Aseptic Co-Packing Services Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

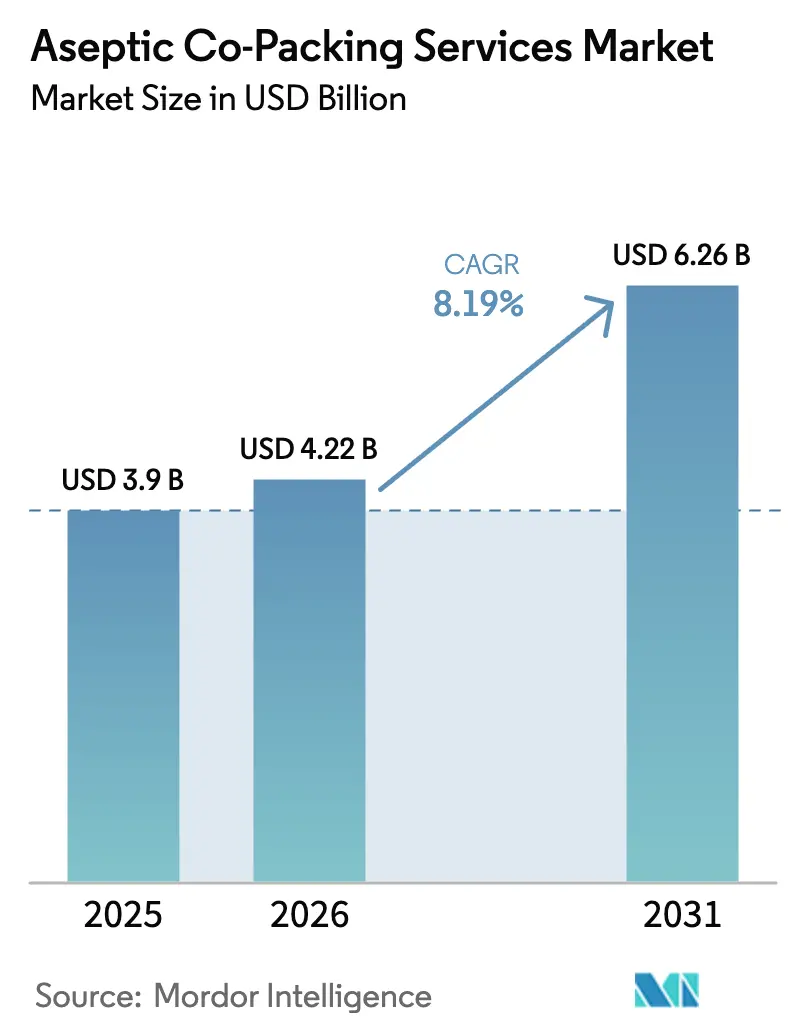

| Market Size (2026) | USD 4.22 Billion |

| Market Size (2031) | USD 6.26 Billion |

| Growth Rate (2026 - 2031) | 8.19% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

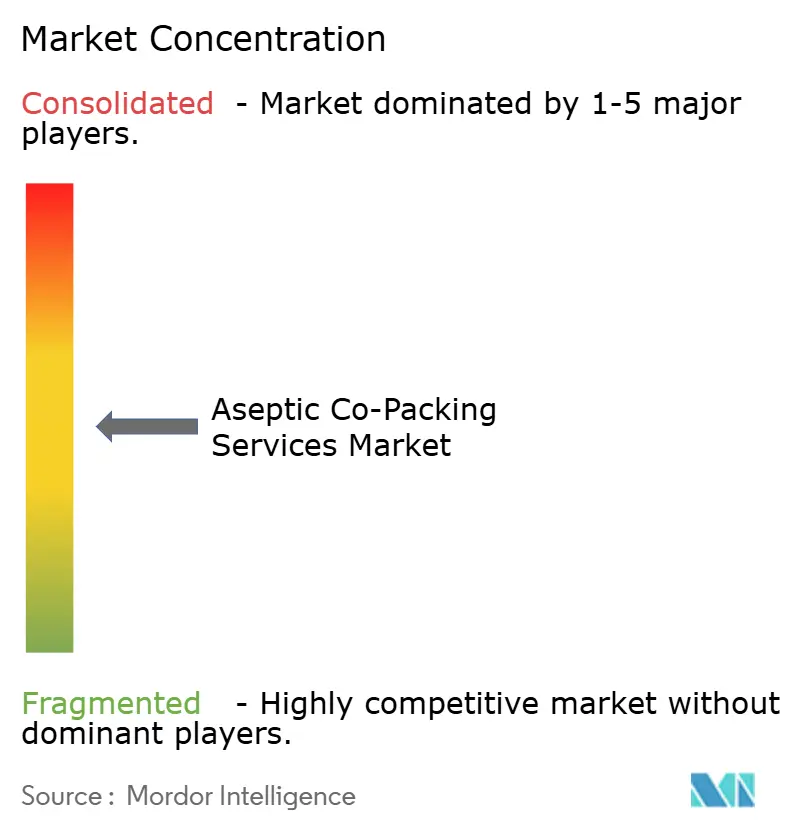

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aseptic Co-Packing Services Market Analysis by Mordor Intelligence

The aseptic co-packing services market size is expected to grow from USD 3.90 billion in 2025 to USD 4.22 billion in 2026 and is forecast to reach USD 6.26 billion by 2031 at 8.19% CAGR over 2026-2031. Growth accelerates as brand owners favor outsourcing over in-house capital projects, largely because contract specialists navigate stringent sterile-pack validation more efficiently. Regulatory convergence among the U.S. Food and Drug Administration, the European Commission, and Asia-Pacific authorities elevates global demand for proven aseptic expertise. Rising clean-label beverage launches, expanding functional-food portfolios, and automation-led cost savings further reinforce the aseptic co-packing services market outlook. Price-competitive Asian facilities pressure North American and European operators to differentiate themselves through premium segments and integrated logistics, while material innovations in barrier plastics and recyclable paperboard open new packaging avenues.

Key Report Takeaways

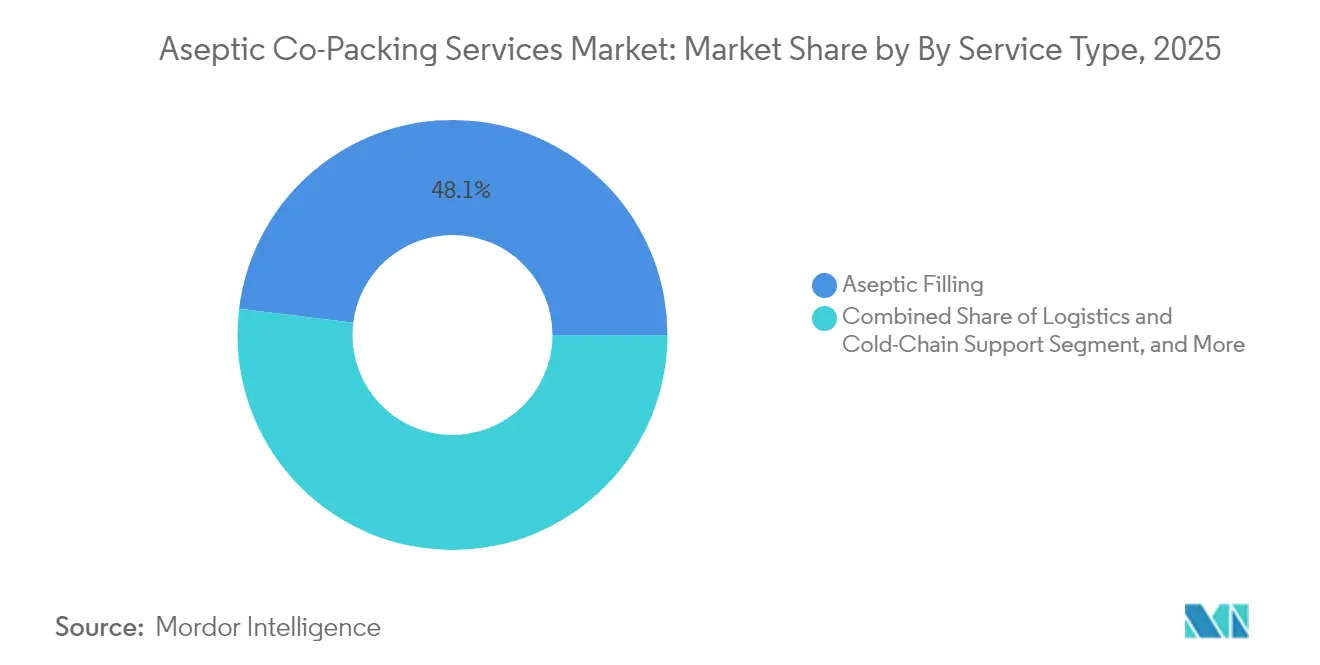

- By service type, aseptic filling captured 48.05% of the aseptic co-packing services market share in 2025.

- By packaging type, the aseptic co-packing services market size for pouches and sachets is projected to grow at a 9.82% CAGR between 2026-2031.

- By material, paper and paperboard captured 42.40% of the aseptic co-packing services market share in 2025.

- By application, the aseptic co-packing services market size for nutraceuticals and functional foods is projected to grow at 11.40% CAGR between 2026-2031.

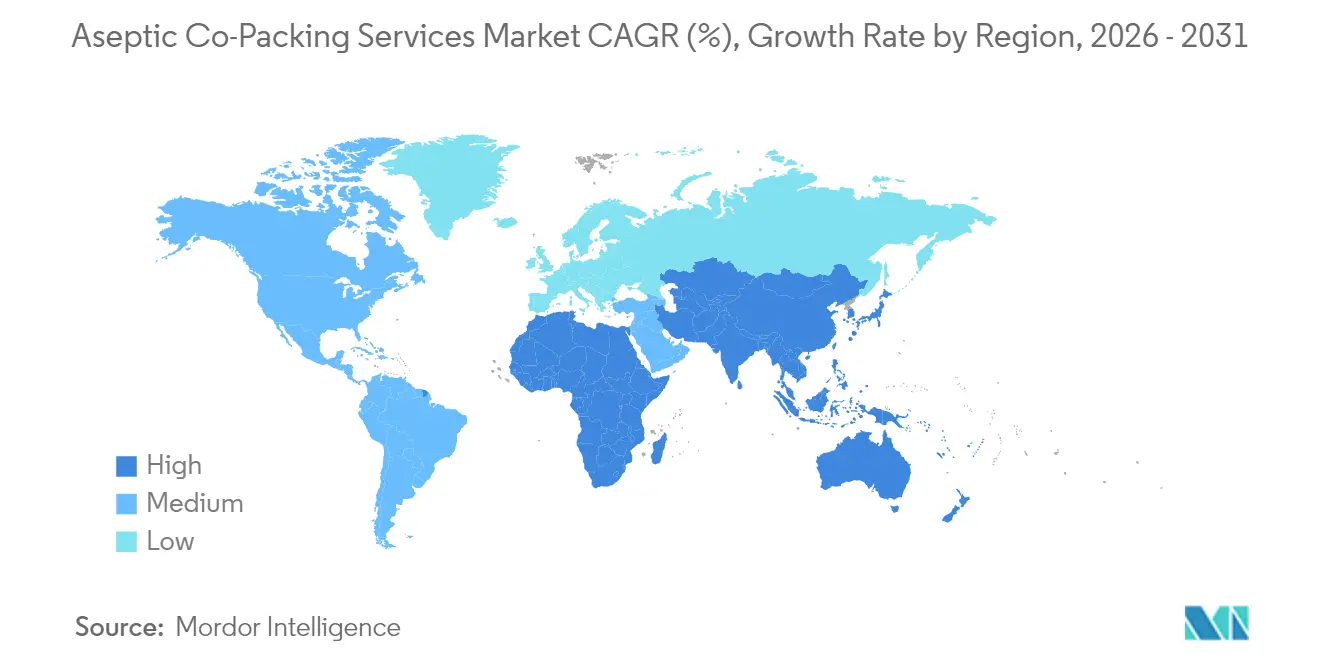

- By region, Asia-Pacific captured 31.45% of the aseptic co-packing services market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aseptic Co-Packing Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating Demand for Shelf-Stable, Clean-Label Beverages | +1.5% | Global, with premium positioning in North America and the EU | Medium term (2-4 years) |

| Rising Co-Packer Outsourcing by Premium Functional-Food Brands | +1.2% | North America and the EU core, expansion to APAC | Short term (≤ 2 years) |

| Expansion Of High-Acid Aseptic Processing Lines in Emerging Asia | +1.8% | APAC core, spill-over to MEA | Long term (≥ 4 years) |

| Cost Savings Over In-House Aseptic Infrastructure | +1.0% | Global | Short term (≤ 2 years) |

| Regulatory Push for Extended Shelf-Life in Dairy Supply Chains | +0.7% | EU and North America, regulatory influence spreading to APAC | Medium term (2-4 years) |

| Sustainability Mandates Favoring Lightweight Aseptic Cartons | +0.6% | EU regulatory leadership, global adoption following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating Demand for Shelf-Stable, Clean-Label Beverages

Consumers are steadily migrating to minimally processed drinks that list familiar ingredients and contain no artificial preservatives. Aseptic technology extends the ambient shelf life of beverages without compromising nutrient integrity or flavor, helping premium functional beverages command higher price points and reduce retail waste.[1]Tetra Pak, “Clean Label Beverages Market Trends,” tetrapak.com Retailers favor lengthy code dates that lower shrink, and regulators encourage pathogen-control methods over chemical additives, creating a reinforcing demand cycle. Brand owners, therefore, partner with specialists to achieve gentle thermal profiles for vitamins, probiotics, and botanical extracts. The result is a structural uplift for the aseptic co-packing services market, particularly in North America and Europe, where clean-label adoption is most pronounced.

Rising Co-Packer Outsourcing by Premium Functional-Food Brands

Functional-food startups typically prioritize formulation and marketing while avoiding USD 50 million-plus investments in sterile plants. Outsourcing grants them regulatory compliance, small-batch flexibility, and access to probiotic or plant-extract handling expertise they cannot replicate internally. Venture capital's preference for asset-light business models accelerates the shift, and the promise of premium margins allows brands to afford co-packing mark-ups. As new ingredients proliferate, specialists who can handle temperature-sensitive or oxidation-prone inputs expand their client base, thereby increasing demand for aseptic co-packing services.

Expansion of High-Acid Aseptic Processing Lines in Emerging Asia

Lower labor costs, abundant fruit feedstocks, and government incentives entice global beverage owners to site high-acid lines in India, Thailand, and Indonesia. Investments such as SIG’s USD 90 million India plant bring European equipment and quality standards to the region. Harmonized rules facilitate exports, allowing a single facility to serve both domestic and Western markets. High-acid categories fruit juices, energy drinks, kombucha, require comparatively simpler sterility protocols, providing an accessible entry path for regional players that now compete head-on with Western incumbents.

Cost Savings Over In-House Aseptic Infrastructure

Regulators require exhaustive microbiological testing, thermal validation, and shelf-life studies, which often exceed USD 10 million per line and can last up to 18 months. Contract specialists amortize these expenses across multiple clients, slashing per-SKU validation charges. Adding rapid technology cycles, such as AI quality control, automated cleaning, and barrier upgrades, intensifies the risk of asset obsolescence. Outsourcing converts fixed costs into variable costs, a boon for seasonal SKUs and launches with uncertain demand. The combination of financial flexibility and reduced regulatory burden underpins a consistent flow of business into the aseptic co-packing services market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-Intensive Validation Cycles for FDA And EU Sterile-Pack Rules | -1.2% | North America and the EU regulatory domains | Short term (≤ 2 years) |

| Limited Availability of Contract Fillers for Low-Volume SKUs | -0.7% | Global, particularly affecting niche brands | Medium term (2-4 years) |

| Volatility In Multilayer Laminated Substrate Prices | -0.9% | Global, with acute impact in emerging markets | Short term (≤ 2 years) |

| Brand-Owner Hesitancy Over Intellectual-Property Leakage | -0.5% | Global, concentrated in high-value formulations | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Validation Cycles for FDA and EU Sterile-Pack Rules

Each new product or packaging format faces distinct sterility validation that keeps lines idle and drains cash. Smaller co-packers struggle to finance USD 2-8 million test regimens, which consolidates capacity among larger firms and limits the geographic reach for niche brands. Regulatory updates can trigger re-validation, creating operational uncertainty and additional capex. Co-packers pass costs through to clients, and price-sensitive categories sometimes revert to lower-cost hot-fill alternatives, dampening potential growth.

Limited Availability of Contract Fillers for Low-Volume SKUs

Most aseptic fillers are optimized for long, high-volume campaigns to minimize clean-in-place downtime. Minimum order quantities of around 75,000 units often exclude small brands, forcing them to compromise on preservative-free processing. Flexible fillers exist, but their limited global footprint generates scheduling bottlenecks. The mismatch between rising SKU personalization and capacity geared toward scale slows certain innovation pipelines, marginally affecting the trajectory of the aseptic co-packing services market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Integrated Logistics Gains Momentum

Aseptic filling represented 48.05% of the aseptic co-packing services market in 2025, underscoring its role as the technology anchor that differentiates specialized providers. Continuous sterile flow, precision dosing, and real-time microbial monitoring create barriers too steep for most brand owners, ensuring robust outsourced demand. Logistics and cold-chain services, which were historically ancillary, are projected to post a 10.10% CAGR to 2031 as clients seek one-stop partners who can execute manufacturing, warehousing, and temperature-controlled distribution under unified quality protocols. [2]KanPak, “Cold Chain Logistics Capabilities,” kanpak.com. The move toward integrated contracts stabilizes revenue streams for co-packers and deepens switching costs for clients.

Formulation and blending units expand to accommodate probiotics, adaptogens, and plant-protein additions that require homogeneous dispersion without compromising sterility. Quality-assurance labs within co-packing campuses ensure regulatory compliance and maintain supply chain transparency. Overall, the aseptic co-packing services market continues its pivot from discrete manufacturing to holistic value-chain orchestration.

By Packaging Type - Flexible Formats Challenge Carton Dominance

Cartons captured 44.70% of 2025 revenue, reflecting operational familiarity and high-speed economics in mainstream juice and dairy lines. Yet pouches and sachets are expected to accelerate at a 9.82% CAGR as convenience-minded consumers gravitate toward single-serve portability and lighter packaging. New spout technologies enhance re-seal functionality and barrier performance.

Glass and PET bottles remain relevant in premium beverages, where tactile cues are important. Bags-in-box secure a share in food-service channels that prioritize bulk economics and ease of dispensing. For co-packers, the growing complexity of mix demands multi-format lines and quick-change tooling protocols, pushing capital budgets toward modular fillers that preserve uptime.

By Material Type: Paperboard Sustainability Meets Plastic Engineering

Paper and paperboard accounted for 42.40% of the revenue share in 2025, driven by corporate sustainability mandates and consumer preference for renewable fiber. Barrier coatings, including aluminum oxide and plant-based polymers, now shield against oxygen and light ingress, widening the application range of paperboard. Plastics, led by multilayer polypropylene and monomaterial PET, register the fastest 9.46% CAGR as recyclability and weight reduction improve their environmental profile.

Glass retains a foothold in shelf-stable coffee concentrates and infant nutrition, where inertness and perceived purity command a premium. Metals serve niche high-pressure uses. The material race spurs co-packers to co-develop substrate specifications with resin suppliers, cementing technical intimacy that underpins long-term contracts

By Application: Functional Nutrition Narrows the Beverage Lead

Beverages accounted for 36.70% of 2025 revenue, but nutraceutical and functional food applications are projected to register an 11.40% CAGR through 2031, eroding beverage dominance as consumers seek health-oriented formats beyond drinks. Protein-rich puddings, fiber gels, and probiotic shots require gentle aseptic handling to protect bioactive compounds.

Dairy consolidates production through ambient-stable lines, which enable distribution into tropical zones without the need for cold chains. Pharmaceutical liquid dose forms, although lower in volume, deliver superior margins due to stringent GMP and serialization demands. The convergence of quality standards between specialized foods and over-the-counter medicines blurs traditional market lines, allowing multi-permit plants to cross-serve categories under shared sterile systems.

Geography Analysis

The Asia-Pacific region generated 31.45% of 2025 revenue and led growth at an 11.25% CAGR, thanks to cost-efficient labor, favorable proximity to raw materials, and synchronized regulatory regimes with Western export markets. Government incentives in India, Thailand, and Vietnam spur capacity additions alongside European technology transfers, positioning the region as the production nerve center of the aseptic co-packing services market.

North America retains high-value segments such as infant formula and medical nutrition because proximity and brand equity foster consumer trust. Yet price competition from Asian imports forces U.S. and Canadian co-packers to automate and migrate toward pharmaceutical and custom-formulation niches. Europe matches North America in volume but sets industry tone on sustainability legislation and circular packaging, influencing global substrate choices.

South America leverages abundant fruit harvests and stable economic reforms to attract mid-tier investments, with Brazil acting as the regional hub for carton production. The Middle East and Africa remain emerging frontiers where infrastructure lags, but rising disposable income and grocery modernization attract capital focused on long-shelf-life dairy and juice.

Competitive Landscape

The top five suppliers control roughly 35-40% of global revenue, indicative of a moderately fragmented structure that still leaves room for regional champions. Tetra Pak, SIG Combibloc, and Refresco exploit scale economies in equipment procurement, packaging material integration, and multinational client relationships. They funnel capital into AI-enabled vision inspection, predictive maintenance, and fully automated clean-in-place loops, which slash downtime and labor expenses.[3]Tetra Pak, “Renewable Materials in Packaging,” tetrapak.com

Smaller firms counter with agile scheduling, niche ingredient know-how, and co-development with start-ups in plant-based nutrition or organic beverages. Vertical integration emerges as a defendable moat: players owning substrate conversion lines lock in clients through material co-innovation. Mergers center on filling geographic gaps and broadening service menus; Refresco’s acquisition of specialty PET fillers exemplifies this trend.

Intellectual-property transfer agreements with equipment OEMs also emerge, providing regional operators with access to next-generation barrier films without the need for massive in-house R&D. Overall, competitive intensity increases in commodity segments, while premium pharmaceutical and nutraceutical lines present profitable niches for technologically advanced plants.

Aseptic Co-Packing Services Industry Leaders

Tetra Pak International S.A.

SIG Combibloc Group AG

Elopak ASA

Refresco Group B.V.

Gehl Foods, LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Tetra Recart introduced recyclable fiber-based aseptic packaging formats for ready meals and soups.

- April 2025: O-AT-KA Milk Products added advanced UHT processing units to meet demand for shelf-stable clean-label beverages.

- March 2025: Gehl Foods LLC expanded its aseptic co-packing capacity with a new high-speed line for dairy-based protein drinks.

- February 2025: Tetra Pak launched a modular aseptic co-packing platform to support small-batch functional beverage startups.

Global Aseptic Co-Packing Services Market Report Scope

| Aseptic Filling |

| Formulation and Blending |

| Sterilization and Decontamination |

| Secondary Packaging and Labeling |

| Logistics and Cold-Chain Support |

| Quality Assurance and Testing |

| Cartons |

| Bottles |

| Pouches and Sachets |

| Bags-in-Box |

| Cups and Trays |

| Other Packaging Types |

| Paper and Paperboard |

| Plastic |

| Glass |

| Metal |

| Other Material Types |

| Beverages |

| Dairy Products |

| Pharmaceuticals |

| Nutraceuticals and Functional Foods |

| Plant-based |

| Others End-use Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Aseptic Filling | ||

| Formulation and Blending | |||

| Sterilization and Decontamination | |||

| Secondary Packaging and Labeling | |||

| Logistics and Cold-Chain Support | |||

| Quality Assurance and Testing | |||

| By Packaging Type | Cartons | ||

| Bottles | |||

| Pouches and Sachets | |||

| Bags-in-Box | |||

| Cups and Trays | |||

| Other Packaging Types | |||

| By Material Type | Paper and Paperboard | ||

| Plastic | |||

| Glass | |||

| Metal | |||

| Other Material Types | |||

| By Application | Beverages | ||

| Dairy Products | |||

| Pharmaceuticals | |||

| Nutraceuticals and Functional Foods | |||

| Plant-based | |||

| Others End-use Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the size of the aseptic co-packing services market in 2026?

The aseptic co-packing services market size is USD 4.22 billion in 2026.

What is the expected CAGR for aseptic co-packing through 2031?

The market is forecast to grow at an 8.19% CAGR between 2026 and 2031.

Which region leads growth for aseptic co-packing?

The Asia-Pacific region combines the highest 2025 revenue share at 31.45% and the fastest 11.25% CAGR from 2026 to 2031.

Which service segment is growing fastest?

Logistics and cold-chain support register the quickest expansion at a 10.10% CAGR.

Which packaging format is disrupting cartons?

Pouches and sachets advance at 9.82% CAGR driven by portable, single-serve demand.

Which end-use will outpace beverages?

Nutraceuticals and functional foods show an 11.40% CAGR, narrowing the beverage lead.

Page last updated on: