Contract (Co-Packing) Services In Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

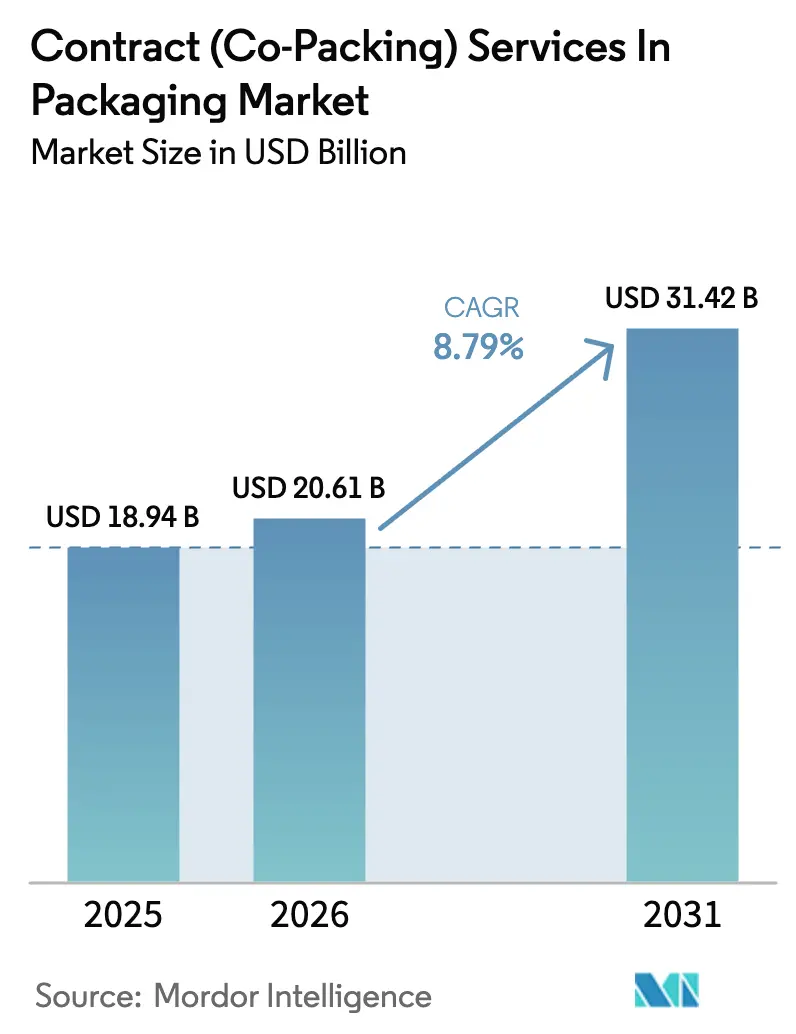

| Market Size (2026) | USD 20.61 Billion |

| Market Size (2031) | USD 31.42 Billion |

| Growth Rate (2026 - 2031) | 8.79% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contract (Co-Packing) Services In Packaging Market Analysis by Mordor Intelligence

The contract packaging services market size in 2026 is estimated at USD 20.61 billion, growing from 2025 value of USD 18.94 billion with 2031 projections showing USD 31.42 billion, growing at 8.79% CAGR over 2026-2031. Improved e-commerce penetration, growing pharmaceutical outsourcing, and stringent sustainability mandates are the primary accelerants for the contract packaging services market. Brand owners are further shifting non-core operations to external partners, with 67% of manufacturers indicating sustained or higher reliance on co-packers, reinforcing long-term volume visibility. The Asia-Pacific region already contributes nearly half of the global revenue, and technology spending on robotics, predictive maintenance, and smart conveyors is strengthening productivity while mitigating labor constraints. In parallel, sustainability regulations are driving the adoption of recyclable, PCR, and compostable substrates, positioning co-packers with materials science expertise to capture an incremental share. Private equity interest, validated by the USD 16.5 billion Catalent transaction, signals confidence in the sector’s durable growth and defensive cash flows. Margin volatility tied to resin prices remains a near-term headwind; however, diversification of feedstocks and formula-based price adjustment clauses support profitability improvements.

Key Report Takeaways

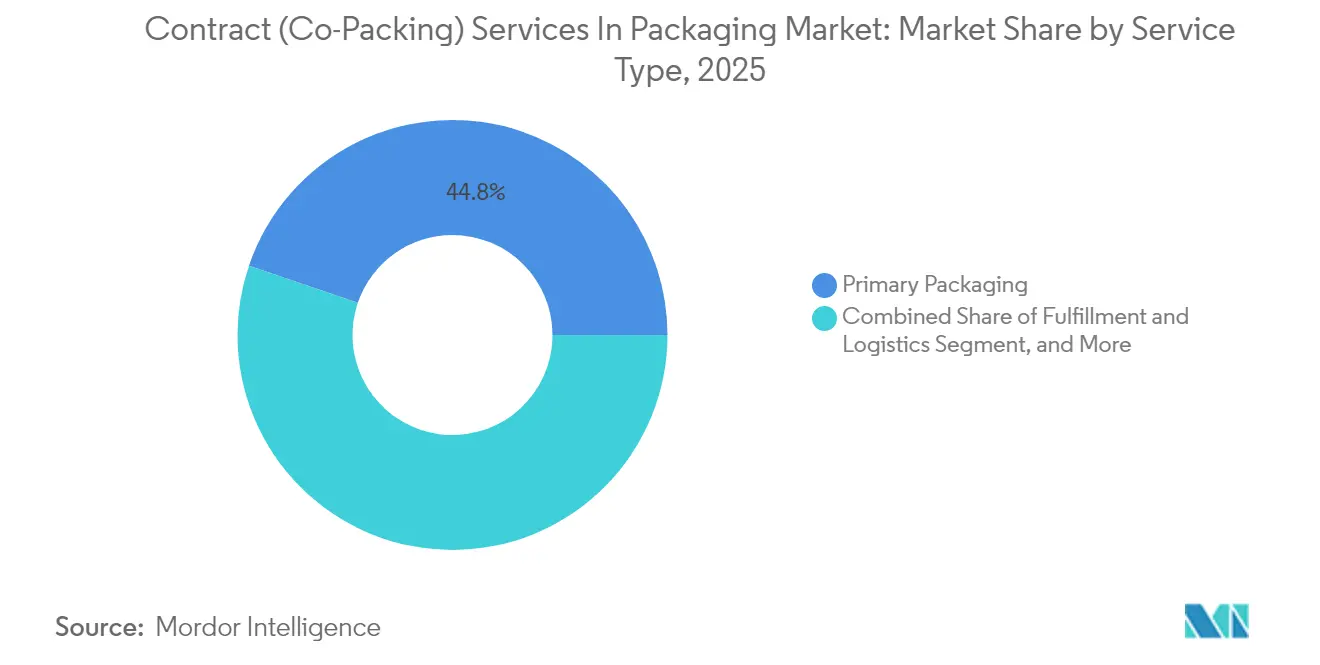

- By service type, primary packaging captured 44.78% of the Contract (Co-packing) Services in Packaging Market share in 2025.

- By material, Contract (Co-packing) Services in Packaging Market size for compostable substrates is projected to grow at a 10.78% CAGR between 2026-2031.

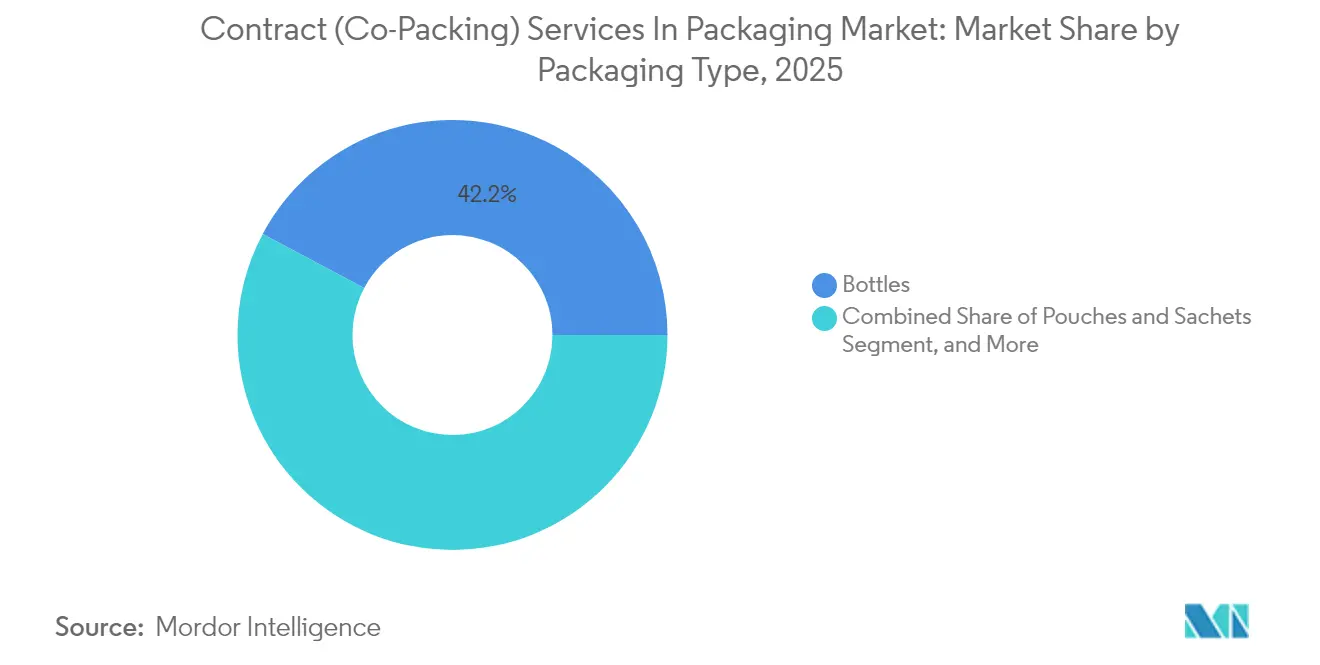

- By packaging type, bottles captured 42.21% of the Contract (Co-packing) Services in Packaging Market share in 2025.

- By end user industry, Contract (Co-packing) Services in Packaging Market size for personal care and cosmetics is projected to grow at 11.05% CAGR between 2026-2031.

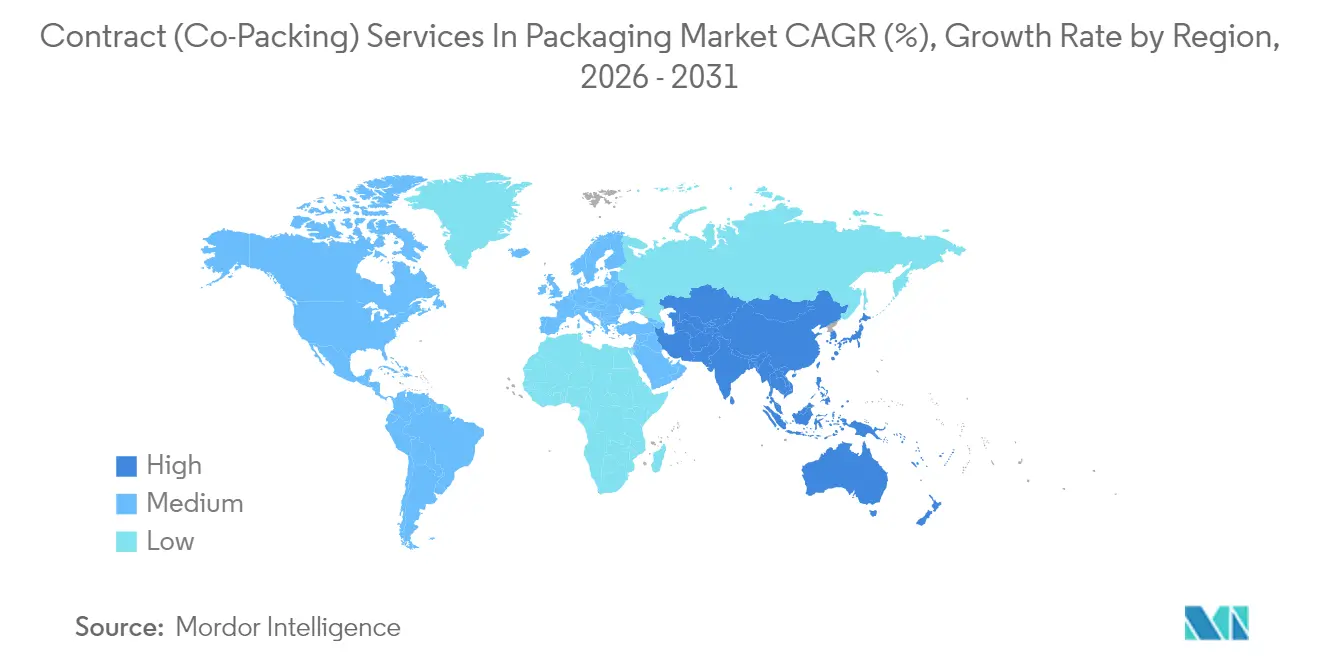

- By geography, Asia-Pacific captured 45.66% of the Contract (Co-packing) Services in Packaging Market revenue share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Contract (Co-Packing) Services In Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising E-Commerce and Omnichannel Packaging Demand | +2.3% | Global, with concentration in North America, Europe, and Asia-Pacific urban centers | Medium term (2-4 years) |

| Growth In Pharmaceutical Outsourcing for Specialized Packaging | +1.8% | Global, with emphasis on the US, EU, and India pharmaceutical hubs | Long term (≥ 4 years) |

| Sustainability Regulations Accelerating Shift to Recyclable Formats | +1.5% | Europe is leading, expanding to North America and selecting APAC markets | Medium term (2-4 years) |

| Automation And Industry 4.0 Adoption Improving Co-Packer Productivity | +1.4% | Developed markets initially, scaling to emerging economies | Long term (≥ 4 years) |

| Demand For Value-Added Fulfillment-Plus-Packaging Bundles | +1.2% | E-commerce concentrated regions: North America, Western Europe, China | Short term (≤ 2 years) |

| Surge In Biologics and Personalized Medicine Needing Aseptic Co-Packing | +0.8% | US, EU, Japan, with emerging presence in Singapore, India | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising E-Commerce and Omnichannel Packaging Demand

Direct-to-consumer shipping requires packaging to withstand compression, vibration, and climatic variations while maintaining a polished unboxing experience that shapes brand perception. Amazon’s frustration-free standards influence global material grammage, void fill, and dimensional limits, obliging co-packers to invest in variable-size automation and on-demand printing, cited by 73% of firms upgrading flexible equipment in 2024.[1]Amazon Sustainability Program, “Packaging Research and Development 2024,” aboutamazon.com Omnichannel merchandising compounds complexity, as one design must satisfy both shelf visibility and parcel handling requirements. International parcel rules further increase labeling and material requirements, so multi-regional co-packers that centralize compliance, printing, and fulfillment enjoy measurable cycle-time savings and penalty avoidance.

Growth in Pharmaceutical Outsourcing for Specialized Packaging

Ninety-four percent of pharmaceutical executives plan to utilize external packaging partners more frequently to acquire aseptic expertise and access capital-intensive fill-and-finish infrastructure. Biologics, antibody-drug conjugates, and cell therapies require ISO 5 clean rooms, nested syringes, and cold-chain validation, which are often unviable to replicate internally for many sponsors. Revised EU GMP Annex 1 demands more rigorous contaminant control, pushing sterile injectables toward contract packaging specialists that offer end-to-end validation and real-time environmental monitoring. The regulation-induced hurdle elevates switching costs and secures multi-year capacity reservations for qualified service providers.

Sustainability Regulations Accelerating Shift to Recyclable Formats

Extended Producer Responsibility schemes across 27 EU states require brand owners to finance downstream recovery, imposing penalties for non-recyclable formats and promoting the adoption of compostable or PCR resins. Compostable substrates are the fastest-growing material cohort, with a 10.95% CAGR, yet moisture barrier and heat-seal limitations demand formulation support that contract packagers increasingly embed via on-site laboratories. California’s 30% PCR mandate for rigid plastic packaging by 2030 heightens U.S. momentum, compelling co-packers to invest in equipment for processing, drying, and color correction of recycled polymers. Providers integrating lifecycle analytics gain a consultative edge while shielding clients from non-compliance levies.

Automation and Industry 4.0 Adoption Improving Co-Packer Productivity

With 750,000 manufacturing vacancies in the United States and 176,000 similar gaps in Germany, robotics serves as the primary lever to sustain throughput. Global packaging robot expenditures are projected to triple to USD 15.73 billion by 2032, offering pick-and-place versatility and clean-room repeatability. Vision systems and AI-driven predictive maintenance reduce changeover hours by up to 40% and curb micro-stoppages, expanding effective line utilization without enlarging the footprint. Remote monitoring dashboards also enhance audit readiness for pharmaceutical and food clients, streamlining quality assurance while reducing manual documentation overhead.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Resin and Substrate Prices Squeezing Margins | -1.2% | Global, with particular impact in regions dependent on imported raw materials | Short term (≤ 2 years) |

| Brand Owners' Reluctance to Cede Quality Control To Third Parties | -0.8% | Developed markets with established in-house capabilities, particularly North America and Europe | Medium term (2-4 years) |

| Fragmented EPR Laws Raising Compliance Complexity | -0.7% | Europe leading, expanding to North America and select APAC markets with varying regulatory frameworks | Medium term (2-4 years) |

| Clean-Room Labor Shortages Limiting Sterile Capacity Ramp-Ups | -0.6% | Developed pharmaceutical manufacturing hubs: US, EU, Japan, with emerging impact in India and China | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Resin and Substrate Prices Squeezing Margins

Polyethylene and polypropylene spot prices fluctuated by 23% in 2024 due to volatility in crude oil prices, logistics disruptions, and force-majeure events at Gulf Coast crackers. Co-packers typically renegotiate input escalators quarterly or semiannually; however, rapid spikes can create margin compression and working-capital strain. Diversification into PCR feedstocks, long-term offtake partnerships, and hedging instruments partially buffers volatility, though smaller regional players with limited scale remain exposed. Elevated inventory to ensure supply continuity, further tying capital and warehouse space, which encourages consolidation or strategic alliances for purchasing leverage.

Brand Owners Reluctance to Cede Quality Control to Third Parties

Regulated industries prize traceability and rapid deviation resolution, making some corporates hesitant to outsource primary packaging of temperature-sensitive or sterile products. Drafting comprehensive quality agreements, conducting linked audit programs, and integrating electronic batch records increase transaction costs and delay ramp-up. Intellectual property concerns persist in the cosmetics and OTC categories, where formulation disclosure accompanies packaging blueprints. Market leaders counter these objections by offering joint-governance structures, validated data connectivity, and serialized packaging lines that comply with FDA and EU directives; however, reluctance still dampens outsourcing velocity in certain segments.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Primary Packaging Leads While Fulfillment Gains Velocity

Primary packaging accounted for 44.78% of the contract packaging services market share in 2025, anchored by regulated industries that outsource aseptic vial filling, blister thermoforming, and barrier pouching. Pharmaceutical sponsors are increasingly offloading low-volume, specialized biologics runs to external clean-room suites, thereby locking in multi-year capacity to de-risk capital deployment and accelerate approval cycles. Nutraceutical and OTC firms also rely on serializable blister platforms to meet the timelines established by the U.S. Drug Supply Chain Security Act. Secondary packaging maintains steady inbound demand for display cartons and multipacks, yet price competition limits margin expansion.

The fulfillment-plus-packaging bundle is the bright spot, expanding at 10.65% CAGR as brands pursue single-invoice solutions that consolidate kitting, inventory, and last-mile delivery. Co-packers are incorporating automated sortation, carton-right-sizing, and transportation management systems to capture this stickier, higher-margin work, reshaping the trajectory of the contract packaging services market size toward integrated logistics engagement. The revenue mix is thus tilting toward providers with warehousing footprints adjacent to parcel hubs or inland ports.

By Material Type: Plastics Dominant yet Compostables Rise

Plastics accounted for 48.53% of 2025 revenue, thanks to attractive economics, lightweight benefits, and broad resin availability. Polyethylene films remain the default choice for perishable food pouches, while polypropylene rigid tubs support heat-stability needs in microwavable applications. Nevertheless, the volatility of resin and consumer pushback on single-use plastics accelerate diversification. Compostable substrates show a 10.78% CAGR as food service chains and beauty start-ups adopt polylactic acid and PBAT blends. Co-packers that master moisture-barrier coatings and low-temperature sealability position themselves for gains in the contract packaging services market share.

Paper and paperboard reclaim attention through e-commerce shippers that optimize cubic efficiency and curbside recyclability. Metal and glass persist in niche segments where oxygen sensitivity and premium aesthetics outweigh cost. Capex allocation is increasingly earmarked for extrusion lamination lines that process PCR and bio-based films, as well as for optical sorters ensuring feedstock purity. Such preparedness not only mitigates the risk of upcoming waste levies but also creates consultative upsell opportunities for brands struggling to meet their carbon footprint targets.

By Packaging Type: Bottles Retain Scale as Pouches Accelerate

Bottles represented 42.21% of the contract packaging services market size in 2025, underpinned by ubiquitous use in beverages, OTC liquids, and personal care. Lightweight polyethylene terephthalate remains the preferred material for water and carbonated drinks, while high-density polyethylene is suitable for pharmaceutical syrups that require child-resistant closures. Enhanced barrier resins and in-mold laser coding strengthen anti-counterfeiting and traceability.

Pouches, however, are the fastest riser at an 11.16% CAGR. Flexible formats reduce shipping mass and offer spout or zipper reclose features that improve consumer convenience. Single-serve stick packs are flourishing in sports nutrition and medical nutrition, taking market share from rigid sachets. Cartons and boxes maintain relevance as secondary containment, especially in e-commerce, where impact resistance and brand visibility are crucial. Blisters protect sensitive tablets from humidity and light, while shrink sleeves provide premium 360-degree graphics and tamper evidence.

By End-user Industry: Food and Beverage Dominates as Personal Care Accelerates

Food and beverage captured 38.62% of 2025 revenue, with stringent HACCP controls steering companies toward co-packers certified under BRCGS, FDA, and SQF schemes. Seasonal surges in confectionery and beverage categories rely on outsourced capacity to avoid capital underutilization. Growth is steady but incremental because large FMCG firms have already optimized outsourcing for decades. Personal care and cosmetics are expanding at a 11.05% CAGR, driven by indie and clean-beauty labels that lack in-house filling equipment.

Demand centers on airless pumps, droppers, and refill pods that require specialized machinery and minimal exposure to oxygen. Pharmaceuticals remain a pillar, especially for biologics and autoinjector kitting, as continuous temperature assurance and strict sterility drive high average selling prices. Consumer electronics, although a smaller slice, prefer antistatic and precision foam inserts whose dimensional tolerances are better met by automated co-packers.

Geography Analysis

Asia-Pacific generated 45.66% of global revenue in 2025 and is growing at an 10.92% CAGR, led by China’s integrated resin-to-packaging value chain and India’s double-digit pharmaceutical export growth. Many Chinese facilities are retrofitting robotic case packers to offset wage inflation and comply with updated emission norms. Indian co-packers are incorporating clean-room modules and serialization to meet the expectations of the U.S. Food and Drug Administration audits, thereby fueling the regional expansion of the contract packaging services market. Japan contributes mechatronic know-how and a zero-defect culture, encouraging collaborations that transfer lean methodologies to the broader region. South Korea’s cosmetics exporters rely on premium airtight compacts and sachets, sustaining high-margin assignments for local co-packers.

North America remains the second-largest cluster, driven by biopharmaceutical and functional food outsourcing. Labor scarcity has triggered the accelerated deployment of robots in blistering and cartoning cells across Midwest hubs. Mexico’s near-shore attractiveness under the United States-Mexico-Canada Agreement delivers cost relief and supply-chain resilience, luring beverage and seasonal confectionery programs south of the border. Canada leverages clean-label brand activity and national cannabis regulations to carve out specialization niches. Europe emphasizes circular-economy compliance across member states, prompting packaging redesign and line retrofits to achieve 100% recyclability by 2031. Germany’s shortage of 176,000 skilled workers has elevated automation budgets, while Italy and the Netherlands advance cold-chain innovations for biosimilars. [2]German Federal Employment Agency, “Labor Market Report 2024,” Eastern European economies offer capacity overflow solutions for Western brand owners coping with soaring energy costs. The Middle East and Africa presently represent a smaller base, yet pharmaceutical industrialization in Saudi Arabia and South Africa signals upcoming demand for GMP-accredited packing hubs.

Competitive Landscape

The contract packaging services market demonstrates moderate fragmentation. The top five providers collectively hold an estimated 32-35% of the revenue, keeping the rivalry intense yet avoiding dominance. Pharmaceutical subsegments tend to be more consolidated due to regulatory entry barriers. The 2024 Catalent acquisition by Novo Holdings, valued at USD 16.5 billion, underscores private equity's conviction in the resilience of biologics packaging and cross-selling.[3]Financial Times Editorial Desk, “Novo Holdings Catalent Acquisition 2024,” ft.com

Other landmark deals include Silgan’s USD 2.3 billion purchase of Berry Global assets to add child-resistant closures, and Tjoapack’s EUR 45 million (USD 49.1 million) automation upgrade to scale blister serialization. Differentiation hinges on comprehensive capability sets that combine formulation advice, smart factory platforms, and downstream logistics. Early adopters of AI-enabled predictive maintenance and camera-based quality inspection report yield improvements above 5%, translating to stickier multi-year contracts.

Sustainability certifications, such as ISCC-Plus, FSC, and EcoVadis, help build trust with consumer-facing brands that are eager to convey their green narratives. Digital disruptors offer online configurators, rapid quoting, and small-batch agility that threaten traditional high-volume incumbents unless they deploy similar cloud platforms. Consequently, the contract packaging services market is likely to witness incremental consolidation, primarily targeting regional players with specialized material or regulatory skill sets.

Contract (Co-Packing) Services In Packaging Industry Leaders

Assemblies Unlimited Inc.

Silgan Holdings Inc.

Stamar Packaging Inc.

Veritiv Corporation

Co-Pak Packaging Corp.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: PCI Pharma Services committed USD 365 million to expand aseptic filling capacity, adding ISO 5 suites, automated lyophilization, and high-speed syringe lines to meet the burgeoning demand for biologics.

- December 2024: Novo Holdings finalized the USD 16.5 billion Catalent acquisition, forming the largest global CDMO spanning drug substance, fill-finish, and advanced packaging.

- November 2024: Silgan Holdings bought Berry Global’s specialty rigid assets for USD 2.3 billion, adding child-resistant closure technology to its pharmaceutical portfolio.

- October 2024: Veritiv established a sustainable packaging division via supplier partnerships for compostable clamshells and molded fiber mailers aimed at food service and e-commerce channels.

Global Contract (Co-Packing) Services In Packaging Market Report Scope

| Primary Packaging |

| Secondary Packaging |

| Tertiary Packaging |

| Design and Engineering |

| Fulfillment and Logistics |

| Plastic |

| Paper and Paperboard |

| Metal |

| Compostable |

| Glass |

| Bottles |

| Blister Packs |

| Pouches and Sachets |

| Cartons and Boxes |

| Shrink Sleeves and Wraps |

| Other Packaging Type |

| Food and Beverage |

| Personal Care and Cosmetics |

| E-commerce and Retail |

| Pharmaceuticals |

| Consumer Electronics |

| Other End-user Industry |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Service Type | Primary Packaging | ||

| Secondary Packaging | |||

| Tertiary Packaging | |||

| Design and Engineering | |||

| Fulfillment and Logistics | |||

| By Material Type | Plastic | ||

| Paper and Paperboard | |||

| Metal | |||

| Compostable | |||

| Glass | |||

| By Packaging Type | Bottles | ||

| Blister Packs | |||

| Pouches and Sachets | |||

| Cartons and Boxes | |||

| Shrink Sleeves and Wraps | |||

| Other Packaging Type | |||

| By End-user Industry | Food and Beverage | ||

| Personal Care and Cosmetics | |||

| E-commerce and Retail | |||

| Pharmaceuticals | |||

| Consumer Electronics | |||

| Other End-user Industry | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What CAGR is projected for the contract packaging services market through 2031?

The market is expected to grow at an 8.79% CAGR between 2026 and 2031 based on revenue projections in this analysis.

Which region currently leads global revenue?

The Asia-Pacific region holds 45.66% of the global revenue, benefiting from its manufacturing scale and pharmaceutical export growth.

Which service type is expanding the fastest?

Fulfillment and logistics services are advancing at a 10.65% CAGR, driven by integrated packaging-plus-delivery demand.

How are sustainability mandates influencing material choices?

Extended Producer Responsibility laws are accelerating the adoption of compostable and PCR materials, with compostables rising at a 10.78% CAGR.

Why are pharmaceutical companies increasing outsourcing?

Complex biologic formulations and new GMP requirements make aseptic filling and specialized packaging more cost-effective when handled by expert contract partners.

What is the major restraint affecting profit margins?

Volatile resin and substrate prices, fluctuating by as much as 23% year after year, compress margins, especially for smaller co-packers.

Page last updated on: