Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 86.36 Billion |

| Market Size (2031) | USD 141.06 Billion |

| Growth Rate (2026 - 2031) | 10.31% CAGR |

| Fastest Growing Market | Africa |

| Largest Market | Asia Pacific |

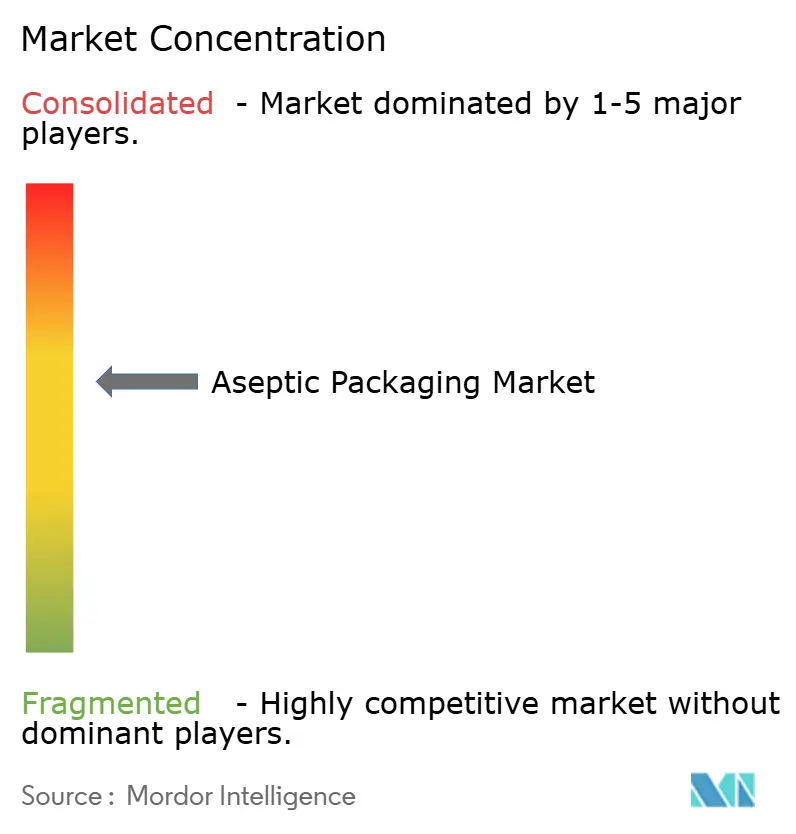

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aseptic Packaging Market Analysis by Mordor Intelligence

The aseptic packaging market size is expected to grow from USD 78.29 billion in 2025 to USD 86.36 billion in 2026 and is forecast to reach USD 141.06 billion by 2031 at a 10.31% CAGR over 2026-2031. Momentum stems from rising logistics costs that favor ambient-temperature distribution, regulatory moves that reward sterile shelf-stable formats, and investments in digitally printed flexible packs that reduce minimum-order quantities for emerging direct-to-consumer brands. Cartons continued to anchor dairy and juice volumes in 2025, yet bags and pouches are gaining share as their cube efficiency trims freight outlays by 20-30%. Composite laminates are also expanding because fiber-based structures with high-barrier coatings sidestep the recycling complications of aluminum foil. Regionally, Asia Pacific leads in volume, while Africa records the fastest growth as cold-chain energy costs rise. Competitive intensity remains moderate, with the five largest suppliers controlling roughly 45% of revenue and regional converters using short-run flexibility to win local orders.

Key Report Takeaways

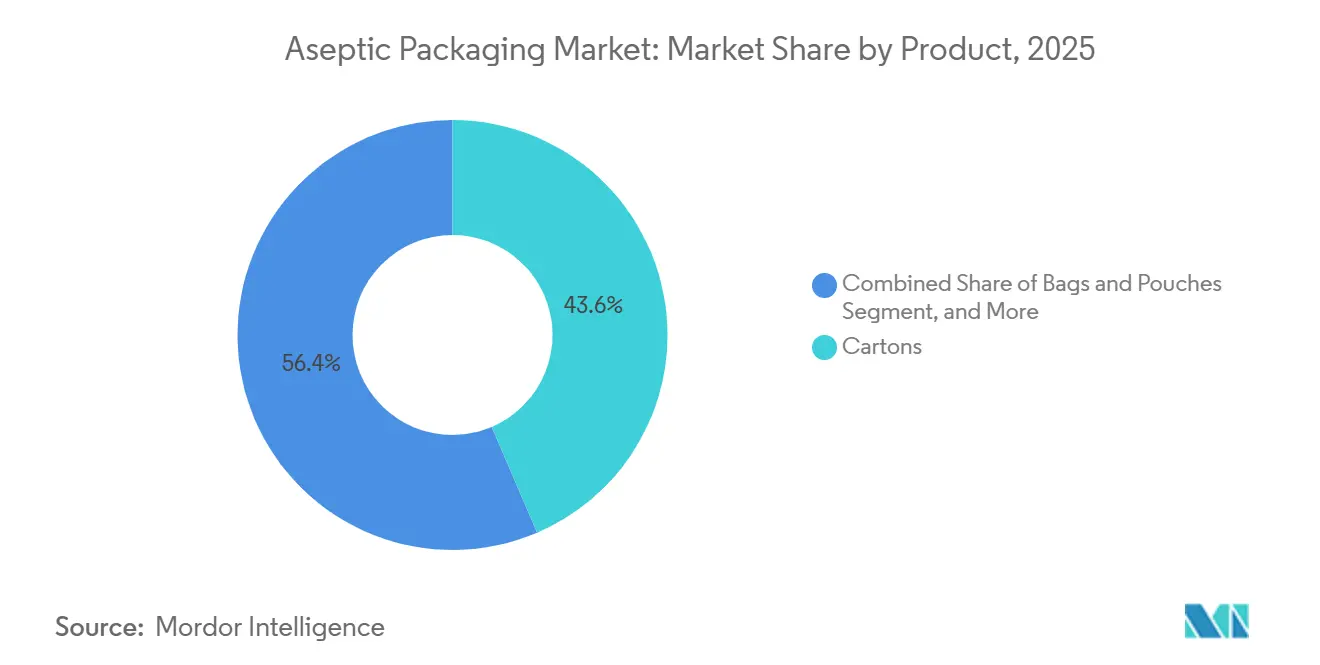

- By product, cartons led with a 43.56% revenue share in 2025, while bags and pouches are forecast to advance at a 11.31% CAGR through 2031.

- By material composition, paper and paperboard held 47.13% of the aseptic packaging market in 2025, whereas composite laminates are projected to grow at an 11.39% CAGR through 2031.

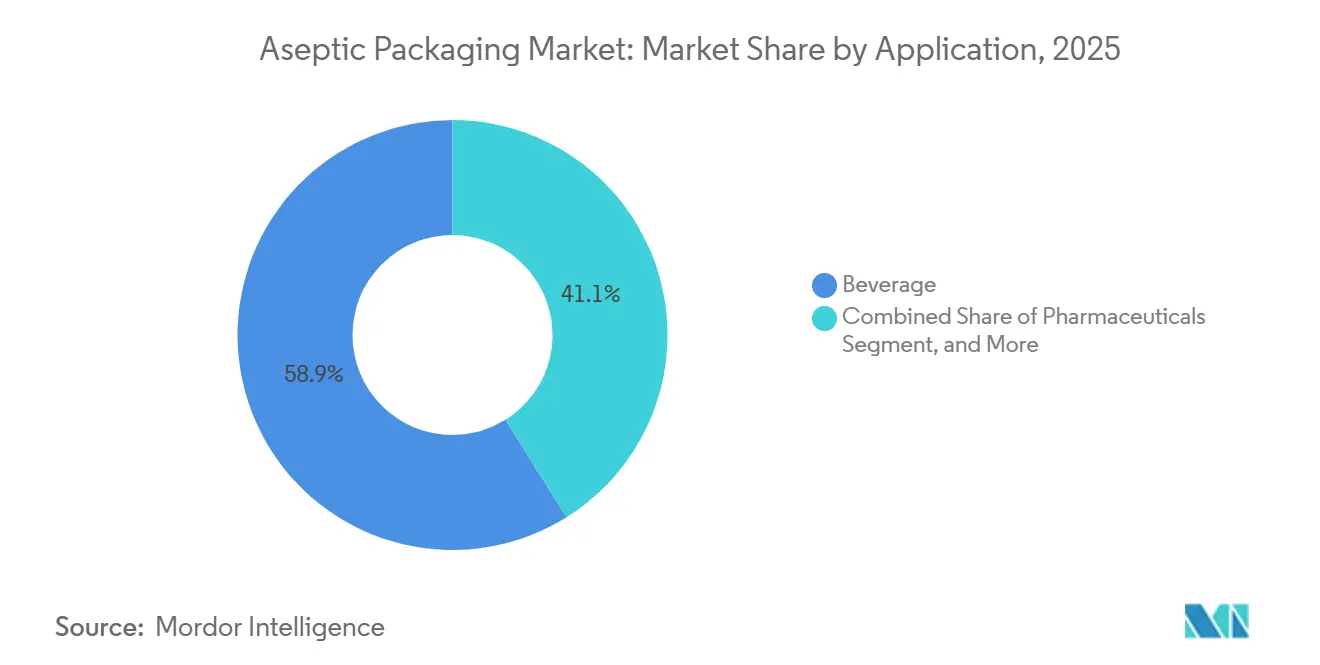

- By application, beverages accounted for 58.89% of the aseptic packaging market share in 2025, and pharmaceuticals are expected to register an 11.13% CAGR between 2026-2031.

- By filling technology, form-fill-seal captured 42.36% revenue in 2025, yet injection systems are on track for an 11.17% CAGR to 2031.

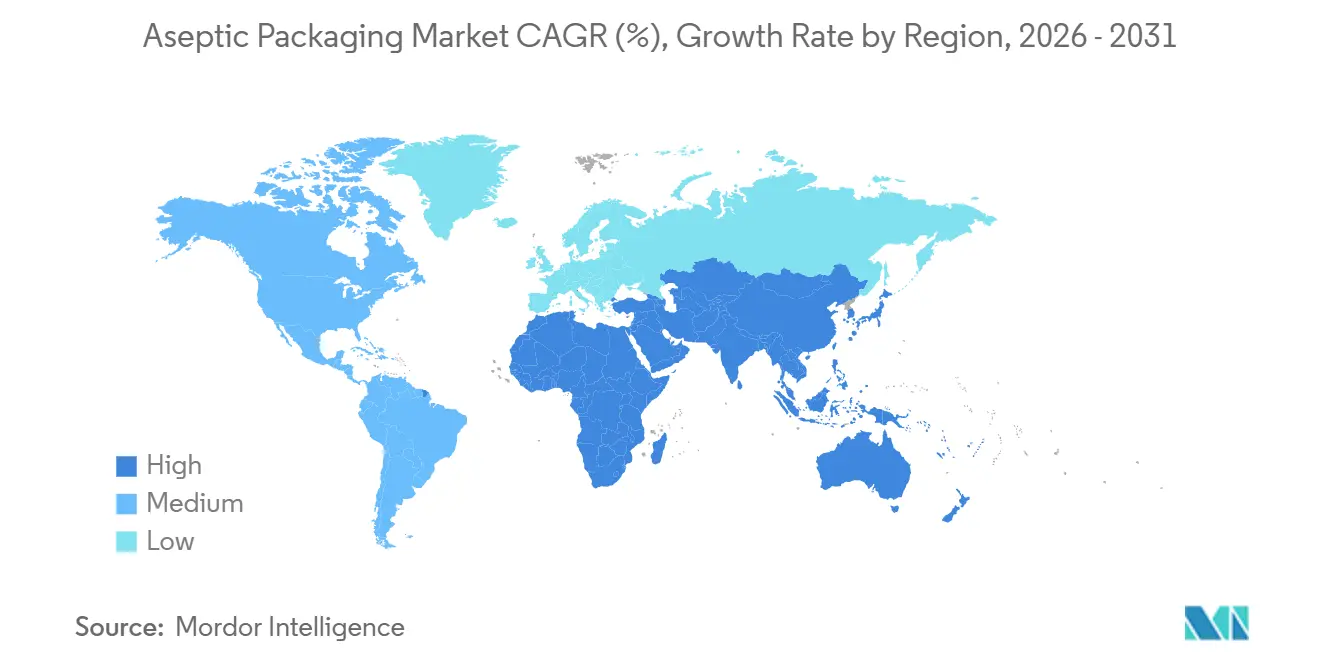

- By geography, Asia Pacific accounted for 35.67% of sales in 2025, while Africa is set to post an 11.34% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aseptic Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid Growth of RTD Functional Beverages | +2.1% | Global, most visible in North America, Europe, Asia Pacific urban centers | Medium term (2-4 years) |

| Expansion of Ambient Dairy Distribution in Emerging Asia | +1.8% | India, Indonesia, Vietnam, spillover to Middle East and Africa | Long term (≥ 4 years) |

| Stringent Food-Safety Regulations Pushing Sterile Packaging Adoption | +1.5% | North America and EU, cascading to Latin America and Middle East | Short term (≤ 2 years) |

| Inflation-Linked Shift from Cold-Chain to Shelf-Stable Logistics | +1.9% | Global, acute in Africa, Latin America, South Asia | Medium term (2-4 years) |

| Shift Toward Sustainable, Lightweight Packaging Mandates | +1.3% | EU, North America, early adopters Japan and South Korea | Long term (≥ 4 years) |

| Rise of Digital-Print-Enabled Short SKUs for D2C Brands | +0.9% | North America and EU, emerging in urban Asia Pacific | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Growth of RTD Functional Beverages

Ready-to-drink shakes, probiotic drinks, and fortified plant-based milks are switching to ambient cartons and pouches, enabling national distribution without refrigeration. Brand examples such as protein beverages in North America cut logistics bills by roughly one-quarter when they moved from cold-chain to aseptic packaging.[1]Tetra Pak, “Annual Report 2025,” TETRAPAK.COM Capital spending reflects the shift, with functional beverage producers accounting for 40% of new carton-filler installations in 2025. Smaller entrants lean on co-packers that run aseptic pouches in lots of 10,000-25,000 units, accelerating flavor tests and limiting inventory exposure. Consumer willingness to pay premiums for claims linked to immunity, gut health, and recovery underpins the higher material cost of aseptic solutions.

Expansion of Ambient Dairy Distribution in Emerging Asia

Ultra-high-temperature milk and yogurt now reach rural consumers who lack reliable refrigeration. Indian cooperatives increased carton capacity by roughly one-fifth during 2024-2025 to penetrate tier-2 and tier-3 cities. Ambient formats reduce monsoon-season spoilage, stabilize demand, and earn modest price premiums over fresh milk while remaining affordable relative to imported powders. Government tax incentives for aseptic equipment in Indonesia and Vietnam sharpened the investment case, and multinational processors recorded double-digit growth from ambient dairy portfolios.[2]Nestlé S.A., “Asia Growth Strategy Presentation 2025,” NESTLE.COM

Stringent Food-Safety Regulations Pushing Sterile Packaging Adoption

The United States Food and Drug Administration updated aseptic processing guidelines in 2024, raising validation requirements for low-acid foods.[3]United States Food and Drug Administration, “Guidance for Industry: Aseptic Processing of Food,” FDA.GOV Europe followed by flagging migration risks in certain adhesive systems. Together, these measures pushed food companies toward aseptic processes that avoid chemical preservatives and achieve commercial sterility through ultra-high-temperature treatment coupled with sterile filling. Large processors absorb compliance costs across high volumes, whereas smaller firms increasingly outsource to aseptic co-packers.

Inflation-Linked Shift from Cold-Chain to Shelf-Stable Logistics

Rising diesel and electricity prices since 2024 have widened the cost gap between refrigerated and ambient distribution. Across several Sub-Saharan corridors, refrigerated warehousing can absorb 18-22% of delivered costs, compared with 8-10% for shelf-stable products. Beverage multinationals responded by reformulating juice and dairy lines for aseptic treatment, boosting retail reach by roughly 40% in pilot African markets. A similar pattern appears in emerging pharmaceutical supply chains, where ambient aseptic vials reduce spoilage losses associated with inconsistent refrigeration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Multilayer Polymer Prices | -1.4% | Global, sharpest in import-dependent Africa and Latin America | Short term (≤ 2 years) |

| High Initial CAPEX for Aseptic Filling Lines | -1.6% | Africa, Latin America, South Asia | Medium term (2-4 years) |

| Limited Recycling Infrastructure for Aluminum-Foil Laminates | -0.8% | Global, regulatory focus EU and North America | Long term (≥ 4 years) |

| Regulatory Uncertainty Around PFAS Barrier Coatings | -0.7% | North America and EU, potential spillover to Asia Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Multilayer Polymer Prices

Swinging polyethylene and polypropylene prices shaved converter margins and forced quarterly price realignments with brand owners. Small converters in Africa and Latin America, lacking hedging options, absorbed the full cost shock, undermining competitiveness against imported pre-made pouches. Forward-looking suppliers are investing in recycled-resin streams to secure feedstock, yet recycled polyethylene currently trades at a noticeable premium over virgin grades, limiting near-term relief.

High Initial CAPEX for Aseptic Filling Lines

Entry-level pouch form-fill-seal systems cost roughly USD 2 million, while high-speed rotary carton fillers climb to USD 15 million. Financing challenges in Sub-Saharan Africa and parts of Latin America raise effective borrowing rates above 12%, concentrating capacity among large cooperatives and multinationals. Smaller brands, therefore, rely on co-packers that charge premiums for short runs, while aging lines in Southeast Asia operate with lower efficiency because upgrades are delayed.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Pouches Gain on Cartons

Bags and pouches are projected to deliver an 11.31% CAGR through 2031, the swiftest among formats, as direct-to-consumer beverage and sauce brands need lightweight packs that suit digital graphics. Cartons retained 43.56% of revenue in 2025, yet their growth rate moderates as retailers reward pouches with 20-30% warehouse cube savings. Bottles continue to serve premium coffees and probiotic drinks that justify higher pack costs, while cans cater to energy cocktails, leveraging metal’s barrier and recyclability.

Cost and branding factors underpin the pouch trajectory. Each flexible pack reduces shipping weight by close to half versus a similar-volume carton, translating to lower freight emissions, an advantage spotlighted by retailers with sustainability scorecards. Digital press advances now permit full-color artwork for runs of fewer than 50,000 pieces, avoiding plate fees that historically handicapped small-batch cartons. Cans and bottles still dominate café or gym channels where resealability and perceived quality matter, yet resealable spouted pouches are narrowing that functional gap, indicating continued share migration toward flexibles in the aseptic packaging market.

By Material Composition: Composite Laminates Outpace Paper

Paper and paperboard accounted for 47.13% of revenue in 2025, reflecting carton dominance in dairy and juice, yet composite laminates are on track for an 11.39% CAGR as converters stack polyethylene and ethylene-vinyl-alcohol layers to achieve foil-barrier performance while meeting recyclability rules. Plastics have broad utility across pouches and bottles, while glass remains niche in ultra-premium cold brews, and metal focuses on energy drinks.

Innovation in laminate structures is reducing reliance on aluminum foil. Amcor’s polyethylene plus silicon oxide laminate achieves sub-0.5 cc oxygen transmission with 20% less weight. The European Union’s 2030 recyclability targets are steering converters toward mono-material solutions, particularly polyethylene. These shifts suggest composite structures will continue to displace foil-lined cartons across the aseptic packaging market, especially in regions with active extended producer responsibility schemes.

By Application: Pharmaceuticals Surge Ahead

In 2025, beverages accounted for 58.89% of total revenue. However, pharmaceuticals are projected to see an 11.13% CAGR through 2031, driven by biologic approvals necessitating sterile, oxygen-free packaging. Meanwhile, as consumers increasingly avoid preservatives, food categories like ambient soups and sauces stand to gain. Personal care, on the other hand, continues to occupy a niche segment.

Blow-fill-seal lines, which mold, fill, and seal single doses without human contact, reduce unit costs by up to 40% compared to traditional vials and stoppers. This cost efficiency is a significant boon for high-volume vaccine production. As a result, the aseptic packaging market for biologics is witnessing rapid growth. In response to this surge, leaders in the glass-vial sector are now incorporating polymer capacities to cater to the rising demand for lightweight and shatterproof formats.

By Filling Technology: Injection Systems Gain Share

Form-fill-seal maintained a 42.36% share in 2025, but injection filling is projected to post an 11.17% CAGR as premium dairy and pharmaceutical co-packers install modular heads that finish changeovers in under an hour. Blow-fill-seal technology remains the frontrunner in sterile pharmaceutical formats. Meanwhile, in large-scale dairies, rotary systems prove indispensable, with their ability to deliver 20,000 units per hour justifying the steeper initial investment.

Major equipment suppliers have introduced servo-driven models that seamlessly integrate with existing aseptic tunnels, reducing retrofit challenges. These advancements address the issue of viscous yogurts and smoothies clogging continuous web systems. Additionally, predictive-maintenance sensors have been implemented, significantly reducing unplanned downtimes and enhancing overall equipment effectiveness in the aseptic packaging market.

Geography Analysis

Asia Pacific accounted for 35.67% of global revenue in 2025, led by expanding dairy demand in India and the growth of ready-to-drink tea in China. Ultra-high-temperature milk in India grew at double-digit rates as ambient packs reached tier-2 cities without reliable refrigeration. Japan and South Korea show premium uptakes in single-serve yogurts, while Southeast Asian startups adopt pouches to penetrate rural channels.

From 2026 to 2031, Africa is projected to witness a robust CAGR of 11.34%. In Nigeria, Kenya, and South Africa, soaring diesel and grid-power expenses are rendering cold chain operations economically unfeasible. As a result, dairy cooperatives and juice processors in these nations are shifting their focus towards shelf-stable product formats. While local production of cartons and pouches is still in its infancy, leading to heightened landed-cost pressures, multinational corporations are proactively forging partnerships with regional converters, aiming to bolster local supply chains.

Europe and North America grow more slowly yet drive sustainability mandates. The EU’s Packaging and Packaging Waste Regulation is accelerating the adoption of mono-material laminates. North America’s growth clusters around functional drinks and sterile biologic fills, while Latin America balances currency volatility against strong demand for ambient dairy. The Middle East offers opportunities in Saudi Arabia and the United Arab Emirates, where high ambient temperatures naturally favor the aseptic packaging market.

Competitive Landscape

Tetra Pak, SIG Combibloc, and Amcor together hold roughly 40-45% of global revenue, combining materials, equipment, and service contracts. Regional converters across China, India, and Brazil, meanwhile, target the aseptic packaging market with cost-effective pouches and small-order flexibility. The new investment includes Tetra Pak’s sensor-enabled seal-integrity technology, filed with the World Intellectual Property Organization.

To secure customer loyalty and boost recurring revenue, multinationals are now bundling digital monitoring subscriptions with their machinery. In response, regional players are catering to craft beverage labels by offering minimum orders ranging from 10,000 to 50,000 units. Meanwhile, pharmaceutical contract packagers are venturing into a lucrative territory, utilizing blow-fill-seal lines to provide unit doses at about one-third the cost of conventional vial assembly.

As supplier differentiation intensifies, sustainability credentials are taking center stage. Elopak has introduced a fiber-based carton featuring a water-based barrier, successfully eliminating foil layers and ensuring complete recyclability within the paper stream. Additionally, Chinese pouch manufacturers, boasting ISO 22000 and FSSC 22000 certifications, have started exporting to Europe at 20-25% discounts, exerting added price pressure on global leaders in the aseptic packaging arena.

Aseptic Packaging Industry Leaders

Tetra Pak International SA

SIG Combibloc Group

Amcor PLC

Elopak ASA

Greatview Aseptic Packaging

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Danone entered a partnership with East African dairy cooperatives to install two aseptic pouch lines, enabling shelf-stable milk distribution across Kenya, Tanzania, and Uganda.

- June 2025: Tetra Pak introduced a next-generation aseptic carton filler equipped with embedded predictive-maintenance analytics that cut unplanned downtime by an estimated 10-15%.

- March 2025: Gerresheimer’s new blow-fill-seal facility in North Carolina commenced commercial production, boosting U.S. aseptic vial capacity for biologic drugs and vaccines.

- January 2025: Tetra Pak committed EUR 120 million (USD 130.4 million) to expand aseptic carton production in Thailand, targeting an additional 8 billion packs per year with integrated digital printing capability.

Global Aseptic Packaging Market Report Scope

The Aseptic Packaging Market Report is Segmented by Product (Cartons, Bottles, Cans, Bags and Pouches, Vials and Ampoules), Material Composition (Paper and Paperboard, Plastics, Glass, Metal, Composite Laminates), Application (Beverage, Food, Pharmaceuticals, Personal Care and Cosmetics), Filling Technology (Form-Fill-Seal (FFS), Blow-Fill-Seal (BFS), Injection Aseptic Filling, Rotary Aseptic Filling), and Geography (North America, Europe, Asia Pacific, Middle East, Africa, South America). Market Forecasts are Provided in Terms of Value (USD).

By Product

| Cartons |

| Bottles |

| Cans |

| Bags and Pouches |

| Vials and Ampoules |

By Material Composition

| Paper and Paperboard |

| Plastics (PP, PE, PET) |

| Glass |

| Metal (Aluminum, Steel) |

| Composite Laminates |

By Application

| Beverage | Ready-to-Drink (RTD) Beverages |

| Dairy-Based Beverages | |

| Food | Processed Food |

| Fruits and Vegetables | |

| Dairy Food | |

| Pharmaceuticals | |

| Personal Care and Cosmetics |

By Filling Technology

| Form-Fill-Seal (FFS) |

| Blow-Fill-Seal (BFS) |

| Injection Aseptic Filling |

| Rotary Aseptic Filling |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Product | Cartons | ||

| Bottles | |||

| Cans | |||

| Bags and Pouches | |||

| Vials and Ampoules | |||

| By Material Composition | Paper and Paperboard | ||

| Plastics (PP, PE, PET) | |||

| Glass | |||

| Metal (Aluminum, Steel) | |||

| Composite Laminates | |||

| By Application | Beverage | Ready-to-Drink (RTD) Beverages | |

| Dairy-Based Beverages | |||

| Food | Processed Food | ||

| Fruits and Vegetables | |||

| Dairy Food | |||

| Pharmaceuticals | |||

| Personal Care and Cosmetics | |||

| By Filling Technology | Form-Fill-Seal (FFS) | ||

| Blow-Fill-Seal (BFS) | |||

| Injection Aseptic Filling | |||

| Rotary Aseptic Filling | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the aseptic packaging market and how fast is it growing?

The aseptic packaging market size was USD 78.29 billion in 2025, is USD 86.36 billion in 2026, and is forecast to reach USD 141.06 billion by 2031 at a 10.31% CAGR.

Which product type is expanding fastest in aseptic applications?

Bags and pouches are the fastest growing, projected for an 11.31% CAGR through 2031 as brands favor lightweight, digitally printed flexibles.

Why are pharmaceuticals adopting aseptic packs at a rapid rate?

Biologic drug approvals and the cost advantages of blow-fill-seal technology are propelling pharmaceutical demand at an expected 11.13% CAGR.

How are sustainability regulations affecting material choices?

European and North American rules that prioritize recyclability are accelerating the shift toward mono-material polyethylene laminates and foil-free fiber cartons.

Which region is expected to post the highest growth through 2031?

Africa leads on growth with an 11.34% CAGR forecast as processors seek shelf-stable formats to bypass limited cold-chain infrastructure.

What is the main barrier for smaller processors switching to aseptic filling?

High capital expenditure, ranging from USD 2 million to USD 15 million per line, limits access to financing in many emerging markets.

Page last updated on: