Automotive MCU Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

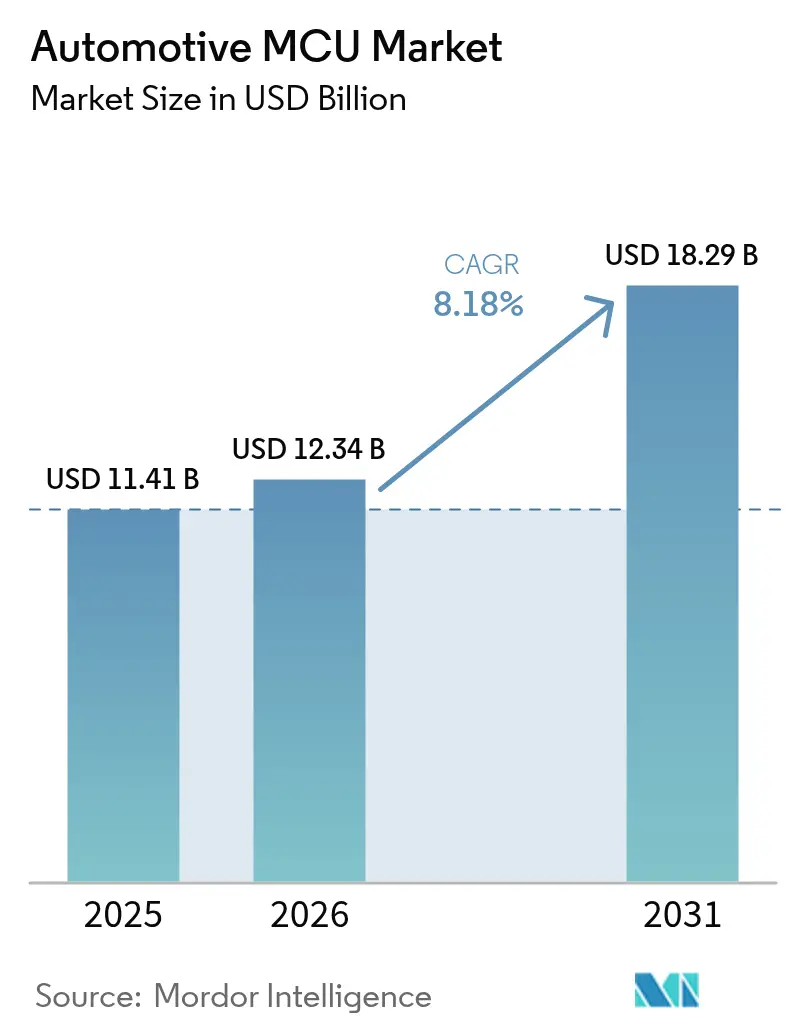

| Market Size (2026) | USD 12.34 Billion |

| Market Size (2031) | USD 18.29 Billion |

| Growth Rate (2026 - 2031) | 8.18% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

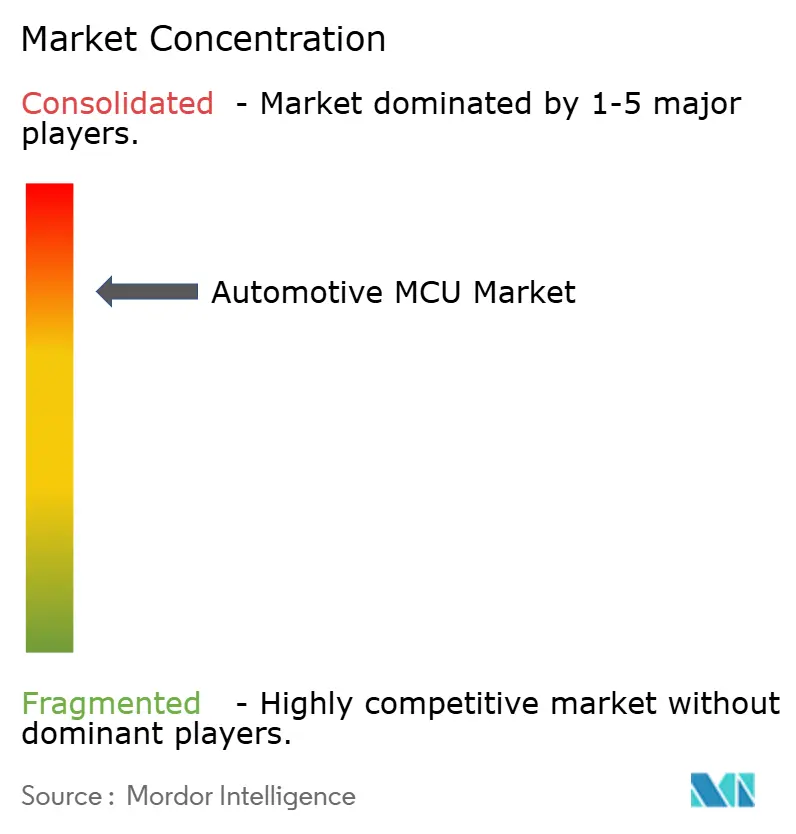

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automotive MCU Market Analysis by Mordor Intelligence

The automotive MCU market size was valued at USD 11.41 billion in 2025 and estimated to grow from USD 12.34 billion in 2026 to reach USD 18.29 billion by 2031, at a CAGR of 8.18% during the forecast period (2026-2031). Rising electric-vehicle (EV) penetration, the migration to zonal electronic/electrical (E/E) architectures, and tighter cybersecurity rules are the primary forces expanding automotive microcontroller content per vehicle. Modern platforms integrate more than 100 controllers versus fewer than 10 in legacy models. Higher-performance 32-bit devices, advanced ≤16 nm FinFET process technologies, and Cortex-R/A-class real-time cores lead the shift to software-defined vehicles and over-the-air (OTA) upgrades that demand low-latency, deterministic processing. Competitive activity centers on RISC-V adoption, security-hardened designs, and geographic supply-chain diversification to satisfy localization requirements and mitigate geopolitical risk. These trends collectively keep the automotive MCU market on a strong growth trajectory through the decade.

Key Report Takeaways

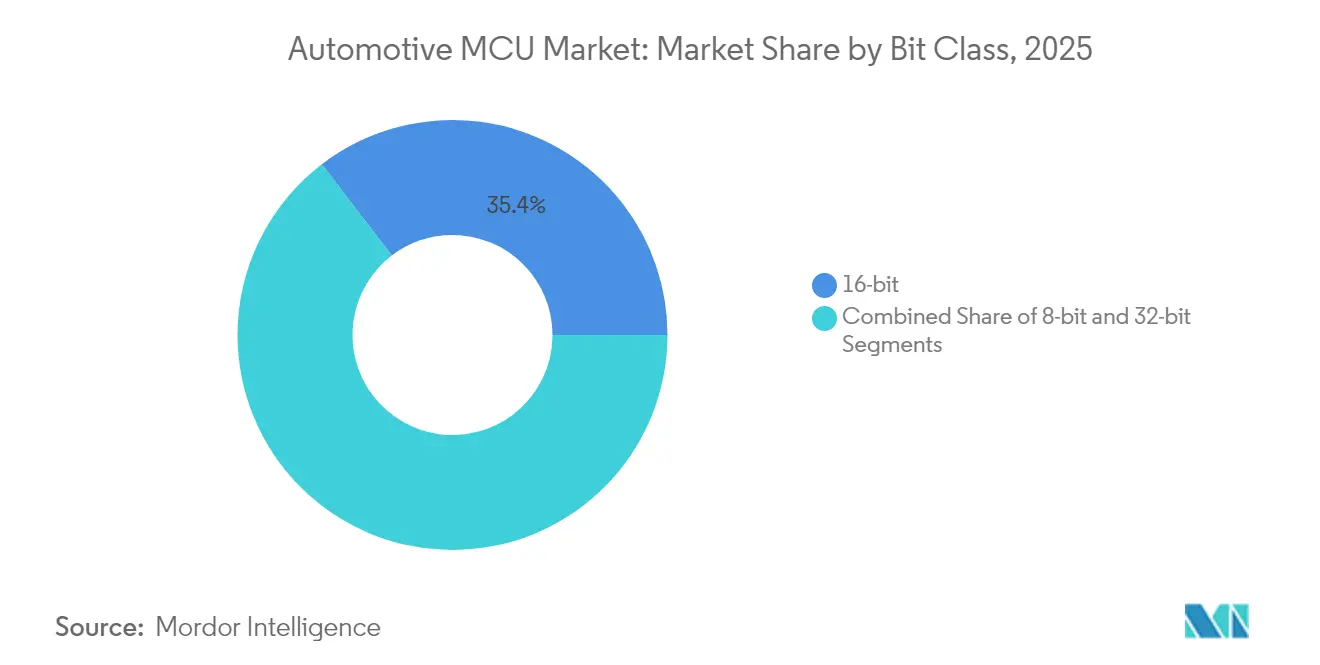

- By bit class, 32-bit devices lead expansion with an 11.2% CAGR through 2031, while 16-bit controllers retained a 35.40% revenue share of the automotive MCU market in 2025.

- By application, safety and ADAS captured 13.6% CAGR, the fastest among segments; powertrain and chassis held 25.60% of the automotive MCU market share in 2025.

- By vehicle propulsion, battery electric vehicles contributed the quickest rise at 13.10% CAGR; commercial ICE maintained a 27.80% slice of the automotive MCU market size in 2025.

- By process node, ≤16 nm FinFET devices posted a 11.9% CAGR, whereas 40-22 nm nodes commanded a 22.10% revenue share in 2025.

- By core architecture, ARM Cortex-R/A solutions accelerated at 15.0% CAGR; RISC-V held 8.35% of 2025 revenue but is growing swiftly.

- Regionally, Asia-Pacific shows the highest 13.2% CAGR, yet North America held a 18.80% share in 2025.

- The five largest suppliers controlled 81.5% of global revenue; Infineon led with 28.5%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Automotive MCU Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Electrification and xEV penetration surge | 2.10% | Global, with APAC and EU leading adoption | Medium term (2-4 years) |

| Growing ADAS and autonomous feature content | 1.80% | North America and EU regulatory push, APAC volume growth | Long term (≥ 4 years) |

| Software-defined vehicle and OTA architecture | 1.40% | Global, with early adoption in premium segments | Long term (≥ 4 years) |

| Cyber-security regulation-driven refresh cycles | 0.90% | EU and North America compliance-driven | Short term (≤ 2 years) |

| Zonal E/E architecture transition | 1.20% | Global, led by European OEMs | Medium term (2-4 years) |

| Localization incentives (CHIPS Acts, etc.) | 0.80% | National, with focus on US, EU, and China | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Electrification and xEV Penetration Surge

Battery-electric cars need more than 300 controllers compared with 70 in ICE vehicles, quadrupling MCU unit demand. Thermal loads in 800 V traction systems drive designs rated for junctions beyond 150°C. NXP’s S32K39/37 controls six-phase motors at >200 kHz, illustrating the high-speed loops required. Moving to 48 V zonal backbones trims wiring mass by 85% and frees power budget for heating, ventilation, and battery-conditioning loops.

Growing ADAS and Autonomous Feature Content

Level 2 platforms already embed about USD 500 in semiconductors, an order of magnitude above basic vehicles. Progression to Level 4 autonomy mandates sensor-fusion, redundancy, and ASIL-D conformance. Texas Instruments’ AWRL6844 radar integrates edge AI in its MCU, processing in-cabin child-presence data in real time. Consolidating perception and control code on single MCUs accelerates the pivot from distributed to centralized compute.[2]European Commission, “Industrial Action Plan for the Automotive Sector,” ec.europa.eu

Software-Defined Vehicle and OTA Architecture

Frequent software updates favour embedded MRAM and fast erase/write cycles. NXP’s 16 nm S32K5 family writes firmware 15 × faster than flash while meeting ASIL-D targets. Zonal controllers manage multiple subsystems, reducing ECU count. Infineon and Flex demonstrated a modular zone platform that bundles Ethernet acceleration and AI inference for real-time adaptation.

Cyber-Security Regulation-Driven Refresh Cycles

UN R155 and ISO/SAE 21434 require certified cyber-security management from July 2024 onward. Hardware security modules and secure-boot roots now ship standard. Automotive cyber incidents generated USD 22.5 billion impact in 2024, reinforcing demand for trusted-execution MCUs. EU mandates add blockchain-based authentication, increasing hardware refresh frequency.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy functional-safety qualification cycles | -1.30% | Global, with stricter EU requirements | Long term (≥ 4 years) |

| Persistent 150mm foundry capacity bottlenecks | -0.80% | Global, with Asia-Pacific manufacturing concentration | Medium term (2-4 years) |

| Junction-temperature derating issues >150°C | -0.60% | Global, particularly in EV applications | Medium term (2-4 years) |

| Rising ISO 26262/21434 compliance costs | -0.90% | EU and North America primarily | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Lengthy Functional-Safety Qualification Cycles

Achieving ASIL-D certification stretches 18-24 months, delaying innovation. Mixed-critical workloads need hardware partitioning and formal proofs, inflating cost and schedule risk.

Persistent 150 mm Foundry Capacity Bottlenecks

More than 75% of automotive controllers still run on ≥28 nm nodes. Mature-node expansion is limited to roughly 7% in 2025, exposing OEMs to supply shocks and geopolitical exposure concentrated in Taiwan and South Korea fabs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Bit Class: Higher-End 32-Bit Solutions Take Share

The 16-bit segment maintained 35.40% revenue in 2025, mainly in body electronics. In contrast, 32-bit devices recorded an 11.2% CAGR, riding ADAS demand and software-defined-vehicle workloads. ARM Cortex-R5 dominates safety-critical roles, while Infineon’s TriCore excels in powertrain. The automotive MCU market size for 32-bit controllers is forecast to expand to USD 10.62 billion by 2031. Heterogeneous computing that blends control and AI neural processing widens the gap with 16-bit devices. 8-bit MCUs linger in low-speed sensor interfaces yet see declining share as integration rises.

Extended peripherals, deterministic latency, and hardware firewalls keep 32-bit parts preferable for ASIL-D systems. Infineon’s latest AURIX-3 devices deliver triple-core lockstep and 1,500 DMIPS per watt, underscoring the efficiency imperative. The automotive MCU market increasingly treats 16-bit as cost bins, while premium tiers pursue 32-bit for advanced cryptography and Ethernet TSN support.

By Application: Safety and ADAS Lead Growth

Safety and ADAS logged a 13.6% CAGR between 2026-2031, climbing on mandatory automated-brake and lane-keep assist regulations. Powertrain and chassis still hold the largest revenue due to universal fitment. The automotive MCU market share for powertrain remained 25.60% in 2025, yet its growth moderates as electrification shifts spend to battery-management units.

Software stacks now blur application lines; predictive maintenance RUNs on powertrain MCUs, while infotainment MCUs host speech AI. Texas Instruments’ AM275x-Q1 merges graphics rendering and driver-monitoring neural nets, evidencing cross-domain convergence. Edge-learning reduces cloud traffic and ensures privacy compliance in regions tightening data-sovereignty laws.

By Vehicle Propulsion Type: EVs Command Momentum

Commercial ICE fleets still led 27.80% of 2025 revenue. Electrified platforms, however, accelerate; battery-electric cars chart a 13.10% CAGR through 2031. The automotive MCU market size for BEV controllers is projected to more than triple, boosted by 800 V inverters and bi-directional charging controls. Hybrid systems require dual-domain MCUs orchestrating combustion and electric loops, translating to complex safety partitions.

MCUs for EVs must tolerate higher dv/dt spikes and integrate galvanic isolation to satisfy IEC 60747-17. Renesas’ RH850/C1M-Ax supports dual traction inverters and synchronous boost converters, highlighting the specialized demands of propulsion electrics.

By Process-Node Technology: FinFET Adoption Rises

40-22 nm nodes kept 22.10% of revenue in 2025, balancing cost and reliability. Yet ≤16 nm FinFET designs show a 11.9% CAGR, fuelled by AI-enabled zonal controllers. The automotive MCU market size linked to ≤16 nm is set to reach USD 5.29 billion by 2031. Radiation robustness and qualification costs slow adoption, but FinFET’s lower leakage aligns with EV power-budget constraints.

Meanwhile, ≥180 nm lines serve cost-sensitive body-control functions but lose share as consolidation intensifies. Automotive qualification lags consumer by 3-5 years; thus, leading-edge 5 nm nodes remain rare in automotive microcontrollers until strict zero-defect reliability proof emerges.

By Core Architecture: RISC-V Emerges as Challenger

ARM Cortex-R/A shipments grow 15.0% CAGR on real-time AI workloads in fail-operational systems. RISC-V commands 8.35% of 2025 revenue yet is scaling near 28% annually as OEMs chase royalty freedom. Infineon’s March 2025 RISC-V MCU family signals mainstream validation, supported by virtual prototypes that shorten time-to-merge for AUTOSAR stacks. Proprietary cores persist in niche torque-control loops where cycle-accurate legacy code is entrenched.

Customization potential lets suppliers tailor RISC-V instruction extensions for battery analytics or radar-fast-chirp loops, improving per-watt performance. The automotive MCU market could see RISC-V double share by 2028 if tool-chain maturity holds pace.

Geography Analysis

North America held 18.80% of revenue in 2025, propelled by autonomous-vehicle pilot zones and the CHIPS Act that subsidizes domestic fabs. Microchip’s USD 880 million Colorado silicon-carbide expansion secures local supply for EV traction inverters. Mexico’s cost-based assembly plants complement U.S. design hubs, while Canada benefits from zero-emission purchase incentives.

Asia-Pacific is the fastest-rising region with a 13.2% CAGR. China’s 25% domestic-chip-content mandate for 2025 energizes local MCU startups and joint ventures; VisionPower Semiconductor’s USD 7.8 billion 300 mm fab in Singapore underpins mixed-signal automotive output. Japan’s Renesas reported 50% year-on-year automotive growth in 2024, while South Korea leverages battery-cell expertise to embed high-density controllers into pack-management systems. India represents a nascent but strategic opportunity as production volumes climb and import duties favour localized sourcing.

Europe’s path to 65% EV penetration by 2030 necessitates heavier MCU content per car. The Industrial Action Plan announced March 2025 directs funds toward digitalization and cybersecurity, compelling OEMs to adopt ISO 21434-compliant controllers. Germany’s cost gap versus Chinese rivals pushes automation and software-centric designs that prioritize zonal compute. The EU Chips Act aims for 20% global semiconductor output by 2030, but cross-border coordination remains a headwind. Strict UN R155 enforcement across member states accelerates hardware security adoption.

Competitive Landscape

Market concentration is moderate: the top five vendors captured 81.5% of 2024 revenue, fostering high entry barriers but vigorous rivalry on feature integration. Infineon, with 28.5% share, leverages its AURIX tri-core safety heritage and the USD 2.5 billion Marvell Automotive Ethernet acquisition to fuse networking and compute for software-defined vehicles. NXP follows with a scalable S32 platform strategy that pairs MRAM flash with dedicated AI accelerators, easing OTA updates. STMicroelectronics differentiates through embedded Phase-Change Memory (PCM) and analog-front-end co-integration.

Microchip and Renesas round out the top five, emphasizing long-term supply commitments and functional-safety tool chains. RISC-V opens disruptive paths for China-based entrants aligned with localization policies. Yet the stringent 15-year product-support expectations and ISO certification overhead temper fast upheaval. White-space prospects include vehicle-to-grid bidirectional charging controllers, in-vehicle payment security MCUs, and AI-enhanced power-domain zonal hubs.

Supplier diversification gains urgency as OEMs hedges geopolitical exposure. Infineon, NXP, and ST are expanding European and U.S. front-end capacity, while foundry collaborations (e.g., VIS-NXP’s Singapore JV) pursue balanced global footprints. These moves aim to guarantee controller availability after the 2021-2023 shortage disrupted production plans worldwide.[4]Microchip Technology, “Microchip Expands Colorado SiC Manufacturing,” microchip.com

Automotive MCU Industry Leaders

Renesas Electronics Corporation

NXP Semiconductors N.V.

Infineon Technologies AG

STMicroelectronics N.V.

Texas Instruments Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Infineon announced the USD 2.5 billion purchase of Marvell’s Automotive Ethernet business, targeting USD 225-250 million revenue in 2025.

- March 2025: NXP unveiled the S32K5 MCU family built on 16 nm FinFET with embedded MRAM and an eIQ Neutron NPU; sampling starts Q3 2025.

- March 2025: Infineon introduced its first automotive RISC-V AURIX devices and virtual-prototype kits for pre-silicon software work.

- January 2025: Texas Instruments launched AWRL6844 60 GHz radar sensor and AM275x-Q1 MCUs with integrated edge AI for in-cabin safety.

Global Automotive MCU Market Report Scope

An MCU is an intelligent semiconductor IC consisting of a processor unit, memory modules, communication interfaces, and peripherals. The global automotive MCU market is segmented by product type (8-bit,16-bit, 32-bit), application (powertrain and chassis, safety and security, body electronics, and telematics and infotainment), vehicle type (passenger ICE vehicle, commercial ICE vehicle, and electric vehicles), and geography. The segmentation comprises an in-depth coverage of the global revenue generated from the sale of application-specific consumer analog ICs and unit shipments.

| 8-bit |

| 16-bit |

| 32-bit |

| Powertrain and Chassis |

| Safety and ADAS |

| Body and Comfort Electronics |

| Telematics and Infotainment |

| Passenger ICE |

| Commercial ICE |

| Battery Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV) |

| Plug-in Hybrid (PHEV) |

| Fuel-Cell Electric Vehicle (FCEV) |

| ≥180 nm |

| 90–65 nm |

| 40–22 nm |

| ≤16 nm (FinFET) |

| ARM Cortex-M |

| ARM Cortex-R/A |

| Proprietary 16/32-bit |

| RISC-V |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East | Israel |

| Saudi Arabia | |

| United Arab Emirates | |

| Turkey | |

| Rest of Middle East | |

| Africa | South Africa |

| Egypt | |

| Rest of Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Bit Class | 8-bit | |

| 16-bit | ||

| 32-bit | ||

| By Application | Powertrain and Chassis | |

| Safety and ADAS | ||

| Body and Comfort Electronics | ||

| Telematics and Infotainment | ||

| By Vehicle Propulsion Type | Passenger ICE | |

| Commercial ICE | ||

| Battery Electric Vehicle (BEV) | ||

| Hybrid Electric Vehicle (HEV) | ||

| Plug-in Hybrid (PHEV) | ||

| Fuel-Cell Electric Vehicle (FCEV) | ||

| By Process-Node Technology | ≥180 nm | |

| 90–65 nm | ||

| 40–22 nm | ||

| ≤16 nm (FinFET) | ||

| By Core Architecture | ARM Cortex-M | |

| ARM Cortex-R/A | ||

| Proprietary 16/32-bit | ||

| RISC-V | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East | Israel | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the automotive MCU market?

The automotive MCU market size is USD 12.34 billion in 2026 and is forecast to reach USD 18.29 billion by 2031.

Which application segment is growing fastest?

Safety and ADAS applications lead, expanding at a 13.6% CAGR as global regulations mandate advanced driver-assistance features.

Why are 32-bit MCUs gaining share over 16-bit devices?

Higher code complexity in EV powertrains and autonomous systems requires floating-point math, enhanced security, and AI acceleration only available in modern 32-bit architectures.

How will RISC-V influence the automotive MCU market?

RISC-V offers open-source flexibility and lower licensing costs, enabling custom instruction sets and fostering new entrants, which could double its market share by 2028.

Which region will contribute most to future growth?

Asia-Pacific shows the highest 13.2% CAGR, driven by China’s localization policies and rapid EV adoption across major Asian economies.

What are the main restraints limiting market expansion?

Lengthy ASIL-D safety qualification, mature-node foundry constraints, and rising compliance costs under ISO 26262/21434 temper growth momentum.

Page last updated on: