Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

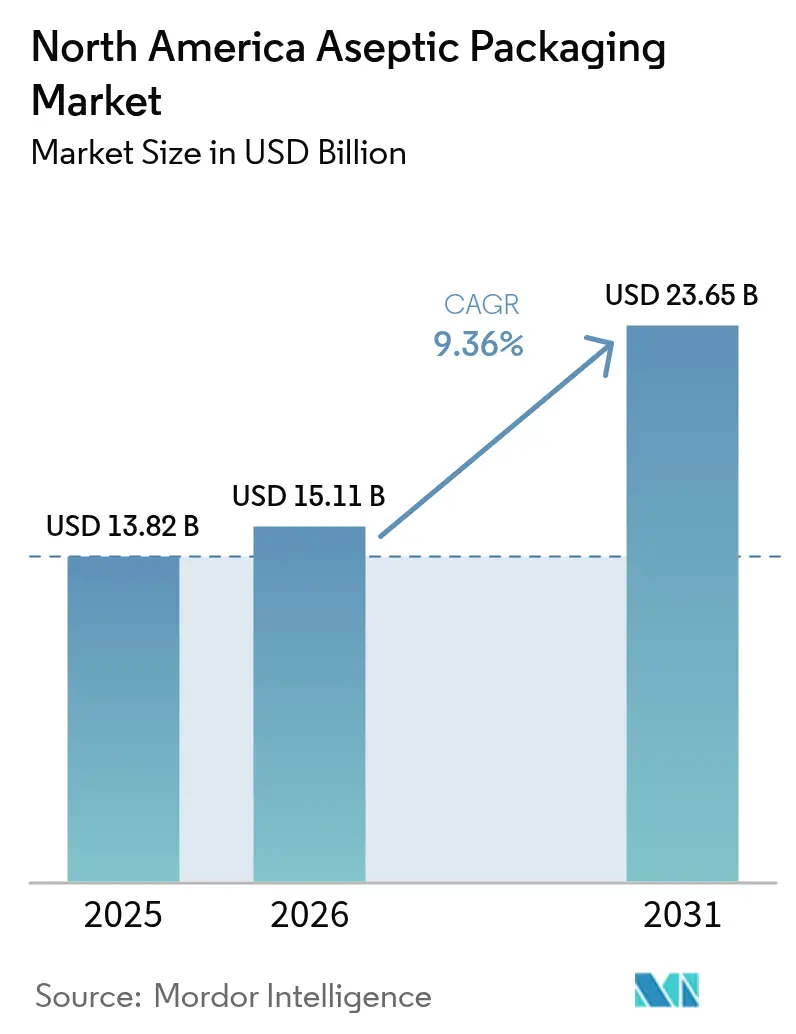

| Base Year Market Size (2025) | USD 13.82 Billion |

| Market Size (2026) | USD 15.11 Billion |

| Market Size (2031) | USD 23.65 Billion |

| Growth Rate (2026 - 2031) | 9.36% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Aseptic Packaging Market Analysis by Mordor Intelligence

The North America aseptic packaging market size is expected to grow from USD 13.82 billion in 2025 to USD 15.11 billion in 2026 and is forecast to reach USD 23.65 billion by 2031 at 9.36% CAGR over 2026-2031. Expansion is led by pharmaceutical biologics that require validated sterile containers, dairy processors intent on extending shelf life without refrigeration, and beverage brands aiming to curb cold-chain freight expenses across continental routes. Adoption further accelerates because inline AI sterility monitoring now verifies microbial integrity in real time, lowering recall risk for regulated drug and food plants. At the same time, material innovations especially fiber-based laminates and inert glass strengthen barrier performance while appeasing sustainability mandates. Competitive momentum therefore swings toward suppliers that bundle filling machinery, data analytics, and recycling partnerships into one integrated offer, adding a new digital layer to an already capital-intensive sector.

Key Report Takeaways

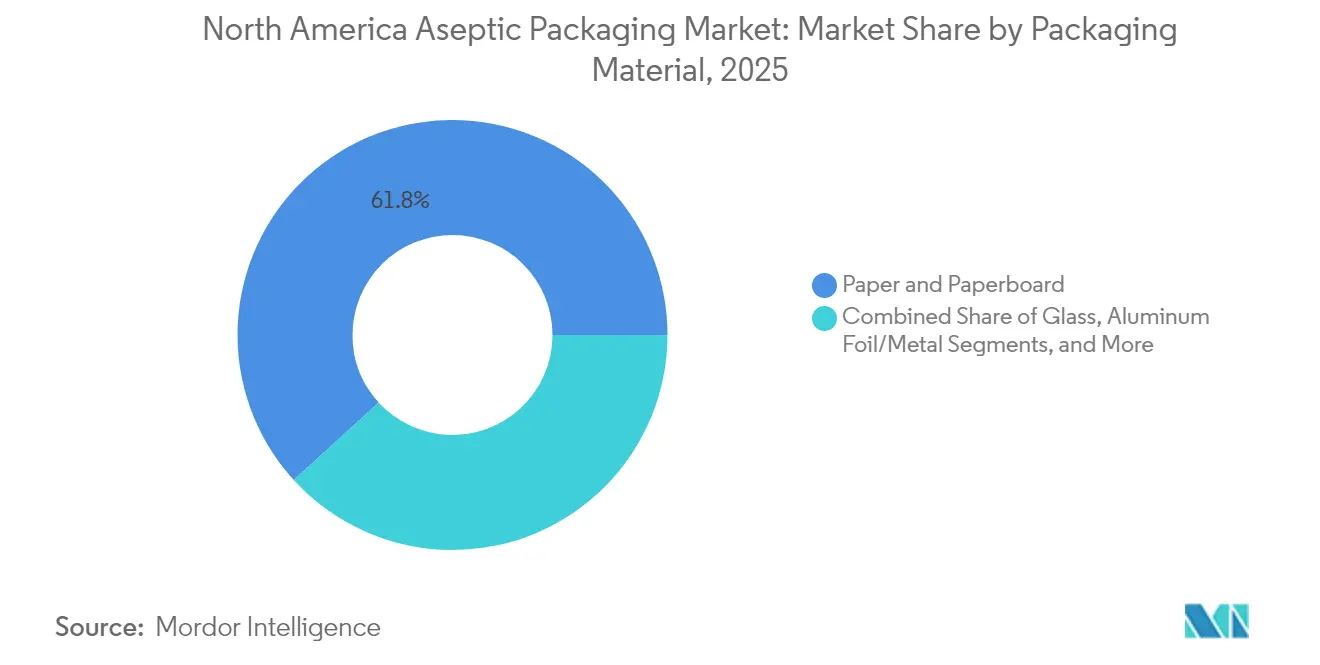

- By packaging material, paper and paperboard led with 61.78% revenue share in 2025; glass packaging is advancing at a 10.24% CAGR through 2031.

- By product type, cartons held 41.95% of the North America aseptic packaging market share in 2025, while vials and ampoules record the fastest 10.79% CAGR to 2031.

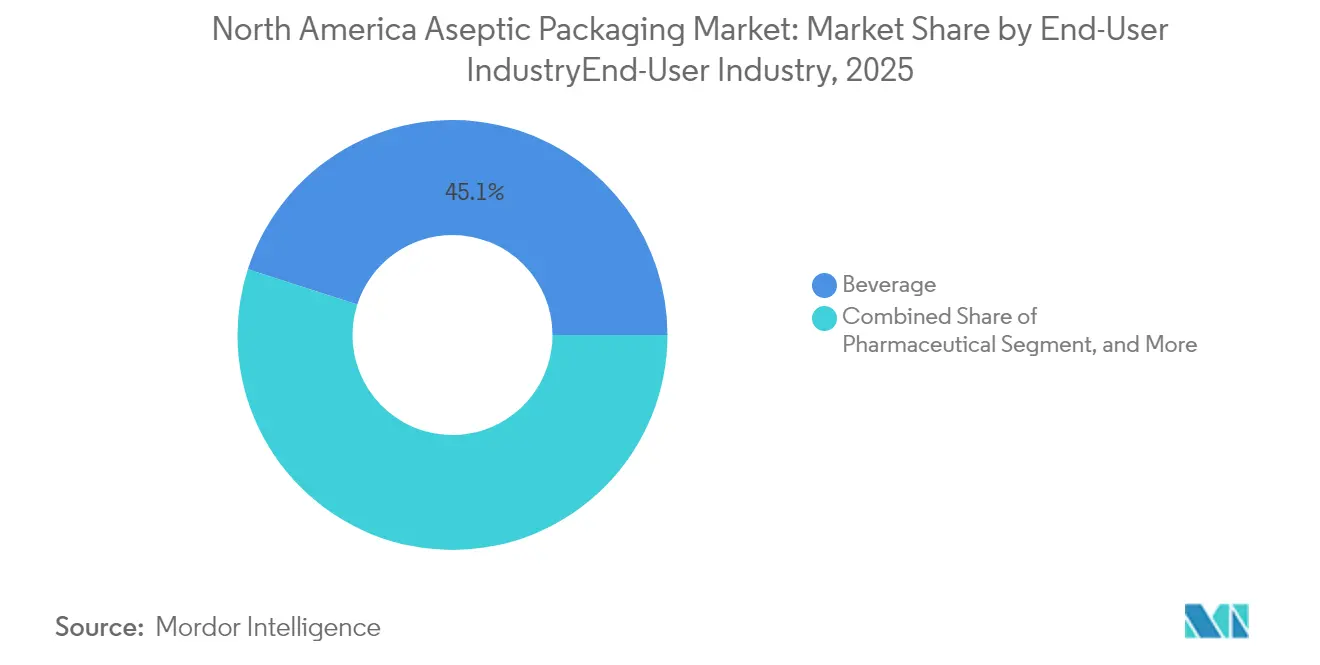

- By end-user industry, beverages commanded 45.05% of the North America aseptic packaging market size in 2025, and pharmaceuticals are moving forward at an 10.84% CAGR through 2031.

- By technology, aseptic liquid filling maintained 48.55% share in 2025; blow-fill-seal equipment is expanding at a 10.05% CAGR to 2031.

- The United States contributed 71.88% of regional revenue in 2025, whereas Mexico showed the strongest 11.23% CAGR outlook through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Aseptic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand to cut cold-chain logistics costs | +1.8% | North America, strongest in Mexico and rural U.S. | Medium term (2-4 years) |

| Preference for products with ≥12-month shelf life | +2.1% | U.S. and Canadian urban centers | Short term (≤2 years) |

| Sustainability push for paper-based and lightweight formats | +1.2% | North America and EU aligned regions | Long term (≥4 years) |

| Rapid expansion of aseptic capacity in U.S. dairy plants | +0.9% | Midwest and Southwest dairy corridors | Medium term (2-4 years) |

| Surge in biologics and RTU injectables needing sterile packs | +0.6% | U.S. hubs, Canadian biotech clusters | Long term (≥4 years) |

| AI-enabled inline sterility monitoring reducing recalls | +0.3% | U.S. and Canadian pharma centers | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Growing Demand to Cut Cold-Chain Logistics Costs

Temperature-controlled transport absorbs 15-25% of distribution budgets, so eliminating refrigeration quickly improves margins.[1] Foreign Agricultural Service, “Mexico: Dairy and Products Semi-Annual 2025,” fas.usda.gov Mexican milk imports, for instance, avoid USD 0.15-0.30 per liter in freight premiums when shipped ambient. Nestlé has earmarked USD 1 billion for aseptic lines in Mexico between 2025 and 2027 to exploit the savings. Rural U.S. counties with limited cold storage echo the calculus, while Canadian dairies rely on shelf-stable packs to reach remote northern communities where logistics costs often exceed product value. As diesel prices and driver shortages linger, the North America aseptic packaging market finds a durable advantage in cutting refrigerated miles.

Preference for Products with ≥12-Month Shelf Life

Bulk buying expanded during pandemic pantry stocking, and ambient-stable items now fetch 20-30% mark-ups in city markets. Tetra Pak surveys show 67% of households rank shelf life above brand loyalty. In pharma, SCHOTT Pharma’s USD 371 million North Carolina plant triples syringe output that holds room-temperature stability for 36 months. Urban shoppers equate longer life with convenience and emergency readiness, prompting beverage reformulations that withstand ambient warehousing. As a result, the North America aseptic packaging market gains momentum from both grocery aisles and hospital inventories.

Sustainability Push for Paper-Based and Lightweight Formats

California SB 54 stipulates 65% recycled content by 2032, intensifying demand for renewable substrates that preserve sterility. Smurfit WestRock aims for 100% recyclable packs by 2030, while Graphic Packaging allocates USD 200 million to fiber-barrier innovations. Although multilayer structures complicate recovery, consumer surveys suggest a 15-20% price tolerance for paper-centric options. Regulators and retailers now reward bio-based coatings that replace petroleum polymers, steering the North America aseptic packaging market toward circular design despite infrastructure gaps.

Rapid Expansion of Aseptic Capacity in U.S. Dairy Plants

Dairy processors spent USD 2.8 billion on upgrades in 2024, channeling 40% into aseptic lines that cut USD 0.12 per gallon in monthly cold storage charges. Midwest cooperatives deploy the technology to reclaim share from plant-based beverages, while Southwest facilities court Hispanic consumers familiar with shelf-stable formats. SIG Combibloc’s USD 35 million expansion in Querétaro supports cross-border dairy exports. Profit upside also stems from premium organic milk that earns 40-50% margins when sold ambient, reinforcing the North America aseptic packaging market trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cap-ex and long ROI for aseptic filling lines | -1.4% | North America, with strongest impact on mid-size manufacturers | Medium term (2-4 years) |

| Complex multi-material recycling infrastructure gaps | -0.8% | U.S. and Canadian waste management systems, limited Mexican infrastructure | Long term (≥ 4 years) |

| Contamination recalls eroding brand trust and margins | -0.7% | U.S. and Canadian markets with established recall systems, emerging in Mexico | Short term (≤ 2 years) |

| Rising polymer and paperboard prices squeezing converters | -0.5% | North America, with acute impact on multilayer composite manufacturers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cap-Ex and Long ROI for Aseptic Filling Lines

Turnkey systems cost USD 10-50 million, and pharmaceutical validation adds another USD 2-5 million, extending payback to 7-10 years. Smaller processors struggle to finance such outlays, especially when technical talent commands 25-30% wage premiums. Leasing models seldom suit bespoke aseptic rigs, so mergers and private equity funding dominate expansion. Consolidation, therefore, rises even as demand surges, tempering the growth curve of the North America aseptic packaging market.

Complex Multi-Material Recycling Infrastructure Gaps

Less than 40% of multilayer cartons enter effective recovery streams versus 75% for single-material packs.[2]U.S. Environmental Protection Agency, “Materials, Waste and Recycling,” epa.gov Only one-third of North American material recovery facilities possess delamination equipment, and producer-funded upgrades add 3-5% to product cost in Canada. Even where pilot plants exist, separating aluminum foil from fiber remains energy-intensive. Until collection networks mature, legacy multilayer designs will face policy penalties that moderate long-run gains for the North America aseptic packaging market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Material : Paper Leads While Glass Gains Ground

Paperboard contributed 61.78% revenue in 2025, a testament to entrenched supply chains and consumer trust in renewable fibers. The segment also aligns with state recycled-content statutes, adding regulatory tailwind to the North America aseptic packaging market. Yet glass records a 10.24% CAGR through 2031, propelled by pharma’s need for chemical inertness. Innovations such as Corning Valor Glass solve historic delamination issues, while SCHOTT’s pre-sterilized vials shrink fill-finish steps. Plastics keep a foothold in flexibles, but single-use scrutiny caps upside. Aluminum foil remains essential for ultra-low oxygen transmission in sensitive biologics. Multilayer composites blend these attributes but confront recycling headwinds already outlined. Overall, material choice in the North America aseptic packaging industry depends on striking an equilibrium among sterility, sustainability, and cost targets.

The outlook shows glass emerging from niche status. Pharma manufacturers value its compatibility with lyophilized biologics and its immunity to extractables, justifying higher weight penalties. Conversely, beverage brands retain paper cartons for ambient juices, plant milks, and broths where fiber-based stories resonate with shoppers. Polymer barrels of regulatory pressure spur a gradual pivot toward bio-based coatings rather than outright abandonment. Collectively, these currents reinforce a diversified substrate mix that shields the North America aseptic packaging market from raw-material shocks.

By Product Type : Vials Accelerate Beyond Carton Mainstay

Cartons captured 41.95% of 2025 volume thanks to decades-old shelf-stable beverage lines and efficient pallet utilization. Nonetheless, vials and ampoules outpace all other formats at a 10.79% CAGR, buoyed by expanding biologic injections that need pristine primary packs. The segment benefits from ready-to-use configurations that arrive washed and depyrogenated, trimming drugmaker cycle times. Blow-fill-seal single-dose designs also attract vaccine programs that require needle-free workstreams. Consequently, pharmaceuticals tilt the North America aseptic packaging market toward container miniaturization and higher unit value.

Bottles serve premium cold brew coffees and nutritional shakes that justify heavier glass or PET. Pouches address soup and sauce brands needing flexible geometry at low gram weight. Meanwhile, in-line AI inspection embedded in new filling heads adds another layer of differentiation by slashing sterile failure rates. Every product family, therefore, jockeys for share via either convenience or compliance, making adaptive production platforms a strategic must for converters.

By End-User Industry : Pharmaceutical Upswing Outruns Beverage Stronghold

Beverages commanded 45.05% of turnover in 2025 and will retain numeric leadership because juice, dairy, and nutraceutical drinks remain pantry staples. However, pharmaceuticals exhibit the steeper 10.84% CAGR through 2031 as gene therapies, monoclonal antibodies, and long-acting injectables scale. Drug developers assign significant value to validated barriers, which elevates the average selling price per unit and pushes the North America aseptic packaging market toward a higher margin mix. West Pharmaceutical Services typifies this shift with expanded sterile component lines in Pennsylvania.

Food processors lean on ambient soups and hummus to reduce preservatives, while personal care entrants trial sterile sachets for probiotic cosmetics. Industrial chemical niches, such as aseptic pesticides, round out demand. Diverse application breadth helps cushion cyclical shocks, though capital spending cadence remains tied to pharma launch pipelines and dairy farm modernization efforts.

By Technology : BFS Innovation Challenges Liquid Filling Dominance

Aseptic liquid systems still own 48.55% share because high-speed rotary fillers marry throughput with carton economies. Even so, blow-fill-seal rigs post a 10.05% CAGR thanks to built-in container molding that minimizes human touchpoints. ApiJect’s pre-filled injector exemplifies BFS versatility, courting mass immunization contracts. Form-fill-seal maintains relevance for flexibles in tomato products and baby food, whereas electron-beam sterilization debuts for heat-sensitive plant proteins.

Looking forward, digital twins simulate airflow and particle counts, shortening qualification timelines mandated by the FDA. Vendors bundling software, IoT sensors, and spare-parts service thus capture sticky revenue streams, reinforcing technological bifurcation inside the North America aseptic packaging market.

Geography Analysis

The United States held 71.88% revenue in 2025, anchored by pharmaceutical corridors in North Carolina, New Jersey, and California that prize proximity to syringe and vial suppliers. SCHOTT Pharma’s recent plant scale-up directly answers that geographic clustering. Dairy belts in Wisconsin and New York also widen aseptic adoption to bypass cold-chain surcharges when shipping coast-to-coast. FDA oversight supplies a stringent regulatory halo that U.S. converters leverage when exporting to Latin America and Europe, boosting order stability in the North America aseptic packaging market.

Canada delivers consistent gains under Health Canada GMP rules congruent with U.S. expectations.Toronto’s biotech corridor and Vancouver’s clean-tech hub fuel demand for small-batch sterile packs, while dairy co-ops rely on aseptic cartons to reach Yukon and Nunavut stores accessible only by seasonal roads. Regulatory reciprocity lowers documentation costs for suppliers, cementing cross-border equipment and material flows.

Mexico logs the swiftest 11.23% CAGR. Nestlé’s USD 1 billion rollout underscores the business case in rural provinces where refrigeration is scarce. National dairy self-sufficiency goals target 25% output growth by 2030, virtually guaranteeing carton volume ramps. COFEPRIS alignment with FDA norms unlocks technology transfers and lifts investor confidence. Consequently, Mexico evolves from an export-receiving node into an integrated production base supporting the wider North America aseptic packaging market.

Regulatory Landscape

In the United States, aseptic processing and packaging for shelf-stable foods is governed by FDA requirements for thermally processed low-acid foods (21 CFR Part 113) and related current good manufacturing practice rules, with an emphasis on validated scheduled processes and documentation. For Grade A dairy, participation in the National Conference on Interstate Milk Shipments (NCIMS) Aseptic Program anchors conformance for interstate milk products, reinforcing a process-control and audit-driven compliance model for fillers and packaging suppliers supporting dairy and beverage plants.

In Canada, aseptic food packaging compliance is tied to the Food and Drugs Act and oversight by the Canadian Food Inspection Agency (CFIA) preventive control framework, while Health Canada administers packaging material safety oversight, including a voluntary Letter of No Objection (LONO) pathway for food contact materials. Cross-border trade in aseptic products benefits from broadly aligned expectations around sterility maintenance, record-keeping, and preventive controls, but suppliers still manage country-specific documentation, inspections, and packaging material safety accountability alongside aseptic process validation.

Value Chain Analysis

The value chain starts with upstream raw materials and components (paperboard and barrier structures, polymers, aluminum foil layers where used, glass for vials and ampoules, closures and fitments), then extends into specialized sterilization-compatible inks and coatings and into packaging component manufacturing. Integrated players such as Tetra Pak and SIG supply both packaging materials and associated filling equipment, while pharma-oriented supply chains add sterile primary packaging preparation steps (washing, depyrogenation, and ready-to-use configurations) and sterile fluid-path consumables, supported by single-use system providers such as Meissner.

Midstream, aseptic filling and packaging is carried out by brand-owned plants and by contract manufacturers providing aseptic filling services and supply chain management (for example, MSI Express/Power Packaging). Downstream distribution includes secondary packaging, palletization patterns, and ambient logistics that reduce cold-chain dependence, though shippers still manage broader inland transportation constraints and visibility needs. Capacity localization remains a central value-chain theme, highlighted by SIG activity in Queretaro, Mexico, which supports shorter lead times and regional supply resilience for North American aseptic carton supply.

Competitive Landscape

Industry structure skews toward mid-level concentration. Multinationals like Tetra Pak, SIG Combibloc, and SCHOTT Pharma pair material production with proprietary fillers, giving them scale economies and regulatory know-how. Capital barriers USD 10-50 million per line hinder new entrants and prompt roll-ups of niche converters unable to self-fund automation upgrades. Patent estates in blow-fill-seal and fiber-barrier laminates form further moats. The North America aseptic packaging market, therefore, rewards depth in validation services and real-time analytics more than commodity tonnage.

Yet white space remains. Sustainability regulations incentivize new recyclable laminates where incumbent intellectual property is thinner. AI quality assurance and closed-loop sensors attract start-ups backed by cloud providers who see industrial data as the next platform. Brands seeking carbon footprint cuts also trial refill-on-demand micro-factories that bypass centralized filling, posing a modest but visible threat to legacy line economics. For now, however, top suppliers preserve margin by bundling OEE dashboards, parts, and compliance audits into evergreen service contracts.

North America Aseptic Packaging Industry Leaders

Sealed Air Corporation

Schott AG

Tetra Pak International S.A.

Amcor plc

SIG Combibloc Group AG

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

One opportunity centers on localized carton converting and finishing capacity that shortens lead times for beverage and dairy customers while reducing exposure to long-haul supply disruptions. Capital deployment already points to this direction: Elopak opened its first US carton converting plant at the Port of Little Rock, Arkansas (USD 100 million, April 2025), and SIG announced a phased plan (April 2026) to expand its Queretaro, Mexico plant to double capacity to 3 billion aseptic carton packs annually by 2028, with new finishing technologies starting in 2026. These moves create room for complementary investments across preforms, closures (including tethered-cap systems), secondary packaging optimization, and local technical service that can accelerate qualification cycles for new SKUs and size formats.

On the end-market side, dairy and adjacent liquid categories support higher mix and format innovation, including larger family-size cartons and differentiated barrier structures aligned with recycled-content and recyclability targets. Danone commissioning a new USD 65 million production line in Jacksonville, Florida (June 2025) and Amcor expanding flexible packaging capabilities in northeast Wisconsin for dairy (announced April 2024) point to continued plant-level modernization where aseptic-ready packaging and filling compatibility becomes part of broader throughput and efficiency programs. In pharmaceuticals, the continued shift toward ready-to-use sterile packs and higher-value primary containers sustains demand for validated, documentation-rich packaging ecosystems, creating openings for suppliers that combine materials, equipment support, and digital quality and traceability services into a single compliance-ready offering.

Recent Industry Developments

- June 2026: Tetra Pak launched a new 48 oz (1,420 mL) Tetra Brik Aseptic Edge carton for the US and Canada, produced at its Denton, Texas facility. The size expansion targets premium dairy and other ambient beverages seeking larger take-home formats and adds momentum to carton format innovation tied to functionality and sustainability cues.

- November 2025: Amcor announced a major capacity expansion project in Oshkosh, Wisconsin, adding printing, laminating, and converting capabilities. The investment strengthens supply for high-throughput flexible packaging programs, including recycle-ready structures, and adds regional capacity that supports food and beverage customers prioritizing shorter lead times.

- December 2024: SIG Combibloc completed a USD 35 million capacity increase in Queretaro, Mexico, lifting aseptic carton output by 40%. The expansion improved regional supply availability for cross-border beverage and dairy customers and reinforced Mexico's role as a manufacturing node serving the broader North American market.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues earned from aseptic packaging formats used to pack food, beverages, and pharmaceutical products in North America, where the pack and product are sterilized and then filled and sealed in a sterile setting to enable longer shelf life.

Scope exclusions: We exclude conventional hot-fill, retort packaging, and non-aseptic cold-chain packaging, even when they serve similar end uses.

Segmentation Overview

- By Packaging Material

- Paper and Paperboard

- Plastics

- Glass

- Aluminum Foil/Metal

- Multilayer Composites

- By Product Type

- Bottles

- Cartons

- Bags and Pouches

- Vials and Ampoules

- Other Product Types

- By End-User Industry

- Pharmaceutical

- Beverage

- Fruit-based Drinks

- Milk and Other Dairy Beverages

- Ready-to-Drink (RTD)

- Other Beverage Types

- Food

- Fruit-based Foods

- Dairy Food

- Processed Foods

- Soups and Broths

- Other Food Types

- Personal Care and Cosmetics

- Industrial

- Other End-User Industries

- By Technology

- Aseptic Liquid Packaging

- Blow-Fill-Seal (BFS)

- Form-Fill-Seal (FFS)

- Electron-Beam Sterilization

- Ultra-High-Temperature (UHT) / HTST

- By Country

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the industry boundaries, map the supply chain, and create a first pass on demand signals by country and end use. We mainly leaned on public sources such as the US FDA rules and recalls database, USDA and Statistics Canada food and beverage production statistics, USITC trade data for relevant packaging materials, and peer-reviewed packaging and food safety journals that describe aseptic process requirements and performance.

To keep the sizing model grounded, we also reviewed company annual reports, investor presentations, packaging association publications, and credible press coverage of capacity adds and plant investments. Where financial disclosure was limited, a paid subscription covering company financials and another covering patent activity were used selectively to validate revenue ranges and technology intensity. The desk sources listed here are illustrative, and many additional public documents were checked for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on interviews and short surveys with packaging converters, material suppliers, machinery and sterilization solution participants, and large end users across beverages, food, and pharmaceuticals. We also spoke with distribution and regulatory-facing roles so assumptions on format mix, price moves, and adoption rates could be corrected where public data was not specific enough. Since this is a North America study, field inputs were balanced across the United States and Canada, with cross-checks on trade exposure where relevant.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 30% | CXOs: 19% | |

| Mid tier: 51% | Functional/Unit leaders: 37% | |

| Smaller Players: 19% | Managers: 44% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic in a practical way. On the top-down side, we reconstructed the addressable aseptic packaging demand pool by linking packaged food, beverage, and pharma output trends in North America to aseptic penetration by format, which was then converted into value using an average selling price range by pack type and material.

On the validation side, selective bottom-up approximations were used to test totals, including sampled supplier revenue roll-ups, channel checks on format shipments, and ASP x volume builds for high-visibility categories such as cartons and plastic bottles. When company coverage was incomplete, gaps were handled by applying observed revenue-per-capacity and price-band logic to similar peers, and then adjusted after primary feedback.

Forecasts were created using scenario analysis supported by regression-based checks, where the key explanatory inputs included ready-to-drink and dairy beverage volumes, shelf-stable food launches, pharma fill-finish activity, aseptic line installation momentum, resin and paperboard price direction, and country-level consumption growth. Assumptions were kept consistent in USD terms, and then re-tested with interview-based expectations on mix shifts and price progression.

Data Validation & Update Cycle

Model outputs were checked against independent signals such as packaging format adoption trends, trade movements in key materials, and reported capacity additions, and then compared across countries to spot outliers. Where variances were large, we re-opened assumptions on penetration, pricing, or end-use allocation, and follow-up calls were triggered to confirm what changed and why.

Before sign-off, the full file is reviewed in multiple steps so arithmetic, definitions, and year alignment stay consistent across tables and narratives. Reports are refreshed annually, and interim updates are made when material events occur, such as major plant startups, regulatory shifts, or sharp input-cost changes. Right before delivery, a final analyst pass is completed so clients receive the most current view available.

Mordor Intelligence's North America Aseptic Packaging Market Market Sizing Compared With Other Published Estimates

Published market values for North America aseptic packaging do not always match because each study draws the market boundary differently, picks different base years, and applies its own view on pricing and adoption speed.

By tracking pack-format mix and end-user splits, and then refreshing currency timing and ASP bands through primary validation, Mordor Intelligence keeps the model tied to aseptic-only packaging used across food, beverages, and pharmaceuticals rather than mixing it with broader shelf-stable or non-aseptic packaging demand.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 13.82 B (2025) | |

| Industry Research Firm A | USD 12.84 B (2024) | Uses an earlier base year and frames scope mainly around food and beverage use, which can shift totals when pharma packs and format-mix pricing are treated differently. |

| Market Publisher B | USD 5.12 B (2021) | Older base year and narrower definition choices around included formats, materials, and application mapping, which lowers the starting point and changes the growth path versus newer demand signals. |

The spread is largely explained by year selection, what end uses are counted, and how format-level pricing is applied. Our approach stays repeatable because the total is built from clear demand indicators, then cross-checked with supplier-side signals and corrected where interviews show practical differences in adoption and pricing.

Key Questions Answered in the Report

What is the current value of the North America aseptic packaging market?

It is USD 15.11 billion in 2026, with a forecast to reach USD 23.65 billion in 2031 at a 9.36% CAGR.

Which end-user application is growing fastest?

Pharmaceuticals expand at an 10.84% CAGR through 2031 due to biologics and ready-to-use injectables.

Why are vials and ampoules gaining share?

Drugmakers prefer sterile, ready-to-use glass containers that minimize contamination and shorten fill-finish cycles.

How does aseptic packaging cut logistics costs?

Eliminating refrigeration removes USD 0.15-0.30 per liter in transport premiums, especially on cross-border dairy routes.

What is the biggest restraint to wider adoption?

High capital expenditure USD 10-50 million per line and long 7-10 year payback periods deter mid-size converters.

Which technology is growing quickest?

Blow-fill-seal equipment posts a 10.05% CAGR because it integrates container molding and filling in one sterile step.

Page last updated on: