AI Framework Optimization Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 5.83 Billion |

| Market Size (2031) | USD 18.66 Billion |

| Growth Rate (2026 - 2031) | 26.20% CAGR |

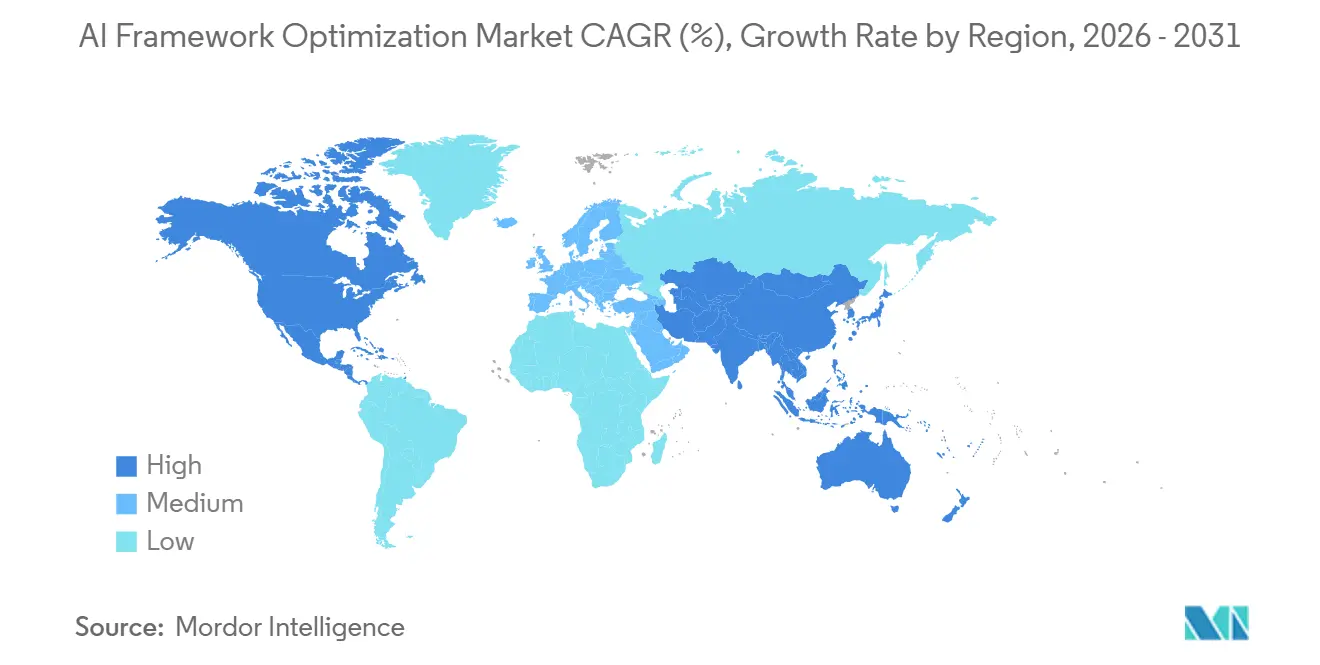

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

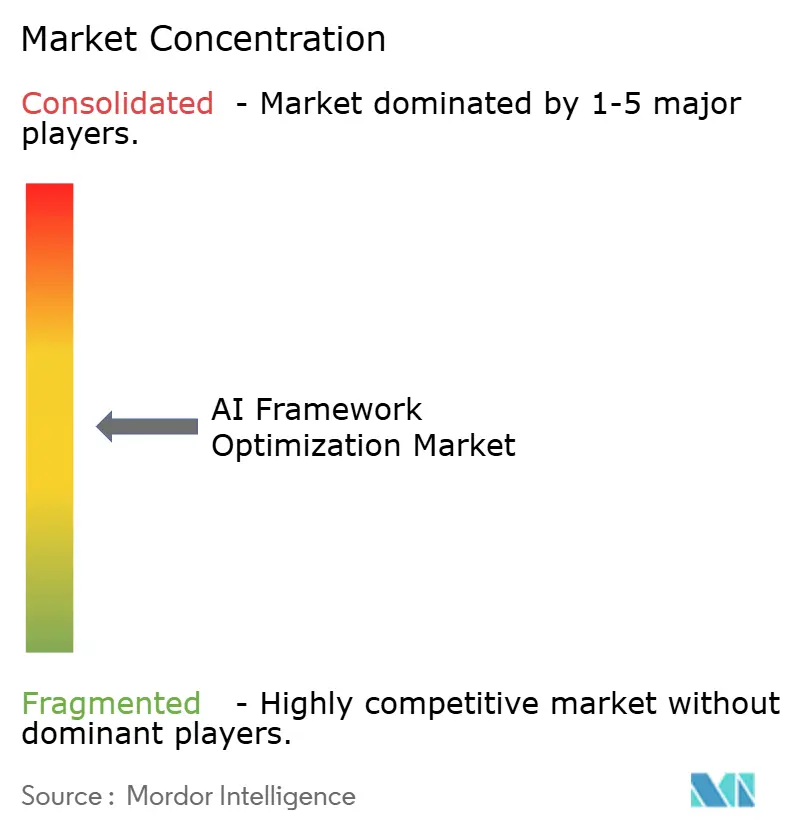

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

AI Framework Optimization Market Analysis by Mordor Intelligence

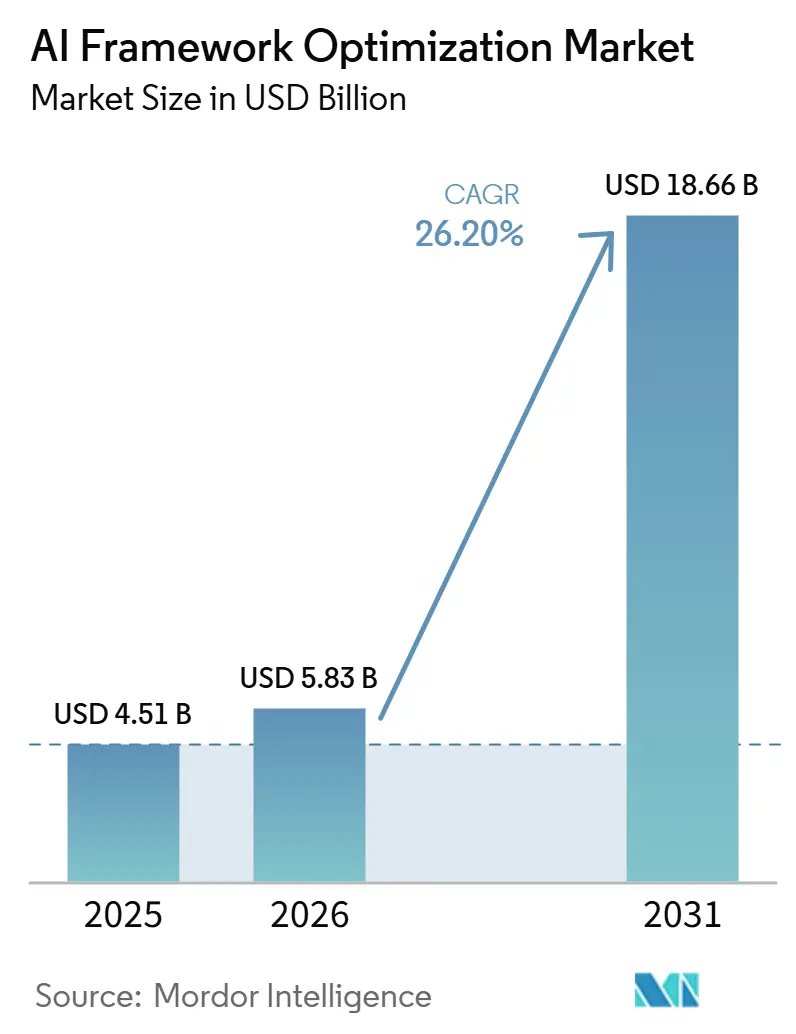

The AI framework optimization market size is expected to grow from USD 4.51 billion in 2025 to USD 5.83 billion in 2026 and is forecast to reach USD 18.66 billion by 2031 at 26.20% CAGR over 2026-2031. The AI framework optimization market is expanding because model deployment has become the main point where enterprises manage cost, latency, and service reliability across production AI systems. Growth is also tied to wider use of generative AI, multimodal models, and agentic workflows, since these workloads create heavier inference traffic and tighter performance requirements. The AI framework optimization market is also being pushed forward by on-device and hybrid architectures, where privacy limits, connectivity gaps, and response-time expectations make cloud-only designs less practical. Competition is led by large platform vendors with deep hardware and software stacks, while specialized vendors are gaining ground in compression, observability, portability, and purpose-built inference tooling. High accelerator costs, fragmented frameworks, talent shortages, and compression accuracy trade-offs continue to slow some deployments, but they have not altered the long-term demand outlook for the AI framework optimization market.

Key Report Takeaways

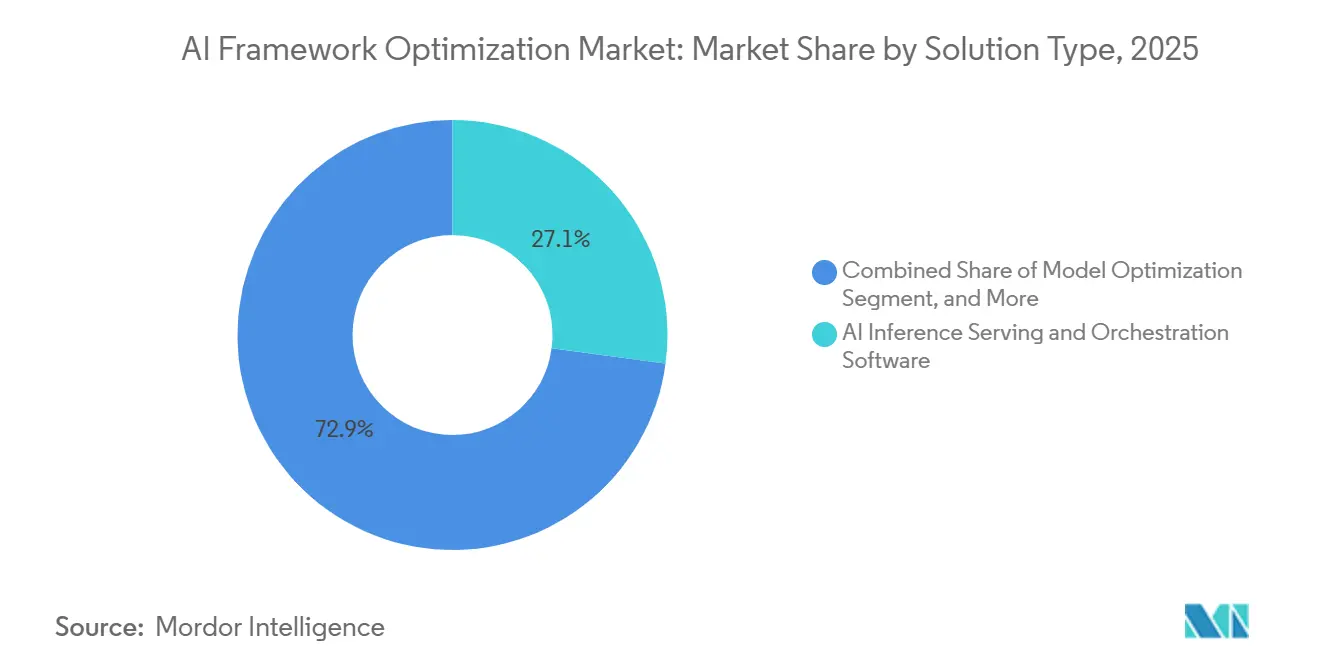

- By solution type, the AI framework optimization market was led by AI Inference Serving and Orchestration Software with 27.11% revenue share in 2025, while Model Optimization and Compression Software is projected to expand at a 27.21% CAGR through 2031.

- By deployment environment, Cloud and Hyperscale Data Centers held 54.33% revenue share in 2025, while On-Device AI is expected to record the fastest CAGR at 27.62% through 2031.

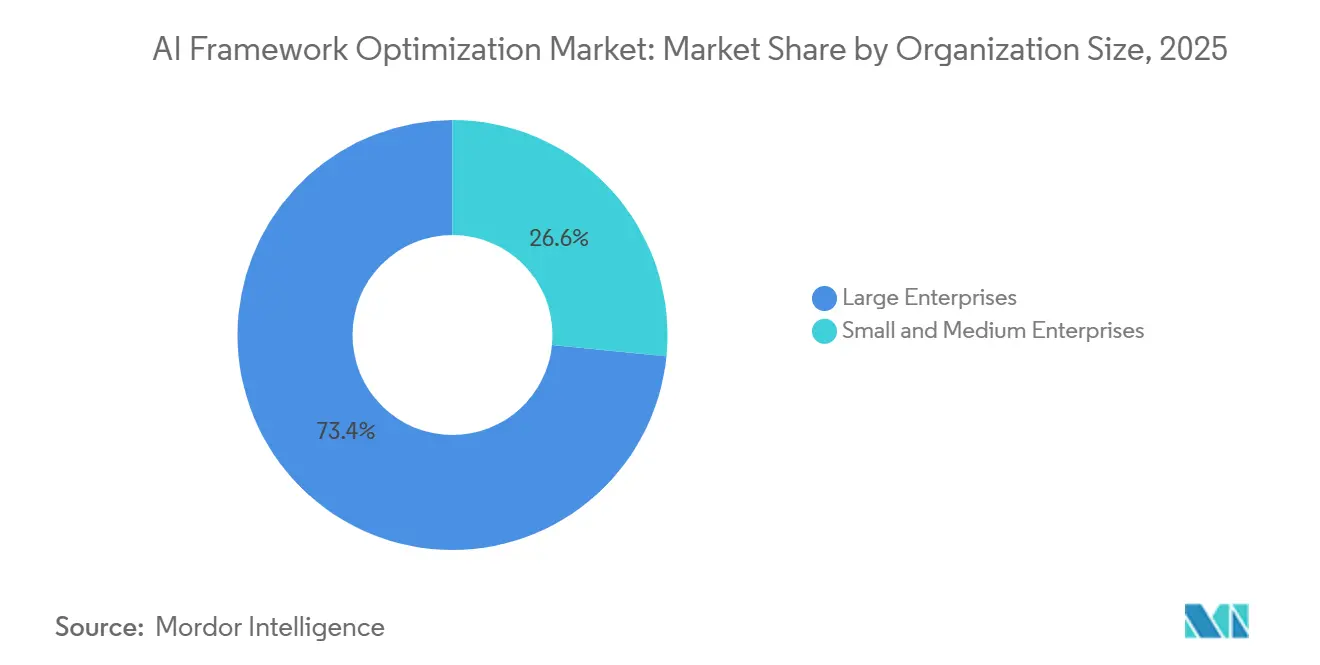

- By organization size, Large Enterprises accounted for 73.42% revenue share of the AI framework optimization market in 2025, while Small and Medium Enterprises are projected to grow at a 27.53% CAGR through 2031.

- By application, Generative AI, Large Language Models, and Multimodal AI captured 43.12% revenue share in 2025 and is forecast to advance at a 27.32% CAGR through 2031.

- By geography, North America held 48.44% revenue share of the AI framework optimization market in 2025, while Asia-Pacific is projected to expand at a 27.42% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global AI Framework Optimization Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Demand for Ultra-Low Latency Inferencing | +4.5% | Global, with concentration in North America and Asia-Pacific | Short term (≤ 2 years) |

| Growth Of Generative AI and Agentic Workflows | +4.2% | Global, fastest uptake in North America and Western Europe | Medium term (2-4 years) |

| Rising Enterprise Spending on AI Runtime Efficiency | +3.8% | North America and Europe, with spillover to Asia-Pacific | Medium term (2-4 years) |

| Expansion of Edge AI and on-Device Intelligence | +3.5% | Asia-Pacific core, with spillover to Middle East and Africa | Long term (≥ 4 years) |

| Hardware-Agnostic Optimization and Interoperability Needs | +2.8% | Global, particularly multi-cloud enterprises in North America and Europe | Medium term (2-4 years) |

| Data Sovereignty and Privacy-First AI Deployment | +2.4% | Europe, Middle East, and Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Ultra-Low Latency Inferencing

Latency is now a basic operating requirement in conversational AI, fraud detection, industrial control, robotics, and other live production systems. The AI framework optimization market is benefiting because every improvement in response time now has a direct effect on user experience, infrastructure utilization, and service consistency. This pressure is stronger in agentic systems, where a single workflow can trigger multiple model calls, retrieval steps, and tool actions before a result is returned. NVIDIA reported in February 2026 that DFlash speculative decoding on Blackwell architecture delivered throughput gains of up to 15x on specific workloads, which shows that large performance headroom still exists at the software layer.[1]NVIDIA, “Boost Inference Performance up to 15x on NVIDIA Blackwell Using DFlash Speculative Decoding,” NVIDIA Technical Blog, developer.nvidia.com That remaining headroom keeps buyers focused on batching, caching, token scheduling, and speculative execution rather than treating inference speed as a solved problem. The AI framework optimization market therefore continues to draw spending into serving software and runtime controls that can hold latency inside production thresholds as workloads become more complex.

Growth of Generative AI And Agentic Workflows

Generative AI has moved beyond isolated pilots and now sits closer to real business processes, customer support flows, developer tools, and internal knowledge systems. The AI framework optimization market is gaining from this shift because agentic workflows multiply inference events faster than traditional single-step AI use cases. Each added reasoning pass, retrieval loop, and external tool call increases memory pressure, token throughput requirements, and the need for better execution planning. NVIDIA introduced Vera in March 2026 as a processor purpose-built for agentic AI, which signals that vendors are already redesigning systems around the heavy runtime behavior of multi-step AI workloads. The practical result is that enterprises are placing more value on orchestration layers that can manage prompts, context, model routing, and repeated execution without unacceptable delay. As agentic designs spread, the AI framework optimization market is likely to stay closely linked to serving efficiency rather than only to model innovation.

Rising Enterprise Spending on AI Runtime Efficiency

Enterprise buyers are increasingly reviewing AI budgets through the lens of unit economics, especially when production workloads run continuously across large user bases. The AI framework optimization market benefits from that shift because runtime gains can improve hardware utilization and reduce waste without requiring a full model redesign. NVIDIA positioned TensorRT LLM AutoDeploy as a way to convert PyTorch models into optimized inference graphs with less manual rework, which lowers deployment friction and shortens the path from experimentation to production tuning. Intel also introduced Vector Core Compute in June 2026 as a disaggregated enterprise inference cloud spanning Intel Xeon, SambaNova RDUs, and NVIDIA Blackwell GPUs, which shows that runtime efficiency is now part of cross-hardware infrastructure planning.[2]Intel, “Intel Announces New AI Innovations at Computex,” Intel Newsroom, newsroom.intel.com This spending logic supports tools that can compress models, distribute workloads, and monitor execution across mixed environments without repeated manual tuning. The AI framework optimization market is therefore being shaped by buyers who want measurable production savings, predictable service levels, and easier runtime governance.

Expansion of Edge AI and On-Device Intelligence

On-device AI is expanding because many applications cannot depend on constant cloud connectivity or tolerate long round trips for each inference task. The AI framework optimization market is moving with this change because local deployment requires compact models, hardware-aware runtimes, and efficient memory management across consumer and industrial devices. NVIDIA launched TensorRT Edge-LLM in 2026 for embedded automotive and robotics inference on DRIVE AGX Thor and Jetson Thor, which confirms that edge optimization is developing as its own product category. AMD also expanded ROCm support in January 2026 across Ryzen AI platforms and ComfyUI workflows, broadening the software base for local inference and client-side optimization. This matters because power limits, device memory, and thermal constraints make software efficiency more important when models move away from centralized data centers. As a result, the AI framework optimization market is drawing more interest from device makers, automotive suppliers, and enterprise buyers that need low-latency AI closer to end users.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost of Specialized AI Infrastructure | -3.2% | Global, most acute in South America and Middle East and Africa | Short term (≤ 2 years) |

| Framework Fragmentation and Integration Complexity | -2.5% | Global, particularly in multi-cloud North American enterprises | Medium term (2-4 years) |

| Shortage Of AI Optimization and Systems Talent | -1.8% | Global, most acute in North America and Europe | Long term (≥ 4 years) |

| Model Accuracy Trade-Offs During Compression | -1.4% | Global, most restrictive in regulated verticals such as healthcare and finance | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost of Specialized AI Infrastructure

Optimization still depends on direct access to the hardware on which models will actually run in production. The AI framework optimization market therefore remains constrained by the cost of accelerator fleets, high-performance servers, and the supporting power and cooling capacity needed to test at scale. This burden is heavier for mid-market buyers and for regions where compute availability and data center readiness are less developed. Cloud access helps, but it can also add recurring expense and reduce direct control over benchmarking, kernel tuning, and validation cycles. The European Commission proposed the Cloud and AI Development Act in June 2026 to create an EU-wide framework for trusted cloud and AI development, which could improve access over time, but this is still a policy response rather than an immediate infrastructure fix. Until access broadens materially, the AI framework optimization market will continue to face slower adoption among organizations that want efficiency gains but cannot secure enough specialized compute to optimize effectively.

Framework Fragmentation and Integration Complexity

The software stack around AI has diversified faster than standard practices have matured, which creates heavy integration work for deployment teams. The AI framework optimization market is affected because enterprises often need the same model to behave consistently across PyTorch, JAX, TensorFlow, ONNX, and hardware-specific runtimes. Research archived on arXiv found that ONNX conversion failures were often linked to incompatibility and type issues, with crashes and incorrect model behavior among the common outcomes.[3]arXiv, “Interoperability in Deep Learning, A User Survey and Failure Analysis of ONNX Model Converters,” arXiv, arxiv.org Every additional accelerator architecture also brings a separate kernel and compilation path, which increases testing effort in mixed-hardware estates and slows rollout. The EU AI Act adds more pressure by requiring stronger documentation and traceability for high-risk systems, which makes ad hoc optimization pipelines harder to defend in regulated settings. This complexity keeps the AI framework optimization market attractive for interoperability-focused vendors, but it also raises switching costs and extends deployment timelines for end users.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Inference Serving Leads While Compression Accelerates

AI Inference Serving and Orchestration Software held 27.11% of the AI framework optimization market share in 2025, which made it the largest solution segment. Its lead reflects the fact that optimization only creates visible business value when models can be served reliably in production with stable latency and availability. Enterprises often begin with serving and orchestration because this layer connects infrastructure decisions directly to user experience, service continuity, and operating cost. The segment also benefits from growing use of agentic workflows, where repeated model calls require stronger routing, caching, and session control than earlier AI deployments. In practical terms, this keeps the AI framework optimization market centered on software that can operationalize models at scale rather than simply improve isolated benchmark scores.

The AI framework optimization market size for Model Optimization and Compression Software is projected to expand at 27.21% CAGR through 2031, making it the fastest-growing solution segment. This growth reflects the commercial push to extract more throughput from existing compute rather than solve every deployment problem with new hardware purchases. ACL Anthology research published in 2025 showed that careful W8A8-INT quantization narrowed the reported accuracy gap versus FP8 to 0.7 points on large models, which helped validate production-grade compression pathways for larger deployments. Graph compilation, runtime acceleration, profiling, observability, and managed services remain important because each handles a different stage between model preparation and live execution. Taken together, these layers give the AI framework optimization market a broad solution mix where no single category can replace the others across all customer environments.

By Deployment Environment: Cloud Anchors Revenue as On-Device AI Captures Growth

Cloud and Hyperscale Data Centers accounted for 54.33% of the AI framework optimization market size in 2025, which kept cloud infrastructure as the main revenue base for deployment. This position reflects the scale at which hyperscalers and large enterprises run shared inference platforms, centralized model updates, and heavy production workloads. Cloud environments also make it easier to roll out optimization changes once and distribute the benefit across many users, teams, and services. For organizations moving from pilot work into sustained production, that operational simplicity remains a strong advantage. As a result, the AI framework optimization market continues to send a large share of spending toward cloud-native serving, scheduling, and observability tools.

The AI framework optimization market size for On-Device AI is projected to expand at 27.62% CAGR through 2031, the fastest rate among deployment environments. Local execution is gaining because privacy requirements, weak connectivity, and strict response-time targets make many workloads difficult to support through cloud-only inference. NVIDIA introduced TensorRT Edge-LLM in 2026 for embedded automotive and robotics inference, which highlights the rise of device-specific optimization stacks. On-premises, edge infrastructure, and hybrid models are also becoming more relevant because many organizations now split workloads across public and private environments instead of relying on a single runtime. This diversification means the AI framework optimization market increasingly rewards vendors that can manage portability, governance, and performance across several deployment paths at once.

By Organization Size: Large Enterprises Dominate But SMEs Narrow the Gap

Large Enterprises held 73.42% of market revenue in 2025, which made them the clear revenue leaders in the AI framework optimization market. Their lead comes from higher inference volumes, larger experimentation budgets, and stronger capacity to support dedicated platform and infrastructure teams. These buyers are also more likely to test several model families, compare hardware options, and negotiate software terms across multiple vendors and deployment environments. In many cases, optimization is treated as an ongoing platform decision rather than a one-time project, which supports broader product adoption and longer contracts. This keeps large enterprise accounts central to road maps across the AI framework optimization market, especially for advanced orchestration, observability, and compliance functions.

Small and Medium Enterprises are projected to expand at 27.53% CAGR through 2031, making them the fastest-growing customer group in the AI framework optimization industry. Their growth is being supported by usage-based APIs, managed inference services, and lighter deployment models that reduce the need for full in-house platform teams. Many SMEs focus on narrow and repeatable workloads where latency and per-request cost affect margins quickly, so optimization benefits become visible soon after deployment. This widens the addressable base of the AI framework optimization market, even though purchasing behavior still differs sharply from that of large enterprises. Over time, this shift should support more packaged offerings, simpler onboarding models, and clearer pricing across the AI framework optimization industry.

By Application: Generative AI and LLMs Define the Market's Center of Gravity

Generative AI, Large Language Models, and Multimodal AI commanded 43.12% of application revenue in 2025, which gave this category the largest position in the AI framework optimization market. This lead reflects the heavy token traffic, high memory requirements, and visible latency risks associated with larger model classes. Improvements in batching, quantization, caching, and speculative decoding therefore have an immediate effect on user-facing performance and operating cost. These models also sit at the center of many agentic workflows, where one output can trigger additional reasoning, retrieval, and tool-based steps. For that reason, the AI framework optimization market remains closely tied to the commercial scaling of generative and multimodal applications.

This application group held 43.12% of the AI framework optimization market share in 2025 and is projected to expand at 27.32% CAGR through 2031. Computer vision, document intelligence, speech, recommendation, predictive analytics, and robotics remain meaningful categories, but their optimization needs are often more workload-specific. Hugging Face and Cerebras demonstrated in 2026 that real-time voice pipelines can now run on Gemma 4-based architectures, which reinforces the commercial relevance of low-latency speech optimization in production settings. Because application requirements differ so widely, no single software architecture is likely to serve every workload equally well, which leaves room for specialized vendors across the AI framework optimization industry. This diversity of use cases also helps explain why the AI framework optimization market supports both broad platform stacks and narrower tools designed for specific inference patterns.

Geography Analysis

North America accounted for 48.44% of the AI framework optimization market size in 2025, which kept the region in the lead on revenue. The United States anchors this position through hyperscale cloud capacity, a dense vendor ecosystem, and a steady pace of product launches across inference software and AI hardware. Canada adds regional depth through its research base and commercialization networks, which help move model work into deployable runtime and serving tools. South America remains smaller, but interest is rising where enterprises are expanding digital infrastructure and looking for lower-cost ways to support local AI execution.

Europe remains a major region in the AI framework optimization market because regulation now shapes deployment design as much as performance does. The EU AI Act, which became fully applicable from August 2, 2026, increases the value of auditable optimization workflows for high-risk systems. Germany, the United Kingdom, and France form the main demand centers through manufacturing, financial services, healthcare, and public-sector use cases that require reliable inference behavior. The European Commission's June 2026 proposal for the Cloud and AI Development Act also points to stronger sovereign compute frameworks, which can support on-premises and hybrid stack adoption across Europe and influence buyer priorities in nearby regulated markets.

Asia-Pacific is projected to expand at 27.42% CAGR through 2031, making it the fastest-growing regional block in the AI framework optimization market. Growth in the region is supported by government-backed AI infrastructure plans, very large device manufacturing bases, and stronger interest in domestic software ecosystems. China, India, Japan, and South Korea each contribute in different ways, with China emphasizing self-reliance, India widening access to compute, Japan linking AI investment to industrial modernization, and South Korea supporting hardware and device ecosystems. Southeast Asia adds momentum because enterprises in Indonesia, Malaysia, and Vietnam are moving from experimentation toward more stable operational deployment. Middle East and Africa also show rising activity as sovereign AI programs and local data initiatives increase interest in optimization software that can work across cloud, private, and edge environments.

Competitive Landscape

The AI framework optimization market is moderately concentrated at the platform layer, where NVIDIA, Microsoft, and Google benefit from broad developer reach and tightly integrated software stacks. Their strength comes from combining runtimes, compilers, serving tools, and hardware alignment in ways that simplify deployment for enterprise customers. Even so, the broader AI framework optimization market remains contested because edge deployment, observability, portable runtimes, and managed compression still support a large field of specialized vendors. This creates a structure where leadership is strong in the core platform layer, but less settled in the layers closest to workload-specific tuning and heterogeneous execution.

NVIDIA strengthened its position in 2025 and 2026 through TensorRT LLM AutoDeploy and DFlash speculative decoding, both of which moved more optimization work into automated software layers and improved the ease of production deployment. Intel also moved to support heterogeneous deployment in June 2026 with Vector Core Compute, which linked Intel Xeon, SambaNova RDUs, and NVIDIA Blackwell GPUs inside a disaggregated enterprise inference cloud. AMD widened its ROCm ecosystem in January 2026 by extending support across Ryzen AI platforms and ComfyUI, which improved its relevance in client-side and local inference workflows. These moves show that competition in the AI framework optimization market is now shaped as much by software usability and portability as by raw silicon performance.

The strongest white-space areas in the AI framework optimization market remain hardware-agnostic runtimes, observability for multi-step inference flows, and managed compression for buyers with limited platform teams. Modular targeted this opening in 2026 through its MAX framework and Mojo 1.0 Beta, which emphasized portability, multi-GPU support, and production-oriented kernel development. Modular also partnered with Hippocratic AI in May 2026 to validate MAX in production healthcare inference on NVIDIA B300 GPUs, giving it a concrete reference point in a regulated deployment setting. Competition is therefore likely to stay active below the top platform tier, especially where customers need cross-hardware flexibility or domain-specific optimization support. This structure helps preserve room for smaller vendors even as a few large ecosystems continue to influence standards, tooling choices, and developer habits across the AI framework optimization market.

AI Framework Optimization Industry Leaders

NVIDIA Corporation

Advanced Micro Devices, Inc.

Microsoft Corporation

Alphabet Inc.

Amazon Web Services, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2026: Groq raised USD 650 million in growth capital led by Disruptive and Infinitum to scale its AI inference cloud to 200 MW by end of 2027, deploying NVIDIA's LPX (Liquid Processing Unit) systems across its 13-datacenter global footprint. The raise signals continued institutional confidence in purpose-built inference infrastructure as a counterweight to general-purpose GPU dominance.

- June 2026: Qualcomm and Hugging Face expanded their strategic relationship to advance open, developer-driven AI from device to cloud. The collaboration targets on-device AI inference optimization across Qualcomm's Snapdragon platform ecosystem, enabling access to hardware-specific AI runtimes directly through the Hugging Face Hub.

- June 2026: Intel unveiled Xeon 6+ processors at Computex 2026 along with Vector Core Compute, a purpose-built enterprise inference cloud for disaggregated inference running on Intel Xeon, SambaNova RDUs, and NVIDIA Blackwell GPUs. The multi-vendor disaggregated architecture signals a shift toward heterogeneous inference stacks requiring multi-runtime optimization orchestration.

- March 2026: NVIDIA launched the Vera CPU, described as the world's first processor purpose-built for agentic AI, delivering twice the efficiency and 50% faster performance versus traditional rack-scale CPUs. Vera features LPDDR5X memory delivering up to 1.2 TB/s bandwidth, targeting the memory-bandwidth bottlenecks that constrain agentic inference workloads.

Global AI Framework Optimization Market Report Scope

The AI Framework Optimization Market refers to the industry segment focused on enhancing and streamlining artificial intelligence (AI) frameworks to maximize computational efficiency, scalability, and performance across diverse hardware and software environments.

The AI Framework Optimization Report is Segmented by Solution Type (Model Optimization and Compression Software, Graph Compilation and Kernel Optimization Software, AI Runtime and Hardware Acceleration Software, AI Inference Serving and Orchestration Software, Performance Profiling, Benchmarking, and Observability Tools, and Professional and Managed Optimization Services), Deployment Environment (Cloud and Hyperscale Data Centers, On-Premises and Private Cloud, Edge Infrastructure, On-Device AI, and Hybrid Deployment), Organization Size (Large Enterprises and Small and Medium Enterprises), Application (Generative AI, Large Language Models, and Multimodal AI, Natural Language Processing and Document Intelligence, Computer Vision and Video Analytics, Speech and Audio AI, Recommendation, Search, and Personalization Engines, Predictive Analytics, Classical ML, and Decision Intelligence, Robotics, Autonomous Systems, and Edge Intelligence, and Other Applications), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| Model Optimization and Compression Software |

| Graph Compilation and Kernel Optimization Software |

| AI Runtime and Hardware Acceleration Software |

| AI Inference Serving and Orchestration Software |

| Performance Profiling, Benchmarking, and Observability Tools |

| Professional and Managed Optimization Services |

| Cloud and Hyperscale Data Centers |

| On-Premises and Private Cloud |

| Edge Infrastructure |

| On-Device AI |

| Hybrid Deployment |

| Large Enterprises |

| Small and Medium Enterprises |

| Generative AI, Large Language Models, and Multimodal AI |

| Natural Language Processing and Document Intelligence |

| Computer Vision and Video Analytics |

| Speech and Audio AI |

| Recommendation, Search, and Personalization Engines |

| Predictive Analytics, Classical ML, and Decision Intelligence |

| Robotics, Autonomous Systems, and Edge Intelligence |

| Other Applications |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Solution Type | Model Optimization and Compression Software | |

| Graph Compilation and Kernel Optimization Software | ||

| AI Runtime and Hardware Acceleration Software | ||

| AI Inference Serving and Orchestration Software | ||

| Performance Profiling, Benchmarking, and Observability Tools | ||

| Professional and Managed Optimization Services | ||

| By Deployment Environment | Cloud and Hyperscale Data Centers | |

| On-Premises and Private Cloud | ||

| Edge Infrastructure | ||

| On-Device AI | ||

| Hybrid Deployment | ||

| By Organization Size | Large Enterprises | |

| Small and Medium Enterprises | ||

| By Application | Generative AI, Large Language Models, and Multimodal AI | |

| Natural Language Processing and Document Intelligence | ||

| Computer Vision and Video Analytics | ||

| Speech and Audio AI | ||

| Recommendation, Search, and Personalization Engines | ||

| Predictive Analytics, Classical ML, and Decision Intelligence | ||

| Robotics, Autonomous Systems, and Edge Intelligence | ||

| Other Applications | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the current and forecast value of the AI framework optimization space?

The AI framework optimization market was valued at USD 4.51 billion in 2025, reached USD 5.83 billion in 2026, and is forecast to reach USD 18.66 billion by 2031 at a 26.20% CAGR.

Which solution category leads revenue in AI framework optimization?

AI Inference Serving and Orchestration Software led revenue with a 27.11% share in 2025 because enterprises prioritize reliable production deployment and low-latency execution.

Which deployment model is growing the fastest?

On-Device AI is the fastest-growing deployment environment, with a projected 27.62% CAGR through 2031, driven by privacy, response-time, and connectivity requirements.

Why are generative AI and agentic workflows driving demand for optimization tools?

These workloads create heavier token traffic and repeated inference events, which makes batching, routing, caching, and compression more important to control cost and latency.

Which region is leading adoption and which region is growing the fastest?

North America held the largest share at 48.44% in 2025, while Asia-Pacific is expected to record the fastest growth at a 27.42% CAGR through 2031.

What are the main barriers slowing adoption?

The biggest constraints are high specialized infrastructure costs, fragmented frameworks, limited interoperability, talent shortages, and the risk of accuracy loss during aggressive model compression.

Page last updated on: