United States Automotive Connectors Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

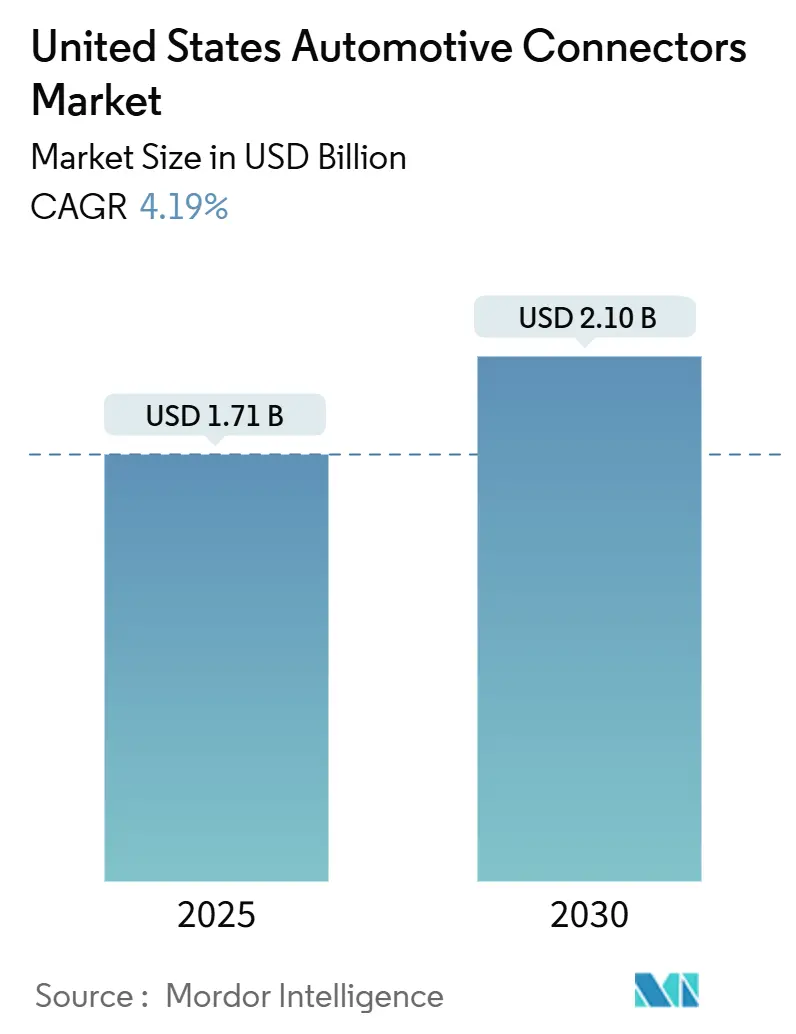

| Market Size (2025) | USD 1.71 Billion |

| Market Size (2030) | USD 2.10 Billion |

| Growth Rate (2025 - 2030) | 4.19% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United States Automotive Connectors Market Analysis by Mordor Intelligence

The United States automotive connectors market size stood at USD 1.71 billion in 2025 and is forecast to reach USD 2.10 billion by 2030, exhibiting a 4.19% CAGR. The expansion is paced by rapid electrification mandates, domestic-content incentives, and the shift from 12 V to 400 V and 800 V electrical architectures. Battery electric vehicles are capturing share from internal-combustion platforms, while 48 V subsystems trim wiring weight and improve power delivery. Federal policy creates nearshoring momentum that shortens supply chains, and the Tesla Low Voltage Connector Standard sets the stage for interface consolidation. Competitive moves focus on acquisitions that deepen technology portfolios and widen factory footprints, positioning incumbents to defend their positions in the United States automotive connectors market. Opportunities revolve around high-voltage battery management, zonal networking, and ruggedized connectors for heavy-duty EV pickups.

Key Report Takeaways

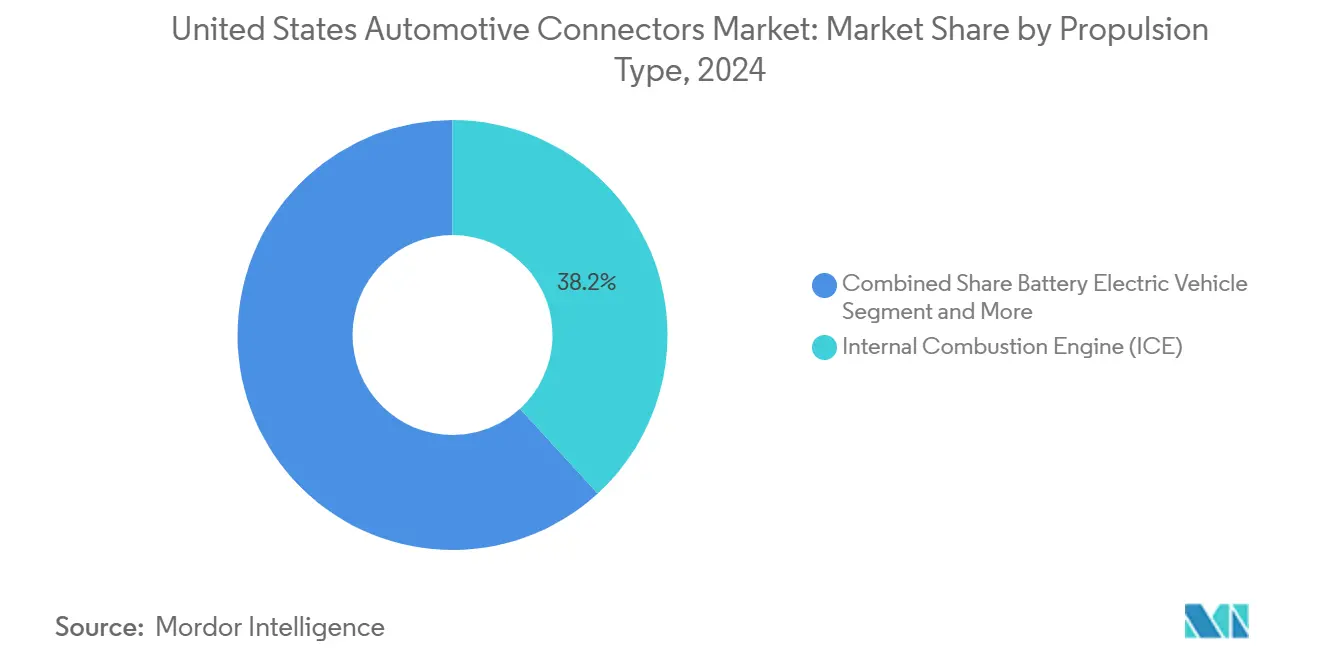

- By propulsion type, battery electric vehicles accounted for the fastest expansion at an 18.54% CAGR while internal-combustion engines retained a 38.21% share of the United States automotive connectors market in 2024.

- By connection type, wire-to-wire interfaces held a 46.37% revenue share in 2024, whereas board-to-board devices registered the highest growth at an 11.26% CAGR through 2030.

- By voltage, low-voltage connectors commanded 57.42% of the United States automotive connectors market share in 2024, and high-voltage products are projected to rise at a 19.27% CAGR to 2030.

- By component, terminal parts made up 43.18% of 2024 revenue, yet housings are advancing the fastest at a 12.83% CAGR.

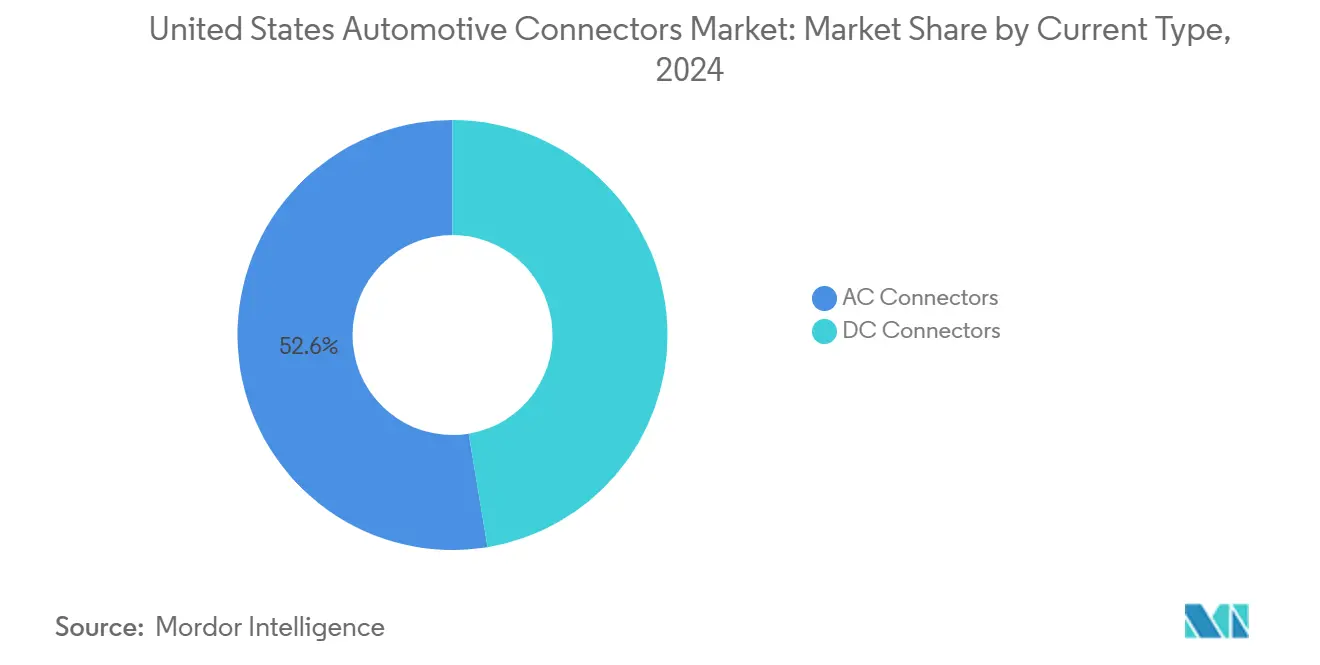

- By current type, AC connectors covered 52.64% of 2024 sales, while combined charging solutions are slated for a 17.21% CAGR.

- By application, battery-management systems overtook other uses with a 19.82% CAGR, although engine and powertrain electronics still captured a 29.09% slice of the United States automotive connectors market size in 2024.

Worldwide, activity is shaped by contributions from multiple countries and regions, with United states representing one among them. The global report on automotive connector market by Mordor Intelligence reflects how these countries and regional layers combine into a single system.

United States Automotive Connectors Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Electrification and EV Adoption | +1.2% | National, concentrated in California, Texas, Michigan | Medium term (2-4 years) |

| Expansion of ADAS and Infotainment Integration | +0.8% | National, early adoption in premium segments | Short term (≤ 2 years) |

| Federal IRA Incentives and Domestic-Content Mandates | +0.6% | National, manufacturing benefits to Southeast, Midwest | Long term (≥ 4 years) |

| 48-V Architectures and Tesla LVCS Standard Emergence | +0.4% | National, Tesla influence in Western states | Medium term (2-4 years) |

| Automotive-Ethernet Migration and X-By-Wire Systems | +0.3% | National, luxury segment leadership | Long term (≥ 4 years) |

| Heavy-Duty E-Pickup/Off-Road Demand for Rugged HV Connectors | +0.2% | Regional, concentrated in Texas, Michigan, Ohio | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Electrification and EV Adoption

Federal and state mandates accelerate electric vehicle penetration beyond market-driven adoption rates, creating step-function demand for high-voltage connectors and battery management interfaces. Tesla's Model Y became the best-selling vehicle in California during 2024, demonstrating mainstream EV acceptance that extends beyond early adopters[1]Gary Gastelu, "The Tesla Model Y Was California’s Best Selling Vehicle In 2024 And It Wasn’t Even Close," American Cars and Racing, americancarsandracing.com.. This transition requires connector manufacturers to pivot from 12V automotive electrical systems to 400V and 800V architectures, necessitating new materials, safety certifications, and thermal management capabilities. Heavy-duty applications particularly drive innovation as electric pickup trucks demand connectors capable of handling 3.75 MW charging loads through Megawatt Charging System protocols developed for commercial vehicle fleets.

Expansion of ADAS and Infotainment Integration

Advanced driver assistance systems create exponential data transmission requirements that strain traditional automotive networking protocols. Modern vehicles integrate over 100 ECUs requiring high-speed connectivity, with autonomous driving functions demanding data rates exceeding 10 Gbps for sensor fusion and real-time processing[2]"Vehicle Architecture: The Innovation Turning Point," Molex, molex.com.. MIPI A-PHY v2.0 development enables automotive Ethernet migration from traditional CAN bus architectures, requiring connectors capable of supporting asymmetric data rates and electromagnetic interference shielding. Camera systems alone demand 6 GHz frequency support for high-resolution ADAS applications, pushing connector manufacturers toward specialized RF interfaces and floating backshell designs that accommodate assembly tolerances.

Federal IRA Incentives and Domestic-Content Mandates

The Inflation Reduction Act's Section 45X tax credits fundamentally alter automotive supply chain economics by providing 10% production tax credits for domestic connector manufacturing. These incentives coincide with domestic content requirements that mandate 50% US-sourced materials for EV tax credit eligibility, forcing OEMs to evaluate supplier relationships and potentially reshoring connector production. Molex's USD 130 million Guadalajara facility expansion demonstrates nearshoring strategies that position suppliers closer to US automotive production while maintaining cost competitiveness[3]"Molex Expands North American Manufacturing Capabilities with Opening of Second State-of-the-Art Factory in Guadalajara," Molex, molex.com.. Scout Motors' USD 300 million supplier park investment in South Carolina exemplifies how federal incentives catalyze regional automotive ecosystem development that benefits connector suppliers through proximity advantages.

48-V Architectures and Tesla LVCS Standard Emergence

Tesla's Low Voltage Connector Standard adoption by Ford and General Motors signals industry convergence around simplified electrical architectures that reduce connector complexity while enabling higher power applications. 48V systems quadruple voltage capacity compared to traditional 12V networks, supporting electric turbocharging, regenerative braking, and advanced climate control without requiring high-voltage safety protocols. This voltage level enables smaller wire gauges and reduced harness weight while maintaining power delivery capability, creating demand for mid-voltage connectors like Molex's MX150 system, rated for 60V applications. Standardization around fewer connector types potentially consolidates supplier relationships while reducing inventory complexity for OEMs managing multiple vehicle platforms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Connector Price-Pressure and Commoditization | -0.7% | National, Acute in High-Volume Segments | Short Term (≤ 2 Years) |

| Raw-Material Cost Volatility and Supply Disruptions | -0.5% | National, Copper-Intensive Applications | Medium Term (2-4 Years) |

| Fragmented Low-Voltage Standard Adoption | -0.3% | National, Legacy Platform Constraints | Long Term (≥ 4 Years) |

| Functional-Safety and Cyber-Security Compliance Burden | -0.2% | National, Premium Segment Impact | Medium Term (2-4 Years) |

| Source: Mordor Intelligence | |||

Connector Price-Pressure and Commoditization

Automotive OEMs intensify cost reduction initiatives as electric vehicle production scales require margin preservation amid battery cost pressures. Traditional wire-to-wire connectors face commoditization as suppliers compete primarily on price rather than technological differentiation, compressing margins across high-volume applications. Molex addresses this challenge through ZeroWear technology that reduces friction and maintains electrical resistance over repeated insertion cycles, enabling higher circuit counts without proportional cost increases. Copper price volatility exacerbates cost pressures as COMEX futures reached USD 5.20 per pound in May 2024, forcing suppliers to implement dynamic pricing mechanisms and inventory hedging strategies.

Raw-Material Cost Volatility and Supply Disruptions

Copper supply constraints create structural headwinds for connector manufacturers as global demand growth outpaces mine production capacity. BHP forecasts 70% copper demand growth between 2021 and 2050, driven by electrification trends, with electric vehicles requiring 3x more copper than internal combustion engine vehicles. Chinese copper cathode production increased 5.42% in 2024, yet concentrate supply tightness persists due to limited new mine development and environmental constraints on existing operations. Connector manufacturers respond through secondary copper utilization and alternative alloy development, though performance compromises may limit adoption in high-reliability automotive applications requiring consistent electrical properties.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: BEV Acceleration Reshapes Connector Demand

In 2024, internal combustion engines maintain a 38.21% market share, creating a temporal mismatch between current revenue and future opportunity, while battery electric vehicles command 18.54% CAGR growth through 2030. Tesla's Supercharger network expansion to non-Tesla vehicles accelerates BEV adoption by addressing range anxiety concerns. At the same time, Ford's Lightning Pro commercial variant demonstrates heavy-duty EV viability that extends beyond consumer applications. Plug-in hybrid electric vehicles serve as transitional technology with moderate growth expectations, while fuel cell electric vehicles remain niche applications limited by hydrogen infrastructure constraints.

Hybrid electric vehicles maintain steady demand as cost-conscious consumers seek electrification benefits without charging infrastructure dependence. The propulsion type segmentation reveals fundamental shifts in automotive electrical architecture as BEV platforms eliminate traditional engine management systems while introducing battery thermal management and high-voltage safety disconnects. ISO 26262 functional safety standards increasingly influence connector design specifications as automotive systems integration levels rise, requiring suppliers to demonstrate compliance capabilities across multiple vehicle architectures and propulsion technologies.

By Connection Type: Zonal Architectures Drive Board-to-Board Growth

Wire-to-wire connections retain 46.37% market share in 2024 through continued dominance in traditional automotive applications, yet zonal architecture adoption reduces overall wire harness complexity and favors high-density interconnects. Molex's MX-DaSH connector family exemplifies this trend by combining high-speed data transmission with power delivery in modular configurations that reduce connector count and installation complexity. Board-to-board connectors accelerate at 11.26% CAGR as automotive electrical architectures transition from distributed ECU topologies to centralized computing platforms that consolidate vehicle functions.

Wire-to-board applications maintain stable demand across engine management and body control modules, while other connection types, including flexible printed circuits, gain traction in space-constrained applications. The evolution of connection type reflects broader automotive industry trends toward software-defined vehicles requiring fewer physical interfaces but higher data throughput capabilities. USCAR standards, including USCAR-2 and USCAR-17, provide reliability benchmarks that guide connector selection across different connection types, ensuring consistent performance across diverse automotive operating environments.

By Voltage: High-Voltage Surge Reflects Electrification Impact

Low-voltage applications maintain a 57.42% market share in 2024 through continued dominance in body electronics, lighting, and infotainment systems that operate within 12V constraints. Medium voltage segments benefit from 48V system adoption that enables higher power applications without high-voltage safety protocols, creating opportunities for suppliers like Molex with MX150 connector systems rated for 60V operation. High-voltage connectors surge at 19.27% CAGR as electric vehicle architectures demand 400V and 800V power distribution capabilities that exceed traditional automotive electrical systems.

Megawatt Charging System development for heavy-duty commercial vehicles pushes voltage requirements beyond passenger car applications, demanding connectors capable of 1000V operation with liquid cooling integration. The voltage segmentation reflects fundamental changes in automotive electrical architecture as vehicles transition from mechanical to electrical control systems. Regulatory compliance factors, including IEC 62196 charging standards and SAE J1772 compatibility requirements, influence connector design specifications across different voltage categories, creating barriers to entry for suppliers lacking certification capabilities.

By Component: Housing Innovation Drives Fastest Growth

Terminal components maintain a 43.18% market share in 2024 through fundamental importance in electrical connectivity, yet housing design increasingly determines connector performance in harsh automotive environments. Eaton's eyelet terminal production capabilities demonstrate scale requirements for high-volume automotive applications, with billions of parts produced annually across multiple stamping facilities. Housing components accelerate at 12.83% CAGR as environmental sealing requirements and miniaturization demands drive innovation beyond traditional terminal-focused development.

Lock mechanisms and other components serve specialized functions in connector assemblies, with position assurance features becoming standard requirements for automotive applications. The component segmentation reveals supply chain complexity as connector manufacturers integrate multiple specialized components from different suppliers to create complete assemblies. Two-shot molding and over-molded designs enable housing components to withstand temperatures up to 200°C while providing water shedding and anti-rotation features essential for automotive reliability standards.

By Current Type: Combined Connectors Lead EV Charging Evolution

AC connectors hold 52.64% market share in 2024 through dominance in residential and workplace charging applications that utilize existing electrical infrastructure. Tesla's NACS (North American Charging Standard) adoption by Ford and General Motors creates potential standardization around fewer connector types, though CCS infrastructure investments maintain competitive positioning for combined connector systems. Combined charging connectors accelerate at a 17.21% CAGR as CCS (Combined Charging System) adoption standardizes DC fast charging across multiple vehicle manufacturers.

DC connectors serve specialized applications, including vehicle-to-grid integration and commercial fleet charging, that require bidirectional power flow capabilities. The current type segmentation reflects charging infrastructure development patterns as public DC fast charging networks expand while residential AC charging remains the primary use case for most EV owners. SAE J3400 NACS standardization and J3271 MCS development demonstrate industry efforts to consolidate charging connector types while maintaining backward compatibility with existing vehicle fleets.

By Application: Battery Management Systems Surge Past Traditional Segments

Engine management and powertrain applications maintain 29.09% market share in 2024 through continued ICE vehicle production, yet this dominance erodes as electrification eliminates traditional powertrain control requirements. ADAS and safety systems drive connector demand through sensor proliferation and real-time data processing requirements that exceed traditional automotive networking capabilities. Battery management systems command a 19.82% CAGR growth as electric vehicle adoption creates entirely new connector application categories absent from internal combustion engine vehicles.

Infotainment systems evolve toward high-bandwidth applications supporting 5G connectivity and over-the-air software updates that require automotive Ethernet infrastructure. Body control and interiors benefit from increased electronic content as vehicles integrate more comfort and convenience features, while vehicle lighting transitions to LED and adaptive systems requiring specialized connectors. The application segmentation reveals automotive industry transformation as mechanical systems yield to electronic alternatives that demand higher performance connectivity solutions across multiple vehicle subsystems.

Geography Analysis

The South now absorbs the largest share of the United States automotive connectors market as Hyundai, Scout Motors, and several battery joint ventures build greenfield plants, attracted by incentive packages. Supplier parks shorten just-in-sequence delivery miles and raise demand for mid-voltage and HV couplers installed on battery lines.

Midwest states such as Michigan and Ohio pivot legacy engine plants toward electric drivetrain parts, keeping connector demand intact while upskilling workforces. Proximity to research centers and test tracks bolsters the adoption of zonal networks and Ethernet harnesses.

The West features California’s ZEV targets and Tesla’s factory hub, pushing HV charging sockets and sensor harnesses orders. The Northeast maintains a mature aftermarket and proximity to cross-border supply from Canada, sustaining low-voltage replacement connectors for fleet maintenance. These patterns illustrate how regional investment flows anchor the United States automotive connectors market.

Mordor Intelligence provides coverage of the automotive connector market across other key regional markets. Detailed country-level analysis extends to India incorporating local coverage and market participation, as required.

Competitive Landscape

The United States automotive connectors market hosts a moderate concentration as TE Connectivity, Amphenol, Aptiv, Molex, Yazaki, and Sumitomo command sizeable footprints. TE Connectivity raised EUR 750 million in senior notes in January 2025 to fund acquisitions that expand automotive sockets and sensors. Amphenol completed the CIT acquisition in 2024 to broaden its end-market reach.

Suppliers pursue vertical integration by in-house stamping and over-molding to shield against logistical shocks. Portfolio gaps are filled through targeted deals that add 48 V power boards, fiber optic jumpers, or sealing IP. Technology differentiation centers on zero-wear plating, multi-gigabit data paths, and liquid-cooled HV docks.

New entrants from consumer electronics offer cost-optimized micro-connectors, pressuring incumbents on pricing. In response, leaders bundle cable assemblies and engineering services to lock customer loyalty. Government incentives favor firms with domestic capacity, nudging Asian manufacturers to build or expand U.S. sites. This blend of consolidation and greenfield investment sustains competitive dynamism in the United States automotive connectors market.

Recent Industry Developments

- October 2024: Molex published comprehensive analysis of 48V automotive system evolution, emphasizing MX150 mid-voltage connector system capabilities for enabling lighter-weight wiring while maintaining performance standards required for electrification applications.

- May 2024: Amphenol completed the acquisition of CIT, expanding capabilities across multiple end markets while reporting record quarterly results driven by automotive and industrial growth.

United States Automotive Connectors Market Report Scope

| Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) |

| Plug-in Hybrid Electric Vehicle (PHEV) |

| Fuel Cell Electric Vehicle (FCEV) |

| Hybrid Electric Vehicle (HEV) |

| Wire-to-Wire |

| Wire-to-Board |

| Board-to-Board |

| Others |

| Low Voltage (Less than 60 V) |

| Medium Voltage (60 to 400 V) |

| High Voltage (More than 400 V) |

| Terminal |

| Housing |

| Lock |

| Others |

| AC Connectors |

| DC Connectors |

| Combined Connectors (Combo/CCS) |

| Battery Management System |

| Infotainment System |

| ADAS and Safety System |

| Engine Management and Powertrain |

| Body Control and Interiors |

| Vehicle Lighting |

| Others |

| Northeast |

| Midwest |

| South |

| West |

| By Propulsion Type | Internal Combustion Engine (ICE) |

| Battery Electric Vehicle (BEV) | |

| Plug-in Hybrid Electric Vehicle (PHEV) | |

| Fuel Cell Electric Vehicle (FCEV) | |

| Hybrid Electric Vehicle (HEV) | |

| By Connection Type | Wire-to-Wire |

| Wire-to-Board | |

| Board-to-Board | |

| Others | |

| By Voltage | Low Voltage (Less than 60 V) |

| Medium Voltage (60 to 400 V) | |

| High Voltage (More than 400 V) | |

| By Component | Terminal |

| Housing | |

| Lock | |

| Others | |

| By Current Type | AC Connectors |

| DC Connectors | |

| Combined Connectors (Combo/CCS) | |

| By Application | Battery Management System |

| Infotainment System | |

| ADAS and Safety System | |

| Engine Management and Powertrain | |

| Body Control and Interiors | |

| Vehicle Lighting | |

| Others | |

| By Geography | Northeast |

| Midwest | |

| South | |

| West |

Key Questions Answered in the Report

What CAGR is forecast for connectors used in U.S. battery electric vehicles?

Connectors dedicated to BEV platforms are projected to climb at an 18.54% CAGR through 2030.

Which connector voltage class is growing the fastest in American auto production?

High-voltage components above 400 V are advancing at a 19.27% CAGR, outpacing low- and medium-voltage ranges.

Which component sub-segment is expanding more quickly than terminals?

Housing parts are rising at a 12.83% CAGR due to sealing and miniaturization pressure.

What recent acquisition strategy did Amphenol pursue?

Amphenol completed a USD 2.025 billion purchase of CIT in January 2025 to broaden its automotive and industrial connector offerings.

Page last updated on: