Pediatric Asthma Treatment Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

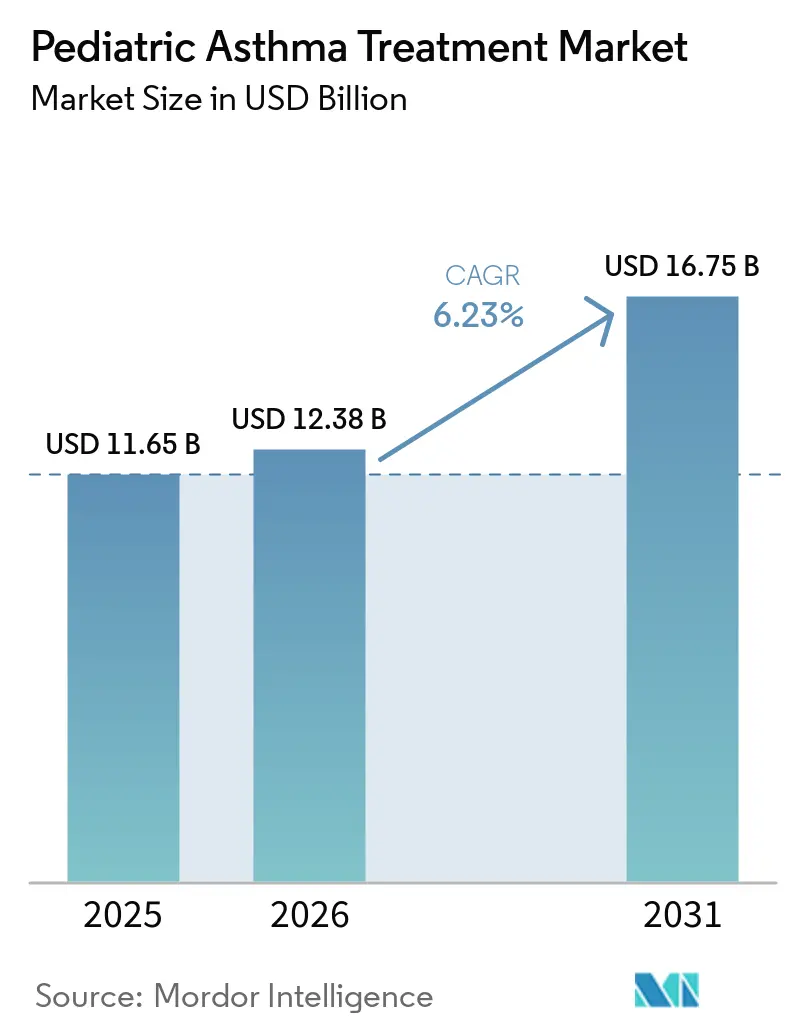

| Market Size (2026) | USD 12.38 Billion |

| Market Size (2031) | USD 16.75 Billion |

| Growth Rate (2026 - 2031) | 6.23% CAGR |

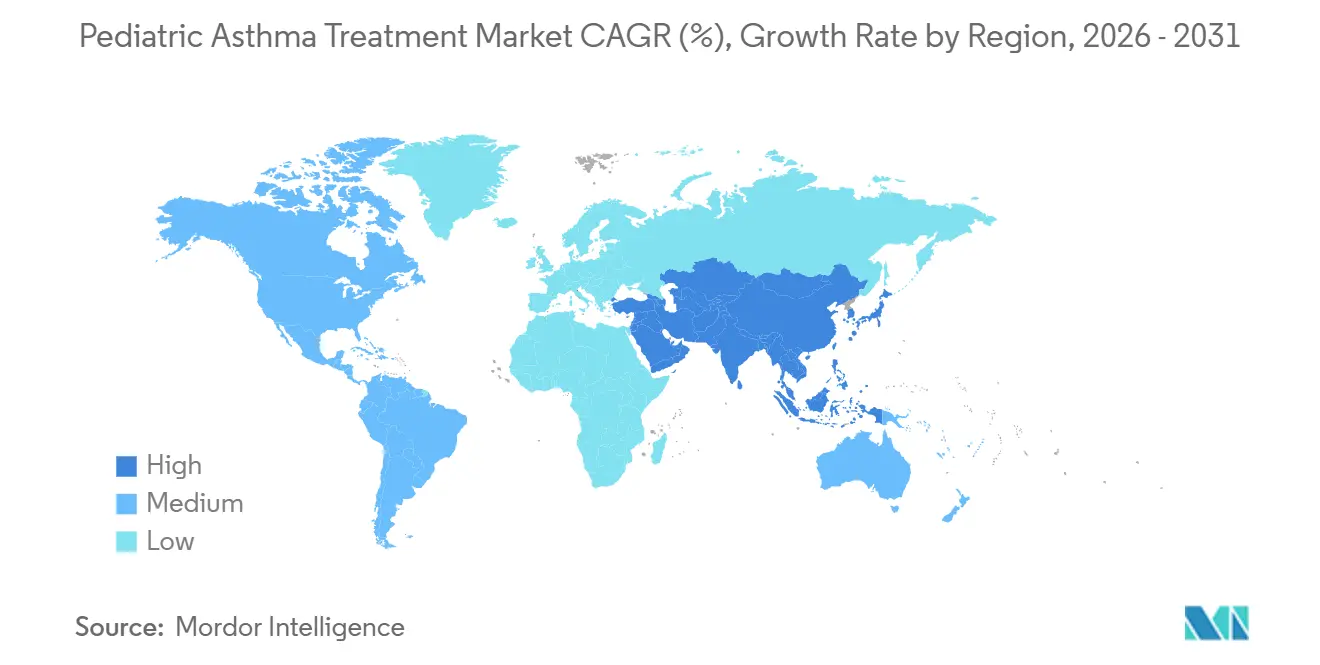

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Pediatric Asthma Treatment Market Analysis by Mordor Intelligence

The Pediatric Asthma Treatment Market size is projected to expand from USD 11.65 billion in 2025 and USD 12.38 billion in 2026 to USD 16.75 billion by 2031, registering a CAGR of 6.23% between 2026 to 2031.

Earlier diagnosis across primary care, clearer pediatric criteria in updated guidelines, and consistent controller initiation are expanding the treated base in the pediatric asthma treatment market. Pollution-linked exacerbations and seasonal respiratory infections keep rescue demand elevated even as controller use rises, which sustains a balanced mix of chronic and acute therapies in the pediatric asthma treatment market. Label expansions for pediatric biologics and the arrival of ultra-long-acting dosing support adherence in severe cases and broaden specialty use within the pediatric asthma treatment market. Digitally enabled inhalers under evaluation in schools and primary care settings are building early evidence for improved technique and adherence, adding a data layer that can guide step-up or step-down decisions in the pediatric asthma treatment market. Payer controls and safety monitoring remain key headwinds, with strict prior authorization criteria and growth-related warnings shaping dosing choices and persistence in the pediatric asthma treatment market.

Key Report Takeaways

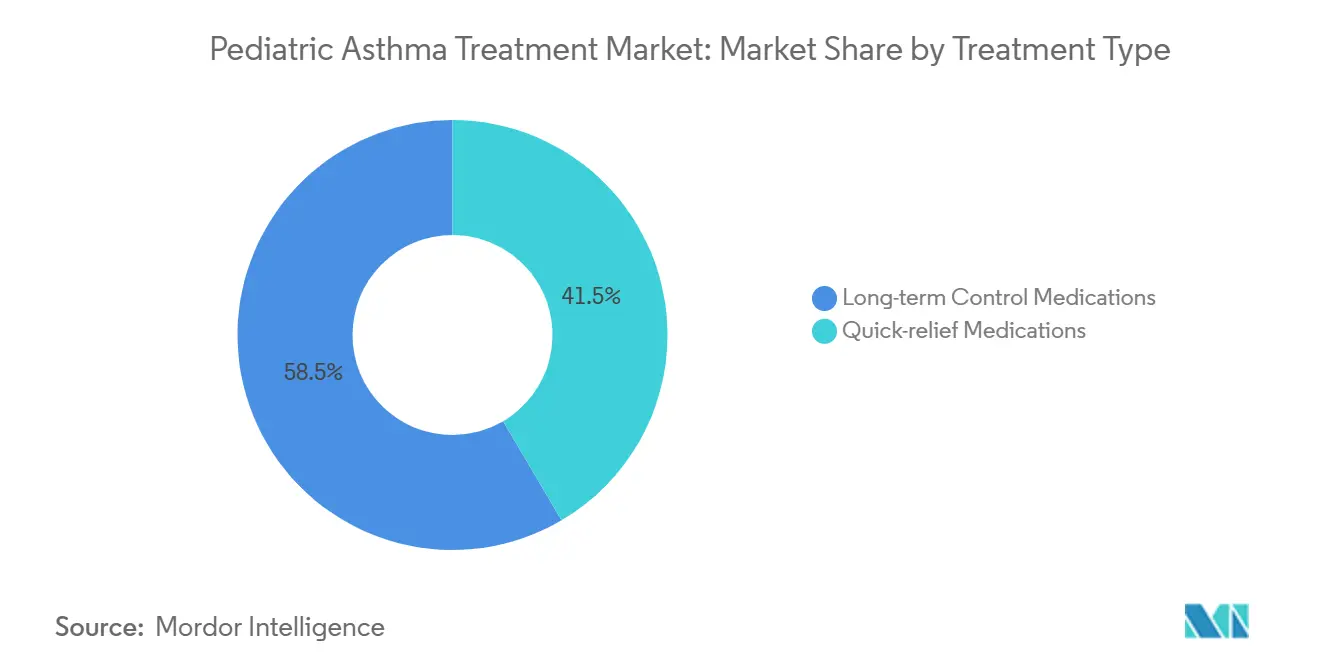

- By treatment type, long-term control medications led with 58.47% of the pediatric asthma treatment market share in 2025. Quick-relief medications are projected to grow at a 6.45% CAGR through 2031 in the pediatric asthma treatment market.

- By drug class, inhaled corticosteroids commanded 34.73% share in 2025. Biologics are set to expand at a 7.41% CAGR through 2031 in the pediatric asthma treatment market.

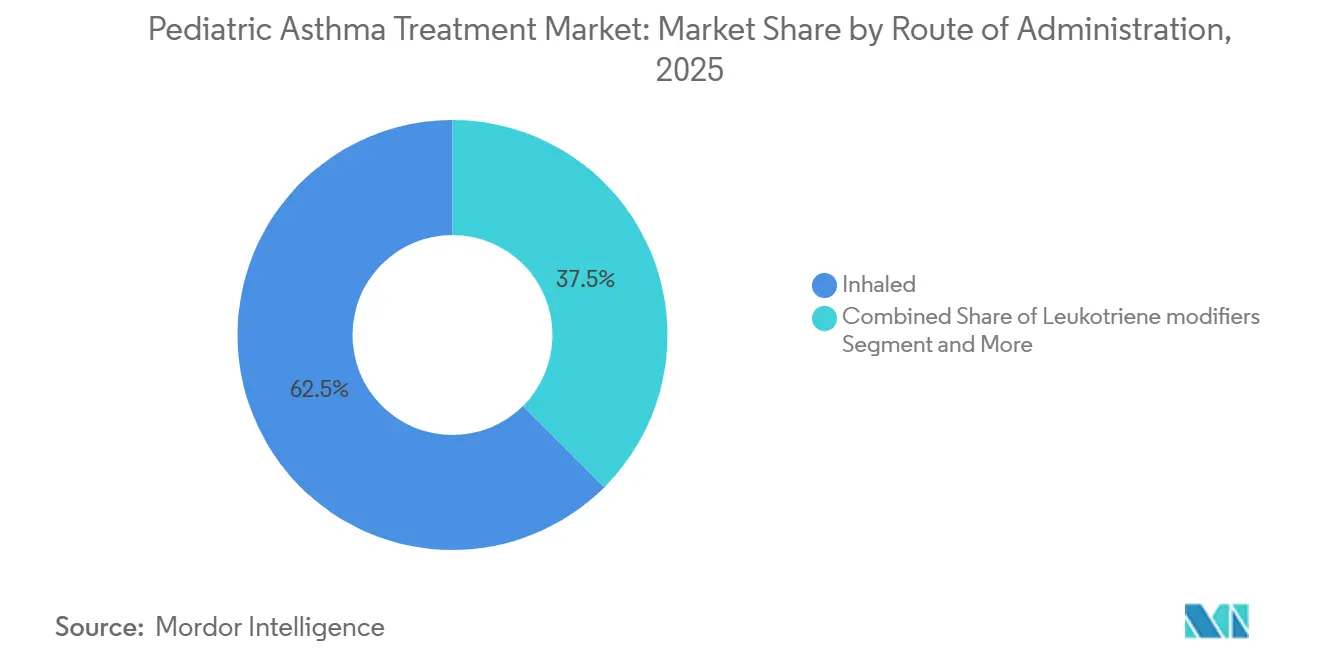

- By route of administration, inhaled formulations held 62.46% share in 2025. Injectables are forecast to post an 8.38% CAGR to 2031.

- By end user, hospitals accounted for 46.89% of the pediatric asthma treatment market share in 2025. Home care is on track to record a 10.69% CAGR through 2031 in the pediatric asthma treatment market.

- By geography, North America held 36.41% share in 2025. Asia-Pacific is forecast to be the fastest growing at an 11.52% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Pediatric Asthma Treatment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Pediatric Asthma Prevalence and Earlier Diagnosis | +1.4% | Global, with early gains in urban China, coastal U.S. states, Australia | Medium term (2-4 years) |

| Air Pollution and Respiratory Infections Elevate Exacerbations | +1.1% | APAC core Beijing, Delhi, Bangkok, spill-over to MEA, U.S. wildfire zones | Medium term (2-4 years) |

| Guideline Shift to ICS-Containing Regimens Increases Controller Use | +0.9% | North America and EU adoption, gradual uptake in APAC and LATAM | Short term (≤ 2 years) |

| Pediatric Biologic Label Expansions and Access Programs | +1.3% | Global, led by U.S., EU, Japan, China approvals since 2025 | Long term (≥ 4 years) |

| Smart Inhaler Adherence Programs in Schools and Primary Care | +0.6% | National, early gains in Leicester in the UK and select U.S. urban districts | Long term (≥ 4 years) |

| At-Home Autoinjectors Enabling Home Dosing and Persistence | +0.9% | North America and EU insurance-covered, APAC emerging markets lag | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Pediatric Asthma Prevalence and Earlier Diagnosis

Health agencies report a consistent pediatric asthma burden and persistent disparities, which continue to expand the treated pool within the pediatric asthma treatment market.[1]Centers for Disease Control and Prevention, “Most Recent Asthma Data | Asthma Data,” Centers for Disease Control and Prevention Updated guidance now clarifies how to diagnose asthma in children under 5 by combining recurrent wheeze patterns, exclusion of other causes, and response to therapy, which moves intervention earlier and increases controller use.[2]Global Initiative for Asthma, “Global Strategy for Asthma Management and Prevention, 2025,” Global Initiative for Asthma China’s 2025 pediatric guideline reinforces inhaled corticosteroids as the foundation for reducing exacerbation risk and aligns clinic workflows around consistent controller access in the pediatric asthma treatment market.[3]Chinese Medical Association Pediatric Branch, “Pediatric Bronchial Asthma Diagnosis and Treatment Guideline 2025,” Chinese Journal of Pediatrics Longitudinal modeling for the Western Pacific Region projects continued increases in prevalence over the long term, which aligns with urbanization and allergen exposure patterns seen across the region.[4]Cheng-hao Yang et al., “Temporal Trends of Asthma Among Children in the Western Pacific Region From 1990 to 2045,” JMIR Public Health and Surveillance Routine biomarker use, such as FeNO and blood eosinophils, along with lung function testing from age 5, is becoming more common in outpatient settings, which supports earlier controller initiation and longer treatment duration. Together, these shifts support a stable base of multi-year therapy within the pediatric asthma treatment market.

Air Pollution and Respiratory Infections Elevate Exacerbations

The latest State of the Air report shows that 156.1 million people live in counties with unhealthy ozone or particulate levels, which sustains high rescue medication demand and emergency utilization for children in the pediatric asthma treatment market.[5]American Lung Association, “State of the Air 2025,” American Lung Association EPA evidence links short-term PM2.5 exposure to higher asthma attack severity in children and documents chronic impacts on lung development, making exposure management a material clinical lever. These conditions reinforce the use of anti-inflammatory reliever strategies and controller intensification during high-risk seasons in the pediatric asthma treatment market. National pediatric guidance in China indicates that severe pediatric cases commonly report recurrent exacerbations despite standard therapies, a pattern that reflects environmental load and adherence gaps. Air quality improvements that reduce PM2.5, PM10, and nitrogen dioxide have documented benefits for pediatric respiratory health, which indicates that public health measures can lower exacerbation frequency over time. These dynamics keep a floor under reliever volume and sustain controller growth in the pediatric asthma treatment market.

Guideline Shift to ICS-Containing Regimens Increases Controller Use

Global guidance now clearly advises against SABA-only management at any age and elevates low-dose ICS as the baseline, which increases controller penetration across pediatric cohorts in the pediatric asthma treatment market. For children ages 6 to 11, daily low-dose ICS or as-needed ICS with SABA is advised, and maintenance and reliever therapy with ICS formoterol is prioritized for moderate to severe disease. The 2025 update also clarifies diagnosis pathways for children under 5, which reduces watchful waiting and supports earlier controller starts. Real-world pediatric data show higher measured adherence where action plans and counseling are systematically reinforced in clinic visits, supporting better symptom control over time. Access moves by manufacturers are also relevant, with a 2025 agreement in the United States to broaden availability and lower pricing for select inhaled respiratory medicines through direct purchasing, which can help align practice with guidance in the pediatric asthma treatment market.

Pediatric Biologic Label Expansions and Access Programs

Label expansions are opening targeted options to younger children with severe disease, including the 2024 US approval of benralizumab for ages 6 to 11 years, which directly broadens eligibility in the pediatric asthma treatment market. China followed with a 2025 pediatric approval for the same agent, which extends access in a large and growing specialist care environment. In the United States, the 2025 approval of depemokimab introduced the first ultra-long-acting biologic with twice-yearly dosing, a profile designed to support persistence among adolescents and adults and to limit clinic visits for families. Company assistance platforms remain important for specialty uptake, such as Xolair’s coverage and copay support that streamline prior authorization and dispensing steps. Payers still apply quantity limits and step edits on several agents, which shapes time to therapy and persistence in the pediatric asthma treatment market. Even with these guardrails, wider indications and less frequent dosing are easing access and supporting steady specialty growth in the pediatric asthma treatment market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Cost and Payer Barriers for Advanced Therapies | -1.2% | Global, acute in U.S. private insurance, EU single payer systems, emerging APAC | Short term (≤ 2 years) |

| Safety Warnings and Side Effects Affecting Long Term Use | -0.7% | Global, heightened in North America and EU | Short term (≤ 2 years) |

| Decarbonization-Driven PMDi Propellant Transition and Reformulation Drag | -0.5% | EU regulation enforcement, North America voluntary transition | Medium term (2-4 years) |

| Pediatric Inhaler Technique Variability Undermining Real World Efficacy | -0.8% | Global, acute in low resource settings | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Cost and Payer Barriers for Advanced Therapies

US medical policies set rigorous conditions for pediatric biologics that require documented allergen sensitivity or biomarker criteria, demonstration of inadequate control on inhaled corticosteroids, recent pulmonary function testing, and evidence of improved outcomes to continue therapy, which slows time to treatment in the pediatric asthma treatment market. These requirements often introduce coordination across prescribers, specialty pharmacies, and assistance portals, which can add administrative friction for families. Several plan criteria include specific total IgE ranges for allergic phenotypes, proof of decreased rescue use, and improved FEV1 before renewal, which formalizes outcomes-based continuous-term utilization management on high-cost products. Manufacturers are addressing affordability with patient assistance programs and direct purchasing models that lower pricing on inhaled medicines and improve availability in the United States. Even so, access frictions remain a near term limiter on uptake across the pediatric asthma treatment market.

Safety Warnings and Side Effects Affecting Long-Term Use

Regulators advise careful growth monitoring in children on fluticasone propionate and other inhaled corticosteroids, with clear labeling that growth velocity can slow and requires clinician oversight in pediatrics. Budesonide suspension labeling updated in 2026 reports dose-related changes in growth over short courses and notes infection risks in infants, which informs dose planning and follow-up in the pediatric asthma treatment market. Guidance encourages the lowest effective ICS dose with step down when control is stable, which balances efficacy and safety in routine pediatric care. Targeted biologics for Type 2 inflammatory asthma have demonstrated meaningful exacerbation reductions in pediatric trials and offer corticosteroid-sparing potential, a profile that can reduce cumulative ICS exposure when children qualify. The net result is a careful approach to escalation and a preference for combination or targeted options that limit high-dose ICS exposure in the pediatric asthma treatment market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Quick-Relief Medications Gain Share Despite Controller Dominance

Long-term control medications held 58.47% in 2025, reflecting guideline-anchored daily ICS use and wider MART adoption, while the quick relief medication segment is projected to grow at 6.45% CAGR from 2026 to 2031. Broader alignment around no SABA-only management and the use of low-dose ICS at baseline continues to support controllers as the bedrock of the pediatric asthma treatment market. The pediatric asthma treatment market benefits from clearer diagnostic pathways under age 5, which moves therapy earlier and lengthens time on controllers. National guidance in China also emphasizes ICS as the cornerstone for reducing acute risk, supporting the controller base in fast-growing APAC settings. Exacerbation volatility tied to pollution and viruses sustains rescue volumes even among treated children, which keeps quick relief options growing inside the pediatric asthma treatment market.

Quick relief growth also reflects structural demand from wildfire smoke events and urban air quality episodes, which intensify breakthrough symptoms and prompt swift treatment escalation. As MART use spreads, the boundary between controller and reliever blurs, since ICS formoterol serves both maintenance and as-needed roles under current guidance. Action plans and technique training that improve adherence can moderate rescue use, but gaps remain in many primary care pathways, which maintains demand diversity in the pediatric asthma treatment market. Long-term control medications that anchor role are likely to persist even as quick relief options post higher growth on environmental and seasonal dynamics.

By Drug Class: Biologics Surge While ICS Holds Largest Share Amid Pricing Pressure

Inhaled corticosteroids led with 34.73% in 2025 due to their efficacy to cost profile and central position across all treatment steps, while biologics are the fastest growing class with a 7.41% CAGR outlook to 2031. Guidance endorses low-dose ICS early and supports combination use for moderate disease, which stabilizes ICS volume in the pediatric asthma treatment market. Safety monitoring and step-down principles help contain high-dose ICS usage, creating opportunities for combinations and targeted options to share control in selected phenotypes. Biologic momentum reflects pediatric label expansions and the arrival of twice-yearly dosing, which aim to improve persistence and patient convenience in the pediatric asthma treatment market.

Biomarker-guided selection for Type 2 inflammatory asthma and improved access tools from manufacturers are supporting a steady rise in specialty use, while payers maintain rigorous criteria for coverage. The pediatric asthma treatment industry continues to balance high volume generics with low volume specialty products, a mix that defines margin trajectories for leading portfolios.

By Route of Administration: Injectables Outpace Inhaled Formulations Amid Home-Use Autoinjectors

Inhaled formulations held 62.46% in 2025 as the core delivery route for ICS, LABA, and relievers, while injectables are projected to grow the fastest at an 8.38% CAGR to 2031. pMDIs with spacers remain central for children who need coordination support, while DPIs and soft mist devices extend choice for older children in the pediatric asthma treatment market. Regulatory focus on device instructions and correct handling underscores the importance of technique to real-world outcomes in the pediatric asthma treatment market. The pediatric asthma treatment industry is also seeing steady gains in injectables as autoinjector labels and patient-friendly devices enable home dosing for eligible adolescents and reduce reliance on infusion centers.

Real-world evidence from Europe indicates comparable outcomes across mepolizumab formats, with autoinjectors rated easiest to use by patients, which supports the home shift in the pediatric asthma treatment market. Ultra-long-acting dosing further compresses visit burden and may sustain persistence relative to more frequent injections. Oral options remain a small share for controller therapy but retain a role for acute bursts, while safety warnings limit long-duration use in children. As device education improves and home administration expands, growth in injectables is likely to remain above inhaled routes within the pediatric asthma treatment market.

By End User: Home Care Surges as Autoinjectors and Telehealth Enable Decentralization

Hospitals accounted for 46.89% in 2025, given their role in acute exacerbation management and initial biologic dosing, while home care is projected to grow the fastest at a 10.69% CAGR from 2026 to 2031. Payer requirements often necessitate documented hospital or emergency encounters as evidence of poor control before specialty approval, which anchors first dosing in supervised settings for many patients in the pediatric asthma treatment market. Clinics maintain a strong role in spirometry, adherence counseling, and action plan reviews, which support stable controller use in the pediatric asthma treatment market. Autoinjector labels and patient support materials enable caregiver administration at home for selected products after initial training, which shifts a portion of care out of facilities.

Digitally enabled inhalers and school-based trials are building workflows for adherence and technique verification outside clinics, which enhances remote review and dose adjustment in the pediatric asthma treatment market. Written action plans remain essential, while guideline support for earlier diagnosis and structured step-up or step-down policies helps standardize home decisions. As home dosing and telehealth normalize, value continues to migrate toward continuous monitoring and away from episodic facility based care in the pediatric asthma treatment market.

Geography Analysis

North America commanded 36.41% in 2025, reflecting high per capita spending and early adoption of biologics, while the Asia-Pacific is the fastest-growing region at an 11.52% CAGR from 2026 to 2031. Guidance against SABA-only regimens and the emphasis on early ICS across primary care sustain controller use in the United States and Canada, which underpins the base of the pediatric asthma treatment market. Pollution-related exacerbations have intensified rescue patterns during wildfire seasons, adding volatility to short-term volumes. Payer policies with step edits and quantity limits moderate specialty adoption curves and keep coverage concentrated among well-documented severe cases.

Asia-Pacific leads growth as urbanization and better access to specialists expand diagnosis and treatment, supported by national guidance that centers on ICS in pediatric care. Pediatric approvals for targeted therapies in China and earlier diagnosis criteria from global guidance support a steady shift toward phenotype-guided care in major urban centers. Device education and access to spacers and DPIs are improving but remain uneven across lower-resource settings, which sustains a wide therapy mix in the pediatric asthma treatment market. As middle-income coverage expands in large markets, controller adherence programs and school-based pilots are poised to extend reach.

Europe sustains a significant share supported by national guideline alignment and technology appraisals for severe cases, while decarbonization policies reshape inhaler portfolios and tender dynamics. The EMA’s support for low GWP propellants and associated device requirements is reshuffling manufacturing plans through this decade and temporarily favoring DPIs or soft mist devices in certain procurements. National health systems are also evaluating connected sensors for pediatric cohorts and assessing practical pathways to integrate adherence data into primary care workflows. Overall, Europe’s combination of guideline adoption and sustainability transitions continues to support diversified portfolios in the pediatric asthma treatment market.

Competitive Landscape

Competition concentrates on severe disease, where a handful of innovator companies lead targeted biologics, while high-volume generics keep the controller and reliever base fragmented in the pediatric asthma treatment market. Innovators focus on phenotype-specific pathways, pediatric label expansions, and dosing innovations that improve persistence and reduce clinic reliance. Portfolio strategies now include ultra-long-acting dosing with twice-yearly administration and caregiver-friendly device formats that match adolescent needs, which differentiate offerings beyond efficacy alone in the pediatric asthma treatment market.

Generic and biosimilar players compete on price in controllers and relievers, leveraging patent expirations and high-volume primary care channels that define the lower-margin core of the pediatric asthma treatment market. Device compatibility and instruction clarity remain competitive levers as education demonstrably reduces critical errors and improves correct use across devices. Access strategies now extend beyond rebates to include direct purchasing routes for inhaled portfolios that can reduce out-of-pocket costs and improve stocking in key segments, which influences share trajectories in the pediatric asthma treatment market.

Sustainability requirements add a further strategic layer as companies convert pMDIs to low GWP propellants with new materials, valves, and actuators. The EMA’s guidance on testing and human factors introduces detailed expectations that can extend development timelines yet also clarify a path to compliance for pediatric use. As conversion proceeds, device lines and tender preferences can shift in the short term, but the long run outlook supports broader environmental alignment across portfolios in the pediatric asthma treatment market.

Pediatric Asthma Treatment Industry Leaders

Amgen Inc.

AstraZeneca PLC

Dr. Reddy’s Laboratories Ltd.

Sanofi S.A.

Sun Pharmaceutical Industries Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Sanofi SA and Regeneron Pharmaceuticals reported that their biologic dupilumab (Dupixent) showed strong results in a pediatric asthma trial. The VOYAGE study demonstrated reduced exacerbations and improved lung function in children compared with placebo

- December 2025: GlaxoSmithKline received US FDA approval for Exdensur depemokimab as an add-on maintenance treatment for severe asthma characterized by an eosinophilic phenotype in patients aged 12 years and older, introducing twice-yearly dosing that targets real-world persistence. This expands an important specialty option with an adherence-oriented profile.

- December 2025: GlaxoSmithKline entered an agreement with the US government to expand access to respiratory medicines and lower pricing for select products through a direct purchasing platform, with the goal of improving affordability and supply resilience. The initiative spans a large base of patients with asthma and COPD and includes supply chain measures for albuterol.

Global Pediatric Asthma Treatment Market Report Scope

As per the scope of the report, the pediatric asthma treatment market includes all pharmacological and supportive therapies used to manage asthma in infants, children, and adolescents. It covers long‑term controller medications, quick‑relief bronchodilators, biologics, and delivery devices tailored for pediatric use. Market growth is driven by rising childhood asthma prevalence, guideline‑driven controller therapy, and expanding access to advanced treatments such as biologics. This market reflects both acute care needs and chronic disease management in pediatric populations.

The pediatric asthma treatment market is segmented by treatment type, drug class, route of administration, end user, and geography. By treatment type, the market is segmented into long-term control medications and quick-relief medications. By drug class, the market is segmented into inhaled corticosteroids (ICS), long-acting beta agonists (LABA), leukotriene receptor antagonists (LTRA), short-acting beta agonists (SABA), long-acting muscarinic antagonists (LAMA), combination inhalers (ICS/LABA), biologics (anti-IgE, anti-IL-5/5R, anti-IL-4R, anti-TSLP), and others. By route of administration, the market is segmented into inhaled, oral, and injectable. By end user, the market is segmented into hospitals, clinics, and home care. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers estimated market sizes and market trends for 17 countries across major regions worldwide. The report offers market value (in USD) for the above segments.

| Long-term Control Medications |

| Quick-relief Medications |

| Inhaled Corticosteroids |

| Long-Acting Beta Agonists |

| Leukotriene Receptor Antagonists |

| Short-Acting Beta Agonists |

| Long-Acting Muscarinic Antagonists Combination Inhalers |

| Biologics |

| Others |

| Inhaled |

| Oral |

| Injectable |

| Hospitals |

| Clinics |

| Home Care |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Long-term Control Medications | |

| Quick-relief Medications | ||

| By Drug Class | Inhaled Corticosteroids | |

| Long-Acting Beta Agonists | ||

| Leukotriene Receptor Antagonists | ||

| Short-Acting Beta Agonists | ||

| Long-Acting Muscarinic Antagonists Combination Inhalers | ||

| Biologics | ||

| Others | ||

| By Route of Administration | Inhaled | |

| Oral | ||

| Injectable | ||

| By End User | Hospitals | |

| Clinics | ||

| Home Care | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the projected size and growth rate for the pediatric asthma treatment market through 2031?

The pediatric asthma treatment market size is expected to reach USD 16.75 billion by 2031, growing at a 6.23% CAGR over 2026 to 2031.

Which treatment types are leading and which are growing fastest in pediatric asthma?

Long term control medications led with 58.47% in 2025, while quick relief options are projected to grow faster at a 6.45% CAGR through 2031.

Which drug classes are most important in pediatrics today?

Inhaled corticosteroids led with 34.73% in 2025, while biologics are the fastest growing class with a 7.41% CAGR outlook through 2031.

How are routes of administration shifting for pediatric care?

Inhaled routes held 62.46% in 2025, yet injectables are forecast to grow fastest at an 8.38% CAGR due to home use autoinjectors and less frequent dosing.

Which care setting is expanding fastest for pediatric asthma?

Home care is the fastest growing end user segment with a 10.69% CAGR forecast, supported by autoinjectors, telehealth, and connected inhalers.

Which regions will drive the next leg of growth in this space?

Asia-Pacific is the fastest growing region at an 11.52% CAGR, while North America remains the largest regional base with a 36.41% share in 2025.

Page last updated on: