Automotive Chip Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

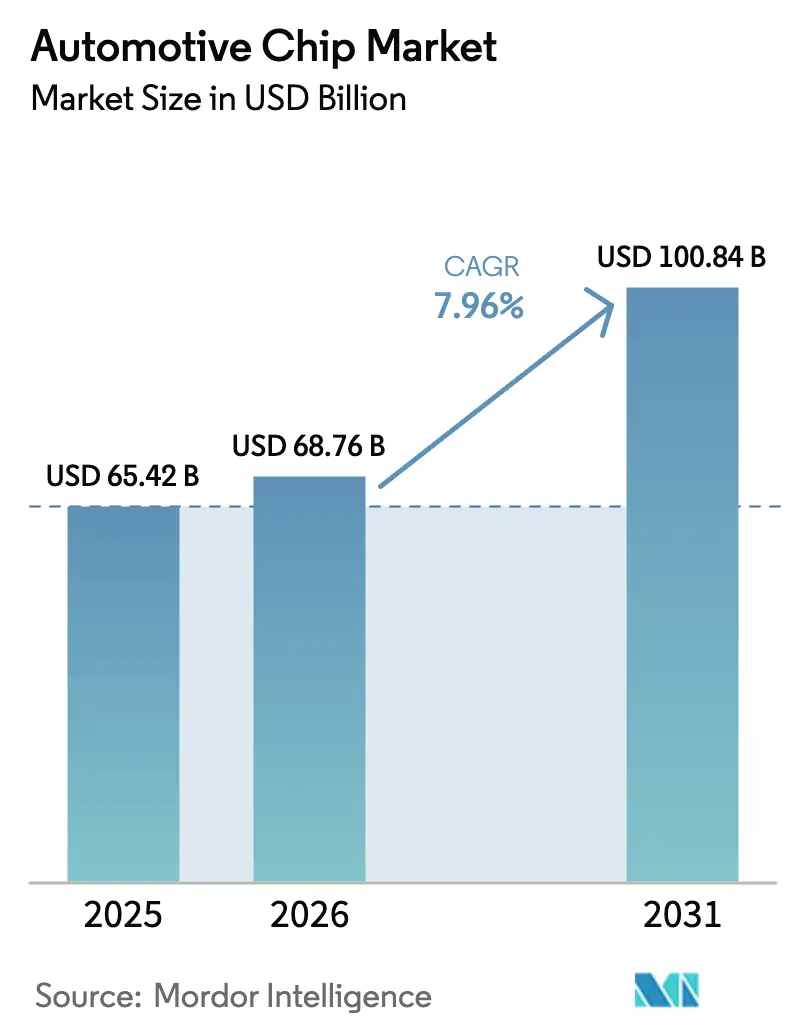

| Market Size (2026) | USD 68.76 Billion |

| Market Size (2031) | USD 100.84 Billion |

| Growth Rate (2026 - 2031) | 7.96% CAGR |

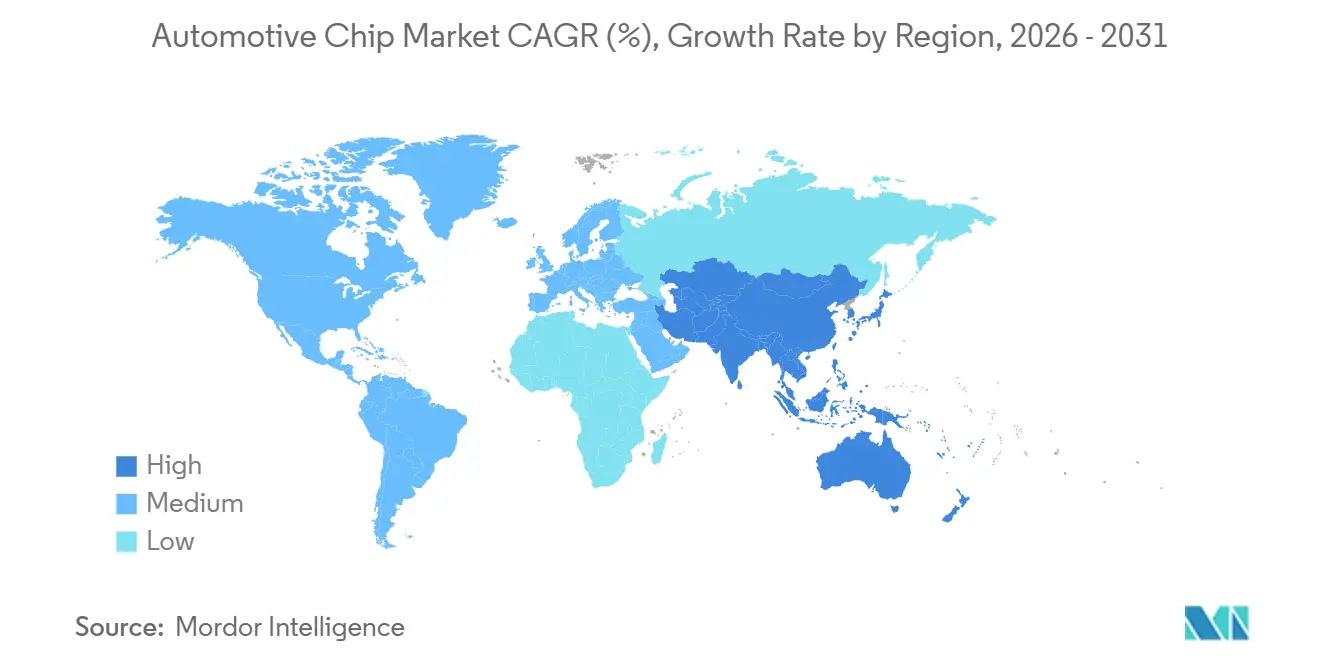

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive Chip Market Analysis by Mordor Intelligence

The automotive chip market size is expected to grow from USD 65.42 billion in 2025 to USD 68.76 billion in 2026 and is forecast to reach USD 100.84 billion by 2031 at 7.96% CAGR over 2026-2031. Software-defined vehicle programs, wide-bandgap power devices, and government incentives for domestic wafer capacity are lifting silicon demand across every vehicle domain. Microcontrollers remain indispensable for real-time safety functions, yet advanced-node system-on-chips are gaining share as zonal gateways replace dozens of legacy control units. Battery cost parity is accelerating battery-electric-vehicle (BEV) penetration, doubling the value of power discretes and sensors per car. Investment programs such as the United States CHIPS and Science Act and the European Chips Act underscore the strategic nature of automotive semiconductors. At the same time, chronic 28-45 nanometer line congestion is lengthening lead times, prompting tier-1 suppliers to pre-pay for capacity or vertically integrate power-device production.

Key Report Takeaways

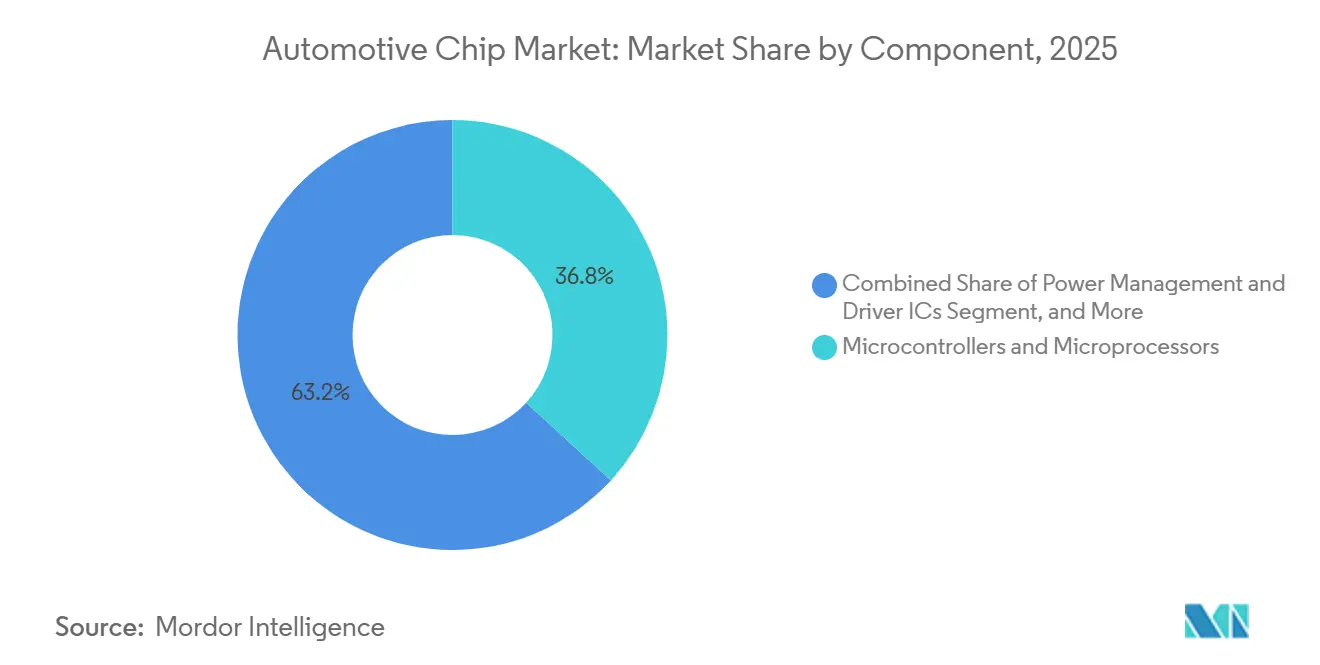

- By component, Microcontrollers and microprocessors owned 36.82% of 2025 revenue, the largest slice of the automotive chip market, rising at an 8.01% CAGR.

- By fabrication node, the 23-45 nanometer class held 44.57% in 2025, and nodes at or below 10 nanometers are forecast to expand at 7.99% CAGR on the back of 4 nm and 5 nm ADAS compute programs.

- By semiconductor material, silicon retained 75.92% in 2025, whereas gallium nitride is poised to post the fastest 8.09% CAGR as on-board-charger efficiencies climb.

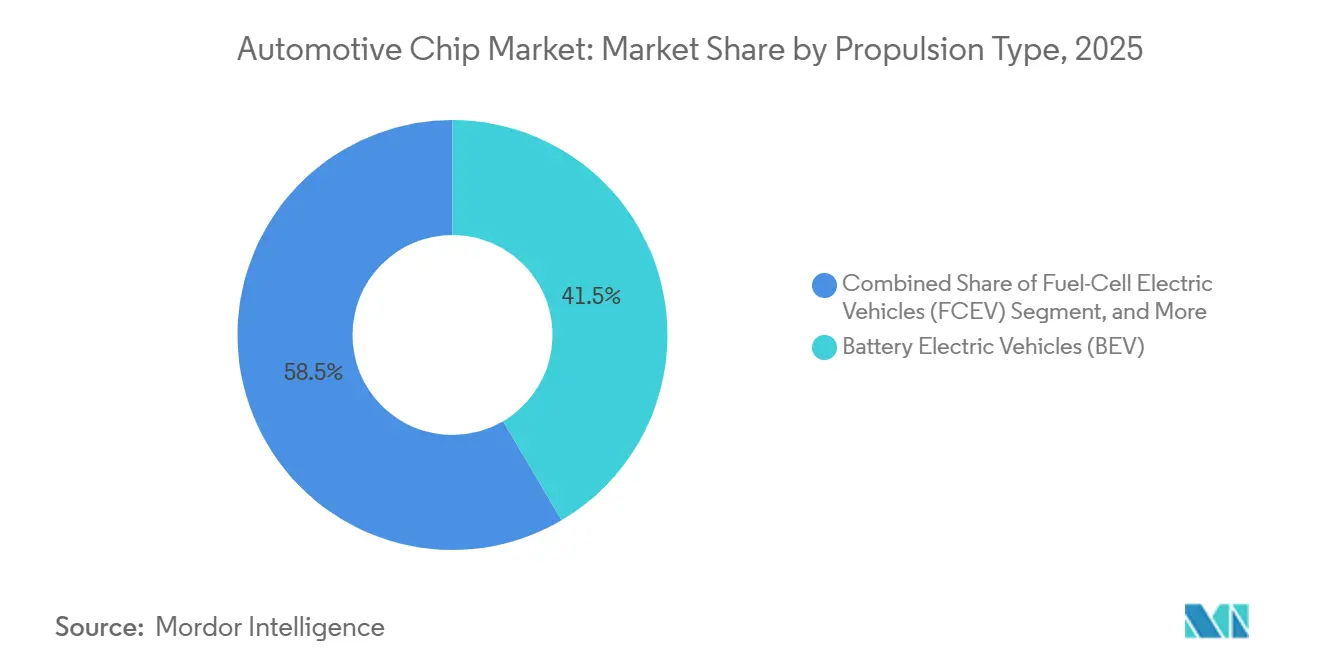

- By propulsion type, BEVs captured 41.53% in 2025, and the segment is anticipated to increase at an 8.17% CAGR through 2031 on the strength of 800-volt platforms.

- By vehicle class, passenger cars commanded 60.48% in 2025 and are expected to grow at an 8.33% CAGR as Level 3 functions migrate into mid-segment models.

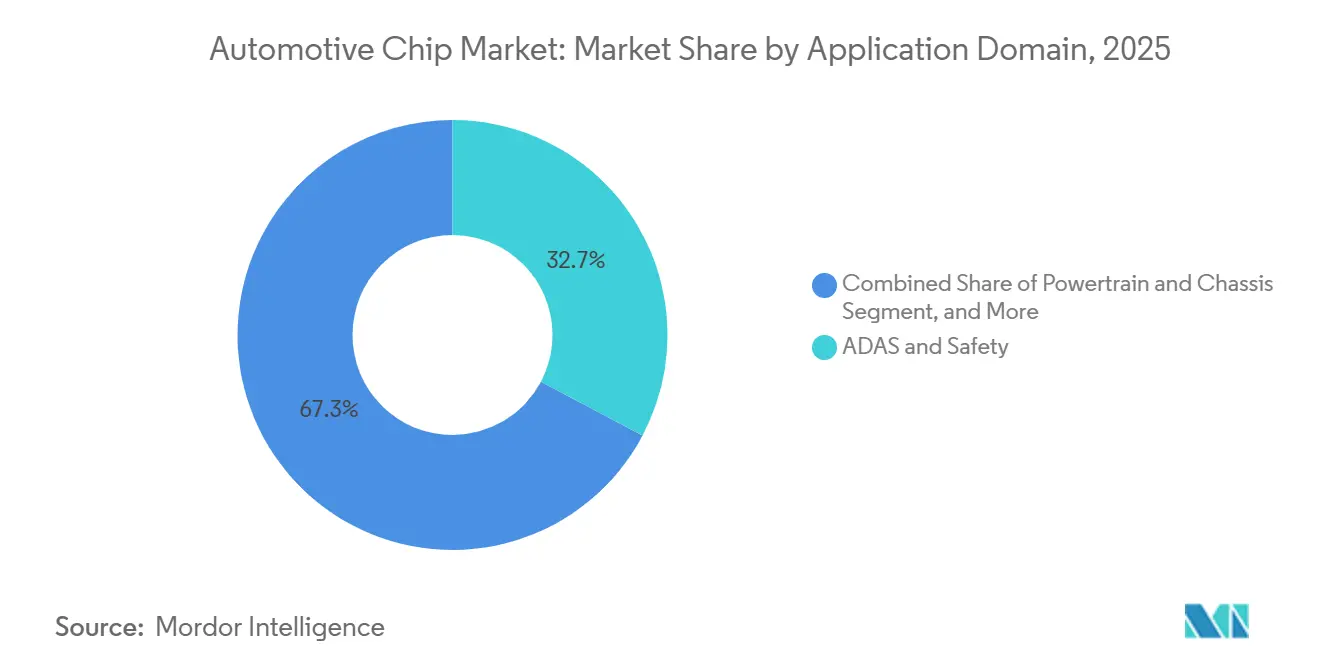

- By application domain, ADAS and safety held 32.74% in 2025, while the same domain records the highest projected 8.28% CAGR as UN Regulation 157 broadens scope.

- By end-market, OEM-installed electronics represented 81.63% in 2025, and aftermarket retro-fits will see an 8.05% CAGR as fleets upgrade older assets.

- By geography, Asia-Pacific led with 40.61% in 2025 and is forecast to grow at the quickest 8.41% CAGR, supported by China’s New-Energy-Vehicle roadmap.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Automotive Chip Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Transition to Software-Defined and Zonal E-Architectures | +1.8% | Global, with early adoption in Germany, US, China | Medium term (2-4 years) |

| Rapid Adoption of SiC and GaN Power Devices in High-Voltage EV Platforms | +1.5% | APAC core, spill-over to North America and Europe | Medium term (2-4 years) |

| OEM Push for 4-Nm / 5-Nm Automotive SoCs Enabling L3+ ADAS | +1.3% | North America, Europe, Japan, South Korea | Long term (≥ 4 years) |

| Government-Mandated Cyber-Security and OTA Standards (UNECE R155/R156) Raising Silicon Content | +1.1% | Europe, North America, with gradual adoption in APAC | Short term (≤ 2 years) |

| Battery Cost Parity Accelerating BEV Penetration | +1.4% | Global, strongest in China, Europe, North America | Short term (≤ 2 years) |

| Chiplet-Based Modular Designs Shortening Tier-1 Time-To-Market | +0.9% | Japan, US, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Transition to Software-Defined and Zonal E-Architectures

Automakers are collapsing as many as 150 control units into a handful of zonal gateways that run containerized software on multi-core processors. Consolidation raises silicon content per car by up to 30% because zonal controllers require fault-tolerant CPUs, time-sensitive-networking switches, and secure power-management ICs. BMW’s Neue Klasse platform will deploy centralized chips that cut wiring mass by 40% and trim integration cost. Volkswagen’s co-operation with Horizon Robotics proves OEMs will share intellectual property if it shortens release cycles. Ethernet PHYs capable of 10 Gbps have emerged as critical enablers because sensor fusion demands sub-millisecond latency.[1]Texas Instruments, “DP83TD510E Single-Pair Ethernet PHY,” Texas Instruments, ti.com

Rapid Adoption of SiC and GaN Power Devices in High-Voltage EV Platforms

Silicon-carbide and gallium-nitride components support 800-volt battery packs that add up to 350 kW fast charging without thermal drift, shrinking charge times below 15 minutes for 80% state-of-charge. onsemi’s EliteSiC M3e module withstands 200 °C junction temperatures, letting automakers scale back inverter coolers by a quarter and remove USD 50 of material per vehicle.[2]onsemi, “EliteSiC M3e Power Module,” onsemi, onsemi.com Volkswagen’s five-year volume guarantee for silicon-carbide parts underlines the strategic value assigned to wide-bandgap devices. Joint gallium-nitride R&D between GlobalFoundries and onsemi on 300 mm wafers aims to halve costs by 2027.[3]GlobalFoundries, “GlobalFoundries and onsemi Collaborate to Advance Gallium Nitride Technology,” GlobalFoundries, gf.com

OEM Push for 4 nm / 5 nm Automotive SoCs Enabling Level 3 plus ADAS

Level 3 highway pilots need 300 TOPS of inference inside 60 W envelopes. Mobileye’s EyeQ6 Lite, taped out at 5 nm, supplies 34 TOPS at 24 W, a 40% efficiency leap and now priced at USD 180 for mid-segment sedans. Renesas is sampling 3 nm devices for Honda’s 2027 launch, pairing Cortex-A720 clusters with dedicated neural engines. Although advanced nodes raise non-recurring costs above USD 500 million, suppliers gain 18 months of exclusive design windows once ISO 26262 ASIL-D approval is completed. Foundries answer reliability concerns by adding redundant metallization and ECC memory structures.

Government-Mandated Cyber-Security and OTA Standards Raising Silicon Content

UN Regulation 155 obligates hardware-anchored secure boot and life-long key management, adding USD 5–15 per electronic unit. Regulation 156 extends oversight to over-the-air update logging, favoring centralized compute layouts that simplify audit trails. NXP’s S32G3 integrates hardware crypto that authenticates firmware in under 100 ms, allowing monthly patch cycles without delaying ignition. Forthcoming post-quantum recommendations by the European Union Agency for Cybersecurity will drive demand for lattice-based accelerators by 2028.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic 28-45 Nm Foundry Capacity Bottlenecks Despite New Fabs | -1.2% | Global, most acute in North America and Europe | Medium term (2-4 years) |

| Functional-Safety (ISO 26262 / ASIL-D) Certification Costs Burdening Mid-Tier Suppliers | -0.8% | Global, particularly impacting smaller suppliers in APAC | Long term (≥ 4 years) |

| Limited Thermal-Management Headroom in 3-D Packaging For In-Cabin Domains | -0.5% | Global, with higher impact in premium vehicle segments | Long term (≥ 4 years) |

| Export-Control Restrictions On EDA / IP for Chinese OEMs | -0.7% | China, with secondary effects in APAC | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic 28-45 nm Foundry Capacity Bottlenecks Despite New Fabs

Automotive microcontrollers lean on mature 28-45 nm platforms where analog and embedded-flash blocks are field-proven. Global foundry utilization ran above 95% all through 2025, sending lead times beyond forty weeks and inflating prices by double digits. New United States and German fabs will add capacity only after 2027, and qualification means automotive volumes will be felt closer to 2030. Tier-1 suppliers have responded with take-or-pay contracts, exchanging flexibility for guaranteed wafers.

Functional-Safety Certification Costs Burdening Mid-Tier Suppliers

ISO 26262 ASIL-D demands exhaustive fault-injection and process audits, costing USD 20–50 million and delaying tape-out by up to two years. Smaller fabless firms now license pre-certified IP blocks to cut expenses but forfeit architectural uniqueness, compressing margins by as much as eight percentage points. Neural-network accelerators amplify the headache because traditional deterministic testing is insufficient, and SOTIF verification layers add further cost.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Microcontrollers Anchor Legacy Domains While Sensors Surge

Microcontrollers and microprocessors owned 36.82% of 2025 revenue, the largest slice of the automotive chip market, as engine, chassis, and body controllers continue to rely on low-latency deterministic logic. Sensors, however, represent the fastest lane, rising at an 8.01% CAGR; radar, camera, and LiDAR arrays are now mandatory in Europe, North America, and Japan for automatic emergency braking systems. The automotive chip market size tied to sensors is expected to double by 2031 as Level 3 plus functionality reaches compact cars. Power-management ICs scale in parity with BEV inverters, while discrete devices such as IGBTs or MOSFETs keep a 15–18% foothold. Memory remains a resilient niche, benefiting from growing over-the-air map downloads and infotainment caching.

OEMs rely on tight software integration between microcontrollers and security modules, ensuring ISO 26262 compliance without oversizing the silicon. Meanwhile, system suppliers are packaging radar transceivers and microprocessors inside single mold-compounds, cutting printed-circuit-board area by 30%. The convergence blurs component boundaries, drawing new competition from consumer-electronics sensor vendors. As vehicles migrate to zonal architectures, mixed-signal microcontrollers with safety-islands and gigabit Ethernet MACs are expected to replace older 16-bit units, improving functional headroom for future software features.

By Fabrication Node: Legacy Lines Still Dominate, Advanced Nodes Accelerate

The 23-45 nanometer class accounted for 44.57% of 2025 shipments, the single-largest automotive chip market share because embedded-flash libraries, analog IP and ISO 26262 tool flows are mature at these geometries. Nodes at or below 10 nanometers are projected to expand at a 7.99% CAGR through 2031 as centralized compute domains need 200 TOPS of AI inference inside 50 W envelopes. This migration raises the automotive chip market size tied to advanced processes despite non-recurring engineering expenses that now top USD 500 million per design. Tier-1 suppliers accept the higher cost because a single 5 nanometer system-on-chip can replace up to ten 40 nanometer microcontrollers, trimming bill-of-materials and wiring harness length.

Foundries answer safety demands by adding redundant metallization, ECC SRAM and extra scribe-line monitors so that first-pass automotive qualification completes inside 24 months. Qualcomm and Mobileye already tape out 4 nanometer and 5 nanometer parts, winning design slots once reserved for integrated-device makers that own legacy fabs. To hedge supply risk, automakers sign capacity agreements that guarantee wafer starts but require multi-year volume commitments. Mature 90 nanometer and larger nodes remain viable for power discretes and high-voltage analog, yet the value pool is shifting to logic-dense products where software-defined features can be unlocked over the air.

By Semiconductor Material: Silicon Leads, Wide-Bandgap Devices Surge

Silicon delivered 75.92% of 2025 revenue because no other substrate matches its cost per transistor across microcontrollers, memory and network ICs. Gallium nitride is forecast to grow at an 8.09% CAGR as on-board chargers move to 98% efficiency and shrink passive components by Silicon-carbide already commands 12-14% of the automotive chip market size and is entrenched in 800-volt traction inverters that cut conduction losses 30% versus silicon IGBTs.

Vertical integration is changing price curves; onsemi’s long-term wafer deal with Wolfspeed secures raw silicon-carbide through 2027, while its collaboration with GlobalFoundries aims to halve gallium-nitride costs on 300 mm by 2027. Cost parity with silicon for 400-volt hybrids could arrive within five years, widening adoption beyond premium BEVs. Gallium-arsenide and indium-phosphide occupy radar and LiDAR niches but together stay below 3% share. As OEMs chase efficiency gains, wide-bandgap substrates are expected to lift the overall automotive chip market share of power devices even if silicon continues to rule logic and memory.

By Propulsion Type: BEVs Drive Dollar Content, Hybrids Bridge the Gap

Battery electric vehicles held a 41.53% slice of 2025 revenue and are set to grow at 8.17% through 2031, the fastest stride among propulsion categories. Each BEV embeds USD 1,200 worth of semiconductors, roughly 2.5 times the figure for an internal-combustion model, because inverters, on-board chargers and battery-management systems demand hundreds of power discretes and scores of microcontrollers.

Hybrids and plug-in hybrids kept 22-25% share in 2025, serving markets where charging coverage lags yet fuel-economy rules tighten. Internal-combustion powertrains still claim near one-third of units but face step-wise declines as charging networks scale. Fuel-cell vehicles remain sub-1% amid hydrogen-infrastructure gaps. The mix shift enlarges the automotive chip market size by elevating the average silicon bill per vehicle even where total vehicle demand stays flat. Suppliers that dominate wide-bandgap power modules and battery-monitoring ICs are best placed to capitalize on the propulsion transition.

By Vehicle Class: Passenger Cars Command Volume, Commercial Fleets Catch Up

Passenger cars generated 60.48% of 2025 revenue and are projected to expand at an 8.33% CAGR as Level 3 automated driving becomes a mainstream feature. Mid-segment sedans now integrate five to seven cameras, three radars and a driver-monitoring sensor, lifting silicon spend per unit toward USD 900. Light commercial vehicles represented roughly one-quarter of the automotive chip market share, buoyed by e-commerce delivery demand that values real-time telematics and collision-avoidance systems

Heavy trucks and buses captured about 11% in 2025 but will accelerate as platooning and automated-dock features roll out on electrified chassis. Regulatory influence is acute in Europe, where General Safety Regulation mandates automatic emergency braking and lane-keeping on all new passenger cars from 2024. As fleets digitize, the automotive chip market size linked to connectivity gateways and smart-tachographs in commercial classes will outpace unit growth. Startups that tailor ADAS stacks to high-gross-weight vehicles could seize early share because incumbents prioritize passenger platforms.

By Application Domain: ADAS Leads, Powertrain Holds Strategic Weight

Advanced driver assistance and safety systems claimed 32.74% of 2025 sales and carry the highest 8.28% CAGR to 2031, nudged by UN Regulation 157 making automated lane-keeping compulsory on new types in Europe and Japan. A single Level 2-plus stack now blends up to 12 cameras, five radars and two LiDAR units, generating data streams that need 100-300 TOPS of inference.

Powertrain and chassis stayed near 29% share in 2025 and will remain critical because electrification multiplies the need for high-current gate drivers and real-time torque control. Telematics and infotainment account for almost one-fifth of the automotive chip market size as consumers demand always-connected cabins. Body and convenience electronics plus battery-management systems round out the balance, but each benefits when OEMs pivot to zonal controllers that host multiple software domains on one processor. The blurring of boundaries means future tenders will bundle ADAS, infotainment and connectivity onto a single SoC—reshaping vendor selection criteria around software ecosystems rather than discrete hardware specs.

By End-Market: OEM-Installed Dominates, Aftermarket Retro-Fit Gains Momentum

OEM-installed electronics accounted for 81.63% of the automotive chip market share in 2025, anchoring the largest slice of industry revenue as automakers integrated factory-fit microcontrollers, sensors, and power devices that satisfy warranty and homologation rules. The segment keeps the automotive chip market size tightly aligned with original-equipment model cycles, so every new vehicle generation immediately lifts silicon demand. From 2026 to 2031, the OEM lane is forecast to expand just below the headline pace because silicon content per vehicle climbs even when global unit production plateaus. In contrast, aftermarket retro-fit solutions are projected to post an 8.05% CAGR as fleet operators digitize existing assets to meet insurance and regulatory safety thresholds.

Each retrofit ADAS kit adds USD 200–400 of semiconductors, including radar sensors, image processors, and gateway microcontrollers that tap the vehicle’s CAN-FD network. A pending European proposal to mandate intelligent speed assistance on commercial fleets older than five years could unlock 15 million retrofit candidates per year, representing more than USD 3 billion in additional semiconductor revenue by 2030. North American insurers already grant double-digit premium discounts for telematics-enabled trucks, stoking demand for aftermarket gateways with over-the-air update capability. Integration complexity remains the main hurdle because installers must decode proprietary CAN messages without factory tools, favoring tier-1 suppliers with multi-brand vehicle access. Vendors that bundle pre-certified sensor modules with plug-and-play software stand to capture early share as fleets chase quick compliance benefits while deferring full vehicle replacement.

Geography Analysis

Asia-Pacific generated 40.61% of global revenue in 2025 and is anticipated to deliver the quickest 8.41% CAGR to 2031, underscored by China’s requirement that one in two new cars be electric or plug-in hybrid by 2035. Domestic makers such as BYD and NIO are integrating home-grown microcontrollers to sidestep export controls, a shift that lifts regional dollar content. Japan and South Korea nurture chiplet research consortia that match best-in-class CPU tiles with local high-bandwidth memory, positioning the bloc to capture next-generation centralized compute sockets. India trails on per-vehicle silicon spend, yet a USD 9.1 billion electronics incentive could lift national assembly capacity twofold by 2028.

North America and Europe combined for roughly 46% of 2025 sales, supported by the USD 52.7 billion United States CHIPS program and EUR 43 billion European Chips Act. U.S. automakers favor domestically sourced microcontrollers to de-risk supply lines after 2021 shortages, and Intel’s Arizona investment adds frontline logic capacity from 2027. Europe keeps the world’s highest semiconductor spend per car, averaging USD 650, because regulatory timetables accelerate BEV and ADAS deployment. Infineon’s Dresden expansion and STMicroelectronics’ Catania silicon-carbide push solidify the bloc’s power-device leadership.

The Middle East and Africa plus South America share the remaining 13%, yet both regions show library pockets of growth. Saudi Arabia’s public-private EV investments pull demand for high-current gallium-nitride chargers, while Brazil’s Rota 2030 fuel-efficiency target adds microcontroller value to flex-fuel drivetrains. Localized assembly is limited, so most chips continue to be imported from Asian foundries, keeping logistics overhead high.

Competitive Landscape

The top ten suppliers captured an estimated 62% of 2025 revenue, yielding a moderate concentration profile. Integrated-device manufacturers such as STMicroelectronics, Infineon, NXP, Renesas, Texas Instruments, and onsemi defend microcontroller and power-discrete incumbency by booking long-term wafer output and embedding proprietary analog intellectual property that fabless rivals struggle to match. Fabless challengers—Qualcomm, Mobileye, and Horizon Robotics—capitalize on access to 4 nm and 5 nm capacity at TSMC and Samsung Foundry, achieving 200–300 TOPS per 50 W while skipping the fixed cost of captive fabs.

Strategic moves center on vertical control of wide-bandgap substrates. onsemi locked in silicon-carbide wafer feedstock through a multi-year Wolfspeed contract, while GlobalFoundries allied with onsemi to migrate gallium-nitride to 300 mm, halving cost by 2027. Infineon secured EUR 1 billion German subsidies to double Dresden power-discrete lines, ensuring captive capacity for 28-45 nm microcontrollers. Patent intensity is climbing: onsemi, Infineon, and Wolfspeed together hold more than half of silicon-carbide MOSFET filings dated 2023-2025, raising licensing barriers for late entrants.

Emerging disruptors in China price ADAS SoCs 25% below Western norms but face tool-chain embargoes. Startups in Europe now target Ethernet switches and lidar photonics fields left open by larger players focusing on AI accelerators. Chiplet ecosystems would let tier-1s blend CPU, GPU, and memory tiles from multiple vendors, trimming non-recurring engineering cost by 35% and compressing design cycles to 18 months, yet thermal stacking remains an unsolved engineering puzzle.

Automotive Chip Industry Leaders

Infineon Technologies AG

NXP Semiconductors N.V.

Renesas Electronics Corp.

STMicroelectronics N.V.

Texas Instruments Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: GlobalFoundries and onsemi finalized process design kits for vertical gallium-nitride transistors, marking the first automotive-grade 300 mm GaN flow ready for customer qualification.

- December 2025: GlobalFoundries and onsemi announced a collaboration to commercialize vertical gallium-nitride technology, targeting 98% efficiency chargers by 2027.

- October 2025: onsemi unveiled its vertical GaN roadmap promising 98% converter efficiency and a 15-20% share of the wide-bandgap segment by 2027.

- September 2025: Qualcomm and BMW confirmed Snapdragon Ride Flex will power Neue Klasse zonal compute from 2027, collapsing 150 ECUs into three gateways.

Global Automotive Chip Market Report Scope

Automotive chips are specialized integrated circuits tailored for vehicles. These chips are integral to modern automobiles, managing engine control, safety features, and infotainment systems. They oversee critical functions, including fuel injection, anti-lock braking (ABS), airbag deployment, navigation, and entertainment. With technological advancements, these chips have evolved, now supporting features like autonomous driving, enhanced connectivity, and advanced safety measures. The study tracks the revenue generated from selling several components utilized for several applications in automotive manufacturing. It also tracks the growing market trends and macroeconomic factors impacting the market.

The Automotive Semiconductor Market Report is Segmented by Component (Microcontrollers and Microprocessors, Power Management and Driver ICs, Discrete Power Devices, Sensors, Memory, Connectivity and Network ICs, Other Components), Fabrication Node (≤10 nm, 11-22 nm, 23-45 nm, >45 nm), Semiconductor Material (Silicon, Silicon Carbide, Gallium Nitride, Other Materials), Propulsion Type (ICE, HEV/PHEV, BEV, FCEV), Vehicle Class (Passenger Cars, LCV, HCV and Buses), Application Domain (Powertrain and Chassis, ADAS and Safety, Body Comfort and Convenience, Telematics Infotainment and Connectivity, BMS), End-Market (OEM-Installed, Aftermarket Retro-Fit), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, Africa). Market Forecasts are Provided in Terms of Value (USD).

| Microcontrollers and Microprocessors |

| Power Management and Driver ICs |

| Discrete Power Devices (IGBT, MOSFET, SiC, GaN) |

| Sensors (Image, LiDAR, Radar, MEMS) |

| Memory (DRAM, NAND, NOR) |

| Connectivity and Network ICs (Ethernet, CAN-FD, LIN, FlexRay) |

| Other Components |

| ≤ 10 nm |

| 11 – 22 nm |

| 23 – 45 nm |

| > 45 nm |

| Silicon (Si) |

| Silicon Carbide (SiC) |

| Gallium Nitride (GaN) |

| Other Semiconductor Materials |

| Internal Combustion Engine (ICE) Vehicles |

| Hybrid and Plug-in Hybrid Electric Vehicles (HEV / PHEV) |

| Battery Electric Vehicles (BEV) |

| Fuel-Cell Electric Vehicles (FCEV) |

| Passenger Cars |

| Light Commercial Vehicles (LCV) |

| Heavy Commercial Vehicles (HCV and Buses) |

| Powertrain and Chassis |

| Advanced Driver Assistance and Safety |

| Body, Comfort and Convenience |

| Telematics, Infotainment and Connectivity |

| Battery Management Systems (BMS) |

| OEM-Installed (Factory-Fit) |

| Aftermarket Retro-Fit |

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia Pacific | China |

| Japan | |

| South Korea | |

| India | |

| Rest of Asia Pacific | |

| Middle East | Saudi Arabia |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa |

| By Component | Microcontrollers and Microprocessors | |

| Power Management and Driver ICs | ||

| Discrete Power Devices (IGBT, MOSFET, SiC, GaN) | ||

| Sensors (Image, LiDAR, Radar, MEMS) | ||

| Memory (DRAM, NAND, NOR) | ||

| Connectivity and Network ICs (Ethernet, CAN-FD, LIN, FlexRay) | ||

| Other Components | ||

| By Fabrication Node | ≤ 10 nm | |

| 11 – 22 nm | ||

| 23 – 45 nm | ||

| > 45 nm | ||

| By Semiconductor Material | Silicon (Si) | |

| Silicon Carbide (SiC) | ||

| Gallium Nitride (GaN) | ||

| Other Semiconductor Materials | ||

| By Propulsion Type | Internal Combustion Engine (ICE) Vehicles | |

| Hybrid and Plug-in Hybrid Electric Vehicles (HEV / PHEV) | ||

| Battery Electric Vehicles (BEV) | ||

| Fuel-Cell Electric Vehicles (FCEV) | ||

| By Vehicle Class | Passenger Cars | |

| Light Commercial Vehicles (LCV) | ||

| Heavy Commercial Vehicles (HCV and Buses) | ||

| By Application Domain | Powertrain and Chassis | |

| Advanced Driver Assistance and Safety | ||

| Body, Comfort and Convenience | ||

| Telematics, Infotainment and Connectivity | ||

| Battery Management Systems (BMS) | ||

| By End-Market | OEM-Installed (Factory-Fit) | |

| Aftermarket Retro-Fit | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| South Korea | ||

| India | ||

| Rest of Asia Pacific | ||

| Middle East | Saudi Arabia | |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

Key Questions Answered in the Report

What is the forecast value of the automotive chip market by 2031?

The automotive chip market is projected to reach USD 100.84 billion by 2031.

Which regional block will contribute the fastest growth through 2031?

Asia-Pacific is expected to post the quickest 8.41% CAGR as China, Japan, and South Korea scale EV mandates.

Why are wide-bandgap devices gaining traction in electric vehicles?

Silicon-carbide and gallium-nitride parts cut inverter losses and enable 350 kW fast-charging, boosting range and shortening charge times.

How will zonal architectures affect semiconductor demand per car?

Consolidating dozens of ECUs into a handful of gateways raises silicon content by 20–30% and drives adoption of multi-core processors with hardware security modules.

What challenge do mid-tier suppliers face with functional safety?

ISO 26262 ASIL-D certification can cost USD 20–50 million and add up to two years to development, pressuring margins for smaller vendors.

Which fabrication node class still suffers from capacity shortages?

The mature 28-45 nm range remains tight, with lead times often exceeding 40 weeks despite newfab announcements.

Page last updated on: