Oman Containerboard Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

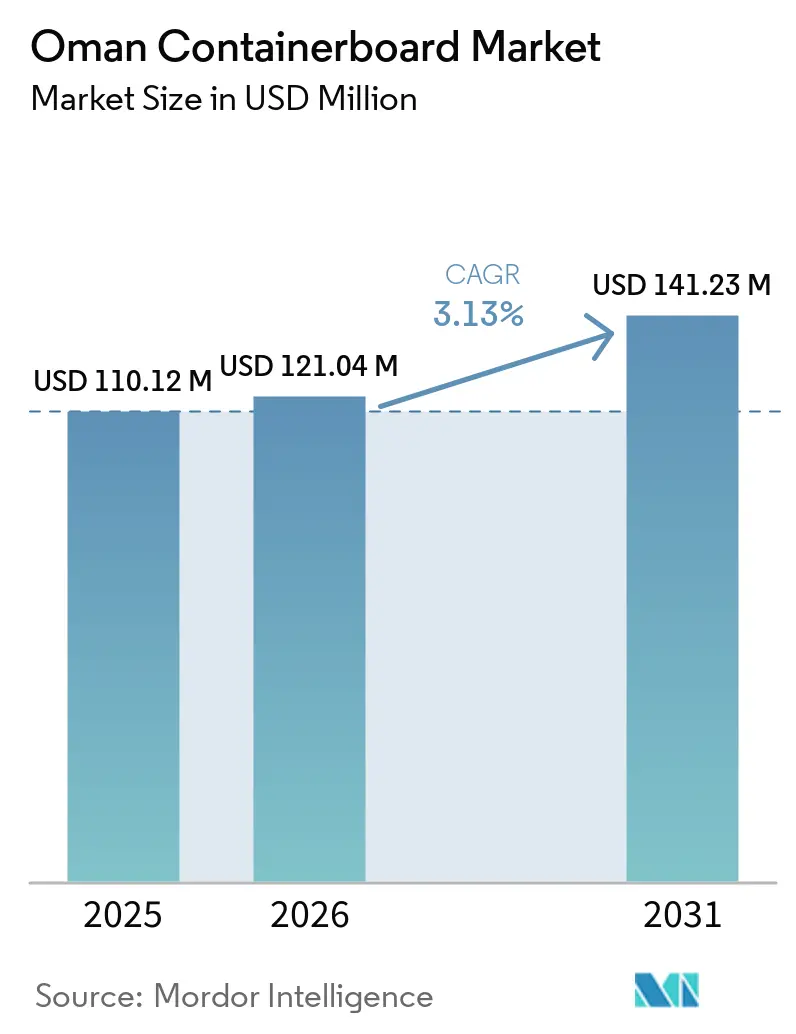

| Base Year Market Size (2025) | USD 110.12 Million |

| Market Size (2026) | USD 121.04 Million |

| Market Size (2031) | USD 141.23 Million |

| Growth Rate (2026 - 2031) | 3.13% CAGR |

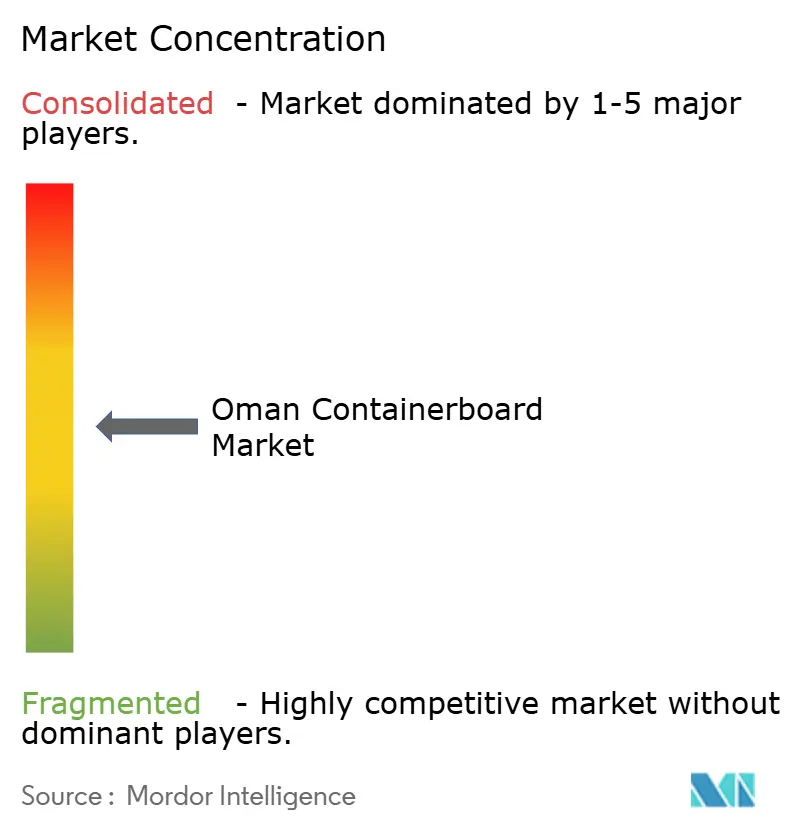

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Oman Containerboard Market Analysis by Mordor Intelligence

The Oman Containerboard Market size is expected to increase from USD 110.12 million in 2025 to USD 121.04 million in 2026 and reach USD 141.23 million by 2031, growing at a CAGR of 3.13% over 2026-2031.

The 2026 demand base already reflects stronger offtake from food processing, retail paper conversion, and parcel-linked shipping activity. The Oman containerboard market is also becoming less tied to oil-linked swings because non-oil manufacturing, logistics, and export processing continue to widen under Vision 2040. Port expansion across Sohar, Salalah, and Duqm is increasing the flow of re-export goods and processed cargo that require corrugated transit formats. Competition is tightening as domestic operators face pressure from larger GCC converters with broader regional distribution reach and more integrated paper supply. Even so, the Oman containerboard market continues to show durable headroom because demand is being supported by food security investments, plastic substitution, cold-chain build-out, and broader packaging upgrades across consumer channels.

Key Report Takeaways

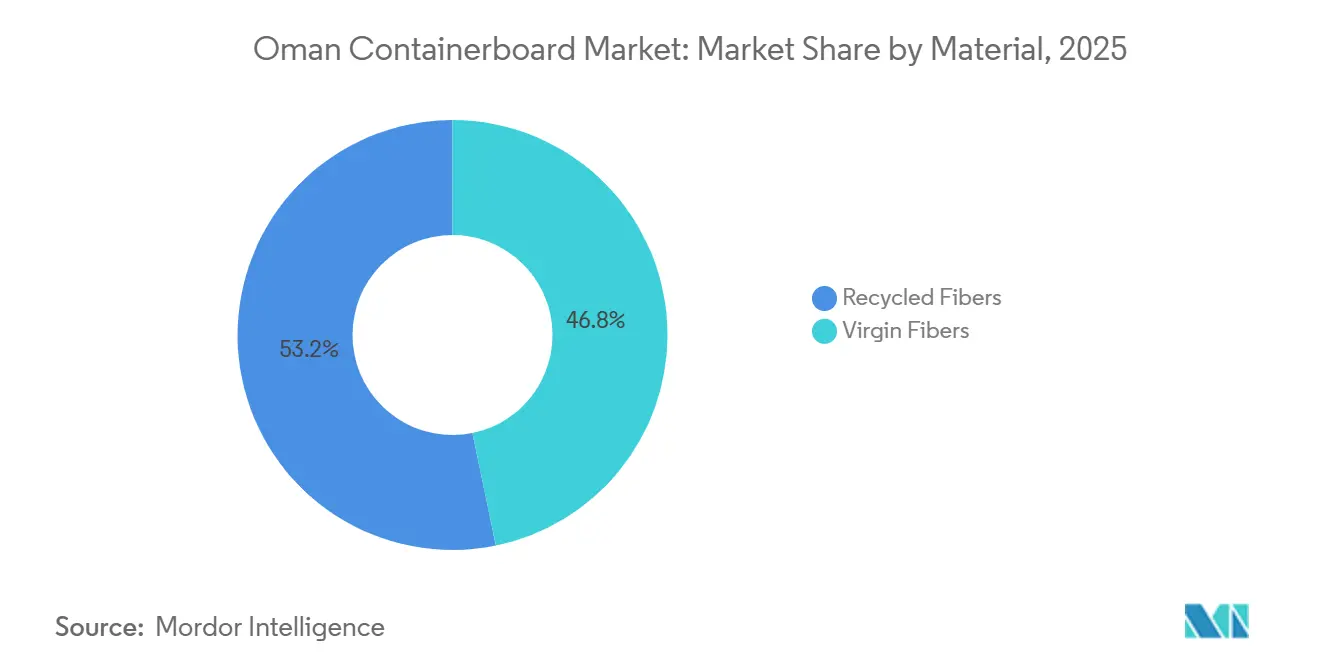

- By material, recycled fibers held 53.22% of the Oman containerboard market share in 2025, and recycled fibers are projected to record the fastest growth within the material split at a 5.08% CAGR through 2031.

- By product type, testliners accounted for 43.34% of the Oman containerboard market size in 2025, while flutings are forecast to post the highest CAGR at 5.33% over 2026-2031.

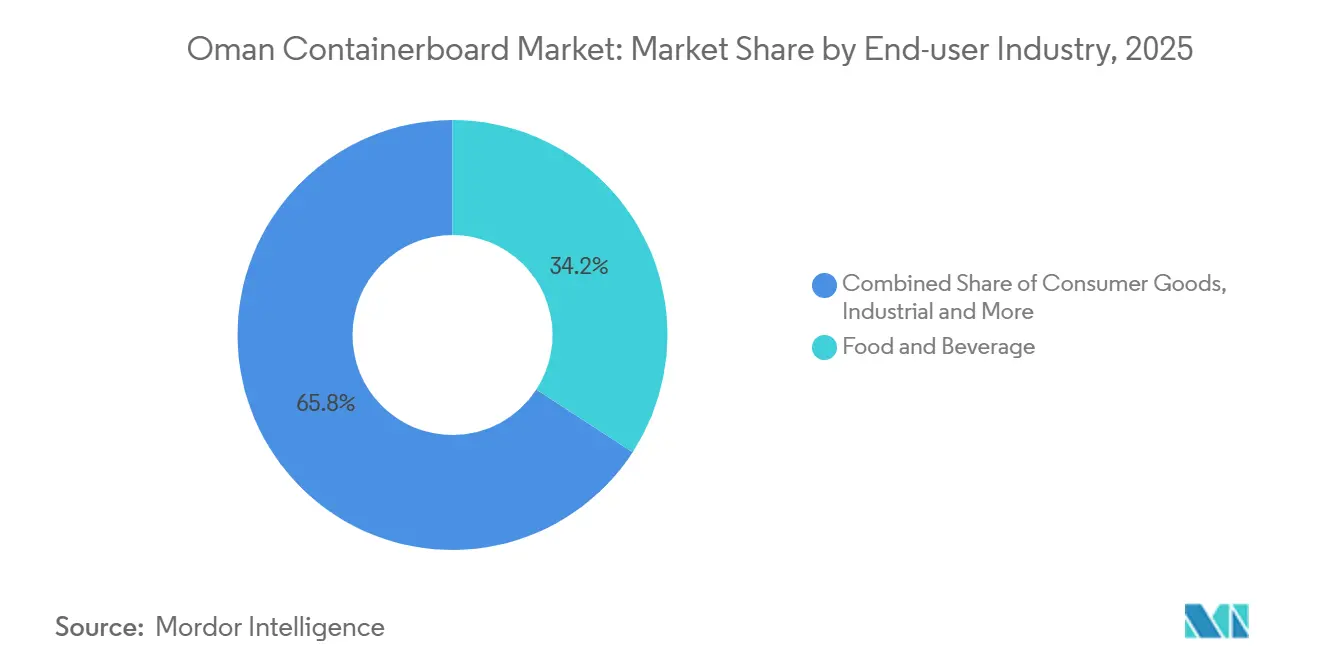

- By end-user industry, food and beverage captured 34.19% of the Oman containerboard market in 2025, while consumer goods packaging is expected to expand at a 4.79% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Oman Containerboard Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Food Security And Local Food Processing Build-Out | +1.1% | National - Muscat, Sohar, Khazaen, Salalah, Duqm | Medium term (2-4 years) |

| E-commerce Parcel Expansion | +0.8% | National, concentrated in Muscat Capital Area and Batinah corridor | Short term (≤ 2 years) |

| Plastic Bag Phase-Out Favoring Paper Conversion | +0.5% | National - all retail and food service sectors | Short term (≤ 2 years) |

| Port And Free-Zone Throughput Expansion | +0.4% | Sohar, Salalah, Duqm, with spill-over to GCC export corridors | Medium term (2-4 years) |

| Recycled Fiber Localization Momentum | +0.3% | Sohar industrial zone, with influence from Muscat and Batinah | Long term (≥ 4 years) |

| Premium Shelf-Ready Export Packaging Demand | +0.2% | Salalah free zone, Duqm Special Economic Zone | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Food Security And Local Food Processing Build-Out

Oman’s food security push remains the strongest near-term demand driver for the Oman containerboard market because new processing capacity directly lifts corrugated consumption across protein, seafood, feed, and packaged food lines.[1]Editorial Team, “JBS and Oman Food Capital Partner to Build Global Multiprotein Export Hub,” Feed and Additive Magazine, feedandadditive.com In May 2026, Invest Oman unveiled a USD 224 million package centered on aquaculture expansion, alternative fish feed production, and shrimp farming complexes across multiple governorates, which deepens the requirement for moisture-resistant and food-safe transport packaging. JBS committed USD 150 million in January 2026 to establish an integrated beef, poultry, and lamb export hub in Oman, and that project adds industrial-scale demand for wax-resistant corrugated boxes built for cold-chain logistics. Madayn’s industrial cities already hosted 121 food sector projects, and 28 new food projects were added in 2025, which shows that the packaging load is spreading across a wider industrial base rather than staying concentrated in one niche cluster. The report material also shows that each new food processing facility can generate 0.8-1.2 kg of corrugated packaging per kilogram of exported finished product, which turns production growth into a sustained pull on containerboard demand. This mix of export proteins, aquaculture, feed, and processed foods gives the Oman containerboard market a broader and steadier demand foundation than retail carton use alone.

E-commerce Parcel Expansion

Parcel activity became a more visible demand engine for the Oman containerboard market in 2025 as online transaction volumes rose sharply and logistics investment kept widening delivery capacity. Oman’s e-commerce transactions increased from 67.5 million in 2024 to 168.8 million in 2025, which lifted demand for transit-weight corrugated boxes across direct-to-consumer and store-replenishment channels.[2]Staff Reporter, “Oman’s e-Commerce Transactions Surge 150% to Reach 168 Million in 2025,” The Arabian Stories, thearabianstories.comThe impact is larger than the headline number suggests because last-mile coverage is still widening, so each new fulfillment point creates fresh demand for parcel cartons, inserts, and protective fluting grades. Desert heat is also changing specification needs, with parcel formats increasingly favoring high-performance fluting and adhesive systems that can tolerate temperatures above 45°C. Digital inkjet capability is starting to matter in this channel because it supports variable data, QR codes, and short runs without the tooling burden of conventional print setups. As the logistics sector continued to absorb OMR 3.4 billion in investment during the Tenth Five-Year Plan, the Oman containerboard market gained a stronger operating base for recurring parcel-box demand.

Plastic Bag Phase-Out Favoring Paper Conversion

The phased ban on single-use plastic shopping bags is shortening paper conversion timelines across retail and food service, which directly supports the Oman containerboard market. Environment Authority Decision No. 8/2024 has added sectors every six months since July 2024, and Phase 3 took effect on July 1, 2025 for grocers, bakeries, sweet shops, confectionery factories, fruit and vegetable outlets, and gift shops. Phase 4 came into effect on January 1, 2026 and extended the ban to building-materials dealers, agricultural supply stores, date retailers, animal-feed outlets, and ice cream and confectionery vendors. These are practical paper-conversion channels because they use lightweight corrugated trays, certified food-safe display units, and secondary transit boxes rather than only simple carry bags. Compliance fines of OMR 50-1,000 per violation, with penalties doubling for repeat breaches, are encouraging retailers to secure alternative paper-packaging supply ahead of the full January 2027 deadlin. Oman also had 83 recycling firms active in 2025, which indicates that the supporting waste-processing base for paper substitution is beginning to widen alongside the ban.

Port And Free-Zone Throughput Expansion

Port and free-zone expansion is raising the trade-linked demand ceiling for the Oman containerboard market by increasing cargo flows, re-exports, and industrial processing activity. Oman’s ports handled 5 million TEUs and 143 million tonnes of cargo in 2025, while first-half container throughput rose 11.7% year over year, which points to a larger packaging base around national gateway infrastructure. Sohar Port and Freezone recorded 72 million metric tonnes of throughput in 2025 and secured USD 968 million in new investment across 8 leasing agreements, which supports a wider mix of manufacturing and export-oriented box demand. The Port of Salalah completed a USD 300 million expansion in early 2025, lifted annual handling capacity from 4.5 million to 6.5 million TEUs, and added 2,000 reefer plugs, which strengthens the case for moisture-resistant corrugated packaging in protein and perishables flows. Asyad Group started deploying an AI orchestration platform across Sohar and Salalah from May 2026 to cut average container dwell time by 22% within the first operating year, which can turn existing terminal capacity into faster packaging turnover. This operating setup also improves Oman’s appeal as a lower-cost GCC base for satellite converting plants that want tariff-free access to nearby demand centers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Imported Linerboard And Freight Volatility | -0.8% | National, acute at Muscat and Sohar entry points | Short term (≤ 2 years) |

| Limited Domestic Recovered Paper Depth | -0.5% | National, concentrated in Muscat and Sohar industrial belts | Medium term (2-4 years) |

| Power Cost And Utility Intensity | -0.4% | National - industrial zones in Muscat, Sohar, Salalah | Medium term (2-4 years) |

| Small Domestic Scale And Export-Cycle Sensitivity | -0.3% | National, amplified in Salalah and Duqm export-dependent zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Imported Linerboard And Freight Volatility

Imported linerboard exposure remains the most immediate constraint on the Oman containerboard market because a large share of virgin kraftliner and a meaningful share of recycled linerboard still comes from outside the country. Shipping disruption in the Red Sea during 2024 forced rerouting through the Cape of Good Hope, and that move sharply raised landed costs for paper delivered into Muscat. The burden was not limited to freight because war-risk insurance also moved up and tightened margins for converters that lacked scale, hedging tools, or preferred supplier allocation. Temporary sourcing from Turkey and Egypt provided only partial relief, since replacement routes still carried a 20-25% price premium over established European supply channels. The result is a market where top-line demand can improve while converter profitability remains uneven, especially for operators without integrated paper supply. That cost sensitivity keeps the Oman containerboard market exposed to any renewed shipping disruption, even when end-use demand stays firm.

Limited Domestic Recovered Paper Depth

Limited domestic old corrugated container collection still holds back the recycled side of the Oman containerboard market, even though recycled grades already form the leading material category. Keryas Paper Industry LLC operates a 180,000-metric-ton annual mill in Sohar, yet domestic collection covers only 15-20% of its recycled linerboard feedstock needs, leaving the balance to imported supply from outside Oman. Peer-reviewed research in 2025 identified weak public awareness, limited technology deployment, and uneven regulatory enforcement as the main obstacles to broader paper recovery in Oman. The same study noted that 43% of municipal solid waste was recycled across all material categories, which shows progress at system level but still not enough OCC capture for full mill utilization. This gap keeps recycled fiber costs elevated and slows the pace at which mills can deepen local sourcing despite strong sustainability pressure from buyers. Progress in material-recovery facilities and waste segregation pilots will determine whether the Oman containerboard market can reduce import dependence during the forecast window.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Recycled Fibers Define The Competitive Baseline

Recycled fibers accounted for 53.22% of the Oman containerboard market size in 2025, making them the leading material category by a clear margin. This lead matters because it has been built in a market where domestic OCC collection remains structurally thin, which forces mills to blend imported recovered fiber and accept tighter input economics in exchange for better sustainability positioning. That trade-off still works for many buyers because recycled grades remain cost-competitive against fully virgin alternatives during normal freight conditions. Recycled fibers are projected to grow at a 5.08% CAGR over 2026-2031, which is faster than the overall market rate and shows that substitution pressure is continuing to build.

Virgin fiber-based boards still retain a necessary place in export-facing food packaging where strength-to-weight performance, wet-strength tolerance, and print-surface quality cannot be fully matched by second-generation recycled grades. That is especially relevant in wax-lined boxes for fishery exports and other moisture-sensitive formats that move through long supply chains. The Oman containerboard industry therefore remains balanced between sustainability-led adoption and technical performance needs rather than moving in a straight line toward one fiber system. The waste-retention policy backdrop in Oman has raised the strategic value of domestic paper recovery infrastructure, while GCC circular economy signals continue to shape buyer specifications for corrugated packaging. As a result, recycled fibers set the commercial baseline, but virgin grades still hold an essential role in applications where export performance requirements are harder to compromise.

By Product Type: Fluting Gains Ground Amid Lightweighting Trends

Testliners held 43.34% of the Oman containerboard market in 2025, reflecting their established role as the dominant facing material in corrugated boxes used for food and beverage, mineral water, fisheries, and general industrial packing. That leadership remains tied to the broad installed base of conventional corrugated formats across Oman’s industrial estates and domestic distribution channels. Keryas Paper Industry LLC’s Sohar mill produces both testliner and fluting medium, which makes it the main domestic supplier supporting the country’s paper and box value chain. Kraftliners remain relevant at the premium end of the mix, especially in export-grade protein packaging that requires stronger burst performance and higher moisture resistance than recycled boards can consistently deliver.

The more important shift for the forecast period sits in fluting, which is expected to expand at a 5.33% CAGR over 2026-2031 and is the fastest-growing product category in the market. That rise is being driven less by traditional heavy transit boxes and more by lightweighting programs in e-commerce logistics and temperature-sensitive distribution. Box design is moving toward better cushioning through flute-profile optimization, including transitions such as B/C double-wall to C/E constructions, rather than by simply adding heavier facing grades. Licensing of Arcwise curved corrugated technology for MENA markets introduced a format that can deliver 20-30% higher compression strength at the same basis weight, which is likely to influence product specifications in Oman’s export and shelf-ready channels. In practical terms, the Oman containerboard industry is likely to keep testliners as the volume anchor while fluting captures more of the value created by performance-led redesign.

By End-User Industry: Food And Beverage Anchors Demand While Consumer Goods Rise Faster

Food and beverage held 34.19% of the Oman containerboard market in 2025, which kept it firmly in the lead among end-user industries. That position is supported by fisheries, mineral water, fresh produce, feed, and processed food activities that continue to scale under Oman’s non-oil industrial agenda. Consumer goods packaging is projected to grow at a 4.79% CAGR over 2026-2031, making it the fastest-growing end-use segment in the forecast period. Its growth is being shaped by urbanization, premiumization, and broader demand for shelf-ready corrugated formats in retail channels. As consumer assortments widen, corrugated display trays and die-cut formats gain relevance over standard slotted cartons in both organized retail and direct distribution.

Food and beverage should still retain its lead because several packaging-demand anchors are already in place or moving ahead. The Nizwa Dates Industrial Complex, the OMR 36 million feed factory at Khazaen Economic Zone, and the JBS multiprotein hub all support sustained use of moisture-resistant and food-grade corrugated packaging across domestic and export channels. Industrial end-uses also benefit from free-zone throughput growth and from the premium box demand created by engineered goods and export logistics. Other end-user industries remain smaller, but ceramics, personal care, and pharmaceuticals are each adopting more paper-based secondary packaging as retail plastic restrictions expand. This keeps the Oman containerboard market broad enough to avoid dependence on one single end-use channel, even though food and beverage remains the core volume base.

Geography Analysis

The Muscat Capital Area and the Al Rusayl-Sohar corridor remain the main production and consumption axis of the Oman containerboard market. Omani Packaging Company SAOG operates a 30,000-metric-ton corrugated converting plant at Al Rusayl Industrial Estate and serves local foodstuff, detergent, mineral water, ceramics, and fishery customers, with secondary exports to GCC and Asian markets.[3]Omani Packaging Company SAOG, “Company Profile,” Omani Packaging Company, omanipackaging.comThis customer mix ties Muscat-region demand to both domestic FMCG distribution and export packaging requirements. Sohar adds upstream weight because Keryas Paper Industry’s mill sits close to Sohar Port and Freezone, which shortens inbound raw-material lead times and supports faster outbound paper and box flows. The corridor therefore combines conversion, paper supply, industrial estates, and port access in one geography, which makes it the most efficient operating base in the country.

Salalah and the Dhofar region show a different demand profile because packaging demand there is tied more directly to cargo handling, fisheries, and cold-chain export activity. Port of Salalah’s general cargo volumes reached 26.4 million tonnes in 2025, up from 22.6 million tonnes in 2024, which points to a heavier base of traded goods moving through transport packaging systems. The terminal expansion completed in early 2025 lifted annual capacity from 4.5 million to 6.5 million TEUs and added 2,000 reefer plugs, which supports higher use of wax-resistant and moisture-barrier corrugated formats in perishables flows. Dhofar and nearby Duqm also benefit from fisheries and aquaculture projects, including the OMR 26 million (USD 67.6 million) tuna and sardine canning facility operated by Oman Food Investment Holding. These southern zones therefore pull the Oman containerboard market toward a more export-facing packaging mix than the Muscat corridor.

Duqm adds another layer because free-zone incentives and industrial land availability are drawing interest from regional converters that want a lower-cost GCC manufacturing base. The estimate that operating costs can run 20% below UAE industrial zones improves the case for satellite corrugated plants serving Saudi Arabia and the UAE from Oman. If that shift continues, the Oman containerboard market will rely less on Muscat-region converting capacity and gain a more balanced national supply network. The wider geographic spread also improves resilience because upstream paper, downstream conversion, port handling, and export packing are no longer concentrated in one corridor alone.

Competitive Landscape

The Oman containerboard market remains moderately fragmented at the converting level, even though one domestic mill gives the upstream chain a partial anchor. Keryas Paper Industry LLC’s 180,000-metric-ton Sohar facility supplies recycled testliner and fluting grades and remains the main domestic paper source for local converters.[4]Keryas Paper Industry LLC, “About Us,” Keryas Paper Industry, keryaspaper.com Omani Packaging Company SAOG represents the listed local converting tier and shows how demand exposure alone does not remove cost pressure in a market that still faces regular paper import risk. Regional groups such as INDEVCO Paper Containers, Obeikan Investment Group, and Napco National are strengthening their position through larger integrated assets and pan-GCC distribution reach. That structure leaves smaller Omani converters competing on response time, customer proximity, and niche service rather than on scale economics alone.

Several recent moves show how competition is shifting from simple box supply toward technology, margin protection, and wider packaging portfolios. INDEVCO Group used the Lebanese-Omani Economic, Trade and Industrial Forum in Muscat in October 2025 to reinforce its commercial presence in Oman. The same group’s 2025 Arcwise licensing for MENA markets introduced a curved corrugated format that can deliver 20-30% higher compression strength at the same basis weight, which matters in lightweighting applications. Napco National’s August 2025 acquisition of Arabian Flexible Packaging widened its offer into films and pouches, giving the group more room to cross-sell bundled packaging solutions to food and beverage buyers in Oman. These moves raise the bar for domestic players because customers can increasingly source corrugated, flexible, and specialty formats from one regional supplier.

A clear opening still exists in digital short-run converting, where variable-data printing and automated die-cutting can serve e-commerce runs below 5,000 units faster and more economically than traditional setups. Another underused differentiator is certified sustainable sourcing, since FSC or PEFC chain-of-custody documentation is becoming more relevant for institutional food buyers and GCC supermarket chains. Gulf Paper Manufacturing Company in Kuwait also remains important because its exported testliner and fluting support supply adequacy for Omani converters when local paper availability is tight. Overall, the Oman containerboard market is competitive enough to pressure margins, but still open enough for technology-led or certification-led specialists to win targeted contracts.

Oman Containerboard Industry Leaders

Keryas Paper Industry LLC

Middle East Paper Manufacturing and Production Company

United Carton Industries Company

INDEVCO Paper Making

Arabian Packaging LLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Oman’s Ministry of Commerce, Industry and Investment Promotion, through Invest Oman, unveiled a USD 224 million food security investment package focused on aquaculture expansion, alternative fish feed production, and shrimp farming complexes across multiple governorates. This investment directly expands the fisheries and food processing sectors that are among the primary users of wax-lined and moisture-resistant corrugated boxes, reinforcing long-term containerboard demand from the food segment.

- April 2026: Asyad Group announced the deployment of an AI orchestration platform across Sohar and Salalah ports from May 2026, targeting a 22% reduction in average container dwell time within the first operating year. Faster port throughput reduces transit-packaging dwell stress, enabling converters to design to lower safety-factor specifications and reducing material cost per box.

- January 2026: JBS, the world’s largest protein company, completed a USD 150 million acquisition of an 80% stake in a newly established food holding company in Oman consolidating 2 production assets for beef, poultry, and lamb export. The joint venture, designed to serve the global halal market, is expected to generate substantial demand for food-grade corrugated packaging aligned with cold-chain export standards.

Oman Containerboard Market Report Scope

The Oman Containerboard Market encompasses the production, distribution, and consumption of containerboard used in the manufacture of corrugated packaging solutions. It includes containerboard made from virgin and recycled fibers, covering key product types such as kraftliners, testliners, and flutings. These materials are primarily used in protective and transport packaging applications across various end-user industries, including food and beverage, consumer goods, industrial, pharmaceuticals, and agriculture. The market is driven by the increasing demand for sustainable, lightweight, and durable packaging solutions.

The Oman Containerboard Market Report is Segmented by Material (Virgin Fibers, and Recycled Fibers), Product Type (Kraftliners, Testliners, and Flutings), and End-User Industry (Food and Beverage, Consumer Goods, Industrial, and Other End-User Industries). The Market Forecasts are Provided in Terms of Value (USD).

| Virgin Fibers |

| Recycled Fibers |

| Kraftliners |

| Testliners |

| Flutings |

| Food and Beverage |

| Consumer Goods |

| Industrial |

| Other End-User Industries |

| By Material | Virgin Fibers |

| Recycled Fibers | |

| By Product Type | Kraftliners |

| Testliners | |

| Flutings | |

| By End-User Industry | Food and Beverage |

| Consumer Goods | |

| Industrial | |

| Other End-User Industries |

Key Questions Answered in the Report

What is the size of the Oman containerboard market?

The Oman containerboard market stood at USD 110.12 million in 2025, reached USD 121.04 million in 2026, and is forecast to reach USD 141.23 million by 2031 at a 3.13% CAGR.

What is driving demand for containerboard in Oman?

The main demand drivers are food processing expansion, the phased plastic bag ban, e-commerce parcel growth, and higher cargo throughput across Sohar, Salalah, and Duqm.

Which material segment leads in Oman?

Recycled fibers led the market with a 53.22% share in 2025, supported by cost competitiveness and stronger sustainability requirements from major buyers.

Which product type is growing the fastest?

Flutings are expected to record the fastest growth at a 5.33% CAGR through 2031, driven by lightweighting needs in e-commerce and cold-chain logistics.

Which end-user segment is most important in Oman?

Food and beverage remained the largest end-user with a 34.19% share in 2025, while consumer goods packaging is expected to grow the fastest at a 4.79% CAGR.

Why do freight and linerboard imports matter so much in Oman?

Oman still depends heavily on imported linerboard, so shipping disruption and higher war-risk costs can quickly squeeze converter margins even when demand remains healthy.

Page last updated on: