Respiratory Protection Equipment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

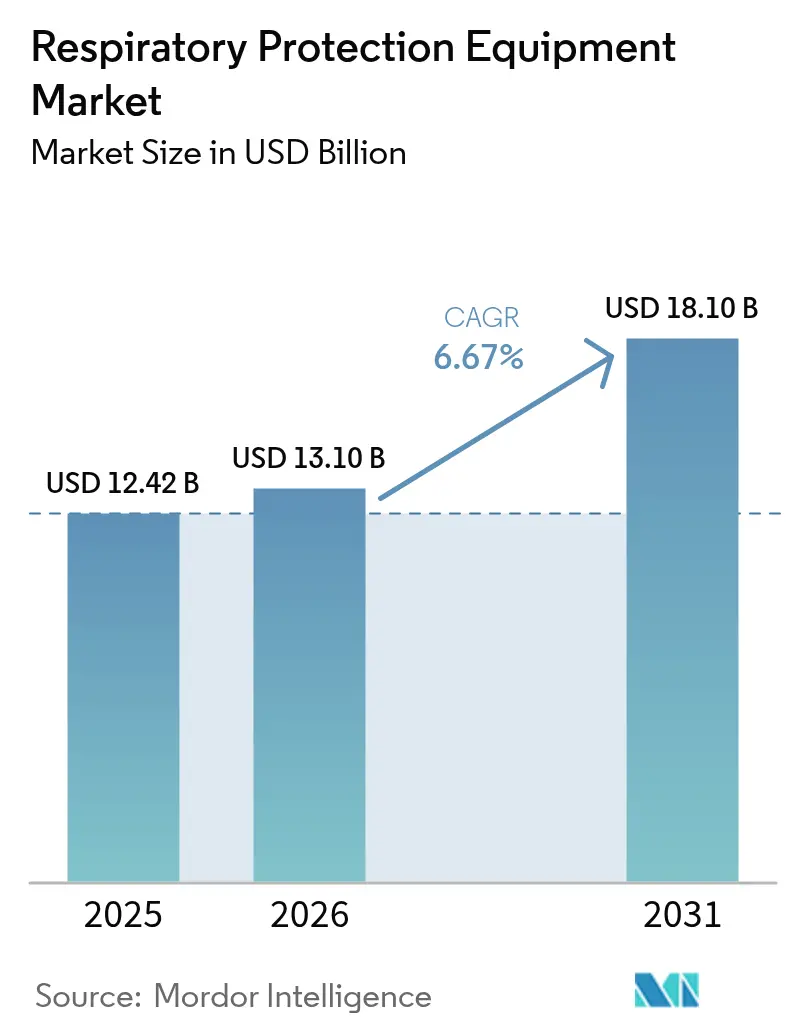

| Market Size (2026) | USD 13.10 Billion |

| Market Size (2031) | USD 18.10 Billion |

| Growth Rate (2026 - 2031) | 6.67% CAGR |

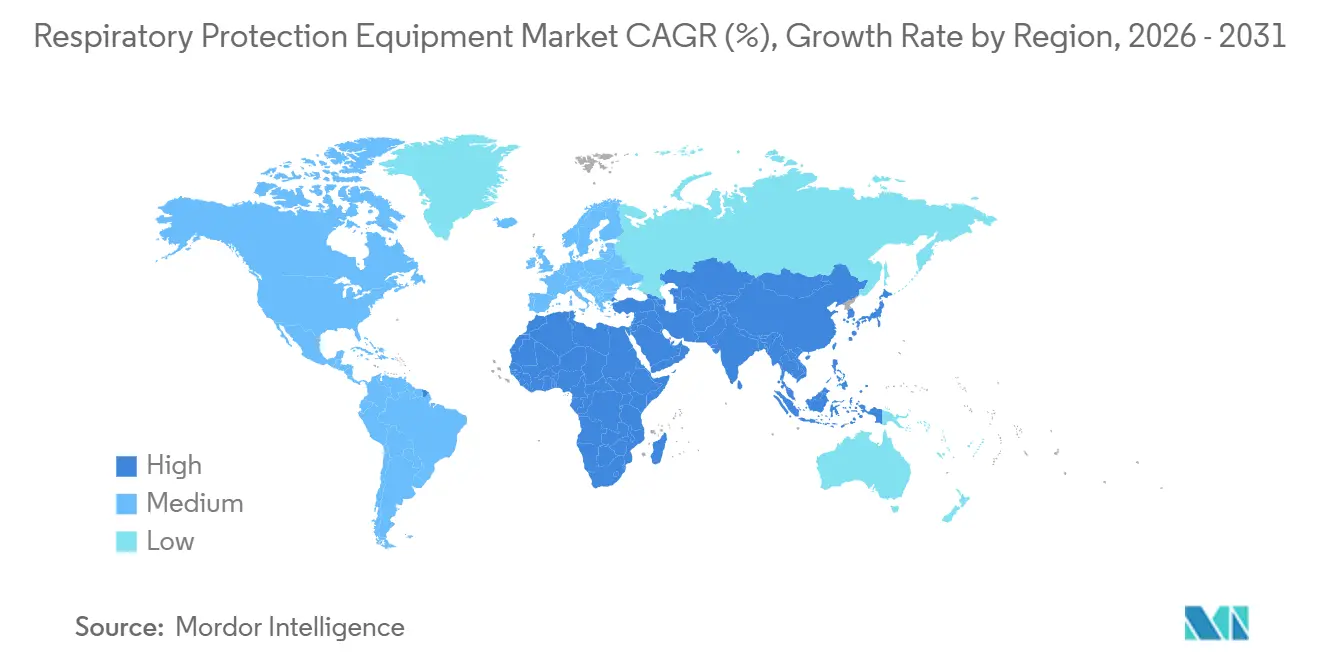

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

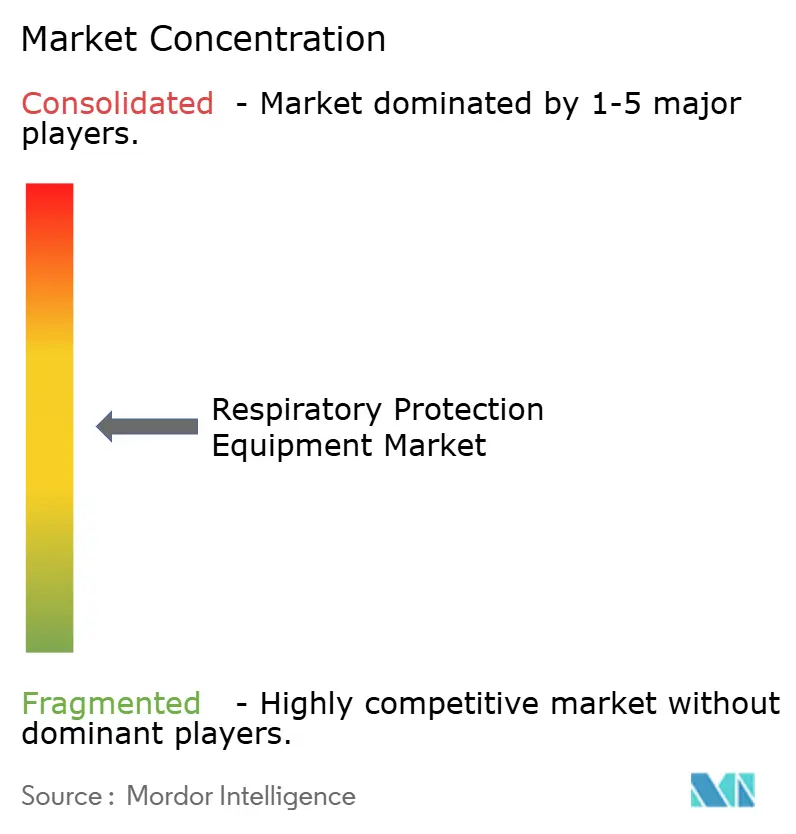

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Respiratory Protection Equipment Market Analysis by Mordor Intelligence

The Respiratory Protection Equipment Market size was valued at USD 12.42 billion in 2025 and is estimated to grow from USD 13.10 billion in 2026 to reach USD 18.10 billion by 2031, at a CAGR of 6.67% during the forecast period (2026-2031).

Tightening occupational exposure limits across construction, mining, and healthcare continue to shift spending from one-off pandemic spikes toward programmatic procurement. U.S. regulatory streamlining that removes pre-use medical evaluations for common filtering facepiece and loose-fitting powered air-purifying models lowers compliance friction for small employers and sustains baseline volume.[1]Occupational Safety and Health Administration, “Respiratory Protection,” U.S. Department of Labor, osha.gov Federal surge-capacity programs have locked in recurring orders, with the Strategic National Stockpile holding more than 350 million N95 units by late 2024.[2]“Strategic National Stockpile,” U.S. Department of Health and Human Services, phe.gov Parallel stockpiles in Canada and Australia reinforce this trend and anchor predictable replenishment cycles. At the same time, upstream oil-and-gas projects in sour-gas fields, wildfire smoke emergencies, and large Asian infrastructure builds provide fresh demand channels that keep factory utilization high even as COVID-19 fades.

Key Report Takeaways

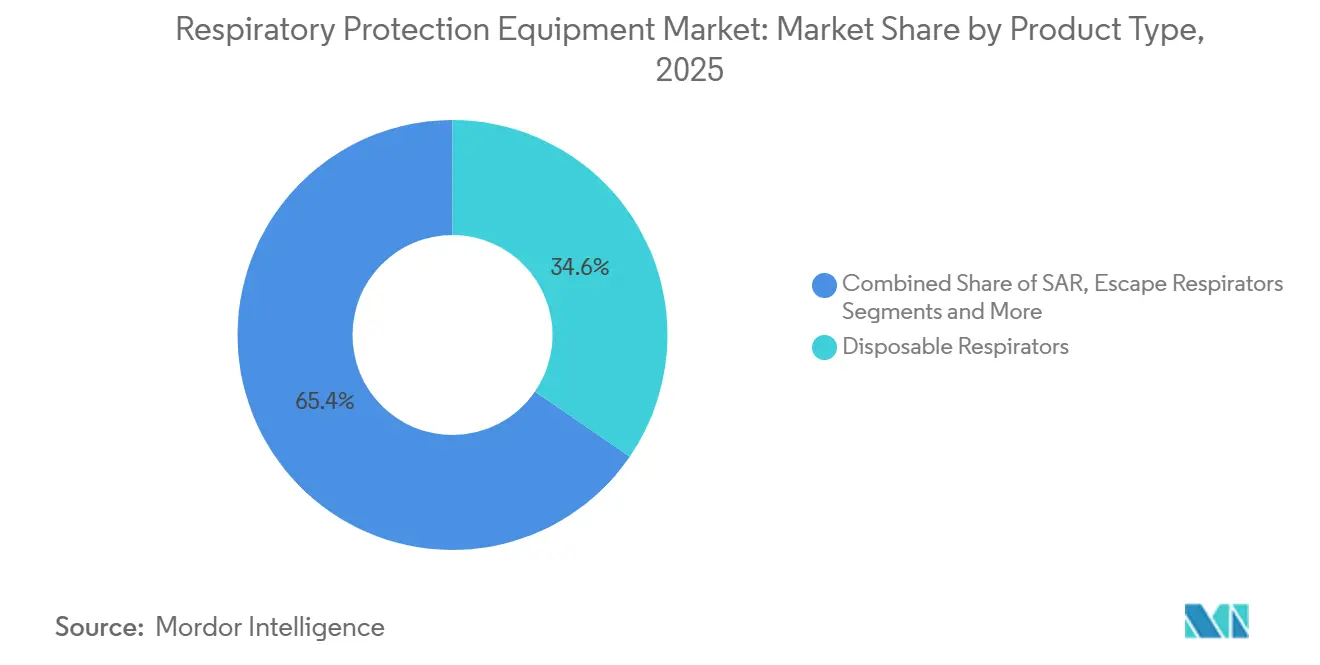

- Disposable respirators led with 34.58% revenue in 2025, while powered air-purifying respirators are forecast to expand at a 9.44% CAGR to 2031.

- Particulate-only devices captured 44.63% share of the respiratory protection equipment market size in 2025, yet biological respirators lead growth with an 8.94% CAGR through 2031.

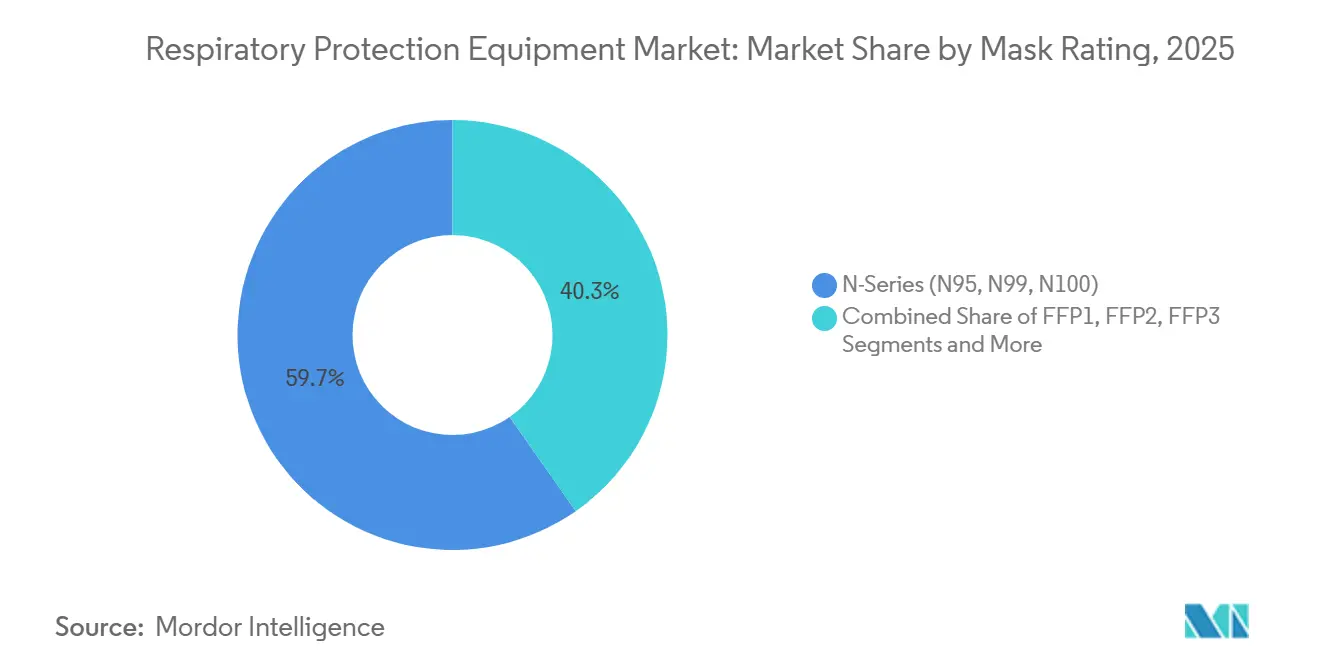

- N-series products dominated 59.72% of 2025 volume, whereas FFP3 units are advancing at a 9.35% CAGR on the back of new European nano-particle rules.

- Fabric disposables held 64.37% of 2025 revenue, yet silicone facepieces will post the fastest 8.24% CAGR as hospitals and semiconductor fabs favor reusable platforms.

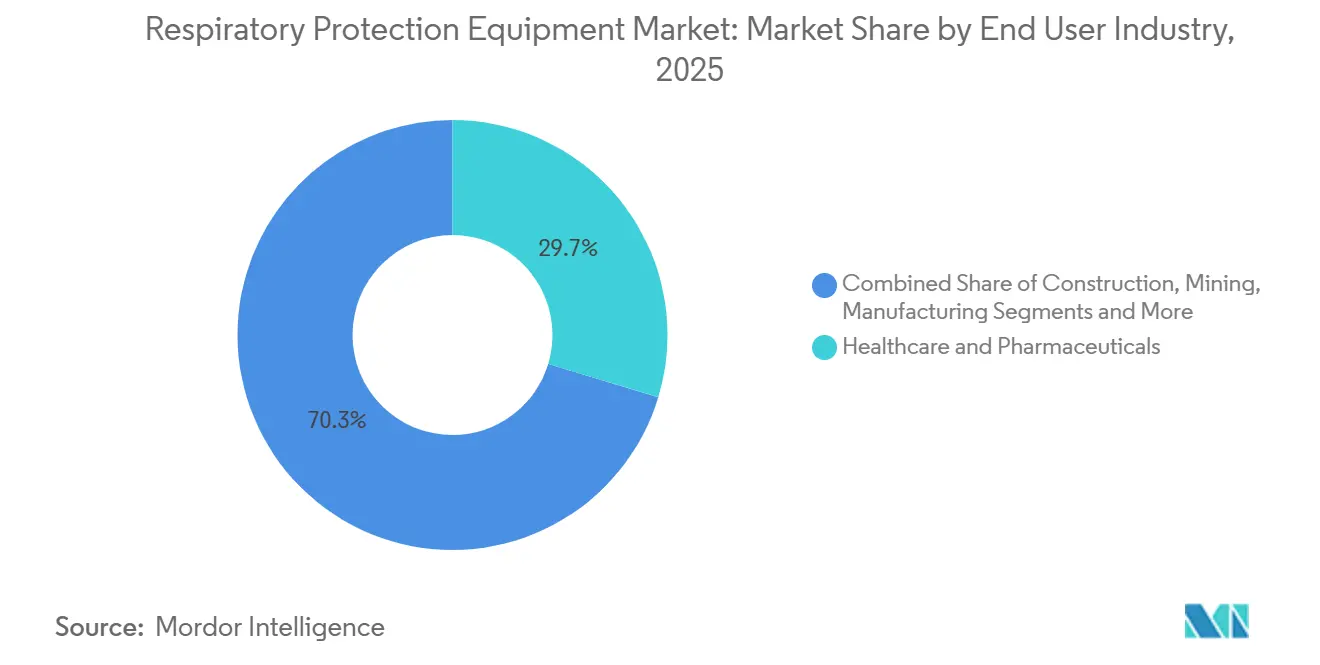

- Healthcare and pharmaceuticals commanded 29.68% of 2025 sales, while firefighting and emergency response is forecast to rise at a 9.73% CAGR to 2031.

- Distributors and wholesalers controlled 51.33% of 2025 revenue; online retail shows the quickest 10.88% CAGR as subscription filter programs reach small worksites.

- North America generated 37.52% of 2025 revenue, but the Asia-Pacific region is on track for the highest 8.32% CAGR thanks to new Indian, Chinese, and Japanese safety mandates.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Respiratory Protection Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent Workplace Safety Regulations | 1.2% | Global, with North America & EU leading enforcement | Medium term (2-4 years) |

| Rising Incidence of Occupational & Infectious Respiratory Diseases | 1.0% | Global, pronounced in APAC manufacturing hubs and healthcare sectors | Long term (≥ 4 years) |

| Industrial Expansion in High-Particulate Sectors (Construction, Mining) | 1.3% | APAC core (China, India), spill-over to MEA and South America | Medium term (2-4 years) |

| Upstream Oil & Gas Resurgence in Toxic-Gas Fields | 0.8% | North America (Permian, Bakken), Middle East, West Africa | Short term (≤ 2 years) |

| Smart, Sensor-Embedded Respirators Enable Predictive Maintenance | 0.9% | North America & EU early adopters, APAC followers | Long term (≥ 4 years) |

| Government Stockpiling Amid Record Wildfire Smoke Seasons | 0.6% | North America (U.S., Canada), Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Stringent Workplace Safety Regulations

Global regulators have tightened exposure rules, forcing employers to move from voluntary programs to mandatory fit testing and record keeping. The U.S. proposal in July 2025 that drops medical clearance for common masks immediately removes paperwork costs for thousands of contractors. OSHA’s silica rule, in full enforcement since 2024, caps worker exposure at 50 µg/m³ and drives orders for P100 filters in stone cutting and sandblasting. Europe’s EN 149 update added nano-particle efficiency tests in 2024, lifting the technical bar for FFP3 approvals and prompting international brands to redesign portfolios.[3]European Committee for Standardization, “EN 149: Respiratory Protective Devices,” en-standard.eu New ISO standards for self-contained breathing apparatus strengthen thermal and communication benchmarks, which accelerates municipal fleet upgrades. Combined, these moves inject a steady floor of compulsory demand into the respiratory protection equipment market.

Rising Incidence of Occupational and Infectious Respiratory Diseases

Silicosis, COPD, and asthma continue to rank among the top work-related illnesses, while healthcare systems prepare for avian influenza spillovers and mpox clusters. NIOSH now advises hospitals to keep a 90-day cache of reusable elastomeric masks, pushing durable-mask orders beyond crisis periods. A 2024 clinical study covering 12-hour nursing shifts reported that 82% of participants favored elastomerics for multi-day use because of lower total cost despite higher breathing effort. Asia’s construction boom aggravates silica Exposure, and state registries in India and China show rising disease incidence, leading to new mandatory respirator rules. WHO’s 2024 preparedness guidance names respiratory protection a Tier 1 countermeasure, prompting stockpiles equal to 10% of each member state’s health-care workforce. These factors compound to keep the respiratory protection equipment market on a solid upward trajectory.

Industrial Expansion in High-Particulate Sectors (Construction, Mining)

Megaprojects across India’s National Infrastructure Pipeline, Indonesia’s new capital, and China’s Belt and Road add millions of worker-years in dusty environments. India now obliges sites exceeding 10,000 m² to supply certified respirators, converting earlier voluntary habits into enforceable rules. China’s push to 90% automated coal mines paradoxically adds near-term mask demand because retrofit crews face diesel particulate and blast dust. Australia’s lithium boom in underground hard rock raises PAPR penetration where heat stress makes half-masks impractical. South Africa reports an 18% drop in silicosis claims after stricter enforcement and real-time dust monitors. Brazil’s fast-growing agribusiness needs pesticide and biomass protection, yet lacks dense distributor networks, which opens room for online platforms. Together, these project pipelines expand the respiratory protection equipment market well beyond healthcare.

Upstream Oil & Gas Resurgence in Toxic-Gas Fields

Hydrogen-sulfide concentrations in U.S. shale plays often exceed OSHA’s 10 ppm limit during flowback, mandating supplied-air or SCBA solutions. Operators deploy trailer-mounted systems that cover multiple workers without cylinder weight. Saudi Arabia’s Jafurah gas project requires every field worker to carry escape respirators plus monitors, creating bulk orders backed by government budgets. West Africa’s deep-water projects add offshore demand for 15-minute escape units, while North American carbon-capture pilots write new rules for supercritical CO₂ plumes. All of these activities inject specialty-grade volume into the respiratory protection equipment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Acquisition & Maintenance Cost of Advanced RPE | -0.7% | Global, acute in price-sensitive APAC and South America markets | Medium term (2-4 years) |

| Low Wearer-Comfort & Compliance Rates | -0.5% | Global, pronounced in high-heat/humidity environments (MEA, South Asia) | Long term (≥ 4 years) |

| Critical Filter-Media Supply Chain Constraints | -0.4% | Global, with bottlenecks in meltblown polymer sourcing | Short term (≤ 2 years) |

| Unclear Nano-Particle Exposure Regulations Delaying Approvals | -0.3% | North America & EU regulatory jurisdictions | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Acquisition and Maintenance Cost of Advanced RPE

Powered air-purifying and supplied-air systems cost USD 800–3,000 per unit plus 20% annual upkeep, which pushes smaller firms toward cheaper disposables. Ansell’s USD 80 million Indian factory will cut elastomeric landed cost by 15%, yet disposable N95s at USD 1–3 each still win on cash outlay. Hospitals face parallel economics: rural facilities avoid elastomerics because they lack centralized decontamination. Fire departments budgeting USD 5,000–8,000 per SCBA struggle to fund annual flow testing and cylinder recertification. Capital intensity therefore caps adoption rates in the respiratory protection equipment market.

Low Wearer Comfort and Compliance Rates

Respirators increase breathing effort, trap heat, and hamper speech. A 2024 study showed 68% of healthcare staff find elastomerics harder to breathe through, and 74% reported more heat discomfort across 12-hour shifts. High humidity in the Middle East and South Asia makes full-shift compliance even harder, triggering mask-hanging behavior that defeats protection. Silicone facepieces cut dermatitis risk but still fog eyewear in 8–12% of users. Until materials like viscoelastic foam seals reach mass market, comfort will restrain the respiratory protection equipment market’s full potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: PAPR Growth Outpaces Disposable Dominance

Disposable masks still dominate on price and convenience, accounting for 34.58% of 2025 revenue in the respiratory protection equipment market. Powered air-purifying respirators, however, are projected to record the highest 9.44% CAGR as clean-room operators and welders embrace lighter blowers and integrated sensors. Half-mask elastomerics remain the standard for oil-and-gas crews because a USD 40 facepiece plus USD 15 cartridges delivers season-long value. Full-face models capture pesticide and confined-space tasks by adding eye protection. Supplied-air and SCBA solutions hold niche but high-value pockets in paint booths and firefighting.

MSA’s 2024 partnership with optrel blended breath-following blowers into welding helmets, cutting user fatigue by 18%. This integration shows how upstream technology raises compliance and ASPs. Disposable demand, by contrast, stays highly price elastic; a 10% price hike can reduce unit volume by 6–8%. Such sensitivity underscores why premium devices will capture growth even as low-cost disposables hold volume leadership in the respiratory protection equipment market.

By Protection Type: Biological Respirators Surge on Preparedness

Particulate-only gear delivered 44.63% of 2025 worldwide sales, yet biological and infectious-agent models will expand at an 8.94% CAGR to 2031. Hospitals now formalize 90-day caches of elastomeric or P100 cartridges after WHO placed respiratory protection in its top countermeasure tier. Gas-and-vapor cartridges support chemical and wastewater sites but require frequent replacement. Combination filters handle spray-painting and pesticide mixing where simultaneous hazards exist.

A clinical comparison in 2024 showed 82% of healthcare workers preferred elastomerics for multi-day use because of lower total cost over disposable N95s. Certifications remain complex since NIOSH evaluates particulate and gas claims separately, which stretches development timelines. Even so, added biological regulations position high-filtration devices to capture greater respiratory protection equipment market share as preparedness spending stabilizes.

By Mask Rating: FFP3 Gains as Nano-Particle Concerns Mount

N-series respirators held 59.72% of global volume in 2025, reflecting NIOSH’s dominance and construction familiarity. FFP3 units are forecast to grow at 9.35% CAGR as Europe enforces tougher nano-particle tests under the updated EN 149. R- and P-series filters serve oily environments, and P100 grades carry 20–30% price premiums yet last longer. FFP1 sits at the low end with only 80% efficiency and is shifting to non-regulated niches.

Pharmaceutical expansions in Ireland and Switzerland now mandate FFP3 or higher, pushing demand. ASTM’s WK73468 standard demands P100-level filtration for first responders, nudging procurement away from legacy mid-tier masks. As nano-particle scrutiny rises, FFP3 penetration will continue to lift the respiratory protection equipment market size for premium grades.

By Facepiece Material: Silicone Comfort Drives Reusable Adoption

Fabric and polypropylene disposables generated 64.37% of 2025 revenue. Silicone facepieces are on pace for an 8.24% CAGR owing to hypoallergenic properties and better seal retention during long shifts. Thermoplastic elastomer provides a middle ground for cost-sensitive buyers who still want comfort. Neoprene lingers in older inventories but suffers ozone and oil degradation.

California’s 2024 law that extends producer responsibility for single-use plastics adds USD 0.10–0.15 per disposable unit. This eco-cost tilts budgets toward reusable silicone platforms, especially in landfill-constrained regions. While certification costs slow material substitution, ongoing R&D into lighter polyurethane foam seals promises to widen the addressable base inside the respiratory protection equipment market.

By End-User Industry: Firefighting Segment Accelerates on Fleet Renewals

Healthcare accounted for 29.68% of 2025 revenue, anchored by infection control. Firefighting and emergency response is projected to log the fastest 9.73% CAGR through fleet renewal programs backed by federal grants. Oil-and-gas sites remain heavy users of supplied-air gear because hydrogen-sulfide routinely exceeds OSHA limits. Construction demand aligns with silica compliance, while mining upgrades to P100 or PAPR solutions as automation retrofits raise short-term dust exposure.

Manufacturing applications vary by task, from organic vapors in paint shops to welding fumes in metal fabrication. Chemicals and wastewater treatment need chemisorbent cartridges for ammonia or chlorine. Wildfire smoke events add public-distribution channels outside traditional industrial markets, further expanding the respiratory protection equipment market.

By Distribution Channel: Online Retail Disrupts Traditional Wholesalers

Distributors and wholesalers still hold 51.33% of 2025 sales, but online retail enjoys a 10.88% CAGR by unbundling price and offering subscription filter deliveries. Amazon Business and Grainger’s portal help small worksites bypass minimum order sizes. Direct sales stay important for large refineries and hospitals that need bespoke configurations and on-site service contracts.

PIP’s acquisition of Honeywell’s PPE brands tightens vertical integration and captures margin across both manufacturing and distribution tiers. Subscription models particularly resonate in pharmaceutical and semiconductor fabs, where automated replenishment averts costly downtime. The shift online therefore adds new buyer segments and raises overall velocity in the respiratory protection equipment market.

Geography Analysis

North America generated 37.52% of 2025 revenue as OSHA enforcement of the crystalline-silica rule combined with oil-field activity to drive steady orders. Federal wildfire-smoke stockpiles add a public health layer of demand, while carbon-capture pilots create new toxic-gas scenarios that need specialized gear. Canada’s government investment in community N95 distribution underpins rural uptake, and Mexico’s maquiladora belt sustains disposable volumes despite uneven enforcement.

The Asia-Pacific respiratory protection equipment market outpaces all regions with an 8.32% CAGR to 2031. India now enforces respirator provision on large sites, China’s mine mechanization temporarily raises dust exposure for retrofit workers, and Japan’s aging labor force values lighter ergonomic designs. Australia doubles lithium output between 2020 and 2025, which favors PAPRs in deep, hot mines. South Korea’s semiconductor and biopharma investments prefer FFP3 or P100 filtration to protect clean-room yields.

Europe maintains mid-single-digit expansion as EN 149 nano-particle updates lift procurement grades and the chemical sector renews full-face inventories. Germany’s chemical giants keep stringent chlor-alkali protection standards. France’s nuclear-maintenance schedules call for supplied-air systems, while the UK’s HSE update in 2024 tightens fit-test record keeping. The Middle East builds demand through gas megaprojects like Jafurah, and South Africa’s mining upgrades sustain orders for high-filtration gear. South American pockets such as Brazilian agribusiness and Argentine lithium see healthy volumes but face distribution bottlenecks that online channels aim to solve.

Competitive Landscape

The key suppliers includes MSA Safety, 3M’s Solventum spin-off, Drägerwerk, and Avon Protection collectively hold share of global revenue. That leaves room for regional champions like Shigematsu in Japan and Sundström in Scandinavia that win with fast domestic certification and close distributor ties. Technology integration marks the new competitive frontier: MSA’s FireGrid-enabled SCBA streams data for predictive maintenance and earned a USD 33 million U.S. Coast Guard contract. Drägerwerk and Sundström embed RFID tags for automated filter tracking, aligning with chemical-plant safety software.

Vertical integration also rises. Ansell’s Indian plant cuts silicone facepiece costs and shields against tariff shifts. Horizontal M&A gains pace as PIP folds Honeywell’s North, Miller, and Morning Pride brands into its network, broadening channel reach. Online newcomers promote subscription cartridges that lower reorder friction, while fit-test-as-a-service startups use smartphone scanning to boost compliance.

As smart sensors become table stakes, laggards that lack connectivity struggle to clear updated ASTM and ISO benchmarks. Fit diversity is another differentiator: Moldex and JSP each offer up to 10 face sizes versus the common three, reducing fit-test failures and winning contracts in markets with rigid enforcement. Moderate concentration and active innovation keep pricing competitive but sustain ample room for specialized differentiation within the respiratory protection equipment market.

Respiratory Protection Equipment Industry Leaders

Honeywell International Inc.

MSA Safety Incorporated

Drägerwerk AG & Co. KGaA

Kimberly-Clark Corporation

Solventum

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: VENUS Safety & Health announced continued expansion of domestic respirator production under India’s Make in India program, strengthening export capacity and reducing import dependence.

- February 2026: Synchrony Medical closed a USD 5 million funding round to accelerate U.S. commercialization of the LibAirty airway-clearance system.

- July 2025: OSHA proposed amendments to 29 CFR 1910.134 to eliminate medical evaluation for filtering facepiece and loose-fitting PAPR users while retaining fit-test and training requirements.

Global Respiratory Protection Equipment Market Report Scope

As per the scope of the market, respiratory protective equipment is a type of personal protective equipment used for protecting an individual against hazardous substances (chemicals, dust particles, and gas) in various industries, including healthcare, public safety services, and manufacturing industries.

The Respiratory Protection Equipment Market Report is segmented by Product Type, Protection Type, Mask Rating, Facepiece Material, End‑user Industry, Distribution Channel, and Geography. By Product Type, the market is segmented into Disposable, Half‑Mask Reusable, Full‑Face Reusable, PAPR, SAR, SCBA, and Escape devices. By Protection Type, the market is segmented into Particulate‑Only, Gas & Vapor, Combination, and Biological protection. By Mask Rating, the market is segmented into N‑Series, R‑Series, P‑Series, FFP1, FFP2, and FFP3. By Facepiece Material, the market is segmented into Silicone, TPE, Neoprene, and Fabric. By End‑user Industry, the market is segmented into Oil & Gas, Healthcare, Construction, Mining, Firefighting, Manufacturing, and Chemicals. By Distribution Channel, the market is segmented into Direct Sales, Distributors, and Online Retail. By Geography, the market is segmented into North America, Europe, Asia‑Pacific, Middle East & Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value in (USD million) for the above segments.

| Disposable Respirators |

| Half-Mask Reusable Respirators |

| Full-Face Reusable Respirators |

| Powered Air-Purifying Respirators (PAPR) |

| Supplied-Air Respirators (SAR) |

| Self-Contained Breathing Apparatus (SCBA) |

| Escape Respirators |

| Particulate-Only Respirators |

| Gas & Vapor Respirators |

| Combination (Particulate + Gas/Vapor) |

| Biological/Infectious-Agent Respirators |

| N-Series (N95, N99, N100) |

| R-Series (R95, R99, R100) |

| P-Series (P95, P99, P100) |

| FFP1 |

| FFP2 |

| FFP3 |

| Silicone |

| Thermoplastic Elastomer (TPE) |

| Neoprene / Rubber |

| Fabric / Polypropylene (Disposable) |

| Oil & Gas |

| Healthcare & Pharmaceuticals |

| Construction |

| Mining |

| Firefighting & Emergency Responders |

| Manufacturing |

| Chemicals |

| Others |

| Direct Sales |

| Distributors / Wholesalers |

| Online Retail |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Product Type | Disposable Respirators | |

| Half-Mask Reusable Respirators | ||

| Full-Face Reusable Respirators | ||

| Powered Air-Purifying Respirators (PAPR) | ||

| Supplied-Air Respirators (SAR) | ||

| Self-Contained Breathing Apparatus (SCBA) | ||

| Escape Respirators | ||

| By Protection Type | Particulate-Only Respirators | |

| Gas & Vapor Respirators | ||

| Combination (Particulate + Gas/Vapor) | ||

| Biological/Infectious-Agent Respirators | ||

| By Mask Rating | N-Series (N95, N99, N100) | |

| R-Series (R95, R99, R100) | ||

| P-Series (P95, P99, P100) | ||

| FFP1 | ||

| FFP2 | ||

| FFP3 | ||

| By Facepiece Material | Silicone | |

| Thermoplastic Elastomer (TPE) | ||

| Neoprene / Rubber | ||

| Fabric / Polypropylene (Disposable) | ||

| By End-user Industry | Oil & Gas | |

| Healthcare & Pharmaceuticals | ||

| Construction | ||

| Mining | ||

| Firefighting & Emergency Responders | ||

| Manufacturing | ||

| Chemicals | ||

| Others | ||

| By Distribution Channel | Direct Sales | |

| Distributors / Wholesalers | ||

| Online Retail | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected value of the respiratory protection equipment market in 2031?

It is forecast to reach USD 18.10 billion by 2031, supported by a 6.67% CAGR from 2026.

Which product type is growing fastest to 2031?

Powered air-purifying respirators lead with a 9.44% CAGR as comfort and sensor features improve.

Which region shows the highest forecast growth?

Asia-Pacific is set to expand at an 8.32% CAGR thanks to new safety mandates and industrial projects.

Why are FFP3 masks gaining share in Europe?

Updated EN 149 nano-particle tests push buyers toward FFP3 filtration for pharmaceutical and clean-room use.

How is online retail changing procurement patterns?

E-commerce and subscription filter programs grow at 10.88% CAGR, offering lower pricing and automated replenishment.

Page last updated on: