North America White LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

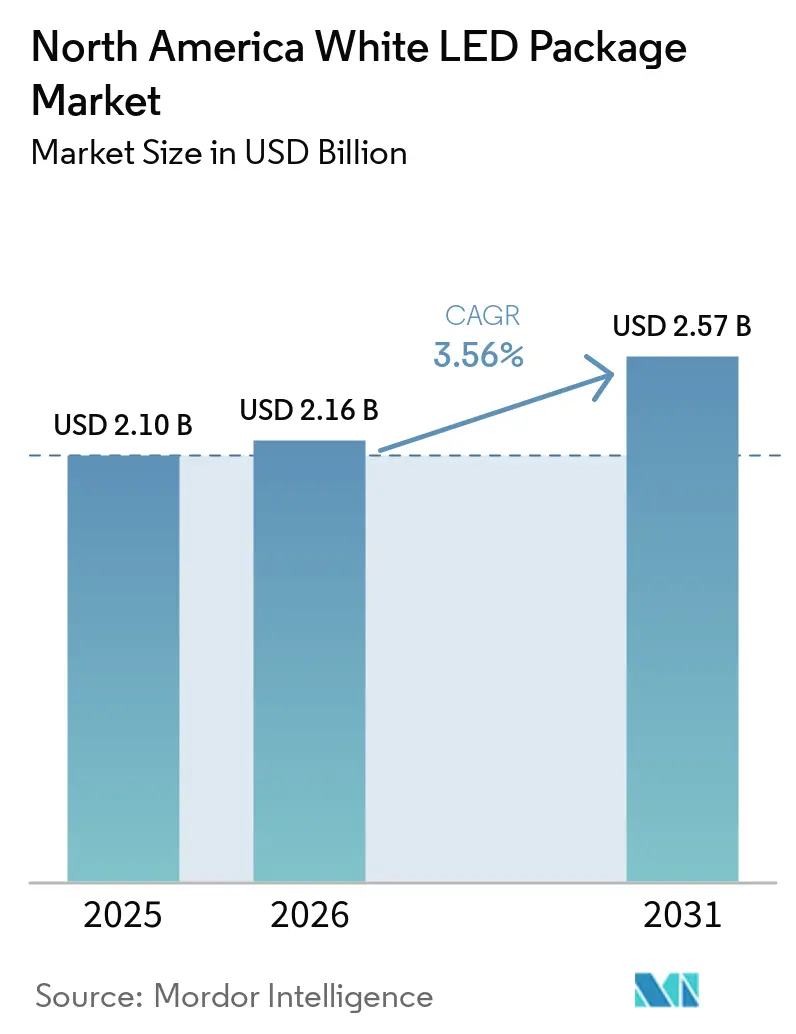

| Base Year Market Size (2025) | USD 2.10 Billion |

| Market Size (2026) | USD 2.16 Billion |

| Market Size (2031) | USD 2.57 Billion |

| Growth Rate (2026 - 2031) | 3.56% CAGR |

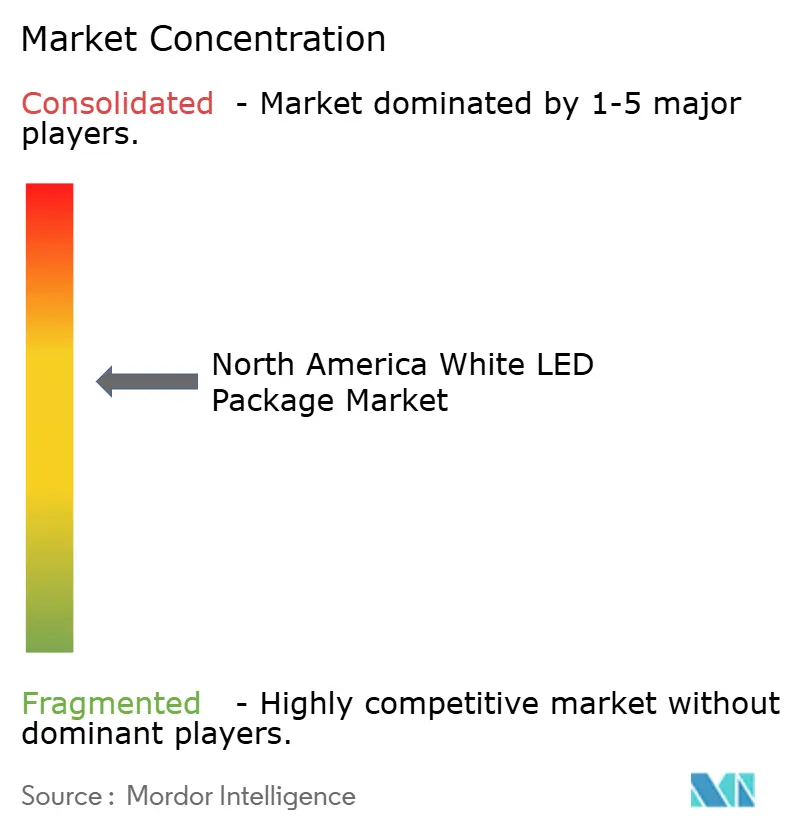

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America White LED Package Market Analysis by Mordor Intelligence

The North America white LED package market size is projected to expand from USD 2.10 billion in 2025 and USD 2.16 billion in 2026 to USD 2.57 billion by 2031, registering a CAGR of 3.56% between 2026 and 2031. Federal procurement rules are accelerating domestic assembly, nine mercury-lamp bans are compressing replacement cycles, and efficiency gains are shrinking the cost-per-lumen gap versus legacy sources. Chip-scale and flip-chip architectures are unlocking thinner form factors for automotive forward lighting, while high-power packages above 1 watt are penetrating vertical farms that demand tunable spectra with photosynthetic luminous efficacy above 400 photosynthetic lm W⁻¹. Smart-city streetlight conversions across U.S. and Canadian municipalities are lifting shipments of outdoor-rated packages with IP65 housing, DALI-2 addressability, and Buy America compliance. Nearshoring of automotive LED module assembly into Mexico is adding geographic resilience even as sapphire substrate imports remain a headline risk.

Key Report Takeaways

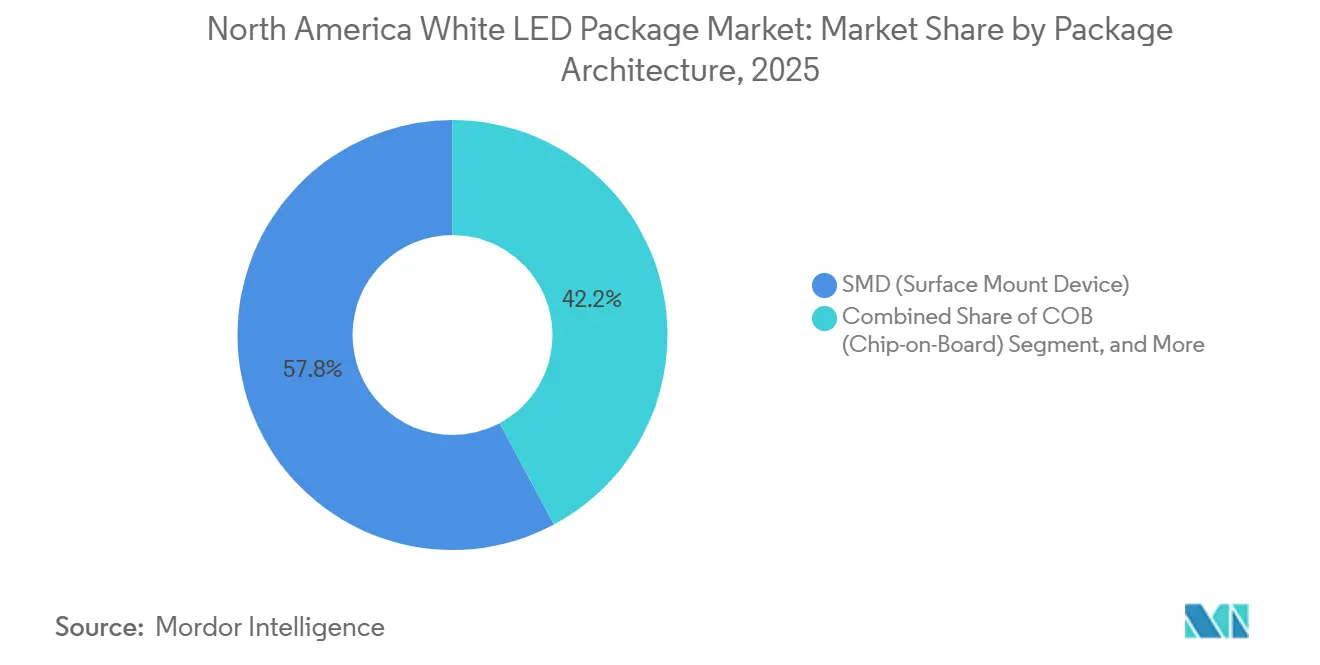

- By package architecture, surface-mount devices led with 57.82% revenue share in 2025, whereas chip-scale packages post the fastest 4.11% CAGR through 2031.

- By power class, mid-power LEDs accounted for 44.79% of the North America white LED package market share in 2025, while high-power packages above 1 watt are advancing at a 4.19% CAGR to 2031.

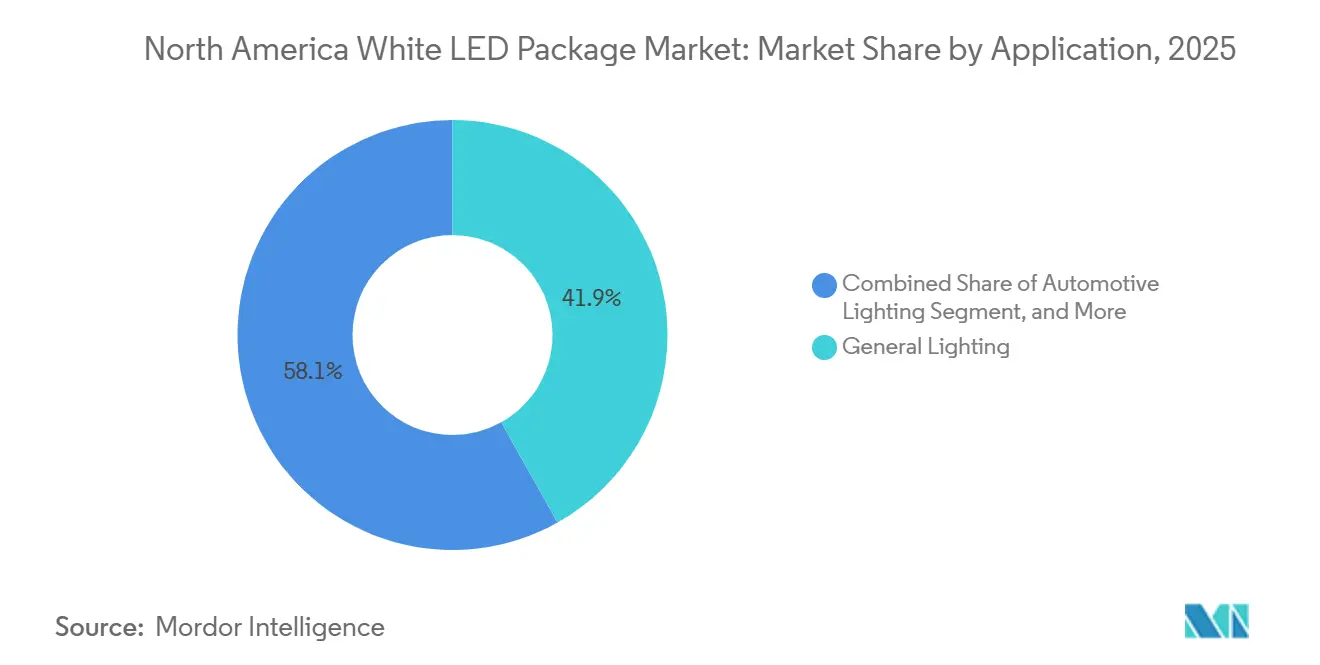

- By application, general lighting captured 41.88% of shipments in 2025, and automotive lighting exhibits the highest 3.91% CAGR over the forecast window.

- By geography, the United States contributed 82.49% revenue in 2025, while Canada records the quickest 3.78% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America White LED Package Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Federal and state efficiency mandates accelerating LED retrofits | +0.9% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Declining cost-per-lumen and efficacy gains | +0.7% | Global, strongest in United States and Canada | Medium term (2–4 years) |

| Smart-city infrastructure investments boosting high-power packages | +0.5% | United States and Canada urban centers | Medium term (2–4 years) |

| Automotive OEM shift to LED headlamps and DRLs | +0.6% | United States, Canada, Mexico corridors | Medium term (2–4 years) |

| Build America, Buy America sourcing rules reshaping supply chain | +0.4% | United States federal-aid projects | Short term (≤ 2 years) |

| Vertical farming demand for high-CRI tunable white packages | +0.3% | United States and Canada CEA hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Federal And State Efficiency Mandates Accelerating LED Retrofits

New general-service-lamp rules finalized in 2024 require omnidirectional lamps to reach about 125 lm W⁻¹ at 810 lm output, triggering redesigns of phosphor blends and driver circuits to meet LM-80 and TM-21 lifetime protocols.[1]U.S. Department of Energy, “Energy Conservation Standards for General Service Lamps,” energy.gov Parallel mercury-lamp bans across nine states eliminate fluorescent ballast demand, and the Federal Aviation Administration now specifies off-the-shelf LED lamps for runway alignment systems, bringing more than 20 airports into early adoption. Together these actions are shrinking retrofit cycles from seven to four years, lifting volumes of mid-power and high-power packages that satisfy strict lumen-maintenance criteria.

Declining Cost-Per-Lumen And Efficacy Gains

Classic phosphor-converted packages saw manufacturing cost drop 95.5% between 2003 and 2020 as wafer diameters quadrupled and yields tripled. Warm-white device efficiency climbed from 5.8% to 38.8% over the same horizon, leaving spectral efficiency and red-phosphor conversion as the next frontiers. Retail luminaire prices fell 27.3% annually from 2008 to 2020, cutting simple payback to under twelve months for many commercial retrofits, while packaging now dominates per-chip cost, favoring suppliers that integrate precision optics and low-thermal-resistance substrates at scale.

Smart-City Infrastructure Investments Boosting High-Power Packages

Municipal ownership transfers, such as Windsor, Colorado’s 3,100-pole acquisition, unlock capex for LED conversions with projected savings topping 500 MWh yearly. Port Moody, British Columbia has earmarked USD 150,000 per year over a decade to convert 2,100 fixtures, standardizing cobra-head luminaires for lifecycle savings of USD 2.3 million. New GSA guidance favors controls-ready luminaires with LLLC and demand-response, specifying high-power packages delivering 115-150 lm W⁻¹ and firmware-updatable drivers.[2]U.S. General Services Administration, “LED Lighting and Controls Guidance,” gsa.gov These city programs pull through outdoor-rated packages that also satisfy Buy America rules.

Automotive OEM Shift To LED Headlamps And DRLs

Content per vehicle is forecast to reach USD 520 by 2030 as adaptive driving beam, digital light processing, and animation features become mainstream. Lumileds’ LUXEON Altilon SMD-A, launched in 2025, offers 1,820 lm in a 1×5 array at 85 °C and fits a 433 µm z-height, enabling thinner headlamp modules. AEC-Q102 qualification and hot binning simplify Tier-1 integration, while nearshore assembly in Mexico reduces tariff exposure and secures supply for U.S. plants.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tariff volatility and substrate supply-chain disruptions | -0.4% | United States and Canada | Short term (≤ 2 years) |

| High capex for advanced packaging lines | -0.3% | United States and Canada | Medium term (2–4 years) |

| Dark-sky compliance ordinances curbing outdoor lumens | -0.2% | United States and Canada | Medium term (2–4 years) |

| Patent cross-licensing barriers for flip-chip architectures | -0.2% | Global, strong in North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tariff Volatility And Substrate Supply-Chain Disruptions

Section 301 duties on imported LED chips create unpredictable landed costs, forcing municipal bidders to hold quotes for shorter windows and eroding margins for fixture makers that sell under long-term price agreements.[3]Federal Highway Administration, “Build America, Buy America Guidance,” transportation.gov Sapphire wafer supply remains Asia-centric, and any logistics shock quickly ripples into North American packaging lines, lengthening lead times during peak retrofit seasons.

High Capex For Advanced Packaging Lines

A mid-scale chip-scale line with AOI, reflow, and photometric test chambers can exceed USD 10 million, a heavy burden for domestic entrants. DOE estimates USD 430 million in redesign costs for lamp makers to meet the 2028 efficacy rule, with most spending tied to package rather than luminaire tooling. Capital scarcity slows adoption of flip-chip and micro-LED processes outside a handful of well-capitalized incumbents.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Package Architecture: Chip-Scale Momentum Outpaces Legacy Formats

Chip-scale technology is set to widen its share as automotive forward-lighting designers prioritize low thermal resistance and thinner optics. Surface-mount devices still anchor cost-sensitive general lighting because existing pick-and-place lines handle them without retooling. Flip-chip variants eliminate wire bonds, dropping junction-to-board resistance below 2 °C W⁻¹ and enabling higher drive currents. Chip-on-board remains preferred for track and high-bay luminaires that benefit from high lumen density despite extra assembly steps.

High cross-licensing fees limit new entrants in flip-chip, preserving margins for incumbents. Yet Build America thresholds are nudging suppliers to open U.S. die-attach lines, which may gradually lower unit costs and speed CSP adoption. The North America white LED package market size for chip-scale devices is on course to capture incremental revenue as Tier-1 automotive contracts shift away from wire-bonded arrays. Sustained SMD dominance in retrofit lamps keeps overall architecture diversity balanced.

By Power Class: High-Power LEDs Accelerate In Premium Niches

High-power packages above 1 W register the quickest uptake as adaptive driving beam modules and vertical farms favor compact sources that simplify optics and wiring. Mid-power LEDs, owning 44.79% of the North America white LED package market share in 2025, remain the volume backbone of troffers and downlights thanks to their favorable cost-per-lumen profiles and long lifetime performance.

As efficacy creeps past 200 lm W⁻¹ for CRI 80 mid-power parts, their competitiveness in streetlighting narrows the gap with traditional high-power SKUs. Nevertheless, the North America white LED package market size tied to horticulture lighting leans heavily on multi-ampere high-power chips that can deliver spectral mixes at photon flux densities above 300 µmol m⁻² s⁻¹. Expected gains in substrate cooling and phosphor stability will keep these packages at the center of premium growth segments.

By Application: Automotive Lighting Leads Growth Trajectory

General lighting maintained 41.88% shipment share in 2025, driven by ongoing retrofit mandates and smart building upgrades. Yet automotive output is scaling faster, reflecting higher dollar content per electric vehicle and the migration to matrix and digital micromirror headlamps.

As automakers bundle daytime running light animations and interior ambient modules, the North America white LED package market size allocated to in-vehicle lighting climbs steadily. Meanwhile, ultraviolet-C disinfection, medical phototherapy, and entertainment spots form a small but profitable specialty tier that values long lifetime and precise spectral peaks. Continued DOE efficacy rules will keep general illumination the largest absolute consumer of packages, but vehicle platforms remain the momentum leader.

Geography Analysis

The United States remained the demand epicenter, holding 82.49% revenue in 2025 on the back of federal building retrofits, highway procurement mandates, and large smart-city streetlight programs. Municipalities from Delaware to Colorado specify warm-white packages under dark-sky rules, stimulating phosphor reformulations and glare-cutoff optics across supplier portfolios. Build America sourcing thresholds of 55% component cost by 2026 are catalyzing new driver and PCB assembly lines in the Southeast and Midwest.

Canada, though smaller, is forecast to grow 3.78% annually through 2031 as cities fund multi-year conversion plans and federal incentives reward energy-efficient infrastructure. The Port Moody program alone covers 2,100 fixtures and channels preference toward 3,000 K packages in residential zones, illustrating how specification nuances influence binning strategies. Provincial utilities are extending rebates that shorten payback below three years for municipal retrofit loans.

Mexico’s emerging role is supply-driven. Tier-1 lighting suppliers are colocating module shops near Bajío auto plants, using proximity to satisfy USMCA regional-content rules without incurring U.S. labor costs. While tariff swings and sapphire wafer dependence pose challenges, the logistics benefit and skilled electronics workforce are expected to pull incremental share away from imported packaged LEDs over the forecast horizon.

Competitive Landscape

Market concentration is moderate, with the five largest suppliers collectively accounting for roughly two-thirds of regional revenue. Lumileds, ams-OSRAM, Nichia, Cree LED, and Seoul Semiconductor defend share via patent pools, rapid LM-80 testing, and automotive AEC-Q102 qualification. San’an Optoelectronics’ pending USD 239 million purchase of Lumileds extends patent access and secures U.S. factory footprints, underscoring the strategic value of intellectual property and domestic production.

Domestic specialists such as LumenFocus and Paramount Lighting exploit Buy America rules by operating fabrication, powder-coat, and ETL labs that achieve 60-65% U.S. component thresholds today and chart pathways to 75% by 2028. These firms do not fabricate wafers but integrate packages, optics, and controls into compliant luminaires for federally funded infrastructure.

Technology differentiation clusters around chip-scale, flip-chip, and ultraviolet-C packages. Lumileds’ Altilon SMD-A delivers single-chip addressability at 1,820 lm, while Cree LED’s XP-G4 runs up to 3 A with 1.3 °C W⁻¹ thermal resistance, appealing to outdoor and architectural projects. ams-OSRAM’s 265 nm device breaks the 10% wall-plug barrier for disinfection, positioning the company for late-decade water-treatment tenders. Competitive intensity is expected to rise as Asian OSATs leverage packaging know-how via North American acquisitions, yet stringent patent cross-licensing keeps entry hurdles high.

North America White LED Package Industry Leaders

Cree LED, Inc.

Lumileds Holding B.V.

Nichia Corporation

ams-OSRAM GmbH

Seoul Semiconductor Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Windsor, Colorado started installation of 1,100 LED streetlights with QR-coded tags linking to the town’s SeeClickFix portal for outage reporting.

- October 2025: Lumileds debuted LUXEON Altilon SMD-A, a 433 µm-tall, single-chip addressable package for automotive forward lighting, pre-designed into 2026 model-year vehicles.

- July 2025: San’an Optoelectronics and Inari Amertron agreed to acquire Lumileds for USD 239 million, granting San’an 74.5% indirect control upon expected 1Q 2026 close.

- May 2025: Port Moody, British Columbia approved a decade-long USD 150,000-per-year program to retrofit 2,100 streetlights with standardized cobra-head LED fixtures.

North America White LED Package Market Report Scope

The North America White LED Package Market is witnessing significant growth due to increasing demand across various applications such as general lighting, automotive lighting, and display backlighting. The adoption of energy-efficient lighting solutions and advancements in LED technology are driving the market's expansion in the region.

The North America White LED Package Market Report is Segmented by Package Architecture (SMD, COB, CSP, and Flip-Chip LED Packages), Power Class (Low Power, Mid Power, and High Power), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| SMD (Surface Mount Device) |

| COB (Chip-on-Board) |

| CSP (Chip Scale Package) |

| Flip-Chip LED Packages |

| Low Power (Less Than 0.5 W) |

| Mid Power (0.5 - 1 W) |

| High Power (Greater Than 1 W) |

| General Lighting |

| Automotive Lighting |

| Display And Backlighting |

| Specialty / Niche |

| United States |

| Canada |

| Mexico |

| By Package Architecture | SMD (Surface Mount Device) |

| COB (Chip-on-Board) | |

| CSP (Chip Scale Package) | |

| Flip-Chip LED Packages | |

| By Power Class | Low Power (Less Than 0.5 W) |

| Mid Power (0.5 - 1 W) | |

| High Power (Greater Than 1 W) | |

| By Application | General Lighting |

| Automotive Lighting | |

| Display And Backlighting | |

| Specialty / Niche | |

| By Geography | United States |

| Canada | |

| Mexico |

Key Questions Answered in the Report

How large will North America’s white LED package demand be by 2031?

Shipments are forecast to support a market value of USD 2.57 billion by 2031, reflecting a 3.56% CAGR from 2026.

Which package architecture is growing the fastest?

Chip-scale packages lead growth at a projected 4.11% CAGR as automotive and specialty lighting favor thinner, thermally efficient formats.

Why are high-power LEDs important for vertical farming?

High-power devices deliver the photon flux needed to exceed 400 photosynthetic lm W⁻¹, enabling tunable light recipes that cut energy costs in stacked farms.

What impact do Buy America rules have on suppliers?

The 55% domestic-content threshold effective Oct 2026 is driving new U.S. assembly lines for drivers, optics, and thermal components, reshaping sourcing strategies.

Which geography shows the quickest growth through 2031?

Canada posts the highest 3.78% CAGR, propelled by municipal retrofit programs and federal efficiency incentives.

How does automotive electrification influence package demand?

Electric vehicles integrate more adaptive and animated lighting, lifting content-per-vehicle to an expected USD 520 by 2030 and bolstering high-power package shipments.

Page last updated on: