Asia Pacific LED Chips Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

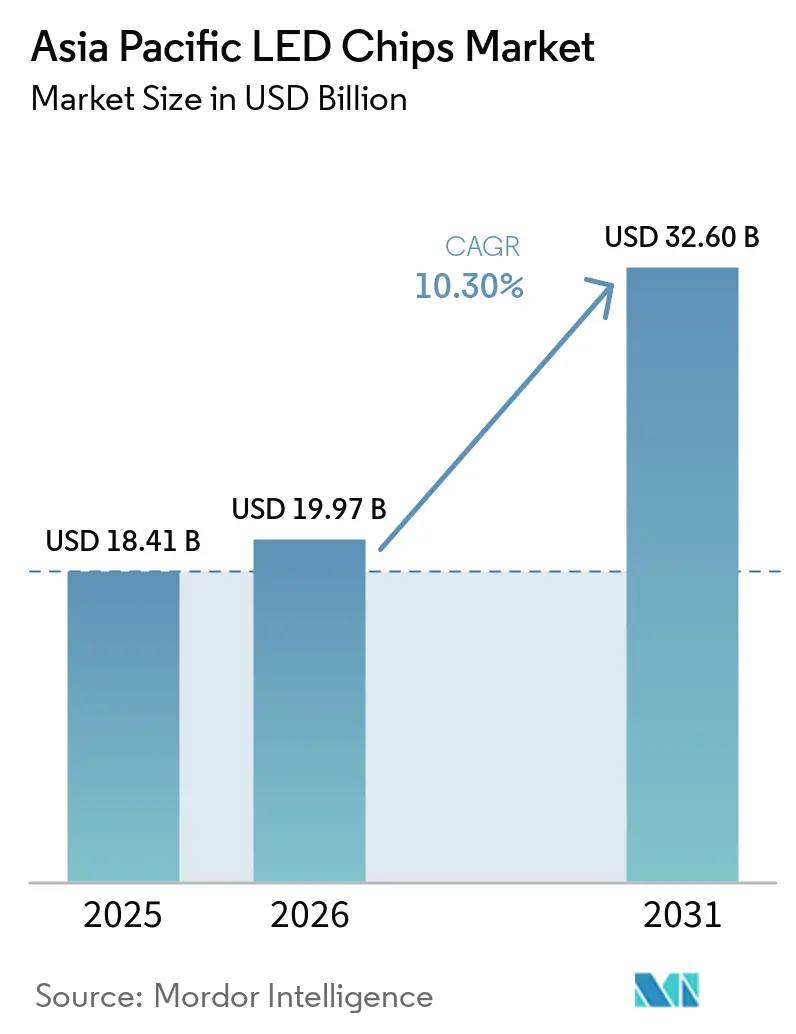

| Base Year Market Size (2025) | USD 18.41 Billion |

| Market Size (2026) | USD 19.97 Billion |

| Market Size (2031) | USD 32.60 Billion |

| Growth Rate (2026 - 2031) | 10.30% CAGR |

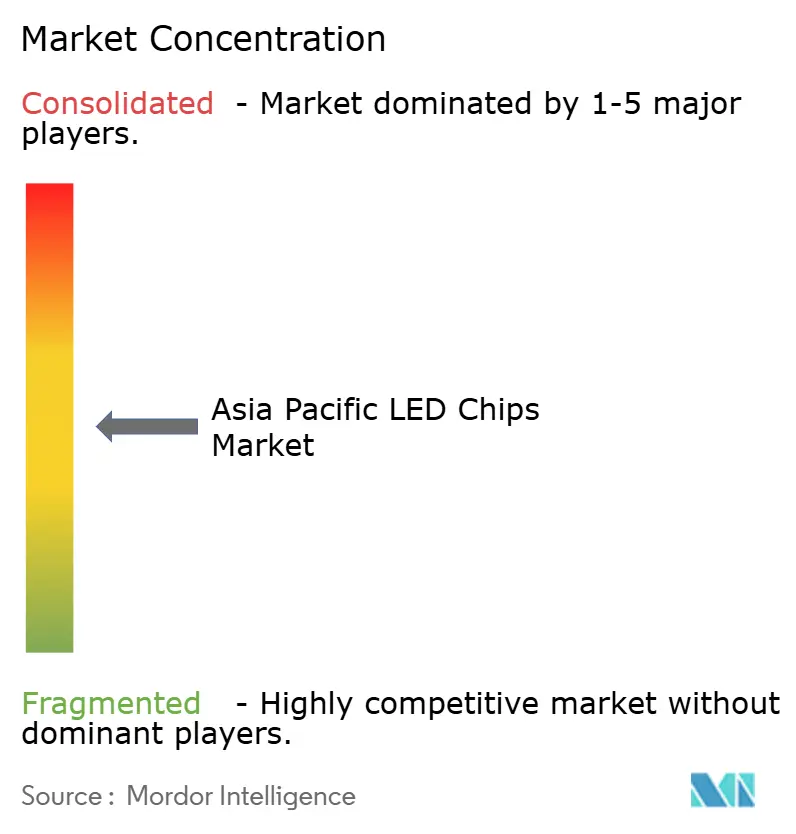

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Asia Pacific LED Chips Market Analysis by Mordor Intelligence

The Asia Pacific LED chips market size is expected to grow from USD 18.41 billion in 2025 to USD 19.97 billion in 2026 and is forecast to reach USD 32.60 billion by 2031 at 10.3% CAGR over 2026-2031. Robust demand for mini-LED backlighting in high-end televisions, accelerating automotive integration, and steady policy support across major economies are reinforcing the region’s leadership in advanced solid-state lighting. China continues to leverage its vertically integrated ecosystem to defend cost advantages, even as subsidy reductions elevate efficiency imperatives. India is emerging as the next growth pole, drawing investment into local epitaxy and chip fabrication through Production Linked Incentive schemes that sharply raise domestic value added. At the technology frontier, micro-LED architectures are gaining momentum, but transfer yield bottlenecks and capital intensity still cap short-term volumes, sustaining a three-tier market spanning conventional LEDs, mini-LEDs, and early-stage micro-LEDs.

Key Report Takeaways

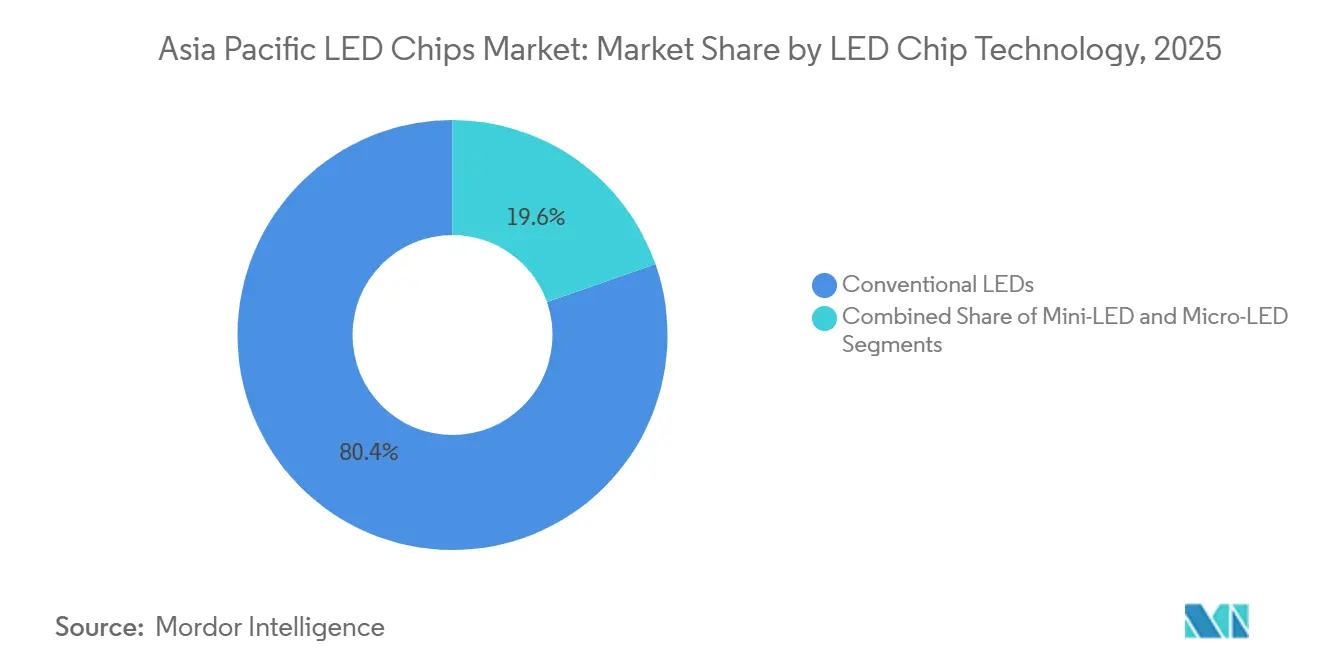

- By LED chip technology, conventional LEDs held 80.36% of the Asia Pacific LED chips market share in 2025, whereas micro-LEDs are projected to grow at a 14.34% CAGR through 2031.

- By semiconductor material, GaN and InGaN commanded nearly 85.23% share of the Asia Pacific LED chips market in 2025, while AlGaInP-based chips are set to post the quickest expansion at about 13.4% CAGR on the back of phosphor-free display demand.

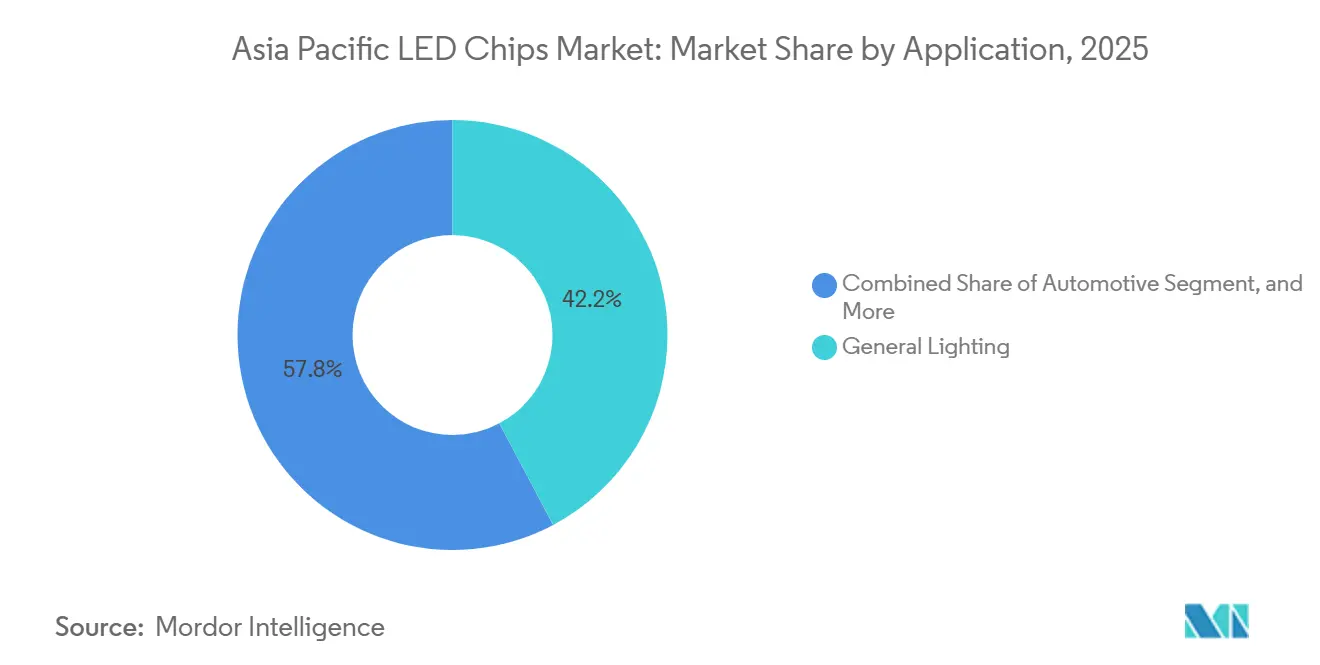

- By application, general lighting accounted for 42.24% share of the Asia Pacific LED chips market size in 2025, while automotive lighting is pacing ahead with a 16.2% CAGR projected to 2031.

- By geography, China held 45.13% of the Asia Pacific LED chips market share in 2025, whereas India is forecast to grow the fastest at 15.89% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Asia Pacific LED Chips Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Expanding Mini-LED Backlighting Adoption in High-End TVs | +2.1% | China, South Korea, Japan, with spillover to Southeast Asia | Medium term (2-4 years) |

| Government-Led "Make in India" Incentives for LED Chip Fabrication | +1.8% | India, with indirect effects on regional supply chains | Medium term (2-4 years) |

| Electrification of Two-Wheeler Mobility in Southeast Asia | +1.5% | Southeast Asia (Vietnam, Thailand, Indonesia), India | Medium term (2-4 years) |

| Corporate Net-Zero Targets Accelerating Industrial LED Retrofits | +1.3% | China, India, ASEAN industrial corridors | Short term (≤ 2 years) |

| Growing Demand for UV-C LED Chips in Sterilization Systems | +1.2% | Global, with early adoption in Japan, South Korea, Singapore | Short term (≤ 2 years) |

| Phosphor-Free Micro-LED Architectures Reducing Cost per Lumen | +1.0% | Global, led by R&D hubs in South Korea, Taiwan, Japan | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government-Led “Make In India” Incentives For LED Chip Fabrication

India’s Production Linked Incentive scheme grants 4-6% rewards on incremental sales of qualified LED components, spurring brownfield expansions and new fabs that target a steep jump in domestic value addition from below 20% toward 80%. Approved applicants have already pledged more than USD 1 billion, unlocking a pathway for global chip producers to diversify sourcing and cut reliance on any single country.[1]Ministry of Commerce and Industry, “13 Companies File Applications Under PLI Scheme for White Goods,” pib.gov.inSuccess depends on parallel investment in GaN epitaxy reactors, trained talent, and supportive infrastructure, areas now moving up the policy priority list.

Electrification Of Two-Wheeler Mobility In Southeast Asia

Electric scooters and motorcycles dominate urban transport in Vietnam, Thailand, and Indonesia, creating a surge in demand for power-efficient LED headlamps, taillights, and instrument clusters. Adaptive beams and daytime running lights raise the chip content per vehicle, while the tropical climate sets strict thermal performance requirements. Vehicle makers favor modular LED assemblies that lower assembly complexity and warranty costs, positioning chip vendors with robust thermal engineering capabilities for outsized gains.

Corporate Net-Zero Targets Accelerating Industrial LED Retrofits

Multinational manufacturers operating across China, India, and ASEAN are upgrading high-bay and outdoor lighting to meet science-based carbon goals. Procurement teams now specify chips exceeding 200 lumens per watt and 50,000-hour lifetimes, pushing suppliers to refine epitaxial structures and thermal resistance. Rapid payback periods in electricity-price sensitive zones shorten adoption cycles, adding a dependable demand floor for high-efficacy chips within the Asia Pacific LED chips market.

Expanding Mini-LED Backlighting Adoption In High-End TVs

Premium television brands are rapidly rolling out mini-LED backlit models that feature thousands of local dimming zones, delivering high dynamic range contrast and wide color gamut. The leap in chip counts per panel rewards suppliers that can control epitaxy, fabrication, and tight wavelength binning internally.[2]Samsung Electronics America, “Samsung Expands 2026 TV Lineup with Refreshed Neo QLED Series and All-New Mini LED TVs,” news.samsung.com Rising penetration of 85-inch and 100-inch screens in China, South Korea, and Japan further multiplies unit demand, cementing mini-LEDs as a near-term growth catalyst for the Asia Pacific LED chips market.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Persistent Yield Challenges in Micro-LED Mass Transfer | -1.5% | Global, with acute impact on South Korea, Taiwan, Japan R&D hubs | Medium term (2-4 years) |

| Supply-Demand Mismatch of 6-Inch GaN Epitaxial Wafers | -1.2% | China, Taiwan, South Korea, with spillover to India | Short term (≤ 2 years) |

| Volatile Rare-Earth Phosphor Prices Affecting Chip Margins | -0.9% | Global, with concentrated supply risk in China | Short term (≤ 2 years) |

| Intellectual-Property Cross-Licensing Barriers for Start-Ups | -0.8% | Global, particularly affecting new entrants in India, Southeast Asia | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply-Demand Mismatch Of 6-Inch GaN Epitaxial Wafers

LED, power, and RF device makers are competing for finite 6-inch GaN wafer capacity, a tension aggravated by the slow migration to 8-inch lines. Price volatility and allocation risk squeeze margins for chip producers lacking captive epitaxy or strategic supply agreements. The dynamic fuels vertical integration moves across China, Taiwan, and South Korea, but raises entry barriers for fabless design houses that depend on merchant wafer supply.[4]Seong Woo Hong et al., “Assembly and Integration of Micro-LED Displays,” International Journal of Extreme Manufacturing, iopscience.iop.org

Persistent Yield Challenges In Micro-LED Mass Transfer

Commercial display production demands near-perfect transfer yields that today’s best laser or roll-to-roll techniques cannot consistently achieve. Even a 99.99% yield leaves thousands of dead pixels in ultra-high-resolution panels, forcing expensive repair cycles that erode profitability.[3]Cheng Luo et al., “Laser-Assisted Mass Transfer Technology for Microlight-Emitting Diodes,” Nanomanufacturing and Metrology, springer.com Until six-sigma yields and high-throughput tools converge, micro-LED volumes will remain constrained, tempering the top-line contribution of this next-generation segment to the Asia Pacific LED chips market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By LED Chip Technology: Performance Tiering Shapes Demand

The conventional LED segment retained 80.36% share in 2025, anchoring the Asia Pacific LED chips market size with dependable cost-per-lumen economics at sub-USD 0.10 per chip. Mini-LED arrays have carved out a premium middle ground, supporting thousands of local dimming zones in televisions and monitors while avoiding the full mass-transfer burden of micro-LEDs. Premium TV makers are scaling screen sizes from 43-inch to 100-inch, raising chip counts per panel and creating fertile ground for value-added binning and thermal management services. Micro-LED chips, although still below 5% volume, are advancing at a 14.34% CAGR on the back of direct-emissive display pilots for ultra-large TVs and augmented-reality wearables. Suppliers that master six-sigma transfer yields and parallel laser tools stand to translate early technical wins into outsized revenue as micro-LED throughput improves.

Price pressure in commodity conventional LEDs continues to compress gross margins, prompting large fabs to automate wafer handling and adopt larger-format reactors to dilute fixed costs. Mini-LED’s sweet spot in television backlighting is widening as blue-chip brands pair quantum dots with denser LED matrices to deliver OLED-like contrast, extending the segment’s runway beyond the forecast horizon. Micro-LED architectures command pricing power that is two to three times higher than mini-LEDs on a per-lumen basis, but the Asia Pacific LED chips market still values predictable delivery schedules over bleeding-edge claims, explaining the cautious but steady pace of micro-LED capacity additions. Technology roadmaps across China, South Korea, and Taiwan now sequence incremental yield milestones, aiming for 99.9999% transfer performance by 2028, which will be a decisive inflection for volume adoption.

By Semiconductor Material: GaN Core, AlGaInP and AlGaN Niches Emerge

GaN and InGaN commanded nearly 85.23% share of the Asia Pacific LED chips market in 2025, while AlGaInP-based chips are set to post the quickest expansion at about 13.4% CAGR on the back of phosphor-free display demand. Continuous strain-management tweaks and quantum-well redesigns have boosted the efficacies of premium GaN chips to beyond 200 lumens per watt, enabling luminaire makers to increase fixture luminous flux without a proportional increase in heat. AlGaInP chips deliver superior red output and are now riding the micro-LED wave, as phosphor-free direct RGB stacks demand uncompromised red purity. Deep-UV AlGaN chips, while still below 5% shipment value, are growing at double-digit rates on the back of healthcare sterilizers and water purification modules that require mercury-free, instant-on disinfection.

Gallium nitride remains the foundational platform for blue and white LEDs, maintaining roughly a 50% revenue share thanks to mature epitaxy, robust light-extraction techniques, and a broad supplier base. Continuous strain-management tweaks and quantum-well redesigns have lifted the efficacies of premium GaN chips beyond 200 lumens per watt, allowing luminaire makers to push fixture luminous flux without a proportional increase in heat. AlGaInP chips deliver superior red output and now ride the micro-LED wave, because phosphor-free direct RGB stacks demand uncompromised red purity. Deep-UV AlGaN chips, while still below 5% shipment value, are growing at double-digit rates on the back of healthcare sterilizers and water purification modules that require mercury-free, instant-on disinfection.

By Application: Automotive Lighting Leads Growth Momentum

General lighting still accounted for about 42.24% of 2025 revenue, supported by road-lamp conversions mandated for completion by 2030. Automotive lighting, fueled by electric-vehicle penetration and adaptive driving-beam legislation, is tracking a 16.2% CAGR well ahead of the broader Asia Pacific LED chips market. Matrix headlamps now integrate 20-100 controllable chips, driving dollar content per vehicle higher and enforcing automotive-grade qualification barriers. Interior ambient systems are evolving from basic RGB strips to dynamically orchestrated mood lighting, multiplying chip counts while raising color-bin uniformity demands. General lighting, still the volume anchor with 40-50% share, is migrating toward 200-plus-lm-per-watt efficacy targets and smart-control interoperability, shifting value toward higher-spec chips rather than pure volume play.

Display backlighting shows a bifurcation: mainstream mobile and monitor SKUs continue to favor cost-optimized edge-lit arrays, whereas premium televisions and professional monitors are moving toward densely packed mini-LED and exploratory micro-LED designs. Industrial and specialty niches, ranging from horticulture to UV-C sterilization, supply high-margin orders in modest volumes that help buffer price erosion elsewhere. Net-zero procurement policies across multinational factories add a stable retrofit pipeline for high-lumen, long-lifetime chips, tying sustainability targets directly to chip specification upgrades.

Geography Analysis

China maintained a 48.01% grip on the Asia Pacific LED chip market in 2025, underpinned by fully integrated supply chains that span from sapphire slicing to finished luminaires. Provincial subsidy tapering is accelerating consolidation, prompting weaker fabs to exit or partner, while stronger players allocate capital to overseas acquisitions and process automation that trims per-unit costs. Local makers also fast-track micro-LED pilot lines to defend technological relevance and capture future export opportunities in premium displays. Regional policy swings toward self-sufficiency are prompting domestic TV and automotive brands to hedge geopolitical exposure by dual-sourcing chips, creating selective openings for non-Chinese vendors that can meet aggressive price-performance benchmarks.

India is charting the fastest trajectory in the Asia Pacific LED chips market, turning its Production Linked Incentive program into tangible fab and packaging projects across Gujarat, Tamil Nadu, and Uttar Pradesh. Approved firms have pledged over USD 1.2 billion, with a clear mandate to lift domestic value add toward the 75-80% band. Success depends on synchronized investments in GaN epitaxy reactors, power-quality infrastructure, and workforce skilling, yet early-stage subsidized output already finds captive demand from a booming domestic luminaire sector. Sustained 15.89% CAGR momentum positions India as a credible second pillar alongside China, broadening regional supply resilience.

Japan and South Korea maintain leadership in high-performance niches, leveraging deep R and D benches to commercialize phosphor-free micro-LED stacks and UV-C devices with class-leading reliability. Southeast Asia, particularly Vietnam and Indonesia, is emerging as an assembly and application hub that marries low labor costs with soaring domestic demand for electric two-wheelers and mobile devices. Taiwan’s contract wafer and equipment houses remain vital to the Asia Pacific LED chips market supply web, even as some fabs diversify into silicon carbide substrates. Collectively, this multipolar landscape dilutes single-country concentration risk, though logistical chokepoints in GaN wafer supply and rare-earth phosphors still warrant close monitoring.

Competitive Landscape

The top five manufacturers, Nichia, Samsung Electronics, San’an Optoelectronics, Seoul Semiconductor, and Epistar, captured roughly 50-60% revenue in 2025, leaving a long tail of regional suppliers focused on commodity general lighting. Leading firms deepen vertical integration to absorb wafer pricing swings and extract margin from epitaxy through packaged devices. Samsung leverages internal backlighting demand to scale mini-LED output rapidly, reinforcing its internal customer advantage that smaller peers cannot replicate.

IP intensity is rising in micro-LED transfer, where portfolio depth around laser liftoff, elastomeric sheets, and fluidic self-assembly determines entry feasibility. Start-ups such as PlayNitride and Jade Bird Display position on narrow, high-brightness niches that incumbents overlook, often partnering with OEMs to co-develop bespoke chipsets. Maturity in conventional LEDs has reduced differentiation to cents-per-kilolumen metrics, pushing volume players toward AI-driven binning and predictive maintenance analytics that shave operating expense. The Asia Pacific LED chips market thus displays a two-track rivalry: scale efficiency in commodity lighting and IP-fortified races in specialty arenas.

Pricing discipline remains fragile when demand softens, as evidenced by mid-2025 inventory write-downs at several Chinese fabs. Yet, capacity rationalization and tighter subsidy regimes are nudging survivors toward healthier utilization rates. Long-range strategic bets on RGB micro-LED displays and UV-C sterilization chips form the next revenue cliffs that will likely separate cash-rich innovators from pure-play commodity houses. Overall, competitive posture favors firms with balanced portfolios that can cross-subsidize R and D through steady cash flow from mid-market products.

Asia Pacific LED Chips Industry Leaders

Nichia Corporation

Samsung Electronics Co., Ltd.

Seoul Semiconductor Co., Ltd.

Epistar Corporation

EVERLIGHT Electronics Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- Jan 2026: Samsung Electronics unveiled its 2026 Neo QLED and Mini LED TVs, ranging from 43-inch to 100-inch, reinforcing its leadership in quantum mini-LED backlighting.

- January 2026: A Nanomanufacturing and Metrology paper reported excimer laser mask projection achieving ±0.3 µm placement accuracy and 99.9% yields, highlighting progress toward industrial micro-LED transfer.

- November 2025: India’s fourth PLI round attracted 13 applicants with planned investments of Rs 1,914 crore (USD 230 million), including Rs 98 crore (USD 12 million) for LED chips and components.

Asia Pacific LED Chips Market Report Scope

The Asia Pacific LED Chips Market Report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, Micro-LED), Semiconductor Material (GaN/InGaN, AlGaInP, Other Semiconductor Materials), Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, Industrial/Specialty Lighting), and Geography (China, Japan, India, South Korea, Southeast Asia, Rest of Asia Pacific). The Market Forecasts are Provided in Terms of Value (USD).

| Conventional LEDs |

| Mini-LED |

| Micro-LED |

| GaN / InGaN |

| AlGaInP |

| Other Semiconductor Materials |

| General Lighting |

| Automotive |

| Backlighting / Displays |

| Consumer Electronics |

| Industrial / Specialty Lighting |

| China |

| Japan |

| India |

| South Korea |

| Southeast Asia |

| Rest of Asia Pacific |

| By LED Chip Technology | Conventional LEDs |

| Mini-LED | |

| Micro-LED | |

| By Semiconductor Material | GaN / InGaN |

| AlGaInP | |

| Other Semiconductor Materials | |

| By Application | General Lighting |

| Automotive | |

| Backlighting / Displays | |

| Consumer Electronics | |

| Industrial / Specialty Lighting | |

| By Geography | China |

| Japan | |

| India | |

| South Korea | |

| Southeast Asia | |

| Rest of Asia Pacific |

Key Questions Answered in the Report

What is the current Asia Pacific LED chips market size and its growth outlook?

The market stands at USD 19.97 billion in 2026 and is projected to reach USD 32.60 billion by 2031, advancing at a 10.3% CAGR.

Which LED chip technology is growing fastest in the region?

Micro-LED chips are advancing the quickest, tracking a 14-15% CAGR through 2031 as display makers pilot direct-emissive products.

Why is India attracting new LED chip investments?

Production Linked Incentive subsidies covering 4-6% of incremental sales are drawing more than USD 1.2 billion in pledged projects aimed at lifting domestic value add to about 80%.

How are automotive trends influencing LED chip demand?

Electric vehicles and adaptive headlamp regulations are boosting matrix headlamp adoption, raising chip counts per vehicle and generating 14-16% CAGR in automotive applications.

Page last updated on: