Argentina Container Glass Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

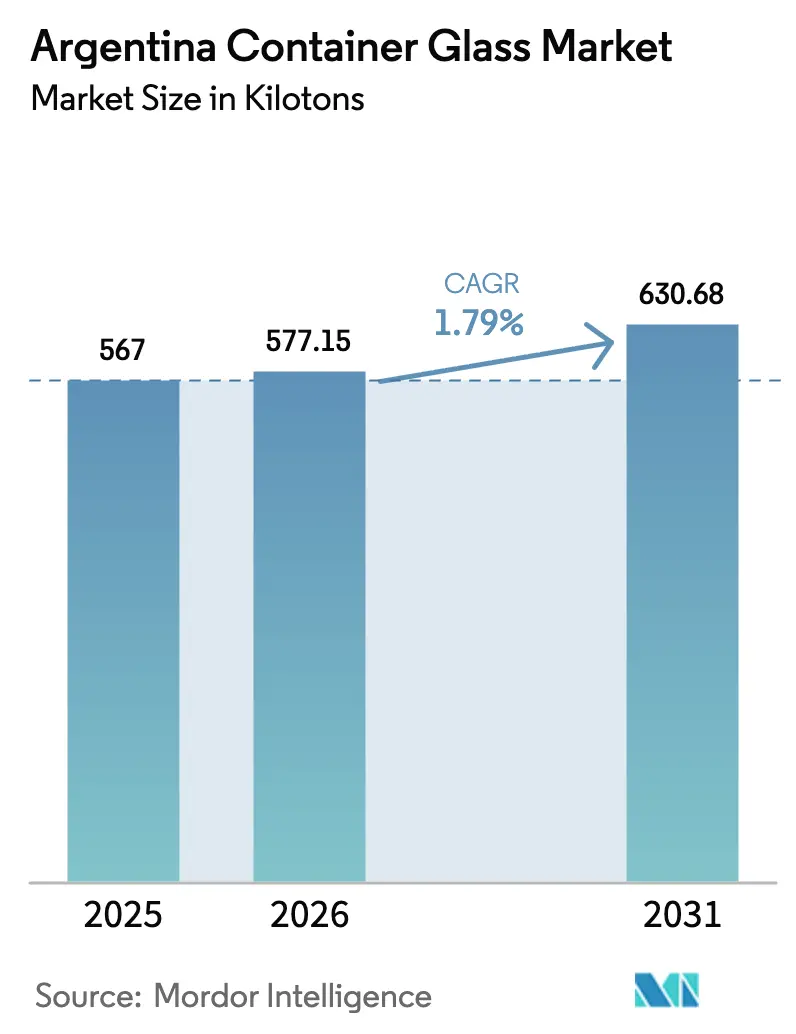

| Base Year Market Size (2025) | 567 kilotons |

| Market Volume (2026) | 577.15 kilotons |

| Market Volume (2031) | 630.68 kilotons |

| Growth Rate (2026 - 2031) | 1.79% CAGR |

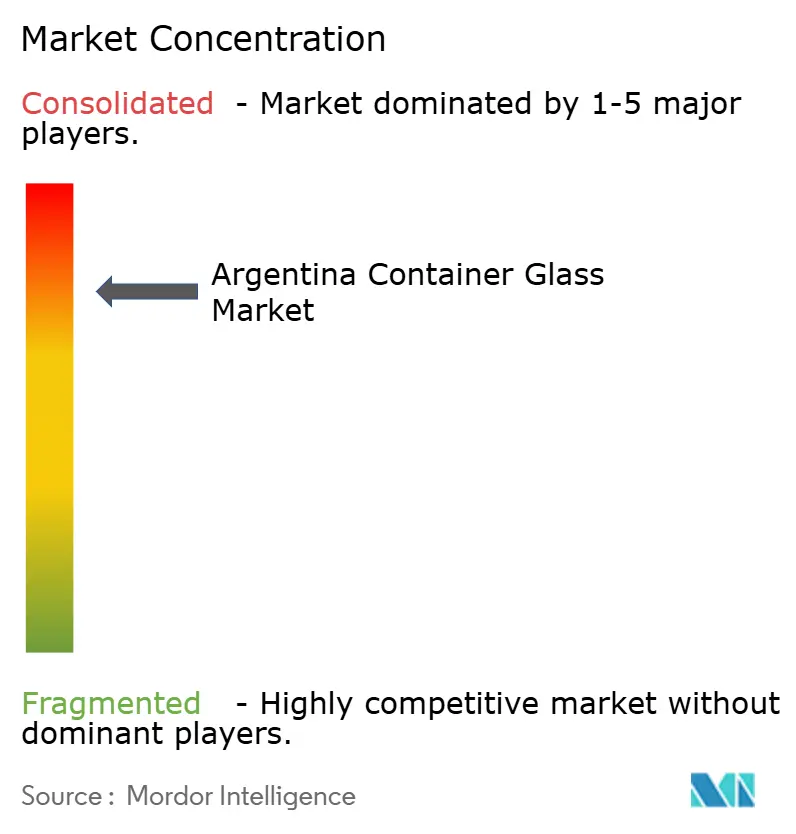

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Argentina Container Glass Market Analysis by Mordor Intelligence

Argentina container glass market size in 2026 is estimated at 577.15 kilotons, growing from 2025 value of 567 kilotons with 2031 projections showing 630.68 kilotons, growing at 1.79% CAGR over 2026-2031. Robust premium‐wine export momentum, widening returnable‐bottle systems, and gradual technology upgrades outweigh hyperinflation and fuel‐price volatility, giving the Argentina container glass market a measured but resilient growth runway. Premium beverage bottlers focus on high-clarity flint containers, prompting manufacturers to prioritize quality control, furnace uptime, and cullet availability. Energy‐saving oxy-fuel and hybrid melters, supported by targeted FDI incentives in Mendoza, are improving cost positions against imported bottles. However, the Argentina container glass market also faces structural headwinds: gas‐supply curtailments undermine furnace continuity, import licenses delay refractory parts, and lightweight PET and aluminum step up competition, especially in carbonated soft drinks. Larger producers utilize vertical integration and recycled-glass networks to defend their margins, while regional players target niche segments, such as craft spirits and cosmetics.

Key Report Takeaways

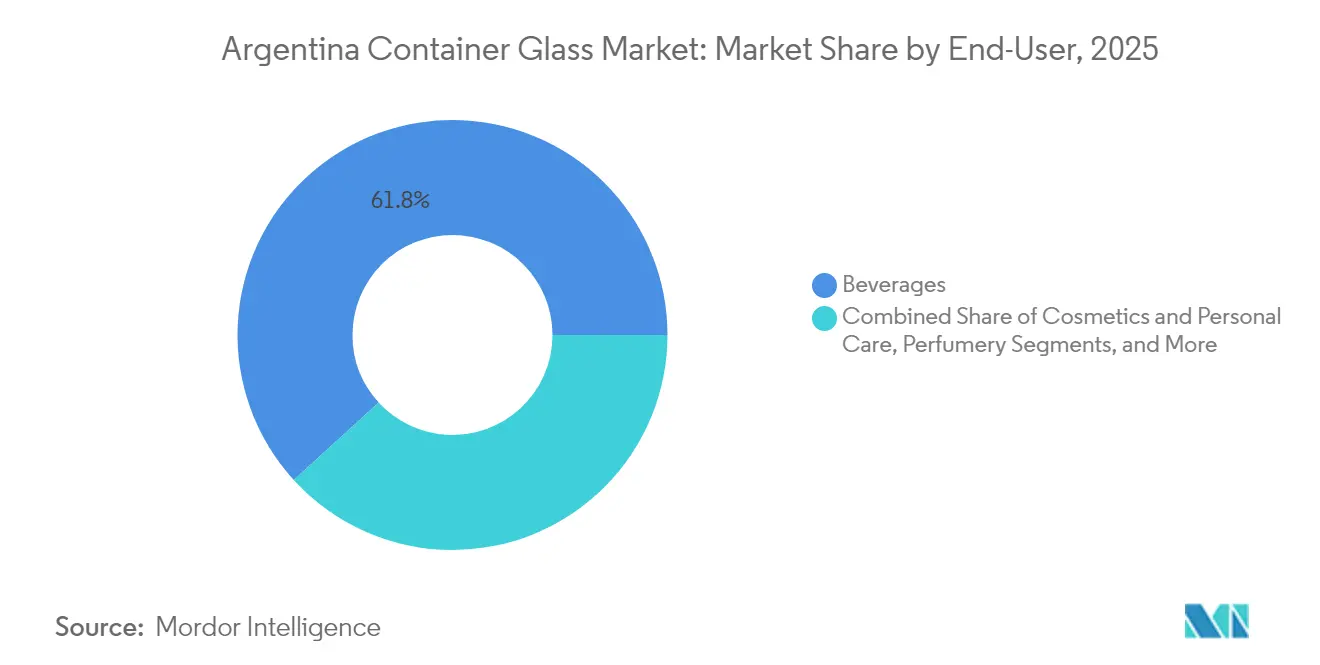

- By end-user, beverages captured 61.78 % of the Argentina container glass market share in 2025.

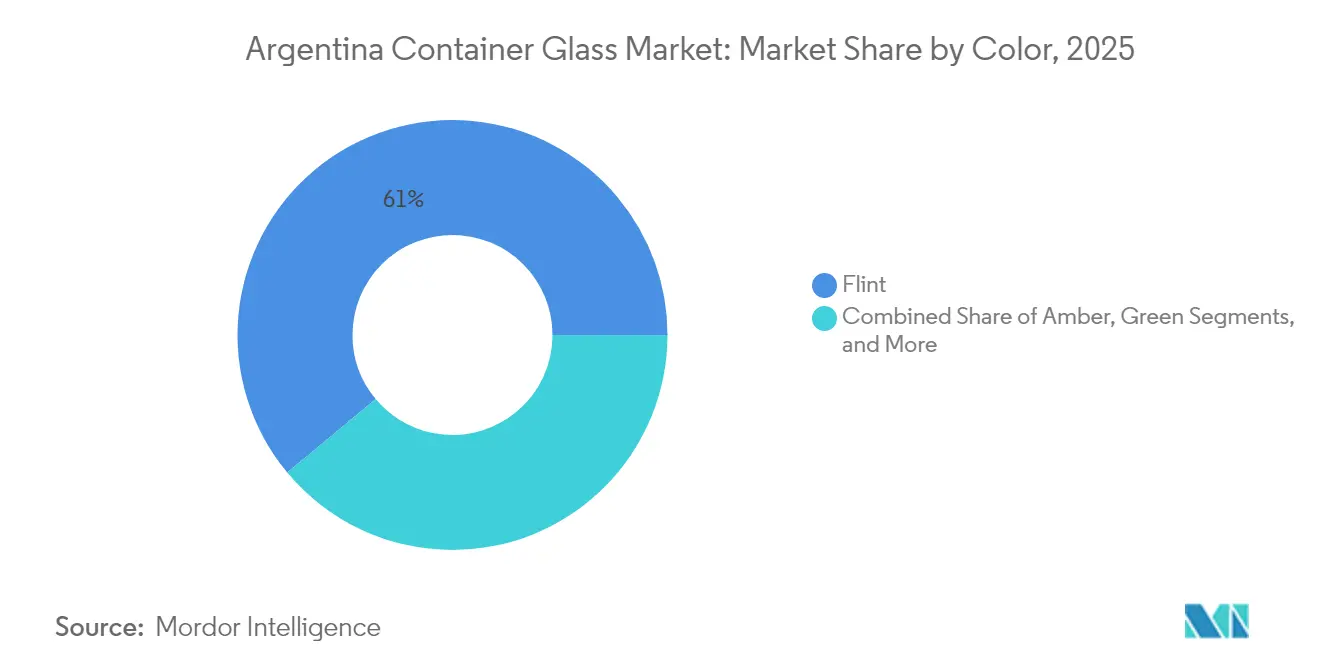

- By color, the Argentina container glass market for amber glass is projected to grow at a 3.05% CAGR between 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Argentina Container Glass Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising premium wine and spirits export bottling demand | +0.8% | National, concentrated in Mendoza wine cluster | Medium term (2-4 years) |

| Government-backed glass recycling mandates and cullet incentives | +0.3% | National, with provincial implementation variations | Long term (≥ 4 years) |

| Expansion of returnable bottle systems by beverage leaders | +0.4% | National, urban centers priority | Medium term (2-4 years) |

| Technological shift to oxy-fuel and hybrid furnaces lowering energy use | +0.2% | National, existing production sites | Short term (≤ 2 years) |

| FDI incentives for Mendoza wine-cluster glass capacity | +0.3% | Mendoza province, spillover to neighboring regions | Long term (≥ 4 years) |

| Near-shoring of specialty pharma glass due to traceability standards | +0.1% | Buenos Aires metropolitan area, key industrial zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Premium Wine and Spirits Export Bottling Demand

Wine exports rose to USD 933 million in 2024, a 15.3% increase that directly translates into additional flint-bottle volumes for the Argentina container glass market. Mendoza, which produces 70% of the country’s wine, underpins over 85% of bottled sales, ensuring a steady demand for high-clarity containers that showcase varietal color. Every USD 1 million in wine exports drives roughly 150-200 tons of glass, magnifying the sector’s importance to furnace utilization. Export orientation supports price premiums that offset inflationary pressure on domestic demand. Sustained growth hinges on favorable forex settings and stable export taxes, both of which influence winery investment in heavier, premium bottle formats. As a result, the Argentina container glass market benefits from a virtuous cycle of currency-aided competitiveness and brand-driven quality cues.

Government-Backed Glass Recycling Mandates and Cullet Incentives

Argentina’s circular-economy statutes empower provinces to mandate cullet content, enabling energy savings of approximately 2-3% for each incremental 10% increase in recycled content. Beverage majors support the push: Coca-Cola Latin America aims to achieve 40% refillable penetration by 2030, integrating standardized bottles that can be refilled and then recycled in domestic furnaces. Provinces such as Buenos Aires and Mendoza subsidize collection infrastructure, widening cullet supply and lowering net gas consumption at glass plants facing volatile winter tariffs. Producers with established reverse-logistics networks enjoy lower variable costs and stronger ESG credentials, positioning them ahead of peers in the Argentina container glass market. Yet, uneven infrastructure in smaller provinces slows national cullet penetration, leaving untapped energy-saving potential across the industry.

Expansion of Returnable Bottle Systems by Beverage Leaders

Coca-Cola FEMSA achieved a 24.1% refillable share in 2024, validating consumer acceptance of returnable containers. Glass units now carry QR-enabled GS1 identifiers, allowing for up to 25 refill cycles and shifting value capture from tonnage to durability.[1]GS1, “Coca-Cola’s Reusable, Refillable Bottles Benefit from Innovative QR Codes,” gs1.org Glass makers must deliver thicker walls and tighter dimensional tolerances, raising per-unit value even as aggregate volume growth levels off. Reverse-logistics hubs in Buenos Aires and Córdoba collect, inspect, and redistribute bottles, incentivizing retailers through deposit credits. Beverage companies report life-cycle cost cuts of 15-20%, encouraging broader adoption.

Technological Shift to Oxy-Fuel and Hybrid Furnaces

Industrial gas allocations declined 6.5% week-over-week in April 2022, following Argentina's increase in exports to Chile, underscoring the fragility of energy security. To hedge, Verallia and others are spending USD 5-10 million per line to retrofit oxy-fuel or hybrid melters, which trim energy use by 15-25% and curb carbon emissions. Paybacks compress to 3-4 years at today’s tariff levels, and the technology operates at lower oxygen-to-fuel ratios, enhancing furnace stability during gas curtailments. Smaller regional furnaces rely on grant financing or phased rebuilds but still target 5-10% efficiency gains through better heat-recovery systems. As energy accounts for up to 30% of production cost, technology adoption directly sustains price competitiveness in the Argentina container glass market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Hyperinflation-driven capital-expenditure delays | -0.5% | National, affecting all production sites | Short term (≤ 2 years) |

| Energy price volatility and gas-supply curtailments to glass plants | -0.4% | National, concentrated in industrial zones | Short term (≤ 2 years) |

| Import-licensing delays for refractory and spare parts | -0.2% | National, affecting maintenance schedules | Medium term (2-4 years) |

| Competition from lightweight PET and aluminum in CSDs | -0.3% | National, urban beverage markets priority | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Hyperinflation-Driven Capital-Expenditure Delays

With consumer inflation running above 100% during 2025, peso revenues lose purchasing power against USD-priced furnace parts, leading firms to shelve rebuilds beyond essential safety work. The BOPREAL bond window, launched in 2024, enables importers to settle debts but sells at 10-15% discounts, effectively raising component costs. Smaller furnaces stretch refractory campaigns, accepting higher risks of defects and an increased probability of emergency shutdowns. Hyperinflation also distorts payback modeling, discouraging energy-efficiency upgrades despite proven savings elsewhere. Consequently, capex lags demand, moderating overall output growth for the Argentina container glass market.

Energy-Price Volatility and Gas-Supply Curtailments

Industrial gas supply decreased to 32 MMm³/d in April 2022, down from 38 MMm³/d the previous year, as residential heating claims priority. Glass furnaces, which must operate continuously at near 1,500 °C, incur severe refractory damage from unplanned cooling. Government winter allocation rules allow 60-day industrial cuts without compensation, leaving manufacturers to import LPG at inflated spot prices or throttle their production. Energy accounts for roughly 28% of ex-works costs; thus, volatility directly erodes margins. Periodic curtailments also force contingency stock builds, extending working-capital cycles. These pressures temper capacity expansions, restraining the Argentina container glass market’s full growth potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User: Premium Beverages Sustain Volume and Value Growth

Beverages dominated the Argentina container glass market size, accounting for a 61.78% share in 2025, driven by the momentum of wine exports. The sub-segment benefits from Argentina’s fifth-place global wine ranking and the premiumization trend that elevates the average bottle weight and incorporates decorative elements. Distillers and craft brewers add incremental demand, while non-alcoholic soft drinks pivot cautiously due to the adoption of PET. The Argentina container glass market reports beverage anchoring furnace load factors, allowing producers to spread fixed costs and prioritize high-clarity flint production.

Cosmetics and personal care, which account for only 3.92% of 2025 tonnage, are projected to grow at a 3.02% CAGR through 2031, making them the fastest-growing volume among end-users. Rising middle-income purchasing power and on-shoring by global beauty houses shield volumes from currency swings. Local fillers demand thick-wall jars with complex embossing, pushing unit value higher and improving mix. Pharmaceuticals, supported by ANMAT guidelines that favor glass for certain suspensions, provide a stable base for demand. Food applications, jams, honey, and condiments post flat tonnage as lightweight PET gains share, yet artisanal brands still opt for glass to convey premium cues. Overall, diversified end-user needs help fortify the Argentina container glass market against material substitution risk.

By Color: Flint Dominance, Amber Acceleration

Flint led the 2025 color split with 61.05% of Argentina's container glass market share due to its importance in showcasing wine hue and clarity. Producers refine batch recipes to minimize iron impurities, achieving the high light transmission demanded by export wineries. Flint’s scale supports longer furnace campaigns and lower unit costs, reinforcing its leadership.

Amber is forecast to rise at a 3.05% CAGR to 2031 as pharmaceutical, nutraceutical, and craft-beer producers seek UV protection. Craft brewers are embracing amber for brand differentiation amid aluminum can shortages. Pharmaceutical fillers adhere to global pharmacopeia light-transmission norms, favoring amber vials for photolabile drugs. Green remains a niche for select wine brands and premium olive oil, while specialty hues such as cobalt blue attract spirits marketers willing to pay up to 40% more per unit. Color diversification lessens product-mix risk and broadens revenue streams within the Argentina container glass market.

Geography Analysis

The Buenos Aires metropolitan corridor hosts the largest furnace capacity, supplying mainstream beverage and food brands that cluster near the nation’s biggest consumption center. Buenos Aires plants utilize multimodal logistics links and proximity to port facilities for importing cullet and soda ash, thereby reducing inbound freight costs. Mendoza’s wine cluster accounts for roughly 70% of national wine output and 85% of bottled-wine shipment volumes, underpinning localized flint-bottle production lines that shorten turnaround and cut breakage rates.

Mendoza benefits from a more reliable gas supply due to regional pipeline prioritization; however, it still faces winter constraints. Provincial incentives such as a 3% gross-income tax rate encourage glass capex, though most projects remain brownfield furnace rebuilds rather than greenfield builds, aligning with the Argentina container glass market’s moderate growth trajectory. Corrientes and Santa Fe harbor smaller furnaces geared toward niche brands, supported by regional access to feedstock such as silica sands and soda ash from Alpat’s expanded capacity.

Logistics economics, with heavy, low-value-density containers, inherently limit import penetration, except for ultralight, premium cosmetics bottles sourced from Brazil or Chile. Consequently, Argentina container glass market participants retain pricing power within their geographic spheres but also share exposure to the same energy-infrastructure bottlenecks. Infrastructure investments under the RIGI framework could diversify capacity geographically; however, until sizable FDI flows materialize, concentration in Buenos Aires and Mendoza will persist.

Competitive Landscape

Verallia Packaging Argentina leads with three oxy-fuel lines and vertical integration, covering batch preparation to decoration, and supplies roughly one-third of the flint demand in the Argentina container glass market. Rigolleau leverages flexible furnaces and deep customer relationships, especially among regionally branded food jars. Nueva Cristalería Rosario, facing ownership succession after its founder’s death in January 2024, specializes in short-run specialty spirits flasks, offering embossed and colored variants at premium prices.

Strategy increasingly revolves around sustainability credentials: producers tout cullet ratios above 40%, carbon footprint disclosures, and participation in beverage take-back schemes. Technology adoption defines the competitive gap; Verallia’s hybrid furnaces cut specific energy to 3.5 GJ/ton, compared with 4.7 GJ/ton at legacy furnaces. Supply-chain shocks have heightened raw-material security. Alpat’s soda-ash expansion to 550 kilotons per year aims to minimize import dependency, benefiting all domestic furnaces.

Substitution pressure from PET and aluminum maintains pricing discipline. Argentina’s single aluminum-can mill struggled to meet carbonated-soft-drink peak demand in 2025, nudging brewers back into glass and buffering the Argentina container glass market against share loss. Export-oriented wineries continue to specify premium glass despite lightweight trials, reinforcing glass’s brand-equity advantage in the premium tier.

Argentina Container Glass Industry Leaders

Verallia Packaging Argentina S.A.

Domingo Mangone S.A.

Rigolleau S.A.

MOMA Food S.R.L.

Micro Envases S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Industrial production grew 9.26% y/y with capacity use at 58.8%, signaling rebound demand for the Argentina container glass market.

- May 2025: Craft‐beer per-capita consumption held steady at around 41 liters, while aluminum-can shortages steered brewers toward glass.

- April 2025: Arca Continental and Coca-Cola Mexico invested MXN 56.5 million (USD 3.3 million) to expand PET collection in San Luis Potosí, underscoring regional commitment to circular packaging.

- October 2024: O-I Glass announced a 7% global capacity reduction by mid-2025 under its “Fit to Win” program, which is expected to impact South American supply dynamics.

Argentina Container Glass Market Report Scope

Glass Containers refer to clean bottles and jars made from glass. The scope excludes windows and other non-container glass products. Container glass is used in the alcoholic and non-alcoholic beverage industries due to its ability to maintain chemical inertness, sterility, and non-permeability. Glass packaging is valued for its unique properties, including its transparency, inertness, and ability to preserve the quality and integrity of its contents.

Argentina container glass market is segmented by end-user vertical (beverages [alcoholic beverages (beer, wine, spirits, and other alcoholic beverages {cider and other fermented drinks}), non-alcoholic beverages (juices, carbonated drinks (CSDs), dairy product-based drinks, other non-alcoholic beverages)], food [jam, jelly, marmalades, honey, sausages and condiments, oil, pickles], cosmetics and personal care, pharmaceuticals (excluding vials and ampoules), and perfumery, by color (green, amber, flint and other colors). The report offers market forecasts and size in volume (kilotons) for all the above segments.

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals (excluding Vials and Ampoules) | ||

| Perfumery | ||

| Green |

| Amber |

| Flint |

| Other Colors |

| By End-user | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals (excluding Vials and Ampoules) | |||

| Perfumery | |||

| By Color | Green | ||

| Amber | |||

| Flint | |||

| Other Colors | |||

Key Questions Answered in the Report

How large is the Argentina container glass market in 2026?

The Argentina container glass market size reached 577.15 kilotons in 2026 and is on track for 630.68 kilotons by 2031.

What CAGR is forecast for container glass demand in Argentina?

Demand is projected to rise at a steady 1.79% CAGR through 2031.

Which end-user drives most glass consumption?

Beverages, led by premium wine exports, accounted for 61.78% of 2025 tonnage.

Which color segment is growing fastest?

Amber glass shows the quickest growth at a 3.05% CAGR due to pharmaceutical and craft-beverage demand.

How are energy-supply issues being addressed by glassmakers?

Producers are switching to oxy-fuel and hybrid furnaces that lower gas use 15-25% and provide resilience during curtailments.

What is the impact of returnable systems on glass demand?

Returnable bottles shift value to thicker, longer-life containers, reducing volume growth but lifting per-unit margins for suppliers.

Page last updated on: