Automotive Integrated Circuits Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

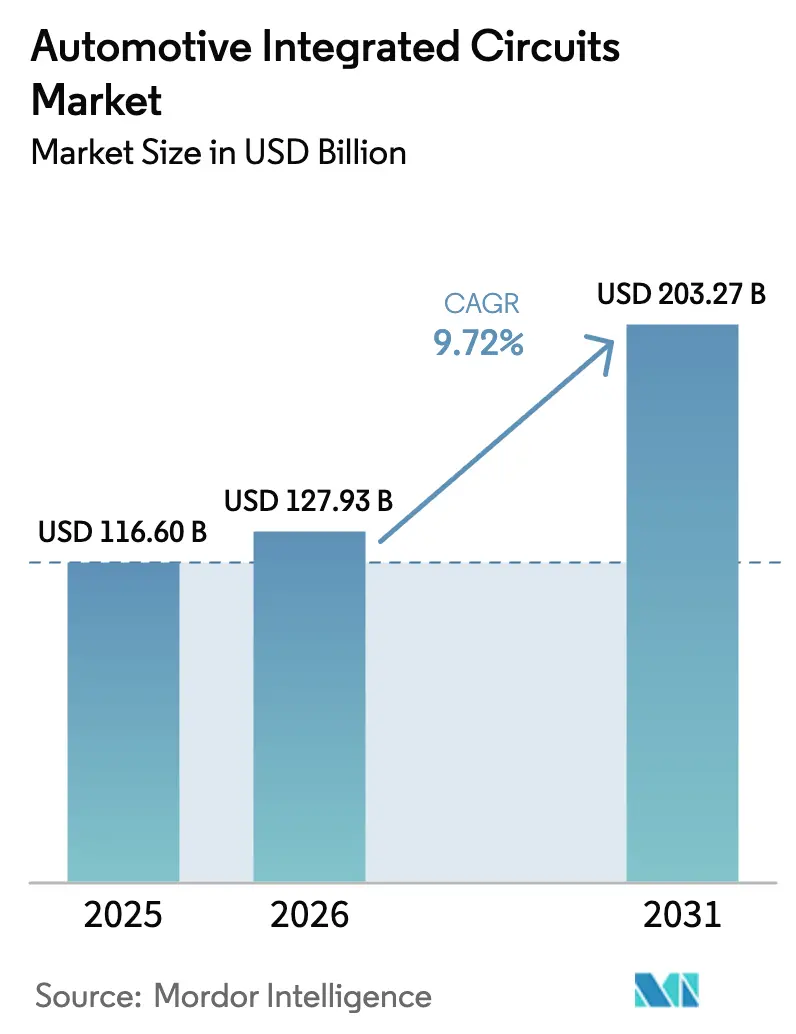

| Market Size (2026) | USD 127.93 Billion |

| Market Size (2031) | USD 203.27 Billion |

| Growth Rate (2026 - 2031) | 9.72% CAGR |

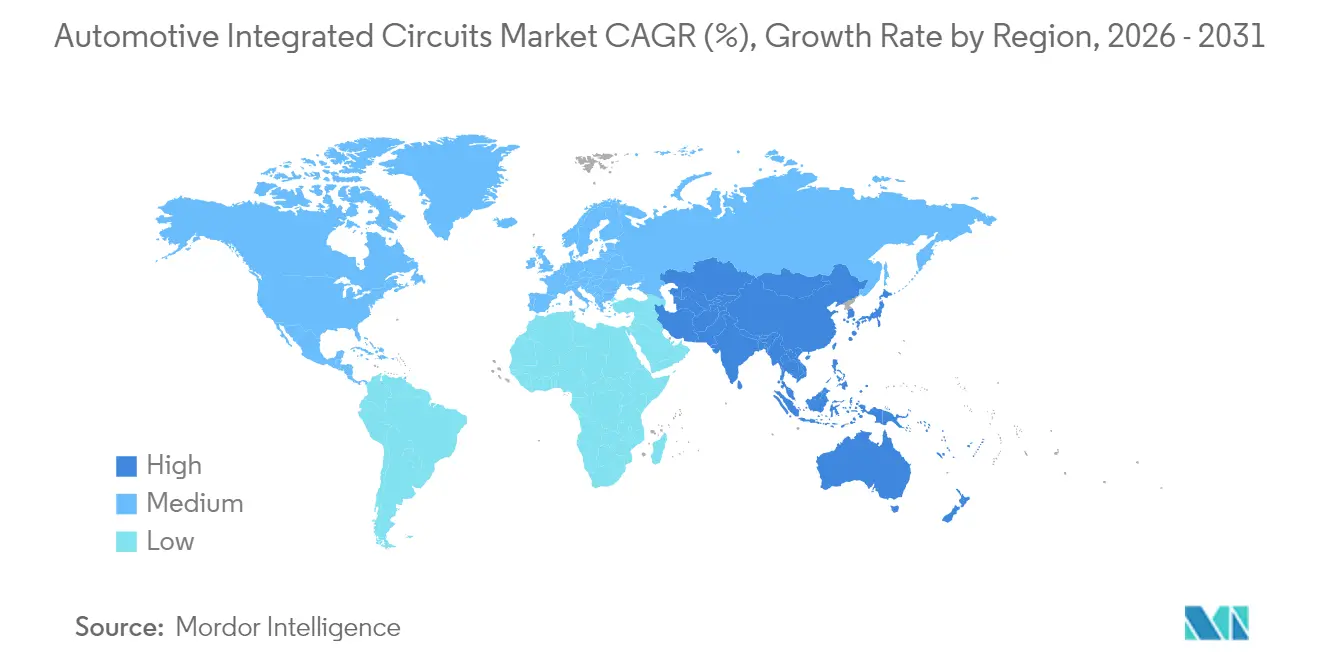

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Integrated Circuits Market Analysis by Mordor Intelligence

The automotive integrated circuits market size was valued at USD 116.60 billion in 2025 and estimated to grow from USD 127.93 billion in 2026 to reach USD 203.27 billion by 2031, at a CAGR of 9.72% during the forecast period (2026-2031). This robust outlook mirrors the industry’s pivot toward software-defined vehicles that replace scores of distributed electronic control units with centralized, high-performance domain and zonal controllers. Regulators have pushed mandatory ADAS features, premium brands have embraced 800-volt electric platforms, and fleet operators are investing in autonomous freight solutions. These parallel forces expand semiconductor content per vehicle, accelerate migration to advanced wafer nodes, and reinforce demand for silicon carbide power devices. Capacity additions under the CHIPS and Science Act and the EU Chips Act will alleviate some supply constraints, yet near-term lithography bottlenecks below 16 nm continue to favor incumbents with qualified automotive lines.

Key Report Takeaways

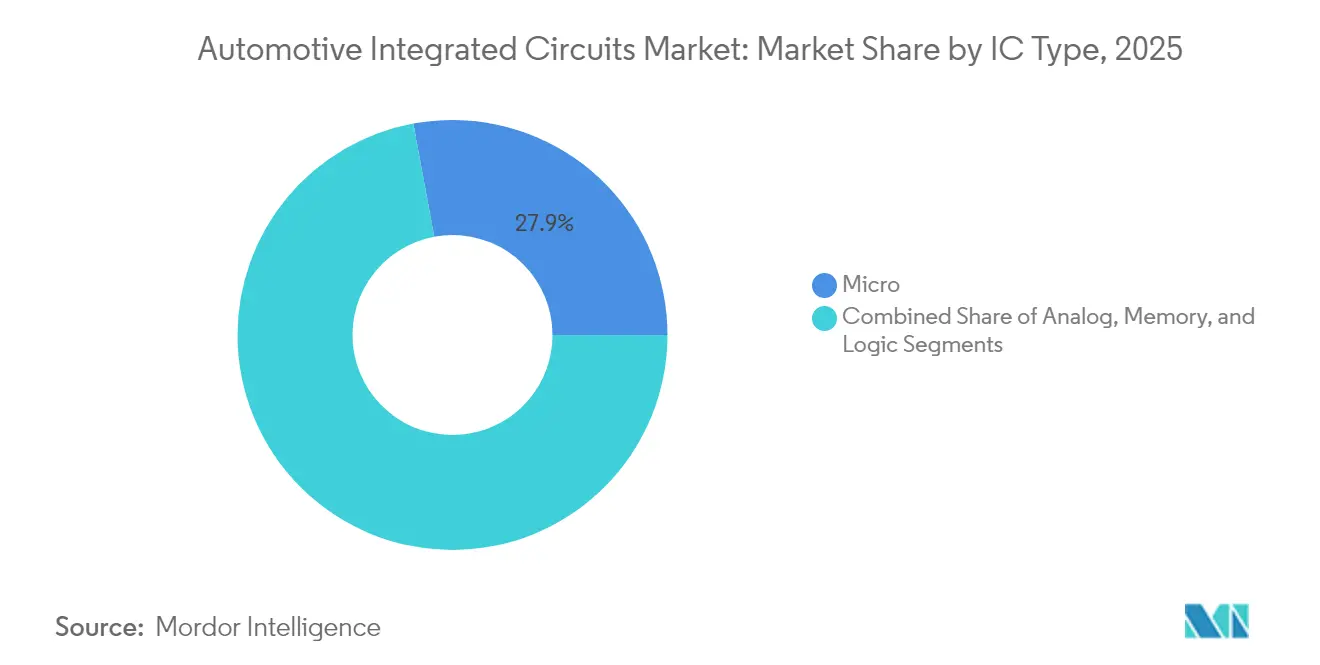

- By IC type, microcontrollers led with 27.92% of automotive integrated circuits market share in 2025 while also posting the segment-best 14.38% CAGR through 2031.

- By application, ADAS and safety captured 24.05% revenue share in 2025; powertrain and battery management is projected to expand at a 13.58% CAGR to 2031.

- By vehicle type, passenger cars held 70.15% of the automotive integrated circuits market size in 2025, whereas heavy commercial vehicles are advancing at a 11.64% CAGR through 2031.

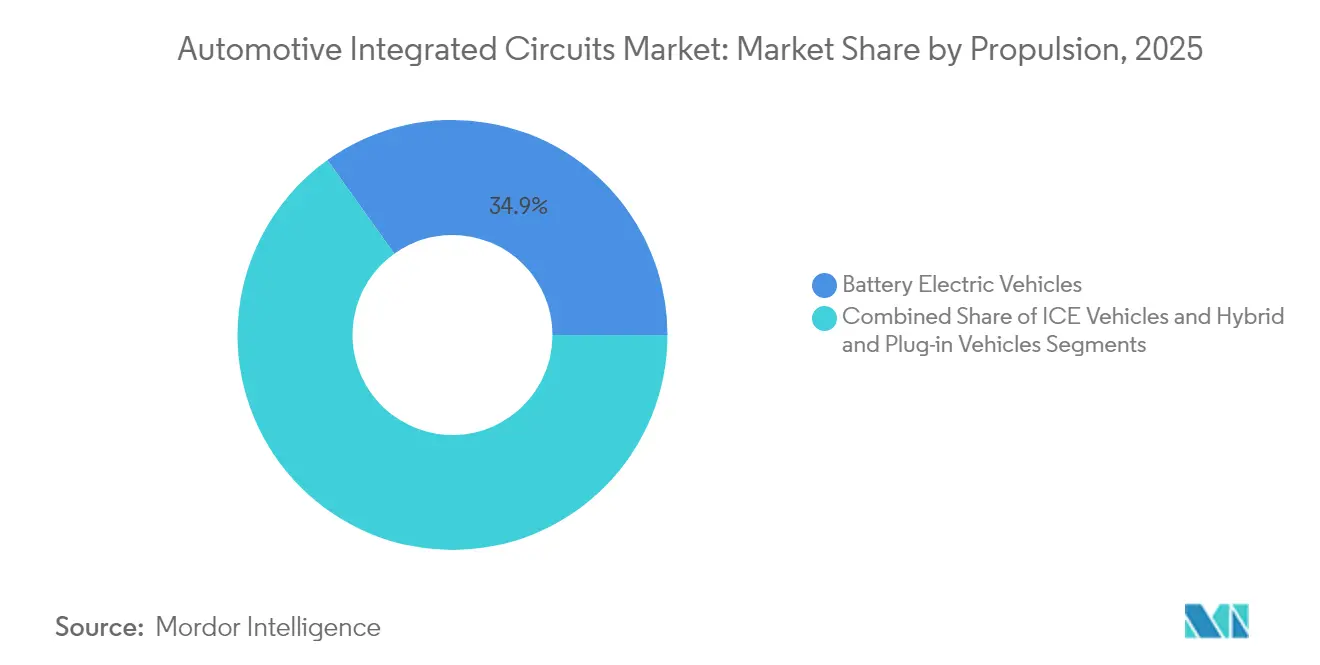

- By propulsion, ICE and hybrid models accounted for 65.12% share of the automotive integrated circuits market size in 2025; battery electric vehicles are growing at a 15.46% CAGR to 2031.

- By wafer node, ≥40 nm processes commanded 41.92% revenue share in 2025; sub-10 nm nodes record the fastest 17.45% CAGR on rising AI workloads.

- By geography, Asia-Pacific contributed 48.12% of global revenue in 2025 and remains the fastest-expanding region at 12.56% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Integrated Circuits Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in ADAS-centric Sensor-Fusion SoCs Adoption in EU | +2.1% | Europe, spill-over to North America | Medium term (2-4 years) |

| Demand for 800-V EV Power ICs in China | +1.8% | APAC core, expanding to global markets | Short term (≤ 2 years) |

| Software-Defined-Vehicle Transition Driving 32-bit and RISC-V MCUs in NA | +1.5% | North America, expanding to Europe | Long term (≥ 4 years) |

| UNECE WP.29 Compliance Catalyzing Telematics Gateway ICs in Japan and Korea | +0.9% | Japan and Korea, expanding to global | Medium term (2-4 years) |

| Zonal E/E Architecture Boosting Domain Controller SoCs in Germany and USA | +1.3% | Germany and USA, global adoption | Long term (≥ 4 years) |

| US-EU CHIPS Act Localization Incentives for Automotive-grade Nodes | +0.7% | North America and Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in ADAS-centric Sensor-Fusion SoCs Adoption in EU

Mandatory automatic emergency braking on all new European models starting 2024 spurred a rapid roll-out of radar-camera-lidar fusion processors. NXP’s SAF86xx family incorporates Arm Cortex-R52 cores with dedicated accelerators, enabling real-time object detection at low latency. Sony followed with the 8.3-megapixel ISX038 image sensor featuring high-dynamic-range pixel technology for glare mitigation.[1]Kenji Tanaka, “ISX038 Automotive CIS,” Sony Semiconductor Solutions, sony-semicon.co.jp Tier-1s adopted Cadence Tensilica vision DSPs to cut development cycles for Euro NCAP-compliant perception stacks. These moves lifted semiconductor value per EU vehicle and created second-order demand for automotive-qualified LPDDR4 memories and high-bandwidth Ethernet PHYs.

Demand for 800-V EV Power ICs in China

Chinese brands raced to 800-V architectures that cut DC-fast-charging times below 30 minutes. BYD’s Seal sedan showcased commercial viability, pairing silicon-carbide inverters with 98.5% efficiency CoolSiC MOSFETs from Infineon. Government subsidies running through 2025 explicitly rewarded fast-charge capability, guiding procurement toward wide-bandgap power devices. Joyson Safety Systems landed a USD 1.2 billion module contract, validating scale economics, while Wolfspeed committed USD 1.5 billion to a new SiC fab that will supply automotive-grade wafers from 2026.

Software-Defined-Vehicle Transition Driving 32-bit and RISC-V MCUs in North America

General Motors, Ford, and Stellantis migrated from dozens of discrete controllers to a handful of reprogrammable domains managed by over-the-air software. NXP’s S32 platform integrates Arm Cortex-A55/A-R52 clusters, hardware security modules, and gigabit Ethernet, allowing OEMs to roll out features post-sale. SiFive’s automotive RISC-V cores gave Tier-1s an open ISA path, and Infineon confirmed a RISC-V MCU line slated for 2026. Cyber-hardening requirements boosted demand for on-chip HSMs and post-quantum-ready cryptography engines.

Zonal E/E Architecture Boosting Domain-Controller SoCs in Germany and USA

BMW’s iX reduced more than 100 ECUs to five domain controllers, trimming wiring mass by 30% and freeing cabin space. Continental launched production zonal gateways capable of handling 20 Gbit/s backbone traffic, built on Arm Cortex-A78AE CPUs with split-lock safety modes. Ford employed the same architectural logic for BlueCruise hands-free driving, funneling raw sensor data into centralized AI accelerators. The result is a steep uptick in multi-core SoCs and high-speed SerDes transceivers within the automotive integrated circuits market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lithography Bottlenecks <16 nm Constraining ADAS SoC Supply | -1.4% | Global, acute in Asia-Pacific | Short term (≤ 2 years) |

| Stricter ISO 26262 and AEC-Q104 Delaying SiC/GaN Qualification | -0.8% | Global, particularly Europe and North America | Medium term (2-4 years) |

| High Cost of FOWLP and SiP Packaging Squeezing Infotainment IC Margins | -0.6% | Global, concentrated in consumer-grade applications | Medium term (2-4 years) |

| Export-control Curbs on EDA Tools Slowing Chinese Supplier Progress | -0.9% | China, indirect global impact | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Lithography Bottlenecks <16 nm Constraining ADAS SoC Supply

ASML shipped only 20 EUV scanners in Q1 2024, leaving global capacity tight. Automotive lines run longer validation loops, so TSMC’s automotive-qualified 7 nm was under 60% utilization despite brisk demand. Mobileye’s EyeQ6 Lite processor suffered allocation-driven delivery slips, prompting OEMs to dual-source fallback 16 nm designs with lower TOPS ratings. Samsung’s USD 17 billion Texas fab will bring incremental headroom after 2026, but near-term shortages persist.

Stricter ISO 26262 and AEC-Q104 Delaying SiC/GaN Qualification

Wide-bandgap devices must now satisfy ASIL-D functional-safety flows in addition to AEC reliability stress. Infineon’s CoolSiC modules endured three-year qualification to clear both barometers. The latest AEC-Q104 demands add high-temp reverse-bias testing above 300 V, stretching validation to as long as 10,000 hours.[2]Automotive Electronics Council, “AEC-Q104 Rev A,” aecouncil.com Keysight estimated that compliance can double development cost, slowing time-to-market for next-gen traction inverters.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By IC Type: Microcontrollers Anchor the Transition to Centralized Compute

Microcontrollers retained 27.92% of automotive integrated circuits market share in 2025 and posted the highest 14.38% CAGR through 2031 as OEMs moved to software-defined domains. The automotive integrated circuits market size for MCU-based architectures is projected to widen in parallel with rising over-the-air update complexity and cybersecurity mandates. Legacy 8-bit controllers that once governed single actuators have ceded volume to multicore 32-bit devices with on-chip flash up to 24 MB. Analog power-management ICs held sizable revenue through battery junction boxes and DC-DC converters, while logic IC demand increased for high-speed sensor interfaces and time-sensitive networking PHYs. Memory adoption accelerated as infotainment, autonomy, and telematics stretched storage requirements past 128 GB per vehicle.

A niche yet crucial segment, digital signal processors, grew inside premium audio and corner-radar modules. Microprocessors, meanwhile, powered domain controllers that aggregate body, chassis, and powertrain functions. Tesla demonstrated the upper envelope by integrating custom 14 nm neural engines that processed full-frame vision inputs at 144 TOPS, illustrating how advanced driver assistance spurs custom compute. Average semiconductor bill-of-materials moved from USD 800 in legacy ICE cars to more than USD 1,350 in 2024 battery electrics, with microcontrollers comprising the single largest cost line.

By Application: ADAS Leads Today; Powertrain Leads Tomorrow

ADAS and safety applications secured 24.05% revenue share in 2025, driven by mandatory lane-keeping and emergency braking systems in the United States, Europe, and Japan. Processor-heavy sensor fusion stacks demanded high in-package bandwidth and embedded AI accelerators. Yet the powertrain and battery-management segment is slated for the fastest 13.58% CAGR, buoyed by 800-V architectures and silicon-carbide adoption. The automotive integrated circuits market size allocated to propulsion electronics will outpace chassis and body electronics as EV penetration climbs. LED matrix headlights, electrochromic glass, and smart-door modules sustained body electronics demand, while chassis electronics benefited from shift-by-wire and active suspension.

Telematics and gateway controllers grew under UNECE WP.29 cyber rules, evidenced by HARMAN’s secure domain routers in 2024 fleets. Qualcomm’s cockpit chips combining infotainment, 5G, and V2X exemplify convergence of once-separate domains. The integrated approach lowers board count and consolidates heat management but raises compute-density requirements.

By Vehicle Type: Passenger Dominance Meets Commercial Acceleration

Passenger cars commanded a 70.15% share in 2025 owing to sheer production scale and early ADAS uptake. Light commercial vehicles embraced electrified last-mile logistics, adding battery-monitoring controllers and telematics. Heavy commercial vehicles clocked the fastest 11.64% CAGR as autonomous freight pilots required sensor fusion processors, L4 compute boxes, and redundant power steering modules. Luxury trims averaged more than 3,000 semiconductors per unit versus 1,200 in entry-level models. Volvo Trucks adopted silicon-carbide traction inverters for its 540 kWh FH e-truck to manage thermal constraints and range efficiency.

By Propulsion: ICE Still Larger; BEV Outpaces

ICE and hybrid vehicles held 65.12% of revenue in 2025, but battery electric vehicles will dominate growth at 15.46% CAGR. The automotive integrated circuits market size for BEV propulsion eclipses that of ICE by 2031 as silicon-carbide MOSFETs, cell-balancing ASICs, and thermal management controllers proliferate. Porsche, Tesla, and Hyundai led the shift to 800-V architectures that demand higher blocking-voltage gate drivers, galvanically isolated current sensors, and advanced thermal interfaces. Silicon-carbide inverters improved WLTP range by 3%-5%, justifying higher component ASPs. Hybrids remained a transitional bridge, keeping demand for 48-V DC-DC regulators and starter-generator controllers.

By Wafer Node: Legacy Volumes; Advanced Value

Nodes ≥40 nm remained the revenue workhorse at 41.92% share because microcontrollers and power ICs favor proven, cost-efficient processes. Nevertheless, sub-10 nm nodes will clock 17.45% CAGR as autonomous features escalate TOPS targets. The automotive integrated circuits market taps advanced foundry IP only after multiyear reliability vetting, yet the lure of integrating CPU, GPU, NPU, and Ethernet MAC on a single die has accelerated acceptance. Chiplet architectures emerged to sidestep EUV scarcity; AMD married 7 nm compute chiplets with 14 nm IO dies, balancing cost and supply resilience. A cross-industry chiplet consortium with BMW, Bosch, and Arm drafted open interconnect specs in 2024, preparing a modular future for automotive SoCs.

Geography Analysis

Asia-Pacific generated 48.12% of 2025 revenue and will post a region-high 12.56% CAGR. China’s requirement for 25% domestic content nudged OEMs toward local fabs, while Japanese and Korean suppliers scaled advanced power devices. Taiwan Semiconductor Manufacturing Company reported automotive turnover of USD 1.85 billion in 2024, benefiting from 12-inch wafer leadership. Samsung and SK Hynix added automotive LPDDR5 and HBM lines, and India emerged as a cost-competitive back-end hub for global players.

Europe preserved a premium hardware niche, grounded in German engineering and EU safety regulation. Infineon and Continental collaborated on power and connectivity modules, leveraging proximity to BMW, Mercedes-Benz, and Volkswagen lines. The EUR 43 billion EU Chips Act aims to double the regional share of global semiconductors by 2030, an objective that could raise regional sourcing from the automotive integrated circuits market should fabs reach schedule. STMicroelectronics recorded EUR 4.26 billion in automotive revenue in 2024 across Franco-Italian facilities.

North America leveraged the USD 52.7 billion CHIPS and Science Act, with new fabs in Arizona, Texas, and New York earmarking capacity for automotive-grade production. OEMs secured long-term supply agreements to hedge geopolitical risk, and Mexico’s assembly clusters integrated more advanced semiconductors to support OTA-ready architectures. Canada’s proliferation of gigafactories drew demand for battery-monitoring ASICs and high-voltage gate drivers.

Competitive Landscape

The automotive integrated circuits market is moderately concentrated, with Infineon, NXP, STMicroelectronics, Renesas, and Texas Instruments accounting for roughly 60% of global revenue in 2024. Infineon rose to the top position at 11.9% share after integrating Cypress Semiconductor’s MCU and memory assets. NXP set itself apart through its S32 vehicle-wide compute platform and 77 GHz radar front-ends that enable scalable ADAS architectures.[4]NXP Semiconductors, “S32 Automotive Platform,” nxp.com STMicroelectronics leveraged in-house silicon-carbide MOSFET capacity to secure traction-inverter design wins with European OEMs. Renesas built on mixed-signal system-on-chip optimized for camera and lidar fusion, while Texas Instruments maintained a dominant position in analog power and signal-conditioning ICs for body, chassis, and infotainment domains.

Technology-focused challengers broaden competitive pressure. Allegro MicroSystems expanded its portfolio of high-accuracy magnetic position sensors for electrified powertrains. Melexis offers advanced high-temperature mixed-signal ICs for zone controllers in harsh environments. Mobileye continued to out-innovate through its EyeQ vision processors, produced on TSMC’s automotive-qualified 7 nm node, and secured multiple next-generation ADAS programs. Automakers’ preference for turnkey hardware–software stacks is intensifying competition around integrated developer platforms, cybersecurity frameworks, and seamless over-the-air enablement. At the same time, restricted foundry access below 16 nm and stringent functional-safety IP requirements keep entry barriers high, further consolidating share among qualified incumbents.

Automotive Integrated Circuits Industry Leaders

-

Intel Corporation

-

Texas Instruments Inc

-

Analog Devices Inc

-

Infineon Technologies AG

-

STMicroelectronics N.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: ROHM launched high-density SiC traction modules rated for 200 °C junctions, lifting inverter power density by 30%.

- March 2025: NXP released 16 nm S32K5 MCUs with Arm Cortex-M33 cores and on-die HSMs to serve OTA-ready architectures.

- January 2025: Infineon Technologies and Visteon partnered on silicon-carbide-based 800-V power electronics aimed at cutting EV charging time.

- January 2025: Honda and Renesas confirmed joint development of a 2,000 TOPS Level-4 autonomous SoC slated for 2027.

Global Automotive Integrated Circuits Market Report Scope

Automotive integrated circuits (ICs) are pivotal in modern automotive manufacturing, bolstering safety, efficiency, and overall performance. These miniature devices, used in applications ranging from engine control units to battery management systems, have transformed the automotive industry. With the ongoing evolution of automotive technology, integrated circuits are poised to take on a pivotal role in shaping the future of transportation. This shift promises safer, more efficient, and environmentally friendly vehicles.

The study tracks the revenue accrued through the sale of integrated circuit products by various players globally. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of the aftereffects of the COVID-19 pandemic and other macroeconomic factors on the market. The report's scope encompasses market sizing and forecasts for the various market segments.

The automotive integrated circuits market is segmented by type (analog IC, logic IC, memory, and micro [microprocessors (MPU), microcontrollers (MCU), and digital signal processors]) and geography (the United States, Europe, Japan, China, Korea, Taiwan, and Rest of the World). The market sizes and forecasts are provided in terms of value in USD for all the above-mentioned segments.

| Analog IC | |

| Logic IC | |

| Memory | |

| Micro | Microcontrollers (MCU) |

| Microprocessors (MPU) | |

| Digital Signal Processors (DSP) |

| Powertrain and Battery Management |

| ADAS and Safety |

| Body Electronics and Lighting |

| Chassis and Control |

| Infotainment and Connectivity |

| Telematics and Gateway |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Off-Highway and Special-Purpose Vehicles |

| Internal Combustion Engine Vehicles |

| Battery Electric Vehicles |

| Hybrid and Plug-in Hybrid Vehicles |

| ≥40 nm |

| 28 nm–32 nm |

| 16 nm–22 nm |

| <10 nm |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Nordics | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Taiwan | ||

| South Korea | ||

| Japan | ||

| India | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Mexico | ||

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By IC Type | Analog IC | ||

| Logic IC | |||

| Memory | |||

| Micro | Microcontrollers (MCU) | ||

| Microprocessors (MPU) | |||

| Digital Signal Processors (DSP) | |||

| By Application | Powertrain and Battery Management | ||

| ADAS and Safety | |||

| Body Electronics and Lighting | |||

| Chassis and Control | |||

| Infotainment and Connectivity | |||

| Telematics and Gateway | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Heavy Commercial Vehicles | |||

| Off-Highway and Special-Purpose Vehicles | |||

| By Propulsion | Internal Combustion Engine Vehicles | ||

| Battery Electric Vehicles | |||

| Hybrid and Plug-in Hybrid Vehicles | |||

| By Wafer Node | ≥40 nm | ||

| 28 nm–32 nm | |||

| 16 nm–22 nm | |||

| <10 nm | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| France | |||

| United Kingdom | |||

| Nordics | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Taiwan | |||

| South Korea | |||

| Japan | |||

| India | |||

| Rest of Asia-Pacific | |||

| South America | Brazil | ||

| Mexico | |||

| Argentina | |||

| Rest of South America | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the automotive integrated circuits market in 2026?

The market stood at USD 127.93 billion in 2026 and is projected to reach USD 203.27 billion by 2031.

Which segment holds the largest automotive integrated circuits market share by IC type?

Microcontrollers commanded 27.92% share in 2025 and remain the fastest-growing category at 14.38% CAGR.

Why are silicon-carbide power devices gaining traction in electric vehicles?

Silicon-carbide MOSFETs deliver up to 98.5% conversion efficiency, enabling 800-V architectures that cut DC-fast-charge times below 30 minutes.

How will sub-10 nm nodes influence future vehicle electronics?

They provide the computational density required for autonomous AI workloads and are forecast to grow at an 17.45% CAGR, though EUV capacity constraints persist.

What impact do regional incentive programs have on the supply chain?

The US CHIPS and EU Chips Acts allocate more than USD 90 billion combined to bolster local manufacturing, diversifying geographic risk and supporting long-term supply for automotive-grade semiconductors.

Which region is expanding fastest in the automotive integrated circuits market?

Asia-Pacific leads with a projected 12.56% CAGR to 2031, driven by China’s localization mandate and rapid EV adoption.

Page last updated on: