timing-Belt TAM | -1.8% | Global, led by EU and California | Long term (≥ 4 years) |

| Raw-Material Volatility | -1.1% | Global | Short term (≤ 2 years) |

| Counterfeit Parts Erode Branded Share | -0.7% | Asia Pacific and emerging markets | Medium term (2-4 years) |

| Belt-Failure Lawsuits | -0.4% | North America and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

ICE Phase-Out Shrinks Timing-Belt Tam After 2030

Regulators are converging on aggressive electrification goals that remove camshaft synchronization from future powertrains. The U.S. EPA targets a fleet average of 85 g CO₂ per mile by 2032, a level that effectively obliges OEMs to prioritize zero-tailpipe technologies. The European Union’s Euro 7 timetable begins in 2026 with even stricter cumulative lifetime emissions limits. As electric models proliferate, demand for timing belts declines, particularly inside mature markets where replacement cycles historically drove steady aftermarket revenue. OEM warranty extensions, typified by Stellantis covering timing-belt failures for up to a decade, soften customer concerns yet underscore the component’s finite future. Timing-belt suppliers must therefore diversify into chain-driven hybrid kits, high-density accessory belts, or sensor-embedded products to remain relevant.

Raw-Material Volatility Squeezes Margins

Natural-rubber output contracted after severe weather reduced harvests in Thailand and China, lifting global prices by two-fifth in 2024. The Association of Natural Rubber Producing Countries projects production growth of only 0.3% versus demand growth of 1.8% in 2025, pointing to persistent tightness. Synthetic rubber offers limited relief because crude-oil price swings and trade tariffs inflate styrene-butadiene costs. Automotive belts and hoses accounts signifcantly for natural-rubber as key raw material, so component makers are exposed to cost spikes that OEMs resist absorbing. Suppliers hedge through long-term contracts and explore bio-based alternatives such as guayule, yet material substitution is constrained by performance requirements. Margin pressure is set to endure over the next two years until plantation supply rebounds or alternative polymers reach commercial scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Belt Type: Drive Belts Lead Despite Stretch-Fit Innovation

Drive belts generated the largest revenue share at 46.73% in 2025, underscoring their indispensable status in alternator, water-pump, and compressor drives. The automotive belts and hoses market size for drive belts is projected to expand steadily because the installed base of internal-combustion and hybrid vehicles remains sizable. Accessory and stretch-fit belts, although smaller in volume, are advancing at a 6.25% CAGR due to OEM mandates for maintenance-free assemblies that cut warranty risk. These belts eliminate tensioners, trim mass, and improve fuel economy. The automotive belts and hoses market benefits as premium elastomers such as EPDM and HNBR escalate average unit price. Continental’s Conti Unipower elastic series illustrates this shift toward tensioner-less systems that still meet stringent NVH thresholds.

Automakers favor micro-V and poly-V profiles for space-constrained electric platforms because they enable higher power transmission per millimeter of width. Timing belts continue to serve the existing parc, but their long-term trajectory skews downward as electrification accelerates. Suppliers mitigate exposure by bundling timing-belt kits with water-pump replacements, a practice that lifts basket size during service visits. Gates’ hybrid-oriented timing-chain kits demonstrate how belt manufacturers diversify into adjacent technologies to offset any decline in conventional belt demand. As long as global ICE production persists, drive belts will anchor supplier revenue, yet strategic investment increasingly funnels toward stretch-fit and micro-V variants that align with future powertrain architectures.

By Hose Type: Thermal Management Drives Innovation

Heating and cooling hoses held 29.12% of the automotive belts and hoses market share in 2025, reaffirming their universal requirement across all propulsion types. Electric models intensify demand for precise thermal control of batteries, inverters, and motors, shifting specification toward multi-layer EPDM or silicone constructions that handle dielectric coolants. The automotive belts and hoses market size for emission and EV thermal-management hoses is anticipated to grow at 6.32% CAGR, the fastest among hose categories, as OEMs install dedicated cooling loops for high-voltage components.

Fuel lines retain relevance in hybrid and traditional vehicles but face gradual erosion beyond 2030. Brake hoses gain from new safety norms that demand higher burst strength under regenerative braking conditions. Meanwhile, turbocharger hoses capitalize on the downsizing trend in commercial vehicles that still rely on diesel power. Hose suppliers with advanced fluorosilicone lining technology meet rising temperature and chemical-resistance thresholds. Power-steering hoses decline as electric racks proliferate, yet heavy-duty trucks sustain demand, stabilizing volumes through the forecast horizon.

By Vehicle Type: Commercial Vehicles Accelerate Growth

Passenger cars dominated revenue with 65.62% share in 2025, reflecting sheer unit production. Nevertheless commercial vehicles are on track for a 6.38% CAGR, faster than the broader automotive belts and hoses market, as e-commerce expansion lifts fleet utilization and drives proactive maintenance. High-mileage duty cycles translate into faster belt and hose attrition, multiplying replacement occasions. The segment also benefits from Euro 7 and EPA Phase 2 regulations that force adoption of high-temperature silicone and low-permeation fuel hoses.

Fleet operators demand premium reliability to curb downtime, steering purchases toward branded components with longer service intervals. Continental’s Elite Truck Belt line targets these requirements by integrating aramid cords that resist shock loads. On the hose side, dual-layer charge-air designs address thermal stress from higher turbo boost. Electric light-commercial vehicles add new loops for battery and cabin thermal management, opening fresh revenue pools for specialized hoses despite lower baseline volumes. As infrastructure spending climbs in developing regions, the commercial-vehicle replacement cycle is expected to outpace that of passenger cars.

By Sales Channel: Aftermarket Dominance Strengthens

The aftermarket accounted for 56.15% of revenue in 2025 and is forecast to grow at 6.29% CAGR, outpacing OEM fitment. Lengthening average vehicle age, deferred new-car purchases, and improved distribution in emerging economies extend the aftermarket runway. The automotive belts and hoses market size for the aftermarket segment will climb as predictive maintenance platforms prescribe preemptive part swaps. OE channels continue to influence design and material standards but face lower volumes per vehicle once electrification reduces belt count.

Brand equity matters more in the aftermarket because workshops rely on supplier catalogs and warranty support. Continental added 700 new part numbers during 2024, making it easier for independent garages to source exact-fit components. Gates and Dayco deploy QR-code authentication to fight counterfeit infiltration, safeguarding consumer trust. Rising labor costs also favor high-end belts and hoses that promise longer life, because mechanics and drivers alike seek to avoid repeat jobs.

Geography Analysis

Asia Pacific commanded 44.08% of global revenue in 2025, anchored by China’s production scale and India’s surging service demand. Mainland China is moving toward smart-EV dominance, with electric vehicles projected to grow expoenentially in 2025, catalyzing need for advanced battery-cooling hoses. ASEAN incentives, such as Thailand’s EV3.5 program, amplify regional belt and hose volume as Chinese OEMs establish localized assembly bases. Furthermore, the presence of a developed rubber supply chain supports domestic component manufacture, partially insulating suppliers from international logistics disruptions.

North America maintains solid demand, benefiting from a vehicle age of 12.5 years that lengthens service parts consumption. The United States also sets the pace for connected diagnostics, which channels aftermarket spend toward premium OE-equivalent parts. Canada actively promotes electric light trucks, evidenced by Goodyear’s CAD 575 million investment in Ontario to produce EV-oriented tire and hose products. Europe contributes a substantial share thanks to stringent Euro 7 targets that necessitate premium materials with higher temperature stability and lower permeation. Nonetheless, growth is tempered as belt-eliminating electric architectures gain traction.

The Middle East and Africa logs the fastest regional growth at 6.42% CAGR through 2031. Infrastructure upgrades, especially in the Gulf Cooperation Council states, boost commercial-vehicle fleets that cycle belts and hoses more frequently. African nations benefit from rising used-vehicle imports, which immediately enter the service market and require replacement parts. Improving logistics corridors and e-commerce platforms shorten delivery times for branded components, further stimulating demand. Government-backed industrialization drives local assembly in Morocco, South Africa, and Egypt, adding OEM-fitment volume that supplements aftermarket gains.

Competitive Landscape

Competitive intensity in the automotive belts and hoses market centers on scale, material science expertise, and global supply footprints. Continental, Gates, Dayco, Sumitomo Riko, and Goodyear share leadership, collectively accounting for well above half of OEM supply volumes but leaving ample room for regional specialists. Continental plans to spin off its automotive division by end-2025 to sharpen product focus and attract investment tailored to electrification priorities[3]“Continental to Spin Off Automotive Business by 2025,” Continental AG, continental.com . Gates invests in sensor-embedded belts that feed diagnostic data to fleet management portals, aligning with predictive maintenance trends. Dayco’s new Mexico plant supports near-shoring, reducing transit times to U.S. OEMs and lowering tariff exposure[4]“Dayco Opens New Mexico Belt Manufacturing Plant,” Dayco, dayco.com .

Material innovation is a defining battleground. Suppliers race to commercialize bio-based elastomers and high-temperature composites. Sumitomo Riko leverages expertise in carbon nanotube reinforcement for lightweight hoses suited to battery-electric cooling loops. Goodyear explores guayule as a sustainable rubber substitute, a move that could buffer price volatility. Meanwhile, counterfeit prevention technology, including holographic labels and blockchain tracking, becomes integral as fake belts cost the industry significantly. Gates’ serial number authentication and Continental’s QR-based verification represent leading approaches.

Mergers, strategic alliances, and localized manufacturing continue to reshape market structure. Japanese-Thai joint ventures expand capacity to serve ASEAN EV production goals, while European suppliers adopt “China-for-China” strategies to mitigate decoupling risk. Investment also flows into automated compounding and extrusion lines that cut scrap and improve energy efficiency. The capacity to pivot quickly toward hydrogen ICE and fuel-cell hose specifications will likely determine long-term winners as regulatory agendas broaden decarbonization pathways.

Automotive Belts And Hoses Industry Leaders

Sumitomo Riko Co. Ltd

Toyoda Gosei Co. Ltd

Continental AG

Gates Industrial Corp

Dayco IP Holdings LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Gates Industrial launched timing chain kits targeting hybrid applications, expanding beyond traditional belt products to meet evolving powertrain needs.

- December 2024: Continental announced plans to spin off its automotive business unit into a separate European company by end-2025 under the leadership of Philipp von Hirschheydt.

- March 2024: Dayco commenced full-scale automotive belt production at its new Mexico facility, supporting near-shoring strategies for regional OEMs.

Global Automotive Belts And Hoses Market Report Scope

Belts and hoses are responsible for the overall performance of the vehicle. Belts are an integral part of the engine's powertrain system that transmits power from the flywheel to the camshaft. Fuel efficiency is related to belts, as they regulate the valve positioning. Drive belts and timing belts are two categories of belts. Hoses are flexible pipes that allow the transportation of fluids with varying pressures.

The automotive belts and hoses market has been segmented by belt type, hose type, vehicle type, and geography. By Belt Type, the market has been segmented into drive belts and timing belts. By hose type, the market has been segmented into fuel delivery system hoses, braking system hoses, power steering system hoses, heating and cooling system hoses, and turbocharger hoses.

By vehicle type, the market has been segmented into passenger cars and commercial vehicles and By Geography, the market has been segmented into North America, Europe, Asia-Pacific, and the Rest of the World. For each segment, the market sizing and forecast have been done on basis of value (USD billion).

| Drive (Serpentine, V-belt) |

| Timing (Toothed) |

| Accessory & Stretch-Fit |

| Micro-V / Poly-V |

| Fuel Delivery |

| Brake |

| Power Steering |

| Heating & Cooling |

| Turbocharger & Charge-Air |

| A/C Refrigerant |

| Emission / EV Thermal-Management |

| Passenger Car |

| Commercial Vehicle |

| OEMs |

| Aftermarket |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Belt Type | Drive (Serpentine, V-belt) | |

| Timing (Toothed) | ||

| Accessory & Stretch-Fit | ||

| Micro-V / Poly-V | ||

| By Hose Type | Fuel Delivery | |

| Brake | ||

| Power Steering | ||

| Heating & Cooling | ||

| Turbocharger & Charge-Air | ||

| A/C Refrigerant | ||

| Emission / EV Thermal-Management | ||

| By Vehicle Type | Passenger Car | |

| Commercial Vehicle | ||

| By Sales Channel | OEMs | |

| Aftermarket | ||

| By Region | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the automotive belts and hoses market in 2031?

The market is forecast to reach USD 32.96 billion by 2031, growing at a 6.05% CAGR during 2026-2031.

Which region is expected to grow fastest for automotive belts and hoses through 2031?

The Middle East and Africa is projected to expand at a 6.42% CAGR, outpacing other regions.

Why are accessory and stretch-fit belts gaining popularity?

OEMs favor maintenance-free, lightweight belts that eliminate tensioners and align with fuel-efficiency goals, driving a 6.25% CAGR for this segment.

How does vehicle age influence aftermarket demand for belts and hoses?

A higher average vehicle age, now 12.5 years in the United States, lengthens replacement cycles and lifts aftermarket sales.

What material trend is shaping future hose specifications?

OEMs increasingly specify EPDM and silicone constructions for superior heat resistance, chemical compatibility, and NVH performance.

How are suppliers combating counterfeit automotive belts?

Companies like Gates and Continental deploy QR-code or serial-number authentication systems so workshops can verify genuine parts before installation.

Page last updated on: