Inhaled Nitric Oxide Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

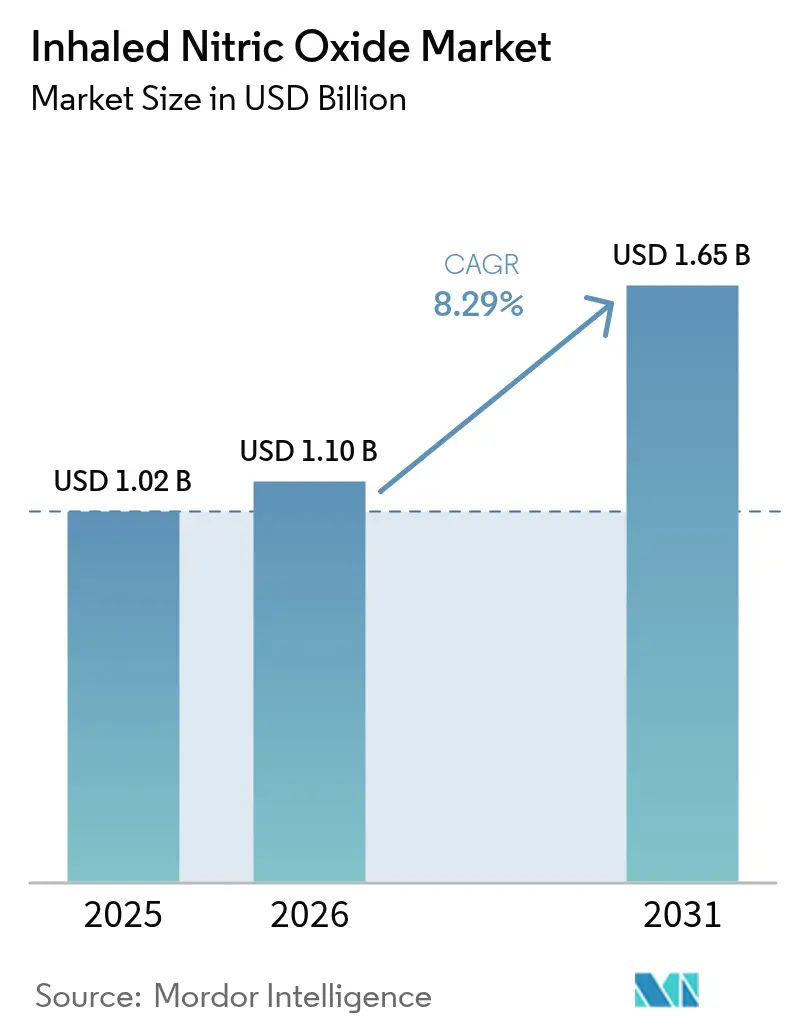

| Market Size (2026) | USD 1.1 Billion |

| Market Size (2031) | USD 1.65 Billion |

| Growth Rate (2026 - 2031) | 8.29% CAGR |

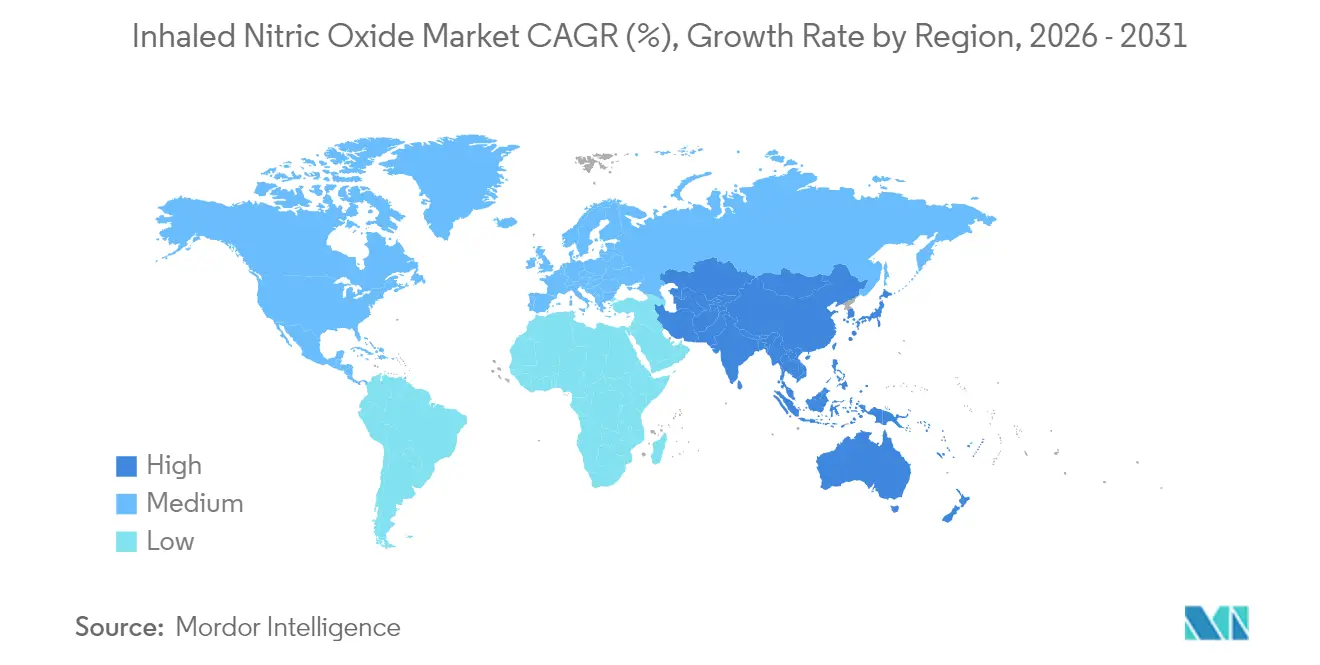

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Inhaled Nitric Oxide Market Analysis by Mordor Intelligence

The inhaled nitric oxide market size is expected to grow from USD 1.02 billion in 2025 to USD 1.10 billion in 2026 and is forecast to reach USD 1.65 billion by 2031 at 8.29% CAGR over 2026-2031. Robust demand for cylinder-free generators, expanding critical-care capacity across emerging economies, and sustained reimbursement for orphan drugs in high-income countries are reinforcing growth. Hospitals are pivoting toward generator-based solutions that reduce logistics costs, shrink carbon footprints, and allow bedside production of higher NO concentrations. These developments are widening access beyond tertiary centers and positioning the inhaled nitric oxide market as a core element of future respiratory care platforms. Competitive dynamics now revolve around intellectual-property-protected generation technologies, deep distribution alliances, and evidence generation for new indications.

Key Report Takeaways

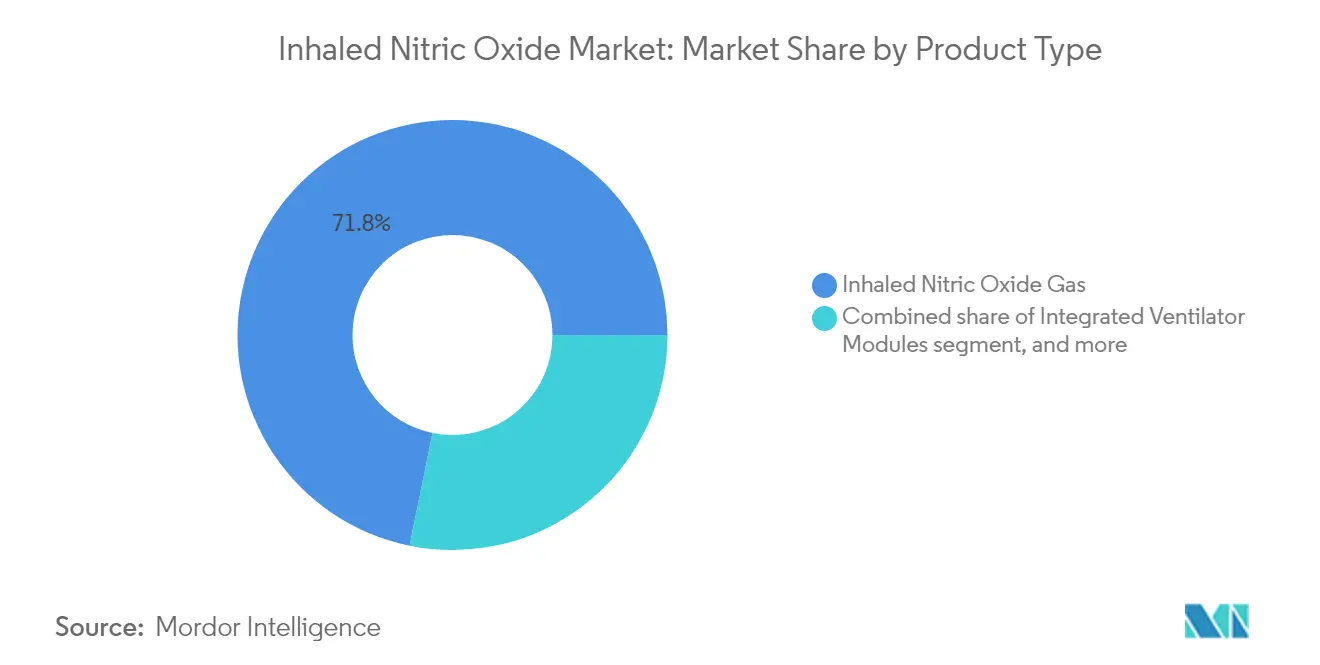

- By product type, inhaled nitric oxide gas held 71.80% of inhaled nitric oxide market share in 2025, while generators and delivery systems are forecast to expand at a 10.18% CAGR through 2031.

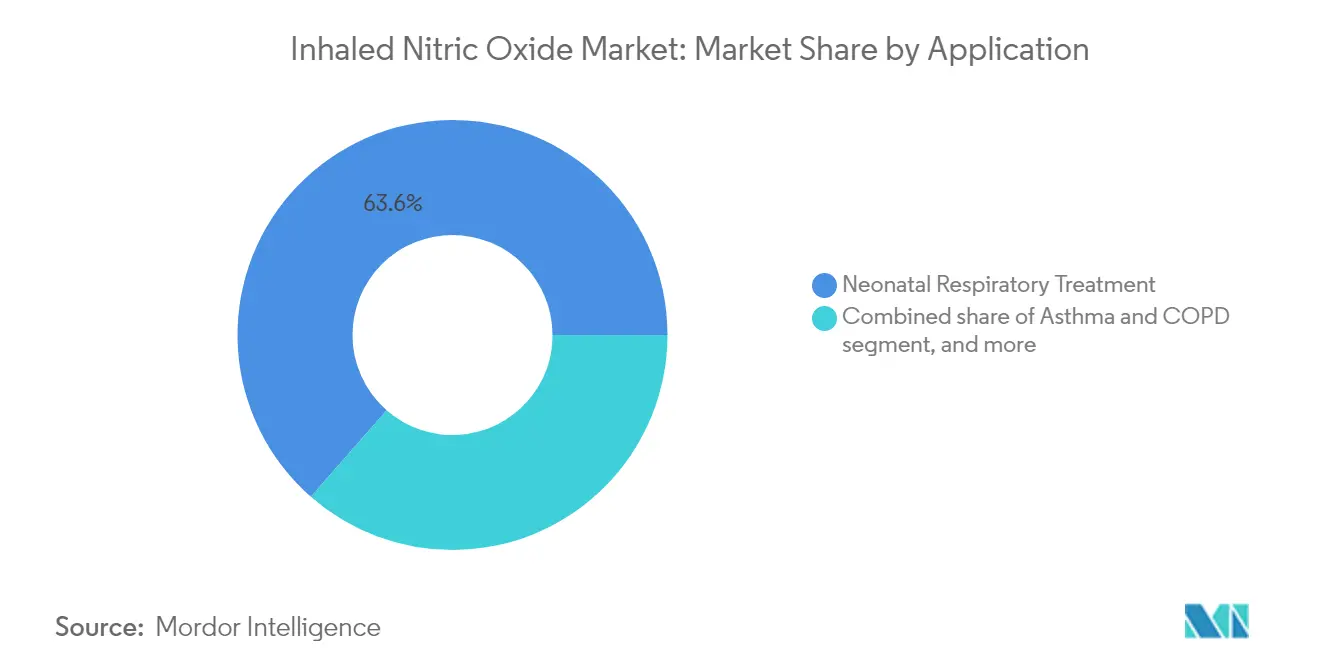

- By application, neonatal respiratory treatment captured 63.55% revenue share in 2025; acute respiratory distress syndrome applications are expected to advance at an 11.05% CAGR between 2026-2031.

- By end user, tertiary hospitals and NICUs accounted for 82.40% of 2025 revenue; home-care settings exhibit the fastest trajectory at an 11.32% CAGR for 2026-2031.

- By geography, North America led with 48.60% revenue share in 2025, whereas Asia Pacific is projected to register a 9.10% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Inhaled Nitric Oxide Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Escalating burden of neonatal and acute pulmonary disorders worldwide | +2.1% | Global; higher impact in Asia Pacific and Africa | Long term (≥ 4 years) |

| Technological advancements in cylinder-free NO generation and dosing equipment | +1.8% | North America and Europe; expanding to Asia Pacific | Medium term (2-4 years) |

| Favorable orphan-drug reimbursement policies in high-income markets | +1.2% | North America and Western Europe | Short term (≤ 2 years) |

| Expanding critical-care infrastructure across emerging economies | +1.5% | Asia Pacific, Middle East, Latin America | Medium term (2-4 years) |

| Growing clinical evidence supporting off-label uses in ARDS and COVID-19 | +0.9% | Global; initial impact in North America and Europe | Medium term (2-4 years) |

| Strategic collaborations between gas giants and device manufacturers | +0.7% | North America and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Escalating Burden of Neonatal and Acute Pulmonary Disorders Worldwide

Persistent pulmonary hypertension of the newborn affects 1.5-2 per 1,000 term and late-preterm births, underpinning steady NICU demand. Countries with high birth rates and improving intensive-care capacity, notably India and China, are scaling nitric-oxide protocols in neonatal guidelines. In parallel, ARDS now represents roughly 10% of ICU admissions worldwide, enlarging the adult addressable pool. During the COVID-19 surge, multi-center studies reported improvements in oxygenation metrics in up to 60% of severe cases when inhaled NO was added to ventilation strategies, cementing off-label traction that continues in 2025[1]PubMed, “Inhaled Nitric Oxide in Severe COVID-19 ARDS,” pubmed.ncbi.nlm.nih.gov.

Technological Advancements in Cylinder-Free NO Generation and Dosing Equipment

Generator-based systems eliminate high-pressure cylinders, slashing storage hazards and transport costs. Beyond Air’s FDA-cleared LungFit PH produces NO on demand from ambient air at bedside concentrations up to 400 ppm, far above the 80 ppm ceiling of legacy units, and integrates with ventilators through proprietary dosing software. Hospitals benefit from simplified logistics, reduced greenhouse-gas emissions linked to cylinder deliveries, and the ability to deploy therapy in operating rooms without respiratory-therapy set-up delays.

Favorable Orphan-Drug Reimbursement Policies in High-Income Markets

In the United States, therapy priced near USD 5,280 per day remains reimbursed under specific Current Procedural Terminology (CPT) and Diagnosis-Related Group (DRG) codes. CMS coverage offsets capital costs and supports routine use in 800+ NICUs. Western European payers similarly fund therapy through national health services when nitric oxide prevents costlier escalation to extracorporeal membrane oxygenation[2]CMS, “Clinical and Payment Policies for Inhaled Nitric Oxide,” cms.gov.

Expanding Critical-Care Infrastructure Across Emerging Economies

China added about 10,000 NICU beds between 2020-2024 while India accelerated tertiary-care investments, enabling broader adoption of cylinder-based and emerging generator modalities. Multinational hospital chains share clinical protocols across Asia Pacific, Latin America, and the Gulf, fostering standardized use of inhaled nitric oxide market therapies. Enhanced medical-gas supply chains lessen logistical bottlenecks, opening the inhaled nitric oxide market to community hospitals previously constrained by storage requirements.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operational costs of NO delivery systems | -1.3% | Global; greater impact in emerging markets | Medium term (2-4 years) |

| Stringent safety regulations for storage and transport of toxic gases | -0.8% | Europe and North America | Short term (≤ 2 years) |

| Availability of alternative pulmonary vasodilator therapies | -0.6% | North America and Europe | Medium term (2-4 years) |

| Patent expiries and pricing pressures reducing profit margins | -0.5% | Global; initial impact in North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Operational Costs of NO Delivery Systems

Legacy cylinder-based platforms require upfront outlays of USD 50,000-100,000 plus recurring consumable expenses near USD 3,000 per patient-day in the United States. Budget-constrained hospitals ration use to the most critical neonates and adults, limiting penetration across lower-tier centers. Even in developed markets, pharmacy committees enforce utilization protocols to curb spending, prompting interest in generator models that promise cost savings over device lifecycles.

Stringent Safety Regulations for Storage and Transport of Toxic Gases

OSHA classifies nitric oxide as a toxic gas, mandating dedicated ventilated storage rooms, continuous NO₂ monitors, and emergency response plans. Compliance workloads deter smaller facilities, especially in Europe where Seveso III directives impose additional reporting thresholds[3]EIGA, “Nitric Oxide Safety Guidelines,” eiga.eu. Generator technologies producing NO from air at point of care partially mitigate these hurdles yet still face validation testing and staff-training requirements.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Cylinder-Free Systems Disrupting Status Quo

The inhaled nitric oxide gas segment maintained a 71.80% revenue position in 2025. Familiarity, national formularies, and integrated cylinder supply chainshave entrenched the incumbent approach in NICUs and adult ICUs. Yet generator-based platforms are forecast to expand at 10.18% CAGR to 2031 as hospitals blend sustainability mandates with business-case savings. Cylinder-free units eliminate the need for costly bulk-gas contracts and lower carbon-emission footprints tied to transport. Device makers now bundle ventilator-compatible cartridges, software-driven dosing, and cloud diagnostics, reducing alarm fatigue and downtime. Integrated ventilator modules, deployed through partnerships between industrial-gas firms and ventilator manufacturers, streamline therapy initiation during intra-hospital transport. Accessories and consumables remain a predictable profit center, with filter and connector kits replaced on rigid preventive-maintenance cycles.

Competition now pivots on intellectual-property firewalls around plasma-ionization technology, smart-sensor feedback, and antimicrobial tubing. Market entrants tout higher maximum‐dose ceilings that allow experimental regimens in refractory hypoxemia and oncology. Generators capable of delivering 400-ppm doses at bedside encourage protocol expansion beyond conventional 80-ppm limits. These advances are reshaping procurement criteria, with purchasing teams ranking footprint, connectivity, and multiyear total-cost-of-ownership ahead of traditional per-hour pricing.

By Application: ARDS Expansion Beyond Traditional Neonatal Base

Neonatal respiratory therapy dominated 2025 revenue at 63.55% on the strength of FDA-approved use in persistent pulmonary hypertension of the newborn. High survival benefits and codified reimbursement codes lock in demand. Clinical focus, however, is swiftly widening to adult ARDS. The ARDS segment is projected to post an 11.05% CAGR to 2031, the highest among all applications. Large randomized trials during and after the COVID-19 crisis showed inhaled nitric oxide improving PaO₂/FiO₂ ratios and facilitating ventilator weaning in a subset of hypoxemic adults. Intensivists are now including nitric oxide in rescue-oxygenation algorithms for trauma-induced lung injury and extracorporeal-membrane support.

Investigators are also exploring nitric-oxide antimicrobial effects for drug-resistant pneumonia, tuberculosis, and malaria. Phase II protocols testing 160-ppm intermittent dosing regimes in infectious diseases may unlock entirely new patient cohorts. Cardiac-surgery teams employ short-term nitric oxide to mitigate right-heart failure during reperfusion, while lung-transplant units examine perioperative NO to improve graft function. These developments collectively enlarge the clinical canvas on which the inhaled nitric oxide market grows.

By End-User: Home Care Expansion Challenging Hospital Dominance

Tertiary hospitals and NICUs represented 82.40% of 2025 sales. High-acuity caseloads, round-the-clock respiratory-therapist staffing, and on-site biomedical departments justify investment in capital-intensive systems. Yet the fastest growth to 2031 lies in home care, tracking an 11.32% CAGR as portable generator devices win regulatory nods. Third Pole Therapeutics’ eNOfit portable cartridge exemplifies this movement by enabling chronic-disease patients to self-administer low-dose nitric oxide under telemonitoring. Specialty pulmonary clinics are adopting compact wheeled systems for outpatient infusions in interstitial-lung-disease–associated hypertension. Ambulatory-surgical centers use nitric oxide to stabilize high-risk pulmonary-hypertension cases during orthopedic or abdominal procedures.

Adoption outside hospital walls depends on battery runtime, Bluetooth-enabled dosage logs, and payer willingness to reimburse oxygenation endpoints tracked remotely. Device makers are bundling analytics dashboards that feed cloud registries, thus supporting value-based-care contracts. Successful transition to outpatient and home care will recast revenue recognition toward annuity-style disposable sales, diversifying earnings streams for manufacturers active in the inhaled nitric oxide market.

Geography Analysis

North America remained the epicenter of the inhaled nitric oxide market in 2025, generating 48.60% of global revenue. Roughly 25,000 U.S. neonates receive therapy each year across more than 800 NICUs. Medicare, Medicaid, and most private insurers reimburse USD 3,000-plus daily therapy costs, protecting provider margins. Canada shows rising adoption in provincial tertiary centers, while Mexico is incorporating nitric oxide into updated neonatal hypoxic-failure guidelines amid hospital-modernization funding. Regional growth is underpinned by early-stage home-therapy trials enrolling pulmonary-hypertension patients discharged with portable generators.

Asia Pacific is the fastest-growing territory, with inhaled nitric oxide market revenues primed for a 9.10% CAGR. China’s Healthy China 2030 blueprint prioritizes neonatal-mortality reduction, spurring procurement of advanced respiratory modalities in top-tier urban hospitals. The National Health Commission green-lighted reimbursements for persistent pulmonary-hypertension protocols that include nitric oxide, boosting penetration from 65 major facilities in 2023 to more than 140 in 2025. Japanese hospitals report the highest per capita utilization, reflecting universal coverage and mature NICU networks. India’s public–private NICU expansion and large annual birth cohort create long-term upside, although gaps in rural infrastructure constrain near-term uptake. Europe generated about 30.40% of 2025 revenue, led by Germany, France, and the United Kingdom. Reimbursement is contingent on cost-utility analysis, so hospitals evaluate total oxygenator days avoided and ECMO deferrals when justifying purchases of next-generation devices. Cylinder-free generators resonate with sustainability mandates embedded in European Green Deal agendas. Eastern-European adoption is accelerating through EU-funded hospital-upgrade programs. The Middle East counts fewer total treatments but high revenue per site as Gulf Cooperation Council hospitals procure premium generator-ventilator bundles for new-build NICUs. African uptake remains nascent except in South-Africa-based academic centers focused on neonatal-asphyxia reduction.

Regulatory Landscape

In the United States, inhaled nitric oxide (iNO) delivery and monitoring hardware sits within established FDA device pathways: nitric oxide administration apparatus, nitric oxide analyzers, and nitrogen dioxide analyzers are regulated as Class II devices with special controls under 21 CFR 868.2380, 868.2385, and 868.5165. In parallel, certain nitric oxide generator and delivery systems indicated for neonates are regulated as Class III (PMA) devices under product code QTB, which increases the evidence and quality-system burden for generator-led platforms as they expand beyond legacy cylinder-based setups.

In the European Union, medicinal product oversight for iNO is anchored by EMA marketing authorization for products such as INOMAX (authorized 01 August 2001; marketing authorization holder Linde Healthcare AB) for neonatal hypoxic respiratory failure with pulmonary hypertension in term and near-term neonates. Delivery and supply systems must also align with applicable safety and performance specifications, including CEN/TS 14507-1 and CEN/TS 14507-2, which emphasize continuity of supply, gas monitoring, and nitrogen dioxide risk controls. This dual-track model (drug authorization plus device compliance) shapes market entry requirements and favors suppliers that can operationalize pharmacovigilance, risk management, and device-service readiness at scale.

Competitive Landscape

The inhaled nitric oxide market features moderate concentration. Mallinckrodt, Linde, and Air Liquide controlled roughly 75% combined revenue in 2024. Mallinckrodt leverages its INOmax Total Care program that bundles delivery systems, disposables, on-site staff training, and 24/7 clinical hotlines, establishing sticky customer relationships. Linde and Air Liquide exploit vertically integrated gas supply chains to bundle cylinder deliveries with ventilator interfaces in one procurement contract.

Disruption is underway from generator specialists such as Beyond Air, VERO Biotech, and Third Pole Therapeutics. Beyond Air’s LungFit PH avoids high-pressure cylinders by creating nitric oxide from ambient air via plasma ionization. FDA clearance in 2022 set a precedent for tank-free models. VERO’s GENOSYL DS mini-cylinder delivery system uses on-cart cartridges that weigh under 9 kg, solving transport bottlenecks within large hospitals. Third Pole’s eNOfit aims to extend therapy to home settings.

Strategic collaborations define current competition. Linde partners with Hamilton Medical to develop ventilator-integrated dosing, while Air Liquide teams with Getinge on closed-loop feedback algorithms. Patent expirations on older cylinder-dosing technology intensify price competition but simultaneously propel generator uptake as hospitals weigh upgrade paths. Suppliers differentiate by embedding wireless telemetry, real-time NO₂ sensing, and cybersecurity layers that comply with FDA and EU medical-device regulations.

Inhaled Nitric Oxide Industry Leaders

Mallinckrodt Pharmaceuticals plc

Linde plc

Air Liquide Healthcare

VERO Biotech LLC

Beyond Air Inc.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A near-term whitespace centers on modernizing hospital-installed delivery fleets, with suppliers refreshing monitoring, automation, and transportability features through FDA 510(k) pathways. In May 2024, FDA clearances for Mallinckrodt Manufacturing, LLC's EVOLVE Nitric Oxide Delivery System (K240410) and Linde Gas & Equipment, Inc.'s NOxBOXi Nitric Oxide Delivery System (K233251) reinforced active replacement cycles within NICUs and adult ICUs. That creates headroom for bundled service models and multi-year consumables pull-through, particularly as tertiary hospitals and NICUs account for 82.40% of 2025 revenue and procurement teams increasingly weigh total cost of ownership, workflow integration (ventilator connectivity and alarms), and compliance overhead for toxic-gas handling, where generator-based alternatives reduce cylinder logistics.

Clinical and technology whitespace also extends to higher-dose and nontraditional use settings where evidence generation is advancing, rather than relying on commercial promotion alone. Peer-reviewed work has described intermittent high-dose regimens, including a Science Translational Medicine report on 300 ppm intermittent iNO for multidrug-resistant Pseudomonas pneumonia, and the PHiNO Study (Phase 2), which reported pulmonary vascular resistance reductions in acute severe right heart failure with INOflo. These research signals support opportunities for manufacturers and hospital networks to expand protocols and registries beyond the core neonatal indication, while aligning delivery-system design with tighter NO2 monitoring, dosing software, and transport-ready form factors that fit ICU and intra-hospital workflows.

Recent Industry Developments

- February 2026: Hong Kong Exchanges and Clearing Limited (HKEX) published a prospectus-level industry overview referencing competitive activity around inhaled nitric oxide delivery systems, including instant-generation and cartridge-based approaches. The disclosure highlights how device form factor, monitoring integration, and regulatory pathways are central to differentiation as hospitals compare cylinder-based franchises with generator-led platforms.

- June 2025: Beyond Air submitted a PMA supplement to the US FDA for LungFit PH II, positioning a smaller, lighter, transport-ready nitric oxide generator for treating persistent pulmonary hypertension of the newborn. The filing signals continued iteration toward bedside generation systems that address ICU transport and footprint constraints while staying within stringent neonatal-use regulatory requirements.

- October 2024: Mallinckrodt began a broader US rollout of the INOmax EVOLVE DS delivery system after completing a pilot program. Expanding deployment of an FDA-cleared platform strengthens Mallinckrodts installed base and reinforces bundled service and disposable utilization models in hospital settings.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the inhaled nitric oxide market is defined as revenue generated from inhaled nitric oxide therapy used in clinical care, including the nitric oxide gas supply and the related generator and delivery equipment used to administer it.

Scope exclusions: This sizing does not count general respiratory drugs that are not nitric oxide, general oxygen therapy equipment, or ventilators unless they are part of nitric oxide specific delivery setups.

Segmentation Overview

- By Product Type

- Inhaled Nitric Oxide Gas

- Nitric Oxide Generators & Delivery Systems

- Integrated Ventilator Modules

- Accessories & Consumables

- By Application

- Neonatal Respiratory Treatment

- Asthma and COPD

- Acute Respiratory Distress Syndrome

- Malaria Treatment

- Tuberculosis Treatment

- Other Applications

- By End-User

- Tertiary Hospitals & NICUs

- Specialty Pulmonary Clinics

- Ambulatory Surgical Centres

- Home-Care Settings

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started with mapping where inhaled nitric oxide is actually used, and what drives demand in hospitals and neonatal units. Public sources were used to anchor disease and procedure related demand signals, such as CDC and NIH pages, WHO health statistics, and clinical guidance from FDA postings and National Library of Medicine articles.

We also reviewed sources that help explain the equipment side and supply chain realities, such as USITC trade statistics for medical gas and device categories, customs and shipment summaries where available, and hospital association publications that discuss critical care capacity. Company annual reports, investor presentations, press releases, and reputable press were used for product timing and geographic exposure. A paid subscription for company financials and patent databases supported cross-checks on revenue direction and innovation activity. The sources listed here are illustrative, and many other public references were also checked to collect data, validate assumptions, and clarify unclear points.

Primary Interviews and Surveys

Primary work focused on clinical and commercial reality checks, since published utilization rates and pricing can differ by care setting. We spoke with hospital respiratory therapy stakeholders, neonatal care specialists, procurement teams, and product and distribution side experts across APAC, EMEA, and the Americas to confirm use patterns, typical duration of therapy, and how generator adoption is changing ordering behavior.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 17% | APAC: 52% |

| Mid tier: 54% | Functional/Unit leaders: 35% | EMEA: 29% |

| Smaller Players: 20% | Managers: 48% | Americas: 19% |

Market-Sizing & Forecasting

Sizing was built using a top-down demand pool approach where treated patient volumes and care setting activity are reconstructed by region, and then translated into therapy value through typical dosing duration and price points. To keep the numbers grounded in market reality, we corroborated totals with selective bottom-up approximations, including sampled hospital channel checks and a limited roll-up of supplier revenue direction for gas and delivery equipment.

Key inputs used in the model include neonatal and pediatric respiratory case volumes linked to pulmonary hypertension care, ICU and NICU bed capacity trends, average treatment duration per episode, adoption levels of cylinder-free generators versus cylinder supply, and regional reimbursement and guideline alignment that influences prescribing. Since not all countries report the same clinical usage indicators, gaps were handled by using proxy indicators (for example, births and critical care capacity) and then narrowing the ranges using interviewees' descriptions of typical penetration rates.

For forecasting, scenario analysis was used with a central case shaped by expert consensus on generator adoption pace, hospital procurement cycles, and the expected stability of therapy pricing in mature markets. Growth and mix shifts were then applied by region to reflect where critical care expansion and regulatory clarity are moving faster.

Data Validation & Update Cycle

Outputs were checked through multiple rounds so that the final totals align with more than one independent signal. We tested for year-over-year jumps that do not match changes in treated volumes, pricing behavior, or equipment installation trends, and any large variances triggered a re-check of assumptions and follow-up calls.

Before sign-off, another analyst reviews the model logic, inputs, and currency conversions, and then the final tables are reconciled back to the defined scope. The report is refreshed annually, and interim updates are made when there are material events, including major approvals, supply disruptions, or meaningful shifts in hospital purchasing behavior. Before delivery, a final review pass is completed so clients receive an up-to-date view.

Mordor Intelligence's Inhaled Nitric Oxide Market Size Measured Against Other Published Estimates

Published market values for inhaled nitric oxide often do not match because each publisher draws the boundary of what counts as the market in its own way. Differences usually come from what is included with therapy revenue, the years used as the starting point, and how demand is validated when public utilization data is limited.

Clinical use signals like neonatal respiratory treatment volumes, ICU and NICU capacity direction, and the observed shift toward generator based delivery are the checks that keep Mordor Intelligence's estimate tied to a defined demand pool rather than a broad respiratory care spend bucket. Some estimates expand scope by bundling adjacent respiratory equipment or by applying uniform penetration assumptions across regions, and that can move the total up or down even when the same therapy is being discussed.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.10 B (2026) | |

| Industry Publisher A | USD 1.06 B (2025) | Uses a different base year and a longer forecast window, and the market definition is presented mainly by application without clearly separating gas revenue from delivery equipment value, which can change the counted spend in early years. |

| Global Publisher B | USD 1.20 B (2025) | Reports a higher starting value that may reflect broader inclusion of delivery systems and additional use cases, and it may rely more on generalized regional growth assumptions rather than care setting level utilization and duration checks. |

Across the three figures, the spread is explained more by scope and starting year choices than by disagreements on the overall clinical relevance of inhaled nitric oxide. By keeping the model anchored to treated volumes, therapy duration, and realistic pricing and adoption patterns, we are able to provide a number that can be traced back to clear drivers and rechecked when inputs change.

Key Questions Answered in the Report

What is the current value of the inhaled nitric oxide market?

The inhaled nitric oxide market size is USD 1.10 billion in 2026 and is projected to reach USD 1.65 billion by 2031 at an 8.29% CAGR.

Which application segment is growing the fastest?

Acute respiratory distress syndrome treatments show the highest growth, expanding at an 11.05% CAGR as evidence for adult use strengthens.

How are generator-based systems changing hospital economics?

Cylinder-free generators cut storage hazards, reduce transport emissions, and lower long-term operating costs, making nitric oxide therapy practical for more care settings.

Which region offers the most attractive growth prospects?

Asia Pacific leads global momentum with a projected 9.10% CAGR to 2031, supported by NICU expansion in China and India and rising reimbursement access.

Who are the leading companies in the inhaled nitric oxide market?

Mallinckrodt, Linde, and Air Liquide dominate with about 75% combined share, while innovators like Beyond Air and VERO Biotech are rapidly gaining traction.

Page last updated on: