Tertiary Packing And Palletizing Solutions Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 17.14 Billion |

| Market Size (2030) | USD 22.15 Billion |

| Growth Rate (2025 - 2030) | 5.26% CAGR |

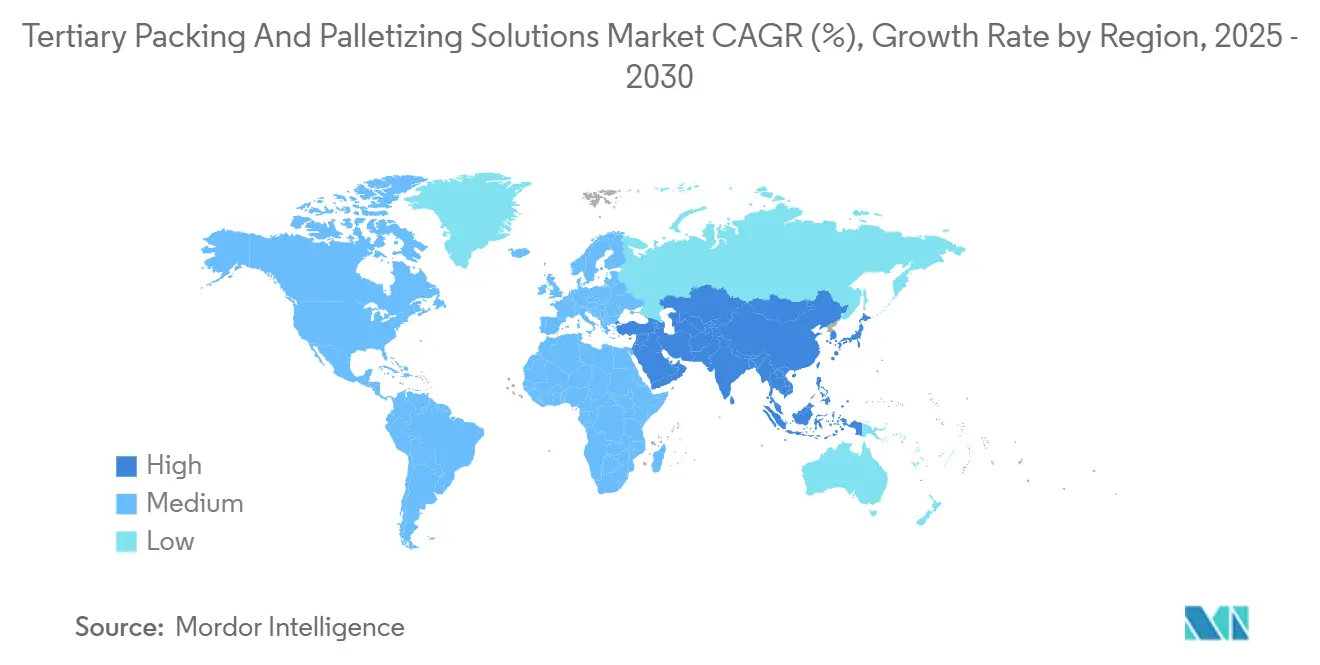

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

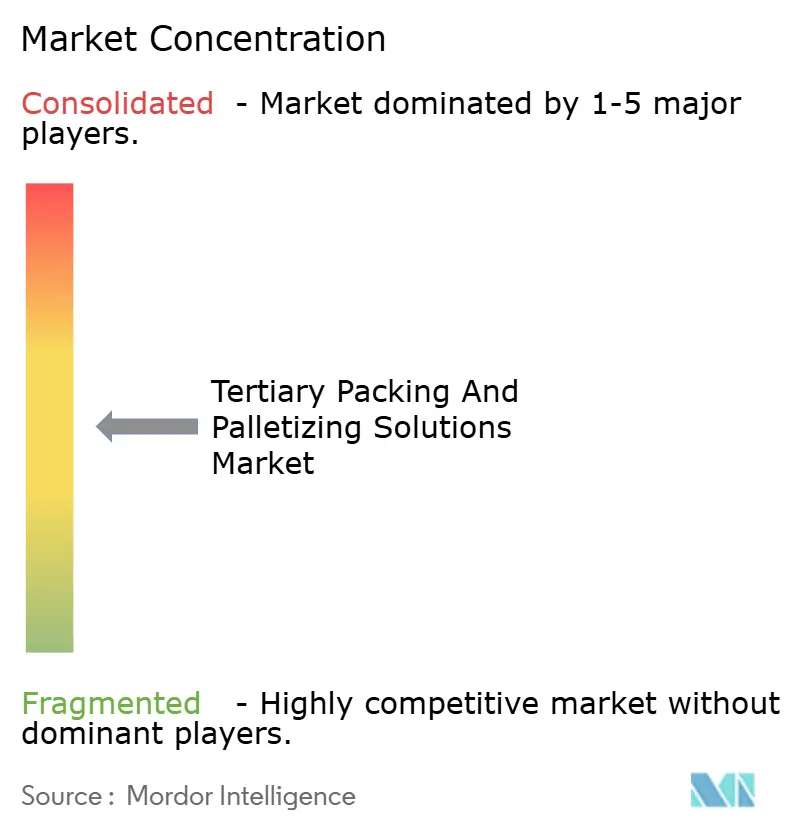

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Tertiary Packing And Palletizing Solutions Market Analysis by Mordor Intelligence

The tertiary packing and palletizing solutions market size stands at USD 17.14 billion in 2025 and is forecast to reach USD 22.15 billion by 2030, advancing at a 5.26% CAGR.

A convergence of labor-shortage pressures, e-commerce fulfillment expansion, and sustainability mandates is steering investment toward flexible, software-defined automation. Conventional palletizers retain a cost-per-cycle edge for single-SKU, high-volume lines, yet collaborative robots and mobile platforms are winning share by enabling rapid SKU changeovers, smaller batches, and mixed-case handling. Vision-guided motion planning, digital-twin modeling, and edge analytics now underpin most new installations, cutting changeover times and improving cube utilization. At the same time, brownfield retrofits dominate in mature economies, prompting premium spending on modular cells that slot into legacy conveyor layouts while limiting downtime.

Key Report Takeaways

- By machine type, conventional palletizers held 39.41% of the tertiary packing and palletizing solutions market share in 2024, whereas cobots and mobile robots are projected to grow at a 15.3% CAGR through 2030.

- By automation level, fully-automatic systems represented 56.82% of the tertiary packing and palletizing solutions market size in 2024, while manual-assist and collaborative cells are poised to expand at a 12.1% CAGR between 2025-2030.

- By end-use industry, food and beverage led with 31.22% revenue share in 2024; e-commerce and 3PL applications are forecast to post a 13.8% CAGR through 2030.

- By packaging material, corrugated cases dominated, but reusable RPCs and totes are expected to rise at an 11.5% CAGR to 2030.

- By geography, North America commanded 33.15% share in 2024, while Asia-Pacific is advancing at a 10.4% CAGR over the same period.

Global Tertiary Packing And Palletizing Solutions Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce fulfillment footprint expansion | +1.2% | Global - North America and Europe | Medium term (2-4 years) |

| Fast-growing SKUs drive late-stage customization | +0.8% | North America and Asia-Pacific | Short term (≤ 2 years) |

| Labor-shortage-induced automation mandates | +0.9% | Global - developed economies | Short term (≤ 2 years) |

| Rising pallet standardization in emerging markets | +0.7% | Asia-Pacific, Latin America and Middle East and Africa | Long term (≥ 4 years) |

| Software-defined palletizing | +1.1% | Global - led by North America and Europe | Medium term (2-4 years) |

| Carbon-neutral warehousing targets | +0.6% | Europe and North America, spreading to Asia-Pacific | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-Commerce Fulfillment Footprint Expansion

E-commerce growth is reshaping palletizing requirements as mixed-SKU outbound orders supplant homogeneous case loads. Amazon’s USD 1 billion automation outlay in 2024 produced a demonstration effect, pushing fulfillment operators to specify adaptive systems that re-sequence patterns in seconds rather than hours. Vision-guided palletizers handle variable box profiles without mechanical change parts, lifting throughput flexibility by 40% while reducing manual touches.[1]Amazon.com Inc., “Annual Report 2024,” ir.aboutamazon.com Compact cells serve micro-fulfillment centers in dense urban zones, where real estate costs demand vertical efficiency. Third-party logistics firms report superior returns when deploying mobile robots that traverse multiple lines, underpinning the rapid uptake of collaborative platforms in this setting.

Labor-Shortage-Induced Automation Mandates

Warehouse vacancies eclipsed 8.3 million in 2024 against 6.5 million available workers, forcing operators to automate beyond pure ROI metrics.[2]Massachusetts Institute of Technology, “AI-Powered Robotics Transform Manufacturing,” technologyreview.com Collaborative robots mitigate staffing gaps by allowing one technician to oversee several palletizing cells, cutting repetitive strain injuries and trimming overtime. In Europe, wage inflation of at least 15% for material handlers has shortened payback periods to below 18 months. Lights-out palletizing during overnight shifts extends asset utilization, while drag-and-drop programming lets existing staff commission new SKUs without external integrator support. These factors make labor economics the most immediate catalyst for the tertiary packing and palletizing solutions market.

Software-Defined Palletizing

AI-powered motion planning replaces rule-based approaches by generating optimal stacking patterns derived from SKU geometry, route constraints, and load-bearing rules. Simulated in digital twins, new recipes download to the cell in minutes, minimizing downtime. Machine-learning algorithms lift placement accuracy to 99.7%, surpassing experienced operators. Cloud optimization services open enterprise-grade analytics to mid-market factories without on-premise computing spend. Edge devices synchronize multiple plants over 5G, creating fleet learning loops that refine algorithms continuously and amplify the network effect across the tertiary packing and palletizing solutions market.

Carbon-Neutral Warehousing Targets

Sustainability programs elevate energy and materials efficiency to procurement criteria equal in weight to throughput. Servo-driven palletizers now draw 40% less power than pneumatic predecessors, aligning with ISO 14001 objectives. AI-optimized stacking increases trailer cube utilization by 15%, abating transport emissions.[3]European Environment Agency, “Industrial Waste Prevention: Good Practices in Europe,” eea.europa.eu Automated cells also slash dunnage waste through exact placement, supporting circular economy commitments. Early adopters combine on-site solar with battery storage to run palletizing lines at net-zero carbon, setting benchmarks competitors must match as environmental disclosures become mainstream.

High Upfront Capex for Brown-Field Integration

Retrofitting legacy halls costs 60-80% more than greenfield builds because floors, networks, and clearance heights rarely align with modern robot envelopes. Mid-tier manufacturers thus face payback horizons near five years, dampening order intake. Modular cells that roll through standard dock doors and bolt to existing conveyors are gaining favor, yet overall capital intensity remains elevated until depreciation cycles unlock funds for holistic refurbishments. Financing packages and equipment-as-a-service models aim to smooth spending curves, but adoption among cautious operators stays measured.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High upfront capex for brown-field integration | -0.9% | Global - North America and Europe | Short term (≤ 2 years) |

| Limited adaptability to hyper-variable packaging | -0.7% | Global - pronounced in e-commerce | Medium term (2-4 years) |

| Cyber-security concerns in OT networks | -0.5% | Global - critical infrastructure focus | Medium term (2-4 years) |

| Skilled-operator deficit for advanced cobot cells | -0.4% | Developed economies, widening to emerging markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cyber-Security Concerns in OT Networks

Attack volume on operational technology surged 150% in 2024, and palletizing controllers tied into enterprise clouds became tempting entry point. Air-gapped alternatives sacrifice the very analytics that justify next-gen systems, highlighting a tradeoff between security and efficiency. Compliance checks and segmentation add 10-15% to project budgets. Vendors embed security chips and encrypted protocols, yet many plants still lack round-the-clock monitoring talent, leaving residual risk that restrains procurement until clear frameworks and managed services mature.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Flexibility Gains Overtake Legacy Throughput

Conventional palletizers commanded the largest stake of the tertiary packing and palletizing solutions market at 39.41% in 2024. Despite that lead, cobots and mobile robots are accelerating at a 15.3% CAGR as factories pivot toward multi-SKU agility. Robotic palletizers serve mid-volume lines by blending speed and programmability, while hybrid cells fuse industrial-arm rates with cobot ease, especially in changeover-heavy beverage plants.

Rapid software iteration favors collaborative devices because pattern updates need no external integrator. Mobile bases allow a single unit to serve multiple lines on staggered schedules, minimizing dormant capital. Depalletizers grow in tandem as reverse logistics and returns processing move toward end-to-end automation. The tertiary packing and palletizing solutions market size attributable to cobots thus scales quickly even though unit prices undercut heavy-duty gantries.

By End-Use Industry: Fulfillment Disrupts Traditional Hierarchies

Food and beverage dominated revenue with 31.22% share in 2024, driven by high-volume bottling and canning operations that still favor conventional high-speed systems. E-commerce and 3PL operations, however, are charting a 13.8% CAGR as mixed-case dispatches require adaptive cells. Pharmaceutical plants add steady demand, expanding digital traceability that pairs vision inspection with palletizing.

Retailers requesting late-stage customization compress batch sizes, forcing consumer-packaged-goods makers to adopt flexible robotic layers. In turn, private-label growth boosts SKU counts, demanding palletizing recipes that shift every few hours. The tertiary packing and palletizing solutions market share of e-commerce is therefore rising even though absolute spend still trails food production lines.

By Automation Level: Collaboration Redefines Labor Allocation

Fully-automatic lines held 56.82% of 2024 revenues, but manual-assist and collaborative platforms outpace them at a 12.1% CAGR. The tertiary packing and palletizing solutions market size for semi-automatic cells grows as brownfield plants opt for phased upgrades rather than single-hit capex.

Operators value collaborative safety certifications that remove hard guarding and reclaim floor space. Predictive maintenance algorithms embedded in these systems cut unplanned downtime by one quarter and alert staff via mobile dashboards. The labor market’s tilt toward tech-augmented roles further entrenches collaborative adoption, making it the bridge between manual handling and lights-out operation.

By Packaging Material Handled: Reusables Gain Momentum

Corrugated cases still account for 42.71% of handled volume, yet reusable RPCs and totes are expanding fastest at an 11.5% CAGR as circular economy programs mature. Vision-assisted end-effectors place RPCs precisely, preventing lid damage and preserving pool life. Shrink-wrapped bundles benefit from beverage line upgrades, while bags, drums, and pails demand niche grippers with automatic center-of-gravity correction.

Manufacturers transitioning to RPC distribution report 20% packaging cost savings despite higher automation complexity. This dynamic pulls incremental spend into the tertiary packing and palletizing solutions market as vision and AI subsystems become prerequisites for handling heterogeneous reusable fleets.

Geography Analysis

North America retained 33.15% of global revenue in 2024 on the back of high labor costs and continued e-commerce infrastructure build-out. Average payback for palletizing cells sits near 24 months, which sustains upgrade cycles even in mature factories. Canada prioritizes hygienic stainless-steel builds for meat processing, while Mexico leverages nearshoring to automate export-oriented plants. Integrators able to mesh new cells with decades-old conveyors enjoy premium margins across the United States retrofit landscape.

Asia-Pacific is the growth pacesetter at 10.4% CAGR through 2030 as China subsidizes robot adoption and India accelerates pharmaceutical exports. Japan’s demographic profile drives strong collaborative robot demand, evidenced by 30% domestic order growth at FANUC in 2024. Southeast Asian nations capitalize on supply-chain diversification, embedding digital-twin-ready palletizing from day one. Regional pallet standardization programs cut customization costs, allowing suppliers to spread engineering effort across multiple markets, thereby enlarging the tertiary packing and palletizing solutions market size in the region.

Europe delivers steady progress anchored in environmental regulation and Industry 4.0 incentives. Germany allocated EUR 2.3 billion (USD 2.5 billion) to industrial robotics in 2024, while the United Kingdom revised food-safety norms that boost demand for wash-down friendly cells. France’s premium packaging expectations fuel flexible palletizing adoption, and Italy leverages domestic machinery expertise to shorten lead times. Energy-efficient servo technologies align with European Union decarbonization rules, ensuring that sustainability remains a key purchase driver continent-wide.

Competitive Landscape

Market concentration is moderate as global robot stalwarts contend with nimble specialists. ABB, FANUC, and KUKA leverage installed bases and multi-country service, yet struggle with fast customization cycles demanded by e-commerce operators. Collaborative pioneers such as Universal Robots scale quickly by offering plug-and-play kits and intuitive software. Software-first challengers like OSARO layer vision and AI onto commodity arms, disentangling value from hardware and exerting pricing pressure on traditional OEMs.

Hybrid offerings that combine autonomous mobile robots with palletizing end-effectors blur categorical boundaries. System integrators differentiate through domain expertise in brownfield retrofits, cybersecurity hardening, and inter-island data orchestration. Patent filings concentrate around collision-avoidance soft skins, machine-learning motion planning, and digital-twin orchestration, indicating a pivot to software-defined differentiation within the tertiary packing and palletizing solutions industry.

Vendor partnerships proliferate as hardware firms embed third-party AI into controllers, accelerating time-to-market for mixed-case capability. Simultaneously, end-users demand open architectures to avoid lock-in, spurring creation of robot-agnostic middleware. This bargaining power shift enables midsize buyers to negotiate performance-based contracts, further redefining competitive advantage.

Tertiary Packing And Palletizing Solutions Industry Leaders

ABB Ltd.

FANUC Corporation

KUKA AG

Yaskawa Electric Corporation

Honeywell Intelligrated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: ABB completed acquisition of ASTI Mobile Robotics for EUR 198 million (USD 216 million), expanding autonomous mobile robot capabilities for integrated palletizing solutions across manufacturing and logistics applications.

- September 2024: Amazon announced USD 1 billion investment in warehouse automation technologies, including advanced palletizing systems for fulfillment centers across North America and Europe, targeting 40% productivity improvement by 2026.

- August 2024: FANUC launched new CRX-25iA collaborative robot specifically designed for palletizing applications, featuring 25 kg payload capacity and integrated vision system for mixed-case handling in e-commerce environments.

Global Tertiary Packing And Palletizing Solutions Market Report Scope

The Tertiary Packing and Palletizing Solutions Market Report is Segmented by Machine Type (Conventional Palletizers, Robotic Palletizers, Cobots and Mobile Robots, Depalletizers, Hybrid Cells), End-Use Industry (Food and Beverage, Consumer Packaged Goods, Pharmaceuticals and Healthcare, Industrial and Chemicals, E-commerce and 3PL), Automation Level (Fully-automatic Systems, Semi-automatic Systems, Manual Assist/Collaborative), Packaging Material Handled (Corrugated Cases, Shrink-wrapped Bundles, Bags and Sacks, Drums and Pails, RPCs and Totes), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

| Conventional Palletizers |

| Robotic Palletizers |

| Cobots and Mobile Robots |

| Depalletizers |

| Hybrid Cells |

| Food and Beverage |

| Consumer Packaged Goods (CPG) |

| Pharmaceuticals and Healthcare |

| Industrial and Chemicals |

| E-commerce and 3PL |

| Fully-automatic Systems |

| Semi-automatic Systems |

| Manual Assist / Collaborative |

| Corrugated Cases |

| Shrink-wrapped Bundles |

| Bags and Sacks |

| Drums and Pails |

| RPCs and Totes |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Conventional Palletizers | ||

| Robotic Palletizers | |||

| Cobots and Mobile Robots | |||

| Depalletizers | |||

| Hybrid Cells | |||

| By End-Use Industry | Food and Beverage | ||

| Consumer Packaged Goods (CPG) | |||

| Pharmaceuticals and Healthcare | |||

| Industrial and Chemicals | |||

| E-commerce and 3PL | |||

| By Automation Level | Fully-automatic Systems | ||

| Semi-automatic Systems | |||

| Manual Assist / Collaborative | |||

| By Packaging Material Handled | Corrugated Cases | ||

| Shrink-wrapped Bundles | |||

| Bags and Sacks | |||

| Drums and Pails | |||

| RPCs and Totes | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the tertiary packing and palletizing solutions market in 2025?

The tertiary packing and palletizing solutions market size is USD 17.14 billion in 2025.

What is the expected growth rate for palletizing cobots through 2030?

Cobots and mobile robots are projected to expand at a 15.3% CAGR over 2025-2030.

Which region is growing fastest for palletizing automation?

Asia-Pacific leads with a 10.4% CAGR, driven by manufacturing expansion and government incentives.

What share do fully-automatic systems hold today?

Fully-automatic palletizers account for 56.82% of 2024 revenue.

Why are reusable RPCs influencing palletizing investments?

RPCs and totes are rising at an 11.5% CAGR because circular economy mandates demand reusable packaging, pushing adoption of vision-enabled palletizers.

What is the main barrier to brownfield palletizing upgrades?

High upfront capex, which can reach 60-80% above greenfield spending, lengthens payback schedules for legacy facilities.

Page last updated on: