Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

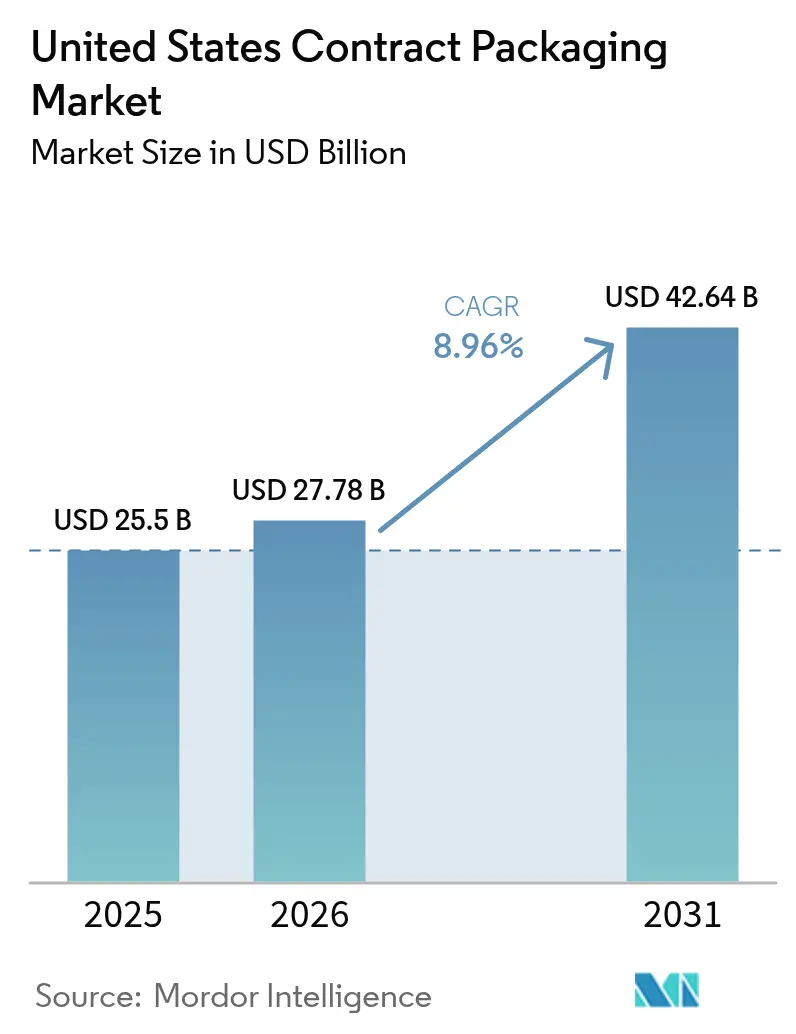

| Base Year Market Size (2025) | USD 25.50 Billion |

| Market Size (2026) | USD 27.78 Billion |

| Market Size (2031) | USD 42.64 Billion |

| Growth Rate (2026 - 2031) | 8.96% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Contract Packaging Market Analysis by Mordor Intelligence

The United States contract packaging market size was valued at USD 25.50 billion in 2025 and estimated to grow from USD 27.78 billion in 2026 to reach USD 42.64 billion by 2031, at a CAGR of 8.96% during the forecast period (2026-2031). Regulatory momentum, led by the US Food and Drug Administration’s pending front-of-package nutrition-labeling rule, is reshaping packaging specifications and timetables, while the explosive rise of e-commerce fulfillment continues to reward vendors able to deliver agile, right-sized formats. Labor shortages across manufacturing hubs are accelerating robotics adoption, and federal reshoring incentives worth USD 280 billion are stimulating new domestic capacity for pharmaceutical and food contract packagers. At the same time, consumer and legislative pressure for eco-friendly materials is steering demand toward biodegradable and bio-based substrates, encouraging suppliers to align automation, material science, and regulatory expertise inside integrated service models. Together, these dynamics confirm that the United States contract packaging market has evolved from a tactical cost-reduction option into a strategic lever for supply-chain resilience and compliance.

Key Report Takeaways

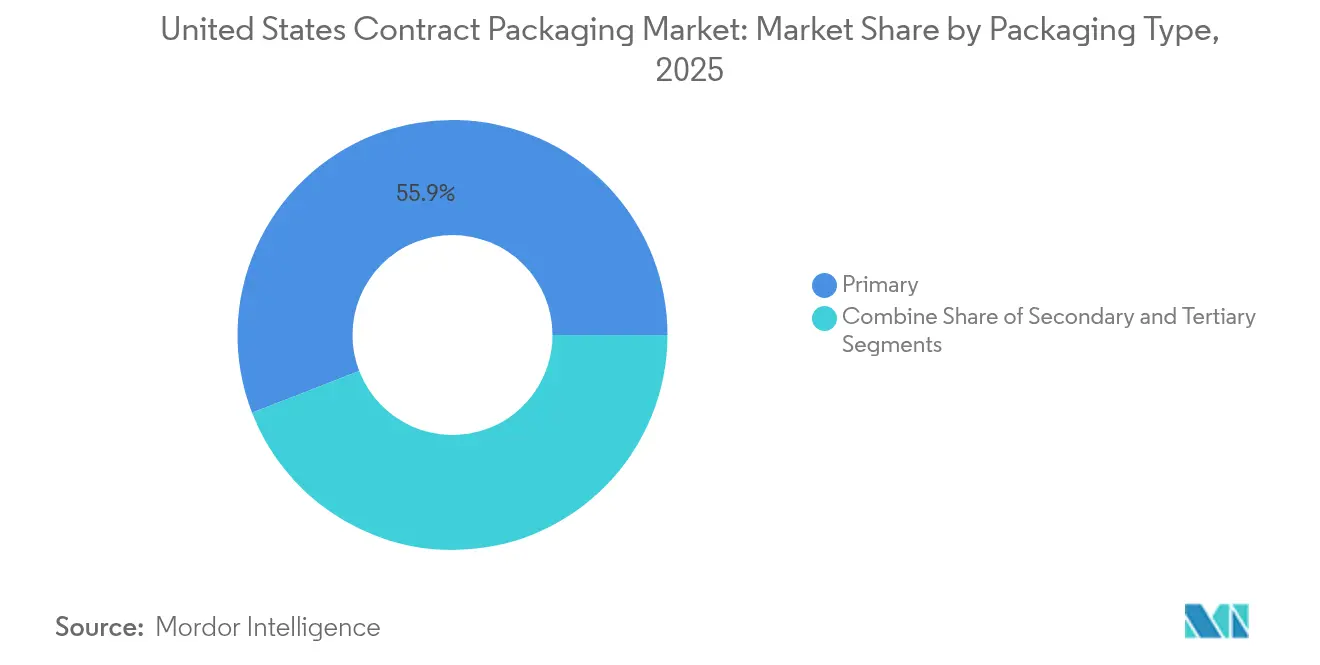

- By packaging type, primary packaging led with 55.88% of United States contract packaging market share in 2025; the segment is expanding at an 11.25% CAGR through 2031.

- By end-user industry, the food sector accounted for 35.06% revenue share in 2025, while pharmaceuticals are projected to grow at a 13.74% CAGR to 2031.

- By service offering, filling and assembly commanded 36.12% share of the United StatesS contract packaging market size in 2025, whereas fulfillment and logistics record the highest projected CAGR at 12.70% through 2031.

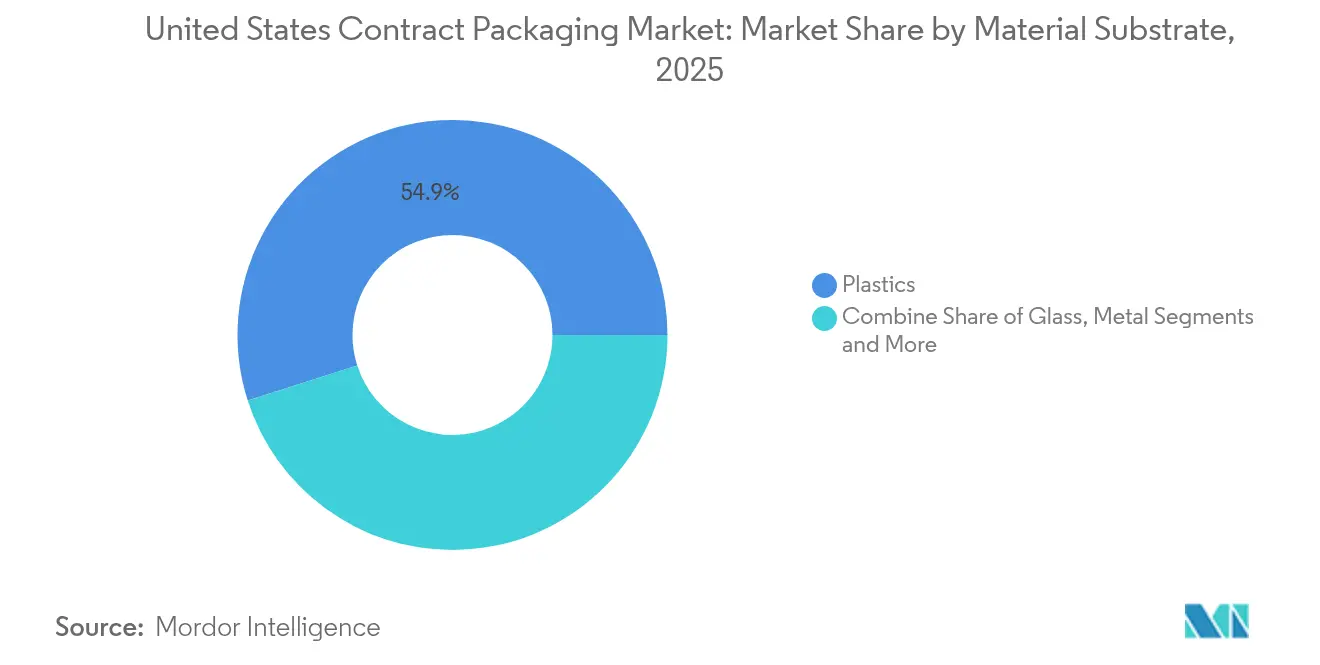

- By material substrate, plastics retained 54.92% share in 2025, yet biodegradable and bio-based options are advancing at a 12.97% CAGR.

- By automation level, semi-automated lines held 32.12% share in 2025, while robotics-integrated systems are rising fastest at 13.70% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Contract Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce boom drives agile co-packing demand | +1.2% | National, concentration in logistics hubs | Short term (≤ 2 years) |

| Pharma and nutraceutical outsourcing surge | +1.5% | Northeast and Southeast manufacturing corridors | Medium term (2-4 years) |

| Labor shortages accelerate robotics adoption | +0.9% | Midwest and Southern manufacturing regions | Medium term (2-4 years) |

| FDA FOP labeling rule spurs relabeling needs | +0.8% | National, early adoption in major metro areas | Short term (≤ 2 years) |

| Reshoring incentives lift domestic demand | +0.7% | Southern states and Rust Belt regions | Long term (≥ 4 years) |

| Eco-friendly packaging mandates and preferences | +0.6% | California, Northeast, urban markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce Boom Drives Agile Co-packing Demand

The rapid expansion of online retail continues to rewrite packaging economics for brand owners. Dimensional-weight shipping policies reward formats that minimize wasted air, pushing co-packers to redesign primary and secondary packs for lighter, tighter footprints. A surge in ready-to-drink coffee, projected to be worth USD 64.78 billion by 2032, illustrates how category-specific growth fuels line extensions that require flexible filling and labeling capability. Contract packagers able to combine AI-driven demand forecasting with rapid changeovers capture a larger share of e-commerce programs, reinforcing the strategic relevance of the United States contract packaging market for omnichannel brands.

Pharma and Nutraceutical Outsourcing Surge

Heightened regulatory scrutiny and a pipeline of complex biologics are driving drug makers to expand external partnerships. Virtual pharmaceutical firms have cut development costs by up to 50% by leaning on specialized packagers that can manage formulation, sterile fill-finish, and serialization in one workflow The need for precise dosing systems for GLP-1 therapies further raises the bar for contamination control, turning capacity expansions such as Novo Nordisk’s USD 4.1 billion North Carolina facility into anchor opportunities for the United States contract packaging market. [1]Feliza Mirasol, “Novo Nordisk Targets USD 4.1 Billion Expansion,” biopharminternational.com As a result, co-packers that hold Annex 1 expertise and vaccine-grade cleanroom certifications are transitioning from transactional vendors to strategic supply-chain partners.

Labor Shortages Accelerate Robotics Adoption

A tightening industrial labor pool has pushed robot suppliers to forecast a rebound in US installations during 2024 as manufacturers move projects off hold. In packaging halls, articulated robots now control pick-and-place tasks for irregular SKUs, while AI vision systems improve uptime by eliminating manual adjustment. Case studies such as Crider Foods’ retort room, where headcount fell from 20 to 4 employees and water use dropped 66%, demonstrate the productivity gains that justify investments even for mid-size vendors. These successes reinforce the competitive differentiation of automation-ready providers across the United States contract packaging market.

FDA FOP Labeling Rule Spurs Relabeling Needs

The FDA’s proposal to mandate front-of-pack nutrition icons by 2028 is set to generate a multiyear surge in label redesign, material qualification, and inventory write-offs. Large brands above the USD 10 million sales threshold face tight compliance windows, encouraging them to leverage contract packagers with turnkey artwork management and digital print capacity. The projected USD 3.2 billion cumulative opportunity aligns precisely with co-packers that maintain high-mix, low-volume lines capable of parallel SKU rollouts. This dynamic underscores how regulatory events translate directly into expanded revenue for the United States contract packaging market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising logistics and cold-chain costs | -1.1% | National, acute impact on temperature-sensitive products | Short term (≤ 2 years) |

| High cap-ex for automation | -0.9% | Manufacturing-intensive regions | Medium term (2-4 years) |

| Fragmented supplement/FOP compliance burden | -0.7% | National, multi-state operations | Short term (≤ 2 years) |

| Brand owners insource core SKUs under inflation | -0.6% | National, high-margin products | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Logistics and Cold-Chain Costs

Geopolitical disruptions in the Red Sea and canal corridors have pushed spot freight rates well above long-term averages, adding volatility to domestic inventory planning. [2]UNCTAD, “Freight Rates and Maritime Transport Costs,” unctad.org Temperature-controlled segments carry even higher risk, as limited reefer container availability inflates landed costs for biologics and premium food products. Brand owners are passing those expenses upstream, pressuring contract packagers to widen working-capital buffers or renegotiate delivery terms. AI-derived demand forecasts, like those deployed by Americold, help mitigate uncertainty but cannot fully erase cost swings, constraining profit margin expansion within the United States contract packaging market.

High Cap-ex for Automation

Packaging machinery shipments reached USD 10.9 billion in 2024, a level that underscores the sizable up-front cash commitment required to transition from manual lines to robotics. Mid-tier co-packers often face limited access to low-cost financing, slowing adoption despite known efficiency benefits. Integration complexity compounds the hurdle because retrofitting legacy conveyors and vision systems entails extended downtime and specialist engineering fees. These realities temper the pace at which the United States contract packaging market can fully automate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: Primary Packaging Dominates Innovation

Primary packaging accounts for 55.88% of United States contract packaging market share in 2025, and its 11.25% CAGR signals that the segment will capture most incremental revenue through 2031. Demand concentrates in injectable kits, child-resistant vials, and smart blister packs that monitor adherence. Increased personalization in oncology and diabetes therapies pushes fill volumes lower and SKU counts higher, favoring agile filling lines with quick-change tooling. Secondary packaging continues to service club-store displays and retail multipacks, yet innovation intensity remains lower as brands channel capital toward intelligent primary containers.

The segment is also where smart packaging technologies take root. QR-enabled packs provide provenance data, while NFC tags collect patient feedback for real-world evidence programs. Investments such as Gerresheimer’s USD 180 million expansion in Georgia underline the capital requirements for medical-grade plastics and injection-molded inhalers. As a result, the United States contract packaging market sees primary packaging evolve from a passive enclosure to a digitally connected interface.

By End-user Industry: Pharmaceutical Growth Outpaces Food Dominance

The food segment remains the largest revenue contributor at 35.06% in 2025, yet pharmaceuticals are advancing at a 13.74% CAGR, twice the overall market rate. This divergence mirrors drug makers’ willingness to outsource highly specialized fill-finish and labeling steps that demand Grade C cleanrooms and real-time environmental monitoring. Updated Annex 1 sterilization guidance adds further impetus by ratcheting up contamination control requirements.

Ready-to-eat and functional beverage lines continue to allocate volume to the United States contract packaging market, but growth moderates as brands mature their direct-to-consumer supply chains. In contrast, Eli Lilly’s and Novo Nordisk’s multi-billion-dollar North Carolina builds are channeling a fresh wave of injectable demand toward regional co-pack partners. Over the forecast horizon, pharmaceutical outsourcing is therefore expected to narrow the historical gap with food in overall contribution to the United States contract packaging market.

By Service Offering: Fulfillment Integration Drives Growth

Filling and assembly generated 36.12% of total 2025 revenue, yet fulfillment and logistics services are on track for a 12.70% CAGR, reflecting a pivot toward end-to-end execution models. Omnichannel brands want a single partner for pack, pick, and last-mile coordination, and they reward suppliers that can link packaging data to inventory systems in real time. The shift also helps co-packers defend margins by adding high-value distribution tasks that rely on systems integration rather than manual labor.

Formulation and blending remain niche but vital for nutraceutical powders and drink mixes, whereas packaging and labeling services face workflow disruption from the FDA’s forthcoming nutrition icon, increasing the importance of late-stage digital print. Veritiv’s USD 60 million acquisition of AmeriPac highlights how fulfillment capability has become a meaningful differentiator inside the United States contract packaging market.

By Material Substrate: Sustainability Reshapes Material Choices

Plastics retained 54.92% revenue share in 2025, yet biodegradable and bio-based substrates are expanding at 12.97% CAGR as consumer goods companies race to hit 2027 waste-reduction pledges. Brands specify sugar-cane, seaweed, and mushroom-based materials not only for environmental credentials but also for brand storytelling. The United States contract packaging market size attached to sustainable pharma packs alone is projected to grow at more than twice the rate of conventional plastics.

Paper and paperboard absorb e-commerce volume because retailers prefer curbside-recyclable solutions that match their sustainability scorecards, while metals maintain relevance in aseptic food and aerosol formats. Glass continues to dominate specialty injection vials where chemical inertness is mandatory, even if weight limits its use in direct-to-consumer shipping. Ongoing innovations in barrier coatings are expected to improve oxygen and moisture resistance of compostable films, widening adoption across the United States contract packaging market.

By Automation Level: Robotics Integration Accelerates

Semi-automated lines still control 32.12% of 2025 revenue, but robotics-integrated systems are rising fastest at 13.70% CAGR, a trend fueled by labor scarcity and stringent quality metrics in pharmaceuticals. Machine vision now inspects fill heights on every vial and rejects variances in real time, supporting zero-defect pledges demanded by drug sponsors. Small-batch changeovers executed through cobots reduce downtime for e-commerce SKUs, improving overall equipment effectiveness.

Manual operations linger in hand-crafted personal-care kits and high-mix promotional packs, where the economics of robotics remain unattractive. Fully automated high-speed lines dominate beverage can and PET bottle filling, but even these plants increasingly retrofit collaborative robots for palletizing tasks. The measurable productivity and traceability gains from automation validate capital plans and strengthen the long-term competitiveness of the United States contract packaging market.

Geography Analysis

The Northeast retains the highest concentration of pharmaceutical contract packaging plants, leveraging legacy proximity to large drug developers and a dense network of cleanroom component suppliers. FDA compliance expertise and a skilled workforce give the region a structural advantage, but its growth rate lags warmer states due to higher real estate and energy costs. The Southeast, led by North Carolina, Georgia, and Florida, is now the fastest-expanding territory in the United States contract packaging market, propelled by multi-billion-dollar biologics and injectables investments from Novo Nordisk, Eli Lilly, and Gerresheimer. Workforce-training partnerships with community colleges improve talent pipelines, reducing one of the historical bottlenecks for high-spec pharmaceutical lines.

Midwestern states continue to dominate food and beverage co-packing because of their established processing plants and central logistics corridors. However, aging facilities face mounting cap-ex requirements to accommodate robotics and sustainable substrates, prompting some operators to seek joint ventures for capital infusion. Rising cold-chain costs particularly affect dairy and ready-meal contract packagers, nudging them toward regional micro-fulfillment models that shorten delivery distances.

On the West Coast, California’s stringent recycled-content mandates accelerate adoption of alternative materials, positioning the region as a test bed for compostable and bio-based innovations. The technology sector’s need for static-safe and temperature-controlled electronics packaging further diversifies regional demand. Meanwhile, the South and Southwest benefit from the CHIPS Act and federal infrastructure funds, drawing global electronics and food brands to build nearshore assembly hubs. Texas and Arizona packaging vendors report record quoting activity for 2025 production slots, confirming the broadening geographic reach of the United States contract packaging market.

Competitive Landscape

Competition remains moderately fragmented. Catalent’s pending acquisition by Novo Holdings exemplifies the consolidation logic: large buyers seek advanced sterile capacity, global regulatory credentials, and digital quality systems that take years to replicate organically. Financial sponsors continue to acquire mid-size co-packers and invest in robotics integration, hoping to unlock multiple expansion through higher utilization and bundled fulfillment services.

Technology capability is becoming the prime axis of differentiation. Providers deploying AI-driven quality analytics offer sub-2-sigma defect rates, a threshold that wins long-term contracts with pharmaceutical innovators. Automation also feeds sustainability targets by lowering rework and waste, reinforcing the business case for capital-heavy players. Smaller regional firms defend share through flexible scheduling, low minimum order quantities, and proximity to niche customers, but they face rising pressure to finance robotics and compliance upgrades to stay relevant in the United States contract packaging market.

Strategic alliances extend beyond acquisitions. Thermo Fisher’s management has signaled that the Catalent transaction will unlock network optimization synergies by spreading fill-finish volumes across complementary sites, illustrating how integrated footprints create customer stickiness. Veritiv’s 2024 purchase of AmeriPac added omnichannel fulfillment to its packaging distribution platform, demonstrating that downstream logistics can be a strong adjacency for co-packers. Emerging disruptors are likewise pairing automation with regional footprints to win reshoring programs, supporting a dynamic yet fragmented competitive field.

United States Contract Packaging Industry Leaders

Aaron Thomas Company

Multipack Solutions LLC

Pharma Tech Industries

Reed-Lane Inc.

Sharp Packaging Services

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Gerresheimer announces USD 180 million expansion of its Peachtree City, Georgia facility to enhance medical systems production capabilities for inhalers and autoinjectors, creating over 400 new jobs and increasing production area by 18,000 square meters across two development stages.

- January 2025: Thermo Fisher CEO highlights positive CDMO outlook citing Catalent acquisition by Novo Holdings and potential benefits from new administration tariff policies, emphasizing focus on building sustainable capacity and improving supply-chain performance.

- June 2024: Novo Nordisk announces USD 4.1 billion investment in new fill/finish manufacturing facility in Clayton, North Carolina, adding 1.4 million square feet of production space and creating 1,000 new jobs to meet growing demand for GLP-1 injectable therapeutics.

- June 2025: Vetter Pharma initiates construction of new manufacturing sites in Des Plaines, Illinois and Saarlouis, Germany as part of EUR 1.5 billion investment plan, with Illinois site doubling existing Skokie facility capacity for injectable compounds.

United States Contract Packaging Market Report Scope

The market is defined based on the revenues generated from various packaging types used across different end-user industries such as Food, Beverage, Pharmaceuticals, Household and Personal Care, Automotive, and others. The analysis is based on the market insights captured through secondary research and the primaries. The market also covers the major factors impacting the growth of the contract packaging industry in terms of drivers and restraints. The study further analyzes the overall impact of COVID-19 on the ecosystem.

The United States Contract Packaging Market is segmented by Packaging Type (Primary, Secondary, and Tertiary) and End-user Industry (Food, Beverage, Pharmaceuticals, Home Care and Personal Care, and Automotive). The market sizes and values are provided in terms of value (USD million) for all the above segments.

By Packaging Type

| Primary |

| Secondary |

| Tertiary |

By End-user Industry

| Food |

| Beverage |

| Pharmaceutical |

| Home and Personal Care |

| Automotive |

| Electronics and High-tech |

| Pet Food |

| Other End-user Industry |

By Service Offering

| Formulation and Blending |

| Filling and Assembly |

| Packaging and Labeling |

| Fulfillment and Logistics |

By Material Substrate

| Paper and Paperboard |

| Plastics |

| Metals |

| Glass |

| Biodegradable/Bio-based |

By Automation Level

| Manual |

| Semi-automated |

| Fully Automated |

| Robotics-integrated |

| By Packaging Type | Primary |

| Secondary | |

| Tertiary | |

| By End-user Industry | Food |

| Beverage | |

| Pharmaceutical | |

| Home and Personal Care | |

| Automotive | |

| Electronics and High-tech | |

| Pet Food | |

| Other End-user Industry | |

| By Service Offering | Formulation and Blending |

| Filling and Assembly | |

| Packaging and Labeling | |

| Fulfillment and Logistics | |

| By Material Substrate | Paper and Paperboard |

| Plastics | |

| Metals | |

| Glass | |

| Biodegradable/Bio-based | |

| By Automation Level | Manual |

| Semi-automated | |

| Fully Automated | |

| Robotics-integrated |

Key Questions Answered in the Report

What is the current size of the US contract packaging market?

The US contract packaging market size is USD 27.78 billion in 2026 and is projected to grow steadily at a 8.96% CAGR to reach USD 42.64 billion by 2031.

Which segment is growing fastest within the market?

Pharmaceutical contract packaging is expanding at a 13.74% CAGR, outpacing all other end-user industries as drug makers outsource complex fill-finish and labeling tasks.

Why are biodegradable materials gaining traction?

State regulations on recycled content, combined with corporate sustainability goals, are pushing brands toward bio-based and compostable substrates, a trend that is driving a 12.97% CAGR for these materials.

How is automation affecting the industry’s cost structure?

Robotics-integrated systems reduce labor reliance, improve quality control, and can lower water and energy consumption, although they require significant upfront capital investment.

What impact will the FDA’s front-of-pack labeling rule have?

The rule will create a concentrated relabeling surge before the 2028 compliance deadline, representing an estimated USD 3.2 billion opportunity for packagers with scalable digital print and regulatory expertise.

How fragmented is the competitive landscape?

The market is moderately fragmented; the top ten providers control roughly half of total revenue, while numerous regional specialists compete on flexibility and proximity.

Page last updated on: