Cough Syrup Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 4.72 Billion |

| Market Size (2031) | USD 6.27 Billion |

| Growth Rate (2026 - 2031) | 5.85% CAGR |

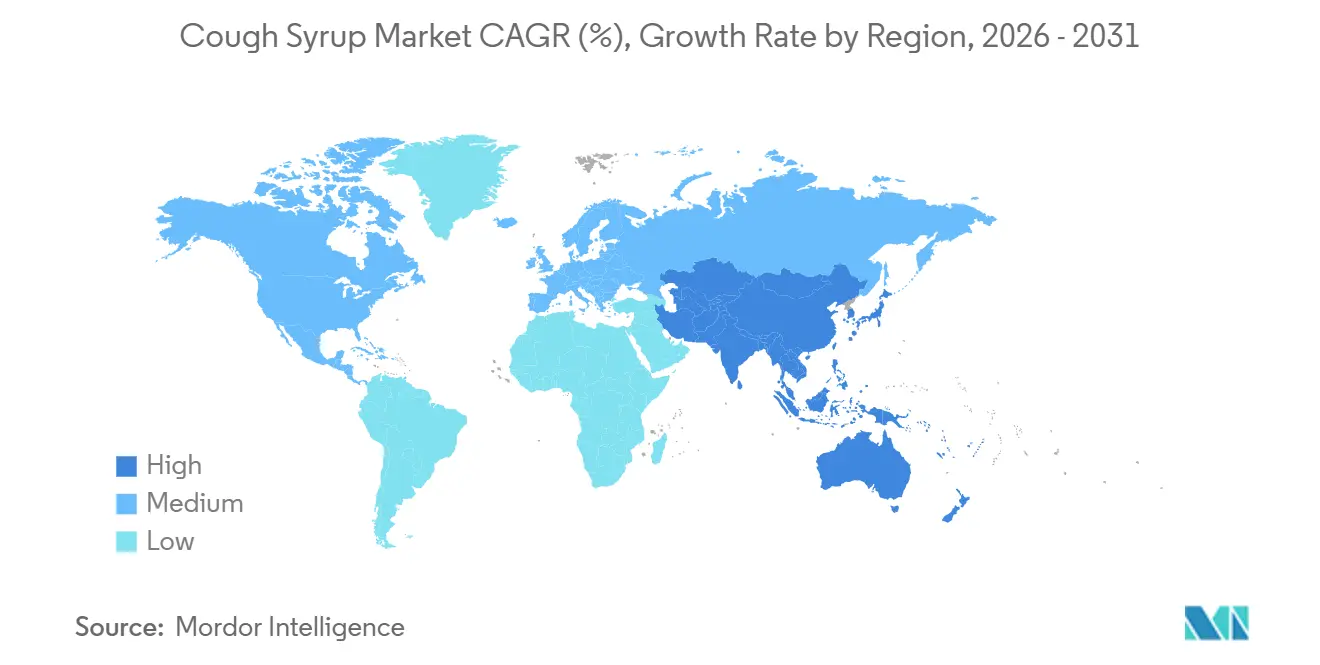

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cough Syrup Market Analysis by Mordor Intelligence

The Cough Syrup Market size was valued at USD 4.46 billion in 2025 and is estimated to grow from USD 4.72 billion in 2026 to reach USD 6.27 billion by 2031, at a CAGR of 5.85% during the forecast period (2026-2031).

The market is being supported by the very high and recurring burden of upper respiratory tract infections, which remain one of the most common infectious conditions worldwide and continue to generate steady treatment demand across both developed and emerging healthcare systems. North America held the largest regional position in 2025 because OTC usage is deeply established, retail pharmacy access is extensive, and major brands retain strong consumer loyalty, while Asia-Pacific is set to grow the fastest as urbanization, pharmacy expansion, and branded medicine adoption continue to improve. The cough syrup market is also shifting toward multi-symptom products, faster digital purchasing, and more targeted differentiation around non-drowsy, sugar-free, alcohol-free, and herbal formulations, which is changing both pricing and assortment strategies across large brands and local players. Competition remains balanced between global consumer health companies with strong brand equity and domestic manufacturers that compete on price, especially in generic and private-label tiers, which keeps the cough syrup market commercially active but not fully consolidated. Regulatory pressure around active ingredients and syrup quality is now becoming a more important variable, and this is raising reformulation costs, tightening compliance expectations, and increasing execution risk for smaller manufacturers in the near term.

Key Report Takeaways

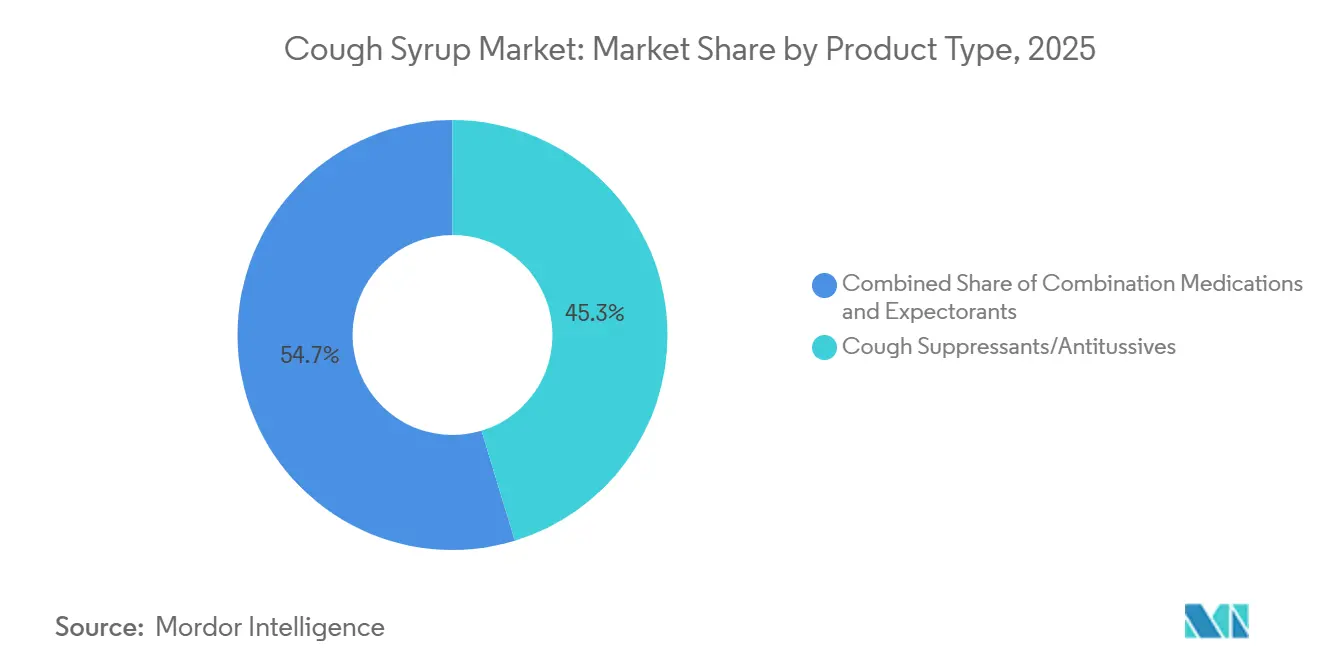

- By product type, cough suppressants or antitussives held 45.31% share in 2025, while combination medications are forecast to expand at a 7.38% CAGR through 2031.

- By age group, adults accounted for 48.24% share in 2025, while pediatrics is projected to record the highest CAGR at 6.52% through 2031.

- By prescription type, OTC formulations represented 60.52% share in 2025 and are expected to project a CAGR at 6.25% through 2031.

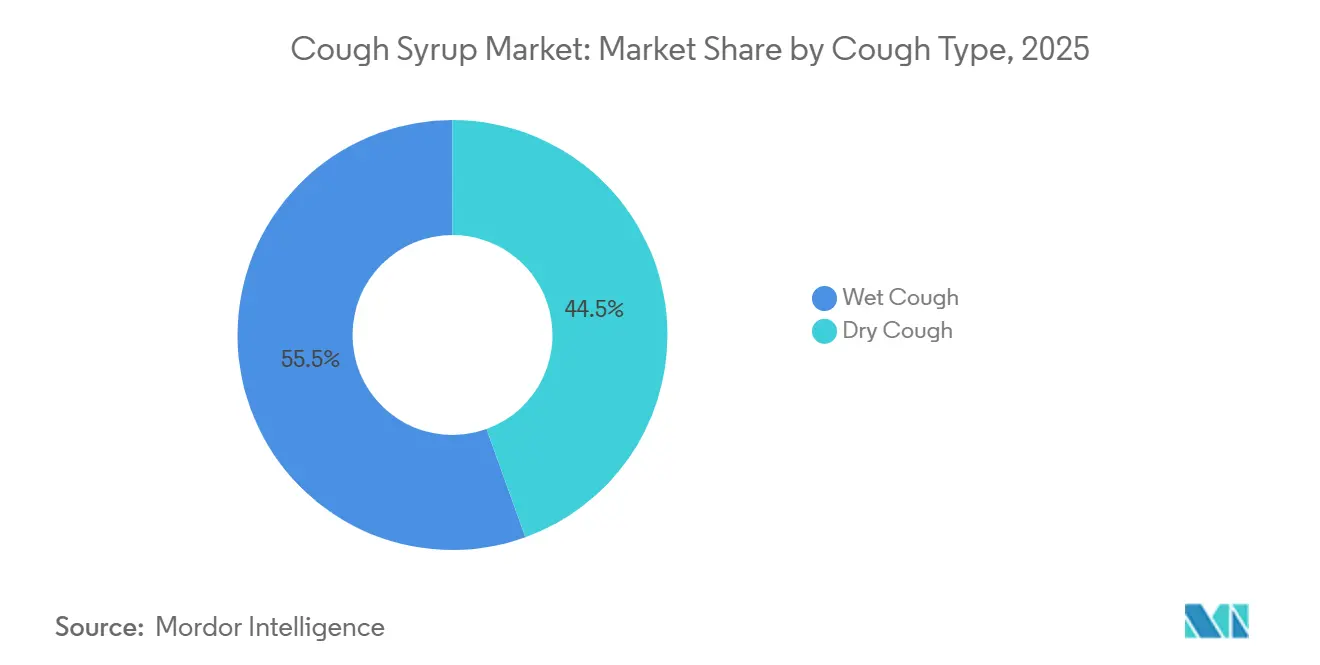

- By cough type, wet cough syrup captured 55.52% share in 2025, while dry cough syrup is expected to grow faster at a 6.55% CAGR through 2031.

- By distribution channel, retail pharmacy held 58.22% share in 2025, while online pharmacy is forecast to advance at an 8.65% CAGR through 2031.

- By geography, North America held 36.52% share in 2025, while Asia-Pacific is projected to expand at a 7.45% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Cough Syrup Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing Prevalence of Upper Respiratory Tract Infections | +1.4% | Global | Short term (≤ 2 years) |

| Growing Preference for Over-the-Counter Cough Remedies | +1.1% | North America & EU | Short term (≤ 2 years) |

| Rising Popularity of Natural and Herbal Ingredients | +0.7% | Europe & APAC core, spill-over to MEA | Medium term (2-4 years) |

| Expansion of E-Commerce and Online Pharmacy Access | +0.8% | APAC core, North America, spill-over to MEA | Medium term (2-4 years) |

| Pediatric-First Formulation Innovation and Palatability Engineering | +0.5% | North America & EU | Long term (≥ 4 years) |

| Non-Drowsy, Sugar-Free, and Alcohol-Free Product Differentiation | +0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Increasing Prevalence of Upper Respiratory Tract Infections

Upper respiratory tract infections remain one of the broadest demand anchors for the cough syrup market because they create a recurring need for short-cycle symptom relief across many age groups and income levels. Long-run age-standardized rates may have eased in some settings, but the absolute number of episodes has continued to rise with population growth, which keeps total treatment volumes elevated across the cough syrup market. The 2025 to 2026 flu season in the United States had already produced at least 47 million illnesses and 610,000 hospitalizations through April 2026, and that scale of seasonal illness continued to support high sell-through for cough and cold remedies[1]U.S. Centers for Disease Control and Prevention, “2025–2026 Flu Season FAQ,” U.S. Centers for Disease Control and Prevention, cdc.gov. This pattern matters because the cough syrup market does not rely only on premiumization or channel gains, it also rests on a large and repeating disease burden that is difficult to displace. A further shift is that viral seasonality is becoming less predictable in some places, which may smooth annual demand but can also complicate inventory timing, promotions, and media spending for manufacturers. That makes the cough syrup market more dependent on supply responsiveness and retail execution rather than only on broad annual category growth.

Growing Preference for Over-the-Counter Cough Remedies

The cough syrup market continues to benefit from a clear consumer preference for self-managed care, especially for minor respiratory conditions that do not always require a physician visit. OTC products already held 60.52% share in 2025 and also carried the fastest forecast growth within prescription type, which shows that this part of the cough syrup market is expanding on both a scale and momentum basis. This shift reflects more than convenience because it also points to a practical move toward accessible, fast, and familiar symptom relief that fits how consumers now respond to everyday illness. In emerging markets, the same pattern is even more visible because pharmacy access often serves as the first point of care, which gives OTC cough syrups a frontline role in treatment behavior. In mature markets, the preference supports higher product variety, wider shelf depth, and faster repeat purchases, but it also gives private labels more room to grow if branded products do not maintain clear differentiation. The result is that the cough syrup market is seeing stronger volume support from consumer behavior itself, not only from new product launches or short-term cold and flu spikes.

Rising Popularity of Natural and Herbal Ingredients

The cough syrup market is seeing steady movement toward natural and herbal formulations, and this is coming through reformulation as much as through entirely new product development. Reckitt stated that ivy leaf extract carries the strongest clinical evidence within the EU-approved herbal cough category, and the company has used that base in its Strepsils Cough Dual Action range, which has been rolling out more broadly after its Poland launch. This matters because herbal options are now being positioned across both dry cough syrup and wet cough syrup uses, which widens their commercial relevance inside the cough syrup market rather than limiting them to a niche wellness segment. Europe has become the most active region for this shift because herbal monographs make approvals more straightforward for certain plant-based actives than some synthetic alternatives. Consumer expectations are also changing because buyers increasingly want products that feel safer without giving up efficacy, which is pushing companies to support botanical ingredients with stronger evidence and clearer claims. That means the cough syrup market is rewarding brands that can combine regulatory acceptance, clinical credibility, and consumer-friendly positioning in the same portfolio.

Expansion of E-Commerce and Online Pharmacy Access

The cough syrup market is being reshaped by online pharmacy expansion, especially in urban and mobile-first populations where convenience now influences even urgent symptom-relief purchases. Online pharmacy is forecast to grow at 8.65% through 2031, which is well above the overall growth pace of the cough syrup market and marks it as the strongest channel growth engine in the report. This rise is tied to home delivery, easier repeat ordering, digital payment habits, and broader use of symptom-led search and recommendation tools on health platforms. In China, India, and Southeast Asia, these platforms are becoming important demand aggregators during seasonal spikes, which can shift volumes quickly and with far more visibility than traditional retail channels. The channel also gives brands more direct access to browsing, conversion, and repeat-purchase data, which improves assortment planning and promotional timing across the cough syrup market. As regulation around digital pharmacy licensing tightens unevenly by country, early channel access and compliance readiness can create a meaningful advantage for brands that move before the field becomes more crowded.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Safety and Labeling Compliance for Active Ingredients | -0.4% | North America & EU | Short term (≤ 2 years) |

| Misuse and Overuse Concerns, Especially in Pediatric Use | -0.5% | APAC, MEA, North America | Short term (≤ 2 years) |

| Price Pressure From Generic and Private-Label Competition | -0.6% | North America & EU | Short term (≤ 2 years) |

| API and Packaging Supply Volatility in Oral Liquid Formulations | -0.4% | Global, especially APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Stringent Safety and Labeling Compliance for Active Ingredients

The cough syrup market is facing a tighter compliance environment because active ingredient scrutiny is now taking place across several large markets at the same time. The FDA proposed removing oral phenylephrine as a recognized nasal decongestant under OTC Monograph M012 in November 2024, and this pushed manufacturers to reassess relevant cold and cough combinations before the following season. The same FDA forecast also signaled continued review of pediatric cough and cold dosing, which raised the likelihood of further labeling and risk management requirements in products for younger children[2]Consumer Healthcare Products Association, “FDA Annual Forecast,” Consumer Healthcare Products Association, chpa.org. In Australia, the Therapeutic Goods Administration reviewed dextromethorphan scheduling in 2024 and kept it pharmacy-only while still highlighting misuse concerns, which shows that regulatory caution is not limited to one region. These actions raise costs because reformulation, revalidation, relabeling, and relaunch work must often happen on existing products that were already commercially established. The effect is especially meaningful in the cough syrup market because smaller manufacturers may not have the technical and financial capacity to absorb repeated compliance cycles as easily as large branded players.

Misuse and Overuse Concerns, Especially in Pediatric Use

Misuse and overuse concerns remain a clear restraint for the cough syrup market, and the pressure is strongest where dextromethorphan-based products are widely used or where pediatric safety has come under closer review. The U.S. Drug Enforcement Administration documented misuse of DXM at doses ranging from 250 mg to 1,500 mg in a single dosage, with adolescents identified as a key concern group. China tightened control by moving DXM into its Category II Psychotropic Drugs framework effective July 1, 2024, which restricted sale to prescription-only and banned supply to minors. In October 2025, contamination-linked pediatric deaths tied to cough syrups produced by Indian manufacturers triggered coordinated action from the FDA, the WHO, and India’s CDSCO, which intensified quality oversight and raised wider safety concerns around oral liquid products. The FDA also continues to advise against use of OTC cough and cold medicines in children younger than 2 years, which keeps parental caution elevated even where products remain legally available. This creates a difficult setting for the cough syrup market because demand still exists in pediatrics, but future growth is likely to favor products with safer actives, clearer dosing, and stronger quality assurance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Combination Formats Redefine Cough Syrup Value Proposition

Cough suppressants or antitussives held 45.31% of revenue in 2025, giving them the largest product type position in the cough syrup market. Their lead rested on long-standing consumer familiarity with suppressant-led relief, especially where dextromethorphan-based products had built strong recognition over many years. That familiarity still matters at shelf level because buyers in the cough syrup market often make fast decisions based on known actives and familiar labels rather than extended comparison. Expectorants also retained an important place because guaifenesin continues to hold strong clinical and consumer recognition in wet cough treatment. This balance shows that the product structure of the cough syrup market is still anchored in established symptom categories even as newer formats expand around them.

Combination medications are projected to grow at 7.38% CAGR through 2031, which makes them the strongest advancing product group in the cough syrup market. Their rise reflects a clear move toward one product covering several symptoms, which reduces shelf complexity for retailers and simplifies choice for consumers. That shift is important because it turns dry cough syrup and wet cough syrup needs into a broader multi-symptom purchase occasion, which expands the practical role of combination products inside the cough syrup market. At the same time, regulatory reviews of certain actives are pushing manufacturers to use combination lines as reformulation vehicles, so these products increasingly serve both commercial and compliance goals. In the cough syrup industry, this gives combination formats a stronger strategic position because they can carry premium claims, support broader distribution, and respond more flexibly when single-ingredient products face pressure.

By Age Group: Adult Leadership Continues While Pediatrics Stays Strategically Important

Adults accounted for 48.24% share in 2025, which made them the largest age cohort in the cough syrup market. This position was supported by high self-medication rates, frequent workplace-driven convenience purchases, and strong brand recall among working-age consumers. Adult buyers also form the core audience for premium non-drowsy, sugar-free, and alcohol-free products, which means the cough syrup market draws a significant share of its value from feature-led purchases in this group. That matters because adult demand is not only broad, it is also commercially attractive due to higher repeat purchases and willingness to pay for convenience-oriented benefits. The geriatric segment remains smaller, but it is gaining relevance as aging populations in Europe and Japan increase demand for respiratory symptom management that is more guided, repeatable, and brand loyal.

Pediatrics is forecast to expand at 6.52% CAGR through 2031, which places it as the fastest-growing age group in the cough syrup market despite the stricter risk environment. Growth is being supported by long-term investment in palatability, clearer dosing formats, and reduced reliance on higher-risk active ingredient profiles. That creates an uneven but important opening because the cough syrup market can still grow in children when products meet tighter expectations around safety, usability, and taste. This is why child-focused innovation is becoming more format-specific and compliance-led rather than simply extending adult syrups into smaller doses. In the cough syrup industry, companies that stay invested in pediatric formulations with stronger safety positioning are more likely to keep access as regulatory scrutiny continues to rise.

By Prescription Type: OTC Leadership Is Structural and Still Expanding

OTC formulations accounted for 60.52% of the cough syrup market share in 2025, making them the clear leader within prescription type. OTC products also posted the highest projected CAGR at 6.25% through 2031, which means the leading segment is still widening its role inside the cough syrup market. This combination of current scale and forward momentum usually points to a structural demand shift rather than a short-term channel gain. In this case, the shift comes from consumer familiarity, fast access, broad retail reach, and the steady normalization of self-care for common respiratory symptoms. The cough syrup market therefore relies heavily on the OTC aisle as both the main revenue base and the most active area of future expansion.

Prescription formulations still matter in severe, chronic, post-surgical, and immunocompromised use cases, but their role is becoming narrower in the cough syrup market. Products that remain prescription-led need clearer clinical differentiation if they are to avoid share pressure from improving OTC alternatives. That pressure rises when active ingredients once associated with physician use become more accepted in non-prescription formats or face closer scrutiny in regulated prescription channels. The result is that prescription-only ranges are becoming more specialized and less central to volume growth in the cough syrup market. For manufacturers that remain heavily exposed to Rx products, portfolio adjustment toward more differentiated respiratory therapeutics may become more important over the forecast period.

By Cough Type: Wet Cough Syrup Holds the Lead While Dry Cough Syrup Gains Pace

Wet cough syrup held 55.52% share in 2025, giving it the larger position within cough type segmentation in the cough syrup market. This lead reflects the frequency of productive cough associated with upper and lower respiratory tract infections, where expectorant-based therapy remains a common treatment approach. The wet cough format also benefits from strong pharmacist and physician familiarity with guaifenesin, which helps maintain steady recommendation and purchase behavior. Another support factor is the expansion of combination products, because many multi-symptom formulations include an expectorant and therefore broaden the commercial reach of wet cough syrup beyond single-ingredient use. For the cough syrup market, that means the largest cough type benefits from both established need and adjacent product innovation.

Dry cough syrup is forecast to grow at 6.55% CAGR through 2031, making it the faster-growing cough type in the cough syrup market. Growth is linked to rising attention on post-viral, allergy-related, and other non-productive cough conditions that require suppression rather than mucus clearance. The dry cough segment is also where botanical actives and lifestyle-compatible claims such as sugar-free and non-drowsy are gaining stronger traction, especially in Europe where evidence-backed herbal options have expanded[3]Reckitt Benckiser Group plc, “How Unique Science and Consumer Obsession Are Expanding Strepsils’ Reach,” Reckitt, reckitt.com. This makes dry cough syrup an important innovation arena because repeat buyers in persistent cough situations often compare formulation features more carefully. As a result, the cough syrup market is likely to see faster differentiation and stronger premiumization in dry cough products than in more established wet cough lines.

By Distribution Channel: Retail Pharmacy Leads While Online Pharmacy Changes the Rules

Retail pharmacy captured 58.22% share in 2025, which kept it as the largest channel in the cough syrup market. Its lead reflects strong pharmacist influence, immediate product access during acute symptom episodes, and the habit of buying cough remedies alongside other health essentials in a single visit. This channel still matters because urgency is a defining part of cough medicine purchasing, and physical pharmacies remain well placed to convert that urgency into same-day sales. Retail outlets also continue to support trusted brand visibility, which is especially important in the cough syrup market where many consumers prefer familiar names when symptoms appear suddenly. That gives retail pharmacy a durable role even as digital health channels gain more share.

The cough syrup market size for online pharmacy is projected to expand at an 8.65% CAGR through 2031, which makes it the fastest-growing distribution route in the report. Digital channels are benefiting from repeat ordering, home delivery, price comparison, and stronger use of app-based discovery in urban populations. They also generate more consumer-level data, which can improve promotional timing, stock planning, and product recommendations in ways traditional shelves cannot easily match. This creates a more concentrated digital shelf where ratings, reviews, and search ranking matter as much as packaging and brand history. For the cough syrup market, online pharmacy is no longer only an alternative channel, it is becoming a core competitive battleground for future growth.

Geography Analysis

North America held 36.52% of the cough syrup market share in 2025, which gave it the leading regional position in the report. The region benefits from strong OTC consumer habits, deep pharmacy coverage, and high brand recognition for established respiratory relief products. In the United States, the 2025 to 2026 flu season had reached at least 47 million illnesses and 610,000 hospitalizations through April 2026, which supported heavy seasonal demand for cough and cold products. Canada and Mexico remain smaller contributors, but both continue to benefit from pharmacy network reach and steady self-medication behavior. This combination keeps North America central to the cough syrup market because it offers both volume stability and strong branded product economics.

Europe remains a major region for the cough syrup market, especially across dry cough syrup and wet cough syrup categories where herbal adoption and OTC familiarity are both well developed. Germany holds the largest national share within Europe, supported by a mature consumer healthcare base and a well-established herbal medicines infrastructure. EU herbal monographs have helped make Europe the most commercially active region for botanical cough formulations, and Reckitt reported that its Strepsils Cough Dual Action range reached market leadership across 15 EU markets. France, the United Kingdom, Italy, and Spain also contribute meaningful revenue, though consumer preferences differ by formulation style and natural ingredient appeal. The region remains important to the cough syrup market because it combines regulatory support for herbal innovation with strong consumer willingness to try differentiated formulations.

Asia-Pacific represents the fastest-growing regional component of cough syrup market size, with a 7.45% CAGR projected through 2031. India and China are the main volume engines because large populations, better pharmacy access, and broader digital health use continue to lift demand. China’s 2024 reclassification of dextromethorphan changed the balance of OTC suppressant products and now favors portfolios with non-DXM alternatives. India adds growth through rising self-medication and a larger elderly population, but quality oversight has tightened sharply after the 2025 contaminated cough syrup events. South Korea, Japan, and Australia remain smaller in volume but stronger in premium pricing and novel delivery formats. The Middle East and Africa, along with South America, are also gaining relevance as retail pharmacy access expands and branded OTC products displace some traditional home remedies. Together, these markets keep the cough syrup market geographically broad, but Asia-Pacific now carries the clearest growth momentum.

Competitive Landscape

The cough syrup market shows moderate concentration at the branded end and much wider fragmentation across generic and private-label supply. Large consumer health companies such as Haleon, Reckitt, Procter and Gamble, Opella Healthcare Group, and others hold strong brand visibility and shelf access in major markets. This gives the cough syrup market a clear set of recognizable leaders, but it does not eliminate price competition because local producers remain active in India, China, Brazil, and other price-sensitive markets. The result is a market where brand strength matters greatly in premium OTC tiers, while share below that level remains widely distributed across regional and store-led offerings.

Strategic behavior in the cough syrup market is centered on format innovation, herbal integration, and better control over supply and channel access. Reckitt opened its largest OTC manufacturing facility in the United States in December 2024, a 310,000 square foot site in Wilson, North Carolina, backed by a USD 200 million investment. That move shows how leading companies are bringing manufacturing capacity closer to demand centers so they can improve resilience and support faster product rollout. Haleon completed the purchase of the remaining 12% stake in its China joint venture in June 2025, which strengthened its control over operations in an important growth market. Reckitt also used clinically supported herbal positioning to expand Strepsils Cough Dual Action, which shows how large players are competing through evidence-backed natural formulations rather than only through legacy brand names.

White space in the cough syrup market is strongest around evidence-backed herbal suppressants, pediatric non-DXM platforms, and digital models that support repeat management of recurring cough symptoms. Private-label programs continue to pressure margins, especially where active ingredient parity is easy to understand and shelf comparison is straightforward. Smaller Indian and Chinese manufacturers still have room to grow in export markets, but the 2025 contamination incidents have made buyers more selective on quality systems and sourcing discipline. Haleon’s annual report also showed that even major respiratory portfolios can face short-term volatility, with its Respiratory Health division reporting a 1.9% organic revenue decline in 2025 after a weaker cold and flu season in North America and Central and Eastern Europe. This leaves the cough syrup market competitive in a very practical way, where scale, regulatory readiness, supply control, and brand trust matter, but none of them fully remove execution risk.

Cough Syrup Industry Leaders

Reckitt Benckiser Group plc

Haleon plc

Kenvue Inc.

Procter and Gamble Company

Opella Healthcare Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: China's API price surge following geopolitical supply chain tensions pushed paracetamol prices to approximately double their pre-crisis levels, with azithromycin and other pharmaceutical APIs rising 30–40%; oral liquid cough syrup manufacturers reliant on single-source Chinese API supply face near-term cost inflation and potential SKU availability risks.

- October 2025: The US FDA issued a public alert confirming the DEG/EG contamination of children's cough syrups manufactured by four Indian companies (Sresan Pharmaceuticals, Shape Pharma, Rednex Pharmaceuticals, and Kaysons Pharma), coordinating with the WHO and India's CDSCO. The FDA confirmed none of the named products entered the US market and reminded manufacturers of existing glycerin testing guidance.

Global Cough Syrup Market Report Scope

As per the scope of the report, Cough syrup is a liquid medication formulated to relieve coughing. It typically contains active ingredients such as suppressants to reduce the cough reflex or expectorants to loosen mucus. Cough syrups may also contain other ingredients to soothe the throat or address symptoms associated with coughs.

The segmentation of the cough syrup market is categorized by product type, age group, prescription type, cough type, distribution channel, and geography. By product type, the market includes expectorants, cough suppressants/antitussives, and combination medications. By age group, it is segmented into pediatric, adult, and geriatric. Based on prescription type, the market is divided into prescription and over-the-counter. By cough type, it is classified into dry cough and wet cough. The distribution channel segmentation includes retail pharmacy, hospital pharmacy, and online pharmacy. Geographically, the market is segmented into North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. For each segment, the market size and forecast are provided in terms of value (USD).

| Expectorants |

| Cough Suppressants/Antitussives |

| Combination Medications |

| Pediatric |

| Adult |

| Geriatric |

| Prescription |

| Over-the-Counter |

| Dry Cough |

| Wet Cough |

| Retail Pharmacy |

| Hospital Pharmacy |

| Online Pharmacy |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Expectorants | |

| Cough Suppressants/Antitussives | ||

| Combination Medications | ||

| By Age Group | Pediatric | |

| Adult | ||

| Geriatric | ||

| By Prescription Type | Prescription | |

| Over-the-Counter | ||

| By Cough Type | Dry Cough | |

| Wet Cough | ||

| By Distribution Channel | Retail Pharmacy | |

| Hospital Pharmacy | ||

| Online Pharmacy | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the cough syrup market?

The cough syrup market is valued at USD 4.72 billion in 2026 and is forecast to reach USD 6.27 billion by 2031, growing at a 5.85% CAGR.

Which region leads global demand for cough syrups?

North America held the largest regional share at 36.52% in 2025, supported by strong OTC adoption, dense pharmacy access, and established brand loyalty.

Which product type is growing the fastest in cough syrups?

Combination medications are projected to grow at a 7.38% CAGR through 2031 as consumers increasingly prefer one product that addresses several symptoms.

Why is online pharmacy becoming important for cough syrup sales?

Online pharmacy is forecast to grow at an 8.65% CAGR through 2031 because delivery convenience, repeat ordering, and digital discovery are changing purchase behavior.

Which age group creates the largest revenue base for cough syrups?

Adults accounted for 48.24% share in 2025, reflecting frequent self-medication, brand familiarity, and strong demand for convenient OTC symptom relief.

What are the main risks shaping future cough syrup demand?

The main risks are tighter active ingredient regulation, pediatric safety concerns, misuse of dextromethorphan, and stronger quality oversight after contamination-related incidents.

Page last updated on: