Automotive Special Purpose Logic IC Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

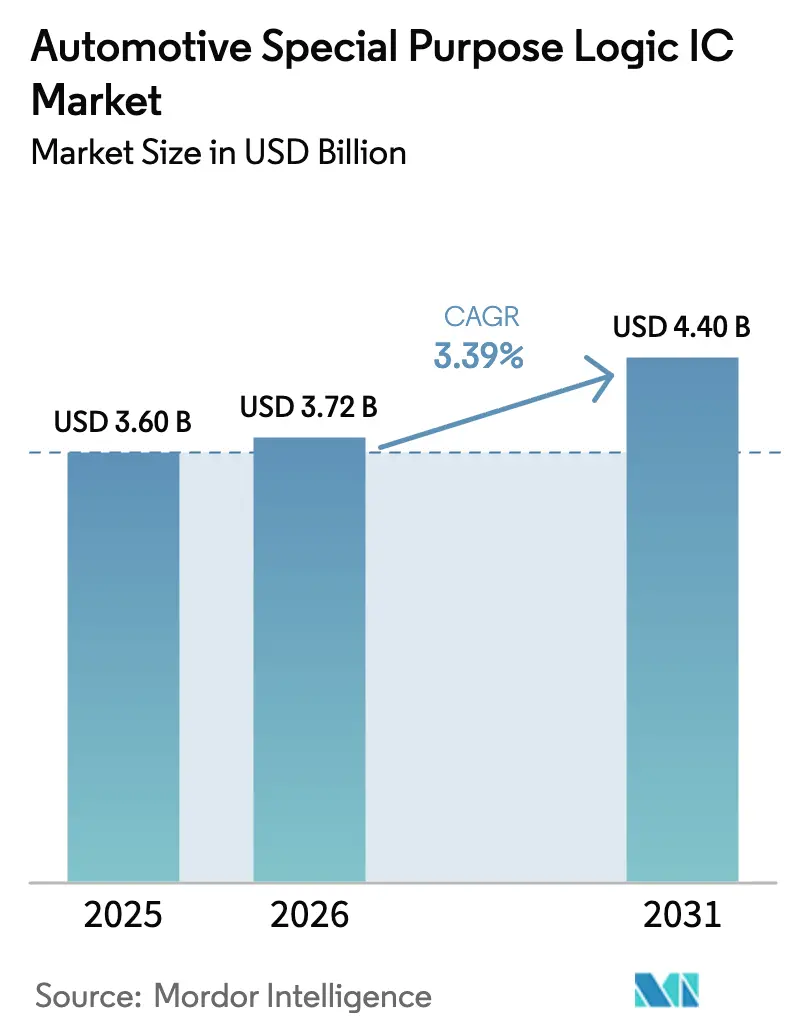

| Market Size (2026) | USD 3.72 Billion |

| Market Size (2031) | USD 4.4 Billion |

| Growth Rate (2026 - 2031) | 3.39% CAGR |

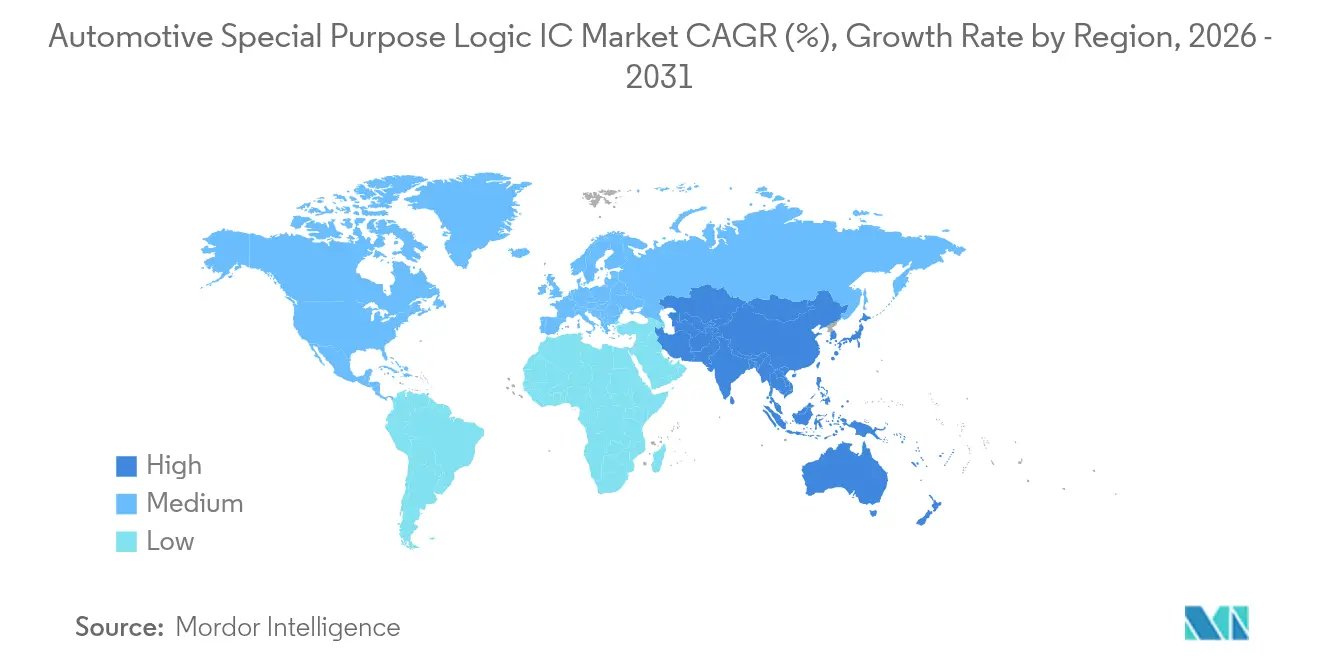

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Automotive Special Purpose Logic IC Market Analysis by Mordor Intelligence

Automotive special-purpose logic IC market size in 2026 is estimated at USD 3.72 billion, growing from 2025 value of USD 3.6 billion with 2031 projections showing USD 4.4 billion, growing at 3.39% CAGR over 2026-2031. Robust demand stems from the rising penetration of ADAS, the widening electrification of powertrains, and a steady shift toward zonal electrical/electronic (E/E) architectures, which require higher integration densities and real-time processing capabilities. Automakers favor logic ICs that combine low-latency performance with strict functional safety compliance, prompting suppliers to move beyond commodity devices toward application-specific solutions. Supply resilience remains a strategic focus as mature-node wafer capacity tightens amid geopolitical tensions, prompting OEMs to dual-source parts and secure long-term foundry agreements. Concurrently, chiplet-oriented System-in-Package (SiP) designs lower total cost of ownership by allowing incremental feature updates without full-mask re-spins.

Key Report Takeaways

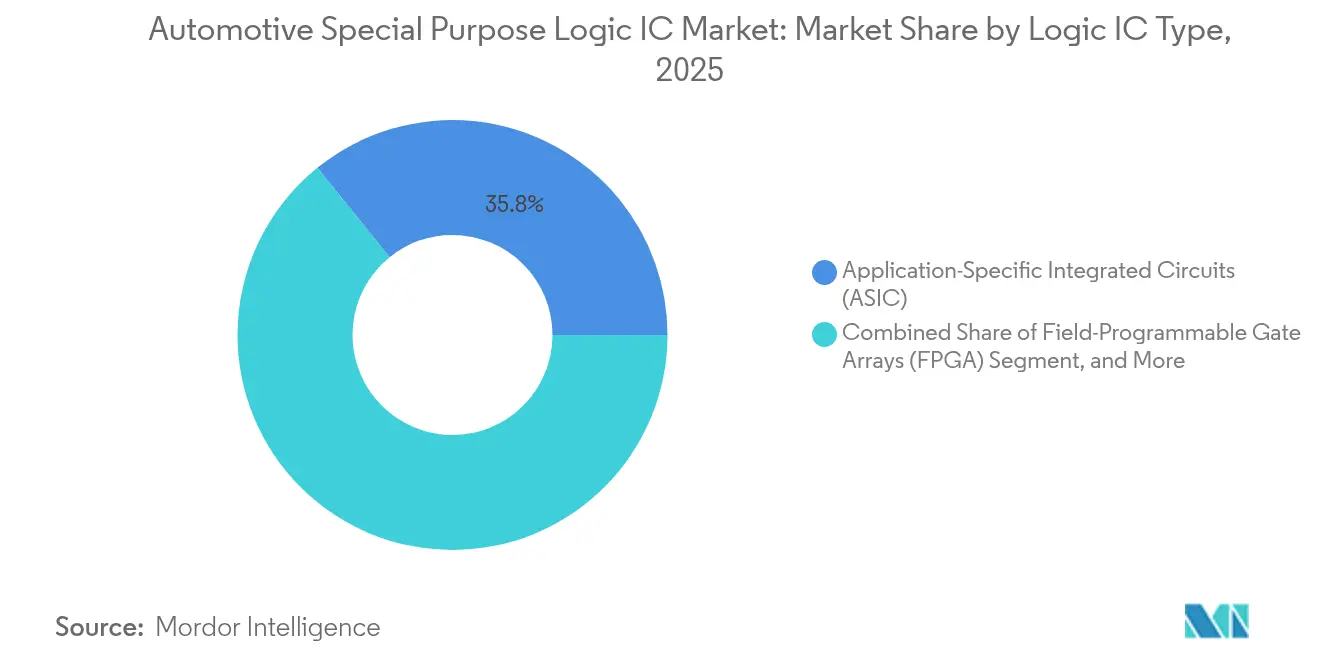

- By logic IC type, ASICs led with 35.82% revenue share in 2025; FPGAs are projected to expand at a 3.58% CAGR through 2031.

- By application, ADAS held a 29.55% market share of the automotive special-purpose logic IC market in 2025 and is expected to grow at a 3.88% CAGR through 2031.

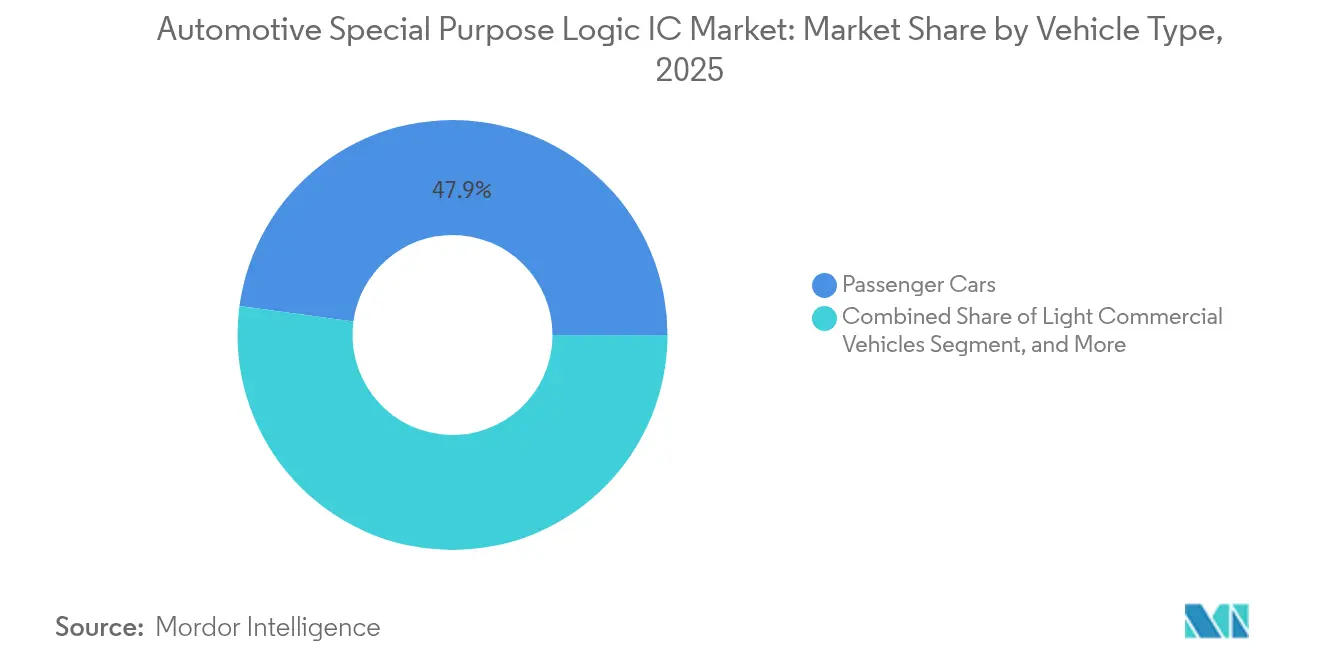

- By vehicle type, passenger cars accounted for a 47.85% share of the automotive special-purpose logic IC market size in 2025, while electric vehicles are expected to advance at a 3.95% CAGR through 2031.

- By packaging technology, SiP captured 30.76% of 2025 revenue and is anticipated to rise at a 3.74% CAGR over the forecast period.

- By geography, the Asia-Pacific region contributed 32.05% of global sales in 2025; it is forecast to record the fastest growth of 3.46% CAGR from 2025 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive Special Purpose Logic IC Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Surging ADAS and autonomous-driving penetration | +0.8% | Global; early adoption in North America and Europe | Medium term (2-4 years) |

| Rapid electrification of powertrains elevates logic-IC content | +0.6% | Asia-Pacific core; spill-over to North America and Europe | Long term (≥ 4 years) |

| Government safety mandates are accelerating semiconductor demand | +0.4% | Global, led by the European framework | Short term (≤ 2 years) |

| Transition to zonal/centralized E/E architectures | +0.3% | Premium segments in North America and Europe | Medium term (2-4 years) |

| Chiplet-based SiP enabling cost-efficient customization | +0.2% | Global manufacturing concentration in the Asia-Pacific | Medium term (2-4 years) |

| Automotive-Ethernet PHY adoption for high-speed data backbones | +0.1% | Premium and luxury segments worldwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging ADAS and autonomous-driving penetration

Euro NCAP protocol updates now require automatic emergency braking on commercial vehicles, instantly boosting demand for logic devices that fuse radar, camera, and LiDAR inputs while meeting ASIL-D safety targets.[1]European Commission Staff, “Road Safety—Vehicle Safety,” European Commission, ec.europa.eu Level 3 autonomy shifts have normalized dual-core lockstep architectures, prompting OEMs to specify custom ASICs that reduce power budgets and BOM costs compared to general-purpose MCUs, as ADAS availability nears that of new-car sales in developed markets.

Rapid electrification of powertrains elevating logic-IC content

Each battery electric model introduces higher-value logic controllers for pack monitoring, motor inverters, and on-board chargers; Tesla’s 4680 cell design alone adds USD 150–200 of semiconductor logic per vehicle for battery management.[2]Tesla Investor Relations. "Quarterly Earnings Reports." 2024. https://ir.tesla.com/quarterly-earnings Wider 800 V architectures in premium EVs create fresh demand for isolated gate drivers and fault-tolerant logic, with SiC and GaN components pushing switching frequencies and thermal limits that legacy devices cannot match.[3]Infineon Technologies. "Press Releases 2024." https://www.infineon.com/cms/en/about-infineon/press/press-releases/2024/

Government safety mandates accelerating semiconductor demand

The EU's General Safety Regulation mandates intelligent speed assistance and emergency braking in all new vehicles, turning legislative requirements into tangible silicon demand. These regulations aim to enhance road safety by reducing accidents and fatalities through the use of advanced vehicle technologies. Concurrently, the NHTSA's proposals for heavy-duty fleets and Japan's functional-safety guidelines further bolster the demand for logic ICs. These measures are designed to ensure compliance with safety standards while addressing the growing complexity of modern vehicles. This trend provides suppliers with clearer visibility into their order books, easing the financial strain of qualification costs and enabling long-term planning for production and innovation.

Transition to zonal/centralized E/E architectures

BMW's move to consolidate over 100 electronic control units (ECUs) into just five zone controllers necessitates the use of advanced logic ICs. These ICs must manage diverse tasks and transmit gigabit data via automotive Ethernet. This transition reflects the industry's efforts to simplify vehicle architectures, reduce wiring complexity, and improve overall system efficiency. While bridge logic, which ensures compatibility with older systems, sees a surge in demand, this is expected to decline as the industry fully transitions to zonal architectures, which offer enhanced scalability and support for future technological advancements.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Stringent manufacturing-process complexity and defect-density limits | –0.4% | Global; acute at mature node fabs | Long term (≥ 4 years) |

| Lengthy AEC-Q qualification cycle prolongs time-to-market | –0.3% | Global; regional test-variance | Medium term (2-4 years) |

| Geopolitical risks around mature-node wafer supply | –0.2% | Asia-Pacific hubs; global spill-over | Short term (≤ 2 years) |

| Escalating ASIC NRE costs for low-volume vehicle programs | –0.1% | Global, premium vehicles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent manufacturing-process complexity and defect-density limits

AEC-Q100 Grade 0 mandates single-digit DPPM rates from –40 °C to +150 °C. This requirement pushes TSMC to implement specialized tweaks in its automotive lines, resulting in lower utilization rates, increased unit costs, and constrained spare capacity during demand surges. Additionally, extended burn-in periods and tighter SPC loops can extend the fab cycle time by as much as 60% when compared to flows used for consumer logic. These factors collectively contribute to the increased complexity and higher costs associated with manufacturing processes for automotive-grade semiconductors.

Lengthy AEC-Q qualification cycle prolonging time-to-market

Qualification windows typically span 12 to 18 months, costing an additional USD 2 to 5 million for each device family. This financial burden sidelines smaller innovators from niche markets and keeps older silicon in production longer than its technological relevance warrants. Such delays hinder the swift adoption of rapidly evolving standards, such as V2X, transforming what could have been early revenue into postponed gains. The extended qualification process also impacts the ability of manufacturers to respond quickly to market demands, further complicating the competitive landscape.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Logic IC Type: ASIC solutions anchor cost control

ASICs accounted for 35.82% of 2025 revenue, underscoring OEM preference for high-volume economies over the programmable convenience of FPGAs. FPGA uptake, however, is rising fastest at 3.58% CAGR as over-the-air update requirements force reconfigurability without mechanical recalls. Intel’s latest automotive FPGA family cuts power consumption by 30% and narrows the cost gap, inviting wider design-ins where algorithm agility is paramount. The automotive special-purpose logic IC market size for FPGA-based implementations is projected to increase steadily as Level 3 autonomy layers demand code adaptability for sensor fusion tweaks.

Second-tier CPLDs serve deterministic tasks such as airbag trigger logic, where nanosecond response times and near-zero standby power outweigh raw computational power. ASSPs remain mid-volume default picks when custom ASIC economics falter, giving Tier 1 suppliers a balance between per-unit cost and schedule risk. Across all categories, the automotive special-purpose logic IC market opportunities tilt toward devices that integrate embedded safety monitors and secure boot features mandated under the UNECE cybersecurity regulation.

By Application: ADAS sustains top billing

ADAS generated 29.55% of industry revenue in 2025 and is poised for a 3.88% CAGR through 2031 as mandatory automatic emergency braking and lane-keeping rules are implemented worldwide. ADAS compute loads no longer isolate vision or radar; centralized domain controllers now perform heterogeneous sensor fusion and decision loops within 50 ms latency. Qualcomm’s Snapdragon Ride blends logic fabric, AI accelerators, and connectivity PHYs in one SoC, reflecting the convergence trend and enabling OEMs to shrink PCB real estate by up to 30%.

Infotainment and connectivity follow closely, driven by dual-screen cockpits and 5G telematics that expand memory bandwidth and necessitate multicore logic. Powertrain and battery management logic ICs are expanding rapidly in EV lineups, particularly as 800 V platforms proliferate beyond the luxury tier. Body electronics maintain a steady clip, yet feature creep-powered doors, ambient lighting, and HVAC zonal control still lift logic density per car. Safety and security logic segments command the highest ASIL grades and therefore sustain premium ASPs, cushioning revenue when unit volumes soften in cyclical markets.

By Vehicle Type: EVs elevate silicon value

Passenger cars retained a 47.85% share in 2025, driven by mainstream volume and incremental ADAS content. Electric vehicles rank as the volume underdog but the growth pacesetter, with a 3.95% CAGR, requiring every pack controller, thermal loop, and inverter to have isolation logic, an innovation unheard of in combustion platforms. Tesla’s in-house silicon epitomizes OEM verticalization, shrinking BOM variance while optimizing firmware cohesion. The automotive special-purpose logic IC market share, currently dominated by specialized EV subsystems, is projected to widen as Chinese brands leverage localized semiconductor ecosystems to reduce costs.

Light commercial vehicles are adopting ADAS and telematics more quickly than heavy trucks, benefiting from urban delivery electrification mandates. Heavy commercial vehicles demand ruggedized logic with 15-year lifespans, pushing suppliers to guarantee extended availability schedules, often at mature process nodes where reliability field data remain abundant.

By Packaging Technology: SiP compresses form factor

SiP led with 30.76% share in 2025, and its 3.74% CAGR underscores OEM appetite for footprint-constrained modules that meet AEC-Q100 without multiple component qualifications. Amkor’s latest automotive SiP cuts PCB area by half versus discrete assemblies and eases thermal routing in dense battery packs. The automotive special-purpose logic IC market size derived from SiP-centric designs will continue to rise as chiplet methodologies enable designers to mix critical IP blocks on known-good dies.

MCM approaches still dominate high-power traction inverters where heat dissipation rules out compact packages. Discrete packages linger in cost-pressured entry models and aftermarket retrofits, although even these segments are adopting higher pin-count QFN formats over older SOIC footprints.

Geography Analysis

Asia-Pacific generated 32.05% of global revenue in 2025 and is on track for a 3.46% CAGR through 2031, lifted by China’s production scale exceeding 30 million vehicles, aggressive EV subsidies, and an expanding domestic fabless ecosystem. Japan adds engineering heft through Renesas and Rohm, exporting logic ICs that anchor global supply chains. South Korea supplies backend capacity yet skews toward memory; nevertheless, Samsung’s automotive foundry services attract Western OEM design wins.

North America ranks second, buoyed by stringent Federal Motor Vehicle Safety Standards and consumer appetite for premium ADAS packages. The USMCA framework incentivizes localized semiconductor sourcing, and CHIPS Act subsidies funnel billions into 28 nm and 16 nm automotive capacity, though tangible wafer starts lag until the late-decade horizon. Tesla’s Austin Gigafactory drives demand for traction inverter logic and high-voltage gate drivers, which are sourced partly from domestic suppliers.

Europe remains a technology crucible led by Germany’s luxury brands. Tight CO₂ norms and the Green Deal are accelerating EV sales, thereby bolstering demand for battery-management logic ICs and high-efficiency power electronics. Supply resilience challenges surface as Brexit complicates cross-channel component flows; however, continental OEMs diversify wafer sources through joint ventures with STMicroelectronics, NXP, and GlobalFoundries to lock mature-node output.

Competitive Landscape

The market is moderately consolidated, with the top players leveraging decades-long OEM relationships and extensive AEC-Q portfolios. Infineon’s USD 3.2 billion acquisition of GaN Systems in October 2024 strengthens its high-voltage logic and power stack for 800V EV drives. NXP’s USD 2.8 billion capacity expansion in Texas and Arizona, announced in September 2024, secures domestic automotive wafer supply amid foundry tightness.

Renesas released its R-Car Gen4 SoC in August 2024, combining logic, AI acceleration, and network security on a single chip to support Level 3 autonomy compute loads. STMicroelectronics and CATL formed a joint venture in July 2024, targeting battery-management logic, which ensures captive demand from China’s dominant pack supplier. Nvidia, Qualcomm, and Intel intensify competitive pressure by converging traditional logic IC, GPU, and connectivity IP into unified automotive compute platforms, as evidenced by Qualcomm’s Snapdragon Ride Flex debut in June 2024. Patent filings for automotive logic ICs increased 40% year-over-year, signaling a crowded IP landscape where niche innovators can differentiate themselves through ASIL-B/C optimizations or ultra-low-leakage processes for battery management.

Automotive Special Purpose Logic IC Industry Leaders

-

Infineon Technologies AG

-

NXP Semiconductors N.V.

-

Renesas Electronics Corporation

-

STMicroelectronics N.V.

-

Texas Instruments Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Texas Instruments secured ISO 26262 ASIL-D certification across its logic IC design flow, opening avenues in safety-critical ADAS controllers.

- November 2024: ON Semiconductor launched EliteSiC M3e MOSFETs with embedded logic control for EV traction inverters.

- October 2024: Infineon closed the USD 3.2 billion GaN Systems purchase, integrating GaN logic and power IP under its Automotive High-Voltage Business Unit.

- September 2024: NXP committed USD 2.8 billion to expand 28 nm and 16 nm automotive wafer capacity in the United States.

Global Automotive Special Purpose Logic IC Market Report Scope

| Application-Specific Standard Products (ASSP) |

| Application-Specific Integrated Circuits (ASIC) |

| Field-Programmable Gate Arrays (FPGA) |

| Complex Programmable Logic Devices (CPLD) |

| Advanced Driver-Assistance Systems (ADAS) |

| Infotainment and Connectivity |

| Powertrain and Battery Management |

| Body Electronics and Comfort |

| Safety and Security Systems |

| Passenger Cars |

| Light Commercial Vehicles |

| Heavy Commercial Vehicles |

| Electric Vehicles (BEV, PHEV, FCEV) |

| System-in-Package (SiP) |

| Multi-Chip Module (MCM) |

| Discrete IC Package |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Logic IC Type | Application-Specific Standard Products (ASSP) | ||

| Application-Specific Integrated Circuits (ASIC) | |||

| Field-Programmable Gate Arrays (FPGA) | |||

| Complex Programmable Logic Devices (CPLD) | |||

| By Application | Advanced Driver-Assistance Systems (ADAS) | ||

| Infotainment and Connectivity | |||

| Powertrain and Battery Management | |||

| Body Electronics and Comfort | |||

| Safety and Security Systems | |||

| By Vehicle Type | Passenger Cars | ||

| Light Commercial Vehicles | |||

| Heavy Commercial Vehicles | |||

| Electric Vehicles (BEV, PHEV, FCEV) | |||

| By Packaging Technology | System-in-Package (SiP) | ||

| Multi-Chip Module (MCM) | |||

| Discrete IC Package | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the 2026 valuation for automotive special-purpose logic ICs?

The market is valued at USD 3.72 billion in 2026.

What compound annual growth rate is projected through 2031?

A 3.39% CAGR is forecast between 2026 and 2031.

Which end-use application is expanding fastest?

Advanced driver-assistance systems generate the strongest momentum, advancing at a 3.88% CAGR.

Why do automakers still favor ASIC-based solutions?

ASICs balance high-volume cost efficiency with functional-safety tailoring, making them a practical choice despite lower flexibility than FPGAs.

How does System-in-Package technology help vehicle electronics programs?

SiP consolidates multiple dies in one footprint, trimming board area by as much as 50% while meeting AEC-Q100 reliability targets.

Which geographic region shows the quickest demand expansion?

Asia-Pacific leads growth at a 3.46% CAGR thanks to China's electric-vehicle output and a robust local semiconductor supply chain.

Page last updated on: