High-Power LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.5 Billion |

| Market Size (2031) | USD 5.95 Billion |

| Growth Rate (2026 - 2031) | 5.76% CAGR |

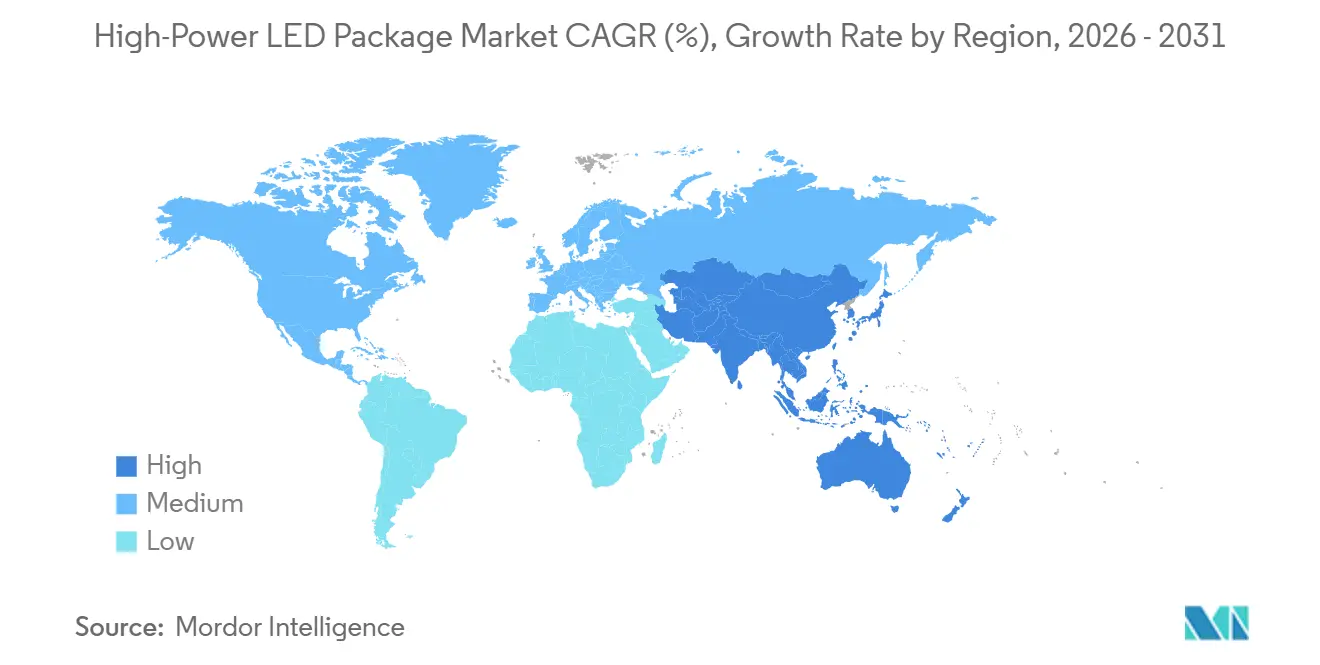

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

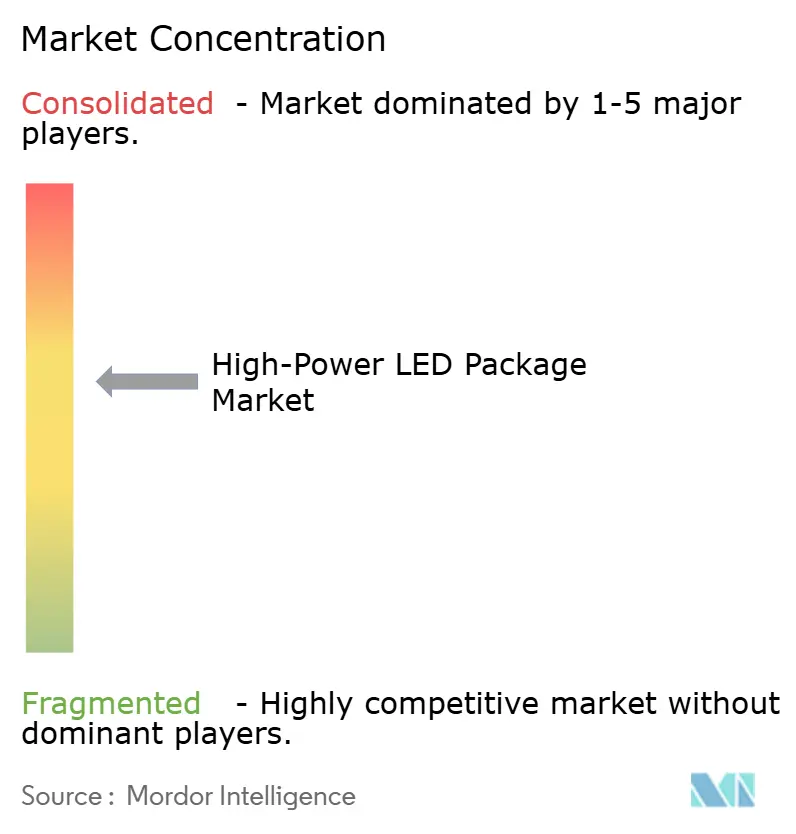

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

High-Power LED Package Market Analysis by Mordor Intelligence

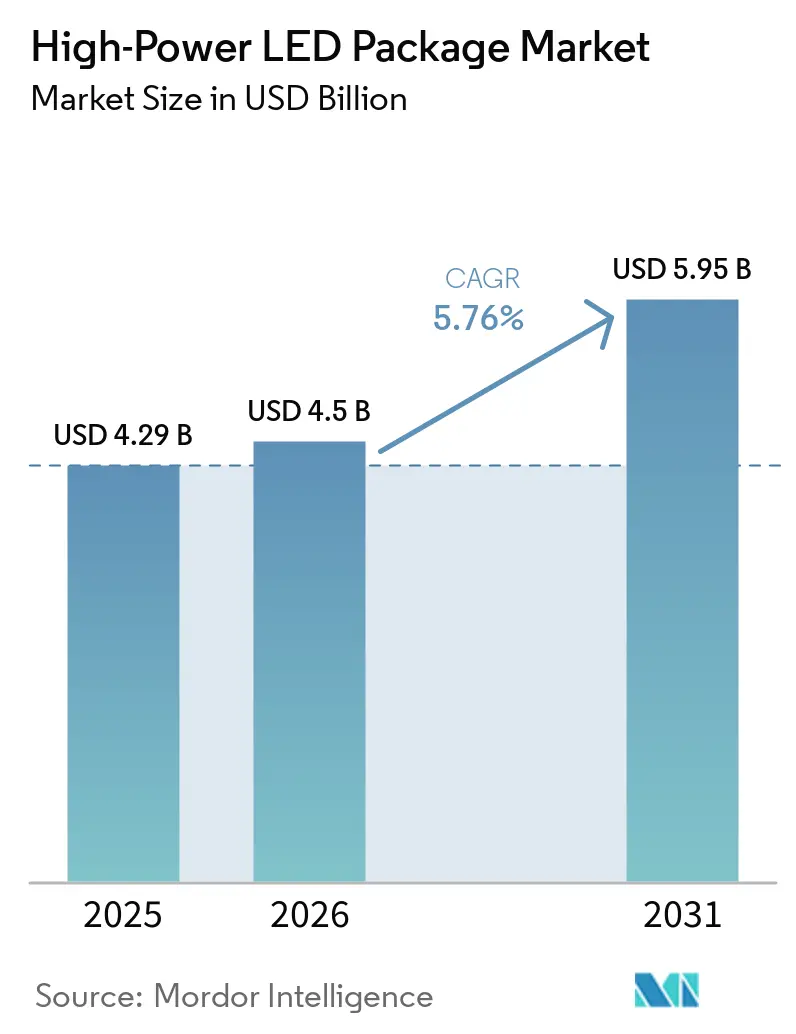

The High-Power LED Package market size is expected to increase from USD 4.29 billion in 2025 to USD 4.50 billion in 2026 and reach USD 5.95 billion by 2031, growing at a CAGR of 5.76% over 2026-2031. Automotive solid-state headlamps, adaptive driving beam platforms, and matrix-LED modules are steering premium demand while municipal street-lighting conversions and vertical-farming fixtures sustain high unit volumes in the 3-10 W tier. Price pressure from surplus epitaxial capacity in China coexists with technical tailwinds such as laboratory efficacy results above 200 lm/W and routine commercial performance at 140-160 lm/W that lower total cost of ownership for retrofit projects worldwide. Regulatory efficacy thresholds in the United States, Europe, and Australia are phasing out compact fluorescent, metal-halide, and high-pressure sodium sources, channeling replacement budgets toward packages that can sustain elevated junction currents without compromising L70 lifetime. Simultaneously, smart-city and smart-building codes that require daylight response and multi-level dimming are nudging fixture designers toward packages with embedded telemetry, integrated thermal vias, and wireless-ready footprints. Asia-Pacific accounts for more than two-thirds of global consumption, yet that dominance is tempered by gallium export constraints and rare-earth phosphor bottlenecks that have already swung component costs by 40-60% within a single quarter.

Key Report Takeaways

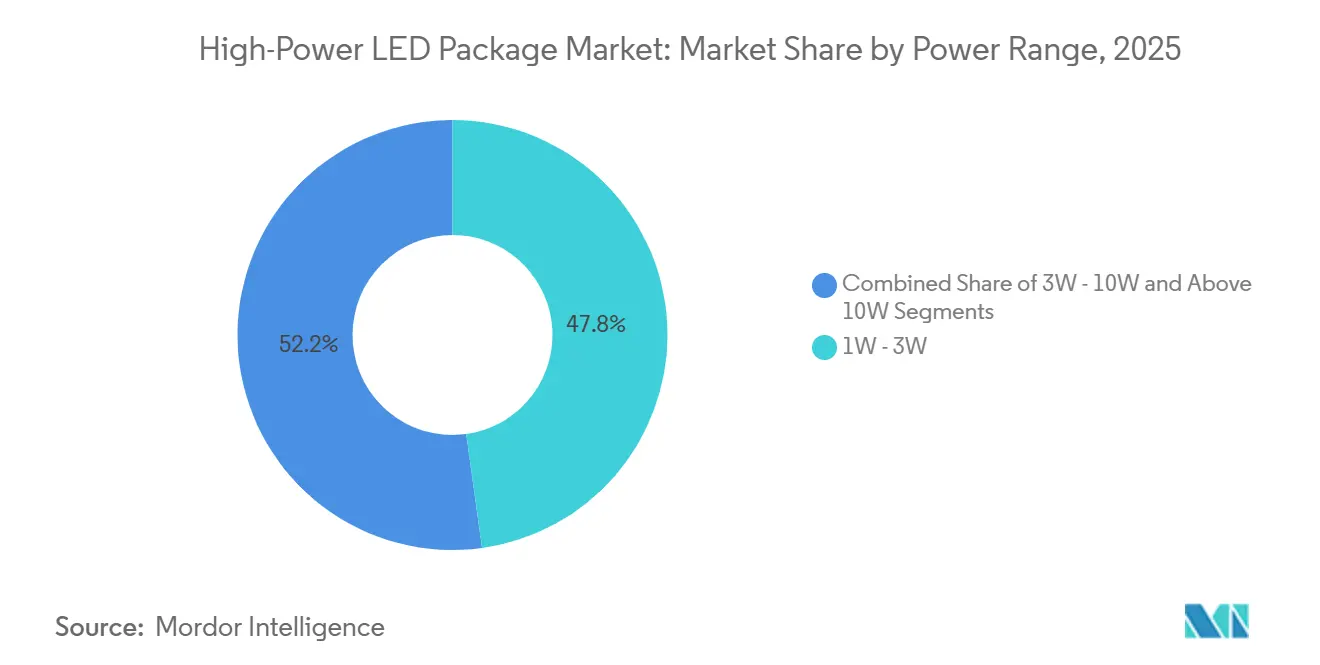

- By power range, the 1-3 W tier led with 47.80% revenue share in 2025, while the above-10 W class is projected to post the fastest advance at a 7.11% CAGR through 2031.

- By architecture, single-die packages commanded 36.29% of 2025 revenue, whereas chip-on-board solutions are forecast to expand at a 6.85% CAGR during 2026-2031.

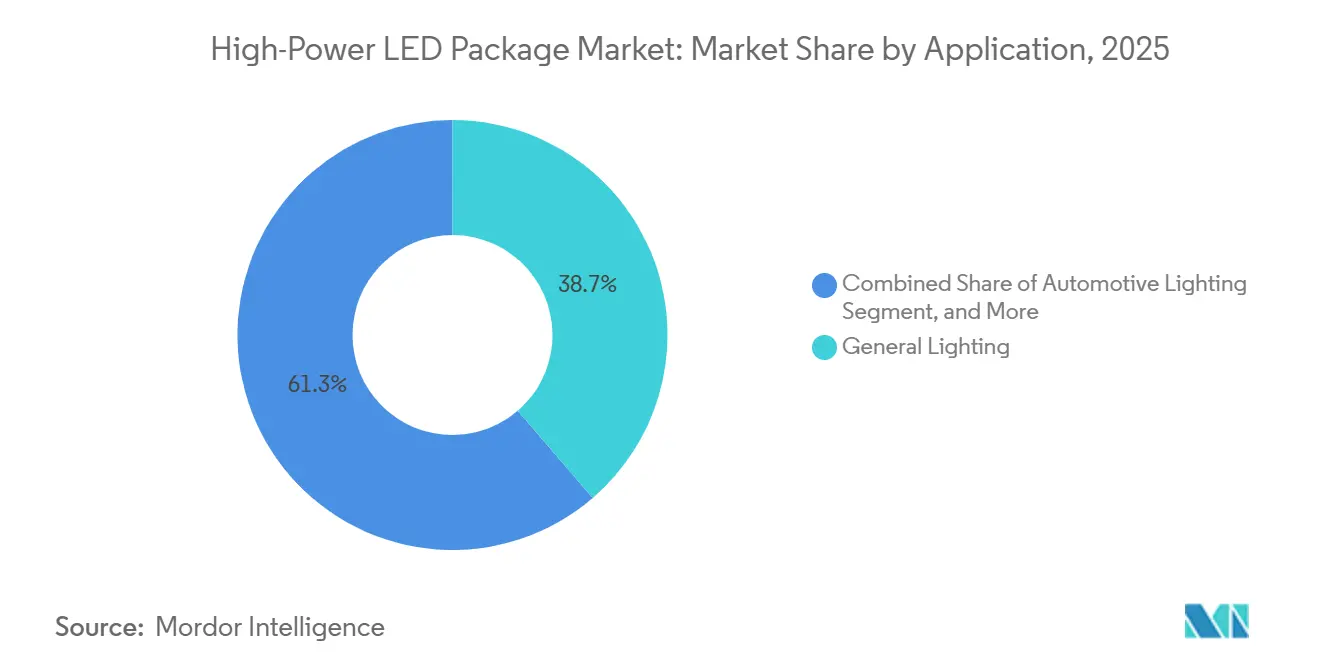

- By application, general lighting accounted for 38.70% of 2025 revenue, but automotive lighting is set to grow at 6.70% through 2031, driven by matrix and pixel headlamps.

- By geography, Asia-Pacific dominated with a 68.60% share in 2025 and is the fastest-growing region, advancing at a 7.20% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global High-Power LED Package Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Rapid Decline in USD per Lumen for High-Power Packages | +1.8% | Global, led by Asia-Pacific and North America | Medium term (2-4 years) |

| Government-Mandated Phase-Out of HID Streetlights | +1.5% | North America and Europe, emerging in India and Southeast Asia | Short term (≤ 2 years) |

| Automotive Shift to Solid-State Headlamps and ADB | +1.3% | Europe, North America, growing in China and Japan | Medium term (2-4 years) |

| Proliferation of Smart Lighting Controls Requiring High-Current LEDs | +0.9% | Global, early in North America smart-cities and Europe commercial buildings | Medium term (2-4 years) |

| Demand Spike From Indoor Vertical Farming Fixtures | +0.7% | North America and Europe controlled-environment agriculture, Asia-Pacific urban farms | Long term (≥ 4 years) |

| Expansion of UV-C High-Power LED Adoption in Disinfection | +0.6% | Global healthcare and water treatment, accelerated in North America and Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Decline in USD per Lumen for High-Power Packages

Manufacturing scale, 95% wafer yields, and process automation have pushed street prices for 3 W packages below USD 0.50 in bulk lots, tipping municipal tenders in favor of LEDs even under strict payback rules.[1]GRE Alpha, “LED Lighting Technology Trends 2026: Market Forces Driving Industry Innovation,” grealpha.com Laboratory prototypes already exceed 200 lm/W and commercial modules routinely deliver 140-160 lm/W at junction temperatures under 85 °C, trimming heatsink mass and simplifying fixture design. [2]Benwei Lighting, “EU Ecodesign Directive (ERP) Requirements for LED Lights,” benweilight.com China’s monthly output of 17.48 million gallium-nitride chips exerts downward price pressure worldwide, yet Kinglight Optoelectronics’ January 2026 price increase signals that margins may have reached a structural floor where future cost cuts hinge on new substrates or phosphor chemistry. The sliding cost per lumen broadens the addressable market from street lighting to sports arenas and seaport illumination, fast-tracking the retirement of high-intensity discharge incumbents and reinforcing efficiency mandates.

Government-Mandated Phase-Out of HID Streetlights

The United States BRIGHT Act and the April 2024 Department of Energy rules require 120 lm/W efficacy for general service lamps by July 2028, while Washington State bans non-compliant metal-halide fixtures from 2026. California municipalities, armed with utility rebates, are front-loading conversions ahead of the federal deadline, and parallel measures in Europe raise the bar to 160 lm/W for non-directional sources. These policies specify 50,000-hour L70 ratings plus IP66 ingress protection, conditions that steer procurement toward multi-die surface-mount and chip-on-board packages capable of spreading thermal load and surviving outdoor environments. India’s Production Linked Incentive scheme, worth INR 6,238 crore (USD 750 million), further supports domestic packaging and export supply into Southeast Asia and the Middle East.

Automotive Shift to Solid-State Headlamps and ADB

Europe represented a significant share of adaptive driving beam volume in 2025 as premium sedans and sport-utility vehicles adopted matrix headlamps with 100-200 addressable dies per module. Pixel-LED designs under development by LG Innotek shrink die footprint to 2 mm × 2 mm, enabling fine-grained beam control and exterior display messaging. The CES 2026 Innovation Award-winning Ultra Thin Pixel Lighting Module delivers 30% higher luminous efficiency alongside a 71% reduction in thickness, attributes that improve pedestrian safety and aerodynamic drag. Automotive qualification under AEC-Q102 demands -40 °C to +150 °C thermal cycling, vibration, and humidity stress, effectively limiting the supplier pool to firms with dedicated automotive-grade lines and test infrastructure, yet rewarding those capable of meeting color-bin tightness within a three-step MacAdam ellipse over 10-plus years of service.

Proliferation of Smart Lighting Controls Requiring High-Current LEDs

California’s Title 24-2025, effective January 2026, compels daylight-responsive controls, multi-level switching, and automated shut-off in commercial buildings. High-current LEDs driven at 700-1,000 mA reduce die count per fixture, easing driver circuit complexity when paired with 0-10 V, DALI, or Bluetooth Low Energy interfaces. GRE Alpha’s collaboration with Japan Display Inc. integrates drivers with liquid-crystal beam-control films that alter the distribution on two axes without moving parts, as proven in the March 2025 refit of the Tottori Prefectural Museum of Art. Smart-city pilots leverage cloud analytics fed by per-fixture telemetry to schedule maintenance and thin out emergency truck rolls, locking in preference for packages that embed temperature sensors and I²C reporting.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Thermal Management Complexity at ≥10 W Junction Power | -0.9% | Global, especially Middle East, Southeast Asia and India | Short term (≤ 2 years) |

| Price Compression From China-Based Overcapacity | -0.7% | Global, sharpest in Asia-Pacific, margin squeeze in North America and Europe | Short term (≤ 2 years) |

| IP Barriers on Flip-Chip and CSP Processes | -0.4% | Global, licensing friction in North America and Europe | Medium term (2-4 years) |

| Supply Risk of High-Purity Gallium and Rare-Earth Phosphors | -0.5% | Global supply chain with Chinese processing concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Thermal Management Complexity at ≥10 W Junction Power

Packages operating above 10 W dissipate 3-5 W of heat inside footprints often under 10 mm × 10 mm, pushing junction temperatures toward 125 °C, where lumen depreciation accelerates, and chromaticity drifts.[3]Dinesh Kumar Patel and Vipin Kumar Sharma, “Illuminating Innovations: A Comprehensive Review of Rare-Earth-Doped Phosphors and Their Applications in LEDs,” Transactions of the Indian Institute of Metals, doi.org In regions where ambient temperatures exceed 40 °C, horticultural fixtures and UV-C modules must use insulated metal substrates with a thermal conductivity of 2 W m⁻¹ K or higher, micro-channel liquid plates, or thermoelectric coolers, each adding USD 5-10 per unit. Bridgelux and peers mitigate hot spots by spreading multiple dies across ceramic carriers, lowering peak junction temperatures by 15-20 °C but raising material costs and assembly complexity. Retrofit housings introduce additional constraints because legacy form factors cannot always accommodate larger heatsinks, elevating recall and liability risk if thermal runaway occurs.

Price Compression from China-Based Overcapacity

China’s 17.48 million-chip monthly output dwarfs domestic consumption, forcing exports that undercut rival suppliers. Sustained equipment subsidies and vertically integrated phosphor lines exacerbate oversupply, pushing average selling prices downward until mid-tier competitors' profit margins vanish. San’an Optoelectronics’ August 2025 agreement to purchase Lumileds for USD 239 million exemplifies the consolidation wave driven by cost pressure, while Kinglight Optoelectronics’ January 2026 price hike underscores that industry economics may have hit a floor. Suppliers lacking wafer capacity or exclusive IP are pivoting to UV-C and horticulture niches where specialized wavelengths and higher qualification hurdles anchor premium price points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: Specialty Demand Fuels the Above-10 W Tier

The 1-3 W bracket accounted for 47.80% of revenue in 2025, underpinned by general-purpose retrofits, commercial downlights, and residential fixtures that align with established drivers and optics. Meanwhile, the 3-10 W segment supports industrial high-bay luminaires and urban streetlights that require elevated lumen density and robust thermal performance. Above-10 W packages, though niche in volume, are forecast to advance at 7.11% through 2031 as vertical farms specify photosynthetic photon flux densities above 1,500 µmol m⁻² s⁻¹ and healthcare operators adopt 265-280 nm UV-C sources for germicidal duty cycles. These high-current modules must survive 50,000-hour L70 ratings inside enclosures where ambient temperatures often exceed 35 °C. Consequently, vendors emphasize ceramic substrates, copper cores, and in-package thermistors that modulate current to prevent thermal runaway.

Thermal management defines the engineering ceiling in this tier because passive heatsinks cannot always maintain sub-100 °C junction temperatures in hot climates. Suppliers offer chip-on-board layouts that distribute dies across broader surfaces, plus optional liquid microchannels or phase-change substrates for extreme environments. Across general lighting, the High-Power LED Package market size in the 1-3 W range benefits from commoditization, yet margin protection becomes increasingly elusive as street prices dip below USD 0.50 per device. Conversely, the above-10 W class commands premium pricing thanks to application-specific wavelengths and lifetime guarantees, enabling vendors to preserve profitability even when unit sales stay modest.

By Architecture: Chip-On-Board Narrows the Gap with Single-Die Staples

Single-die surface-mount packages retained the largest 36.29% slice of 2025 revenue because standardized footprints like 2835 and 5050 ensure drop-in compatibility with legacy optics and drivers. These packages underpin commodity bulbs, tubes, and retrofit kits, but they face share erosion as fixture designers crave slimmer profiles and smoother beam patterns. Multi-die surface-mount devices combine two to four chips to increase lumen output without increasing board space, serving floodlights and high-bay fixtures where drive currents are higher.

Chip-on-board solutions, growing at 6.85% through 2031, populate automotive headlamps and architectural grazers that demand uniform light fields and micron-level alignment tolerances. LG Innotek’s Ultra Thin Pixel Lighting Module exemplifies this push by replacing plastic lenses with white silicone reflectors, boosting package efficiency by 30% and cutting thickness to 0.12 inches. Automotive OEMs value COB designs because they accommodate 100-200 addressable dies inside a single module, simplifying thermal paths and electrical routing while enabling dynamic beam shaping. The High-Power LED Package market share for chip-on-board is therefore set to climb steadily as premium lighting applications prioritize optical homogeneity and styling freedom.

By Application: Automotive Leads Growth Amid Regulatory Lighting Retrofits

General lighting accounted for 38.70% of 2025 revenue as efficacy mandates swept incandescent and compact fluorescent products from shelves. Retrofit lamp and street-light orders dominate volumes but yield modest margins given intense price competition. Automotive lighting, however, is on course for a 6.70% CAGR to 2031, fueled by adaptive driving beam platforms, pixel headlamps, and 3D grille illumination that harness hundreds of micro-LEDs for safety and design differentiation. Tight binning, AEC-Q102 longevity, and -40 °C to +150 °C cycling specifications erect entry barriers that shield pricing power.

Display backlighting remains a mature outpost, though the adoption of mini-LED and micro-LED in tablets, monitors, and televisions is renewing demand for smaller die sizes and tighter tolerances. Specialty niches such as UV-C disinfection and horticulture offer double-digit growth, leveraging narrow spectral bandwidths and robust lifetime guarantees that justify above-average average selling prices. As a result, suppliers that command holistic epitaxial control and proprietary phosphor blends secure defensible positions in these segments while leveraging shared die platforms to service mainstream markets.

Geography Analysis

Asia-Pacific accounted for 68.60% of global revenue in 2025 and is projected to grow at 7.20% through 2031 on the back of infrastructure buildouts, domestic stimulus, and an outsized manufacturing base spanning epitaxial wafers to phosphors. China controls 98% of gallium refining capacity and 85% of europium processing, a concentration that exposes the global supply chain to sudden policy shifts or plant outages. India’s Production Linked Incentive worth INR 6,238 crore (USD 750 million) underwrites new packaging lines intended for local street-lighting conversions and exports across South Asia and the Middle East. Japan maintains leadership in flip-chip intellectual property and commands premium pricing in automotive OEM supply, thanks to vendors like Nichia and Citizen.

North America and Europe together account for roughly one-quarter of total demand, with their trajectories tightly linked to regulatory pressure and smart-building investments. The United States will enforce 120 lm/W efficacy in general service lamps by July 2028, and California’s January 2026 Title 24 code embeds telemetry obligations that favor packages with integrated sensors and BLE radios. Europe’s proposed Stage 4 Ecodesign targets 160 lm/W for non-directional lamps, a benchmark that compels co-design of thermal substrates and high-frequency drivers capable of sustaining current pulses without undermining L70 lifetime.

South America, the Middle East, and Africa trail in absolute numbers yet record step-change growth as municipal planners embrace LED conversions powered by concessional finance from multilateral banks. Off-grid solar lanterns and hybrid streetlights require 700-1,000 mA drive currents and IP66 or higher ingress protection to survive dust-laden, high-temperature climates, channeling demand toward high-power packages with robust solder-joint reliability. Regional diversification strategies are accelerating: Taiwanese and South Korean vendors are investing in Thailand and Vietnam assembly lines to sidestep single-country risk, while the United States and European Union have earmarked USD 3.2 billion and EUR 2.8 billion (USD 3.16 billion) respectively for domestic gallium and rare-earth processing plants that aim to dent China’s near-monopoly within five years.[4]Linda R. Rowan, “Critical Mineral Resources: National Policy and Critical Minerals List,” congress.gov

Competitive Landscape

The top five suppliers, Nichia, ams OSRAM, Samsung Electronics, Lumileds, and Seoul Semiconductor, collectively hold a significant share of revenue in 2025, a level that classifies the sector as moderately concentrated. Cross-licensing is reshaping competitive lines: the October 2025 agreement between Nichia and ams OSRAM broadens industry access to flip-chip and chip-scale packages used in matrix headlamps, potentially opening the premium automotive tier to additional licensees. San’an Optoelectronics’ pending USD 239 million acquisition of Lumileds deepens Chinese vertical integration from wafer to module and pairs Western customer channels with low-cost epitaxial infrastructure.

Technology differentiation is migrating from raw efficacy to system integration. LG Innotek bundles ultra-thin silicone optics, vehicle-to-everything communication, and driver-embedded diagnostics into modules aimed at generating USD 691 million in automotive lighting sales by 2030. GRE Alpha, through a partnership with Japan Display Inc., offers driver boards paired with liquid-crystal beam-shape films that enable silent, motorless beam steering for galleries and retail. Smaller specialists such as Crystal IS carve niches in deep-UV chips for water disinfection, while Bridgelux tailors red-blue co-packs for photosynthesis optimization. Amid oversupply, mid-tier firms are retreating from commodity general lighting toward these higher-margin verticals or seeking consolidation to reach economies of scale.

Compliance costs also tilt the field. Europe’s EPREL database and documentation burden favor manufacturers with certified laboratories, prompting startups to partner with contract test houses or pursue markets outside the European Economic Area.

High-Power LED Package Industry Leaders

Nichia Corp.

OSRAM Opto Semiconductors GmbH

Samsung Electronics Co., Ltd. (LED BU)

Cree LED Inc.

Lumileds Holding B.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: LG Innotek showcased its Nexlide automotive lighting range at the DVN Lighting Workshop in Munich, unveiling 2 mm × 2 mm pixel LEDs and 3D multi-effect modules that aim to capture USD 691 million in automotive lighting revenue by 2030.

- January 2026: Kinglight Optoelectronics raised prices across its LED package catalog after prolonged deflation to restore research and development funding and bolster margins.

- November 2025: LG Innotek won a CES 2026 Innovation Award for its Ultra-Thin Pixel Lighting Module, reporting 30% higher luminous efficiency and 71% reduced thickness versus plastic-lens designs.

- October 2025: Nichia and ams OSRAM entered a cross-license covering LED packages and modules for automotive matrix headlamps, lowering intellectual property barriers for flip-chip solutions.

Global High-Power LED Package Market Report Scope

The High-Power LED Package Market Report is Segmented by Power Range (1W-3W, 3W-10W, and Above 10W), Architecture (Single-die Packages, Multi-die Packages, COB, and Other Architectures), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

| 1W - 3W |

| 3W - 10W |

| Above 10W |

| Single-die Packages (SMD / Discrete) |

| Multi-die Packages (SMD) |

| COB (Chip-on-Board) |

| Other Architecture (CSP, Flip-chip, Hybrid modules) |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Southeast Asia | |

| Rest of Asia-Pacific | |

| South America | |

| Middle East and Africa |

| By Power Range | 1W - 3W | |

| 3W - 10W | ||

| Above 10W | ||

| By Architecture | Single-die Packages (SMD / Discrete) | |

| Multi-die Packages (SMD) | ||

| COB (Chip-on-Board) | ||

| Other Architecture (CSP, Flip-chip, Hybrid modules) | ||

| By Application | General Lighting | |

| Automotive Lighting | ||

| Display and Backlighting | ||

| Specialty / Niche | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Southeast Asia | ||

| Rest of Asia-Pacific | ||

| South America | ||

| Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the High-Power LED Package market in 2031?

The market is forecast to reach USD 5.95 billion by 2031, expanding at a 5.76% CAGR during 2026-2031.

Which power range currently accounts for the largest share of sales?

Packages rated at 1-3 W led with a 47.80% revenue share in 2025 because they align with general lighting retrofits and standard driver platforms.

Why are chip-on-board architectures growing faster than single-die packages?

Automotive headlamps and architectural fixtures demand uniform light fields and thin profiles that chip-on-board designs provide, boosting their forecast CAGR to 6.85%.

How will new efficacy regulations shape demand in North America?

United States rules requiring 120 lm/W efficacy by Jul 2028 will accelerate the retirement of fluorescent and high-intensity discharge lamps, driving retrofit orders toward LED packages that comply.

What supply-chain risks affect phosphor availability?

85% of europium processing occurs in a handful of Chinese plants, so any disruption or export control can halt phosphor shipments worldwide within weeks.

Which applications are expected to post the fastest growth through 2031?

Automotive lighting, UV-C disinfection, and vertical-farming fixtures are projected to advance faster than general lighting as they integrate high-density dies, specialty wavelengths, and dynamic control features.

Page last updated on: