Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 175.14 Billion |

| Market Size (2031) | USD 214.96 Billion |

| Growth Rate (2026 - 2031) | 4.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Interior Market Analysis by Mordor Intelligence

Automotive Interior Market size in 2026 is estimated at USD 175.14 billion, growing from 2025 value of USD 168.11 billion with 2031 projections showing USD 214.96 billion, growing at 4.18% CAGR over 2026-2031. This measured expansion conceals a more profound transformation as software-defined cockpits, biometric monitoring, and sustainable materials move from niche options to mainstream specifications. Automotive OEMs re-engineer cabin layouts around high-density displays and centralized compute units, while suppliers explore subscription revenue tied to over-the-air feature upgrades. Electric vehicle platforms add further content per car because silent cabins heighten the importance of premium surfaces, ambient lighting, and wellness features. The Asia-Pacific region already sets the pace for these upgrades, and its volume advantage encourages fast local iteration. Simultaneously, aftermarket demand stays resilient because fleet operators and retail owners keep refreshing worn trim with longer-life, digitally upgradable modules, dampening fears that shared mobility would erode replacement cycles.

Key Report Takeaways

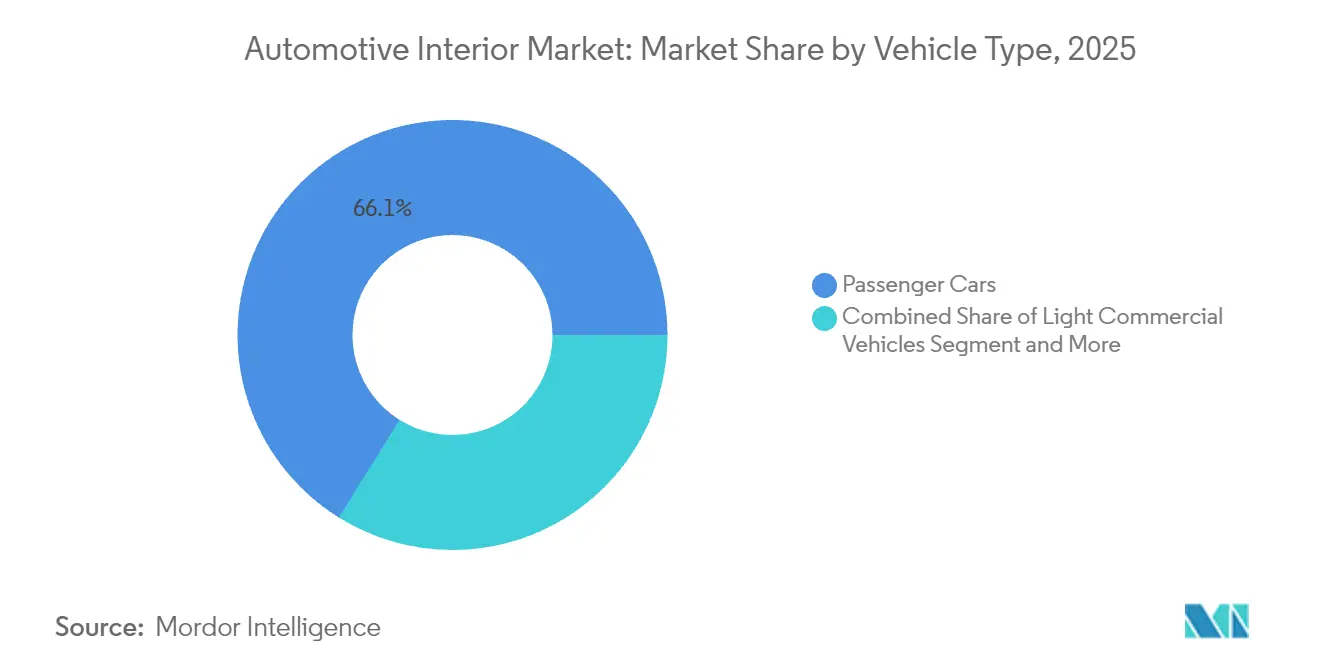

- By vehicle type, passenger cars accounted for 66.13% of the automotive interior market size in 2025, while electric passenger cars are projected to rise at a 4.21% CAGR to 2031.

- By propulsion, internal combustion engine vehicles held 72.47% automotive interior market share in 2025, whereas electric vehicles are forecast to post the fastest growth at a 4.27% CAGR through 2031.

- By component, seating systems captured 34.05% revenue share in 2025; driver and occupant monitoring systems hold the highest projected CAGR at 4.23% during the forecast period.

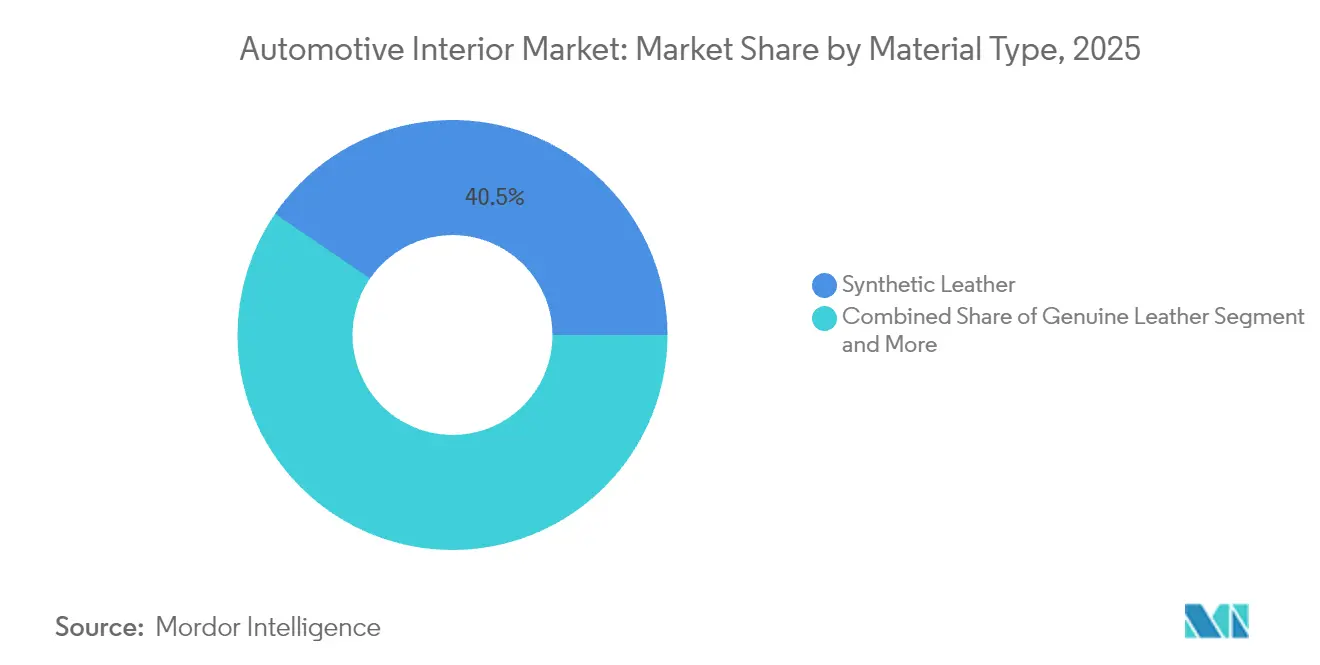

- By material, synthetic leather held 40.46% share of the automotive interior market size in 2025, whereas natural and recycled materials will advance at a 4.24% CAGR through 2031.

- By sales channel, the aftermarket segment commanded 72.77% of the automotive interior market size in 2025 and maintains a 4.29% CAGR outlook to 2031.

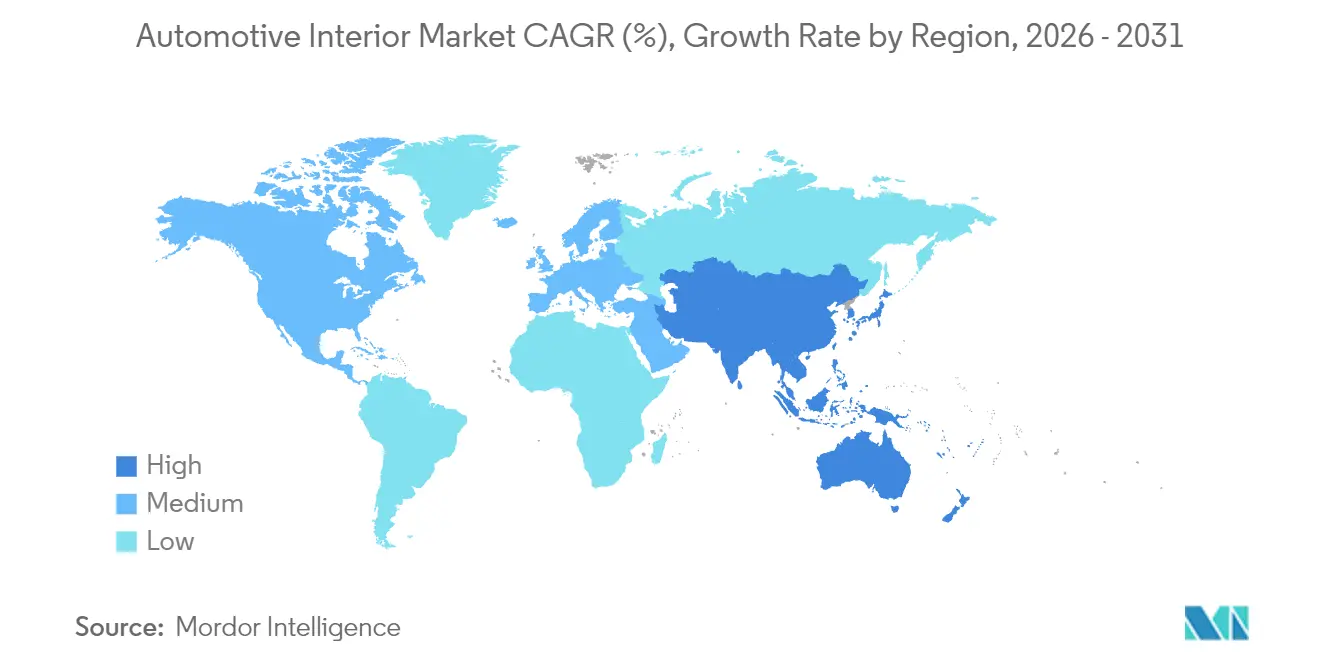

- By geography, Asia-Pacific led with 37.43% of automotive interior market share in 2025; the region is on track to expand at a 4.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Interior Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift Toward Software-Defined Vehicles | +0.8% | Global, led by North America and China | Medium term (2-4 years) |

| Rising Demand For Premium and Electric SUVs | +0.6% | Asia-Pacific core, spill-over to global | Short term (≤ 2 years) |

| Over-The-Air Upgradable Cockpit Architectures | +0.5% | North America and EU early adoption | Medium term (2-4 years) |

| Lightweight Sustainable Materials Mandated | +0.4% | Global, EU regulatory leadership | Long term (≥ 4 years) |

| Adoption Of In-Cabin Health, Safety & Biometrics Regulations | +0.3% | EU leadership, global adoption | Medium term (2-4 years) |

| Solid-State Ambient Lighting | +0.2% | Global, premium segments first | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Shift Toward Software-Defined Vehicles & HD Displays

Software-centric design decouples cabin functions from fixed hardware and allows continuous upgrades through secure over-the-air patches. Continental now delivers cockpit domains that host three or more ultra-high-resolution displays driven by processors exceeding 1,000 DMIPS [1]“Integrated High-Performance Cockpit Platforms,” Continental AG, continental-automotive.com. Qualcomm’s Snapdragon Digital Chassis powers numerous vehicle models and underscores how semiconductor players influence cabin electronics [2]“Snapdragon Digital Chassis Adoption Update,” Qualcomm Incorporated, qualcomm.com . Suppliers that blend electronics, software, and user-experience design monetize new features long after production, reshaping cost-plus contracts into recurring revenue frameworks. Predictive maintenance and usage-based insurance ride on the same data backbone, expanding the business case for interior sensor suites. Traditional component-only firms risk erosion unless they partner or acquire digital talent.

Rising Demand for Premium & Electric SUVs in China & ASEAN

Electric premium SUVs sold in China carry a one-fifth higher interior bill-of-materials than their ICE peers, mainly due to ambient lighting, multi-screen infotainment, and advanced monitoring. Companies like NIO and XPeng have normalized biometric sensing even in mid-range trims, prompting global suppliers to localize advanced modules in Changzhou, Wuhan, and Rayong. Thailand’s fast-growing EV export base pulls seat, trim, and cockpit makers into Southeast Asia, lowering lead times for Japanese, Korean, and Western OEMs that assemble there. ASEAN’s middle-income families increasingly weigh the in-cabin experience when buying a first SUV, so local Tier-1s invest in color, material, and finish studios close to Bangkok and Ho Chi Minh City. The high gross margins on premium interiors soften price sensitivity, letting suppliers recoup R&D more quickly. Localization further shields vendors from potential geopolitical tariffs on cross-border components.

Over-The-Air Upgradable Cockpit Architectures

Stellantis equips STLA Brain with centralized compute and secure gateways that allow cabin features to refresh in minutes rather than during annual shop visits. For suppliers, subscription tiers on seat massage patterns, ambient lighting themes, or advanced driver monitoring offer lifetime revenue proportional to miles driven. Warranty costs fall because remote diagnostics resolve software faults without part swaps. Hardware must still meet automotive grade, so suppliers invest in cybersecurity certification to comply with ISO 21434. The upfront spend is high, yet early movers lock OEMs into multi-cycle programs, making switching costly. Over-the-air capability reinforces the value of modular design, letting carmakers delay particular feature launches until after production while capturing data that informs future cabin options.

Lightweight Sustainable Materials Mandated by OEM Carbon Targets

Automakers commit to net-zero scopes and translate lofty pledges into procurement rules that favor recycled or bio-based feedstocks. BMW targets half recycled plastic content in all new interiors by 2030. Seat maker Adient has partnered with multiple biomaterial startups to offer drop-in replacements for petrochemical foams. California’s latest vehicle standards echo Europe’s circular-economy push, giving North American suppliers similar incentive signals. Vendors that scale algae-based polyurethane or recycled PET fabrics capture price premiums and win long-duration contracts. Petrochemical incumbents face compressed margins as they chase compliance via costly offsets. In the long term, material provenance data will flow through vehicle blockchains so that recyclers and regulators can audit end-of-life recovery.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent Chipset Shortages | -0.3% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| Lower Refresh-Cycle In Shared-Mobility Fleets | -0.2% | North America and EU fleet markets | Medium term (2-4 years) |

| High Raw-Material Volatility | -0.2% | Global, EU regulatory complexity | Medium term (2-4 years) |

| IP- & Standards-Fragmentation | -0.1% | Global, acute in Android Automotive | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Persistent Chipset Shortages in the Infotainment Domain

Lead times for automotive-grade processors still range from 26 to 52 weeks, hurting interior build schedules and forcing OEMs to prioritize safety controllers over infotainment head units. Tier-1s that adopt chip-agnostic architectures buffer some risk, yet smaller players lose allocation clout against consumer electronics giants. Margins narrow because suppliers stockpile semiconductors at peak spot prices, tying up working capital. In emerging markets, cost-sensitive OEMs downgrade cabin specs or postpone rollouts of multi-camera monitoring. The shortage accelerates vertical integration as Continental, ZF, and others add internal ASIC design to secure strategic components. Until new fabs in Arizona, Saxony, and Penang ramp, the constraint will continue to clip near-term upside for display-heavy interiors.

High Raw-Material Volatility for PU & Bio-Based Polymers

Polyurethane foam costs climbed one-fourth in 2024, mirroring spikes in crude oil, while bio-based substitutes swung even wider because of crop-yield uncertainty. Seat and trim producers hedge with futures contracts, but tier-2s lack the scale to absorb the hit directly or renegotiate with OEMs. Volatility complicates the pivot to greener inputs, since bio-based pricing depends on corn, soybean, or sugarcane harvests. Suppliers with captive chemical divisions, such as Lear, report steadier gross profit through integrated sourcing. Smaller firms explore long-term indexed deals or shift to multi-material designs that cut PU volume per seat. Lumpy costs also delay the payback on recycling infrastructure because feedstock input prices remain unpredictable.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Vehicle Type: Electric Premiumization Drives Content Growth

Passenger cars sustained 66.13% of overall revenue in 2025, showing the segment's scale advantage in the automotive interior market. Electric passenger cars represent the fastest growing slice at a 4.21% CAGR as higher in-cabin technology density lifts basket value per unit. The automotive interior market size for electric cars benefits from wide, flat floors that free up storage modules, lounge-style seating, and panoramic display surfaces. Light commercial vehicles track parcel delivery expansion, but cabin upgrades stay utilitarian, so growth stems mainly from mandated driver monitoring rather than luxury trim. Medium and heavy trucks remain sensitive to downtime; therefore, suppliers pitch durable fabrics and antimicrobial surfaces to fleet buyers.

The electrification wave lets suppliers insert wellness functions such as active noise cancellation and air ionizers that were previously cost-prohibitive. Tesla sparked minimalist layouts, yet legacy OEMs show there is still an appetite for robust switchgear coupled with multi-screen clusters. New EU rules that require inward-facing cameras on heavy trucks generate incremental demand for occupant monitoring kits. Over time, cabin differentiation shifts from mechanical craftsmanship to software-driven personalization that updates throughout the vehicle's life, extending aftermarket potential even in commercial fleets.

By Propulsion Type: ICE Dominance Masks EV Growth Trajectory

Internal combustion vehicles still accounted for 72.47% revenue in 2025, anchoring volumes across the automotive interior market. Nonetheless, electric models grow 4.27% annually and dictate forward design language. Battery layouts remove transmission tunnels, so floor-mounted sensor pods and illuminated storage compartments gain prominence. The automotive interior market share for EV-specific components expands as low cabin noise raises occupant awareness of rattles and panel gaps, forcing tighter manufacturing tolerances. Hybrids serve as transition products and often bundle larger displays and premium fabrics to justify higher price tags despite modest pure-electric range.

EV architecture increases demand for real-time energy visualizations, prompting suppliers to reconfigure cluster graphics and center-stack UX to display charging data. Silence inside the cabin accentuates audio quality and encourages OEMs to specify higher wattage speakers and vibration-damping mats, further boosting content per car. Thermal management for battery longevity influences HVAC routing, giving suppliers experienced in dual-zone and tri-zone climate control a competitive edge.

By Component Type: Monitoring Systems, Eclipse, Traditional Priorities

Seating remained the single largest component group, representing 34.05% of the automotive interior market size in 2025 because every vehicle needs seats and most trims offer multiple upgrade packages. Yet driver and occupant monitoring units clocked the quickest 4.23% CAGR, powered by EU General Safety Regulation requirements and insurer discounts for cars with fatigue detection. Infotainment ranks second in value and benefits from centralized computing that supports six-year software roadmaps. Ambient lighting moves beyond aesthetics and now signals state-of-charge, navigation cues, and driver alerts.

Door and side-panel suppliers introduce lightweight foamed composites that integrate touch sensors. HVAC modules evolve toward individualized micro-climate bubbles with active pollen and particulate filtration. Upholstery makers embrace closed-loop recycling, recovering seat fabric when vehicles retire to salvage yards. The “other” bucket, mostly biometric and wellness modules, records double-digit share gains, from a low base, hinting at future mainstream adoption.

By Material Type: Sustainability Mandates Reshape Preferences

Synthetic leather led at 40.46% revenue in 2025 due to cost-efficiency and a broad color palette. Genuine leather remains aspirational but feels pressure from vegan and carbon critiques. The automotive interior market size tied to natural and recycled inputs grows at a 4.24% CAGR because regulatory credits tilt bill-of-materials selection toward lower life-cycle emissions. Fabrics from recycled PET now meet durability specs once exclusive to PVC, narrowing performance gaps. Plastics houses retrofit extrusion lines to accommodate bio-PA and recycled PP, absorbing capex to stay on OEM sourcing lists.

Material sourcing evolves into a brand story that OEMs market directly to consumers, so traceability platforms map supply chains down to the plantation or refinery. Suppliers that manage full cradle-to-grave loops secure preferential nomination as carmakers expect end-of-life take-back. Cost premiums are gradually mitigated by scale and green-bond financing that funds capacity expansion of novel biomaterials.

By Sales Channel: Aftermarket Resilience Defies Fleet Predictions

Despite ride-hailing and car-sharing narratives, the aftermarket held 72.77% revenue in 2025 and maintains a 4.29% CAGR outlook. Fleet managers stretch asset lives but demand rugged, serviceable trim; thus, suppliers focus on modular inserts that minimize downtime. OEM integrated channels yield higher per-unit margin but move more slowly in volume, keeping the aftermarket crucial for growth in the automotive interior market. E-commerce portals give small brands global reach, boosting competition.

Digitally upgradable hardware, such as seat controllers or ambient lighting drivers, enables owners to unlock features post-purchase, intertwining aftermarket and software revenue. Direct-to-consumer kits bundle plug-and-play wiring harnesses with cloud activation codes, lowering installation barriers. The channel mix underscores that physical wear, spills, and personal preference drive replacement even as ownership models evolve.

Geography Analysis

Asia-Pacific delivered 37.43% of global revenue in 2025 and will post the fastest 4.31% CAGR through 2031. China’s indigenous brands fit multi-screen cockpits and wellness seats even on compact SUVs, lifting average interior spend. Mainland volume plus regional free-trade zones entice Yanfeng, Magna, and FORVIA to localize R&D and build material labs close to OEM design centers. Thailand scales EV assembly for export to Australia and the Middle East, catalyzing new Tier-2 clusters that supply seat frames, trims, and screens. Japan and South Korea use advanced sensor algorithms for occupant monitoring, often licensing software globally. Rising disposable incomes across Indonesia and Vietnam elevate demand for comfort features, sustaining growth even if macroeconomics fluctuate.

North America stands as the second-largest revenue pool. The United States pushes driver-monitoring requirements through the expanding FMVSS docket, raising baseline sensor content. Pickup and SUV popularity inflates cabin surface area, which favors high-margin upholstery and infotainment upgrades. Canada’s harsh winters boost heated steering wheel usage and seat usage, further enlarging vehicle content. Mexico’s competitive labor costs and USMCA rules-of-origin keep interior manufacturing vibrant for regional and export volumes.

Europe maintains moderate growth backed by stringent green and safety mandates. The EU General Safety Regulation obliges all new cars to include passive driver monitoring from 2026, guaranteeing demand for inward-facing cameras. Germany’s premium marques lead experimentation with high-resolution OLED clusters and recycled composites, while Eastern Europe offers cost-effective assembly for volume models. Regulatory focus on circularity pushes suppliers to adopt closed-loop material flows. Supply-chain rerouting post-Brexit opens share opportunities for continental producers who can supply UK plants without tariff risk.

Competitive Landscape

Global tier-1 suppliers retain bargaining power due to design integration, logistics scale, and decades-long OEM partnerships. Adient, FORVIA, Lear, and Magna control about two-fifths of the spend, reflecting a moderately concentrated automotive interior market. Yanfeng and Hyundai Mobis leverage regional cost advantages and fast development cycles to win new awards, especially from Chinese and Korean OEMs. Software-native entrants collaborate with incumbents, licensing driver monitoring algorithms or ambient lighting controllers overlaying existing hardware.

Strategic moves skew toward vertical integration and digital capability acquisition. Lear purchased embedded software boutiques to speed ComfortMax seat intelligence features with General Motors. FORVIA issued notes to fund sustainable-material R&D and cockpit platforms [3]“Completion of Senior Notes Offering,” FORVIA SE, forvia.com .

In the current year, patent filings in interior technology surged, underscoring heightened competition, particularly in analytics and eco-materials. Startups face challenges due to stringent compliance requirements with ISO 26262 and ISO 21434, leading many to sidestep direct confrontations with established players. As a result, market differentiation is increasingly centered on software-driven experiences and validated sustainability, moving away from a sole emphasis on mechanical craftsmanship.

Automotive Interior Industry Leaders

Faurecia SE

Adient plc

Lear Corporation

Yanfeng Automotive Interiors

Magna International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: FORVIA completed a USD 500 million senior notes offering to fund strategic acquisitions and R&D in sustainable materials and software-defined cockpits, expanding its bio-based component portfolio.

- February 2025: Lear Corporation announced ComfortMax integration on General Motors’ next electric platform, bundling biometric analytics with personalized climate for every seat.

- November 2024: Adient plc entered a joint development agreement with Paslin Company to automate seating assembly lines, targeting a 30% cost reduction and higher customization throughput.

Global Automotive Interior Market Report Scope

Automotive interiors of the vehicles consist of infotainment systems, instrument panels, body panels, etc. The automotive interior plays a vital role in a vehicle's performance, aesthetic appeal, and salability.

The automotive interiors market scope of the report covers segmentation based on vehicle type, component type, and geography.

The market is segmented by Vehicle Type: Passenger Cars and Commercial Vehicles.

By Component type, the market is segmented into Infotainment Systems, Instrument Panels, Interior Lighting, Body Panels, And Other Component Types.

By geography, the market is segmented into North America, Europe, Asia-Pacific, and the rest of the world.

For each segment, the market sizing and forecast have been done based on value (USD billion).

By Vehicle Type

| Passenger Cars |

| Light Commercial Vehicles |

| Medium and Heavy Commercial Vehicles |

By Propulsion Type

| Internal-Combustion Engine (ICE) |

| Electric Vehicle (EV) |

By Component Type

| Instrument Panels & Cockpit Modules |

| Infotainment & Connected Displays |

| Seating Systems |

| Interior Lighting (Ambient, Functional) |

| Door & Body Trim Panels |

| HVAC & Thermal Comfort |

| Upholstery & Surface Materials |

| Driver / Occupant Monitoring Systems |

| Other Components |

By Material Type

| Synthetic Leather (PU, PVC) |

| Genuine Leather |

| Fabrics & Textiles |

| Plastics & Composites |

| Natural & Recycled Materials |

By Sales Channel

| OEM |

| Aftermarket |

By Geography

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle-East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle-East and Africa |

| By Vehicle Type | Passenger Cars | |

| Light Commercial Vehicles | ||

| Medium and Heavy Commercial Vehicles | ||

| By Propulsion Type | Internal-Combustion Engine (ICE) | |

| Electric Vehicle (EV) | ||

| By Component Type | Instrument Panels & Cockpit Modules | |

| Infotainment & Connected Displays | ||

| Seating Systems | ||

| Interior Lighting (Ambient, Functional) | ||

| Door & Body Trim Panels | ||

| HVAC & Thermal Comfort | ||

| Upholstery & Surface Materials | ||

| Driver / Occupant Monitoring Systems | ||

| Other Components | ||

| By Material Type | Synthetic Leather (PU, PVC) | |

| Genuine Leather | ||

| Fabrics & Textiles | ||

| Plastics & Composites | ||

| Natural & Recycled Materials | ||

| By Sales Channel | OEM | |

| Aftermarket | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle-East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

How big is the automotive interior market in 2026?

The automotive interior market size equals USD 175.14 billion in 2026 and is projected to reach USD 214.96 billion by 2031 at a 4.18% CAGR.

Which component category currently leads in spending?

Seating systems lead with 34.05% revenue share in 2025, reflecting their universal fitment and upgrade potential.

What region shows the fastest growth through 2031?

Asia-Pacific exhibits the quickest 4.31% CAGR thanks to China’s premium SUV boom and Southeast Asian EV exports.

Why are driver monitoring systems gaining traction?

EU and U.S. regulations now mandate fatigue and distraction detection, propelling the segment at a 4.23% CAGR.

How does sustainability influence material choice?

OEM carbon neutrality goals push recycled and bio-based inputs, enabling natural and recycled materials to grow at a 4.24% CAGR through 2031.

Page last updated on: