North America Mid-Power LED Package Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

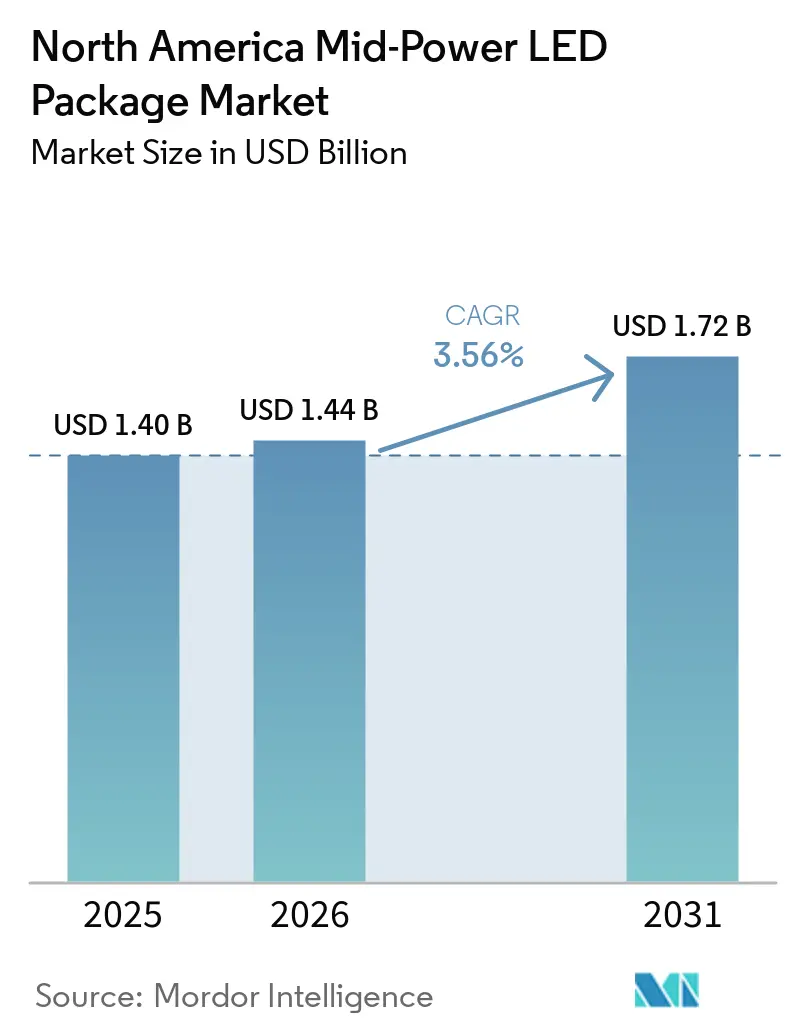

| Base Year Market Size (2025) | USD 1.40 Billion |

| Market Size (2026) | USD 1.44 Billion |

| Market Size (2031) | USD 1.72 Billion |

| Growth Rate (2026 - 2031) | 3.56% CAGR |

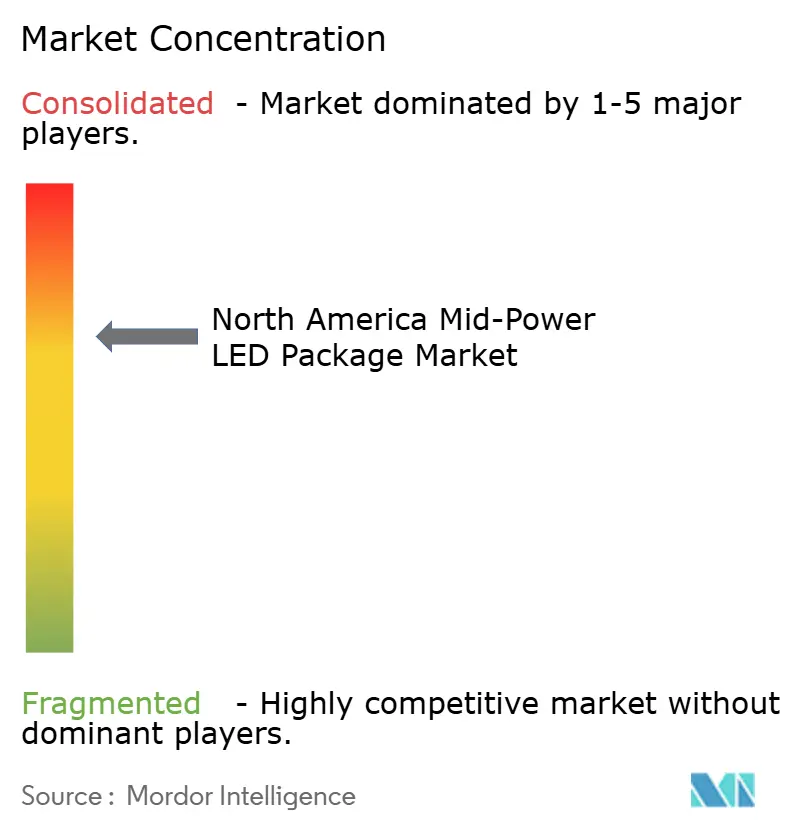

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Mid-Power LED Package Market Analysis by Mordor Intelligence

The North America mid-power LED package market size is projected to expand from USD 1.40 billion in 2025 and USD 1.44 billion in 2026 to USD 1.72 billion by 2031, registering a CAGR of 3.56% between 2026 to 2031. Maturing general-lighting retrofits now advance alongside faster-growing automotive, horticulture, and human-centric applications that make better use of mid-power cost-per-lumen economics. Specifiers continue to center designs on the 0.5 W-to- Less Than 1 W class because it balances efficacy, thermal simplicity, and driver compatibility. SMD form factors still dominate shipments, yet flip-chip CSPs are gaining momentum in headlamps and slim architectural fixtures, where lower profiles and higher luminance justify a premium. Nearshoring module assembly to Mexico shortens lead times and lowers landed costs, giving regional OEMs a hedge against Asia-centric supply risks and disruptions to rare-earth materials.

Key Report Takeaways

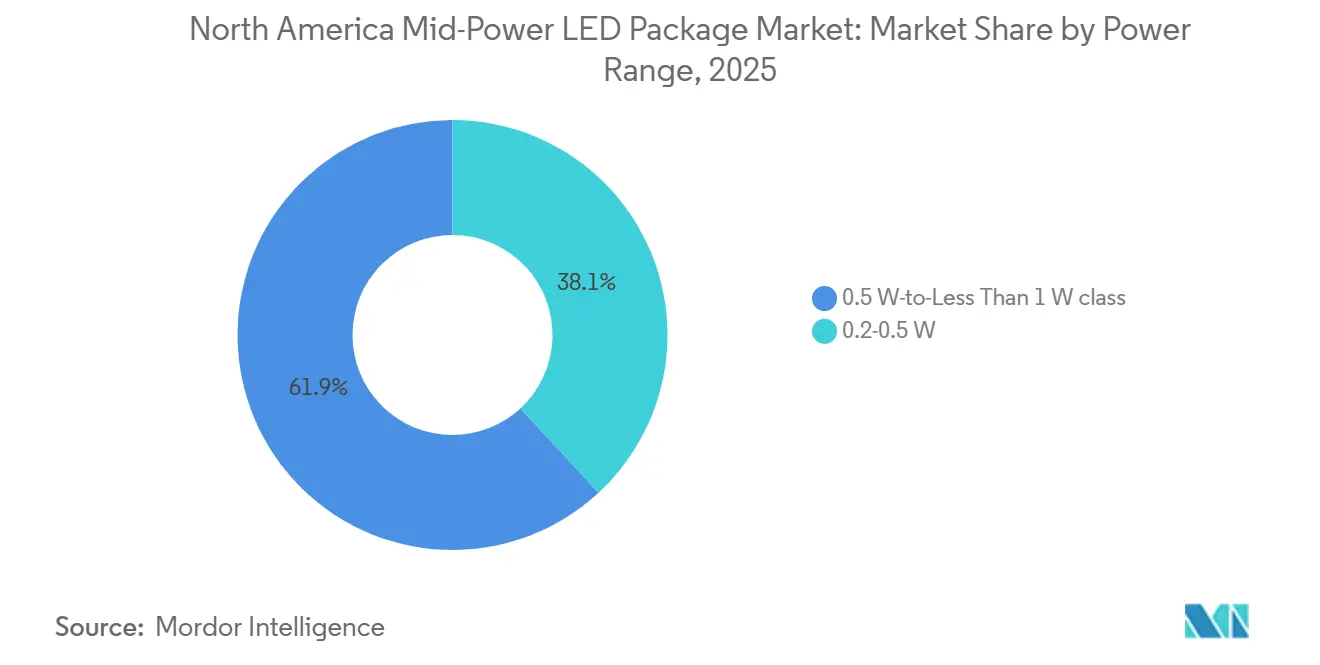

- By power range, the 0.5 W-to- Less Than 1 W class captured 61.88% of the North America mid-power LED package market share in 2025 and is forecast to record the fastest 3.96% CAGR through 2031.

- By package architecture, SMD devices led with 73.49% revenue share in 2025, and CSP is projected to grow at the highest 4.11% CAGR to 2031.

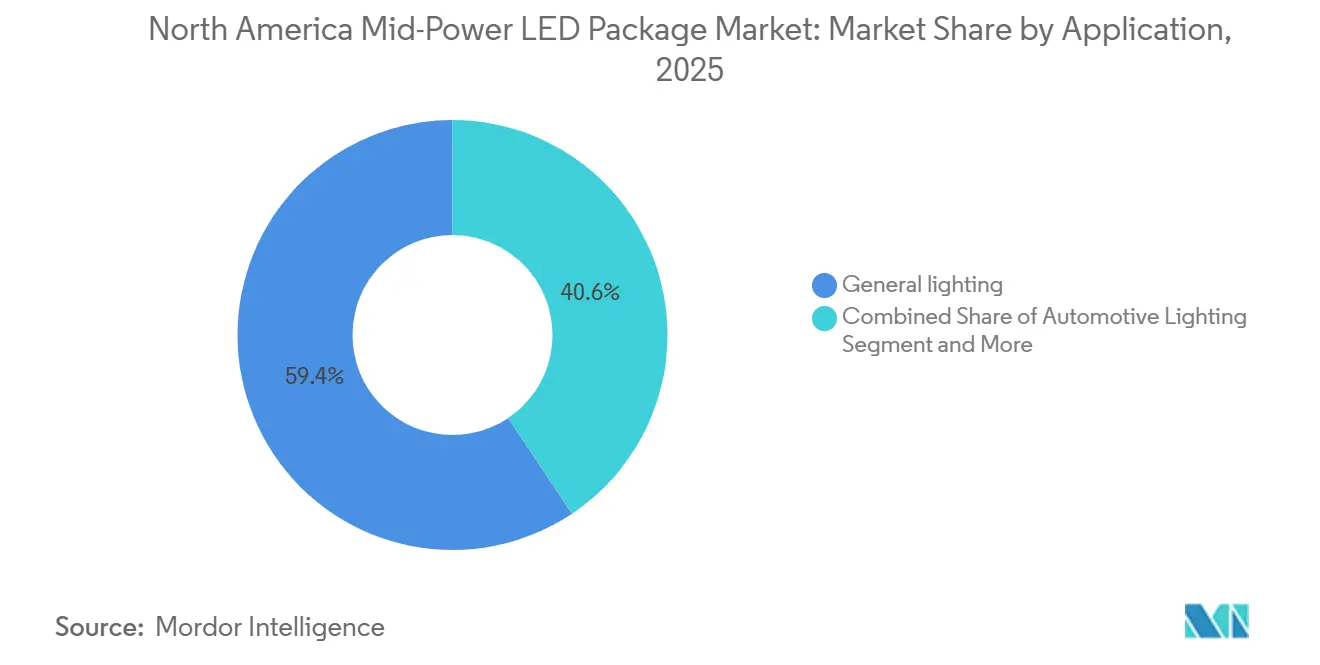

- By application, general lighting held a 59.39% share of the North America mid-power LED package market in 2025, and automotive lighting is advancing at a 4.37% CAGR during 2026-2031.

- By geography, the United States accounted for 88.84% of 2025 revenue, and Canada represents the fastest regional growth at a 3.31% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

North America Mid-Power LED Package Market Trends and Insights

Drivers Impact Analysis*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Alignment of Automotive LED Standards | +1.0% | United States and Canada (FMVSS 108, TSD 108 alignment), Mexico (Tier-1 nearshoring investments) | Medium term (2–4 years) |

| Wave of Energy-Efficient Building Codes | +0.8% | United States (California Title 24, IECC 2024, New York, Oregon), Canada (provincial codes tied to ASHRAE 90.1-2022) | Short term (≤ 2 years) |

| Continued Drop in Mid-Power LED Chip Costs | +0.6% | North America (import-driven price pressure, Mexico assembly savings, competitive Asian sourcing) | Short term (≤ 2 years) |

| Broader Utility Rebates For Mid-Power Fixtures | +0.5% | United States (Georgia, Texas, Midwest, California), Canada (provincial utility incentives) | Short term (≤ 2 years) |

| Growing Use of LEDs in Vertical-Farm Horticulture | +0.4% | United States (urban farms, legalized-state cannabis), Canada (controlled-environment agriculture) | Medium term (2–4 years) |

| Uptick In Tunable-White, Human-Centric Lighting | +0.2% | United States (premium office retrofits, WELL-certified projects in major metros) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Standardization of Automotive LED Requirements

Transport Canada TSD 108 Revision 8 became mandatory in October 2025, aligning the photometric and durability rules with U.S. FMVSS 108. Tier-1 suppliers now engineer a single module platform for the continent, and that platform predominantly specifies arrays of 0.5 W to 0.8 W mid-power packages, which spread heat more evenly than sparse high-power clusters.[1]Transport Canada, “TSD 108 Revision 8,” tc.canada.ca NHTSA’s refusal in 2024 to relax adaptive-beam glare thresholds reinforces the need for high-density arrays that maintain uniform luminance across complex optics. SAE J1889 added accelerated thermal-cycling tests in April 2025, favoring lower-junction-temperature mid-power packages. Mexico’s February 2026 automotive strategy signals future approvals for matrix and sequential functions, further increasing device count per vehicle. Together, the harmonized requirements expand demand for mid-power LEDs in signal, DRL, and adaptive systems.

Surge In Energy-Efficient Building Codes

California Title 24-2025 lowered lighting power densities by up to 15%, effective January 2026, while IECC 2024 calls for continuous dimming to 10% and broader occupancy sensing in cities that adopted the code in 2026. Oregon’s 2026 Residential Specialty Code and New York City’s 2025 Energy Conservation Code add similar controls, shortening retrofit paybacks to as little as 12-18 months in high-use spaces. Because mid-power packages integrate seamlessly with legacy constant-current drivers, contractors can reuse wiring and minimize downtime, thereby accelerating project approvals. Utilities in the Midwest and Southeast continue to offer rebates of USD 30-80 per DLC-qualified luminaire, and most of those fixtures use 2835 or 3030 mid-power LEDs. Collectively, stricter codes and rebate economics sustain high retrofit volumes despite plateauing first-wave conversions.

Declining Cost of Mid-Power LED Chips

Manufacturing yields above 95% and efficacy levels of 150-200 lm/W let suppliers cut die counts per fixture while maintaining target lumen output, driving device prices down 5% quarter-over-quarter in late 2025. China supplies a significant share of global packaged LEDs, and its scale advantage allows aggressive spot pricing that pulls retrofit contractors away from premium Japanese and Korean brands. Labor costs in Mexico sit 50-60% below U.S. averages, and tariff-free North American Free Trade Agreement provisions remove 15-25% of landed costs versus Asian imports once inventory carrying costs are considered. Foxconn and Flex both expanded Mexican capacity in 2025, underscoring confidence in regional cost competitiveness. These structural savings improve fixture margins and help offset rare-earth–driven phosphor inflation.

Rapid Expansion of Horticulture Lighting in Vertical Farms

USDA data show greenhouse operations increased by 55% between 2020 and 2023, with the vertical-farm market value reaching USD 4.8 billion in 2024.[2]U.S. Department of Agriculture, “Greenhouse and Nursery Survey 2023,” usda.gov Cannabis legalization in additional states is stimulating demand for layered cultivation racks that increase the number of luminaires per square foot, each fixture often running mid-power LEDs at 0.3 W to 0.6 W to ensure uniform canopy coverage. Because growers swap lighting every 5 to 7 years to chase higher photon efficacy, the replacement cycle remains brisk compared to office lighting. Suppliers able to offer tuned spectra red-blue or full-spectrum white capture additional value through seedling health gains and faster crop turns.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Price Pressure From Low-Cost Asian Imports | -0.6% | United States, Canada, Mexico | Short term (≤ 2 years) |

| Thermal Management Challenges Above 1 W Ceiling | -0.4% | North America | Medium term (2–4 years) |

| Supply Chain Vulnerability For Phosphor Materials | -0.3% | North America | Medium term (2–4 years) |

| Slow Retrofit Cycle in Commercial Real Estate Segment | -0.2% | United States | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Vulnerability for Phosphor Materials

China’s rare-earth export curbs in April and October 2025 placed europium, terbium, and yttrium under license, driving multi-fold price spikes in non-Chinese spot markets.[3]TD Economics, “Implications of China’s Rare-Earth Export Controls,” td.com U.S. yttrium imports collapsed from 333 t to 17 t within eight months, and stopgap stockpiles can cover only one to two quarters of LED phosphor demand. A negotiated one-year suspension defers full enforcement to November 2026, yet the episode spotlighted single-source risk, prompting OEMs to request dual-supply certification or non-rare-earth phosphor roadmaps.

Slow Retrofit Cycle in Commercial Real Estate Segment

Class B and C office landlords frequently face split-incentive barriers, in which tenants pay utility bills while owners shoulder capital upgrades. With high-vacancy rates persisting in several U.S. metros, many landlords are postponing retrofit expenditures despite shorter paybacks, dragging the long-tail retrofit pipeline beyond the forecast window.[4]Building Owners and Managers Association, “Split Incentive Barriers in Office Retrofits,” boma.org Utility rebate budgets also fluctuate year to year, adding uncertainty for contractors that specialize in turnkey lighting upgrades.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Range: 0.5 W-to- Less Than 1 W Consolidates Market Leadership

Commercial retrofits and automotive signal lamps together propelled the 0.5 W-to-Less Than 1 W class to a 61.88% share in 2025, the highest in the North America mid-power LED package market. That weight reflects steady gains in efficacy that let designers hit lumen targets with fewer diodes, reducing pick-and-place steps and driver channel counts. Moving to the next forecast period, the same class is forecast to grow at a 3.96% CAGR, outperforming both lower-wattage and near-1 W classes as OEMs converge on this sweet spot for thermal reliability.

Fixture makers migrated from 0.2 W to 0.5 W devices toward the mid-range as Title 24 and IECC constraints tightened, as higher-wattage packages allow slimmer boards and simpler controls. Automotive Tier-1 suppliers enlarged DRL and matrix arrays with 0.6 W-to-0.8 W emitters after SAE revised thermal-cycling tests, confirming reliability under vibration.[5]SAE International, “J1889 LED Signal Lamp Performance Requirements,” sae.org

By Package Architecture: SMD Dominates, CSP Climbs

SMD formats such as 2835 and 3030 held 73.49% of 2025 revenue thanks to entrenched SMT equipment, decades of IEC footprint standardization, and wide availability from low- to premium-grade vendors. These packages sit at the heart of most DesignLights Consortium-listed luminaires, tying them tightly to retrofit incentive programs. In turn, the North America mid-power LED package market size for SMD is expected to expand steadily alongside the commercial build-out of smart-ready luminaires.

CSP shipments start from a smaller base yet carry a higher 4.11% CAGR to 2031 as flip-chip, lead-frame-free construction meets automotive height and thermal targets. Seoul Semiconductor’s WICOP UHL headlamp win on the 2024 Genesis GV80 demonstrated tangible luminance and heat-sink savings, sparking broader OEM interest. As CSP die-attach yields improve and capital amortizes, price gaps with mainstream SMDs narrow, paving the way for adoption in premium architectural downlights that crave slim bezels.

By Application: General Lighting Rules, Automotive Accelerates

General lighting retained a dominant 59.39% slice of 2025 revenue as utility rebates and stricter state codes funneled projects toward DLC-qualified troffers, panels, and area lights. Specifiers favor mid-power packages because they integrate with familiar 0-10 V or DALI drivers, keeping installation risk low when retrofitting occupied spaces. Title 24-driven demand in California, plus IECC uptake nationwide, anchors the base load of the North America mid-power LED package market across the forecast.

Automotive lighting outpaces all other applications with a 4.37% CAGR to 2031. NHTSA’s adaptive-beam approval unlocked mainstream matrix headlamps that need 20-40 individually addressable mid-power LEDs each, far more than static halogen or HID predecessors. Transport-Canada harmonization and Mexico’s supplier localization multiply the pull on regional package output, pushing device counts higher even as per-unit prices drift lower with CSP penetration.

Geography Analysis

The United States accounts for 88.84% of 2025 revenue due to its vast commercial floor area, deep rebate programs, and large domestic auto output. California, Oregon, and New York City together account for a significant share of floor-space-driven retrofits, and each jurisdiction now mandates continuous dimming or lower power densities, creating multi-year retrofit backlogs. Detroit-adjacent assembly plants source growing volumes of mid-power signal and DRL modules as model-year 2026 platforms migrate to all-LED exterior lighting.

Canada, while smaller, posts a healthy 3.31% CAGR through 2031 on the back of transport code harmonization that expands automotive LED content and provincial code tightening that raises retrofit urgency in Toronto, Vancouver, and Montréal. Magna International’s Queretaro expansion, although located in Mexico, serves both Canadian and U.S. OEM programs, reinforcing continental supply chains.

Mexico functions mainly as a manufacturing hub, benefiting from USD-denominated foreign direct investment, such as LG Innotek’s MXN 3.5 billion (USD 197 million) Querétaro plant and Excellence Optoelectronics’ Phase 1 module line, which starts production in July 2026. Domestic consumption still trails its neighbors, yet municipal street-lighting retrofits in Mexico City and Guadalajara keep a baseline demand that absorbs locally produced packages.

Competitive Landscape

Nichia, Citizen, and Toyoda Gosei defend design wins within established automotive platforms through long-term agreements that lock in mid-power emitters for entire vehicle generations. Seoul Semiconductor and LG Innotek leverage vertical integration and sizeable patent portfolios to win adaptive headlamp sockets that prize luminance density. Chinese and Taiwanese challengers such as NationStar, Hongli Zhihui, and Everlight undercut pricing in retrofit channels, forcing incumbents to bundle extended warranties and photometric testing services.

Everlight intensified litigation by filing a February 2026 patent suit against Seoul Semiconductor over flip-chip packaging, signaling that intellectual-property enforcement is a critical lever to slow price erosion. Cree's LED OptiLamp launch with on-chip drivers aligns with a strategic shift to smart-lighting ecosystems, bundling silicon and firmware to capture value in commercial retrofits.

Bridgelux courts OEMs that want domestic supply resilience by coupling its Fremont headquarters with CSP modules qualified to DesignLights Consortium premium grades. Suppliers eye nearshoring to Mexico for just-in-time deliveries, yet must still clear IATF 16949 and AEC-Q102 bars before penetrating high-reliability automotive lines.

North America Mid-Power LED Package Industry Leaders

Nichia Corporation

Lumileds Holding B.V.

Cree LED Inc.

Samsung Electronics Co., Ltd.

Seoul Semiconductor Co., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Cree LED unveiled OptiLamp LEDs with embedded driver and 24-bit pixel control during ISE 2026, simplifying smart-ready fixture architecture.

- February 2026: Everlight Electronics filed a U.S. patent infringement suit against Seoul Semiconductor, alleging WICOP HF modules violate flip-chip packaging IP.

- December 2025: Samsung Electronics expanded its Micro RGB TV range for 2026, featuring sub-100 µm LEDs for 100% BT.2020 color with VDE certification.

- March 2025: Seoul Semiconductor introduced SunLike full-spectrum LEDs at JAPAN SHOP 2025, citing studies on eye-health benefits.

North America Mid-Power LED Package Market Report Scope

The North America Mid-Power LED Package Market Report is Segmented by Power Range (0.2-0.5 W and 0.5- Less Than 1 W), Package Architecture (SMD including 2835, 3014, 3030, Others and CSP), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty/Niche), and Country (United States, Canada and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

| 0.2-0.5 W |

| 0.5- Less Than 1 W |

| SMD (Surface Mount Device) | 2835 |

| 3014 | |

| 3030 | |

| Others (3528, 3020, 5050, etc.) | |

| CSP (Chip Scale Package) |

| General Lighting |

| Automotive Lighting |

| Display and Backlighting |

| Specialty / Niche |

| United States |

| Canada |

| Mexico |

| By Power Range | 0.2-0.5 W | |

| 0.5- Less Than 1 W | ||

| By Package Architecture | SMD (Surface Mount Device) | 2835 |

| 3014 | ||

| 3030 | ||

| Others (3528, 3020, 5050, etc.) | ||

| CSP (Chip Scale Package) | ||

| By Application | General Lighting | |

| Automotive Lighting | ||

| Display and Backlighting | ||

| Specialty / Niche | ||

| By Country | United States | |

| Canada | ||

| Mexico | ||

Key Questions Answered in the Report

What is the projected value of the North America mid-power LED package market by 2031?

It is expected to reach USD 1.72 billion by 2031.

Which power class holds the largest share of shipments?

Packages rated 0.5 W-to- Less Than 1 W commanded 61.88% of 2025 revenue.

Why are CSP devices growing faster than traditional SMD packages?

Automotive headlamps and slim architectural fixtures need the higher luminance, lower profile, and better thermal paths that flip-chip CSP provides.

How will new building codes influence demand?

Stricter power densities, mandatory dimming, and occupancy sensors in IECC 2024 and Title 24-2025 compress retrofit paybacks to under 3 years, enabling sustained fixture upgrades.

Which country is the fastest-growing market within the region?

Canada shows a 3.31% CAGR through 2031, driven by transport code harmonization and provincial energy-code updates.

What is the main supply-chain risk for LED phosphors?

Dependence on Chinese exports of europium, terbium, and yttrium exposes U.S. and Canadian suppliers to potential shortages and price spikes.

Page last updated on: